Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

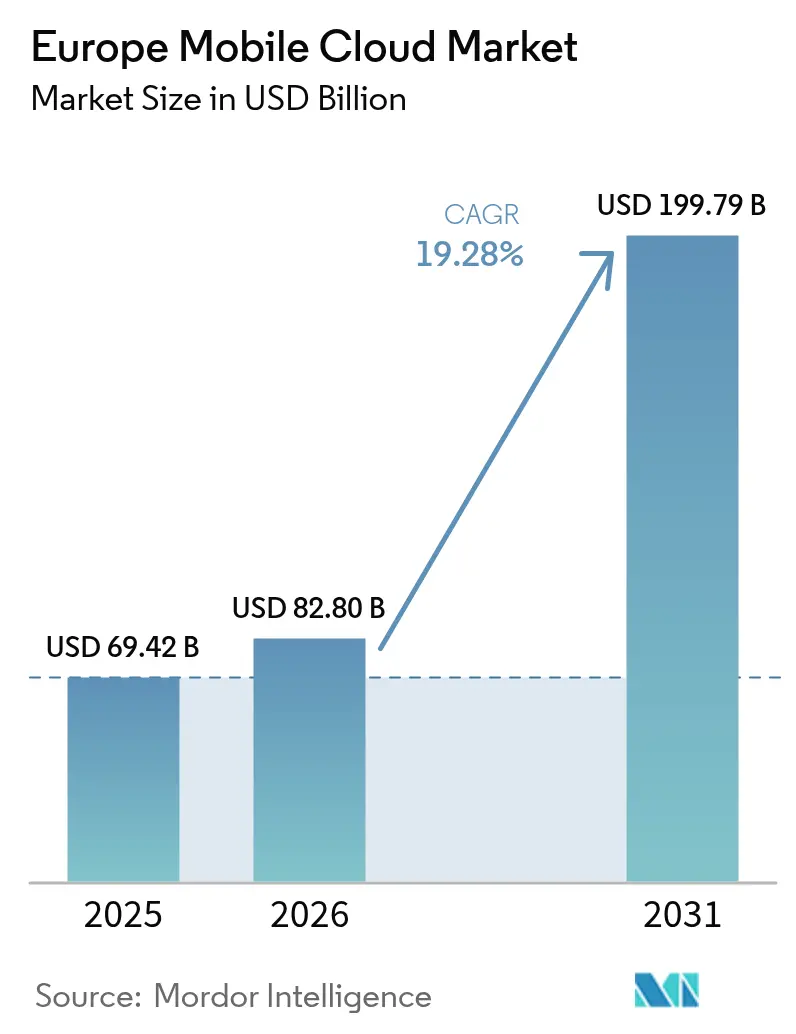

| Base Year Market Size (2025) | USD 69.42 Billion |

| Market Size (2026) | USD 82.8 Billion |

| Market Size (2031) | USD 199.79 Billion |

| Growth Rate (2026 - 2031) | 19.28% CAGR |

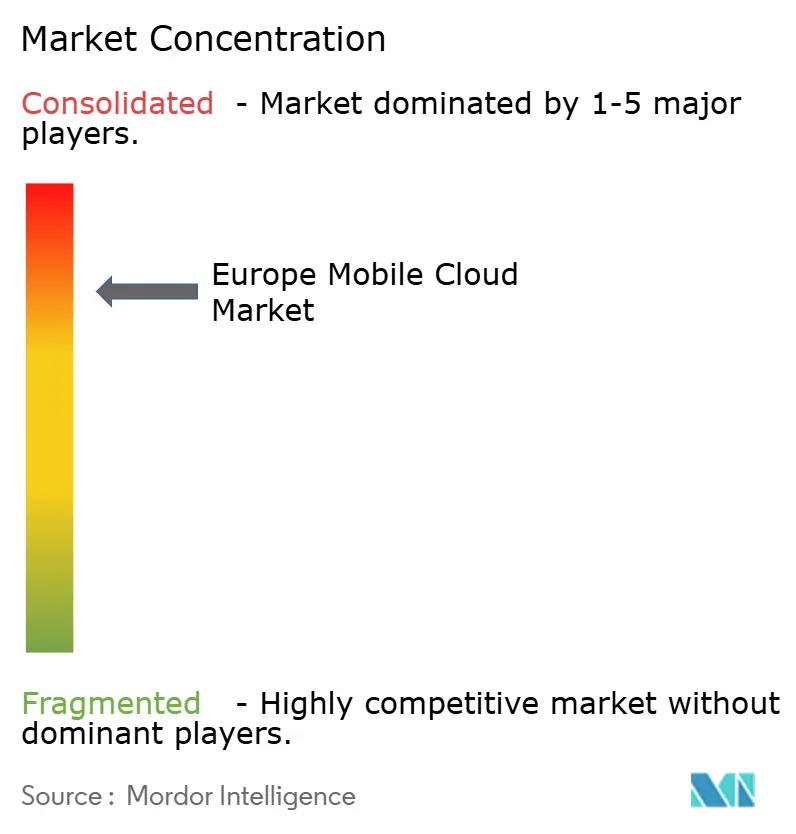

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Mobile Cloud Market Analysis by Mordor Intelligence

The Europe mobile cloud market size was valued at USD 69.42 billion in 2025 and estimated to grow from USD 82.8 billion in 2026 to reach USD 199.79 billion by 2031, at a CAGR of 19.28% during the forecast period (2026-2031). Rising adoption of sovereign-cloud frameworks, expanding 5G standalone (SA) coverage, and intensifying enterprise focus on low-latency mobile workloads underpin this trajectory. National data-sovereignty mandates are forcing workload repatriation from extra-regional hyperscale zones to EU-hosted platforms, while 5G SA networks already deliver sub-10 millisecond round-trip latency, opening fresh demand for real-time industrial, gaming and fintech use cases. Telco–cloud alliances—such as Deutsche Telekom’s NVIDIA-powered industrial AI cloud—illustrate how telecom operators are transforming into infrastructure suppliers for AI workloads. At the same time, regulatory scrutiny of hyperscaler market power is prompting price realignments, including the removal of egress fees, which lowers switching barriers and encourages multi-cloud strategies.

Key Report Takeaways

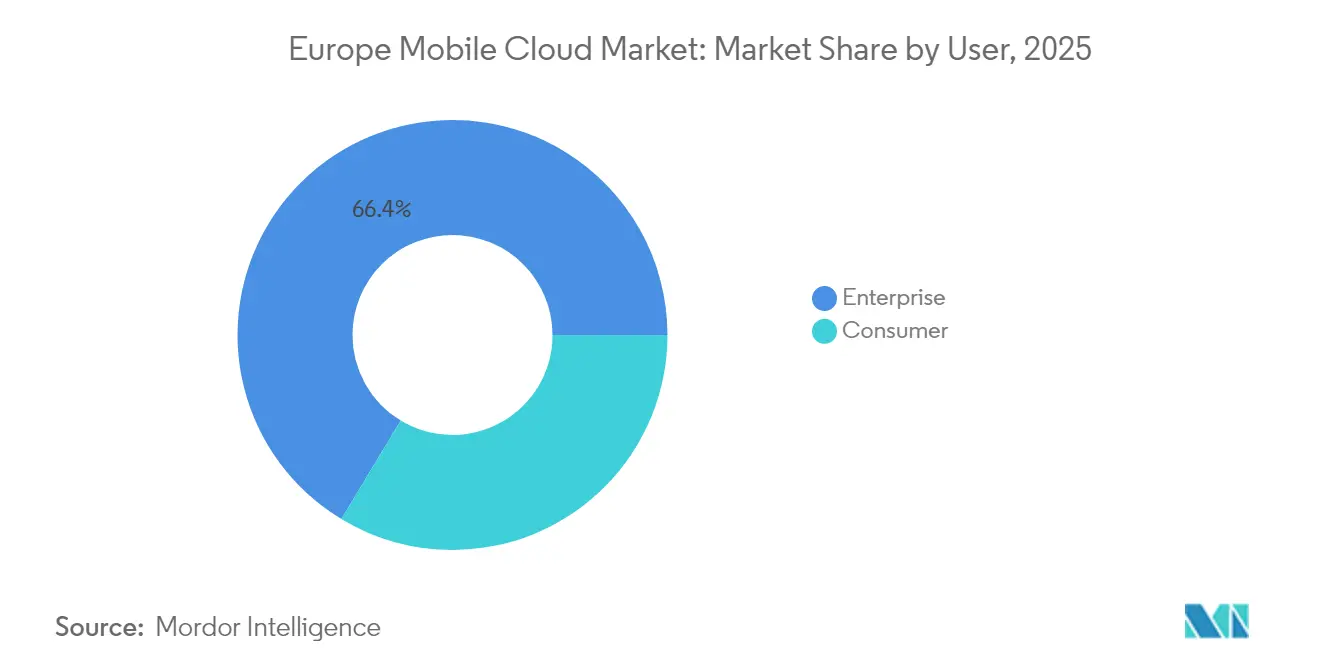

- By user type, enterprise customers commanded 66.35% of Europe mobile cloud market share in 2025, while the consumer segment is projected to expand at a 19.62% CAGR through 2031.

- By application, gaming led with 31.35% revenue share in 2025; finance and business applications are forecast to grow at a 22.15% CAGR to 2031.

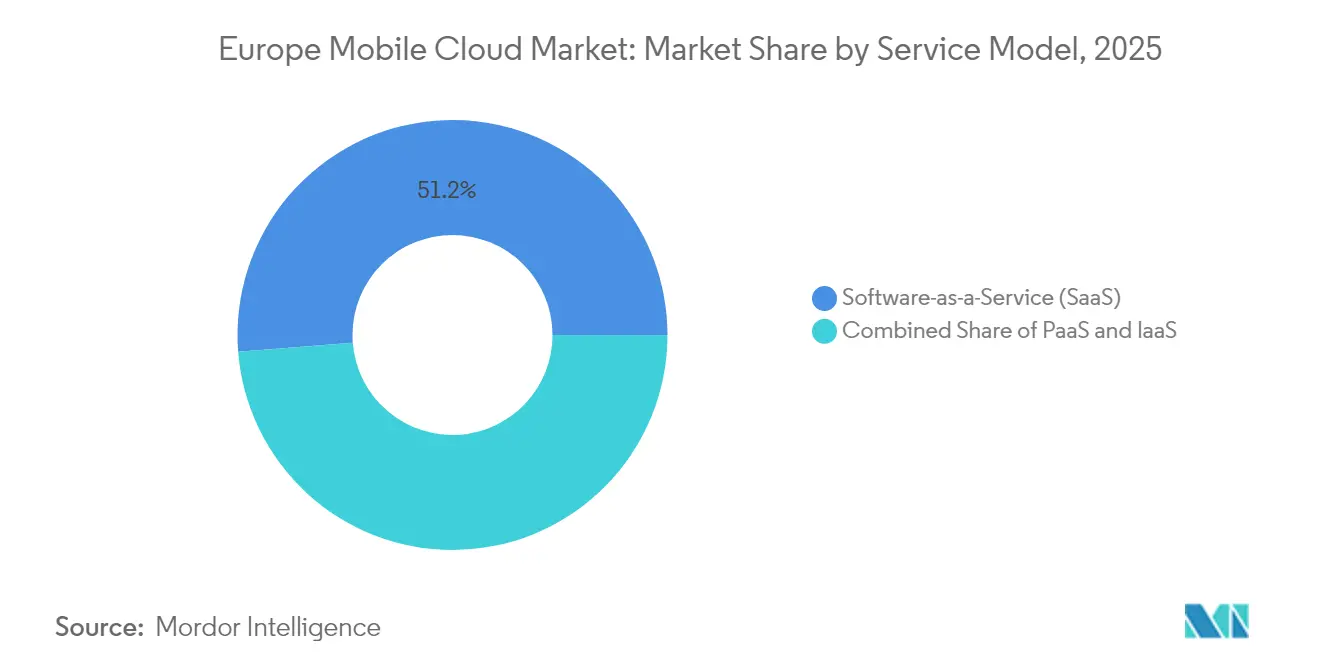

- By service model, Software-as-a-Service held 51.25% of the Europe mobile cloud market size in 2025; Platform-as-a-Service is projected to advance at 19.74% CAGR between 2026-2031.

- By deployment model, public cloud accounted for 57.10% of the Europe mobile cloud market size in 2025, whereas hybrid cloud is set to record a 19.45% CAGR to 2031.

- By geography, Germany led with 25.60% share in 2025; Spain is poised to post the fastest expansion at 19.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Mobile Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sovereign-cloud zones across EU-27 | +3.2% | Germany and France strongest | Medium term (2-4 years) |

| 5G SA roll-out lowering latency | +2.8% | Germany, UK, Italy, Spain | Short term (≤ 2 years) |

| Enterprise FinOps for multi-cloud | +2.1% | Financial hubs across EU | Medium term (2-4 years) |

| Telco edge-cloud API monetization | +1.9% | Europe-wide | Short term (≤ 2 years) |

| AI-assisted mobile app dev-ops shrinks time-to-cloud | +1.7% | Nordic countries, Germany, UK | Medium term (2-4 years) |

| Green-datacentre tax incentives in Germany and Nordics | +1.4% | Germany, Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Development of Sovereign-Cloud Zones Across EU-27

The European Commission’s EuroStack programme targets 10,000 distributed edge-cloud nodes by 2030, creating local processing points that satisfy strict data-residency statutes.[1]Tim Höttges, “Deutsche Telekom presents 8ra sovereign-cloud programme,” telekom.com Orange and Capgemini’s Bleu platform was launched in 2024 to offer Microsoft technology under SecNumCloud rules, proving that compliance-first offerings can attract sensitive workloads. The forthcoming EU Cloud Services Scheme will certify providers against sovereignty and security standards, accelerating repatriation of critical-sector data previously hosted outside the bloc. Simultaneously, the EU Data Act obliges vendors to abolish switching fees by January 2027, undermining lock-in economics and incentivizing a competitive ecosystem. As public agencies adapt procurement rules, European operators expect a sizeable uplift in cloud demand tied to regulated industries.

Intensifying 5G SA Roll-out Lowers Mobile-Cloud Latency

More than 60 operators worldwide have launched commercial 5G SA networks, including installations across Germany, the UK, Italy, and Spain.[2]“5G standalone coverage update,” ericsson.com Network slicing allows predefined latency and bandwidth classes that match mobile-cloud application requirements, directly monetised through premium service tiers. Deutsche Telekom’s 5G+ Gaming pilot has already proven sub-10 millisecond end-to-end latency for cloud gaming traffic. The GSMA projects EUR 164 billion in European economic value from 5G by 2030, most of which depends on SA deployment. Core-network upgrades, such as O2 Telefónica’s cloud-native dual-mode core, further cut maintenance downtime and enable continuous feature releases.

Surge in Enterprise FinOps Tooling for Multi-Cloud Cost Control

Large organisations increasingly embed FinOps practices to manage dispersed cloud spend. A Central and North West London NHS Trust pilot lowered total IT costs by 15-18% after adopting a managed multi-cloud model, validating tangible savings from disciplined unit-economics tracking. Vodafone keeps “commercial tension” among AWS, Azure and Google Cloud to secure optimal pricing, signalling that hyperscaler diversification is a deliberate cost-containment lever. Once the Data Act’s mandatory cost-reporting templates become law, CFO teams will gain clearer visibility into true workload costs and will scale FinOps automation accordingly. Banks such as BBVA, which recorded a 94% reduction in data-analysis access time after migrating analytics workloads to AWS, show that performance benefits can accompany disciplined cost governance.

Telco Edge-Cloud Partnerships Monetising Network APIs

The Aduna joint venture, formed by Ericsson and 12 global carriers, seeks to commercialise network APIs—quality-on-demand, precise location, identity verification—estimated to unlock USD 10-30 billion in new revenue by 2030. Standardised interfaces under the GSMA Open Gateway framework let developers consume advanced network functions without extensive integration, shortening innovation cycles. Nokia’s collaboration with Google Cloud widens API reach to the developer community, embedding telecom capabilities inside mainstream hyperscaler platforms. Deutsche Telekom’s Global Telco AI Alliance is designing multilingual LLMs tailored for telco workflows, a step that positions operators as value-added platform providers rather than commodity bandwidth sellers. As enterprises push latency-critical analytics from the core to the edge, revenue upside for carriers grows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscaler market-power scrutiny | -2.3% | UK and EU-27 | Short term (≤ 2 years) |

| Cross-border data-transfer compliance | -1.8% | EU-27 and EEA | Medium term (2-4 years) |

| Energy-price volatility squeezing datacentre OPEX | -1.5% | Germany, UK, Nordic countries | Short term (≤ 2 years) |

| Shortage of certified cloud-security professionals | -1.2% | Europe-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Scrutiny of Hyperscaler Market Power (CMA and EU DMA)

The UK Competition and Markets Authority found AWS and Microsoft each control 30-40 % of domestic cloud spend, proposing Strategic Market Status obligations that could force interoperability and pricing remedies.[3]Competition and Markets Authority, “Cloud services market study interim findings,” gov.uk The watchdog estimates competitive reforms might save UK businesses GBP 430 million annually. Parallel Digital Markets Act enforcement in Brussels adds further compliance layers for “gatekeeper” platforms, including limits on tying software licences to cloud consumption. Both AWS and Microsoft have pre-emptively eliminated egress fees for customers switching providers, demonstrating behavioural adjustments ahead of final rulings. While such concessions help clients, they compress provider margins and may reduce near-term investment pace.

Cross-Border Data-Transfer Compliance Costs (Schrems II and GDPR)

GDPR rulings require “appropriate safeguards” for transfers to jurisdictions lacking equivalent privacy protections, compelling providers to deploy additional encryption, audit, and contractual measures. The forthcoming Data Act intensifies requirements by mandating interoperability APIs for data porting and standardised cost disclosures, creating extra engineering overhead for vendors. Healthcare projects illustrate the stakes: NHS Scotland’s GBP 206 million cloud-integration tender requires providers to satisfy UK privacy law while maintaining cross-border interoperability, raising procurement complexity. National variations persist—Germany’s federal states interpret localisation rules differently, forcing multi-region architecture duplication and inflating compliance spend. These frictions trim the addressable growth rate for cross-border workloads until legal harmonisation progresses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By User: Enterprise Dominance Drives Infrastructure Investment

Enterprise workloads produced 66.35% of 2025 Europe mobile cloud market revenue as corporates prioritised performance guarantees and sovereignty compliance. Financial institutions such as BBVA highlighted time-to-insight gains—94% faster analytics—after pivoting to cloud-native data platforms. These measurable outcomes justify premium contract values and spur continued infrastructure investment. Consumer adoption, while smaller, is expanding briskly at a 19.62% CAGR due to cloud gaming subscriptions and mobile entertainment bundles. Telefónica Germany moved 1 million 5G users onto AWS core cloud, blending enterprise and consumer value chains, proving that differentiated network services can monetise both segments. Although enterprises remain the bedrock of the Europe mobile cloud market, consumer growth diversifies revenue and cushions against corporate budget cycles. The consumer-driven upswing is increasingly tied to edge-compute nodes situated near population centres, reducing jitter for graphics-intensive titles and video streaming. Network operators benefit from incremental wholesale traffic, while hyperscalers distribute content caches across metropolitan points of presence. Meanwhile, enterprise buyers widen multi-cloud footprints to mitigate lock-in, with Vodafone registering cost savings by maintaining “commercial tension” across three large providers. Advanced FinOps dashboards track usage by business unit, ensuring every workload runs in the optimal cost-performance zone. This dual-track evolution keeps the Europe mobile cloud industry resilient

By Application: Gaming Leads Innovation in Cloud-Native Experiences

Gaming secured a 31.35% slice of 2025 revenue and is projected to expand at 21.68% CAGR, propelled by pay-as-you-go cloud gaming services that remove local hardware constraints. Deutsche Telekom’s 5G+ Gaming offer demonstrates how network slicing guarantees frame-rate consistency at mobile broadband speeds. Finance and business applications rank second in value, powered by real-time risk analytics delivered over secure, low-latency pipes. Enterprises in capital-markets hubs depend on deterministic latency for algorithmic trading, steering demand toward edge-optimised zones.

Education and healthcare applications continue gaining share as remote-learning platforms and diagnostic AI workloads migrate to cloud. Regulators permit sensitive health data to reside in sovereign cloud zones, enabling providers to roll out AI-powered imaging without contravening privacy law. Entertainment platforms capitalise on the same edge footprints that gaming uses, streaming adaptive-bitrate video without buffering. Collectively, these diverse use cases reinforce growth across the Europe mobile cloud market, ensuring that incremental capacity finds ready buyers.

By Service Model: SaaS Maturity Versus PaaS Innovation

Software-as-a-Service solutions retained 51.25% share of Europe mobile cloud market size in 2025 as enterprises embraced managed, subscription-based software to cut support overheads.Microsoft’s cloud revenue advanced 23% to USD 137.4 billion, underscoring sustained appetite for full-stack suites that bundle productivity, collaboration, and security. Nonetheless, Platform-as-a-Service is scaling faster, with a 19.74% forecast CAGR, reflecting developer enthusiasm for serverless and AI/ML-ready environments. Integrated DevSecOps pipelines shorten release cycles, and per-second billing aligns costs with demand surges.Infrastructure-as-a-Service underpins both models and remains essential for legacy lift-and-shift migrations. AWS recorded 19% revenue growth in Q3 2024 on the strength of enterprise consumption alongside surging AI inference workloads. Telcos are blending the models: Deutsche Telekom’s industrial AI cloud combines GPU-rich IaaS, curated ML frameworks, and managed service layers, erasing rigid boundaries between categories. As customers demand higher abstraction without forfeiting control, service-model convergence is set to reshape provider roadmaps throughout the Europe mobile cloud market.

By Deployment Model: Public Cloud Scale Meets Hybrid Sovereignty

Public cloud remained the deployment of choice with 57.10% of 2025 spend owing to economies of scale and continuous feature delivery. Yet, hybrid architectures are accelerating at 19.45% CAGR because they satisfy sovereignty and latency constraints without sacrificing elasticity. Germany’s Energy Efficiency Act incentivizes colocation of renewable-powered private-cloud nodes, allowing regulated entities to keep sensitive datasets on-premises while bursting to public regions for analytics. The Europe mobile cloud market size for hybrid models is therefore expanding swiftly from a relatively smaller base. T-Systems illustrates the trend: after two decades of cloud evolution, the company now brokers multi-cloud, edge, and private zones under a unified governance plane. The EU-backed 8ra project aims for 10,000 interconnected edge nodes by 2030, effectively creating a continent-wide hybrid fabric that balances sovereignty with hyperscale economics. As the European Data Act phases out switching fees, CIOs gain negotiating power and can blend providers to fit each workload’s compliance profile. Private cloud retains relevance for ultra-low-latency industrial automation and highly classified government functions, ensuring all three deployment flavours coexist.

Geography Analysis

Germany delivers the single-largest slice of Europe mobile cloud market revenue, reflecting substantial industrial digitisation budgets and strong regulatory support for energy-efficient data centers. Federal plans to host at least one European AI Gigafactory underscore continued infrastructure expansion. Power-grid constraints, however, necessitate new allocation processes, compelling operators to coordinate closely with grid authorities. Spain’s solar advantage is changing data center siting economics; integrated photovoltaic arrays reduce operating costs and carbon footprints, aiding compliance with EU climate targets. National 5G corridors funded through the Connecting Europe Facility further boost Spain’s readiness for low-latency mobile-cloud services. The United Kingdom remains an innovation hub, evidenced by NHS Scotland’s GBP 206 million cloud-integration tender and the wholesale migration of NHS Spine applications to cloud platforms. Yet a 48% cybersecurity skills gap highlights workforce shortages that could slow some deployments. France leverages public-private consortia—such as Bleu—to compete for sovereignty-sensitive workloads, while Italy’s operators deploy nationwide 5G SA coverage that paves the way for edge-native applications. Finland and its Nordic peers benefit from natural free-cooling and abundant hydro power, lowering PUE and attracting hyperscale investments.Eastern and South-East European members, grouped under Rest of Europe, are accelerating cloud adoption via EU Digital Europe Programme grants, which fund cloud skills and SME transformation initiatives. Cross-border fibre upgrades along the Baltic and Balkan corridors enhance latency profiles, allowing regional startups to target pan-European user bases. Collectively, geographic diversification ensures the Europe mobile cloud market continues expanding even when individual economies face cyclical headwinds.

Competitive Landscape

Europe mobile cloud market structure is highly concentrated: AWS and Microsoft together control an estimated 60-80 % of regional spend, triggering CMA and EU scrutiny. Preliminary findings show both hyperscalers earn returns above their cost of capital, evidencing durable pricing power. Regulatory pressure has prompted self-remediation; both firms dropped egress fees for departing customers and pledged expanded interoperability APIs. Google Cloud, while smaller, leverages AI innovation to gain share, partnering with Deutsche Telekom to streamline internal IT and edge-cloud offerings.

European telcos are emerging as formidable challengers. Deutsche Telekom’s sovereign-cloud framework with Google, Orange’s Bleu joint venture with Capgemini, and public-sector contracts such as NHS Scotland’s integration tender illustrate a compliance-first differentiator. Equipment suppliers like Ericsson extend reach through the Aduna joint venture, exposing network capabilities as programmable APIs, potentially diverting value from generic IaaS to connectivity-aware PaaS products. Specialist providers focusing on vertical clouds—finance, healthcare, manufacturing—find opportunity in regulatory niche markets underserved by generic hyperscaler templates.

Technology roadmaps converge on AI acceleration. Microsoft embeds Co-Pilot functionality across workspace apps, driving upsell within its install base. AWS expands Trainium and Inferentia chip fleets to meet inference demand from European customers building generative models. Deutsche Telekom’s NVIDIA-powered industrial AI cloud focuses on deterministic performance and compliance for factory workloads, reflecting market appetite for purpose-built infrastructure. Strategic alliances, interoperability commitments and sovereign-cloud certifications will define competitive advantage over the forecast horizon.

Europe Mobile Cloud Industry Leaders

IBM Corporation

Amazon Web Services Inc.

Google LLC

Oracle Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Deutsche Telekom and NVIDIA agreed to build Europe’s first industrial AI cloud with 10,000 GPUs, operational by 2026.

- April 2025: Deutsche Telekom extended its Google Cloud partnership to 2030, covering the One Data Ecosystem and SAP2SKY migration.

- February 2025: NHS Scotland issued a GBP 206 million cloud-integration tender to modernise health IT infrastructure.

- January 2025: Orange and Capgemini commenced commercial rollout of Bleu “cloud de confiance” services for French organisations.

Europe Mobile Cloud Market Report Scope

The mobile cloud refers to cloud-based data, applications, and services designed specifically to be used on mobile and other portable devices. It allows for the delivery of applications and services to mobile users via a remote cloud server or environment.Cloud computing is used in mobile cloud to deliver applications to mobile devices.

The report divides the market into different types of users, such as businesses and consumers, who use different kinds of mobile cloud applications. The report only looks at the European market.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By User

| Enterprise |

| Consumer |

By Application

| Gaming |

| Finance and Business |

| Entertainment |

| Education |

| Healthcare |

| Travel |

By Service Model

| Software-as-a-Service (SaaS) |

| Platform-as-a-Service (PaaS) |

| Infrastructure-as-a-Service (IaaS) |

By Deployment Model

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

By Country

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Rest of Europe |

| By User | Enterprise |

| Consumer | |

| By Application | Gaming |

| Finance and Business | |

| Entertainment | |

| Education | |

| Healthcare | |

| Travel | |

| By Service Model | Software-as-a-Service (SaaS) |

| Platform-as-a-Service (PaaS) | |

| Infrastructure-as-a-Service (IaaS) | |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe mobile cloud market?

The Europe mobile cloud market value stands at USD 82.8 billion in 2026 and is projected to reach USD 199.79 billion by 2031.

Which segment generates the largest share of revenue?

Enterprise users lead with 66.35% of Europe mobile cloud market share, reflecting companies’ demand for compliant, low-latency cloud services.

Why is gaming important for future growth?

Gaming already holds 31.35% of revenue and is expanding at 21.68% CAGR because 5G SA networks enable sub-10 millisecond latency, delivering console-grade experiences over mobile connections.

How are regulatory actions affecting the market?

Investigations by the UK CMA and EU regulators are pressuring hyperscalers to boost interoperability and drop egress fees, reducing vendor lock-in and fostering multi-cloud adoption.

Which deployment model is growing the fastest?

Hybrid cloud is forecast to rise at 19.45% CAGR as organisations balance data-sovereignty requirements with the scalability of public cloud platforms.

What role do telcos play in the competitive landscape?

Telecom operators are evolving into cloud-platform providers, exemplified by Deutsche Telekom’s NVIDIA-enabled industrial AI cloud and the Ericsson-led Aduna network-API venture, adding new competitive dynamics to the market.

Page last updated on: