Chronic Obstructive Pulmonary Disease (COPD) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

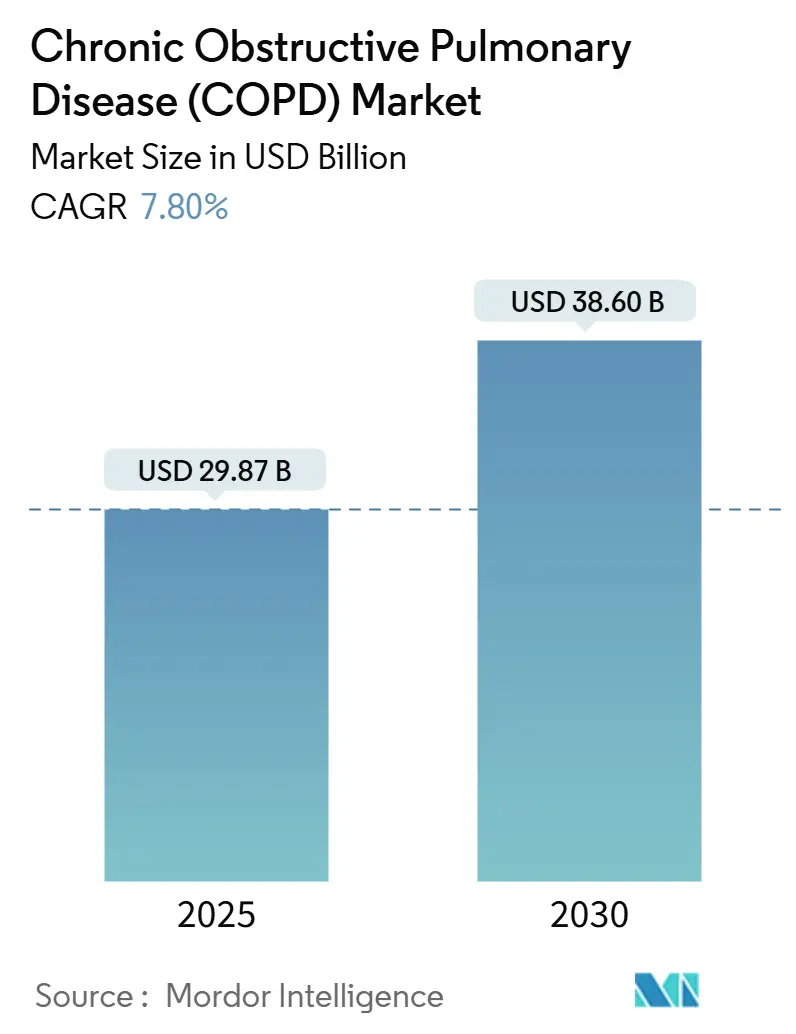

| Market Size (2025) | USD 29.87 Billion |

| Market Size (2030) | USD 38.60 Billion |

| Growth Rate (2025 - 2030) | 7.80% CAGR |

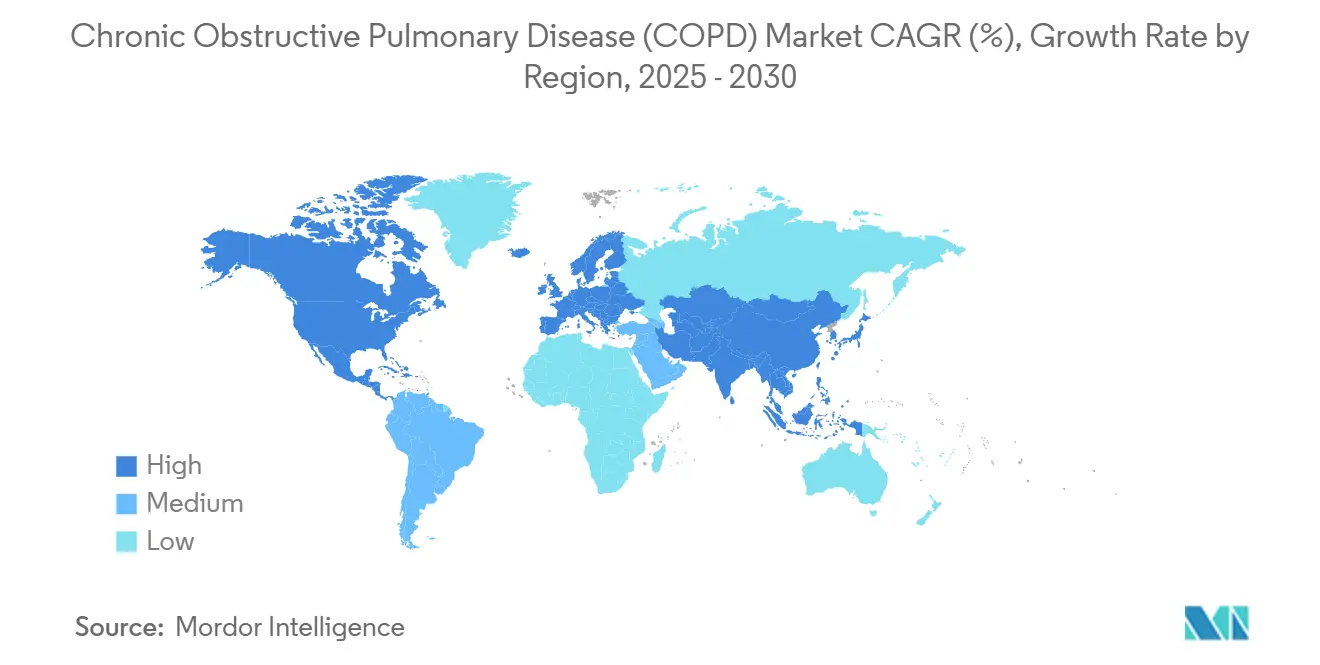

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

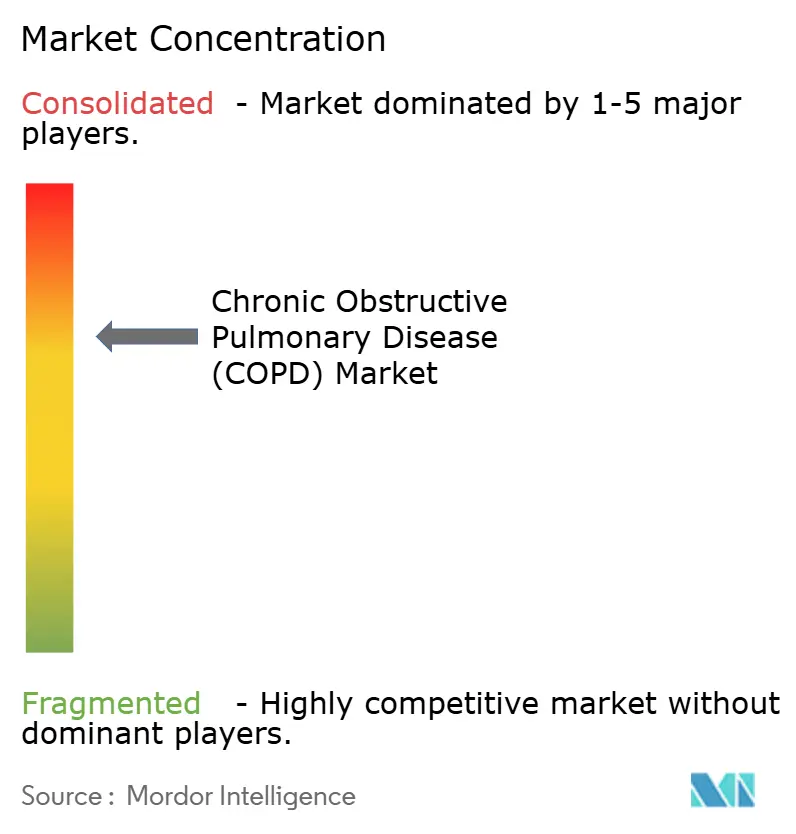

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chronic Obstructive Pulmonary Disease (COPD) Market Analysis by Mordor Intelligence

The Chronic Obstructive Pulmonary Disease Market size is estimated at USD 29.87 billion in 2025, and is expected to reach USD 38.60 billion by 2030, at a CAGR of 7.80% during the forecast period (2025-2030).

The uptake of triple-combination inhalers, early penetration of first-in-class biologics for eosinophilic phenotypes, and Medicare-driven shifts from inpatient to home-based respiratory care are redefining addressable patient pools, reimbursement levers, and profit pools across the COPD market. Continuous remote monitoring through connected inhalers, pulse oximeters, and spirometers is generating real-world evidence that payers now require for premium reimbursement, while European propellant phasedowns are forcing inhaler reformulations that refresh product lifecycles and pricing. Competitive intensity is highest where formulary access, digital-adherence tooling, and low-GWP propellant readiness intersect, driving a surge of partnerships between pharmaceutical manufacturers and device-software specialists.

Key Report Takeaways

- By product type, Drug Class therapies held 64.80% of the COPD market share in 2024, whereas Consumables & Accessories are forecast to expand at a 7.40% CAGR to 2030.

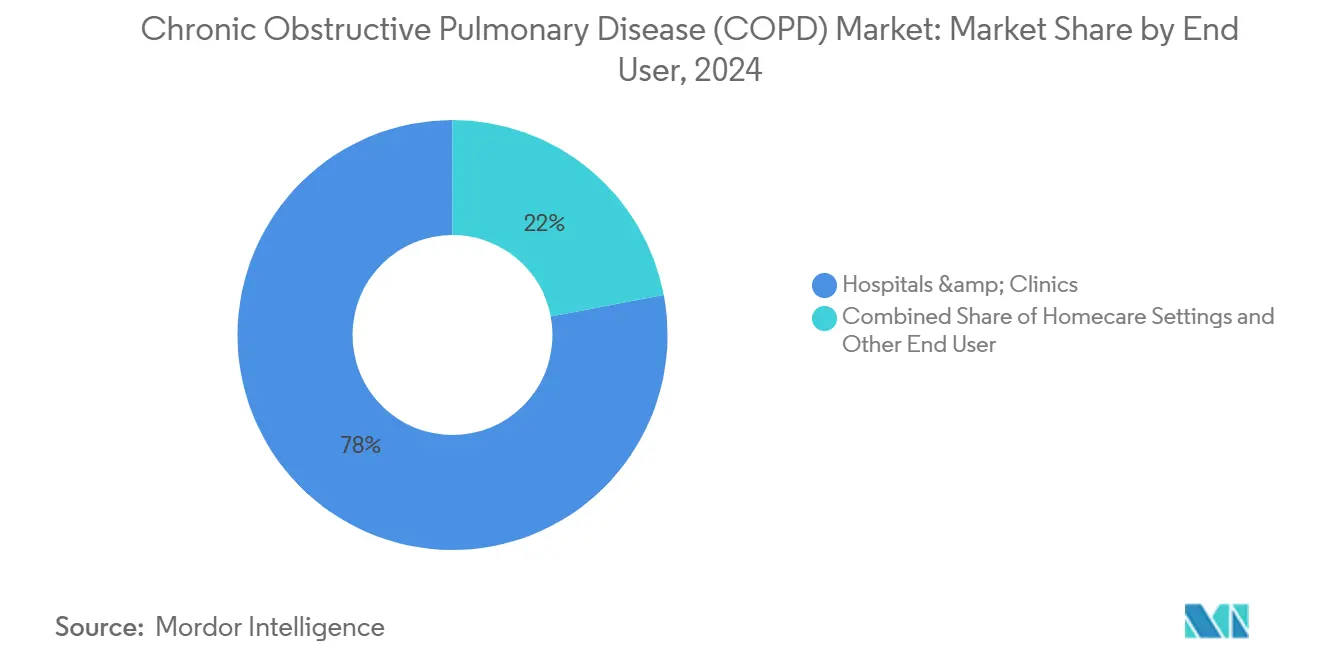

- By end user, hospitals and clinics held 77.97% of the COPD market share in 2024, whereas home care settings are forecast to expand at a 6.81% CAGR through 2030.

- By geography, North America captured 38.12% of the revenue in 2024, while the Asia-Pacific region is projected to record the fastest growth of 7.30% CAGR through 2030, as spirometry capacity scales in China and India.

Global Chronic Obstructive Pulmonary Disease (COPD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging, Smoking, and Air-Pollution Burden Lifting COPD Incidence and Severity | +1.20% | Global, with acute concentration in Asia-Pacific urban centers and Eastern Europe | Long term (≥ 4 years) |

| Digital Respiratory Devices, Connected Inhalers, And Remote Monitoring Improving Adherence and Outcomes | +0.90% | North America & Western Europe, early pilots in urban China | Medium term (2-4 years) |

| First-In-Class Biologics for Eosinophilic COPD Broadening Addressable Treated Population | +0.80% | North America, EU-5, Japan; limited LMIC penetration due to pricing | Medium term (2-4 years) |

| Shift To Home-Based Care: Portable Oxygen and Non-Invasive Ventilation Enabling Care Outside Hospitals | +0.70% | North America (Medicare-driven), Western Europe, Australia | Short term (≤ 2 years) |

| Low-GWP Propellant Transition (HFA-152a) Catalyzing Inhaler Product Refresh and Formulary Churn | +0.60% | EU (F-gas regulation mandate), North America (voluntary adoption) | Short term (≤ 2 years) |

| Rising Spirometry/PFT Capacity and Earlier Diagnosis Embedded In Primary Care Pathways | +0.50% | Asia-Pacific (China, India), Latin America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging, Smoking, and Air-Pollution Burden Lifting COPD Incidence and Severity

Global demographics and environmental trends are converging to drive the growth of the COPD market. Large urban centers in China and India continue to post PM2.5 readings that are well above the WHO limits, thereby amplifying lifetime exposure risks. Smoking cessation campaigns are curbing prevalence among affluent populations, yet male smoking rates remain over 50% in several rural Chinese provinces, offsetting public-health gains. By 2030, China is expected to have 280 million citizens aged 65 and above, many of whom will have experienced cumulative exposure to smoke and pollution, which accelerates the progression of airflow limitation.[1]Source: World Health Organization, “Air Quality and Health,” who.int Epidemiological data from Delhi and Mumbai show annual PM2.5 averages above 100 μg/m³, which is double the level linked to rapid lung-function decline, thereby raising the long-term threshold for COPD incidence. Biomass fuel use in sub-Saharan Africa and Southeast Asia is another vector, exposing women who cook indoors to particulate levels comparable to those in dense traffic corridors, which sustains demand for portable spirometers in underserved clinics.

Digital Respiratory Devices, Connected Inhalers, and Remote Monitoring Improving Adherence and Outcomes

Bluetooth-enabled dose counters embedded in inhalers have shifted from small pilots to a baseline requirement for several U.S. managed-care formularies. Propeller Health’s collaboration with GSK’s Ellipta devices reduced rescue-inhaler use by 58% in 2024 field trials. Commercially insured patients under 60 sustain 72% app engagement beyond 90 days, but adherence falls to 31% among Medicare beneficiaries over 70, illustrating a digital literacy divide. Payers are tying reimbursement to objective adherence metrics, prompting manufacturers to invest in user-friendly interfaces and multilingual support. The FDA’s 2024 draft guidance on software as a medical device clarified submissions for AI-enabled exacerbation prediction in wearables, which has shortened regulatory cycles for start-ups bundling connected pulse oximeters into COPD market offerings.[2]Source: U.S. Food and Drug Administration, “Guidance on Software as a Medical Device,” fda.gov

First-in-Class Biologics for Eosinophilic COPD Broadening the Treated Population

Regeneron’s dupilumab gained FDA approval for COPD with type 2 inflammation in September 2024, achieving a 30% reduction in moderate to severe exacerbations compared to placebo. The USD 37,000 annual list price positions the therapy between conventional inhalers and hospitalization costs, but payer uptake hinges on biomarker-driven prescribing, which covers only 15–20% of COPD patients who meet eosinophil thresholds. AstraZeneca’s benralizumab and GSK’s mepolizumab are pursuing label expansions in comparable phenotypes, intensifying biologics competition. Market penetration depends on routine eosinophil testing in primary care; however, coverage for blood counts remains uneven across U.S. commercial plans and is largely absent in many low- to middle-income countries. Early real-world data will determine whether the biologics class can expand the COPD market or cannibalize the high-dose triple inhaler market.

Shift to Home-Based Care Accelerating Adoption of Portable Oxygen and Non-Invasive Ventilation

Medicare’s 2024 fee-schedule update increased reimbursement for portable oxygen concentrators and non-invasive ventilators, encouraging hospitals to discharge COPD patients earlier and reduce the need for skilled-nursing facility days. Durable medical-equipment suppliers responded by bundling hardware leases with subscription consumables, creating predictable annuity streams that grow faster than inpatient drug budgets. Remote monitoring platforms now integrate oxygen-saturation feeds, spirometry data, and inhaler-use logs into unified dashboards for pulmonologists, closing feedback loops that previously required in-person visits. Early results from U.S. pilot networks indicate a 20% reduction in 30-day readmissions, resulting in favorable shared-savings metrics that further incentivize payer adoption. However, seniors over 70 demonstrate 40% lower engagement with app-based reminders, which tempers the projected upside until human-factors design catches up with the needs of the geriatric population.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Underdiagnosis/Misdiagnosis Due To Limited Spirometry Use and Uneven Primary Care Capacity | -0.90% | Global, acute in LMICs and rural regions of high-income countries | Long term (≥ 4 years) |

| Affordability And Access Constraints for Advanced Drugs/Devices in LMICs | -0.70% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| F-Gas/Propellant Transitions and Supply Chain Complexity Elevating Costs and Near-Term Stockout Risk | -0.50% | EU (regulatory mandate), North America (voluntary adoption) | Short term (≤ 2 years) |

| Digital Divide and Health Literacy Barriers Limiting Uptake of Remote Monitoring and Connected Devices | -0.40% | Elderly populations globally, rural and underserved communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Underdiagnosis and Misdiagnosis Due to Limited Spirometry Use

Less than 30% of symptomatic adults in primary care settings receive spirometry before receiving empiric treatment, a gap that is most acute in lower-middle-income countries, where device density averages below 1 per 100,000 residents.[3]Source: European Respiratory Society, “Spirometry Utilization Audits,” ersnet.org Misclassification as asthma or heart failure delays the initiation of appropriate bronchodilators and leaves reversible airflow limitation unmanaged until the condition becomes irreversible. In Germany and the United Kingdom, audits conducted in 2024 revealed that only 42% of eligible patients underwent testing within six months of symptom onset, despite guideline updates that mandated spirometry. The consequence is a higher frequency of exacerbations, longer inpatient stays, and inflated downstream treatment costs, which erode payer willingness to reimburse premium inhalers. Scaling diagnostic capacity, therefore, remains a strategic imperative for stakeholders seeking to expand the COPD market without compromising cost-effectiveness benchmarks.

Affordability and Access Constraints for Advanced Drugs and Devices in LMICs

Branded triple-combination inhalers are priced above USD 200 per month, well beyond the reach of most COPD patients in South Asia and sub-Saharan Africa, where out-of-pocket spending accounts for more than 60% of total health expenditure. Generic alternatives exist, but they suffer from fragmented distribution networks and variable quality assurance, resulting in subtherapeutic dosing and inadequate disease control. Biologics carry wholesale prices above USD 30,000 annually and are almost absent from LMIC formularies, limiting addressable volume. Import tariffs ranging from 15% to 30% on home oxygen devices double end-user costs, further restricting market expansion. Manufacturers pursuing the COPD market in these geographies must adopt tiered pricing, local production, and partnership models to capture volume growth without eroding global margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Maintenance Therapies Underpin Revenue Leadership

Drug Class therapies generated 64.80% of COPD market revenue in 2024, as long-acting bronchodilators and inhaled corticosteroid combinations remain first-line maintenance options. Leading molecules, including tiotropium, indacaterol, and fluticasone-based triple inhalers, dominate prescribing guidelines, reinforcing stable demand and consistent cash flows. Manufacturers protect COPD market share by packaging established actives into once-daily fixed-dose combinations that simplify regimens and bolster adherence. Yet approaching patent cliffs for Advair, Symbicort, and related franchises accelerates pricing pressure, prompting developers to pivot toward next-generation mechanisms and digital-adherence add-ons. Meanwhile, Verona Pharma’s ensifentrine launch in 2024 introduced the first dual PDE-3/4 inhibitor to the COPD market, signaling that novel pharmacology can still capture formulary space if exacerbation data remain compelling.

The cost of biology has hindered broad adoption, yet premium reimbursement in high-income markets creates a lucrative, albeit narrow, revenue stream. Biologics’ success hinges on concurrent expansion of eosinophil testing, and early data indicate that payer-mandated biomarker thresholds are already limiting initial uptake. Still, the COPD market size for biologics could climb rapidly if inhaled protein delivery platforms under development by AstraZeneca and GSK solve current cold-chain and administration hurdles. Pipeline visibility and regulatory clarity, therefore, position Drug Class innovations as a central lever for sustaining double-digit revenue contribution even as generic erosion intensifies.

Remote monitoring devices, including wearable pulse oximeters and handheld capnographs, have evolved from niche home care aids to integral elements of value-based contracts in the COPD market. The FDA’s 2024 clearance of algorithms predicting exacerbations 72 hours in advance enables clinicians to preempt severe events with medication adjustments, thereby reducing emergency department visits. Manufacturers differentiate through battery life, sensor accuracy, and interoperability with popular inhaler platforms, fostering an ecosystem effect that locks patients into holistic solutions. Subscription cloud services that analyze real-time data amplify recurring revenue and feed anonymized datasets into machine-learning models, reinforcing competitive moats.

The digital-literacy gap among elderly patients, necessitating caregiver engagement and simplified interfaces temper market expansion. Industrial design choices—single-button operation, large displays, tactile feedback—are improving uptake, and early studies show 20% adherence lifts when devices pair automatically via Bluetooth Low Energy without complex user input. Growing evidence of reduced readmission rates is incentivizing insurers to reimburse devices alongside traditional pharmacotherapy, positioning monitoring solutions as a pivotal growth vector across the COPD market.

Consumables & Accessories, although constituting a smaller revenue base, are experiencing a 7.40% CAGR, driven by a systemic shift toward home-based respiratory management. Single-use pulse oximeter sensors, nebulizer masks, capnography sampling lines, and spirometry mouthpieces enable connected care pathways and generate predictable replenishment cycles. Durable medical equipment providers bundle consumables within subscription models, reinforcing customer lock-in and smoothing revenue volatility compared to one-time device sales. Environmental mandates add momentum, as low-GWP propellant canisters and recyclable plastics attract stewardship incentives that tilt purchasing decisions. Adherence-linked reimbursement from payers further elevates demand for verified high-quality consumables that transmit usage data to clinicians via IoT hubs.

Emerging COPD market entrants are experimenting with direct-to-consumer channels that deliver pre-configured supply packs to patients’ homes, circumventing traditional hospital procurement. Early pilots in Australia and the United Kingdom achieved reorder rates above 85% when apps automatically flagged depleted supplies, demonstrating that convenience can translate into high retention. Consumables’ superior growth trajectory also offsets slower volume increases in legacy drug categories, hedging manufacturer portfolios against potential pricing compression.

By End-User Setting: Homecare Overtakes Hospital as Cost-Effective Venue

Hospitals and clinics held 77.97% of the COPD market share in 2024, whereas home care settings are forecast to expand at a 6.81% CAGR through 2030. Hospital settings historically consumed the bulk of COPD expenditure, but payer incentives now favor home care models that slash length-of-stay and post-acute costs. Under Medicare readmission penalties, U.S. hospitals partner with home health agencies to transition patients to portable oxygen concentrators within 48 hours of discharge, reducing inpatient days by up to 30%. Public insurance systems in Germany and Japan mirror the trend, reimbursing tele-rehabilitation sessions that substitute for outpatient clinic visits. Equipment leasing models distribute capital costs over multiyear contracts, lowering entry barriers for payers and facilitating widespread uptake.

Homecare’s ascendancy reshapes procurement dynamics, as purchasing decisions shift from hospital pharmacy committees to integrated delivery networks and patient-centric supply portals. Vendors investing in logistics and customer-support infrastructure gain a first-mover advantage, while hospitals reallocate resources toward managing acute exacerbations. The shift underpins sustained demand for consumables and monitoring devices, ensuring that the COPD market remains vibrant even as inpatient drug volumes plateau.

Geography Analysis

North America retained 38.12% of 2024 revenue by virtue of high per-capita healthcare spending, broad insurance coverage, and rapid uptake of connected respiratory devices. The United States alone accounts for nearly 90% of regional COPD market size; Medicare Part D and commercial insurers both employ step-therapy ladders that start with generics before escalating to triple inhalers and biologics. Early adoption of adherence-linked reimbursement has attracted hardware-software partnerships, with device makers sharing risk through value-based contracts. Canada’s provincial formularies mirror U.S. patterns but exhibit wider access to triple combinations, particularly in Ontario and Quebec, due in part to centralized price negotiations and bundled tenders. Mexico’s dual-tier system splits private payers who embrace branded innovations and public IMSS clinics limited largely to short-acting bronchodilators, keeping overall growth moderate.

Europe held the second-largest COPD market share in 2024, anchored by Germany, the United Kingdom, France, Italy, and Spain. Germany’s Disease Management Program for chronic respiratory diseases enrolls over 1 million patients in structured follow-up protocols, boosting adherence and funding device upgrades through statutory insurance. The United Kingdom’s NHS updated its COPD pathway in 2024 to ensure spirometry in all primary-care settings, yet fiscal pressures delay national scaling of connected inhalers beyond pilots concentrated in London and Manchester. France improved reimbursement for portable oxygen concentrators, aligning with a national hospital-avoidance strategy. Italy and Spain face budget constraints slowing biologic uptake despite positive cost-effectiveness appraisals, resulting in patchy access that shapes manufacturer launch sequencing across EU-5.

Asia-Pacific is expanding at a 7.30% CAGR, the fastest regional trajectory, as China and India embed spirometry-based screening into adult physicals and distribute subsidized inhalers through national insurance schemes. China’s policy mandating annual pulmonary testing for urban adults over 40 could surface an estimated 15 million previously undiagnosed cases by 2027, enlarging COPD market size for both drugs and devices. India’s Ayushman Bharat added tiotropium and formoterol to its essential medicines list, reducing out-of-pocket costs for 200 million covered citizens, yet rural distribution gaps persist. Japan’s aging society sustains high penetration of home oxygen therapies, while South Korea reimburses 80% of inhaler expenses, fostering robust demand for premium triple combinations. Australia’s Pharmaceutical Benefits Scheme covers triple inhalers for patients meeting severity criteria and integrates telehealth-driven monitoring pathways, bolstering early adoption of AI-assisted predictive algorithms.

Emerging COPD market opportunities in the Middle East, Africa, and Latin America remain fragmented. Gulf Cooperation Council nations such as Saudi Arabia and the UAE invest heavily in pulmonary clinics, importing advanced diagnostic devices but still lack comprehensive epidemiological datasets. South Africa allocates limited public funds to chronic respiratory conditions amid competing infectious-disease burdens, though private insurers in major cities cover branded inhalers. Sub-Saharan regions grapple with biomass-fuel exposure and under-diagnosis due to limited spirometry, constraining COPD market growth until infrastructure improves. Brazil and Argentina lead South America in volume, yet stockouts of tiotropium and formoterol within public systems in 2024 pushed patients toward out-of-pocket purchases, underscoring supply-chain volatility’s dampening effect on adoption.

Competitive Landscape

The COPD market exhibits moderate concentration, with the top five pharmaceutical manufacturers, such as GSK, Boehringer Ingelheim, AstraZeneca, Novartis, and Chiesi, capturing roughly 55% of global prescription sales. These incumbents defend their franchise positions through once-daily fixed-dose combinations, patent-extension strategies, and large sales forces targeting pulmonology specialists. Digital-adherence tie-ins are the latest differentiation lever; GSK’s Trelegy Ellipta bundles Propeller Health sensors under outcomes-based agreements that trigger rebates if adherence targets are missed. Nevertheless, Verona Pharma’s 2024 approval of ensifentrine introduced a dual PDE-3/4 mechanism that challenges entrenched players by positioning it below biologics in price while promising meaningful reductions in exacerbations.

Device competition remains fragmented among regional specialists, with NDD Medical Technologies and Vyaire Medical vying for leadership in spirometry through accuracy and EMR integration. Start-ups such as Adherium focus on sensor-enabled add-ons rather than complete platforms, partnering with large pharmaceutical companies to integrate connectivity into existing inhalers. Supply-chain adaptability around low-GWP propellants is emerging as a strategic moat; AstraZeneca’s USD 400 million upgrade to its Dunkirk facility will add 50 million HFA-152a units annually by 2026, hedging against EU quota tightening.

White-space opportunities cluster in underserved phenotypes and geographies. Biologics for non-eosinophilic COPD represent an untapped 80% of the patient pool, but heterogenous inflammatory pathways complicate target identification. AI-based exacerbation prediction, leveraging continuous device data, may unlock risk-sharing contracts that lower payer barriers, provided validation cohorts reflect real-world heterogeneity. Manufacturers willing to invest in local production and tiered pricing in India, Indonesia, and Nigeria could capture high-volume growth, though regulatory uncertainty and intellectual-property enforcement remain obstacles. Pipeline patent filings in 2024 reveal that AstraZeneca and GSK are experimenting with inhaled protein formulations that might bypass cold-chain requirements, potentially reshaping biologic delivery paradigms if stability hurdles are overcome.

Chronic Obstructive Pulmonary Disease (COPD) Industry Leaders

AstraZeneca PLC

GlaxoSmithKline PLC

Koninklijke Philips N.V.

Boehringer Ingelheim GmbH

ResMed

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Teva and Propeller Health launched the connected ProAir RespiClick inhaler in U.S. managed-care channels, tying rebates to verified adherence metrics.

- November 2024: Cipla received Indian approval for its generic tiotropium/olodaterol, expanding access to dual-bronchodilators at a 60% discount compared to branded references.

- October 2024: Vyaire Medical introduced Vyntus SPIRO, featuring AI-assisted quality control that flags suboptimal patient effort in real-time, securing the CE mark and awaiting FDA 510(k) clearance.

- September 2024: Regeneron secured FDA approval for dupilumab in COPD patients with elevated eosinophils, following Phase 3 trials that showed a 30% reduction in exacerbations compared to placebo.

Global Chronic Obstructive Pulmonary Disease (COPD) Market Report Scope

| Drug Class | Bronchodilators | Short-acting Beta 2 Agonists |

| Long-acting Beta 2 Agonists | ||

| Anticholinergic Agents | ||

| Anti-inflammatory Drugs | Oral & Inhaled Corticosteroids | |

| Phosphodiesterase-4 Inhibitors | ||

| Other Anti-inflammatory Drugs | ||

| Combination Drugs | ||

| Diagnostic Devices | Spirometers | |

| Electrocardiogram (ECG) | ||

| Others | ||

| Monitoring Devices | Pulse Oximeters | |

| Capnograph | ||

| Portable Table-Top Pulse Oximeter | ||

| Wearable Devices | ||

| Fourier Transform Infrared Spectroscopy (FTIR) | ||

| Consumables and Accessories | Masks | |

| Spirometry Accessories | ||

| Pulse Oximeter Sensors | ||

| Capnography Accessories | ||

| Gas Analyzer Accessories | ||

| Others | ||

| Hospitals & Clinics |

| Homecare Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Drug Class | Bronchodilators | Short-acting Beta 2 Agonists |

| Long-acting Beta 2 Agonists | |||

| Anticholinergic Agents | |||

| Anti-inflammatory Drugs | Oral & Inhaled Corticosteroids | ||

| Phosphodiesterase-4 Inhibitors | |||

| Other Anti-inflammatory Drugs | |||

| Combination Drugs | |||

| Diagnostic Devices | Spirometers | ||

| Electrocardiogram (ECG) | |||

| Others | |||

| Monitoring Devices | Pulse Oximeters | ||

| Capnograph | |||

| Portable Table-Top Pulse Oximeter | |||

| Wearable Devices | |||

| Fourier Transform Infrared Spectroscopy (FTIR) | |||

| Consumables and Accessories | Masks | ||

| Spirometry Accessories | |||

| Pulse Oximeter Sensors | |||

| Capnography Accessories | |||

| Gas Analyzer Accessories | |||

| Others | |||

| By End User | Hospitals & Clinics | ||

| Homecare Settings | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the COPD market in 2030?

The COPD market size is forecast to reach USD 38.6 billion by 2030, growing at a 5.3% CAGR.

Which product category currently leads global revenue?

Drug Class therapies, including long-acting bronchodilators and triple combinations, commanded 64.80% of 2024 revenue.

Which region is expanding the fastest?

Asia-Pacific is expected to register the quickest 7.30% CAGR through 2030 as China and India scale diagnostic capacity.

How are low-GWP propellants affecting inhaler strategy?

EU F-gas rules push inhaler makers to adopt HFA-152a, enabling pricing resets but raising supply-chain risk due to limited propellant suppliers.

What role do connected devices play in COPD management?

Bluetooth-enabled inhalers and wearable monitors improve adherence and enable AI-driven exacerbation prediction, lowering readmission rates in value-based contracts.

Page last updated on: