Healthcare Management Service Organization Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

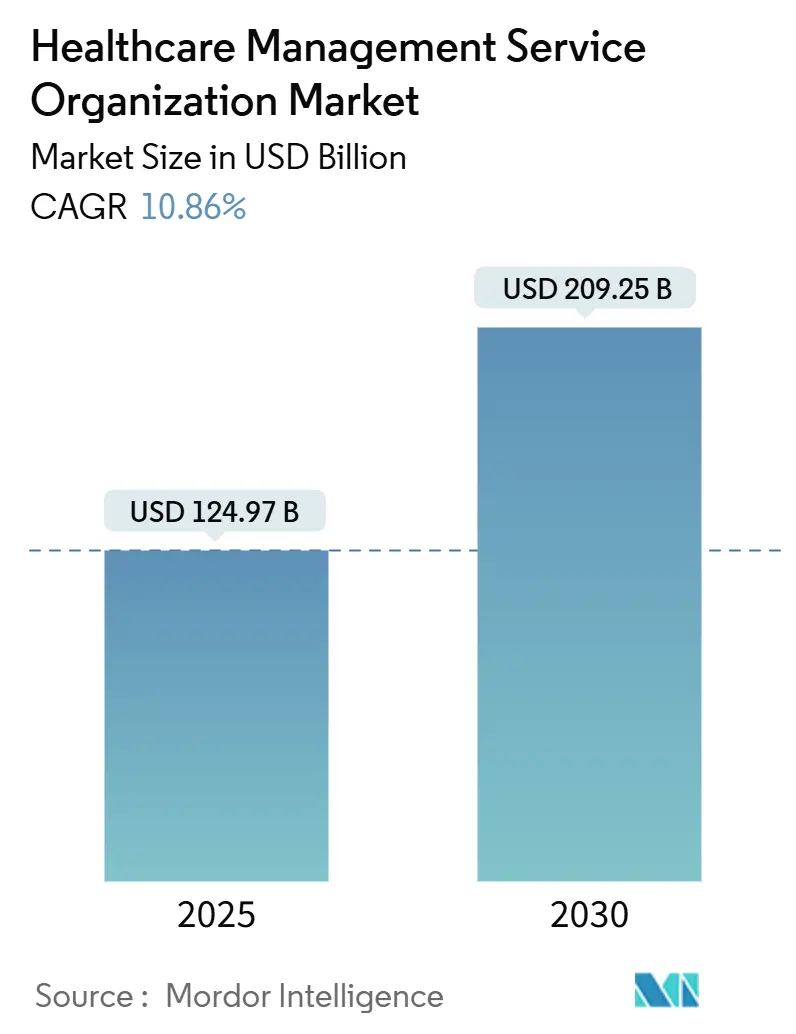

| Market Size (2025) | USD 124.97 Billion |

| Market Size (2030) | USD 209.25 Billion |

| Growth Rate (2025 - 2030) | 10.86% CAGR |

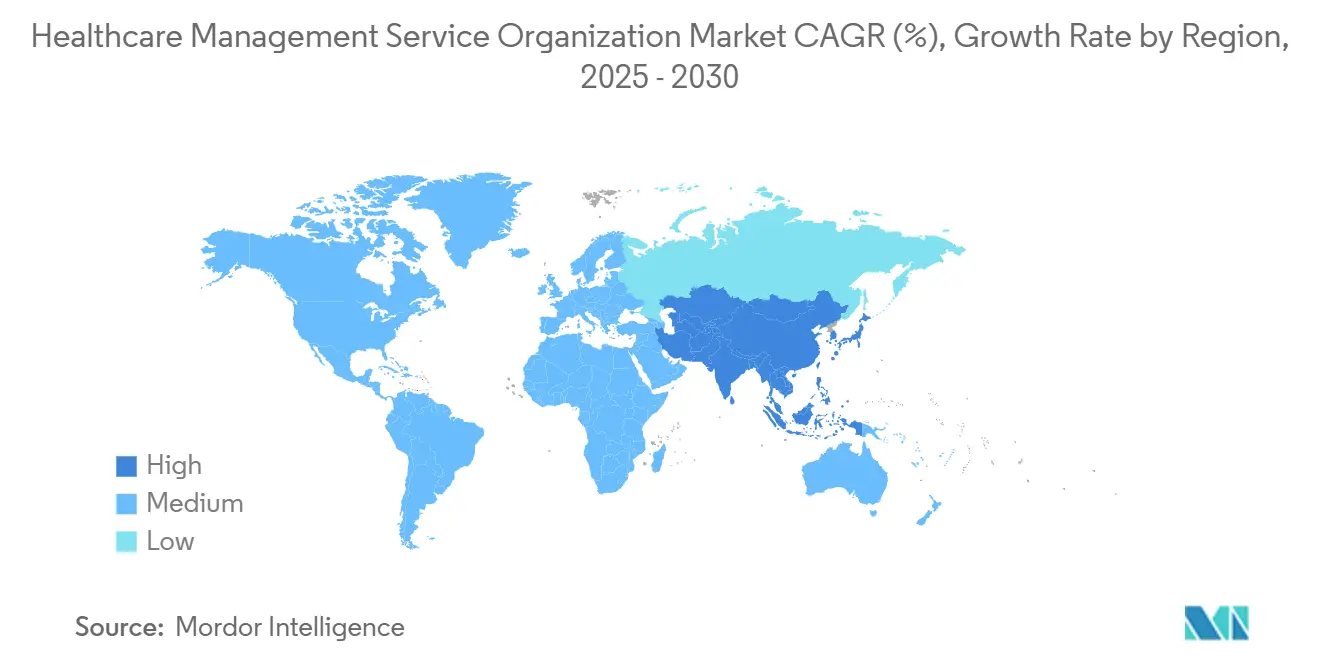

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Management Service Organization Market Analysis by Mordor Intelligence

The Healthcare Management Service Organization market size stood at USD 124.97 billion in 2025 and is set to advance to USD 209.25 billion by 2030, translating into a 10.86% CAGR over the forecast period. Demand accelerates as physician groups migrate from fee-for-service toward value-based contracts that reward quality, cost efficiency and risk management. Private-equity funding fuels consolidation, data-driven platforms shorten revenue-cycle cash lags, and regulatory pay raises for frontline staff amplify the need to outsource non-clinical tasks. North America preserves its lead owing to Medicare Shared Savings Program expansion, while Asia-Pacific gains pace on infrastructure upgrades and pro-innovation policies. Competitive intensity rises around AI-enabled denial prevention, specialty-focused operating models and compliance services that guard against corporate practice of medicine violations.

Key Report Takeaways

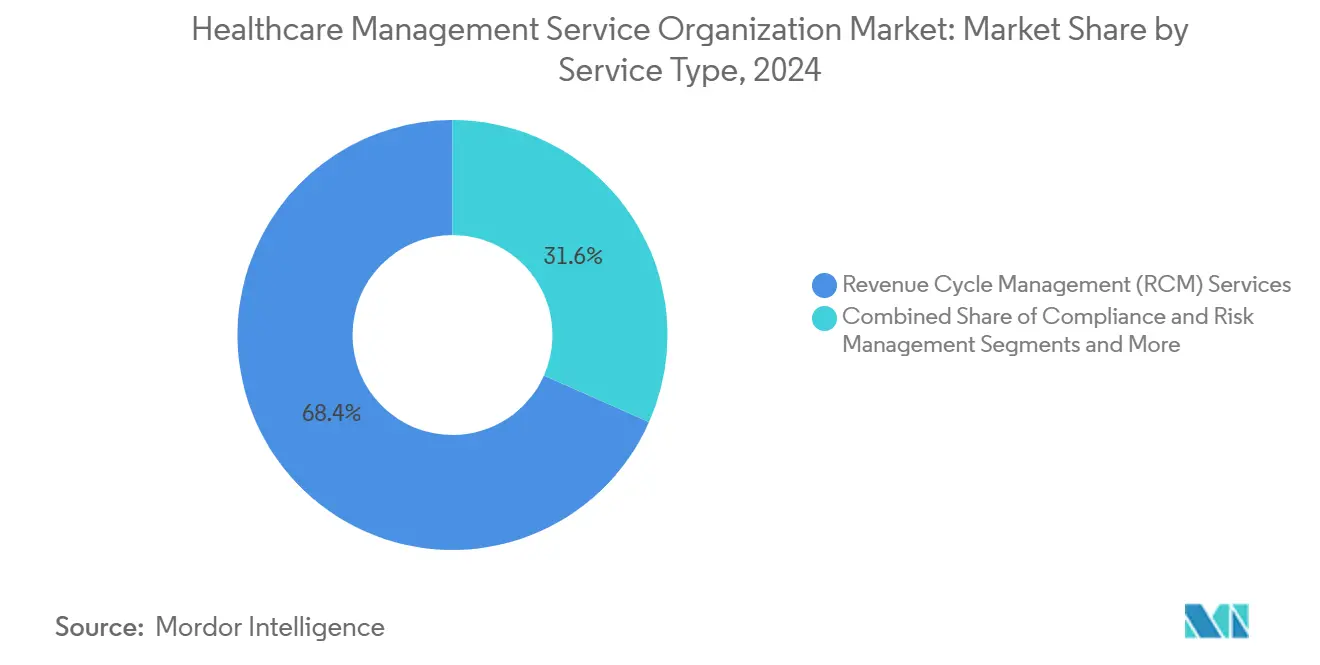

- By service type, revenue-cycle management led with 68.36% share in 2024; AI-enabled denial management posted an 11.23% CAGR to 2030.

- By ownership model, private-equity-backed MSOs held 39.58% of the Healthcare Management Service Organization market share in 2024 while scaling at an 11.74% CAGR through 2030.

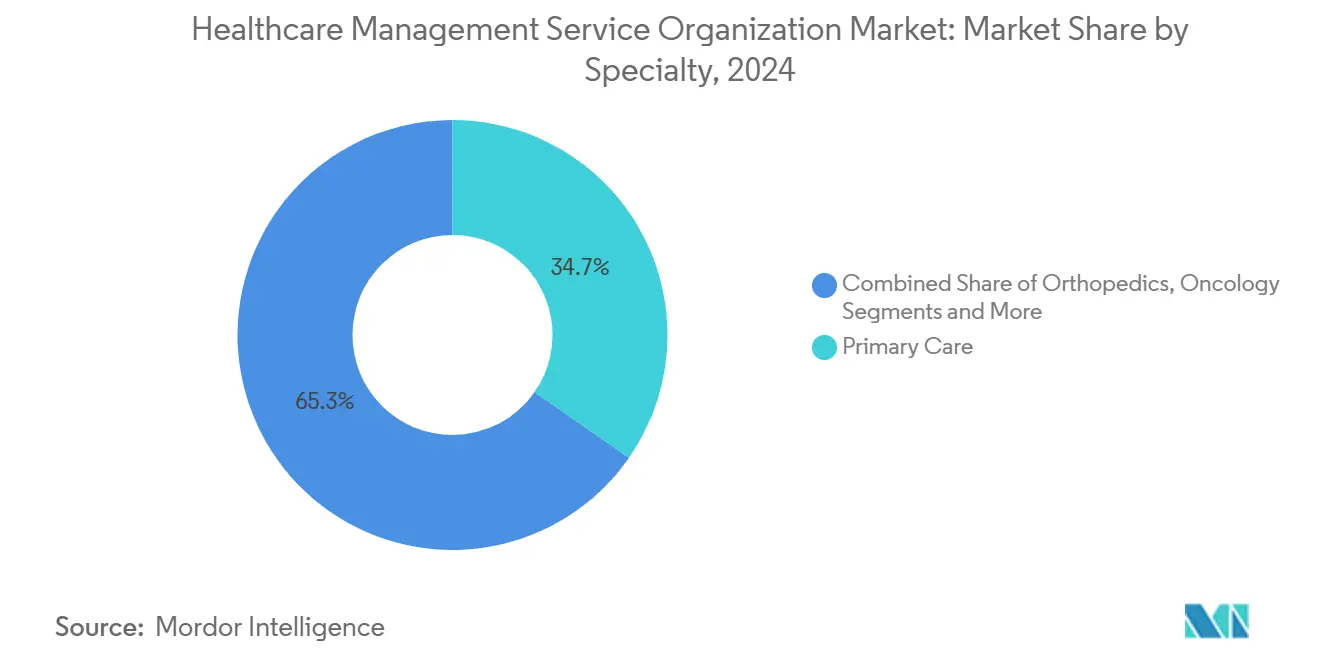

- By specialty, primary care accounted for 34.67% of the Healthcare Management Service Organization market size in 2024; orthopedics is projected to expand at a 9.46% CAGR through 2030.

- By practice size, medium practices captured 43.55% share in 2024, whereas large practices are forecast to grow at a 10.78% CAGR.

- By geography, North America retained 49.77% share in 2024 while Asia-Pacific is expected to register the highest 9.62% CAGR through 2030.

Global Healthcare Management Service Organization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost pressure driving outsourcing of administrative tasks | +2.1% | Global, highest in North America & Europe | Medium term (2-4 years) |

| Transition to value-based care models requiring analytics & RCM expertise | +2.8% | North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing physician-practice consolidation & private-equity investment | +1.9% | North America & Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| AI-driven proactive denial-management platforms within MSOs | +1.7% | Global, led by North America | Medium term (2-4 years) |

| Accreditation-driven specialty-specific MSO models | +1.2% | North America & Europe | Long term (≥ 4 years) |

| Telehealth & remote-patient-monitoring integration expanding MSO service scope | +1.4% | Global, accelerated post-pandemic adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost Pressure Driving Outsourcing Of Administrative Tasks

Nursing wages will rise 4% in 2025 after California mandated a USD 25 minimum wage for healthcare workers, a policy shift that tightens margins for independent groups. Leaders rank workforce costs as their top operational challenge, driving practices to partner with MSOs that pool billing, scheduling and supply-chain services at scale. Shared service centers lower fixed overhead, preserve physician autonomy and ensure compliance with state wage laws. The Healthcare Management Service Organization market responds by bundling HR, revenue-cycle and procurement on subscription models that adjust with patient volume. As labor inflation persists, outsourced administrative support becomes non-discretionary, reinforcing double-digit service adoption.

Transition To Value-Based Care Models Requiring Analytics & RCM Expertise

The Medicare Shared Savings Program expanded to 480 ACOs serving 10.8 million beneficiaries in 2024.[1]CMS Press Office, “CY 2025 Medicare Physician Fee Schedule Final Rule – Medicare Shared Savings Program Provisions,” Centers for Medicare & Medicaid Services, cms.gov New health-equity benchmarks and prepaid savings options introduced in 2025 raise data-tracking complexity that small practices cannot shoulder alone. MSOs step in with cloud analytics, risk stratification and quality reporting that link clinical and financial indicators in near real time. Their tools capture new HCPCS codes under Advanced Primary Care, helping physicians qualify for bonus pools. As payers shift more dollars into two-sided risk, MSOs that fuse care-coordination software with predictive revenue-cycle engines gain sticky multiyear contracts. This evolution cements the Healthcare Management Service Organization market as the operational backbone for value-based business lines.

Increasing Physician-Practice Consolidation & Private-Equity Investment

Private-equity acquisitions of physician groups climbed over 10 years. Fresh capital finances multi-state roll-ups where MSOs standardize coding, procurement and IT across hundreds of sites. Astrana Health’s USD 745 million purchase of Prospect Health added 610,000 members, illustrating how scale economics reward firms with turnkey management systems. Yet some regulators push back: Oregon’s Senate Bill 951 now limits non-physician control of clinical decisions, spurring MSOs to craft governance models that preserve doctor autonomy. This balanced positioning widens the addressable base of practices that reject outright sale but still need enterprise infrastructure.

AI-Driven Proactive Denial-Management Platforms Within MSOs

Claim-denial rates jumped to 11% in 2024, costing providers USD 19.7 billion to dispute.[2]Todd Shryock, “Revolutionizing Denials Management With Artificial Intelligence,” Medical Economics, medicaleconomics.com Nearly half of hospitals have already embedded AI in revenue-cycle workflows to cut average payment lags from 90 days to 40 days.[3]Paul Barr, “3 Ways AI Can Improve Revenue-Cycle Management,” American Hospital Association, aha.org MSOs deploy machine-learning models that flag high-risk claims pre-submission, auto-populate prior-authorization forms and orchestrate intelligent appeals. Savings free up clinical capital for population-health initiatives, and reduced burnout keeps billing staff turnover down. These differentiated capabilities underpin the fastest-growing revenue stream in the Healthcare Management Service Organization market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory scrutiny over CPOM & anti-kickback compliance | -1.8% | North America primary, state-level variations | Long term (≥ 4 years) |

| Data-privacy & cybersecurity risks in outsourced systems | -1.3% | Global, heightened in regulated markets | Medium term (2-4 years) |

| Labor-cost inflation eroding MSO margin advantage in high-wage regions | -1.1% | North America & Europe, urban centers | Short term (≤ 2 years) |

| Physician skepticism toward third-party ownership models causing contractual churn | -0.9% | North America, emerging elsewhere | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny Over CPOM & Anti-Kickback Compliance

Oregon’s new law requires physician majority ownership of practices and curtails MSO influence over clinical judgment. California courts now question the “friendly PC” model that lets management firms control finances and staffing. Federal OIG guidance published in 2025 mandates documented risk audits, billing integrity reviews and whistle-blower hotlines for outsourced vendors. Compliance costs rise, slowing multi-state expansion and prompting MSOs to invest in specialized legal, audit and governance functions.

Data-Privacy & Cybersecurity Risks In Outsourced Systems

Healthcare registered 677 major breaches in 2024, exposing 182.4 million records; one-third originated from business associates such as MSOs. The WPS MAC breach alone compromised nearly 950,000 Medicare beneficiaries through MOVEit transfer software. Insurers and providers now demand zero-trust architectures, AI-driven threat analytics and cyber-risk sharing clauses. For MSOs, enhanced security spend trims operating margins until new fee models recoup costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Revenue-cycle platforms anchor growth and cross-sell breadth

Revenue-cycle management accounted for 68.36% of the Healthcare Management Service Organization market share in 2024, reflecting provider urgency to protect margins amid 11% denial rates and USD 19.7 billion in appeal costs. AI-enabled denial surveillance within this line is forecast to log an 11.23% CAGR through 2030, outpacing every other service bucket. Contractually bundled modules now add charge-capture audits, contract-modeling and patient-payment plans, widening wallet share and reducing vendor sprawl at the practice level.

Practice & operations, compliance-risk, IT/EHR-cybersecurity, staffing and supply-chain services together form the remainder of the Healthcare Management Service Organization market size and ride the same outsourcing wave triggered by nurse-wage inflation and 677 cyber breaches logged in 2024. Workforce management subscriptions mitigate 4% annual wage hikes, while zero-trust security overhauls assuage payer audit requirements. The cross-sell cadence positions diversified vendors to defend price as one-stop partners in administrative resilience.

By Ownership Model: Private-equity platforms command capital but face policy headwinds

Private-equity-backed organizations held 39.58% of Healthcare Management Service Organization market share in 2024 and project an 11.74% CAGR, financed by roll-up leverage and multi-state technology deployment. Large buys such as Astrana Health’s USD 745 million Prospect Health deal illustrate scale-seeking capital flows that rapidly extend analytics and contracting platforms.

Physician-owned, hospital-affiliated and payer-backed MSOs divide the balance of the Healthcare Management Service Organization market size, each emphasizing distinct value levers. Doctor-controlled models stress clinical autonomy—a theme amplified by Oregon’s CPOM statute—while hospital systems integrate MSOs to steady declining facility margins. Payer-led entrants, such as Wellvana’s CVS acquisition, harness claims data to steer total-cost contracts. Long-run share trajectories will hinge on governance transparency and the ability to co-manage downside risk without triggering state anti-kickback alarms.

By Specialty: Primary-care scale meets orthopedic acceleration

Primary care generated 34.67% of the Healthcare Management Service Organization market size in 2024, buoyed by 480 Medicare Shared Savings ACOs covering 10.8 million lives and new HCPCS codes under Advanced Primary Care. The segment’s depth supplies predictable patient panels that underpin long-term MSO contracts tied to quality bonuses and two-sided risk pools.

Orthopedic MSOs headline growth at a 9.46% CAGR, leveraging bundled-payment accreditation and implant cost transparency to unlock payer premiums. Oncology, gastroenterology and behavioral health follow, each demanding specialized coding, registry reporting and outcomes analytics. Specialty diversification hedges reimbursement volatility and amplifies cross-referral synergies, lifting aggregate Healthcare Management Service Organization market share captured by multi-line vendors.

By Practice Size: Medium groups dominate today; large groups scale fastest

Medium practices with 6–25 physicians controlled 43.55% of Healthcare Management Service Organization market share in 2024, balancing resource depth with nimble governance to adopt full-suite outsourcing. They typically start with revenue-cycle modules before layering compliance, HR and EHR optimization, producing stable multi-year renewals.

Large practices above 26 physicians are projected to expand at a 10.78% CAGR through 2030 as scale economics favor centralized analytics and population-health engines. Solo and micro practices remain cost-sensitive but purchase modular RCM and telehealth support to stay independent. Vendor pricing tiers and cloud delivery lower entry barriers, ensuring each size band remains addressable within the overarching Healthcare Management Service Organization market size narrative.

Geography Analysis

North America maintained 49.77% share in 2024, propelled by CMS innovation models, sophisticated payer mix and the deepest pool of private-equity capital. Oregon’s CPOM restrictions and California’s wage mandates compel MSOs to tailor governance and labor strategies by state, yet Medicare’s ACO framework still underwrites robust service demand.

Europe exhibits slower aggregate growth but benefits from e-health interoperability and mature single-payer datasets that streamline analytics deployment. MSOs partner with local physician cooperatives to navigate Germany’s statutory insurance coding, the UK’s NHS procurement rules and France’s CPAM reporting standards. Brexit-related uncertainty complicates cross-border delivery in the UK–EU corridor, nudging vendors toward country-specific licenses.

Asia-Pacific records the fastest 9.62% CAGR as China, India and Australia inject funding into digital health and preventive-care networks. Global insurers establish remote monitoring ecosystems, boosting demand for MSOs that can localize workflow in Mandarin, Hindi or Japanese. Regional policy experimentation—from Japan’s dementia-care budget incentives to India’s Ayushman Bharat reimbursement expansion—creates new risk pools addressable only through scalable back-office infrastructure.

Competitive Landscape

The Healthcare Management Service Organization market hosts a mix of multibillion-dollar conglomerates and niche specialists. Optum Health’s USD 105.4 billion services revenue in 2024 underscores the advantage of integrating analytics, pharmacy and care delivery under one roof. Kaiser Permanente’s Risant Health unit acquired Cone Health to add 1,100 beds and widen its managed-care footprint.

Mid-tier players pursue technology partnerships; athenahealth embeds AI scribes and coding APIs that dovetail with MSO billing engines. New entrants monetize specialty niches, such as behavioral-health networks that integrate remote therapy and analytics for social-determinants risk scoring. As AI and cybersecurity requirements inflate R&D budgets, inorganic consolidation is likely to intensify, with acquirers targeting interoperable platforms and robust compliance cultures.

Competitive moves center on: 1) horizontal mergers that bundle RCM, staffing and IT, 2) vertical tie-ups between payers and provider groups, and 3) cloud-native startups that lower onboarding time for small practices. MSOs able to prove tangible cash-flow uplift and regulatory risk mitigation sustain pricing power in an otherwise price-sensitive environment.

Healthcare Management Service Organization Industry Leaders

UnitedHealth Group

R1 RCM

Privia Health

Agilon Health

Conifer Health Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: NeueHealth agreed to go private via USD 1.3 billion acquisition by a New Enterprise Associates affiliate.

- December 2024: Kaiser Permanente’s Risant Health closed its purchase of Cone Health, adding 1,100 beds across North Carolina.

- November 2024: Astrana Health signed a definitive USD 745 million deal to acquire Prospect Health, absorbing 610,000 members.

Global Healthcare Management Service Organization Market Report Scope

| Revenue Cycle Management (RCM) Services |

| Practice & Operations Management |

| Compliance & Risk Management |

| IT / EHR & Cybersecurity Services |

| Staffing & HR Support |

| Supply-Chain & Procurement |

| Physician-Owned MSOs |

| Hospital-Affiliated MSOs |

| Private-Equity-Backed MSOs |

| Payer-Backed MSOs |

| Primary Care |

| Orthopedics |

| Oncology |

| Gastroenterology |

| Behavioral Health |

| Multispecialty & Other |

| Solo / Small (1-5 physicians) |

| Medium (6-25 physicians) |

| Large (26+ physicians) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Revenue Cycle Management (RCM) Services | |

| Practice & Operations Management | ||

| Compliance & Risk Management | ||

| IT / EHR & Cybersecurity Services | ||

| Staffing & HR Support | ||

| Supply-Chain & Procurement | ||

| By Ownership Model | Physician-Owned MSOs | |

| Hospital-Affiliated MSOs | ||

| Private-Equity-Backed MSOs | ||

| Payer-Backed MSOs | ||

| By Specialty | Primary Care | |

| Orthopedics | ||

| Oncology | ||

| Gastroenterology | ||

| Behavioral Health | ||

| Multispecialty & Other | ||

| By Practice Size | Solo / Small (1-5 physicians) | |

| Medium (6-25 physicians) | ||

| Large (26+ physicians) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Healthcare Management Service Organization market in 2025?

It is valued at USD 124.97 billion with a forecast to reach USD 209.25 billion by 2030.

Which service line dominates outsourced MSO contracts?

Revenue-cycle management leads with 68.36% share, propelled by AI denial-prevention engines that shorten payment cycles.

Why are private-equity-backed MSOs growing fastest?

Access to capital enables rapid acquisitions and investment in analytics platforms, supporting an 11.74% CAGR through 2030.

Which specialty offers the quickest growth opportunity for MSOs?

Orthopedics, benefiting from bundled-payment accreditation and implant cost controls, is expected to post a 9.46% CAGR.

What is the chief regulatory risk facing MSOs in North America?

State-level corporate practice of medicine laws, such as Oregon’s Senate Bill 951, that limit non-physician control of clinical decisions.

How are cyber threats influencing MSO procurement decisions?

Record breach volumes have pushed providers to demand zero-trust architectures and contract clauses that transfer part of the cyber-risk to vendors.

Page last updated on: