Healthcare Technology Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

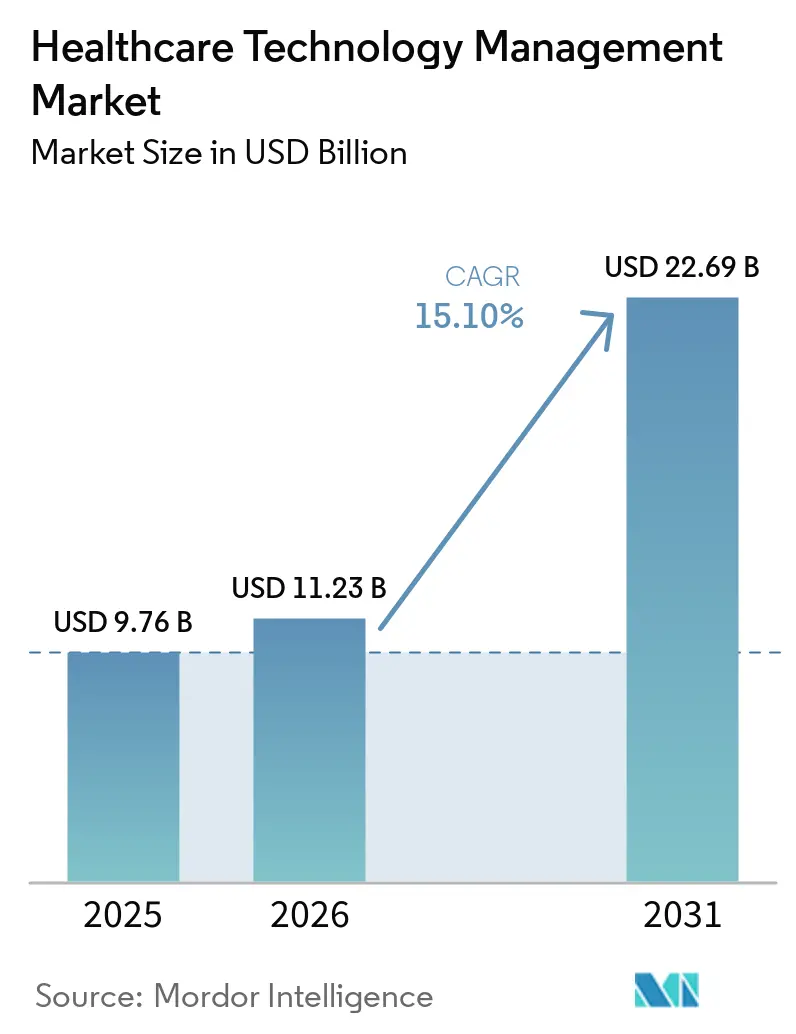

| Market Size (2026) | USD 11.23 Billion |

| Market Size (2031) | USD 22.69 Billion |

| Growth Rate (2026 - 2031) | 15.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Technology Management Market Analysis by Mordor Intelligence

The Healthcare Technology Management Market size is expected to increase from USD 9.76 billion in 2025 to USD 11.23 billion in 2026 and reach USD 22.69 billion by 2031, growing at a CAGR of 15.10% over 2026-2031.

The healthcare technology management market is experiencing growth as clinical engineering becomes integral to hospital operations, emphasizing device uptime, audit readiness, and workflow continuity. This expansion is driven by an increasing number of connected medical devices, stricter lifecycle documentation requirements, cost pressures on health systems, and hospital digitization programs across North America, Europe, and Asia. Large acute care hospitals now manage equipment from 25 to 50 vendors, prompting a shift from single OEM tools to enterprise platforms capable of handling diverse fleets in a unified system. Cloud adoption in ambulatory and community settings further supports market growth by reducing local infrastructure demands and simplifying updates.

Key Report Takeaways

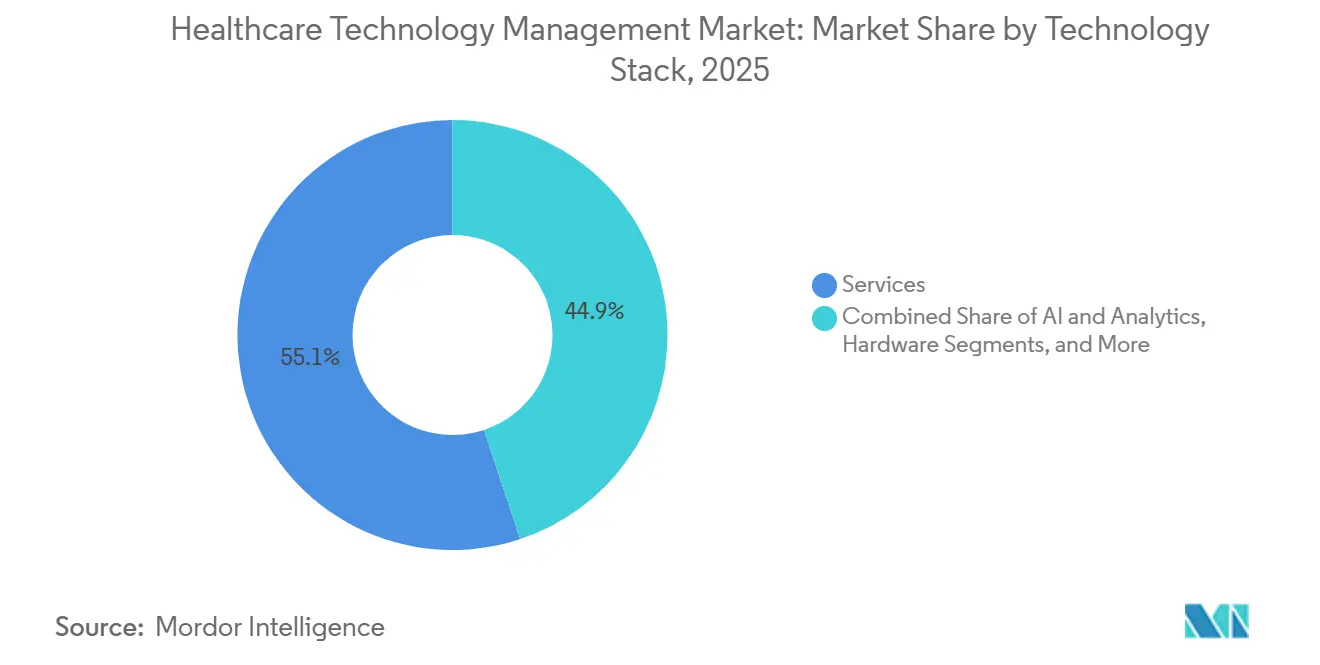

- By technology stack, services held 55.13% of revenue in 2025, while AI and analytics are projected to grow at a 17.25% CAGR through 2031.

- By deployment, on-premises accounted for 57.13% of revenue in 2025, while cloud-based deployment is projected to expand at a 16.55% CAGR through 2031.

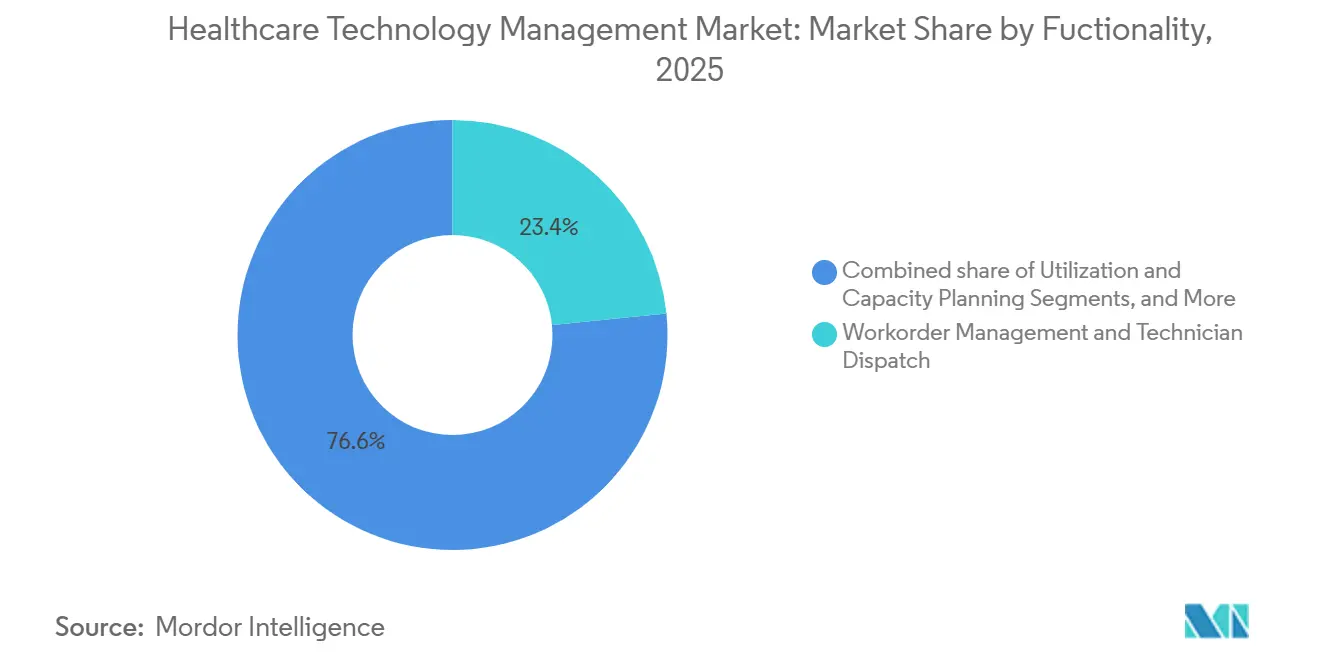

- By functionality, workorder management and technician dispatch held 23.44% of revenue in 2025, while utilization and capacity planning is expected to grow at a 16.88% CAGR through 2031.

- By end user, hospitals held 46.93% of revenue in 2025, while clinical research, CRO, and trial sites are projected to advance at a 17.45% CAGR through 2031.

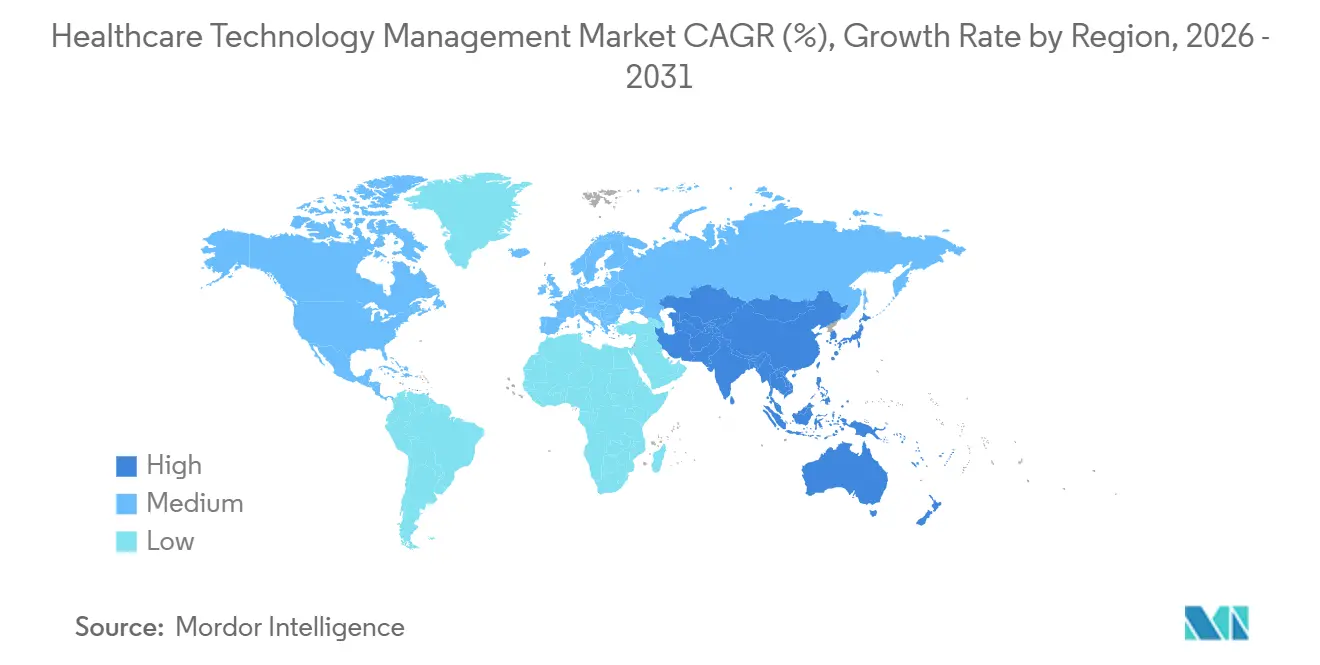

- By geography, North America held 39.56% of global revenue in 2025, while Asia Pacific is projected to grow at an 18.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Technology Management Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expansion of connected medical devices and multi vendor environments | +3.8% | Global | Medium term (2-4 years) |

| Rising compliance burden across device lifecycle management | +2.5% | North America and EU | Long term (≥ 4 years) |

| Hospital cost containment programs prioritizing uptime and utilization | +2.2% | North America, spill over to APAC | Medium term (2-4 years) |

| Rising right to repair and service access pressure | +1.2% | North America, with early EU follow on | Short term (≤ 2 years) |

| Cybersecurity exposure of networked clinical equipment | +3.0% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Connected Medical Devices and Multi-Vendor Environments

Hospitals today manage a broader range of device types, vendors, and service histories compared to previous years, driving growth in the healthcare technology management market. Acute care hospitals typically operate equipment from 25 to 50 OEM brands, each with unique firmware cycles, calibration schedules, and maintenance patterns. This complexity highlights the need for vendor-neutral platforms that consolidate asset data into a single system. Community hospitals and ambulatory networks, often lacking integration teams, prefer cloud-native tools with pre-built connectors to larger digital systems. The integration of Kahua and Nuvolo has demonstrated how seamless transitions from construction handover to live operations can address asset record gaps that have historically delayed biomedical teams.

Rising Compliance Burden Across Device Lifecycle Management

Expanding compliance requirements are driving demand in the healthcare technology management market. The FDA's final cybersecurity guidance for June 2025 emphasizes post-market vulnerability monitoring across the device lifecycle, increasing the need for platforms that track firmware versions, patches, and vulnerabilities.[1]U.S. Food and Drug Administration, “Cybersecurity in Medical Devices, Digital Health Center of Excellence,” U.S. Food and Drug Administration, fda.gov In Germany, the EUR 4.3 billion (USD 4.98 billion) Krankenhauszukunftsgesetz program is accelerating hospital system upgrades and integrating lifecycle management tools into procurement programs. Similarly, the EU Cyber Resilience Act and EU MDR are pushing health systems to adopt automated records and audit trails, replacing spreadsheet-based tracking with platforms capable of generating inspection-ready records across multi-site fleets.[2]International Trade Administration, “Germany, Healthcare and Medical Technology,” U.S. Commercial Service, trade.gov

Hospital Cost-Containment Programs Prioritizing Uptime and Utilization

Hospital finance teams are prioritizing uptime and equipment utilization as critical cost and capacity factors. Imaging equipment and ventilator fleets, representing significant asset value, face financial risks from failures, delays, and underutilization. Maintenance strategies are shifting to condition-based and predictive approaches using asset signals and failure probability models. TRIMEDX introduced AI-based capital planning and inventory optimization features in TRIMEDX AIQ in January 2026, enabling health systems to evaluate repair versus replacement decisions. An IBM Maximo implementation in Poland demonstrated AI-enhanced asset management, extending equipment life by 17% and improving mean time to repair by 57%, highlighting the financial and operational benefits of such platforms.

Rising Right-To-Repair And Service-Access Pressure

Pressure to expand service access beyond OEMs is reshaping the healthcare technology management market. Hospitals and independent service providers are challenging software locks, parts restrictions, and limited access to service tools that delay repairs and restrict post-warranty options. Buyers increasingly prefer platforms that support both OEM and ISO workflows within a unified environment, avoiding separate work order structures. While neutral service management platforms are gaining traction, adoption depends on local contract terms and the willingness of health systems to renegotiate long-standing service agreements.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shortage of biomedical engineering and HTM talent | -2.2% | Global, most acute in North America | Long term (≥ 4 years) |

| Fragmented legacy asset data and interoperability gaps | -1.5% | Global, concentrated in smaller markets | Medium term (2-4 years) |

| OEM service lock in and contractual barriers | -1.8% | North America and EU | Medium term (2-4 years) |

| Budget deferrals in smaller hospitals and post acute facilities | -0.8% | Global, highest in South America and MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Biomedical Engineering And HTM Talent

The healthcare technology management (HTM) market is constrained by a talent shortage, limiting the scalability of service capacities. AAMI noted in 2025 that demand for HTM roles remained strong with high job satisfaction, while the U.S. Bureau of Labor Statistics projected an 18% growth for biomedical equipment technicians through 2033, equating to nearly 8,800 annual job openings. This gap forces health systems to face challenges in expanding in-house teams, increasing reliance on outsourced managed services. While AI-driven triage and remote diagnostics ease some workloads, they cannot replace skilled on-site personnel essential for maintenance, inspections, and complex repairs. In regions with slow technician pipeline development, demand remains high, but service implementation and coverage often lag.

OEM Service Lock-In And Contractual Barriers

The HTM market faces challenges from OEM contracts that limit access to diagnostic data, firmware updates, and calibration records. These restrictions create switching costs and often lock hospitals into separate service environments, even when a unified asset risk view is preferred. This issue is most pronounced in high-value imaging and radiation therapy sectors, where OEM influence is significant, and independent alternatives are limited. Consequently, third-party platform adoption slows as hospitals gain only partial visibility into mixed fleets instead of full lifecycle control. The market advances more rapidly where health systems renegotiate service terms or adopt broader multi-vendor agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Stack: Services-Led Entry, Software-Enabled Scale

In 2025, services accounted for 55.13% of the healthcare technology management market, reflecting the preference for outsourced managed HTM contracts before standalone software adoption. Providers often bundle field support, workflow execution, and software into a single offering, making services the dominant layer. Hospitals typically prioritize an immediate operational model over building internal capabilities, with software adoption following operational trust.

Hardware remains critical as hospitals rely on RTLS tags, BLE readers, and IoT sensor arrays to enhance asset visibility. Beyond tracking, improved device location and condition signals enable faster dispatch, better utilization data, and stronger documentation. AI and Analytics, projected to grow at a 17.25% CAGR through 2031, indicate a shift toward predictive and decision-support layers. TRIMEDX advanced this trend in February 2026 by integrating supply chain automation and predictive failure intelligence into TRIMEDX AIQ, while the industry moves toward subscription-based analytics modules for optimization.

By Deployment: On-Premises Dominance Coexists with Cloud Acceleration

On-premises deployment held 57.13% of the healthcare technology management market share in 2025, driven by the needs of academic medical centers, veterans affairs systems, and defense-linked health settings with strict data governance requirements. These organizations often maintain local systems to support complex clinical environments and ensure compliance, security, and infrastructure control. This sustains the relevance of on-premises deployments alongside growing cloud adoption.

Cloud-based deployment is forecast to grow at a 16.55% CAGR through 2031 as ambulatory groups and community health systems seek reduced infrastructure burdens and faster updates. Nuvolo’s recognition as a 2026 ServiceNow Store Partner of the Year highlights the appeal of unified platforms integrating CMMS, facilities management, and cybersecurity. Hybrid deployment is also gaining traction, with large systems retaining local processing for time-sensitive alerts while moving analytics to the cloud. IBM and Oracle expanded their partnership in 2025 to support this transition with a Maximo Application Suite connector for Oracle Fusion Cloud ERP.

By Functionality: Workorder Systems as the Foundation, Utilization Analytics as the Prize

Workorder Management and Technician Dispatch accounted for 23.44% of the healthcare technology management market in 2025, reflecting its foundational role in regulated biomedical operations. Clear corrective and preventive documentation makes work order systems a priority for buyers, ensuring compliance and service traceability. These modules remain essential even as advanced functionalities gain prominence.

Utilization and Capacity Planning, projected to grow at a 16.88% CAGR through 2031, is gaining importance as hospitals seek insights into fleet usage and distribution. Asset Tracking and Location Services are also becoming strategic, as precise location data improves turnaround times and utilization accuracy. Midmark RTLS advanced this trend in March 2026 with a hybrid BLE and Wireless IR architecture, enabling room-level precision and integration with EHRs for workflow automation. The market is evolving toward a model where compliance is established through work order systems, while advanced analytics and forecasting deliver added value.

By End User: Hospitals Anchor Revenue, Clinical Research Sites Lead Growth

Hospitals represented 46.93% of end-user revenue in 2025, maintaining their central role in the healthcare technology management market. Inpatient settings manage complex multi-vendor fleets and face significant compliance demands, making lifecycle control a daily operational necessity. Hospital demand continues to shape vendor offerings, service models, and contracting structures, with enterprise agreements often starting in hospitals and extending to outpatient networks.

Ambulatory centers, long-term care providers, and diagnostic imaging groups are expanding adoption as connected devices extend beyond inpatient settings. Clinical Research, CRO, and Trial Sites are projected to grow at a 17.45% CAGR through 2031, driven by the need for comprehensive maintenance records to ensure data integrity in trials. The industry is addressing this demand by treating research sites as a distinct segment with stringent audit and documentation requirements. Medical equipment distributors and OEM service partners are also leveraging these platforms to measure service performance against SLA benchmarks, expanding their reach beyond direct hospital sales.

Geography Analysis

In 2025, North America accounted for 39.56% of the healthcare technology management market, driven by a robust acute care hospital network, stringent Joint Commission and CMS mandates, and a consolidating managed services layer. The U.S. remains the largest revenue contributor, with enterprise buyers favoring large multi-site fleets and formal outsourced service programs. Agiliti's acquisition by Thomas H. Lee Partners in May 2024, valued at USD 2.5 billion, highlighted strong capital support for technology-driven expansion across over 10,000 facilities. The FDA's 2025 cybersecurity guidelines have expanded platform requirements, particularly for health systems managing enterprise-scale networked devices. Canada and Mexico contribute modestly, with private hospital digitization and cloud adoption supporting incremental growth.

Asia Pacific is projected to grow at an 18.12% CAGR through 2031, making it the fastest-growing region in the healthcare technology management market. Growth is fueled by regulatory modernization, hospital infrastructure investments, and improved asset management maturity across public and private networks. In China, IoT protocol standards for hospital equipment management are driving a shift from siloed systems to standardized procurement. In India, private hospital groups are integrating clinical asset visibility into digital transformation strategies, with Infosys securing a seven-year AI-driven ERP program with IHH Healthcare in 2026. Japan, Australia, and South Korea add advanced capabilities by connecting utilization data, tracking home-deployed devices, and enhancing digital health infrastructure.

Europe shows a mixed adoption pattern in the healthcare technology management market. Germany, the UK, and France are advancing cloud-enabled upgrades, while Southern and Eastern Europe lag. Germany's Krankenhauszukunftsgesetz, supported by EUR 4.3 billion (approximately USD 4.98 billion), is driving modernization across 1,900 hospitals and accelerating digital lifecycle tool adoption. EU MDR and Cyber Resilience Act requirements are increasing demand for platforms with robust functionality and lifecycle documentation.

Competitive Landscape

The healthcare technology management market is moderately consolidated at the top, with TRIMEDX, Agiliti, GE HealthCare, and Siemens Healthineers maintaining long-term enterprise relationships. These vendors compete through service scale, contract depth, a strong installed customer base, and the ability to manage large multi-vendor fleets under defined service levels. The next tier is more fragmented, with regional ISOs, RTLS specialists, and focused CMMS providers emphasizing implementation cost, flexibility, and local responsiveness. This structure creates stability among enterprise leaders while fostering a diverse middle segment of specialists. Consolidation pressures are expected to remain strongest in the upper tier, where compliance, integration, and analytics development demand significant investment.

Competition in the healthcare technology management market is shifting from maintenance logging to intelligent operational support. TRIMEDX expanded its TRIMEDX AIQ platform in February 2026, integrating supply chain automation to link predicted failures with parts ordering and procurement workflows. Nuvolo, now part of Trane Technologies, connects CMMS data with facilities and building systems, enhancing reliability and compliance management. IBM and Oracle are advancing platform integration by linking asset management with enterprise cloud applications, supporting large-scale health system deployments. This evolution drives competition toward platform breadth, automation depth, and value delivery across engineering, finance, and operations.

The mid-market community hospital segment presents significant opportunities, as buyers often find full managed services too costly and enterprise platforms overly complex. Vendors offering modular SaaS tools with pre-designed compliance templates are well-positioned to serve this segment without requiring substantial upfront investments. RTLS-focused players and point solutions remain relevant, as hospitals frequently prioritize specific operational goals over full-stack platforms. However, rising compliance standards are increasing product requirements, pressuring smaller vendors to meet documentation and cybersecurity expectations. The market remains competitive but is increasingly shaped by firms that balance flexibility with sustained product investment.

Healthcare Technology Management Industry Leaders

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Siemens Healthineers AG

TRIMEDX Holdings, LLC

Agiliti Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Midmark RTLS introduced a hybrid BLE and Wireless IR system, combining facility-wide BLE coverage with room-level IR precision to automate workflows and support applications like asset tracking and staff safety.

- February 2026: TRIMEDX enhanced its AIQ platform with supply chain automation, including predictive failure forecasting and automated parts ordering, to minimize operational disruptions.

- January 2026: TRIMEDX added AI-driven capital planning and inventory optimization to its AIQ platform, helping healthcare finance leaders optimize costs and reduce unplanned inventory expenses.

- September 2025: Oracle launched AI-powered inventory management and procurement features in its Fusion Cloud Applications, streamlining workflows and improving supply visibility for healthcare organizations.

Global Healthcare Technology Management Market Report Scope

As per the scope of the report, Healthcare Technology Management (HTM) is the systematic planning, selection, acquisition, deployment, maintenance, and safe use of medical equipment and healthcare software. It is led by clinical engineers and technicians to ensure hospital tools are safe, effective, and cost-efficient.

The healthcare technology management market is segmented by technology stack, deployment, functionality, end-user, and geography. By technology stack, the market includes services, software, hardware, and AI and analytics. By deployment, the market is segmented into on-premises, cloud-based, and hybrid. By functionality, the market is categorized into asset tracking & location services (RTLS), utilization & capacity planning, workorder management & technician dispatch, regulatory & compliance reporting, costing & chargeback/cost allocation, performance benchmarking & SLA management, spare parts forecasting & automated replenishment, and device interoperability & clinical workflow enablement. By end-user, the market is segmented into hospitals, ambulatory & outpatient centers, diagnostic imaging centers & labs, long-term care & nursing homes, home healthcare providers, clinical research/CROs/trial sites, government & public health facilities, private clinics/specialty centers, and medical equipment distributors/OEM service partners. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Services |

| Software |

| Hardware |

| AI and Analytics |

| On-Premises |

| Cloud-Based |

| Hybrid |

| Asset Tracking & Location Services (RTLS) |

| Utilization & Capacity Planning |

| Workorder Management & Technician Dispatch |

| Regulatory & Compliance Reporting |

| Costing & Chargeback / Cost Allocation |

| Performance Benchmarking & SLA Management |

| Spare Parts Forecasting & Automated Replenishment |

| Device Interoperability & Clinical Workflow Enablement |

| Hospitals |

| Ambulatory & Outpatient Centers |

| Diagnostic Imaging Centers & Labs |

| Long-term Care & Nursing Homes |

| Home Healthcare Providers |

| Clinical Research / CROs / Trial sites |

| Government & Public Health Facilities |

| Private Clinics / Specialty Centers |

| Medical Equipment Distributors / OEM Service Partners |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology Stack | Services | |

| Software | ||

| Hardware | ||

| AI and Analytics | ||

| By Deployment | On-Premises | |

| Cloud-Based | ||

| Hybrid | ||

| By Functionality | Asset Tracking & Location Services (RTLS) | |

| Utilization & Capacity Planning | ||

| Workorder Management & Technician Dispatch | ||

| Regulatory & Compliance Reporting | ||

| Costing & Chargeback / Cost Allocation | ||

| Performance Benchmarking & SLA Management | ||

| Spare Parts Forecasting & Automated Replenishment | ||

| Device Interoperability & Clinical Workflow Enablement | ||

| By End User | Hospitals | |

| Ambulatory & Outpatient Centers | ||

| Diagnostic Imaging Centers & Labs | ||

| Long-term Care & Nursing Homes | ||

| Home Healthcare Providers | ||

| Clinical Research / CROs / Trial sites | ||

| Government & Public Health Facilities | ||

| Private Clinics / Specialty Centers | ||

| Medical Equipment Distributors / OEM Service Partners | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for healthcare technology management?

The healthcare technology management market is forecast to reach USD 22.69 billion by 2031 from USD 11.23 billion in 2026, at a 15.10% CAGR.

Which technology layer leads revenue today?

Services led revenue with 55.13% in 2025, reflecting the strong role of outsourced managed HTM contracts.

Which deployment model is growing fastest?

Cloud based deployment is the fastest growing model, with a projected 16.55% CAGR through 2031 as smaller and distributed providers shift toward SaaS CMMS tools.

Which end users are expanding fastest?

Clinical Research, CRO, and Trial Sites are projected to grow at a 17.45% CAGR through 2031 because regulated studies require complete device maintenance records.

Why is North America the largest regional contributor?

North America held 39.56% in 2025 because of its large acute care infrastructure, mature compliance requirements, and a more developed managed services ecosystem.

What is driving vendor competition now?

Competition is increasingly centered on compliance automation, multi vendor fleet visibility, predictive analytics, and tighter integration with supply chain and enterprise systems.

Page last updated on: