Healthcare Supply Chain Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.94 Billion |

| Market Size (2031) | USD 6.52 Billion |

| Growth Rate (2026 - 2031) | 10.62% CAGR |

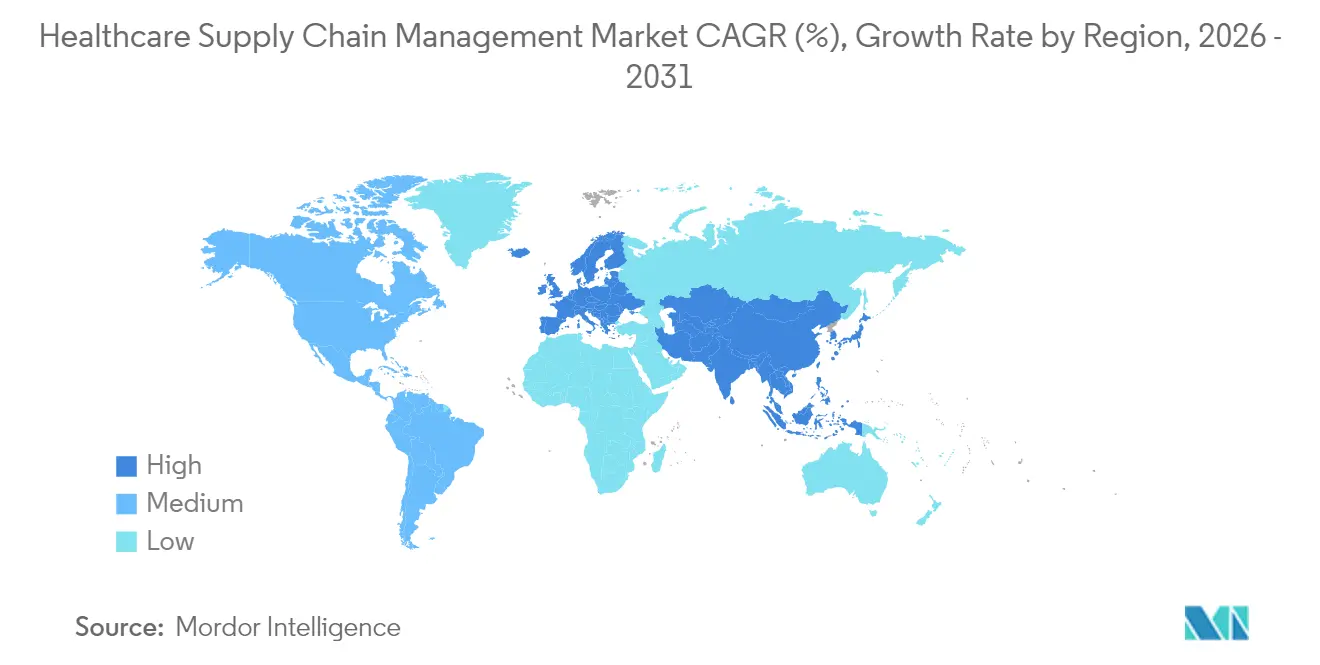

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Supply Chain Management Market Analysis by Mordor Intelligence

The healthcare supply chain management market size was valued at USD 3.56 billion in 2025 and estimated to grow from USD 3.94 billion in 2026 to reach USD 6.52 billion by 2031, at a CAGR of 10.62% during the forecast period (2026-2031). Cloud migration, artificial intelligence–driven demand sensing, and end-to-end traceability mandates are redefining how hospitals, pharmaceutical manufacturers, and distributors plan, source, and move products. Unit-level serialization required by the Drug Supply Chain Security Act (DSCSA) is accelerating platform adoption that unifies purchasing, inventory, logistics, and compliance workflows. Group Purchasing Organizations (GPOs) are expanding their remit from price aggregation to data-driven procurement services, while cold-chain design upgrades protect high-value biologics and cell-and-gene therapies. Strategic acquisitions such as UPS’s purchase of Andlauer Healthcare Group confirm the pivot toward integrated, technology-enabled logistics that improve resilience and lower total delivered cost.

Key Report Takeaways

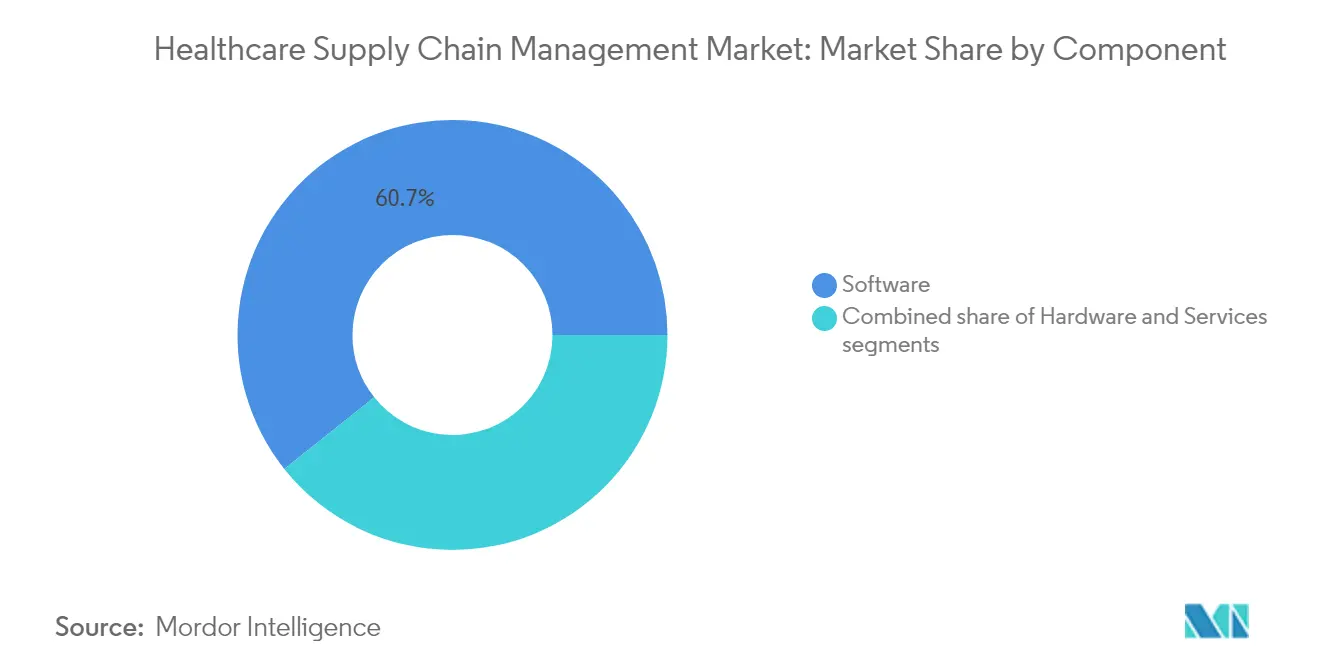

- By component, software solutions captured 60.70% of the healthcare supply chain management market share in 2025, whereas services are projected to grow at an 11.45% CAGR to 2031.

- By deployment mode, on-premise systems held 53.60% revenue share in 2025; cloud deployment is expected to advance at a 11.95% CAGR through 2031.

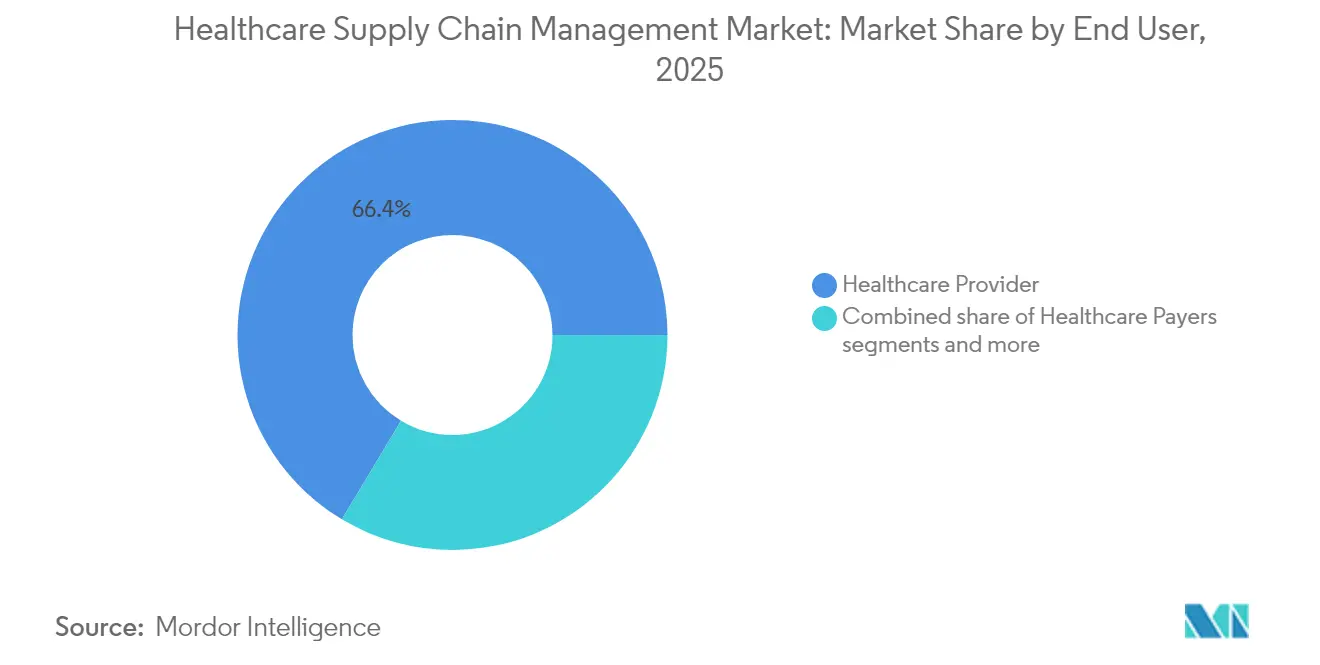

- By end user, healthcare providers commanded 66.40% share of the healthcare supply chain management market size in 2025, while pharmaceutical and biotech companies record the fastest segment CAGR at 12.18% between 2026 and 2031.

- By geography, North America led with 45.10% of healthcare supply chain management market share in 2025; Asia-Pacific is the fastest-growing region at a 12.42% CAGR for the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Supply Chain Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first upgrades to cut inventory waste | +2.1% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Mandatory UDI & track-and-trace regulations | +1.8% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| AI-driven demand sensing & predictive restocking | +2.3% | Global, led by North America innovation hubs | Medium term (2-4 years) |

| Rapid outsourcing to GPOs for cost containment | +1.7% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| Vendor-managed inventory for critical drugs | +1.4% | Global, with pharmaceutical hub concentration | Medium term (2-4 years) |

| Climate-resilient cold-chain design mandates | +1.2% | Global, priority in temperature-sensitive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Upgrades to Cut Inventory Waste

Nearly 70% of U.S. hospitals plan to run core supply operations on cloud platforms by 2026, unlocking real-time visibility that trims excess stock and reduces stockouts. Machine-learning engines embedded in these platforms analyze consumption patterns, seasonality, procedure schedules, and supplier lead times to keep inventory within clinically safe but financially lean thresholds. Health systems that completed migration report inventory-related savings of up to 30% alongside improved clinician satisfaction due to fewer product shortages. Cloud architecture also streamlines integration with electronic health records and simplifies multi-site coordination, critical as provider networks consolidate.

Mandatory UDI & Track-and-Trace Regulations

The FDA’s Unique Device Identification system and DSCSA serialization requirements force every device and drug unit to carry a machine-readable code that travels across the entire chain, from factory to bedside. Compliance platforms automatically capture, store, and exchange this data, cutting recall investigation times from weeks to hours and strengthening patient safety. Providers that align early gain operational benefits through automated expiration alerts and end-to-end provenance auditing[1]Source: U.S. Food and Drug Administration, “Drug Supply Chain Security Act Product Tracing Requirements – FAQs,” fda.gov.

AI-Driven Demand Sensing & Predictive Restocking

Hospitals and distributors now embed artificial intelligence into demand planning to predict usage with higher precision. Early adopters record 22% boosts in supply chain productivity as AI blends historical demand, surgical schedules, epidemiological alerts, and external disruptions to trigger proactive replenishment. Vendors are pairing these algorithms with vendor-managed inventory programs, allowing manufacturers to adjust stock remotely and avert critical drug shortages.

Rapid Outsourcing to GPOs for Cost Containment

Facing double-digit inflation in consumable prices, 93% of U.S. hospitals intend to deepen reliance on GPOs by 2026. GPO contracts now extend beyond unit pricing to include data analytics, supplier score-carding, and compliance monitoring. Member hospitals report 13.1% procurement savings and faster access to shortage allocation insights, benefits especially valued by community facilities with tight margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front integration & training costs | -1.9% | Global, particularly acute in resource-constrained markets | Short term (≤ 2 years) |

| Cyber-security & data-privacy liabilities | -1.6% | Global, with heightened concern in North America & EU | Medium term (2-4 years) |

| Shortage of supply-chain IT talent in hospitals | -1.3% | Global, most severe in North America & EU | Medium term (2-4 years) |

| Opaque supplier ESG data blocking compliance | -0.8% | EU & North America core, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Integration & Training Costs

Implementing a full-stack platform demands USD 2–15 million for a mid-sized system, covering software, hardware, interfaces, and six-to-twelve-month staff education. Complex links to electronic health records and financial modules often double initial budgets, stretching payback horizons to 18–24 months and deterring smaller providers[2]Source: TECSYS, “Future Trends in Healthcare Supply Chain,” tecsys.com .

Cyber-Security & Data-Privacy Liabilities

Digital supply networks widen attack surfaces. Healthcare breach costs average USD 10.9 million and 40% of IT teams report insufficient cyber skills. Each additional trading-partner integration multiplies risk, forcing providers to vet global suppliers and distributors for adherence to security frameworks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Digital Transformation

Software platforms accounted for 60.70% of the healthcare supply chain management market in 2025, reflecting urgent demand for unified command centers that coordinate sourcing, contracting, logistics, and compliance. Services, though smaller, post the fastest 11.45% CAGR thanks to provider reliance on implementation, workflow redesign, and change-management support . Hardware—RFID readers, automated dispensing cabinets, and IoT sensors—remains indispensable for real-time data capture, even as budgets tilt toward cloud licenses.

Software’s edge stems from embedded analytics that spot variance, predict demand, and surface compliance gaps. Oracle Health’s next-generation EHR integrates supply chain modules, enabling clinicians to place auto-replenish orders without leaving patient charts. Such convergence aligns procurement decisions with clinical pathways, shrinking waste and improving case costing

By Deployment Mode: Cloud Migration Accelerates Despite Legacy Footprint

On-premise installations still hold 53.60% share, a legacy of sunk infrastructure and data-sovereignty policies at large academic centers. Yet the healthcare supply chain management market is decisively tilting toward cloud, forecast to grow at a 11.95% CAGR as CIOs prioritize scalability, continuous upgrades, and decreased capital expense. Vendors offer hybrid options that segregate protected health information on internal servers while routing analytics workloads to encrypted public clouds. Regulatory bodies increasingly accept cloud hosts certified to HITRUST and ISO-27001, easing perceived security barriers.

Cloud deployments accelerate AI rollout and speed compliance updates. Real-time DSCSA data-exchange requirements arriving in November 2024 are easier to meet when serialization engines sit on elastic, API-friendly clouds rather than bespoke local servers.

By End User: Providers Lead, Pharma Accelerates

Hospitals and health systems generated 66.40% of 2025 revenue. Their large SKU breadth, just-in-time surgery schedules, and pressing cost pressure sustain investment.. Pharmaceutical and biotech firms, however, show the highest 12.18% CAGR, driven by stringent GDP (Good Distribution Practice) requirements and the growth of temperature-sensitive biologics. As drug portfolios grow more complex, manufacturers embed internet-connected sensors and blockchain ledgers to assure integrity. Payers, though smaller in spend, now demand transparency to reconcile device utilization with claims, nudging them toward shared data platforms.

Geography Analysis

North America retained 45.10% of healthcare supply chain management market share in 2025. DSCSA deadlines and a mature GPO ecosystem underpin stable demand, while ongoing consolidation among IDNs fuels enterprise-scale platform rollouts. Canada’s provincially funded health systems invest in supply-chain command centers to curb rising procedure costs.

Asia-Pacific records the steepest 12.42% CAGR to 2031. Rapid hospital construction in China and India, vaccine self-sufficiency programs, and governmental push for digital health infrastructure drive adoption. Thailand’s vendor-managed inventory pilots and Singapore’s IoT-enabled hospital campuses showcase regional innovation. The healthcare supply chain management market size for Asia-Pacific is projected to double by 2030 as cold-chain for advanced therapeutics scales.

Europe shows steady growth underpinned by Medical Device Regulation (MDR), climate-aligned ESG mandates, and Brexit-triggered buffer-stock strategies. Multinational health systems seek platforms that consolidate multilingual labeling, track environmental metrics, and interface with country-specific e-procurement portals.

Competitive Landscape

The sector remains moderately fragmented, yet merger activity is rising as players chase end-to-end offerings. GHX, SAP, Oracle Health, and McKesson anchor the incumbent tier, leveraging deep hospital footprints and broad product lines. UPS’s USD 1.6 billion acquisition of Andlauer Healthcare Group adds temperature-controlled warehousing, positioning UPS as a dominant logistics integrator. Cardinal Health’s USD 1.2 billion purchase of Specialty Networks strengthens specialty pharma distribution and data analytics.

Competition now centers on AI capabilities, regulatory compliance automation, and ecosystem openness. Oracle’s AI-driven clinical digital assistant routes device preference cards directly into purchase orders, while Clarium’s USD 10.5 million seed round targets AI algorithms that cut perioperative waste. Traditional warehouse-management vendors such as Manhattan Associates embed generative AI into planning tools to predict shortages and recommend alternate sourcing. As platform breadth trumps point solutions, mid-sized vendors face buy-or-partner decisions to stay relevant.

Healthcare Supply Chain Management Industry Leaders

SAP AG Group

McKesson Corporation

Avery Dennison Corporation

Oracle Corporation

Tecsys Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: UPS announced the USD 1.6 billion takeover of Andlauer Healthcare Group, enhancing global cold-chain reach.

- April 2025: McKesson agreed to acquire a controlling stake in PRISM Vision Holdings for USD 850 million, expanding specialty distribution in ophthalmology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the healthcare supply chain management market as the total global spending on purpose-built software, enabling hardware (RFID, barcode, mobile scanners), and associated implementation or support services that allow hospitals, distributors, pharma and biotech manufacturers, and contract makers to plan, source, track, and settle the flow of medicinal products, devices, and consumables.

Scope Exclusion: Pure-play freight forwarding, general third-party logistics fees, and stand-alone warehouse automation equipment fall outside this valuation.

Segmentation Overview

- By Component

- Software

- Hardware

- Services

- By Deployment Mode

- On-premise

- Cloud-based

- By End User

- Healthcare Providers

- Healthcare Payers

- Pharma & Biotech Companies

- Contract Manufacturing Organizations

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with supply-chain IT directors, group purchasing officers, and regulatory consultants across North America, Europe, and Asia-Pacific help us lock in average software license fees, cloud migration timelines, and realistic adoption ceilings. Follow-up calls with inventory technology integrators verify payback assumptions that surfaced in secondary research.

Desk Research

Mordor analysts review publicly available datasets from agencies such as the United States FDA (UDI compliance filings), CMS hospital cost reports, Eurostat trade codes for HS 3004 and 9018, and World Bank health-expenditure dashboards. We also mine association white papers from AHRMM, GS1 Healthcare, and the European Federation of Pharmaceutical Industries, together with peer-reviewed journals tracking RFID uptake in sterile supplies. Company 10-Ks, procurement frameworks published by large provider networks, and news archives on Dow Jones Factiva add incremental context. D&B Hoovers provides revenue splits that let us sanity-check vendor coverage. This list is illustrative; many other open sources inform our desk work.

Market-Sizing & Forecasting

A top-down build begins with global health-expenditure pools and regional procurement ratios, which are then refined through production and trade data reconstructs of software and RFID hardware. Select bottom-up checks, sampled average selling price multiplied by installed base of tier-one hospitals and pharma plants, act as guardrails. Key model variables include average acute-care beds per facility, mandated DSCSA serialization deadlines, RFID adoption rates, inventory turnover days, cloud penetration in hospital IT budgets, and regional currency movements. Multivariate regression combined with scenario analysis forecasts each driver, while judgment from our primary experts steers the final CAGR. Gaps uncovered in bottom-up rolls are bridged through weighted interpolation rather than forced extrapolation.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer analyst cross-checks, and senior sign-off. We benchmark results against external spend indices and refresh the model annually, with mid-cycle revisions triggered by material regulatory or mega-merger events. A final quality sweep occurs immediately before report release to ensure clients receive the most current view.

Why Mordor's Healthcare Supply Chain Management Baseline Commands Reliability

Published estimates often diverge because firms pick different inclusion rules, currency bases, and refresh cadences.

Key Gap Drivers: Some publishers fold freight and cold-chain charges into market value, others start from 2024 data then inflate, and many apply flat software price curves without validating regional ASP drift. Mordor's disciplined scope, dual-path modeling, quarterly FX resets, and annual primary probes keep our 2025 figure tightly anchored.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.56 B | Mordor Intelligence | - |

| USD 3.93 B | Global Consultancy A | Counts broad 3PL and courier revenue |

| USD 3.95 B | Industry Research House B | Uses blended 2024 base and adds installation fees |

| USD 3.60 B | Trade Journal C | Excludes enabling hardware such as RFID readers |

Taken together, the comparison shows that once scope inflation and dated baselines are stripped away, Mordor Intelligence delivers a balanced, transparent benchmark that decision-makers can trace to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the healthcare supply chain management market?

The healthcare supply chain management market is worth USD 3.94 billion in 2026 and is projected to grow to USD 6.52 billion by 2031.

Which region is expanding the fastest?

Asia-Pacific leads growth with a 12.42% CAGR, fueled by rising healthcare spending, infrastructure expansion, and government digitization initiatives.

Why are GPOs becoming more important?

Hospitals look to GPOs for collective purchasing power and analytics support, achieving average supply cost reductions of 13.1% while offloading complex contracting tasks.

How do DSCSA regulations affect supply chain management technology adoption?

Unit-level serialization and electronic data exchange mandates force providers and distributors to deploy integrated traceability platforms that improve recall speed and regulatory compliance.

What role does artificial intelligence play in healthcare supply chains?

AI models predict demand, automate replenishment, and flag anomalies, delivering 22% efficiency gains and lowering inventory waste across multi-site health systems.

Page last updated on: