Long Term Care Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.13 Billion |

| Market Size (2031) | USD 9.49 Billion |

| Growth Rate (2026 - 2031) | 9.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

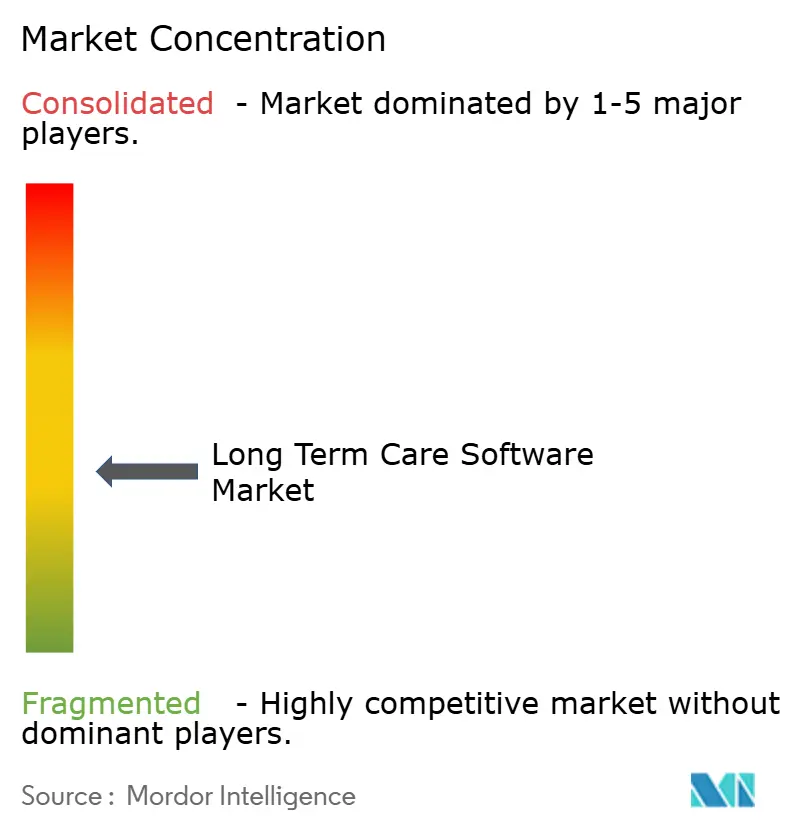

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Long Term Care Software Market Analysis by Mordor Intelligence

The long term care software market size is expected to grow from USD 5.62 billion in 2025 to USD 6.13 billion in 2026 and is forecast to reach USD 9.49 billion by 2031 at 9.13% CAGR over 2026-2031. Cloud-based interoperability mandates, workforce shortages, and value-based reimbursement models collectively reshape vendor strategies as facilities prioritize scalable, compliance-ready platforms. Consolidating operators seek enterprise-grade functionality that supports admissions through discharge, while smaller facilities favor subscription pricing that mitigates capital outlays. Analytics capabilities emerge as the leading purchase criterion because predictive insights directly influence reimbursement and quality scores. Competitive intensity increases as vendors embed artificial intelligence, mobile access, and cybersecurity safeguards to satisfy both regulatory scrutiny and clinical workflow needs.

Key Report Takeaways

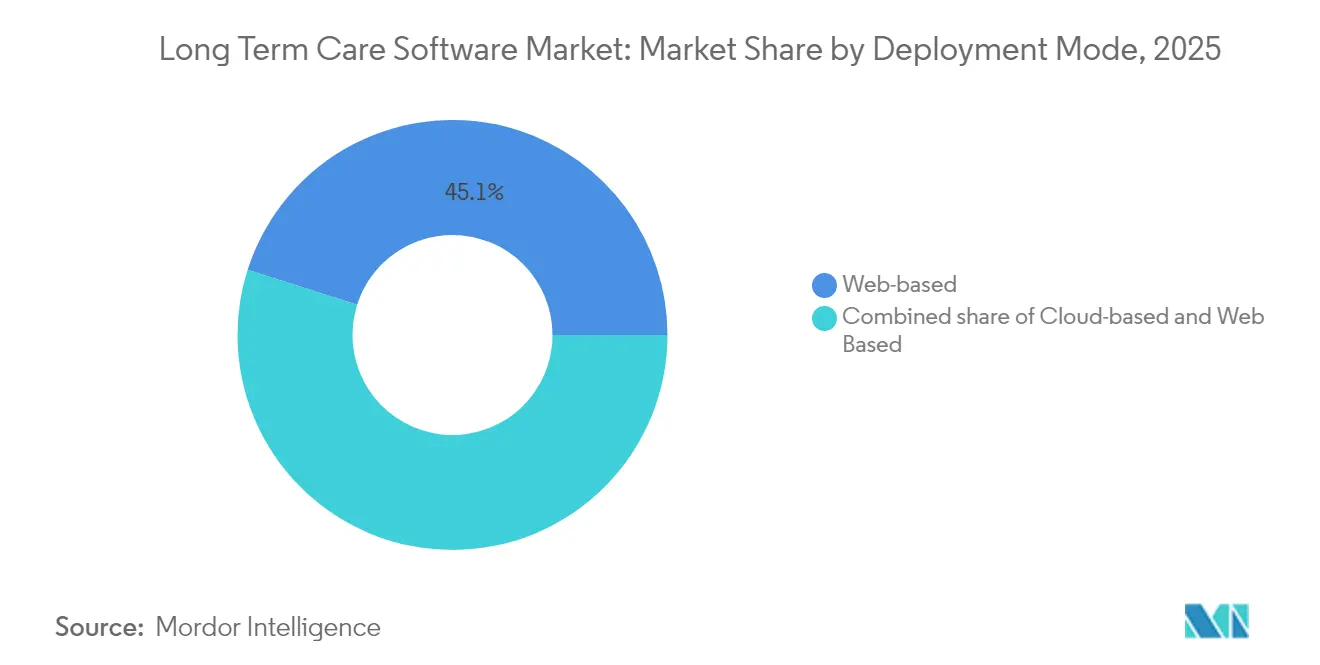

- By deployment model, web-based solutions led with 45.10% of long term care software market share in 2025, whereas cloud-based platforms are forecast to grow at a 9.41% CAGR through 2031.

- By product module, Electronic Health Records accounted for 37.80% of the long term care software market size in 2025, while Analytics & Business Intelligence modules are expanding at a 9.88% CAGR to 2031.

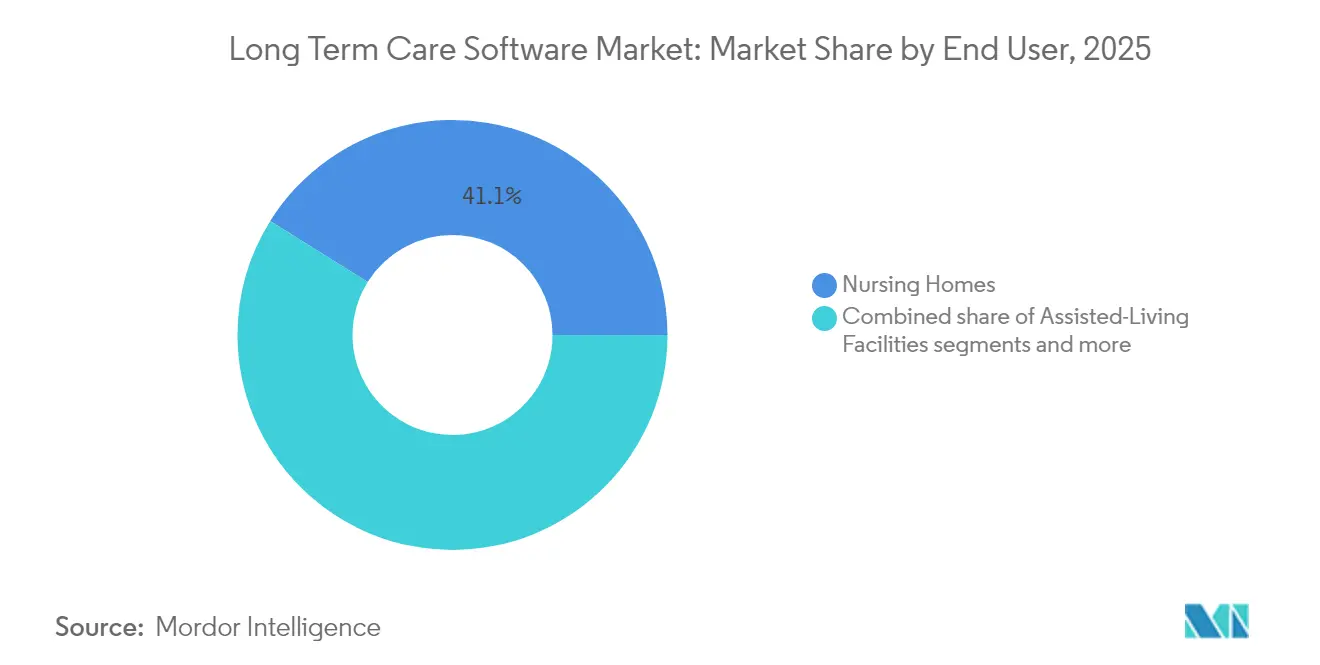

- By end-user facility type, nursing homes held 41.10% revenue share of the long term care software market in 2025; assisted-living facilities are projected to record the fastest CAGR at 10.44% through 2031.

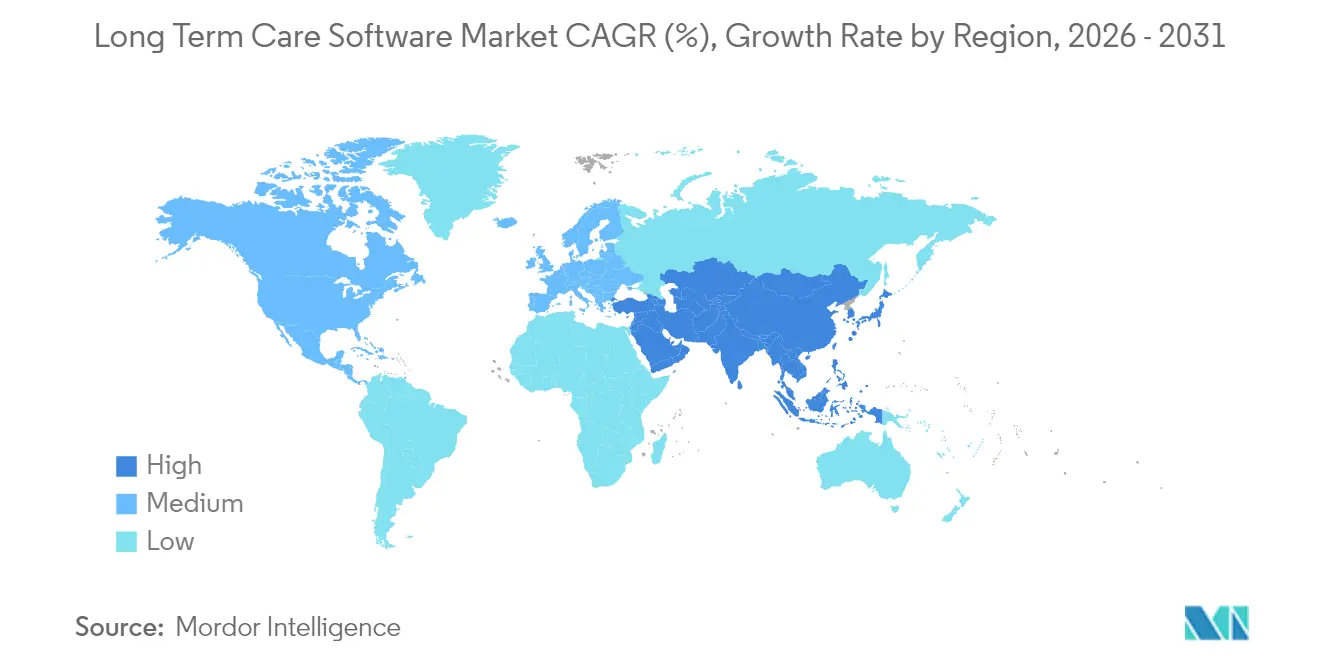

- By geography, North America commanded 41.80% of long term care software market share in 2025, whereas Asia-Pacific is anticipated to register the highest CAGR at 9.74% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Long Term Care Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population & chronic-disease burden | +2.1% | Global, highest in Japan, Germany, United States | Long term (≥ 4 years) |

| Government incentives for post-acute EHR interoperability | +1.8% | North America, Europe | Medium term (2-4 years) |

| Shift to cloud-based SaaS lowering IT barriers | +1.4% | Global, strongest in APAC emerging markets | Short term (≤ 2 years) |

| Value-based reimbursement models demanding analytics | +1.2% | North America core, expanding to Europe | Medium term (2-4 years) |

| AI-driven fall/readmission risk prediction | +0.9% | United States, Western Europe, Australia | Short term (≤ 2 years) |

| Workforce shortages accelerating mobile workflow adoption | +1.1% | Global, acute in United States and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Chronic-Disease Burden

Long-term care demand magnifies as older cohorts expand and comorbidities rise, forcing facilities to adopt software that unites documentation, predictive analytics, and remote monitoring. Brazil’s older-adult population is set to triple by 2050, and government technology grants already fund IoT-enabled monitoring pilots to sustain independent living[1]Source: AARP International, “Brazil,” aarp.org . Germany anticipates a nursing shortfall exceeding 1.9 million professionals by 2040, making technology-assisted workflows indispensable for maintaining care standards without proportional head-count growth. Facilities worldwide deploy fall-detection sensors, wearables, and AI triage tools that escalate alerts directly into Electronic Health Records, improving response times while reducing liability exposure. Regulatory frameworks such as HIPAA in the United States and GDPR in Europe require secure, interoperable systems, making the long term care software market a critical enabler of safe, compliant care management. Sustained demographic momentum underpins multi-year investment cycles and discourages deferral of software upgrades.

Government Incentives for Post-Acute EHR Interoperability

The HTI-1 final rule obliges long-term care facilities to implement certified health IT modules supporting USCDI v3 by January 2026, converting compliance pressure into capex prioritization. Information-blocking penalties accelerate platform replacement among operators reliant on closed systems. TEFCA’s trusted exchange framework broadens data-sharing incentives, favoring vendors with robust APIs and single-tenant security architectures. CMS quality initiatives reward demonstrable interoperability, making EHR adoption a direct revenue driver rather than an administrative chore. State Medicaid adjustments further stimulate purchases by boosting reimbursement for certified technology users, especially among high-Medicaid nursing homes confronting razor-thin margins.

Shift to Cloud-Based SaaS Lowering IT Barriers

Subscription-based deployment compresses upfront costs and provides automatic updates, allowing facilities without dedicated IT staff to maintain regulatory compliance. Capital requirements for on-premises platforms can exceed USD 600,000, but multi-tenant SaaS pricing typically averages USD 1,200 per user annually, equalizing access between rural homes and large chains. Cloud data centers deliver encryption, redundancy, and SOC 2 certification, alleviating cybersecurity fears while enabling real-time analytics. Interoperability is simplified through FHIR-enabled endpoints, catalyzing cross-continuum data flows that reduce readmission penalties. The long term care software market thus finds new addressable demand among operators that historically considered enterprise systems unreachable.

Value-Based Reimbursement Models Demanding Analytics

CMS ties Skilled Nursing Facility reimbursements to quality metrics such as rehospitalization rates and infection prevention, placing predictive analytics at the core of fiscal strategy. PDPM heightens the need for acuity-driven resource planning, and real-time dashboards now influence shift staffing, therapy minutes, and supply allocation. Managed Medicaid and commercial risk contracts impose financial bonuses and penalties linked to measured outcomes, making analytic functionality an essential procurement criterion. Facilities that leverage forecasting engines for high-risk resident identification report measurable gains in Five-Star Quality Ratings and reduced antipsychotic medication usage. The long term care software market thereby becomes integral to sustaining margins under value-based payment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & data-privacy concerns | -1.3% | Global, heightened in Europe (GDPR), North America (HIPAA) | Short term (≤ 2 years) |

| High implementation & maintenance cost for smaller operators | -0.8% | Global, acute in rural and developing markets | Medium term (2-4 years) |

| Fragmented state-level regulations raising integration complexity | -0.7% | North America core, emerging in federated systems globally | Medium term (2-4 years) |

| Limited interoperability standards versus acute-care EHRs | -0.6% | Global, most acute in developing healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security & Data-Privacy Concerns

Healthcare ransomware events grew in 2024, and long-term care organizations now face average breach costs surpassing USD 10 million, including penalties and brand erosion. NIST’s 2024 guide sets stricter encryption and audit-log standards, raising integration complexity for older web-based applications. GDPR provisions on cross-border data transfers add legal uncertainty for multinational chains. Smaller facilities lacking full-time security personnel often postpone upgrades despite SaaS improvements, leaving legacy systems exposed. The resulting risk aversion tempers near-term long term care software market adoption until vendors demonstrate turnkey compliance tooling.

High Implementation & Maintenance Cost for Smaller Operators

Basic EHR projects can still require USD 20,000-65,000 in direct spend and another USD 25,000 in staff training, a heavy burden for facilities operating on 2% margins. Ongoing support averages 18% of purchase price annually, pressuring cash flows during census dips. Rural operators pay higher broadband fees and endure latency that hampers cloud reliability. Multi-module platforms demand integration expertise often outsourced to consultants, increasing total cost of ownership. Many independents therefore delay system replacement, reinforcing fragmentation within the long term care software market and creating acquisition targets for larger chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Transformation

The long term care software market size for web-based deployments stood at USD 2.53 billion in 2025, representing 45.10% share of total revenue. Cloud platforms, however, are forecast to expand at a 9.41% CAGR, elevating the long term care software market share of SaaS offerings by the end of the decade. Operators migrate to cloud to reduce upgrade downtime, access AI modules, and centralize multi-facility reporting. PointClickCare’s Azure migration and WellSky’s partnership with Google Cloud showcase how hyperscale resources accelerate feature rollouts. Hybrid deployments persist among enterprise chains that segregate protected health information servers while leveraging cloud analytics for de-identified data sets. Over the forecast horizon, vendor roadmaps prioritize containerized microservices, ensuring feature parity across deployment options and smoothing transition pathways for bandwidth-limited sites.

Cloud dominance reshapes vendor economics by replacing perpetual licenses with recurring monthly revenue, improving predictability yet intensifying churn risk. Smaller suppliers unable to finance cloud redevelopment become acquisition candidates, accelerating consolidation. Facilities cite mobile accessibility and automatic security patching as top benefits, while remaining skeptics worry about internet outages and data-sovereignty rules. Market education campaigns from public cloud providers and regional broadband expansion programs alleviate many lingering objections, reinforcing the trajectory toward SaaS penetration.

By Product Module: Analytics Emergence Reshapes Priorities

Electronic Health Records retained a 37.80% revenue contribution to the long term care software market size in 2025 because compliance documentation remains the first prerequisite for licensure. Analytics & Business Intelligence modules are projected to account for USD 2.27 billion by 2031, reflecting a 9.88% CAGR. Facilities increasingly bundle fall-prediction engines and readmission risk scores into care pathways, triggering earlier interventions and limiting penalty exposure. eMAR adoption accelerates as medication error prevention tools integrate barcode scanning and predictive drug-interaction alerts. Revenue-cycle modules embed payer-latest rulesets to ensure PDPM accuracy, and many vendors now offer optional clearinghouse connections for instant claim edits.

AI-powered workforce scheduling platforms such as Kevala report 8% labor-cost reduction by matching staffing levels to acuity forecasts. Bundled procurement rises because chains prefer single-vendor suites that harmonize data models across clinical, financial, and operational domains. Open-API ecosystems retain relevance for specialized functions like lease asset tracking or advanced wound-care imaging, but interoperable vendors increasingly swallow niche markets through organic module launches and bolt-on deals.

By End-User Facility Type: Assisted Living Accelerates Growth

Nursing homes and skilled-nursing facilities generated USD 2.31 billion in software spend during 2025, equating to 41.10% of the aggregated long term care software market size. Assisted-living communities, however, are advancing at a 10.44% CAGR thanks to aging-in-place preferences and higher resident acuity. These sites demand hybrid care-hospitality platforms that unify health records, lifestyle scheduling, and resident engagement apps. Mobile POS devices now facilitate dining-room medication administration, enhancing compliance without medicalizing the environment.

Home-health and hospice agencies adopt cloud tools optimized for distributed workforces, integrating telehealth feeds, wound-image uploads, and GPS-verified visit logs. Regulatory complexity varies: U.S. nursing homes adhere to both CMS surveys and state mandates, while assisted-living rules differ considerably by jurisdiction, influencing procurement cycles. As payer networks extend bundled-payment pilots that encompass post-acute settings, cross-continuum data visibility becomes indispensable, steering all facility types toward comprehensive suites.

Geography Analysis

North America captured 41.80% share of the long term care software market in 2025, anchored by Medicare and Medicaid incentives that reward certified EHR use. The January 2026 HTI-1 deadline accelerates refresh cycles, and information-blocking enforcement drives multi-state chains to harmonize on API-first platforms. Labor shortages propel adoption of virtual-nursing dashboards; 74% of hospital leaders now view remote monitoring as integral to future care delivery. Canada prioritizes operational efficiency over reimbursement optimization, whereas Mexico’s mid-income segment expands private long-term care demand, stimulating vendor localization efforts.

Asia-Pacific is projected to record a 9.74% CAGR, the fastest among major regions. Japan’s health ministry subsidizes sensor-equipped beds and robotic lifts to mitigate the projected 570,000 caregiver deficit by 2040. China’s long-term care facilities report an average nursing-service need score of 162.15, translating into rising software budgets for resident assessment and staffing tools. Australia’s digital-health strategy targets full electronic medication chart coverage by 2027, further enlarging the long term care software market.

Europe demonstrates sustained investor confidence, with EUR 2.3 billion in nursing-home property transactions during 2024. GDPR imposes strict data-processing rules that slow cross-border deployments, yet standardization efforts spur vendors to develop configurable consent-management modules. Germany’s hospital-funding reform boosts digital infrastructure grants, and France’s Ma Santé strategy earmarks funding for interoperable post-acute solutions. Switzerland’s trend toward home-based care intensifies demand for cost-effective SaaS.

Emerging regions such as South America and the Middle East & Africa exhibit double-digit growth potential but face currency volatility and infrastructure gaps. Vendors often partner with telecom operators to bundle connectivity and hosting, reducing hurdles for early adopters.

Competitive Landscape

The long term care software market remains moderately fragmented; the top five vendors controlled close to 35% revenue in 2024, yet M&A activity is rising as larger players pursue portfolio breadth. PointClickCare’s acquisition of American HealthTech extended its footprint across skilled-nursing, assisted-living, and critical-access hospital segments. WellSky invested in generative-AI documentation tools co-developed with Google Cloud, underscoring the strategic imperative to automate charting and free clinical time. MatrixCare partnered with Health Gorilla to unlock nationwide exchange via TEFCA-aligned networks, positioning itself as an interoperability frontrunner.

Private-equity involvement intensifies: Nordic Capital’s majority stake in Sensio adds smart-sensor capabilities that complement analytics suites. Valsoft’s acquisition of American Data shows investor appetite for niche vendors with loyal customer bases. Disruptors such as Kevala leverage AI scheduling agents to win share among staffing-constrained facilities. Differentiation now hinges on total cost of ownership, security posture, and the depth of predictive analytics; features alone no longer secure contracts.

Cybersecurity capabilities influence RFP outcomes as facilities scrutinize SOC 2 reports and incident-response playbooks. Vendors offering end-to-end managed services—including training, regulatory updates, and analytics concierge—gain renewal advantages. Platform ecosystems continue expanding through API marketplaces that invite third-party applications for wound imaging, resident engagement, and family communications.

Long Term Care Software Industry Leaders

McKesson Corporation

Allscripts Healthcare Solutions

Netsmart Technologies Inc.

Cerner Corporation (Oracle)

Epic Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: HEALWELL AI completed acquisition of Orion Health for NZD 175 million (USD 105 million) to create a global data-interoperability leader, affecting 150 million patient lives worldwide.

- July 2024: Nordic Capital acquired majority stake in Sensio, enlarging its European long-term care technology presence

Global Long Term Care Software Market Report Scope

As per the report's scope, long-term care software refers to software services that include electronic medical records, e-prescribing, medication management, patient monitoring, remote training, etc., which enhance the business operation's needs, patient experience, and outcomes. The Long-term Care Software Market is Segmented by Product (Electronic Health Records, E-prescribing, Clinical Decision Support Systems, Remote Patient Monitoring Systems, Real-time Location Systems, Billing, Invoicing, and Scheduling Software, and Other Products), Deployment (Cloud Bases and On-premise), End User (Home Healthcare Agencies, Hospice Care Facilities, and Nursing Homes and Assisted Living Facilities), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Cloud-based |

| Web-based |

| On-premises |

| Electronic Health Record (EHR) |

| eMAR / Medication Management |

| Revenue-Cycle & Financial Management |

| Workforce & Scheduling |

| Analytics & Business Intelligence |

| Nursing Homes / Skilled-Nursing Facilities |

| Assisted-Living Facilities |

| Home-Health & Hospice Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Deployment Model | Cloud-based | |

| Web-based | ||

| On-premises | ||

| By Product Module | Electronic Health Record (EHR) | |

| eMAR / Medication Management | ||

| Revenue-Cycle & Financial Management | ||

| Workforce & Scheduling | ||

| Analytics & Business Intelligence | ||

| By End-User Facility Type | Nursing Homes / Skilled-Nursing Facilities | |

| Assisted-Living Facilities | ||

| Home-Health & Hospice Agencies | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for Long Term Care Software providers by 2031?

The long term care software market size is forecast to reach USD 9.49 billion by 2031 based on a 9.13% CAGR.

Which deployment model is growing fastest among senior-care operators?

Cloud-based SaaS platforms are expanding at a 9.41% CAGR as facilities seek scalability and automatic updates.

Why are analytics modules becoming critical in long-term care?

Analytics & Business Intelligence tools support fall prevention, readmission reduction, and value-based reimbursement optimization, making them the fastest-growing module at a 9.88% CAGR.

Which region offers the highest growth potential through 2031?

Asia-Pacific leads with a projected 9.74% CAGR due to rapid aging demographics and government technology incentives.

How are staffing shortages influencing software purchasing decisions?

Facilities increasingly adopt AI-powered scheduling and mobile workflows to offset caregiver deficits, driving demand for integrated workforce management features.

What competitive moves are reshaping vendor positioning?

Notable actions include PointClickCare's acquisition of American HealthTech and WellSky's generative-AI partnership with Google Cloud, both aimed at broadening platform capabilities.

Page last updated on: