Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

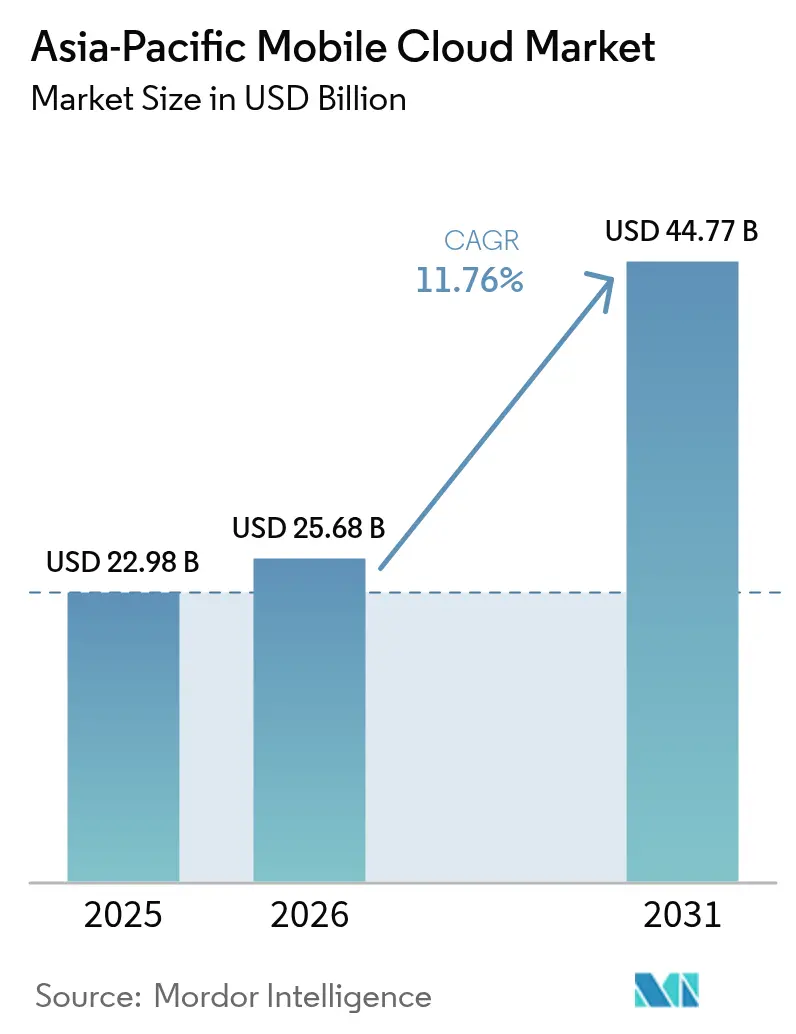

| Base Year Market Size (2025) | USD 22.98 Billion |

| Market Size (2026) | USD 25.68 Billion |

| Market Size (2031) | USD 44.77 Billion |

| Growth Rate (2026 - 2031) | 11.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Mobile Cloud Market Analysis by Mordor Intelligence

Asia-Pacific mobile cloud market size in 2026 is estimated at USD 25.68 billion, growing from 2025 value of USD 22.98 billion with 2031 projections showing USD 44.77 billion, growing at 11.76% CAGR over 2026-2031. This growth is underpinned by a decisive pivot from desktop-centric computing toward mobile-first architectures that place backend services, storage, and edge content delivery directly onto smartphones. Rapid 5G commercialization has cut average round-trip latency below 20 milliseconds in major urban clusters, unlocking near real-time gaming, augmented-reality retail, and low-latency fintech use cases. Parallel government programs such as Digital India, which earmarked USD 1.2 billion for national cloud infrastructure in 2024, are catalyzing enterprise migration to mobile-platform-as-a-service environments. Enterprises are embracing hybrid and edge deployment models to comply with data-localization laws while maintaining the agility of global hyperscale platforms. Together, these factors position the Asia-Pacific mobile cloud market as one of the world’s fastest-expanding digital service arenas.

Key Report Takeaways

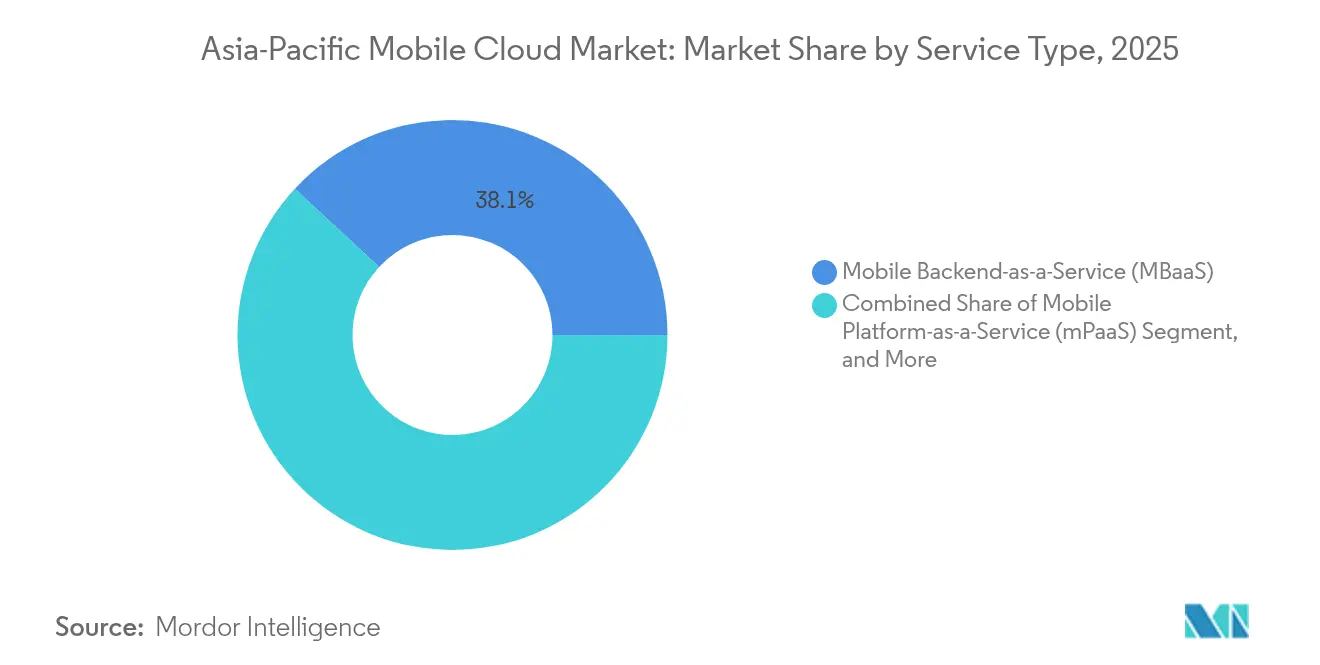

- By service type, Mobile Backend-as-a-Service led with 38.10% revenue share in 2025, while Mobile Content Delivery and Edge CDN are forecast to grow at an 11.79% CAGR through 2031.

- By deployment model, the public-cloud segment held a 63.20% share in 2025; hybrid and multi-cloud architectures are projected to expand at a 11.72% CAGR through 2031.

- By user type, enterprises commanded 71.10% spending share in 2025 and are set to advance at a 11.88% CAGR through 2031.

- By industry vertical, gaming captured 24.55% of 2025 revenue, while healthcare is on track for the fastest growth at an 11.21% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Mobile Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rollout of 5G networks across key Asia-Pacific economies | +2.8% | China, South Korea, Japan, India, Singapore | Medium term (2-4 years) |

| Rising mobile-only consumer base demanding on-device cloud storage | +2.1% | India, Indonesia, Philippines, Vietnam | Long term (≥ 4 years) |

| Government-funded digital-nation programs | +1.9% | India, Indonesia, Singapore, Malaysia | Medium term (2-4 years) |

| Enterprise shift toward edge-enabled mPaaS for ultra-low latency apps | +1.6% | Global, with concentration in China, Japan, Australia | Short term (≤ 2 years) |

| Proliferation of super-apps generating massive real-time data workloads | +1.4% | China, Southeast Asia (Singapore, Indonesia, Thailand) | Medium term (2-4 years) |

| OEM-driven device-bundled cloud subscriptions boosting ARPU | +1.2% | China, India, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rollout of 5G Networks Across Key Asia-Pacific Economies

China deployed 3.68 million 5G base stations by late 2024, delivering sub-15 millisecond latency for mobile cloud workloads. South Korean carriers invested USD 8.4 billion in 2024 to densify millimeter-wave coverage, enabling real-time inventory sync for e-commerce apps. India’s operators activated 450,000 5G sites by mid-2025, enabling fintech platforms to achieve sub-50-millisecond API calls on cloud backends. Japan’s NTT Docomo linked standalone 5G with edge nodes, cutting gaming latency by 40% versus 4G. Singapore’s regulator mandated nationwide 5G by 2025, spurring enterprises to rebuild mobile apps for edge-native deployment.

Rising Mobile-Only Consumer Base Demanding On-Device Cloud Storage

India counted 780 million mobile-only internet users in 2024, representing 68% of online citizens and making handset-based cloud backup a necessity.[1]GSMA Intelligence, “Mobile Economy APAC 2024,” gsma.com Indonesia’s USD 77 billion digital economy is 92% smartphone-transacted, so retailers rely on cloud backends for one-tap checkout. The Philippines logged 89 million mobile internet subscribers who consumed 18 GB of data monthly, driving demand for cloud-based video caching. Vietnam’s rising super-app culture funnels ride-hailing, payments, and e-commerce through cloud-scale APIs that must elastically scale on mobile platforms. Consumers in these markets are showing higher willingness to pay for premium storage tiers than desktop users, strengthening recurring revenue for mobile cloud vendors.

Government-Funded Digital-Nation Programs

India’s Digital India program subsidizes mobile cloud access for small firms, cutting infrastructure costs by up to 45%. Indonesia’s 1000 Start-ups Movement funnels venture capital toward mobile-first businesses that rely on scalable cloud services.[2]Ministry of Communications and Information Technology, “Regulation 71,” kominfo.go.id Singapore’s Smart Nation mandate requires all public services to be mobile-ready by 2025, producing a standards blueprint that private enterprises adopt. Malaysia’s MyDigital plan dedicates USD 4.8 billion to accelerate cloud migration with specialized funding for mobile device management tools. These programs widen the addressable base for the Asia-Pacific mobile cloud market by onboarding thousands of first-time cloud customers.

Enterprise Shift Toward Edge-Enabled mPaaS for Ultra-Low Latency Apps

Enterprises are moving from monolithic backends to micro-service mobile platform-as-a-service stacks deployed at the edge, trimming application response times by up to 50%.[3]Amazon Web Services, “AWS Mobile Services,” aws.amazon.com Tencent Cloud added 180 edge nodes in China to serve mini-program traffic under 20 milliseconds. Alibaba Cloud and China Mobile co-located 220 edge sites that render 3D product models for e-commerce in real time. Google Cloud rolled out Anthos for Mobile, giving regulated industries a hybrid control plane that spans on-premise and public nodes. As more mobile workloads demand real-time performance, edge-enabled mPaaS has become a core driver of spending in the Asia-Pacific mobile cloud market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent cross-border data-sovereignty barriers in Asia-Pacific | -1.8% | China, India, Indonesia, Vietnam | Long term (≥ 4 years) |

| Skills shortage in cloud-native mobile DevSecOps | -1.1% | India, Philippines, Indonesia, Malaysia | Medium term (2-4 years) |

| Energy-cost spikes at hyperscale data centers in Japan and Australia | -0.9% | Japan, Australia | Short term (≤ 2 years) |

| Rising spectrum-usage fees limiting telco cloud CAPEX | -1.3% | India, Australia, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Cross-Border Data-Sovereignty Barriers in Asia-Pacific

China’s Personal Information Protection Law obliges cloud providers to keep personal data inside national borders, requiring city-level data centers that raise operating costs. India’s Digital Personal Data Protection Act enforces similar localization, prompting hyperscalers to commit multi-billion-dollar builds to satisfy compliance. Indonesia’s Regulation 71 and Vietnam’s Cybersecurity Law both deter cross-border replication, fragmenting regional architectures. These rules slow multi-cloud adoption because enterprises must validate jurisdictional compliance before deploying Asia-wide platforms. Domestic providers that already operate sovereign clouds gain an edge, complicating competitive dynamics in the Asia-Pacific mobile cloud market.

Rising Spectrum-Usage Fees Limiting Telco Cloud CAPEX

India’s 2022 5G auction raised USD 19 billion, which diverted capital away from planned investments in edge nodes and mobile cloud platforms. Australia’s 2024 millimeter-wave auction forced carriers to curtail non-core spending as license fees climbed. Indonesia hiked spectrum usage fees by 25% in 2024, cutting operator budgets for 5G-integrated cloud rollouts. Japan’s dynamic pricing scheme raised costs for heavy bandwidth users, delaying rural edge deployments. As spectrum payments climb, telcos prioritize network coverage over cloud platform expansion, limiting bundled connectivity-plus-compute offers and slowing overall growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Backend Dominates, Edge CDN Accelerates

Mobile Backend-as-a-Service accounted for 38.10% of 2025 revenue, the largest slice of Asia-Pacific mobile cloud market share, by delivering turnkey authentication, database, and push-notification modules that compress development cycles. Edge-anchored Mobile Content Delivery is forecast to grow at an 11.79% CAGR through 2031, mirroring latency needs of gaming and streaming apps. The Asia-Pacific mobile cloud market size derived from edge CDN services is projected to more than double between 2026 and 2031 as developers position compute within 10 milliseconds of users. Tencent Cloud’s 180 edge nodes already shave video load times by one-third for WeChat mini-programs. Alibaba Cloud’s tie-up with China Mobile co-locates micro-data centers at 5G towers to support augmented reality commerce. In Southeast Asia, Google Cloud’s Anthos for Mobile enables banks to deploy containerized services across on-premise racks and public zones, meeting data-residency requirements. Competitive lines are blurring as edge CDN vendors embed serverless compute while MBaaS providers launch global file and media delivery services, intensifying vendor consolidation.

Enterprises cite cost optimization as a key reason for favoring MBaaS, reporting a 40-50% faster time-to-market compared to in-house stacks. Start-ups in India’s fintech sandbox iterate payment APIs in under eight weeks by relying on pre-built identity, analytics, and notification modules. Edge CDN growth is tied to rising mobile screen time. GSMA estimates Asia-Pacific users spent 5.2 hours per day on smartphones in 2024, a behavior that accelerates cache demand. The Asia-Pacific mobile cloud industry segment mix is likely to evolve as video, gaming, and immersive commerce gain share, forcing backend providers to integrate lightweight edge nodes to remain competitive.

By Deployment Model: Public Cloud Leads, Hybrid Gains Momentum

Public cloud captured 63.20% revenue in 2025 thanks to on-demand pricing, broad¬est geographic coverage, and rich developer ecosystems. Hybrid and multi-cloud configurations, however, are forecast to expand at an 11.72% CAGR as banks and hospitals balance residency mandates with global scalability. The Asia-Pacific mobile cloud market size attributable to hybrid architectures is expected to rise from USD 9.38 billion in 2026 to USD 16.33 billion in 2031. DBS Bank routes transactions through private nodes while leveraging AWS for analytics, trimming total cost by 22%. Commonwealth Bank uses dual public clouds to keep customer data local but train AI models abroad, demonstrating how organizations optimize compliance and performance.

Private cloud adoption is most prevalent in China, where state-linked enterprises and large internet firms run sovereign mobile clouds to align with cybersecurity directives. Japanese conglomerates such as Rakuten blend on-premise edge nodes with public burst capacity to process fluctuating mobile workloads. As hybrid footprints widen, demand rises for unified control-plane software; VMware, Red Hat, and IBM are tailoring tools to orchestrate security policies across clusters.

By User Type: Enterprise Wallets Drive Spending

Enterprises generated 71.10% of 2025 revenue and will expand at a 11.88% CAGR to 2031, reflecting larger contract values and multi-year commitments. A typical Asia-Pacific mobile cloud market size deal for Fortune 500 clients ranges between USD 50,000 and USD 500,000 annually, far outweighing consumer subscriptions that average USD 30 per year. Work-from-anywhere policies make mobile device management critical, Tata Consultancy Services enabled 450,000 employees to access apps on smartphones, resulting in a 35% reduction in VPN costs. Bring-your-own-device policies increase the need for cloud-managed security and synchronization, prompting enterprises to prefer platforms that bundle identity and threat detection modules.

Consumer spending centers on cloud photo backup and video archive services, especially in India and Indonesia, where mobile-only users dominate. OEM-led bundles from Xiaomi and Oppo ship with 5 GB free tiers that convert 12% of users to paid plans, illustrating an underserved direct-to-consumer angle. The Asia-Pacific mobile cloud industry will continue to see consumer growth, but enterprise demand for compliance, low latency, and integration depth ensures that the enterprise segment retains revenue leadership.

By Industry Vertical: Gaming Tops Revenue, Healthcare Scales Fastest

Gaming secured 24.55% revenue in 2025 through real-time rendering, multiplayer state sync, and heavy CDN usage that together rely on sub-20 millisecond performance. Healthcare, although smaller today, is forecast to grow at an 11.21% CAGR as telemedicine and e-prescription apps transfer patient data across secure cloud backends. The Asia-Pacific mobile cloud market size linked to healthcare is set to nearly double by 2031 as hospitals deploy mobile-first electronic health records. India’s Practo handled 12 million teleconsults in 2024 on AWS mobile backends while maintaining sub-second scheduling. Fintech ranks second in spending; Indonesia’s Bank Jago realized a 40% latency cut after migrating to Google Cloud in 2024.

Media and entertainment rely on edge CDN to buffer streaming peaks. Retail and e-commerce businesses utilize cloud APIs to synchronize inventory and facilitate checkout within super-apps. Education demand spiked as Tencent Education served 180 million learners who generated 2.5 billion daily API calls on Tencent Cloud. Travel and hospitality now prioritize contactless journeys that require real-time updates. Across verticals, security and compliance complexity is rising, with healthcare bearing the highest cost uplift because of stringent privacy laws.

Geography Analysis

China is the largest individual market, backed by 1.05 billion smartphone users and domestic hyperscalers that supply 65% of in-country capacity. Alibaba Cloud spent USD 3.8 billion in 2024 to add data-center clusters near 5G towers so WeChat mini-programs meet sub-20 millisecond targets. Tencent Cloud extended reach into tier-2 cities with 180 edge nodes by mid-2025 to support short-video and gaming traffic. India represents the fastest-growing geography, lifted by Digital India funding and 450,000 active 5G sites that bring the Asia-Pacific mobile cloud market closer to users. Japan exhibits high hybrid-cloud penetration because enterprises, such as Sony, synchronize industrial IoT and mobile devices under ISO 27001 frameworks. Australia and South Korea record among the region’s highest per-capita cloud spends as nearly universal smartphone penetration meets extensive 5G coverage. Singapore’s Smart Nation requirement that every public service be mobile-accessible by 2025 creates a halo effect where private firms adopt compatible backends.

Indonesia, Malaysia, and the Philippines constitute emerging high-growth clusters. Indonesia’s mobile-driven digital economy, valued at USD 77 billion in 2024, relies on super-apps whose real-time data flow mandates scalable mobile cloud capacity. The Rest of Asia-Pacific, covering Vietnam and Thailand, is benefiting from telco bundles where 5G data plans include 50 GB to 200 GB cloud storage, lowering acquisition costs for cloud vendors. Data-sovereignty rules still fragment architectures, but domestic providers that operate sovereign clouds gain share within China and India.

Regulatory Landscape

Mobile cloud deployments across Asia-Pacific continue to fall within a patchwork of data sovereignty and critical-infrastructure oversight regimes. This environment pushes providers toward in-country hosting, stronger resilience controls, and security certifications that procurement teams can audit. In February 2025, Singapore's Infocomm Media Development Authority (IMDA) issued voluntary Advisory Guidelines for Resilience and Security of Cloud Services, referencing ISO 27001 and MTCS to shape cloud security baselines used in procurement and enterprise risk programs.

At the regional level, policy bodies are working to reduce friction in cross-border service delivery while maintaining trust requirements. The ASEAN Framework on Cross-border Cloud Computing Principles introduces the Trusted Data Corridor concept to enable designated pathways for compliant data flows across participating member states, and APEC's 2026 roadmap for innovative and resilient services prioritizes trusted digital transactions and cross-border data flow facilitation. In July 2026, Singapore opened public consultation on a Digital Infrastructure Bill covering major data center and cloud facility services, signaling tighter oversight of cloud infrastructure as essential digital infrastructure.

Value Chain Analysis

The Asia-Pacific mobile cloud value chain begins with foundational infrastructure inputs, including data centers, power and cooling, and long-haul and metro fiber. It then extends through hyperscale and regional cloud providers supplying compute, storage, and managed cloud primitives. On top of that layer, mobile cloud service enablers such as MBaaS, mPaaS, identity and API management, observability, and mobile content delivery and edge CDN are integrated by system integrators and developer platforms into mobile apps used by enterprises and consumers across gaming, BFSI, retail, and healthcare.

Distribution and service delivery are increasingly shaped by partnerships between cloud providers and telecom operators that bundle 5G access, edge locations, and cloud platforms into packaged offers. Local infrastructure investors also expand capacity to meet residency and latency needs. Recent moves in India and South Korea show the chain tightening between backbone connectivity, localized regions, and AI-ready facilities, including Tata Communications' collaboration with AWS in July 2025 on high-capacity long-distance connectivity between AWS infrastructure locations in Mumbai, Hyderabad, and Chennai, and SK Group and AWS' multi-year partnership in June 2025 to build cloud infrastructure in South Korea, including an AWS AI Zone in Ulsan. As localization requirements intensify, multizone and in-country region architectures, often supported by telecom and colocation partners, have become a key operational step between hyperscale platforms and regulated enterprise mobile workloads.

Competitive Landscape

The Asia-Pacific mobile cloud market remains moderately fragmented; no provider exceeded 15% share in 2024. Amazon Web Services, Microsoft Azure, and Google Cloud leverage global tooling and partner ecosystems, while Alibaba Cloud, Tencent Cloud, and Huawei Cloud win with localized data centers and in-language support. AWS launched 24 Local Zones in 2024 to deliver single-digit-millisecond latency for workloads in Mumbai, Seoul, and Jakarta. Alibaba Cloud’s Mobile Edge Computing platform co-located compute at 180 China Mobile sites, cutting content delivery lag by 35%.

Telcos such as NTT Communications, SK Telecom, and Singtel bundle cloud storage with 5G, increasing average revenue per user and lowering churn. OEMs led by Xiaomi, Oppo, and Vivo pre-install proprietary cloud apps that convert up to 18% of users to paid plans, creating a parallel channel that bypasses traditional vendors. Platform differentiation now centers on integrated DevSecOps pipelines, serverless edge runtimes, and AI-assisted features such as on-device image recognition. Hyperscalers have responded through targeted acquisitions; Microsoft absorbed Xamarin and Visual Studio Mobile Center, while AWS doubled down on Amplify to tighten developer lock-in.

Emerging white-space exists in cross-provider governance layers. VMware, IBM, and Red Hat are positioning policy-driven orchestration platforms that give enterprises unified visibility across sovereign and global regions. As edge deployments scale, specialist vendors offering carrier-grade observability and compliance automation could capture new value pools in the Asia-Pacific mobile cloud market.

Asia-Pacific Mobile Cloud Industry Leaders

IBM Corporation

Amazon Web Services Inc.

Google LLC

Oracle Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is expanding mobile-first cloud backends and edge delivery capacity in markets where data residency and latency requirements are tightening alongside fast-growing mobile usage. India stands out as a whitespace area supported by large, dated capacity commitments. Amazon committed an additional USD 13 billion in June 2026 to expand AWS data center capacity in Mumbai and Hyderabad through 2030, while AirTrunk announced a USD 30 billion commitment in June 2026 to develop 5 GW of new data center capacity in India, including a 3 GW project in Raigad Pen, Maharashtra. These investments broaden the footprint for MBaaS, mPaaS, and mobile content delivery services that need proximity to end users and access to regulated datasets.

A second opportunity is building interoperable compliance and governance layers that enable enterprises to run mobile workloads across sovereign and global clouds without duplicative security work. In February 2026, ASEAN Digital Ministers endorsed a Malaysia-led Regional Framework on Cross-Border Cloud Computing, and the broader ASEAN cross-border cloud principles, including the Trusted Data Corridor concept, provide a policy foundation for providers and enterprises to design compliant cross-border architectures for super-apps, regional retailers, and banks. With Asia-Pacific data center operational capacity reported at 13.8 GW in 2025 and a development pipeline reaching 19.4 GW, vendors that combine localized infrastructure with cross-cloud policy controls, resilient service operations, and edge-native developer tooling have room to win mobile cloud workloads spanning multiple jurisdictions and performance zones.

Recent Industry Developments

- July 2026: Amazon Web Services (AWS) advanced its India buildout as Telangana state officials laid the foundation stone for a flagship AWS data center in Bharat Future City under a large investment commitment. The project strengthens in-country capacity options for latency-sensitive mobile backends and data-residency constrained workloads across enterprise and public-sector use cases.

- March 2026: Microsoft announced a more than USD 1 billion cloud and AI infrastructure investment in Thailand spanning 2026 to 2028, alongside partnerships with local entities including Gulf Development, Advanced Info Service, CP Group, and True Corporation. The initiative expands the regional cloud footprint and partner channels supporting mobile application modernization, governance, and AI-enabled mobile services.

- March 2025: Microsoft Azure announced a USD 2.1 billion investment to expand its cloud infrastructure across India, including three new data center regions in Chennai, Pune, and Kolkata optimized for mobile backends and edge computing. The expansion deepens local processing and storage capacity that helps enterprises deploy low-latency mobile applications while aligning operations with India's data protection requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Asia-Pacific mobile cloud market includes cloud services and platforms delivered through mobile devices and mobile applications. Coverage includes mobile backend, mobile platforms, cloud-enabled device management, and mobile content delivery capabilities across the region.

Scope exclusions: We exclude on-device-only software and handset hardware revenue. We also exclude telecom connectivity charges unless they are bundled as part of a mobile cloud service.

Segmentation Overview

- By Service Type

- Mobile Backend-as-a-Service (MBaaS)

- Mobile Platform-as-a-Service (mPaaS)

- Mobile Device Management-integrated Cloud

- Mobile Content Delivery / Edge CDN

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid and Multi-Cloud

- By User Type

- Enterprise

- Consumer

- By Industry Vertical

- Gaming

- Banking, Financial Services and Insurance (BFSI)

- Media and Entertainment

- Education

- Healthcare

- Travel and Hospitality

- Retail and E-commerce

- Government and Public Sector

- Other Industry Verticals

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Singapore

- Indonesia

- Malaysia

- Philippines

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model, especially around regional demand drivers and where spending is likely to be captured within mobile cloud services. We referenced public sources such as ITU indicators for mobile broadband usage, World Bank macro series for country-level spending capacity, OECD digital economy notes (where available), national telecom and digital ministry publications, and standards and guidance from bodies such as NIST.

On top of that, we reviewed company annual reports, earnings decks, product documentation, association websites, and reputed press to understand go-to-market patterns and the pace of cloud adoption by verticals. For numerical cross-checks, paid subscriptions were used selectively for company financials and intelligence, news and financials, patent databases, and shipment-level import export data where it helped validate directional movement. These examples are not exhaustive, and many other public and internal sources were also referenced for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how mobile cloud revenue is recognized across service types and which deployment choices are most common in different APAC countries. We spoke with a mix of cloud service providers, system integrators, enterprise users, and industry specialists. The respondent input then helped confirm adoption levels by verticals such as BFSI, gaming, media, retail, and public sector across major APAC economies.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | |

| Mid tier: 47% | Functional/Unit leaders: 28% | |

| Smaller Players: 22% | Managers: 56% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where regional cloud and mobility indicators are used to reconstruct addressable spend that can realistically flow into mobile-first cloud services. That addressable structure is then allocated across service types, user types, and key countries. After the structure is set, we corroborate it with selective bottom-up approximations, including sampled provider revenue disclosures, channel checks on typical contract values, and volume assumptions tied to active mobile app usage.

In the model, we treated a few practical inputs as key levers, including smartphone and mobile broadband penetration, enterprise cloud adoption intensity, mobile app traffic growth that drives content delivery demand, security and compliance spend behavior for mobile device management, and the share of workloads moving to hybrid and multi-cloud setups. Forecasts were built using scenario analysis, where growth paths for these variables were adjusted based on what interviewees expect by country and by vertical, and then market totals were recalculated for each year. Where bottom-up signals were missing for smaller countries or niche use cases, gaps were handled through proportional allocation using country IT spend capacity and validated adoption benchmarks, before totals were normalized back to the regional sum.

Data Validation & Update Cycle

Outputs are checked through triangulation across independent signals, and obvious jumps are reviewed before the final numbers are signed off. We run variance checks across country totals, service mix splits, and implied pricing. Any outliers trigger a second pass that re-tests the assumptions and, where needed, re-contacts selected experts for clarification.

The report is refreshed annually, and interim updates are done when material events can change adoption or pricing in a visible way. Before delivery, an analyst performs a fresh pass on the latest public information and key indicators, so clients receive an updated view that remains traceable to the same model logic.

Mordor Intelligence's Asia Pacific Mobile Cloud Market Market Sizing Compared With Other Published Estimates

Published market sizes for APAC mobile cloud often do not match each other because the scope can shift in small but meaningful ways, and the math behind pricing and adoption is not always aligned. Differences also come from which countries are counted in APAC, how hybrid and multi-cloud revenue is treated, and whether adjacent areas are bundled into the total.

The benchmark table shows a tighter spread against one estimate and a wide gap against another, which is usually explained by what is included in mobile cloud and how the forecast baseline is chosen. In Mordor Intelligence's model, revenue is counted only when it maps to mobile backend, mobile platforms, cloud-enabled device management, or mobile content delivery. General cloud or telecom connectivity revenue is not added unless it is explicitly part of those mobile cloud services.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 22.98 B (2025) | |

| Industry Research Group A | USD 20.90 B (2025) | Uses a different base year structure and country basket for APAC, and it appears to apply a narrower service capture that can miss parts of enterprise mobile platform and device management revenue. |

| Global Consultancy B | USD 62.10 B (2024) | Likely folds broader cloud spending triggered by mobile usage into the total, and the starting year and implied growth rate suggest that adjacent cloud categories are being counted beyond mobile backend, platform, and mobile delivery services. |

Taken together, the comparison indicates that scope boundaries and starting-year assumptions drive most of the variance, not a single demand indicator. By keeping the inputs tied to observable mobile adoption signals and by matching revenue to clearly defined service buckets, the resulting market size stays easier to reproduce and to explain during planning discussions.

Key Questions Answered in the Report

How big is the Asia Pacific mobile cloud market in 2026?

It is valued at USD 25.68 billion with an 11.76% CAGR outlook to 2031.

Which deployment model currently dominates spending?

Public-cloud deployments lead with 63.20% of 2025 revenue, though hybrid architectures are growing faster.

Which service type is expected to grow the fastest?

Mobile Content Delivery and Edge CDN is projected to expand at an 11.79% CAGR through 2031.

Why is healthcare a high-growth vertical?

Telemedicine apps and mobile electronic health records require secure, low-latency cloud backends, pushing healthcare’s forecast CAGR to 11.21%.

What role do 5G networks play in market expansion?

5G reduces latency below 20 milliseconds, enabling real-time mobile cloud applications like multiplayer gaming and fintech payments.

Page last updated on: