Private Nursing Services Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 53.71 Billion |

| Market Size (2031) | USD 73.68 Billion |

| Growth Rate (2026 - 2031) | 6.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

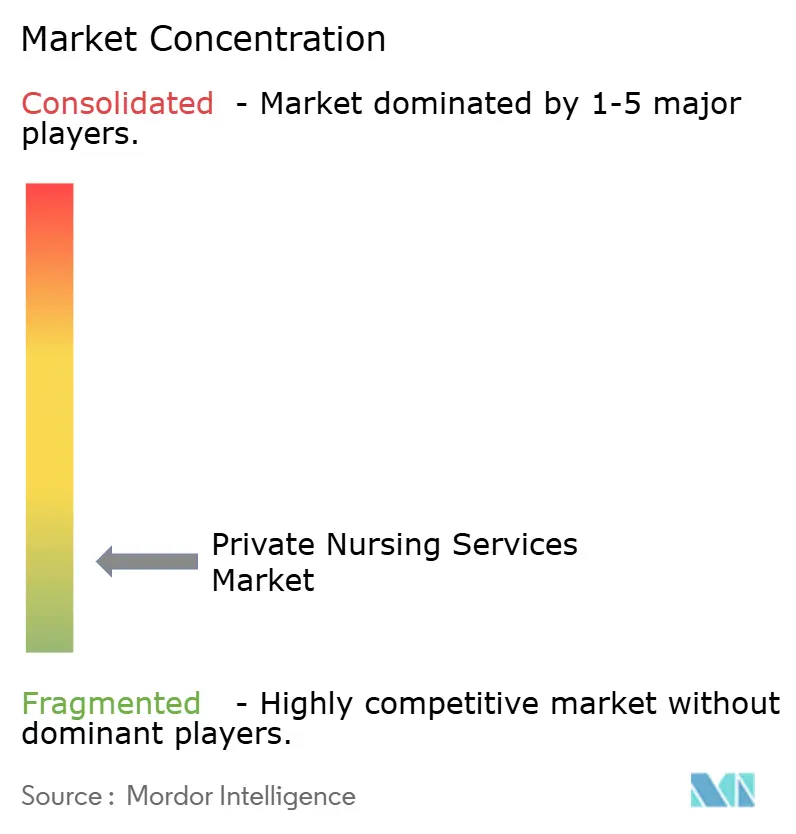

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Private Nursing Services Market Analysis by Mordor Intelligence

The Private Nursing Services Market size is estimated at USD 53.71 billion in 2026, and is expected to reach USD 73.68 billion by 2031, at a CAGR of 6.53% during the forecast period (2026-2031).

Momentum reflects a decisive shift from volume-based reimbursement toward value-oriented, home-centered models that let payers trim episode costs by up to 50% without eroding clinical results.[1]Centers for Medicare & Medicaid Services, “CY 2025 Home Health Prospective Payment Update,” cms.gov Longer lifespans, a growing burden of chronic disease, and telehealth innovation continue to redraw the competitive map, encouraging providers to layer higher-acuity services such as infusion therapy and ventilator management on top of routine skilled-nursing visits. Venture funding has accelerated platform consolidation, while hospital-at-home waivers allow acute-care hospitals to subcontract at inpatient rates, creating fresh revenue streams for specialized agencies. Labor supply remains the critical constraint as wage inflation outpaces stagnant public-payor tariffs.

Key Report Takeaways

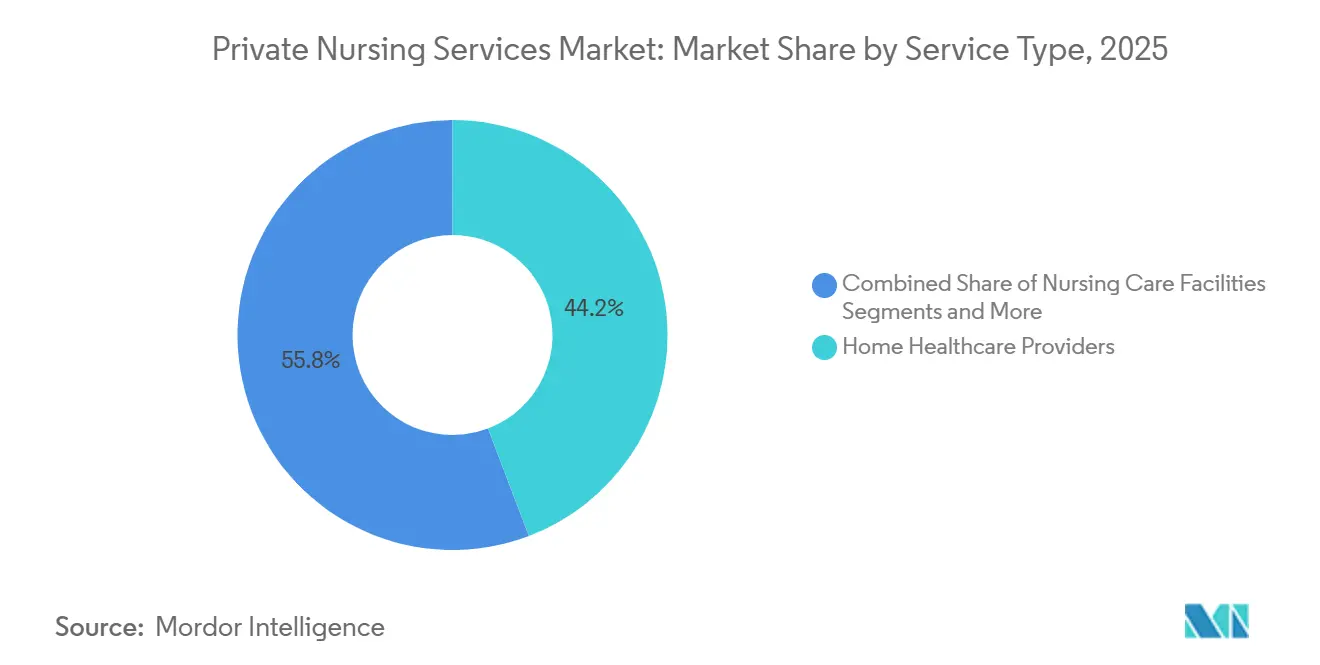

- By service type, home healthcare providers led with 44.22% revenue share in 2025, whereas other specialized private nursing services are set to grow at a 9.74% CAGR to 2031.

- By end user, the elderly segment accounted for 52.65% of demand in 2025, yet special groups are projected to expand at a 10.88% CAGR through 2031.

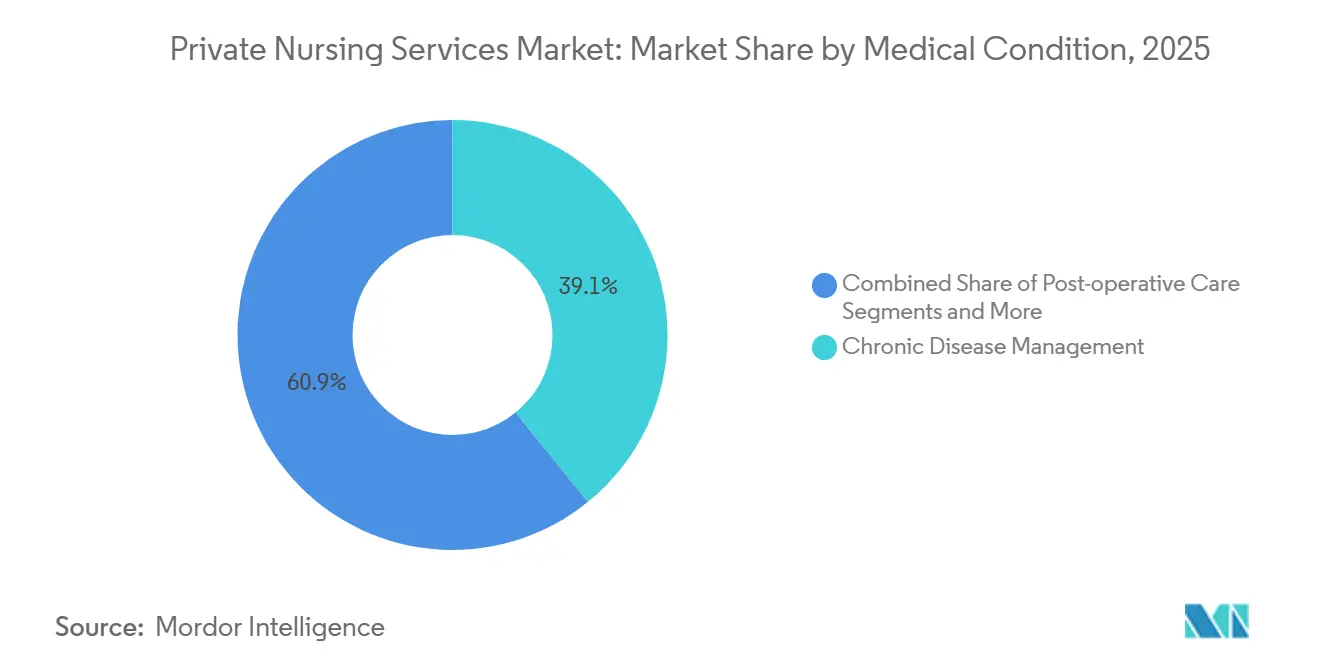

- By medical condition, chronic disease management held 39.14% of the private nursing services market share in 2025, while post-operative care is climbing at a 9.55% CAGR toward 2031.

- By payment model, insurance-covered services captured 55.23% of 2025 revenue, but subscription-based packages are advancing at a 10.54% CAGR out to 2031.

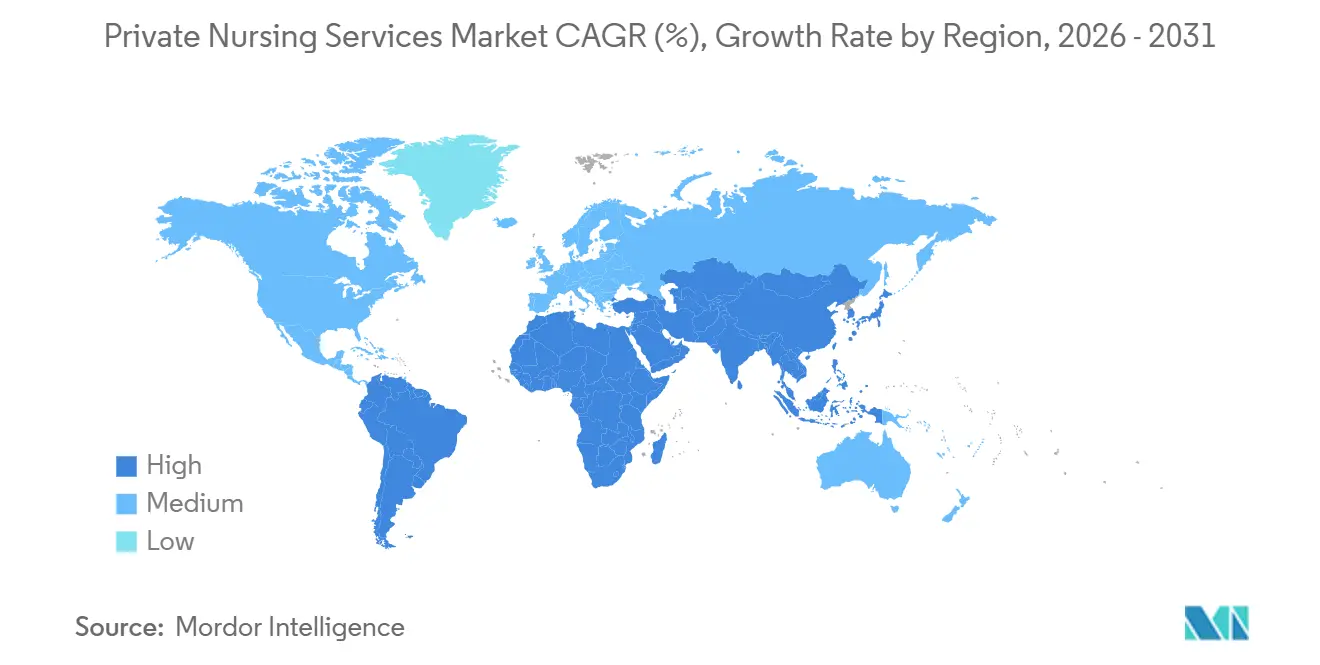

- By geography, North America commanded 36.33% of revenue in 2025, with Asia-Pacific forecast to post the quickest 8.35% CAGR over the outlook window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Private Nursing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Rising Life Expectancy | +1.8% | Global, highest in Japan, Europe, North America | Long term (≥ 4 years) |

| Escalating Chronic Disease Burden Requiring Long-Term Care | +1.5% | Global, heavy in North America and Asia-Pacific | Long term (≥ 4 years) |

| Cost Savings Versus Institutional Care for Payers | +1.2% | North America, Europe, early Asia-Pacific adopters | Medium term (2-4 years) |

| Telehealth and Remote Monitoring Enabling Higher-Acuity Home Care | +1.0% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Venture-Capital Funding of Hospital-at-Home Platforms | +0.6% | North America, select EU and Asia-Pacific hubs | Short term (≤ 2 years) |

| Employer-Sponsored Return-to-Work Recovery Programs | +0.4% | North America, Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Life Expectancy

The global cohort aged 65 and older reached 771 million in 2024 and will top 1.5 billion by 2050.[2]United Nations, “World Population Prospects 2024,” un.orgIn Japan, 29.1% of citizens were over 65 in 2024 and land scarcity keeps facility capacity tight.[3]Ministry of Health, Labour and Welfare, “Annual Report on Long-Term Care Insurance 2024,” mhlw.go.jp Home-based nurses fill the gap by supporting multigenerational households and delaying the need for institutional beds. Life expectancy climbed to 73.3 years in 2024, lengthening the frail-elderly phase that demands assistance with daily living. Together, these trends underpin durable expansion of the private nursing services market as families and payers favor aging in place.

Escalating Chronic Disease Burden Requiring Long-Term Care

Noncommunicable illnesses cause 74% of global deaths, and 828 million adults live with diabetes, 445 million of whom lack treatment. Six in ten U.S. adults have at least one chronic condition, and four in ten live with two or more. Private nursing teams provide medication management, wound care, and biometric checks that stave off repeated emergency visits. Medicare Advantage plans now cover up to 60 home-nursing visits per year, giving the segment a stable reimbursement lane. Similar benefit expansion is appearing in Canada, Germany, and Australia.

Cost Savings Versus Institutional Care for Payers

Hospital-at-home programs trimmed 30-day spending by 38% relative to standard inpatient episodes in 2024, while readmission fell 25%. Medicaid budgets in Oregon and Washington shifted funds from nursing homes to home- and community-based services, cutting per-member costs by up to 60%. Private employers mimic the model, underwriting two-week post-surgery nursing packages that hasten return to work. As a result, payers view the private nursing services market as a lever for bending the medical cost curve.

Telehealth and Remote Monitoring Enabling Higher-Acuity Home Care

The FDA cleared 87 remote-monitoring devices in 2024, broadening the clinical toolkit for nurses who supervise patients at home. CMS kept pandemic-era telehealth flexibilities through 2025, allowing virtual medication reconciliation and care-plan updates. Sensi.AI uses passive sensors to spot falls and non-adherence, alerting nurses before complications emerge. These advances lift the acuity ceiling, letting agencies treat heart-failure or COPD flare-ups that once required skilled-nursing-facility stays.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Shortage of Licensed Nurses and Aides | −1.1% | Global, acute in North America, Europe, Japan | Long term (≥ 4 years) |

| Public-Payor Reimbursement Pressure | −0.8% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Rising Professional-Liability Insurance Premiums | −0.5% | North America, Western Europe | Short term (≤ 2 years) |

| Data-Privacy Compliance Costs for Cross-Border Records | −0.3% | European Union, United States, select Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global Shortage of Licensed Nurses and Aides

The World Health Organization warns of a 13 million-nurse shortfall by 2030, magnified by retiring baby boomers and lagging school capacity. The United States alone needs 193,100 new registered nurses each year through 2032, yet enrollment edged up only 3.1% in 2024. Japan projects a deficit of 270,000 long-term-care workers and now permits foreign caregivers, although language and credential obstacles slow deployment. Agencies hike hourly pay to USD 38 yet still trail hospital wages, forcing some to cap case volumes. Staff scarcity thus throttles the private nursing services market.

Public-Payor Reimbursement Pressure

Medicare’s Patient-Driven Groupings Model shaved 7.69% from base rates between 2020 and 2024, and only a 2.6% bump arrived for 2025. Medicaid freezes in states like California lock rates below inflation, compressing margins. The UK caps domiciliary-care tariffs at GBP 18.50 per hour, under the GBP 21 service cost, prompting exits from NHS contracts. Persistent tariff tightness forces consolidation and curbs service lines that lack supplemental private pay.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Higher-Acuity Offerings Outpace Traditional Home Health

Home healthcare providers generated 44.22% of revenue in 2025, illustrating their broad reach across nursing, therapy, and aide visits. The private nursing services market size for other specialized offerings is slated to expand at a 9.74% CAGR, the highest among service types, as infusion pumps and portable ventilators migrate into homes. Portable chemotherapy pumps with wireless monitoring let nurses administer complex regimens outside infusion centers. Nursing care facilities grow more slowly, pressured by consumer preference for aging in place. Retirement communities and group homes remain niche due to high capital requirements and limited insurance coverage. CMS hospital-at-home waivers, extended through 2025, enable hospitals to bill DRG rates and subcontract nursing at negotiated per-diems, deepening the revenue reservoir for specialized services.

Insurance parity policies reinforce this bifurcation. Group homes in Washington receive Medicaid rates 20% above individual care, attracting new builds but facing zoning pushback. In parallel, the private nursing services market share for routine home-health visits risks erosion as labor costs rise. Agencies respond by layering wound-vac dressing changes, antibiotic infusions, and ventilator weaning to command premium pricing. The strategy aligns with payer incentive to curb avoidable readmissions, sustaining revenue even as basic visit rates flatten.

By End User: Special Groups Gain Momentum

The elderly held 52.65% of 2025 revenue, anchored by age-linked conditions like osteoarthritis and dementia. However, special groups—disabled individuals and palliative patients—are set to grow 10.88% per year through 2031. Rising disability prevalence, at 1.3 billion globally, drives demand for cognitive and mobility support. Medicare hospice enrollment reached 1.72 million in 2024, with 98% of care delivered at home, underscoring the appeal of familiar surroundings.

Adults aged 18-64 represent a smaller slice of the private nursing services market but serve strategic hospital-at-home referrals for orthopedic surgery and bariatric care. Children remain the smallest cohort, yet Medicaid programs in Texas and Florida now cover up to 16 hours per day of pediatric skilled nursing, pushing premium reimbursement that bolsters agency margins. Across segments, subscription bundles that mix nursing with telehealth triage support caregivers who juggle work and family responsibilities.

By Medical Condition: Post-Operative Episodes Accelerate

Chronic disease management captured 39.14% of 2025 revenue, fueled by diabetes, hypertension, and heart failure. The private nursing services market size for post-operative care is projected to advance at a 9.55% CAGR, the fastest among conditions, as enhanced-recovery protocols discharge patients earlier. A 2024 JAMA Surgery study reported 3.2% 30-day readmissions for home-managed hip replacements versus 5.8% under inpatient care, validating the model. Geriatric-dementia programs scale as cognitive impairment rises to 78 million cases by 2030. Pediatric skilled nursing commands high rates due to ventilator dependence and gastrostomy care.

Medicare Advantage contracts often tie shared-savings bonuses to readmission reduction. Agencies install remote-monitoring kits that flag vital-sign drift, allowing early nurse intervention. By integrating telehealth and in-person care, providers stretch workforce capacity without sacrificing outcomes, an approach that strengthens the private nursing services market share of chronic-care bundles.

By Payment Model: Subscriptions Offer Predictability

Insurance covered 55.23% of revenue in 2025, spanning Medicare, Medicaid, and commercial plans. Subscription packages, priced on a per-member-per-month basis, are on track for a 10.54% CAGR. Aetna and Cigna launched riders at USD 40–60 per month for up to 40 nursing hours annually, targeting high-deductible enrollees. Direct-to-consumer platforms sell USD 200–500 tiers that blend nursing, aide support, and 24/7 phone triage.

Fee-for-service and out-of-pocket spending persists in markets with limited insurance, such as Mexico and India, where families pay cash to bypass long waitlists. Employer-funded bundles are widening in scope, covering quarterly nurse visits for chronic-condition workers to blunt medical trend. As capitated models spread, providers assume utilization risk yet gain revenue predictability.

Geography Analysis

North America generated 36.33% of 2025 revenue. CMS raised the home-health base rate 2.6% for 2025, a modest offset against 12% labor-cost growth since 2020. Canada expanded provincial budgets, while nursing shortages still limit visit volume in rural zones. Mexico’s private insurance penetration hit 8.2% in 2024, creating a fledgling affluent segment.

Asia-Pacific grows at 8.35% through 2031, propelled by Japan’s super-aged demographic and 13,400 visiting-nurse stations. China’s 2024 guidelines allow foreign joint ventures to own 70% of nursing agencies, though reimbursement remains urban-skewed. India’s market is metro-centric, hampered by sub-2% insurance coverage. Australia redirected AUD 4.9 billion to in-home packages in 2024, supporting 275,000 seniors.

Europe exhibits mixed dynamics. Germany, France, and the UK reimburse domiciliary nursing but cap tariffs, pushing providers to private-pay niches. Spain and Italy expand budgets yet delay payments. Brazil leads South America on the back of 25% private-health coverage, but currency swings blur ROI. Gulf Cooperation Council states license private agencies under Vision 2030, while workforce pipelines rely on expatriate nurses. South Africa’s urban private market serves only 17% of citizens due to limited medical-scheme enrollment.

Competitive Landscape

The private nursing services market features moderate fragmentation. UnitedHealth Group closed its USD 3.3 billion Amedisys deal in March 2024, forming the largest U.S. home-health network and capturing downstream savings via managed-care integration. Vesta Healthcare channels its USD 65 million raise into predictive analytics that flag decompensation before hospital admission.

Regional agencies compete on cultural alignment and language services but wrestle with wage inflation. AI-enabled platforms like Sensi.AI let one nurse manage an expanded census, bolstering margins. Compliance requirements grew in 2024; CMS Conditions of Participation now demand patient-specific infection-control and competency-based training, favoring operators with robust quality infrastructure. Niche white-space persists in pediatric skilled nursing, where Medicaid pays premiums, and in concierge subscriptions for affluent seniors seeking rapid access.

Private Nursing Services Industry Leaders

The Ensign Group Inc.

Amedisys Inc.

UnitedHealth Group (LHC Group)

BAYADA Home Health Care

AccentCare Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: CMS allocated USD 75 million for tuition reimbursement and training programs aimed at bolstering nursing-home staff competencies.

- July 2025: Homewatch CareGivers announced a clinical expansion with a dedicated nursing services vertical supported by hospital partnerships.

- March 2025: Click Holdings acquired a 25% stake in a Hong Kong nursing-care competitor with a 9,000-person talent pool, reinforcing its healthcare HR presence.

Global Private Nursing Services Market Report Scope

Private nursing services are defined as personalized, one-on-one skilled nursing care provided by Registered Nurses (RNs) or Licensed Practical Nurses (LPNs) in a patient's home or preferred setting. These services offer continuous support beyond typical hospital care, addressing medical needs such as medication management, wound care, and chronic condition oversight, while fostering greater independence and comfort for patients.

The Private Nursing Services Market Report is segmented by Service Type, End User, Medical Condition, Payment Model, and Geography. By Service Type, the market is segmented into Retirement Communities, Group Care Homes, Nursing Care Facilities, Home Healthcare Providers, and Other Specialised Private Nursing Services. By End User, the market is segmented into Children, Adults, Elderly, and Special Groups. By Medical Condition, the market is segmented into Chronic Disease Management, Post-operative Care, Geriatric/Dementia Care, Pediatric Skilled Nursing, and Palliative & Hospice. By Payment Model, the market is segmented into Insurance-Covered Services, Subscription-Based Packages, Fee-for-Service/Out-of-Pocket, and Other. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Retirement Communities |

| Group Care Homes |

| Nursing Care Facilities |

| Home Healthcare Providers |

| Other Specialised Private Nursing Services |

| Children |

| Adults |

| Elderly |

| Special Groups (Disabled, Palliative) |

| Chronic Disease Management |

| Post-operative Care |

| Geriatric / Dementia Care |

| Pediatric Skilled Nursing |

| Palliative & Hospice |

| Insurance-Covered Services |

| Subscription-Based Packages |

| Fee-for-Service / Out-of-Pocket |

| Other (Employer, Charity, Govt Grants) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Retirement Communities | |

| Group Care Homes | ||

| Nursing Care Facilities | ||

| Home Healthcare Providers | ||

| Other Specialised Private Nursing Services | ||

| By End User | Children | |

| Adults | ||

| Elderly | ||

| Special Groups (Disabled, Palliative) | ||

| By Medical Condition | Chronic Disease Management | |

| Post-operative Care | ||

| Geriatric / Dementia Care | ||

| Pediatric Skilled Nursing | ||

| Palliative & Hospice | ||

| By Payment Model | Insurance-Covered Services | |

| Subscription-Based Packages | ||

| Fee-for-Service / Out-of-Pocket | ||

| Other (Employer, Charity, Govt Grants) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the private nursing services market?

The market stands at USD 53.71 billion in 2026.

How fast is Asia-Pacific growing?

Asia-Pacific is projected to register an 8.35% CAGR through 2031.

Which service type is expanding the quickest?

Other specialized private nursing services, including infusion therapy and ventilator management, are advancing at a 9.74% CAGR.

Why are subscriptions gaining traction?

They offer predictable monthly costs and align provider incentives with utilization control, growing at a 10.54% CAGR.

What limits overall market expansion?

A global shortage of nurses, estimated at 13 million by 2030, constrains capacity and raises labor costs.

How does hospital-at-home impact costs?

CMS data show hospital-at-home programs reduce 30-day episode spending by 38% compared with traditional inpatient stays.

Page last updated on: