Accountable Care Solutions Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

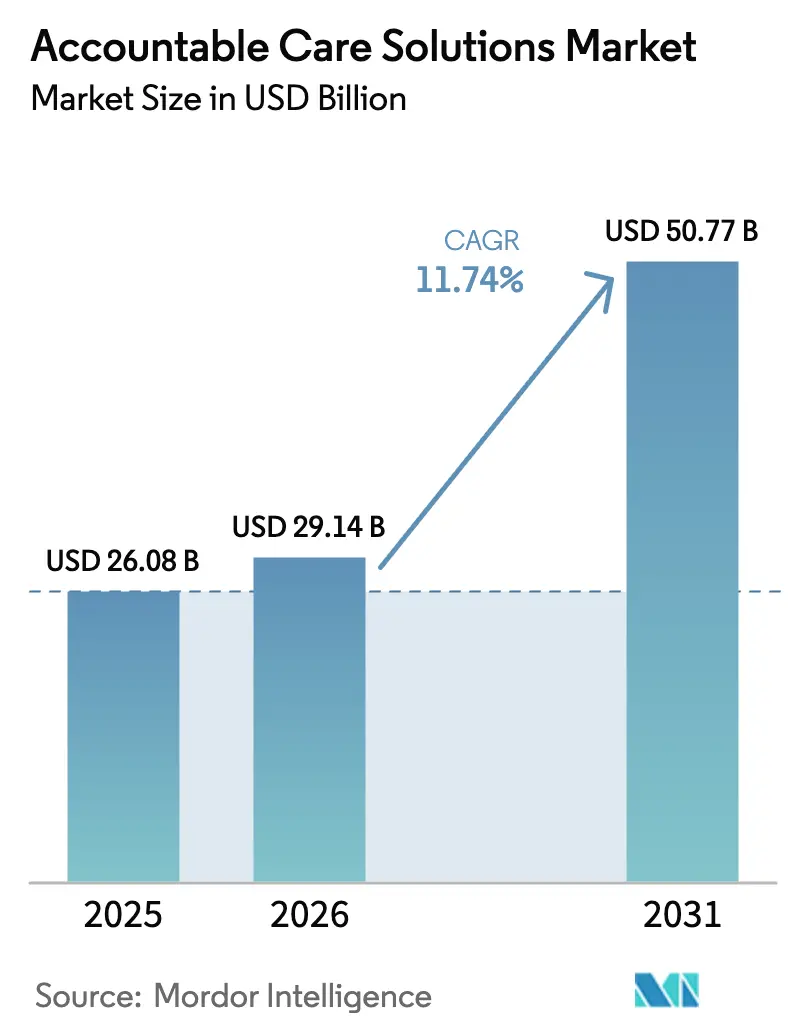

| Market Size (2026) | USD 29.14 Billion |

| Market Size (2031) | USD 50.77 Billion |

| Growth Rate (2026 - 2031) | 11.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Accountable Care Solutions Market Analysis by Mordor Intelligence

The accountable care solutions market size was valued at USD 26.08 billion in 2025 and estimated to grow from USD 29.14 billion in 2026 to reach USD 50.77 billion by 2031, at a CAGR of 11.74% during the forecast period (2026-2031). Regulatory pressure from the Centers for Medicare & Medicaid Services (CMS) to place every Traditional Medicare beneficiary in an accountable care relationship by 2030 anchors demand. Cloud-first strategies, now averaging USD 38 million in annual spending per health system, supply the scalable infrastructure needed for AI-driven analytics. Widespread deployment of healthcare big-data platforms—in which 89% of provider organizations already use artificial intelligence to simplify clinical and administrative work—further accelerates investment. As providers move from fee-for-service to value-based reimbursement, integrated platforms that coordinate clinical, financial, and population-health workflows replace isolated point solutions. Competitive momentum remains moderate because large vendors consolidate share through cloud-native platforms, yet smaller entrants still find room to differentiate on specialized analytics or regional compliance strengths.

Key Report Takeaways

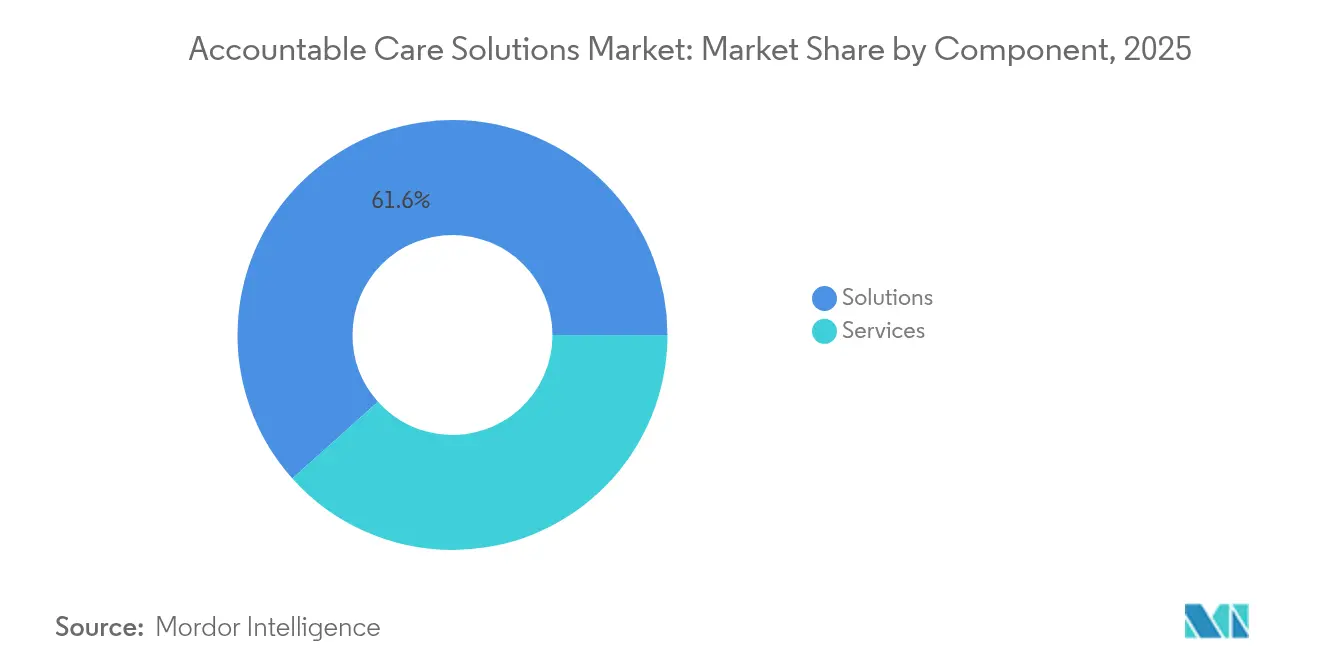

- By component, solutions led with 61.62% revenue share in 2025; services are projected to expand at a 12.76% CAGR to 2031.

- By application, electronic health records captured 28.96% of the accountable care solutions market share in 2025, while population & care management is advancing at a 13.08% CAGR through 2031.

- By deployment mode, cloud-based deployments commanded 63.35% of the accountable care solutions market size in 2025 and are forecast to grow at a 11.88% CAGR by 2031.

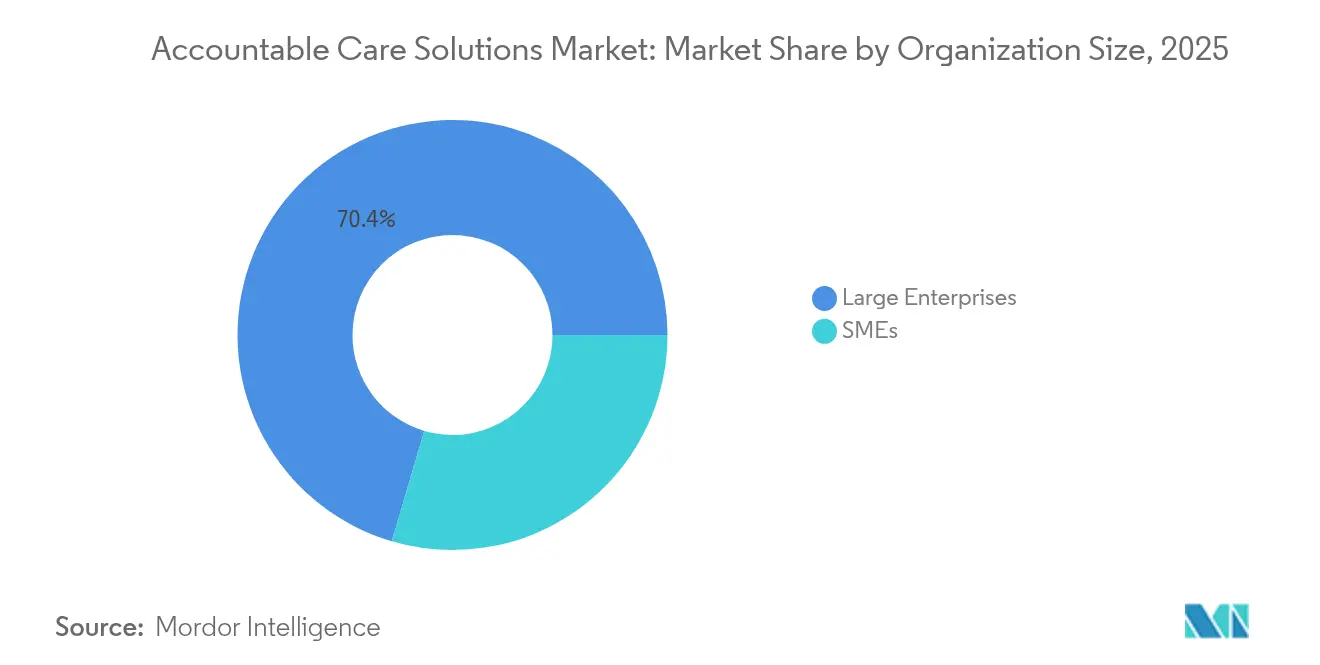

- By organization size, large enterprises held a 70.44% share of the accountable care solutions market in 2025; SMEs are expanding at a 12.31% CAGR between 2026 and 2031.

- By end-user, healthcare providers held a 60.12% share of the accountable care solutions market size in 2025, and healthcare payers are projected to grow at a 12.00% CAGR to 2031.

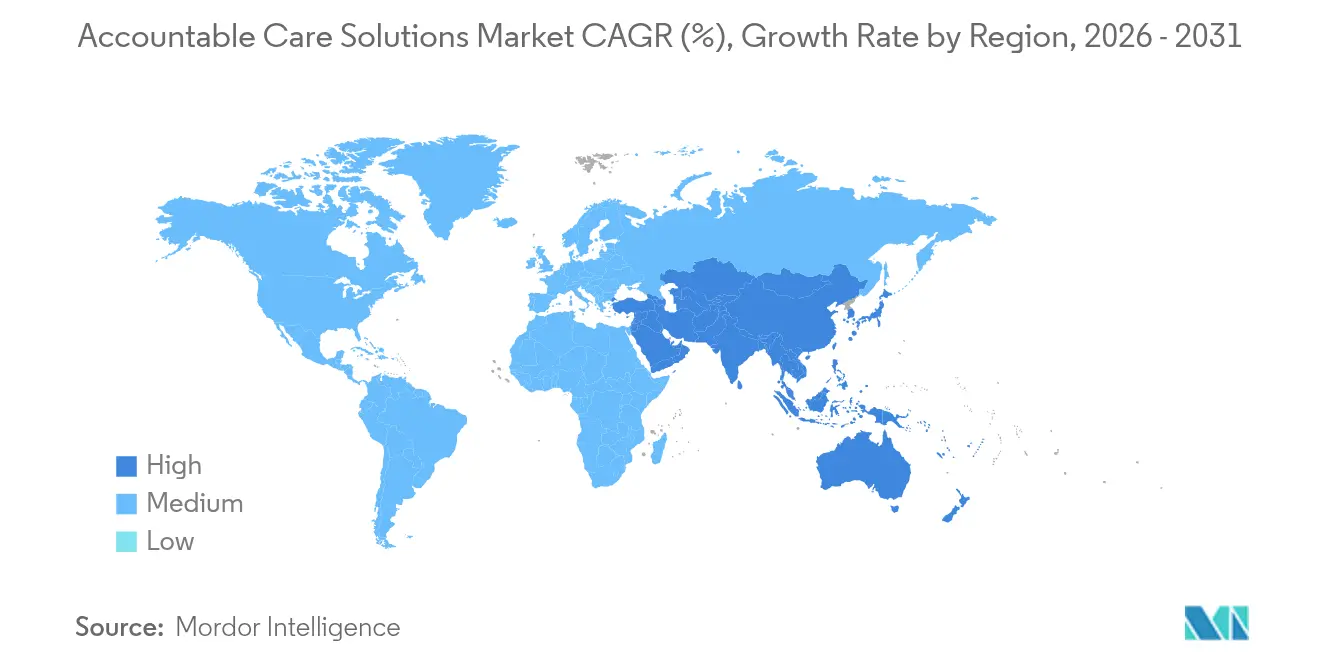

- By geography, North America led with 42.10% revenue share in 2025; Asia-Pacific is set to grow at a 12.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Accountable Care Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory value-based-care and reimbursement reforms | +3.2% | North America core, expanding to APAC & Europe | Long term (≥ 4 years) |

| Growing volumes of healthcare big-data analytics | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Need to curb escalating healthcare expenditures | +2.1% | Global | Long term (≥ 4 years) |

| Rapid migration toward scalable cloud-first IT stacks | +1.9% | Global, led by North America & APAC | Short term (≤ 2 years) |

| AI-powered social-determinants risk-stratification use cases | +1.4% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Provider-enablement venture platforms integrating tech + MSO services | +1.1% | North America core, selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory value-based-care and reimbursement reforms

CMS now counts 476 accountable care organizations (ACOs) that collectively manage care for over 11.2 million Traditional Medicare beneficiaries[1]Centers for Medicare & Medicaid Services, “CMS Moves Closer to Accountable Care Goals with 2025 ACO Initiatives,” cms.gov, underscoring a clear shift to outcome-linked payment. New programs such as the ACO Primary Care Flex Model provide upfront investment for primary-care modernization in underserved communities. Commercial insurers and Medicaid programs replicate these models, broadening the accountable care solutions market beyond Medicare. The ACO REACH framework adds equity mandates alongside cost controls, signaling a mature stage for value-based care. Providers that cling to fee-for-service see shrinking margins as reimbursement pivots toward shared savings and capitated payments.

Growing volumes of healthcare big-data analytics

A large percent of hospitals[2]Jordan Everson, “Current Use And Evaluation Of Artificial Intelligence And Predictive Models In US Hospitals,” Health Affairs, healthaffairs.org already rely on predictive models to inform clinical decisions, and healthcare AI funding climbed to USD 11 billion in 2024 with most capital aimed at administrative automation. Modern analytics platforms ingest claims, clinical, and social-determinant data to forecast risk and close care gaps in near real time. For accountable entities, earlier identification of high-risk patients trims avoidable admissions, improving both quality scores and shared-savings potential. As datasets grow richer, real-time dashboards help clinicians prioritize outreach, reinforcing the value proposition of integrated platforms within the accountable care solutions market.

Need to curb escalating healthcare expenditures

Automation could cut USD 200 billion–USD 360 billion in healthcare spending by streamlining administrative tasks, according to industry estimates. Seventy-four percent of hospital chief financial officers have adopted automated revenue-cycle workflows to offset labor shortages and uncompensated care pressures. Predictive denials management and centralized referral systems reduce leakage and unnecessary tests. For organizations in shared-savings contracts, avoiding high-cost acute events is essential, making accountable care platforms a frontline tool in cost-containment strategies.

Rapid migration toward scalable cloud-first IT stacks

Seventy-two percent of provider executives report positive results from cloud migration, citing superior performance for AI models and easier interoperability. Real-time image analysis on cloud infrastructure has cut radiology read times by 40% in early deployments. Smaller hospitals gain access to enterprise-grade analytics without large capital budgets, supporting faster uptake of accountable care solutions among SMEs. Multicloud-by-design strategies help providers match workloads to optimal environments while maintaining compliance with HIPAA and regional data-sovereignty rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cyber-security vulnerabilities | -1.8% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| High CAPEX/OPEX for legacy-to-digital transformation | -1.3% | Global, pronounced in established markets | Medium term (2-4 years) |

| Fragmented interoperability across disparate systems | -1.1% | Global, severe in North America & Europe | Medium term (2-4 years) |

| Clinician burnout due to EHR workload & alert-fatigue | -0.9% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-privacy & cyber-security vulnerabilities

Healthcare experienced 677 large-scale breaches in 2024, exposing records of 182.4 million people and raising hesitation around expansive cloud deployments. The Change Healthcare ransomware incident alone affected more than 100 million patients and highlighted systemic risk across interconnected platforms. Average breach costs reached USD 4.88 million, amplifying liability concerns. Regulators responded by finalizing new interoperability and cybersecurity standards that impose penalties for lax security, forcing vendors to fortify defenses.

High CAPEX/OPEX for legacy-to-digital transformation

Three-quarters of health-system executives admit current budgets fall short of full digital transformation needs despite listing it as a priority. Integrating modern care coordination modules with entrenched EHRs demands workflow redesign, staff retraining, and dual-system maintenance. Nearly half of clinicians still cannot seamlessly access outside patient data, underscoring additional integration costs. The drawn-out transition strains operating margins, yet remains unavoidable for organizations seeking to thrive in the accountable care solutions market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform consolidation drives solutions dominance

Solutions generated 61.62% of 2025 revenue, showing that organizations favor unified platforms linking clinical, financial, and population-health functions. Services will outpace software with a 12.76% CAGR because expert training, workflow redesign, and ongoing optimization are indispensable once platforms go live. The accountable care solutions market size for services is projected to widen as ACOs seek external help to fine-tune risk-adjustment algorithms and regulatory reporting. Epic Systems’ addition of 176 facilities in 2024 illustrates a consolidation wave toward comprehensive platforms.

Services growth reflects recognition that software alone cannot deliver outcomes without sustained change management. Health systems contract for analytics-as-a-service, virtual command centers, and managed population-health operations. These arrangements keep capital budgets lean and shift accountability for performance metrics to solution partners, reinforcing the trajectory of the accountable care solutions market

By Application: Population management takes the lead

Electronic health records hold 28.96% of 2025 revenue, anchoring data capture for every downstream workflow. Yet population & care management will rise at a 13.08% CAGR to 2031, becoming the primary engine of the accountable care solutions market. Kaiser Permanente’s decision to deploy Innovaccer’s population-health platform across California underscores this pivot toward proactive coordination.

Analytics, revenue-cycle automation, and patient-engagement modules also gain momentum as organizations prioritize end-to-end visibility into risk and resource use. AI-based revenue-cycle tools are already live in a large number of hospitals, streamlining pre-authorization and reducing denials. These interconnected applications cement EHRs as a foundation but push new spending toward high-impact population-health workflows that drive value-based reimbursement success within the accountable care solutions market.

By Deployment Mode: Cloud adoption accelerates

Cloud-based options controlled 63.35% of 2025 spending, and the segment will expand at a 11.88% CAGR as AI models demand scalable compute resources. The accountable care solutions market share for cloud platforms is set to widen because compliance features, once perceived as a weakness, now meet or exceed on-premise security standards. On-premise deployments persist in a minority of institutions with immutable data-sovereignty mandates, while hybrid architectures permit sensitive workloads to remain on site.

Providers moving to multicloud-by-design reduce vendor lock-in and right-size capacity for imaging, claims, or real-time alerting. Early adopters report tangible gains: AI-enhanced imaging workflows cut reading times and reduced re-scans, illustrating how cloud deployment translates into operational efficiencies that strengthen business cases for further investment in the accountable care solutions market.

By Organization Size: SMEs narrow the digital divide

Large enterprises contributed 70.44% of 2025 revenue, but SMEs will record the faster 12.31% CAGR as subscription-based models erase historic barriers. Cloud delivery removes the need for data-center buildouts, letting regional hospitals and physician groups adopt sophisticated tools at predictable costs. The accountable care solutions market size allocated to SMEs rises as payer contracts increasingly include smaller provider networks in shared-savings arrangements.

For SMEs, preconfigured analytics dashboards, low-code care-management workflows, and vendor-managed cybersecurity enable rapid time-to-value. Large health systems continue to invest in bespoke integrations spanning acute, post-acute, and virtual-care settings. Over time, convergence in functional capabilities narrows the performance gap, promoting more uniform adoption of accountable care principles across the healthcare landscape.

By End-User: Payers intensify platform spending

Healthcare providers still dominate with 60.12% of 2025 sales, reflecting their frontline care-delivery role. Payers, however, will accelerate at 12.00% CAGR as they shoulder greater responsibility for population health, especially in Medicare Advantage and Medicaid managed-care lines. Optum’s analytics-heavy offerings and Transcarent’s January 2025 acquisition of Accolade for USD 621 million highlight payer moves into integrated navigation and care-coordination.

Payer platforms now ingest multi-payer claims, benefit data, and social-risk indicators to coordinate directly with provider partners, a capability essential for downside-risk contracts. For the accountable care solutions market, this trend expands total addressable spend and pushes vendors to create features that satisfy both clinical and actuarial requirements.

Geography Analysis

North America generated 42.10% of global revenue in 2025, supported by CMS rules that already place 53.4% of Traditional Medicare members under accountable care contracts. Regional growth of 10.82% CAGR through 2031 represents a shift from initial build-out to optimization. Cloud migration, AI-embedded population health, and equity-focused models such as ACO REACH drive refresh cycles of existing platforms. Large systems like Highmark Health now link Epic and Google Cloud for administrative and clinical analytics, demonstrating ecosystem-level collaboration.

Asia-Pacific is the fastest-growing territory at 12.34% CAGR, propelled by national digital-health blueprints and startup funding. Southeast Asia alone projects USD 6.1 billion in digital-health revenue for 2024, aided by Indonesia’s Halodoc closing a USD 100 million round. Governments in Thailand, Australia, and Singapore inject capital into AI, telemedicine, and IoT monitoring, creating fertile ground for vendors that localize solutions to diverse regulatory settings. Cloud flexibility is critical because data sovereignty rules vary widely across the region.

Europe expands at 11.33% CAGR as integrated-care mandates and GDPR compliance shape procurement criteria. Germany’s national cloud strategy for healthcare shows how public-sector guidance accelerates adoption while setting strict data-sovereignty bars. Meanwhile, the Middle East & Africa advance at 11.90% CAGR, reflecting sovereign investments in hospital digitization and national health-information exchanges. South America grows at 11.59% CAGR as countries modernize insurance schemes and subsidize telehealth, using accountable care principles to manage chronic-disease burdens. The geographic spread proves that, while regulatory frameworks differ, the accountable care solutions market meets a common goal: better outcomes at lower cost.

Competitive Landscape

The accountable care solutions market is moderately concentrated. Epic Systems widened its lead in 2024 by winning 176 additional hospitals as Oracle Health ceded 74 sites, signaling provider preference for deeply integrated platforms. UnitedHealth Group scales analytics through Optum but now faces increased antitrust and cybersecurity scrutiny after high-profile breaches.

IBM, Oracle, Innovaccer, Allscripts, and point-solution specialists compete on AI performance, user-experience simplicity, and interoperability standards. Incumbents bundle care-management, risk-adjustment, and revenue-cycle modules into unified suites, locking in long-term clients. Disruptors target niches such as social-determinants analytics or small-provider enablement, often leveraging cloud marketplaces for rapid distribution.

Strategic partnerships abound: AI companies integrate with EHR vendors, and payers invest directly in platform developers to customize features for shared-risk contracts. Success metrics increasingly center on measurable shared savings, hospital readmission rates, and patient engagement scores—quantitative proof that platforms deliver value in the accountable care solutions market.

Accountable Care Solutions Industry Leaders

CVS Health Corporation

Epic Systems Corporation

Oracle Corporation

UnitedHealth Group

Veradigm, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CMS updated the ACO REACH Model for Performance Year 2026, raising the Quality Withhold to 5% and adjusting risk-score growth limits, reinforcing sustainability goals for value-based care.

- January 2025: Transcarent acquired Accolade for USD 621 million to merge AI-driven navigation and care-coordination features under one platform.

- January 2025: CMS introduced the ACO Primary Care Flex Model, a five-year program that tests prospective payments and incentives to attract more participants to the Shared Savings Program.

- December 2024: The U.S. Department of Health and Human Services finalized HTI-2 and HTI-3 rules, setting governance for TEFCA and expanding information-blocking exceptions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the accountable care solutions market as every software platform, analytics module, and related service that helps providers and payers coordinate value-based care, share risk, manage population health, and measure outcomes across integrated networks.

Scope Exclusion: Stand-alone wellness or fitness apps that operate outside an accountable care organization are not considered.

Segmentation Overview

- By Component

- Solutions

- Services

- By Application

- Electronic Health Records

- Healthcare Analytics

- Population & Care Management

- Revenue Cycle & Claims Management

- Payment & Risk Adjustment

- Health Information Exchange (HIE)

- Patient Engagement & Portals

- Other Applications

- By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

- By Organization Size

- Large Enterprises

- SMEs

- By End-User

- Healthcare Providers

- Healthcare Payers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team conducted interviews with ACO medical directors, payer IT leads, cloud-hosting partners, and regional policy advisors in North America, Europe, and Asia-Pacific. These conversations verified market definitions, refined average selling prices, and filled data gaps that public datasets could not resolve.

Desk Research

We began by reviewing high-credibility, open sources such as Centers for Medicare & Medicaid Services cost reports, ONC interoperability scorecards, OECD health-spending tables, and analyses issued by the American Hospital Association and Healthcare Information Management Systems Society. Company filings, investor decks, and peer-reviewed journals added product-level detail.

To deepen the evidence base, Mordor analysts accessed D&B Hoovers for vendor financials, Dow Jones Factiva for transaction news, Marklines for payer-provider technology links, and Questel for patent flows. The sources named here are illustrative; many additional documents supported data collection, cross-checks, and clarification.

Market-Sizing & Forecasting

The model starts with a top-down split of national health-expenditure pools into value-based reimbursement streams, followed by adoption ratios for EHR, analytics, PHM, RCM, and HIE modules. Supplier revenue roll-ups and sampled ASP × install counts provide bottom-up anchors that adjust totals where variances exceed tolerance bands. Key inputs include CMS Shared-Savings enrolment, cloud deployment penetration, median subscription pricing shifts, chronic-disease prevalence, and regional regulatory milestones. A multivariate regression with scenario analysis projects values to 2030, while gap areas in bottom-up estimates are bridged with verified channel checks.

Data Validation & Update Cycle

Outputs pass analyst peer review, variance checks against independent benchmarks, and senior sign-off. Reports refresh each year, with interim revisions triggered by material events. A final data sweep is completed before client delivery.

Why Mordor's Accountable Care Solutions Baseline Commands Reliability

Published market values often vary; differences in scope, input variables, and refresh cadence create visible gaps. By anchoring revenue only to solutions directly enabling accountable care contracts and by updating models annually, Mordor reduces these discrepancies.

Key Gap Drivers include: some publishers omit services revenue, others hold ASPs constant across the horizon, and a few blend broader care-management tools that inflate totals. Currency translation years and cloud-adoption assumptions also shift figures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.08 B (2025) | Mordor Intelligence | - |

| USD 25.7 B (2024) | Regional Consultancy A | Services revenue excluded; relies on 2023 vendor press releases |

| USD 24.95 B (2024) | Trade Journal B | Uses flat ASP; limited primary validation |

| USD 28.60 B (2025) | Global Consultancy C | Includes general care-management tools and assumes rapid cloud saturation |

The comparison shows that Mordor's disciplined scope selection, mixed-method modelling, and annual refresh deliver a balanced, transparent baseline clients can trace to clear variables and repeat with confidence.

Key Questions Answered in the Report

What regulatory factor is most compelling providers to adopt accountable care solutions?

CMS policies that tie reimbursement to patient outcomes are driving providers toward platforms that coordinate care and document quality performance.

How do cloud-native deployments change the implementation strategy for accountable care platforms?

Cloud delivery supplies on-demand computing for AI workloads and reduces capital spending on data centers, making advanced functionality accessible to organizations of all sizes.

Why are health insurers stepping up investment in accountable care technology?

Payers leverage these platforms to collaborate with provider networks, manage downside-risk contracts, and embed member engagement tools that improve care continuity.

What integration hurdle most often delays digital transformation projects in healthcare?

Aligning new care-coordination modules with entrenched EHR workflows requires significant change-management and staff retraining efforts.

How does big-data analytics strengthen population health programs?

Predictive algorithms surface high-risk patients sooner, enabling care teams to intervene before conditions escalate into costly acute events.

Which cybersecurity concern weighs heaviest on cloud adoption decisions?

The rise of sophisticated ransomware attacks has heightened demand for vendors that offer real-time threat monitoring and stringent data-protection protocols.

Page last updated on: