Population Health Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 75.32 Billion |

| Market Size (2031) | USD 176.90 Billion |

| Growth Rate (2026 - 2031) | 18.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Population Health Management Market Analysis by Mordor Intelligence

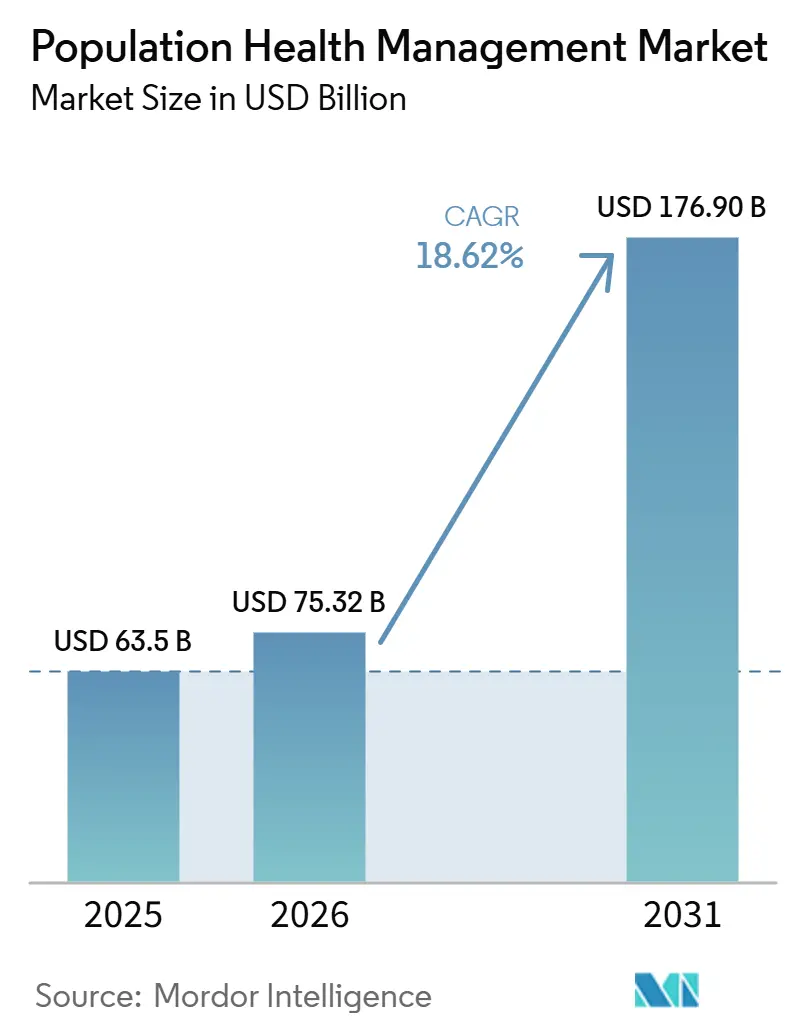

The Population Health Management Market size is expected to grow from USD 63.5 billion in 2025 to USD 75.32 billion in 2026 and is forecast to reach USD 176.90 billion by 2031 at 18.62% CAGR over 2026-2031.

This rapid expansion mirrors healthcare's pivot from one-off treatments to continual oversight of whole populations, creating new layers of demand for data-driven care coordination. Fresh momentum comes from three converging forces: value-based reimbursement, AI-enabled analytics, and rising chronic-disease prevalence. Each factor pushes decision-makers to invest in connected tools that spot care gaps earlier and allocate resources more precisely. Stronger financial incentives, rather than technology improvements alone, are pushing organizations toward full-scale adoption, and reimbursement changes can accelerate digital upgrades more than raw innovation.

Another dimension shaping the Population Health Management industry is the clear link between preventive care and cost control; payers and providers see measurable savings when hospitalizations fall and readmissions drop. North America leads with an estimated 48.8% Population Health Management market share in 2024, yet Asia-Pacific's growth pace hints that leadership could diversify as digital health spending rises across emerging economies. An early focus on cloud delivery enables new entrants in fast-growing regions to leapfrog legacy systems and reduce time to value. Continued deal activity—USD 69 billion in 2024 healthcare M&A alone—signals that scale, data breadth, and ecosystem reach are becoming the real competitive currencies.

Key Report Takeaways

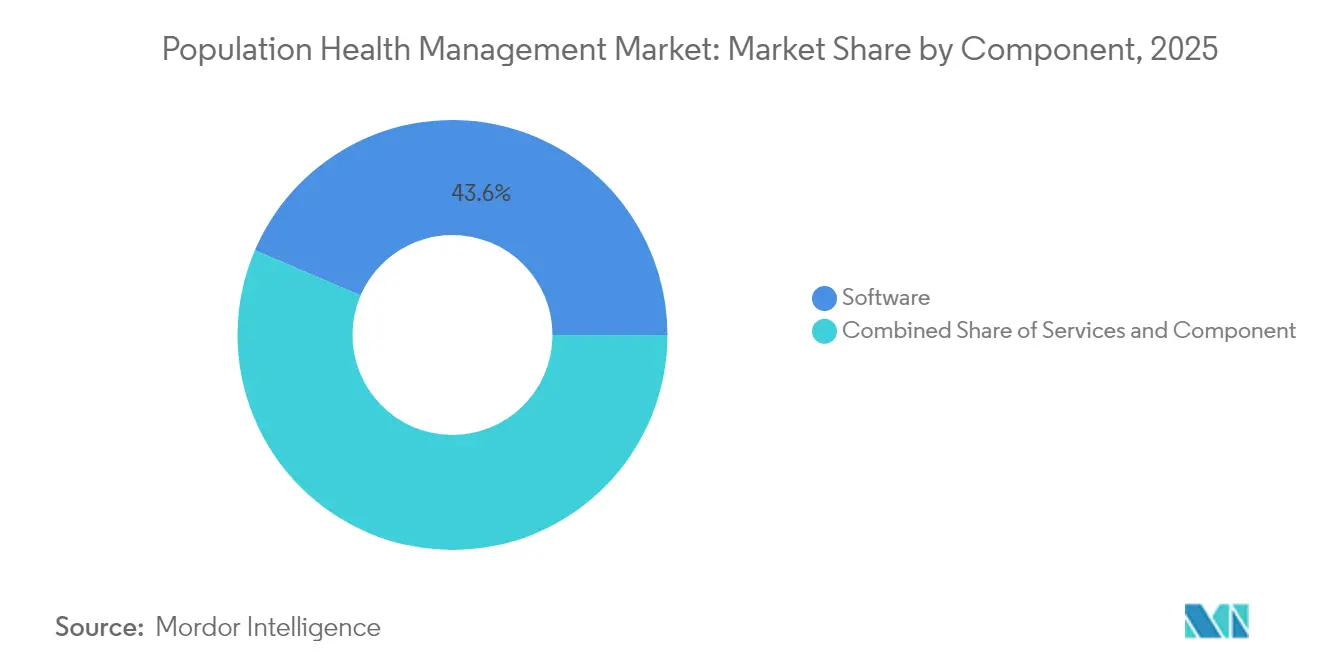

- By component, software led with 43.55% revenue share in 2025, while services are projected to expand at 19.94% CAGR through 2031.

- By solution type, population health analytics accounted for 31.05% in 2025, whereas patient engagement solutions are advancing at a 21.48% CAGR to 2031.

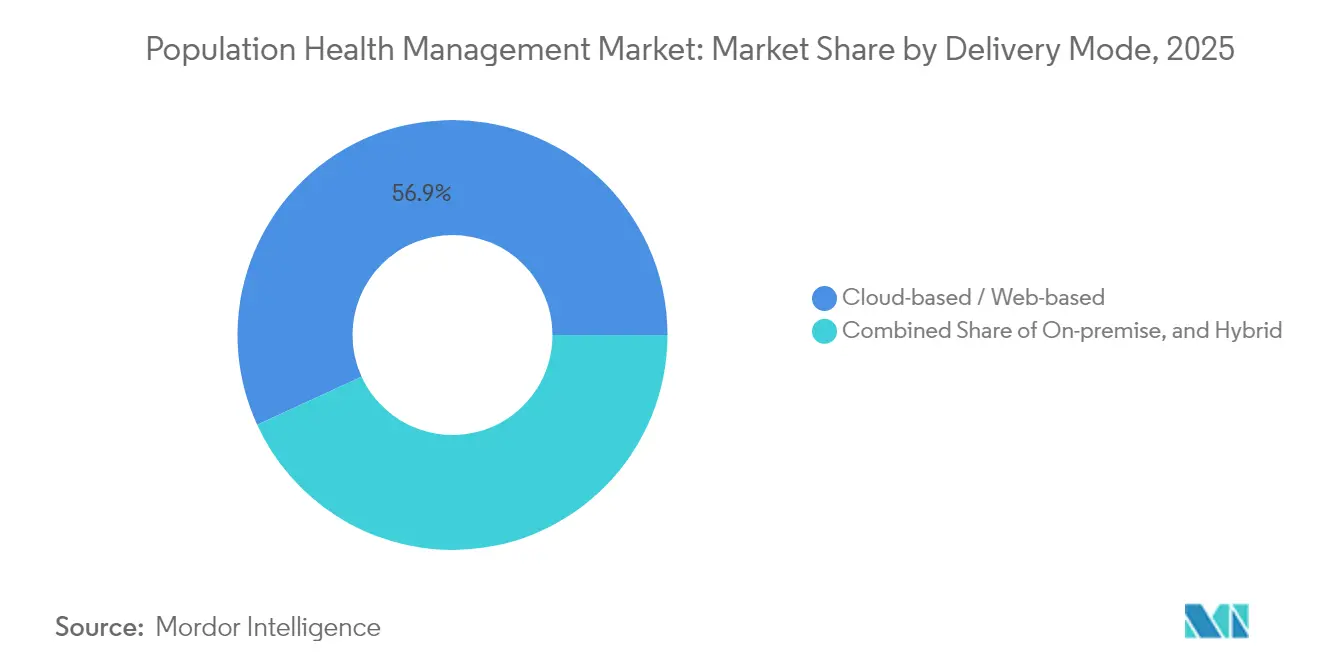

- By delivery mode, cloud deployment held 56.85% of the population health management market in 2025, yet the hybrid model is growing at a 21.74% CAGR toward 2031.

- By end user, healthcare providers accounted for 62.35% of the population health management market share in 2025; the payers segment registered the fastest 25.32% CAGR through 2031.

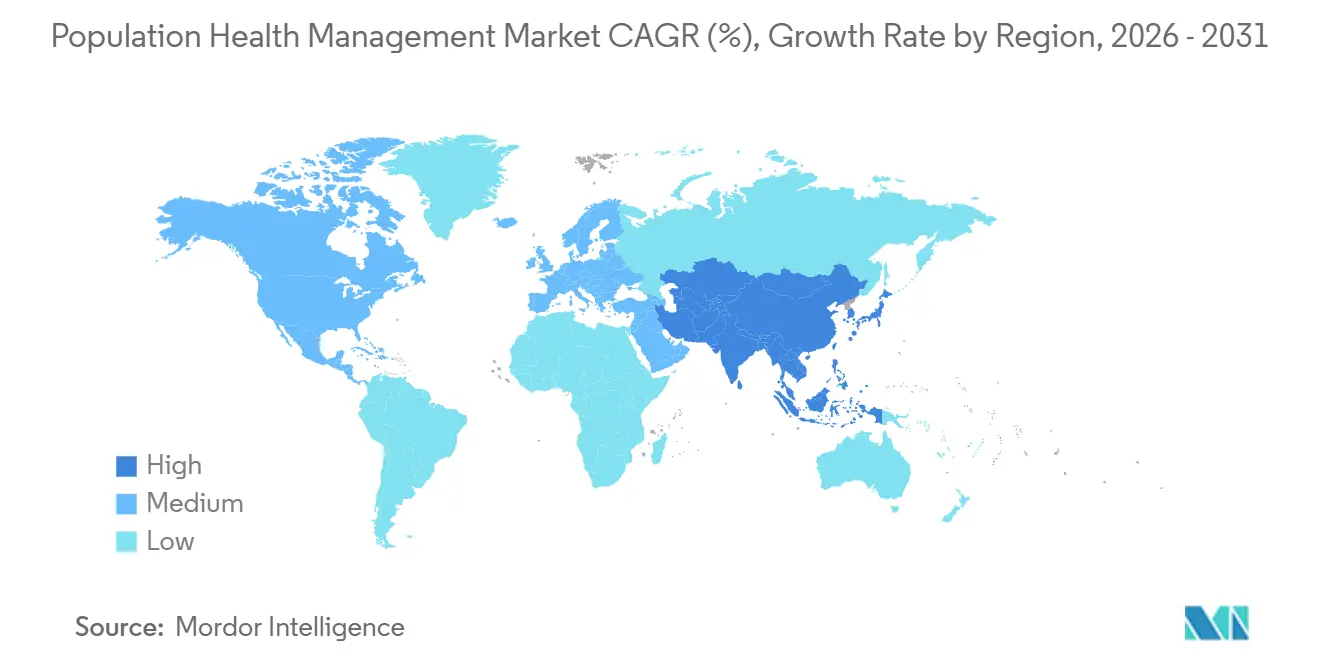

- By geography, North America captured 48.35% share in 2025. Asia-Pacific registers the fastest 18.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Population Health Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Percentage Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need for Unified Longitudinal Patient Records | +3.2% | Global, with emphasis on North America | Medium term |

| Escalating Chronic-Disease Burden | +4.1% | Global, with higher impact in developed regions | Long term |

| Public–Private Funding Surge | +2.8% | North America & Europe | Short term |

| Shift to Value-based Payment Models | +3.5% | North America, with growing influence in Europe | Medium term |

| AI-powered Predictive Analytics | +3.9% | Global, with initial concentration in developed markets | Medium term |

| Regulatory Incentives | +2.4% | North America & Europe | Short term |

| Source: Mordor Intelligence | |||

Need for Unified Longitudinal Patient Records Across Care Continuum

Healthcare organizations that create holistic patient files report 7% higher coding-gap closure and 17% more annual wellness visits, showing that integrated data directly boosts quality metrics. The practical takeaway is that a coherent record not only supports clinicians but also improves revenue capture under risk-based contracts. Because longitudinal data sets are strategic assets, organizations treat interoperability as a board-level priority rather than an IT task.

Escalating Chronic-Disease Burden Requiring Long-term Surveillance

Chronic conditions now consume 90% of healthcare spending in the United States[1]Henry Ford Health, “Rewriting the Rules of Value-Based Care,” Henry Ford Health, henryford.com. Population health platforms address this pressure by layering continuous monitoring on top of clinical workflows, cutting hospitalizations 29% in programs such as Senscio Systems' Ibis Health. Algorithm-driven alerts can normalize proactive care behaviors among patients, making continuous contact a routine expectation.

Public–Private Funding Surge in Digital Health Infrastructure

Government programs like the Medicare Shared Savings Program support 480 ACOs that cover 10.8 million beneficiaries[2]Centers for Medicare & Medicaid Services, “Fact Sheet: Calendar Year (CY) 2025 Medicare Physician Fee Schedule Proposed Rule (CMS-1807-P)-Medicare Shared Savings Program Proposals,” Centers for Medicare & Medicaid Services, cms.gov. At the same time, private equity has funneled fresh capital into interoperability and AI assets, evidenced by USD 101 million for HEALWELL AI's Orion Health acquisition. Blended public and private funding reduces project risk for health systems and enables faster experimentation with novel care models.

Shift to Value-based Payment Models Accelerating PHM Adoption

CMS proposals for 2025 introduce prepaid shared savings and equity-focused benchmarks that reward proactive outreach in underserved communities. NextGen clients already recorded USD 82 million in Medicare savings through such arrangements[3]NextGen Healthcare, “Population Health Management Solution,” NextGen Healthcare, nextgen.com. When providers assume downside risk, they treat analytics engines as mission-critical infrastructure rather than optional add-ons.

Restraints Impact Analysis*

| Restraint | (~) Percentage Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multidisciplinary Implementation Teams | -1.8% | Global, with higher impact in emerging markets | Short term |

| Reimbursement Gaps | -2.5% | Global, with varying impact based on healthcare system structure | Medium term |

| Data-privacy & Interoperability Barriers | -2.7% | Global | Medium term |

| Limited Digital Literacy | -1.6% | Emerging markets, particularly in rural areas | Long term |

| Source: Mordor Intelligence | |||

Need for Multidisciplinary Implementation Teams

Health Catalyst observes that effective deployments require combined clinical, analytics, and administrative expertise. Scarcity of data scientists and care-coordination specialists delays go-lives, nudging organizations toward managed-service models. The services segment is expected to outpace software until talent pipelines catch up.

Reimbursement Gaps for Preventive/Population-based Care

Fee-for-service remains dominant in many markets, limiting payment for preventive tasks vital to Population Health Management market success. The slow ROI on prevention forces CFOs to weigh short-term losses against future savings. Blended payment models are expected to expand as stakeholders grow comfortable with delayed financial returns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Component: Software Dominance Challenged by Services Growth

Software commands a 43.55% Population Health Management market share in 2025, delivering analytics dashboards, risk models, and quality-reporting tools core to value-based programs. These platforms support care-gap closure and regulatory submissions, anchoring many provider digital strategies. Providers often accept vendor lock-in to obtain rapid compliance updates because software licenses bundle incremental upgrades.

The services segment, however, is forecast to grow at a 19.94% CAGR from 2026-2031, overtaking hardware's contribution as organizations lean on external experts for implementation, change management, and ongoing optimization. This trend reveals that many health systems prefer to outsource complexity rather than build in-house capabilities, indirectly expanding addressable revenue for consulting partners. Hardware currently forms the smallest slice of the Population Health Management market size, yet remote monitoring devices such as glucometers and pulse oximeters are starting to shift that balance. The inference is that consumer comfort with wearables will softly enlarge the install base of clinical-grade devices, reinforcing data pipelines built by software vendors. As more physiological data streams enter analytics engines, providers can intervene earlier, reducing acute-care costs. This feedback loop creates new demand for secure network gear and edge storage, indicating hardware revenues may spike once reimbursement codes for remote monitoring mature.

Solution Type: Analytics Platforms Evolve Beyond Risk Stratification

Population Health Analytics held 31.05% market share in 2025, underpinned by platforms like Milliman's MARA that parse acute, chronic, and social drivers of risk. Shared analytics frameworks align incentives on a single version of truth, deepening payer-provider collaborations.

Patient Engagement Solutions, forecast to post a 21.48% CAGR, reflect growing awareness that activated members complete four times more health actions than inactive peers. The rising tide suggests member-facing apps will soon migrate from optional engagement add-ons to central components of risk contracts. Care Coordination and Risk-Stratification tools remain vital in the Population Health Management industry, linking multidisciplinary teams across settings. Tighter EHR integration will lower clinician screen time and subtly improve job satisfaction. Clinical Workflow Management systems—though smaller—embed population insights at the point of care, driving adherence. Uptake is likely to strengthen as frontline staff demand frictionless interfaces that mirror consumer apps.

Delivery Mode: Cloud Solutions Dominate as Hybrid Models Accelerate

Cloud deployments captured a 56.85% Population Health Management market size share in 2025, offering rapid scaling and low upfront hardware costs. Cloud services shift cybersecurity responsibilities to vendors, reducing the burden on smaller providers.

Hybrid models, predicted to expand at 21.74% CAGR, allow organizations to keep sensitive datasets on-premise while exploiting cloud analytics horsepower. This dual setup appeals to large enterprises balancing control and agility, implying hybrid adoption will spike whenever new privacy regulations emerge. On-premise installations continue among institutions with stringent data-sovereignty rules. The inference is that specialty hospitals and government facilities will sustain niche demand, ensuring vendors maintain flexible deployment options. Yet even these organizations often pilot cloud modules for non-PHI workloads, signaling a phased migration strategy rather than outright resistance.

End-User: Providers Lead While Payers Accelerate Adoption

Healthcare Providers hold a commanding 62.35% Population Health Management market share in 2025, driven by direct accountability for clinical outcomes. Integrated delivery networks use population platforms to unify inpatient, outpatient, and home-care data, illustrating that scale improves insight depth. Provider consolidation is driving demand for multi-tenant solutions that span geographies.

Payers, forecast at 19.62% CAGR, are embedding population tools to refine risk adjustment and enhance member outreach. Payer investment in member engagement will encourage providers to align communication strategies, creating a more unified patient experience. Employer coalitions and public health agencies represent smaller but influential segments. Self-insured employers drive innovation by demanding measurable ROI on workforce wellness, while governments pilot statewide platforms. If early pilots demonstrate cost savings, broader public sector rollouts may increase demand for scalable, multilingual interfaces.

Geography Analysis

North America commands a 48.35% Population Health Management market share in 2025, supported by mature EHR penetration, value-based incentives, and active M&A worth USD 69 billion in 2024. Consolidation is integrating disparate data sources and improving the predictive accuracy of regional analytics pools.

Asia-Pacific is the fastest-growing region, poised for a 18.96% CAGR through 2031. Rapid urbanization, smartphone ubiquity, and an aging population converge to create fertile ground for Population Health Management industry solutions. Cultural adaptation, such as simplified user interfaces, may be as decisive as price when attracting first-time digital health users.

Europe maintains significant momentum, spurred by an older demographic set to top 300 million adults over 60 by 2050. GDPR compliance forces vendors to bake privacy safeguards into product design, shaping global best practices. Strong privacy norms may eventually position European suppliers as preferred partners for cross-border data collaborations.

Competitive Landscape

The market shows moderate consolidation, with Oracle Health, Optum, Epic, and Allscripts shaping large-scale deals, while specialized firms like Innovaccer and ZeOmega carve out innovation niches. Optum alone deployed USD 31 billion across twelve acquisitions in two years, signaling a strategy to build end-to-end service stacks. Diversified portfolios help incumbents weather reimbursement shifts by cross-selling analytics, revenue-cycle, and telehealth modules.

Competitive differentiation now hinges on AI maturity and evidence of clinical impact. Companies showcasing reduced readmissions or verified cost savings gain faster traction because clients increasingly seek validated outcomes over promises. Transparent ROI reporting will become a trust signal, prompting vendors to publish peer-reviewed case studies.

White-space opportunities persist in integrating social determinants data, behavioral health, and pharmacy insights into unified dashboards. Early movers that can ingest non-clinical signals—such as housing stability or food access—into risk scores may unlock untapped value, especially in capitated contracts.

Population Health Management Industry Leaders

Allscripts Healthcare Solutions Inc.

Cerner Corporation

Mckesson Corporation

Health Catalyst

Optum Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Transcarent finalized its merger with Accolade, combining AI-guided WayFinding navigation with advocacy and primary-care services to serve 1,400 employer clients. The tie-up aims to streamline care journeys and lower costs.

- April 2025: MedeAnalytics, Socially Determined, and Mathematica partnered to insert social-risk factors into population analytics, helping health systems tailor interventions to community needs.

- March 2025: CoachCare purchased VitalTech, adding remote patient-monitoring devices and telehealth software that enrich chronic-care programs

- February 2025: Teladoc Health agreed to acquire Catapult Health for USD 65 million, seeking to integrate at-home diagnostic testing into its virtual-care model.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the population health management (PHM) market as the combined revenue generated by software platforms, associated implementation and analytics services, and enabling hardware that aggregate multi-source clinical, financial, and behavioral data to improve outcomes for defined patient cohorts. According to Mordor Intelligence, the market was valued at USD 63.5 billion in 2025 and is tracked across component, solution, delivery mode, end-user, and all major geographies.

Scope exclusion: stand-alone wellness apps or wearables that are not integrated into PHM workflows are outside the study.

Segmentation Overview

- By Component

- Software

- Stand-alone Software

- Integrated Software Suites

- Services

- Consulting & Training

- Implementation & Integration

- Support & Maintenance

- Hardware

- Servers & Storage

- Networking Devices

- Wearable & Remote-Monitoring Devices

- Software

- By Solution Type

- Population Health Analytics

- Patient Engagement Solutions

- Care Coordination Tools

- Risk-Stratification & Reporting Solutions

- Clinical Workflow Management

- By Delivery Mode

- On-premise

- Cloud-based / Web-based

- Hybrid

- By End-User

- Healthcare Providers

- Payers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple consultations with hospital CIOs, payer actuaries, care-management nurses, and PHM platform executives across North America, Europe, and Asia help us validate pricing ranges, refresh adoption curves, and fine-tune barrier assumptions before numbers are locked.

Desk Research

Mordor analysts begin with open datasets such as WHO Global Health Expenditure, OECD Health Statistics, and the Centers for Medicare & Medicaid Services to size national care spending, followed by adoption indicators from HIMSS, CDC chronic-disease dashboards, and peer-reviewed journals like Health Affairs. We enrich this foundation with company filings, investor decks, and reputable news feeds captured through Dow Jones Factiva and fiscal snapshots from D&B Hoovers, giving us verified vendor revenue trails. Additional insight comes from trade associations such as the American Hospital Association and the European Public Health Alliance, which clarify policy shifts that alter spending pools. This source list is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down construct converts national health-IT outlays and EHR penetration into an addressable spending pool, which is then selectively cross-checked bottom-up with sampled vendor revenues, average subscription fees, and implementation service ratios. Key variables like chronic-disease prevalence, value-based payment penetration, cloud migration rates, and per-capita health expenditure feed a multivariate regression that projects demand to 2030. Gap pockets in bottom-up inputs are bridged through median peer ratios from primary calls.

Data Validation & Update Cycle

Outputs pass a three-layer review that flags anomalies against external care-spend series and public vendor prints. Any variance above five percent triggers re-engagement with sources. Reports refresh each year, with interim updates after material regulatory or reimbursement events.

Why Mordor's Population Health Management Solutions Baseline Earns Trust

Published estimates often diverge because firms pick different revenue buckets, price progressions, and refresh cadences.

Key gap drivers include platform scope (some tally only software), inclusion of emerging regions, and whether services are priced at historical or forward ASPs. Mordor Intelligence applies one transparent scope, annual FX resets, and verified vendor filings, producing a balanced midpoint that decision-makers can lean on confidently.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 63.5 Bn (2025) | Mordor Intelligence | - |

| USD 103.63 Bn (2025) | Global Consultancy A | Adds chronic-care platforms and uses aggressive 22 % CAGR |

| USD 36.98 Bn (2024) | Industry Database B | Counts software only, excludes services and Asia Pacific |

The comparison shows that once harmonized for scope and currency, our figure sits between optimistic and conservative peers, underscoring why clients view Mordor's baseline as the most dependable launch point for strategic planning.

Key Questions Answered in the Report

How big is the Population Health Management Market?

The Population Health Management Market size is expected to reach USD 75.32 billion in 2026 and grow at a CAGR of 18.62% to reach USD 176.9 billion by 2031.

Which region holds the largest Population Health Management market share?

North America leads with roughly 48.35 % share, driven by value-based care incentives.

Why are services outpacing software in growth?

Organizations rely on external experts to manage complex implementations and close talent gaps, boosting demand for services.

Which is the fastest growing region in Population Health Management Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Page last updated on: