Chronic Care Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.11 Billion |

| Market Size (2031) | USD 13.05 Billion |

| Growth Rate (2026 - 2031) | 12.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

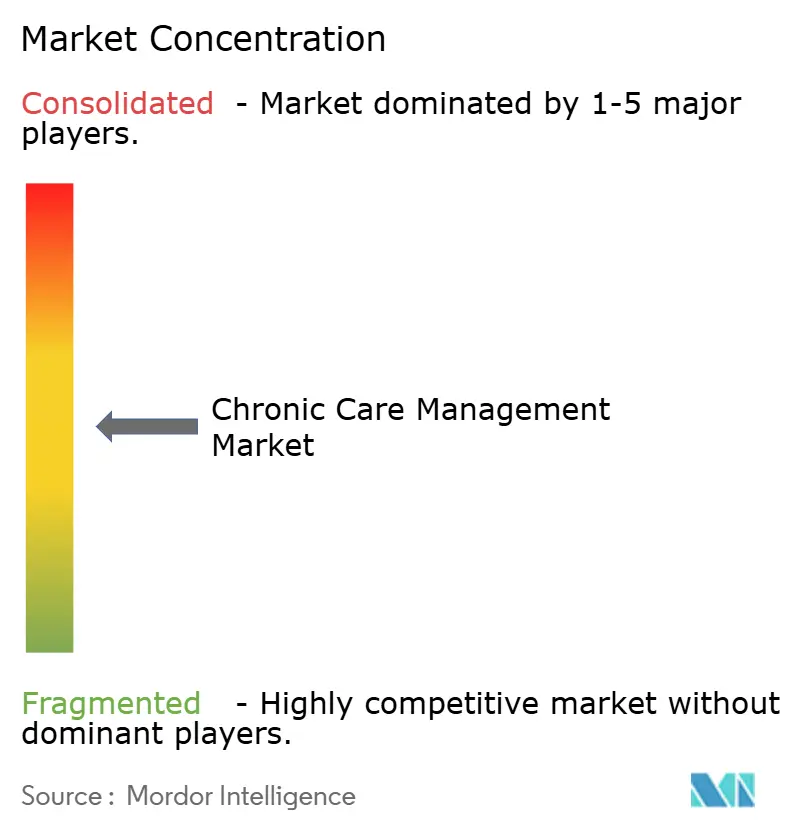

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chronic Care Management Market Analysis by Mordor Intelligence

The Chronic Care Management Market size is projected to expand from USD 6.30 billion in 2025 and USD 7.11 billion in 2026 to USD 13.05 billion by 2031, registering a CAGR of 12.90% between 2026 to 2031.

The U.S. healthcare system is witnessing a significant shift in reimbursement practices, transitioning from time-based activities to a focus on documented patient outcomes. This change is driving the need for advanced data capture, monitoring, and care coordination systems. The chronic care management market is further supported by the CY 2026 Medicare Physician Fee Schedule, which includes a 10% increase in CCM reimbursement rates, enhancing the economic case for structured program adoption in ambulatory settings.[1]Centers for Medicare & Medicaid Services, “Calendar Year (CY) 2026 Medicare Physician Fee Schedule Final Rule,” CMS Newsroom, cms.gov The market is increasingly becoming software-driven as providers, payers, and care platforms adopt automation for intake, documentation, care gap closure, and patient engagement to reduce per-patient operating costs.

Key Report Takeaways

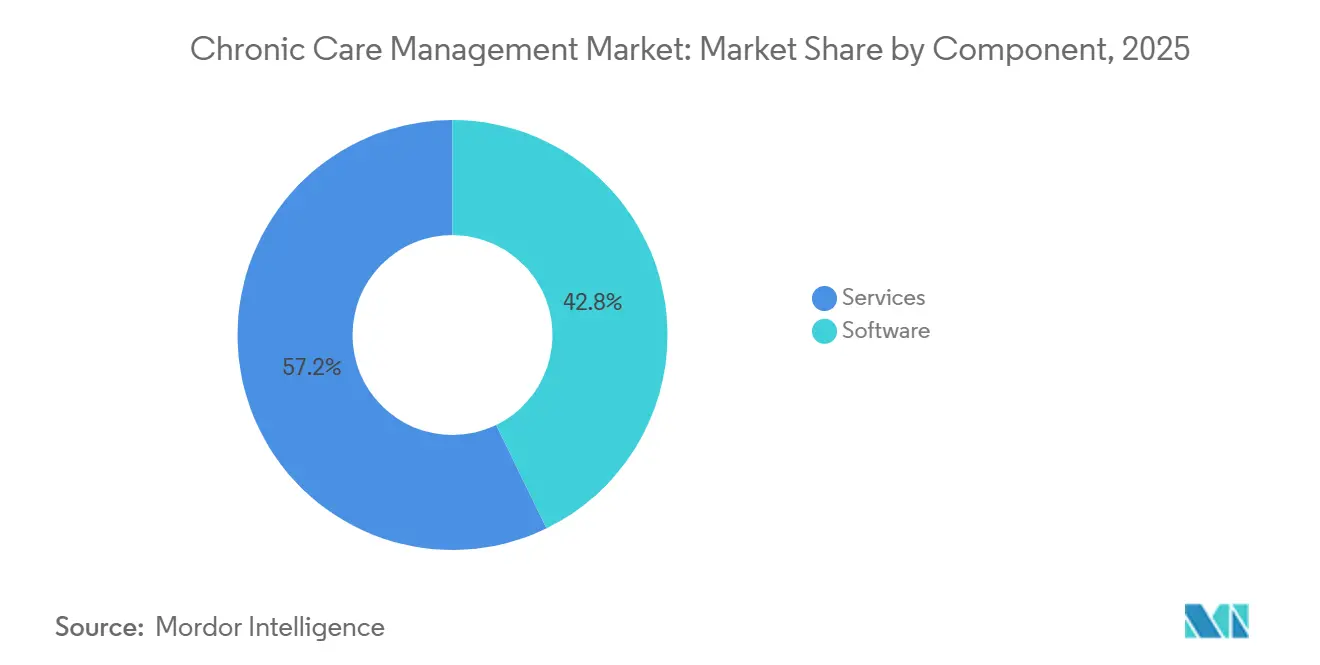

- By component, services held 57.18% of revenue in 2025, while software is projected to expand at a 15.90% CAGR through 2031.

- By deployment, cloud-based deployment accounted for 71.22% of revenue in 2025, while on-premise deployment is forecast to grow at a 14.25% CAGR through 2031.

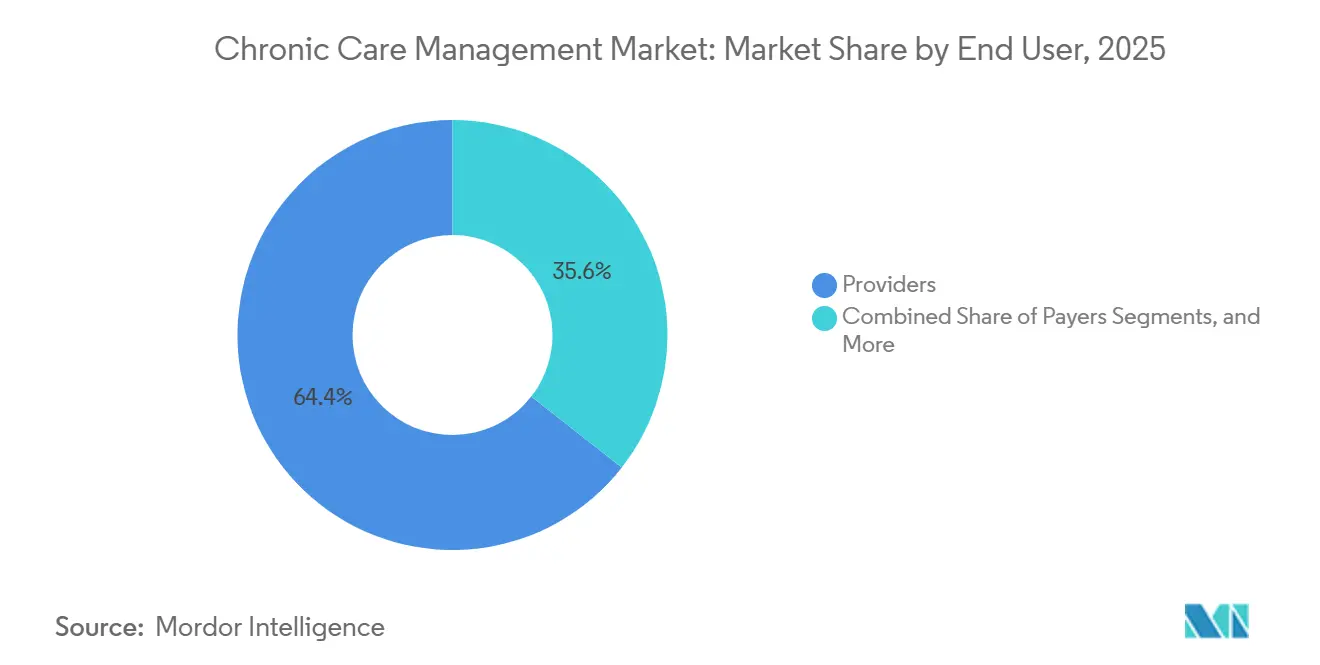

- By end user, providers captured 64.45% of revenue in 2025, while payers are projected to record the highest CAGR at 16.69% through 2031.

- By disease category, diabetes accounted for 34.66% of revenue in 2025, while chronic respiratory diseases are expected to advance at a 15.33% CAGR through 2031.

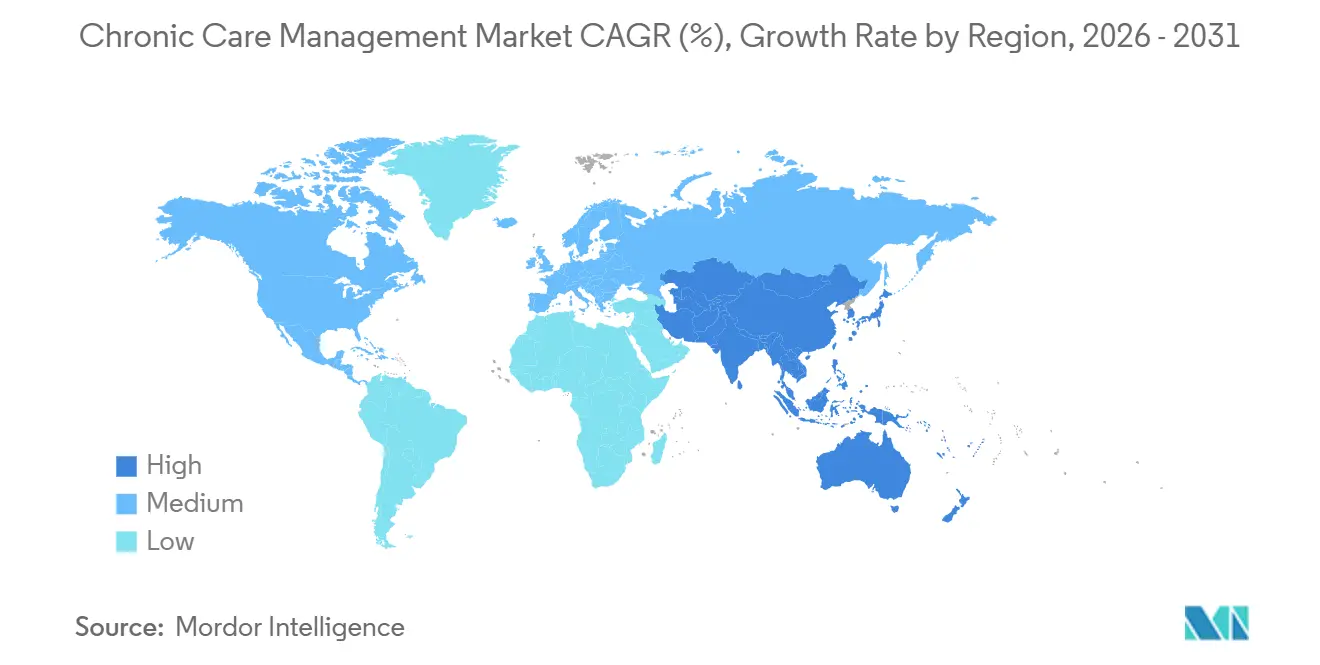

- By geography, North America held 41.55% of revenue in 2025, while Asia-Pacific is projected to expand at a 16.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chronic Care Management Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising medicare and value-based care adoption | +3.5% | North America as the primary market, with spillover into Western Europe through value-based contracting pilots | Medium term (2-4 years) |

| Expansion of remote patient monitoring partnerships | +2.0% | Global, with concentration in North America, Japan, Australia, and South Korea | Short term (≤ 2 years) |

| Under-diagnosed multimorbidity in aging populations | +2.5% | Asia-Pacific, Western Europe, and North America | Long term (≥ 4 years) |

| Provider need to reduce avoidable readmissions | +1.5% | North America and Europe, with early traction in Australia and Singapore | Medium term (2-4 years) |

| Reimbursement friction for documentation-heavy workflows | +1.5% | North America first, with relevance in U.K. and EU reimbursement reform settings | Short term (≤ 2 years) |

| Ai-enabled care gap detection and time capture | +3.0% | Global, with leading adoption in North America, the U.K., South Korea, and Taiwan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Medicare and Value-Based Care Adoption Accelerates Platform Deployment

Medicare's payment reforms are reshaping the landscape of chronic care management. Providers are now prioritizing systems that emphasize reporting, coordination, and measurable outcomes over mere monthly activity tracking. Benefiting from CMS's push for deeper accountable care participation and the 2025 APCM pathway, the chronic care management market is witnessing a shift towards structured primary care management and value-based reimbursement. The 2026 fee schedule further fueled this momentum by boosting CCM reimbursement rates, enhancing ROI for providers who can scale compliant programs.[2]Centers for Medicare & Medicaid Services, “Calendar Year (CY) 2026 Medicare Physician Fee Schedule Final Rule,” CMS Newsroom, cms.gov This shift is pivotal; manual workflows falter when timely data capture, validated care plans, and consistent follow-ups are tied to reimbursement. Consequently, there's a surging demand for software that seamlessly integrates clinical actions, documentation, and payment readiness.

AI-Enabled Care Gap Detection Redefines Time-to-Intervention Economics

AI-driven care gap detection is revolutionizing the chronic care management market by accelerating the pace from problem identification to clinical intervention. Cadence unveiled its AI-centric Proactive Care Engine on July 1, 2025, boasting a nearly 30% closure rate for care gaps in patients monitored for a minimum of 90 days. This underscores the tangible benefits of automated surveillance in enhancing follow-up performance. The competitive landscape is shifting, with a focus moving from staffing scale to the quality of data, workflow automation, and real-time action triggers. Projections indicate that by 2026, agentic AI will carve out a significant portion of healthcare IT budgets in the Asia-Pacific, with chronic disease management emerging as a prime investment area. Organizations leveraging persistent AI monitoring can act swiftly, bridge more care gaps, and manage larger patient groups without a proportional increase in labor.

Under-Diagnosed Multimorbidity in Aging Populations Creates Latent Demand

The intersection of aging populations and under-diagnosed multimorbidity is amplifying the demand for chronic care management. Patients grappling with multiple chronic conditions often navigate disjointed care pathways. A 2025 study highlighted in Frontiers in Public Health emphasized the efficacy of AI-driven precision medicine in early identification of multimorbid patients, facilitating enhanced care coordination.[3]Medical Economics, “Finalized 2025 Medicare Physician Fee Schedule Advances CCM and Value-Based Care with New Advanced Primary Care Management Codes,” Medical Economics, medicaleconomics.com This insight is crucial; multimorbid patients exert more strain on costs, utilization, and adherence than those with single conditions. Consequently, platforms adept at assessing risk across multiple conditions are gaining prominence over those focusing on isolated diseases. The demand surge is most pronounced in regions where aging, chronic disease prevalence, and workforce shortages converge, hinting at sustained growth in both established and emerging health systems.

Remote Patient Monitoring Partnerships Extend the Data Perimeter for Chronic Care

Remote patient monitoring (RPM) partnerships are revolutionizing chronic care management by shifting oversight from sporadic office visits to continuous home surveillance. A 2026 study in the Journal of Medical Internet Research highlighted the efficacy of RPM. It found that for Louisiana Medicare beneficiaries with diabetes and hypertension, RPM enrollment led to a notable decline in avoidable hospitalizations and emergency department visits.[4]Frontiers Media, “AI-Enabled Precision Medicine Models for Multimorbidity,” Frontiers in Public Health, frontiersin.org This underscores the significance of connected monitoring in chronic disease management. The integration of device data into care workflows outpaces traditional visit schedules, enhancing program economics. Vendors that unify device feeds, alerts, care plans, and outreach into a cohesive workflow are gaining a competitive edge over those treating RPM as a mere add-on.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Clinical documentation burden and billing challenges | -1.5% | Global, with highest pressure in North America and Western Europe | Short term (≤ 2 years) |

| Fragmented interoperability across EHR and RPM platforms | -1.8% | Global, especially in APAC and the U.S. where standards and legacy systems vary | Medium term (2-4 years) |

| Care team staffing constraints and patient retention | -1.2% | North America, Western Europe, and Australia | Medium term (2-4 years) |

| Narrow margin pressure in small practices | -0.8% | North America, South America, and Rest of Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Interoperability Across EHR and RPM Platforms Constrains Scale

Fragmented interoperability continues to hinder the chronic care management market, as effective workflows require complete and timely patient records from multiple systems. A 2025 ONC survey revealed that 60% of U.S. health systems identified fragmented and unstructured data as a barrier to managing care gaps effectively. Humana’s planned 2026 partnership with b.well Connected Health aims to address this by integrating provider, plan, pharmacy, and application data in real time. However, smaller vendors and provider groups often lack the resources for such advanced data integration, limiting the market's ability to scale evenly and affecting care plan quality, patient identification, and billing accuracy.

Clinical Documentation Burden Creates Adoption Drag and Compliance Exposure

Documentation requirements remain a significant challenge in the chronic care management market, as Medicare CCM mandates consistent outreach, care plan updates, time tracking, and audit-ready records. Smaller and independent practices face greater strain, as the same teams often manage patient communication, billing, and clinical coordination. While the 2026 reimbursement increase strengthens the financial case for CCM, it also raises the importance of maintaining compliant workflows. Organizations using AI-assisted documentation can manage more patients efficiently, while those relying on manual processes face heavier workloads and increased operational risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Displace Service-Only Models

In 2025, services accounted for 57.18% of the chronic care management market, highlighting the reliance on outsourced care coordination models during the market's early stages. Providers often depended on third-party organizations for clinical staffing, outreach, and billing support, as these services were easier to implement than internal digital workflows. While human intervention remains critical for managing complex chronic populations, the market is shifting toward platform-led automation, reducing reliance on labor-intensive delivery methods.

Software is projected to grow at a 15.90% CAGR through 2031, driven by AI systems automating tasks like intake, documentation, care plan generation, and routine patient engagement without proportional headcount increases. CCS announced in April 2026 that its AI deployment aims to process 70%-80% of over 100,000 monthly intake documents by year-end 2026, delivering over 30% in annual cost savings. eClinicalWorks launched the healow CCM Specialist Service in April 2026, reflecting a trend toward hybrid models where software and services converge. The industry is moving toward AI-augmented human interaction for complex tasks, while software handles repetitive, high-volume workflows.

By Deployment: Cloud Dominance Meets On-Premise Resilience

Cloud-based deployment held 71.22% of the chronic care management market in 2025, driven by its scalability, interoperability, and ability to handle large data volumes. Cloud environments support remote patient monitoring, centralized analytics, distributed care teams, and continuous updates, making them the preferred choice for organizations seeking fast implementation and system-wide visibility. Major vendors are aligning product roadmaps with cloud-native AI functionalities, reinforcing this trend.

Oracle launched an AI-driven EHR for ambulatory providers in August 2025, emphasizing voice-first clinical intelligence and conversational workflows. Epic introduced Agent Factory in March 2026, enabling AI agent deployment across clinical workflows. On-premise deployment is expected to grow at a 14.25% CAGR through 2031, as data sovereignty and residency requirements remain critical in governance-heavy contracts. While cloud solutions dominate by volume, on-premise systems retain relevance in markets with stricter regulatory controls.

By End User: Payers Accelerate Beyond Traditional Provider Dominance

Providers held 64.45% of the chronic care management market in 2025, reflecting their role in patient enrollment, care plan execution, discharge follow-ups, and chronic disease oversight. Reimbursement incentives favor structured workflows that document activities, ensure continuity, and close care gaps. Embedded analytics within EHR systems further support providers by integrating chronic disease management into routine clinical operations.

Payers are forecast to grow at a 16.69% CAGR through 2031, making them the fastest-growing end-user group. Vertical integration is driving this growth, as insurers increasingly manage member engagement, analytics, and chronic care workflows. UnitedHealth Group projected nearly USD 1 billion in cost savings in 2026 through AI-driven operational improvements and EMR consolidation. Humana’s interoperability initiatives and UnitedHealthcare’s Avery launch in March 2026 highlight the shift toward member retention and chronic condition support. Other end users, such as ACOs, FQHCs, and rural health clinics, are also gaining relevance as reimbursement pathways evolve.

By Disease Category: Diabetes Anchors Revenue While Respiratory Segment Accelerates

Diabetes accounted for 34.66% of the chronic care management market in 2025, supported by reimbursed monitoring, care coordination, and digital disease management programs. The segment benefits from structured monitoring, consistent outreach, and measurable interventions, maintaining its position as a revenue driver. Cardiovascular diseases and cancer also remain significant due to their need for long-term management and workflow support under value-based care models.

Chronic respiratory diseases are projected to grow at a 15.33% CAGR through 2031, driven by post-COVID-19 respiratory burdens, rising COPD prevalence, and increased adoption of RPM-compatible spirometry and oxygen monitoring. Other chronic conditions, such as kidney disease and musculoskeletal disorders, are gaining attention due to new reimbursement pathways. Twin Health reported significant diabetes and weight-loss outcomes in August 2025 without high-cost GLP-1 medications, reflecting payer interest in cost-effective digital models. The market is shaped by disease prevalence, reimbursement design, and digital tools that enhance platform deployment for specific patient groups.

Geography Analysis

In 2025, North America accounted for 41.55% of the chronic care management market, establishing itself as the largest regional contributor to current revenues. This leadership is driven by the maturity of Medicare's CCM billing, increased payer digitization, and significant investments in chronic care software and services. The CY 2026 Physician Fee Schedule introduced a 10% reimbursement increase for CCM, encouraging broader provider adoption and improving program economics. The U.S. market is also becoming polarized between integrated payer-delivery platforms and specialist vendors supporting smaller and mid-sized practices.

Europe remains the second-largest region in the chronic care management market, with Germany and the U.K. leading adoption. Germany's DiGA framework facilitates digital health reimbursements, creating a streamlined pathway for certified chronic disease management applications. The U.K. is advancing in digital chronic care, with studies highlighting the cost-effectiveness of remote monitoring systems for older adults under public insurance frameworks. Other countries like France, Italy, and Spain are expanding gradually as demographic pressures rise and reimbursement structures mature.

Asia-Pacific is projected to grow at a 16.45% CAGR through 2031, making it the fastest-growing region in the chronic care management market. Growth is driven by the rising chronic disease burden, investments in digital health policies, and the need for structured care delivery in fragmented health systems. Countries like India, China, Japan, South Korea, and Australia are advancing through diverse initiatives, including national digital health programs, preventive AI strategies, and clinically governed decision support models. The Middle East, Africa, and South America remain in early stages, with demand focused on urban modernization projects and selective health system digitization rather than widespread national adoption.

Competitive Landscape

The chronic care management market is moderately fragmented at the vendor level, yet it becomes more concentrated at the intersection of payer integration and care delivery control. EHR vendors, payer-owned platforms, specialist chronic care companies, and analytics providers compete across adjacent segments of the value chain. Factors such as switching costs, workflow depth, reimbursement alignment, and data access are as critical as standalone clinical functionality. While no single vendor type dominates the market, a select group of integrated players exerts a stronger influence on industry standards.

Epic Systems, Oracle Health, eClinicalWorks, and NextGen Healthcare, rooted in EHR, are embedding chronic care functions into daily clinical workflows. Oracle’s August 2025 launch of its revamped AI-driven ambulatory EHR highlights how major platform vendors now prioritize AI-enabled chronic disease management as a core growth area. Epic’s March 2026 Agent Factory further raises the competitive bar by enabling health systems to deploy AI agents within clinical operations, reducing reliance on standalone chronic care tools. Specialist platforms like ChartSpan, Prevounce Health, HealthSnap, and ZeOmega focus on delivering deeper program execution and condition-specific workflows, excelling in areas requiring faster outcome tracking, quarterly reporting, and targeted disease management.

Payer-owned platforms add competitive pressure by integrating care management with claims, benefits, quality scores, and member engagement. Initiatives like Humana’s real-time interoperability with b.well and UnitedHealthcare’s Avery launch demonstrate how payers are transforming chronic care into a member-focused navigation and retention tool. The competition now centers on outcome readiness, as platforms reliant on manual documentation must adapt to workflows emphasizing interoperability, automation, and measurable performance. Vendors capable of automating intake, care gap detection, outreach, and reporting within a single system are better positioned to protect margins as payment models evolve.

Chronic Care Management Industry Leaders

Epic Systems Corporation

Oracle Corporation

ChartSpan Medical Technologies, Inc.

ZeOmega, Inc.

Medecision, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Cohere Health expanded its Cohere Unify platform, integrating agentic AI to enhance care management, appeals, claims operations, and quality functions by leveraging clinical and utilization data.

- April 2026: eClinicalWorks launched the healow CCM Specialist Service, embedding certified clinicians into EHR workflows to automate outreach, documentation, and billing compliance for Medicare CCM.

- April 2026: CCS deployed enterprise-wide agentic AI, projecting over 30% cost savings and automating 70%-80% of 100,000 monthly intake documents by year-end 2026.

- April 2026: Humana Inc. implemented b.well Connected Health, enabling real-time health data integration to improve care coordination and quality workflows for its special needs plan population.

- March 2026: Epic Systems introduced Agent Factory and Curiosity, medical models trained on anonymized patient records to predict disease progression, medication efficacy, and outcomes.

- March 2026: UnitedHealth Group launched Avery, a generative AI companion on its app, to streamline benefits navigation, appointment scheduling, and chronic disease management while targeting USD 1 billion in AI-driven cost reductions in 2026.

Global Chronic Care Management Market Report Scope

As per the scope of the report, chronic care management (CCM) is an ongoing healthcare service. It provides regular out-of-office support to patients with multiple long-term health conditions (like diabetes or heart disease). Care teams coordinate treatments, manage medications, and check on patients between regular doctor visits.

The chronic care management market is segmented by component, deployment, end-user, disease category, and geography. By component, the market includes software and services. By deployment, the market is segmented into cloud-based and on-premise solutions. By end-user, the market is categorized into providers, payers, and other end-users. By disease category, the market is segmented into diabetes, cardiovascular diseases, chronic respiratory diseases, cancer, and other chronic diseases. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Providers |

| Payers |

| Other End Users |

| Diabetes |

| Cardiovascular Diseases |

| Chronic Respiratory Diseases |

| Cancer |

| Other Chronic Diseases |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment | Cloud-Based | |

| On-Premise | ||

| By End User | Providers | |

| Payers | ||

| Other End Users | ||

| By Disease Category | Diabetes | |

| Cardiovascular Diseases | ||

| Chronic Respiratory Diseases | ||

| Cancer | ||

| Other Chronic Diseases | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of chronic care management in 2026?

The chronic care management market is valued at USD 7.11 billion in 2026 and is forecast to reach USD 13.05 billion by 2031 at a 12.90% CAGR.

Which region leads global revenue?

North America led with a 41.55% revenue share in 2025, supported by mature Medicare billing infrastructure and stronger payer digitization.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow at a 16.45% CAGR through 2031, driven by rising chronic disease burden and stronger digital health investment.

Which end-user group is expanding the fastest?

Payers are projected to grow at a 16.69% CAGR through 2031 as insurers build more proprietary care management and member engagement capabilities.

Which disease area contributes the largest revenue base?

Diabetes accounted for 34.66% of revenue in 2025, making it the largest disease category because of its strong fit with reimbursed monitoring and structured follow-up.

What is the main shift shaping vendor strategy?

Vendor strategy is moving toward AI, interoperability, and outcome-ready workflows, with Oracle, Epic, Humana, UnitedHealth, CCS, and Cadence all making visible platform moves in 2025 and 2026.

Page last updated on: