Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

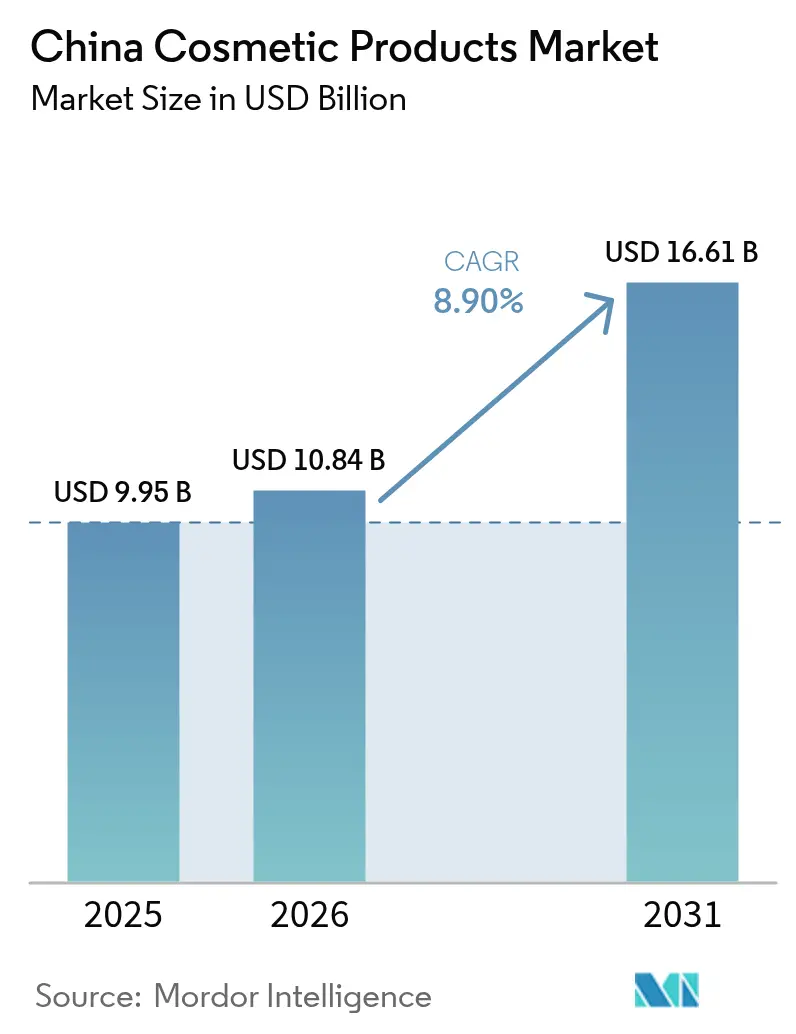

| Base Year Market Size (2025) | USD 9.95 Billion |

| Market Size (2026) | USD 10.84 Billion |

| Market Size (2031) | USD 16.61 Billion |

| Growth Rate (2026 - 2031) | 8.90% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Cosmetic Products Market Analysis by Mordor Intelligence

The China cosmetic products market size was valued at USD 9.95 billion in 2025 and estimated to grow from USD 10.84 billion in 2026 to reach USD 16.61 billion by 2031, at a CAGR of 8.9% during the forecast period (2026-2031). This growth is driven by enhanced digital engagement, rising incomes in smaller cities, and regulatory initiatives aimed at improving product standards. Increasing disposable incomes, particularly among the middle class, are enabling more consumers to purchase premium beauty and personal care products. Consumers are demonstrating a growing willingness to invest in skincare, makeup, and personal grooming. The premiumization trend is gaining momentum as consumers prioritize efficacy, safety, and brand authenticity. Online channels are leading growth, with live-stream commerce and short-video platforms converting social media impressions into rapid purchases and facilitating record-speed new product launches.

Key Report Takeaways

- By product type, facial cosmetics dominated with a 50.92% revenue share in 2025, while lip and nail make-up is projected to grow at a 9.95% CAGR to 2031.

- By category, mass products captured 69.12% of the Chinese cosmetic products market share in 2025, while premium products are expected to grow at a 10.1% CAGR through 2031.

- By ingredient type, conventional ingredients represented 73.10% of 2025 revenue, though natural/organic formulations will experience the fastest growth at an 10.75% CAGR.

- By distribution channel, online retail stores accounted for 54.05% of the Chinese cosmetic products market size in 2025 and are growing at an 11.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Influence of social media platforms | +1.7% | Nationwide | Short term (≤ 2 years) |

| Surge in premium facial products | +1.0% | Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Consumer focus on anti-aging products | +0.9% | Nationwide | Long term (≥ 4 years) |

| Adoption of k-beauty and j-beauty cosmetic products | +0.3% | Coastal provinces | Medium term (2-4 years) |

| Rising disposable income boosts cosmetic purchases | +0.4% | Nationwide | Long term (≥ 4 years) |

| Increased urbanization drives demand for cosmetics | +0.2% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Influence of social media platforms

The widespread adoption of smartphones has significantly enhanced the functionality and accessibility of social media. In December 2024, mobile phone shipments in China rose by 22.1% year-on-year, reaching approximately 34.53 million units, as reported by the China Academy of Information and Communications Technology (CAICT) [1]Source: China Academy of Information and Communications Technology (CAICT), "China's mobile phone shipments," china.org.cn. Live-streaming and short-video platforms have transformed into comprehensive storefronts with integrated checkout systems. Consumers now spend an average of 8 hours per week on social networks, with nearly 10% of domestic e-commerce orders originating from live-stream sessions. Influencers with millions of followers frequently drive product sell-outs within hours of launch. In response, beauty brands are increasingly investing in collaborations with Key Opinion Leaders (KOLs) and leveraging real-time analytics. This approach ensures that creative assets remain aligned with rapidly changing internet trends. As a result, a feedback loop is established, enabling data-driven product adjustments to effectively capture market sentiment and guide subsequent launches. This strategy not only accelerates innovation cycles but also strengthens brand loyalty.

Surge in premium facial products

China's premium cosmetics market is set for substantial growth, with a projected CAGR of 10.64% from 2025 to 2030. This growth is primarily driven by a significant consumer shift toward natural ingredients, avoiding synthetic additives. Both mainstream and private-label brands are adapting to this trend, aligning their product offerings with the increasing demand for ethical and eco-friendly cosmetics. As disposable incomes rise, Chinese consumers are demonstrating a greater willingness to invest in premium products. In 2024, China's per capita disposable income reached CNY 41,314, reflecting a 5.3% increase compared to the previous year, according to the National Bureau of Statistics of China [2]Source: National Bureau of Statistics of China, "Households' Income and Consumption Expenditure in 2024," stats.gov.cn . Renowned brands such as Estée Lauder, Lancôme, and Chanel, along with domestic high-end lines like Perfect Diary’s premium offerings, are becoming more accessible. The segment's growth is further supported by leading players employing effective digital strategies to strengthen their online presence. Collaborations with influencers are increasingly prevalent, enhancing brand visibility and expanding consumer reach for both domestic and international beauty brands.

Consumer focus on anti-aging products drives the growth

China's cosmetics market is experiencing significant growth in the anti-aging segment, driven by demographic shifts and evolving consumer preferences. This trend is strongly influenced by a cultural focus on self-care, with consumers increasingly emphasizing early preventative measures for optimal outcomes. The aging population in China is a major factor contributing to this growth. According to data from the State Council of the People's Republic of China, in 2024, 310.31 million individuals aged 60 and above represented a substantial share of the country's total population [3]Source: State Council Information Office, “China's economic performance in 2024,” stats.gov.cn. Consumers are increasingly seeking makeup products that enhance a youthful appearance while avoiding issues such as settling into fine lines, wrinkles, or dull skin. This demand includes hydrating foundations and BB/CC creams formulated with anti-aging ingredients like peptides and hyaluronic acid. Technological advancements are revolutionizing delivery systems within the cosmetics market. A recent study demonstrated that ribose/collagen/decarboxy carnosine hydrochloride/palmitoyl tripeptide-1 composite nanocarriers (RCDP NCs) can achieve a dermal penetration depth of 460.0 μm within 4 hours. This innovation improves cellular absorption and delivers superior anti-aging benefits. Leading brands are leveraging this opportunity, with L'Oréal identifying the aging demographic as one of its four strategic growth priorities in the Chinese market.

Adoption of K-beauty and J-beauty cosmetic products

Chinese domestic cosmetics brands are integrating Korean and Japanese beauty principles into their product development, reshaping the country's beauty market. Chinese consumers, particularly the younger demographic, demonstrate a preference for Japanese brands due to their perceived quality and international appeal. This shift in consumer behavior reflects a broader cultural transformation in China's beauty industry, where traditional Chinese beauty practices are being blended with international influences. Local brands are adapting by incorporating Japanese skincare philosophies, such as multi-step routines and gentle formulations, alongside Korean beauty trends like innovative textures and packaging designs. The resulting hybrid approach allows Chinese brands to create products that resonate with modern consumers while maintaining their cultural identity. This market evolution has led to Chinese brands developing products that combine Korean and Japanese beauty elements while maintaining distinct Chinese characteristics, such as the use of traditional Chinese medicinal ingredients and cultural symbolism in product design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer concerns over product safety and ingredients | -0.3% | Tier-1 cities | Short term (≤ 2 years) |

| Complex supply chain management | -0.5% | Export-oriented provinces | Medium term (2-4 years) |

| Stringent regulatory environment limits growth | -0.4% | Nationwide | Medium term (2-4 years) |

| High competition among domestic and international brands | -0.5% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer concerns over product safety and ingredients

Regulatory compliance has become a critical differentiator in China's cosmetic products market. The implementation of the Cosmetic Supervision and Administration Regulation (CSAR) has established higher standards for product safety and ingredient transparency. CSAR provides a comprehensive framework for managing cosmetic products, encompassing stringent pre-market and post-market oversight, efficacy evaluations, and safety assessments. Chinese consumers are increasingly prioritizing product formulations, with a strong focus on ingredient safety and associated risks. Brands that effectively communicate their safety standards and ingredient benefits are gaining a competitive advantage, while those failing to meet these expectations face swift consumer backlash and increased regulatory scrutiny.

Complex supply chain management

China's cosmetics industry is undergoing significant transformation, contending with supply chain challenges that are redefining its competitive dynamics and operational strategies. Geopolitical tensions and increasing costs, particularly for raw materials sourced from China, are exerting substantial pressure. In response, companies are diversifying supply chains and adopting cost-management strategies, such as order consolidation and predictive analytics. In April 2025, the U.S. government imposed a 54% tariff on imports from China. This development has led to a market divide: premium brands effectively absorb these rising costs, while smaller, value-focused brands face considerable difficulties. To address these challenges, some brands are renegotiating supplier agreements and emphasizing transparency with customers. Others are exploring nearshoring and domestic production as strategic alternatives. These disruptions are accelerating a shift toward localization, providing a competitive advantage to domestic Chinese brands with well-established local supply networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Cosmetics Maintains Lead While Lip and Nail Make-up Products Surge

In 2025, facial cosmetics led the Chinese cosmetic products market, capturing 50.92% of the market share. This reflects the increasing focus on daily skincare routines and the growing popularity of multi-step regimens. Chinese consumers are increasingly adopting serums, toners, and masks that offer benefits such as hydration, brightening, and repair. Additionally, social media campaigns and hashtags play a significant role in educating consumers about these skincare practices. Domestic brands are leveraging traditional medicine by incorporating ingredients like ginseng, angelica, and snow mushroom to create differentiated products. Moreover, the lip and nail makeup segment is growing at the fastest rate in the market, with a projected CAGR of 9.95% through 2031. This growth is driven by the rising culture of self-expression, advancements in long-lasting pigments, and the popularity of hybrid products such as tinted lip balms with SPF.

The rapid growth of the lip and nail segment is further supported by live-stream haul formats, where influencers quickly showcase multiple shades, encouraging real-time purchasing decisions. Meanwhile, facial cosmetics are advancing with innovations such as booster ampoules, microbiome-friendly moisturizers, and artificial intelligence-powered skin mapping that enables personalized product bundles. In response to these trends, multinational companies are establishing local innovation centers to accelerate product development and adapt textures to regional climates and diverse skin types. These factors ensure that the China cosmetic products market remains dynamic, continuously evolving with emerging micro-trends.

By Category: Mass Dominates, Premium Compounds Growth

In 2025, mass lines contributed 69.12% of sales, driven by extensive distribution networks, competitive pricing strategies, and increased awareness of entry-level grooming products. Their penetration into lower-tier cities and rural areas strengthens the daily essentials market, offering products such as cleansing gels, basic moisturizers, and cost-effective lip colors. However, premium SKUs are projected to grow at a 10.1% CAGR through 2031, surpassing the overall market growth rate. This trend highlights the willingness of urban millennials and Gen Z consumers to invest in high-quality textures, patented active ingredients, and sophisticated brand narratives. Live-commerce platforms emphasize ingredient sourcing and clinical claims, enhancing perceived value and boosting average basket sizes.

Retailers are adopting tiered shelf strategies, combining mini-sized prestige creams with mass-market cleansers during promotional campaigns to gradually encourage up-trading among loyal customers. Cashback programs on super apps foster repeat purchases, while loyalty data enables hyper-personalized notifications. International luxury brands are focusing on niche categories such as couture makeup, while emerging Chinese prestige brands leverage culturally resonant storytelling. This dual approach supports volume growth in mainstream products and margin expansion in premium lines, diversifying revenue streams within China's cosmetic products market.

By Ingredient Type: Natural Formulations Quickening Pace

In 2025, conventional/synthetic ingredients accounted for a dominant 73.10% market share, primarily due to their cost-effectiveness and scalable production processes. However, the natural/organic segment is anticipated to grow at a robust rate of 10.75% between 2026 and 2031. Modern consumers increasingly associate "clean beauty" with health benefits, sustainability, and ethical sourcing. Retail platforms enhance product visibility by tagging SKUs with labels such as vegan, non-GMO, and eco-certifications. In response, brands are reformulating their offerings to exclude parabens, silicones, and microplastics. Furthermore, botanical extracts like peony, honeysuckle, and mulberry are gaining traction due to their traditional medicinal significance and perceived mildness.

Supply chains are undergoing transformation, shifting towards traceable farming cooperatives and environmentally friendly packaging solutions. Domestic innovators are leveraging upcycled plant waste to extract active molecules, thereby converting agricultural by-products into valuable revenue streams. On a larger scale, multinational corporations are partnering with academic institutions to validate efficacy claims through rigorous in vitro and in vivo studies. Regulatory authorities are increasingly requiring clinical evidence to substantiate marketing claims, raising industry standards and curbing greenwashing practices. This evolving regulatory environment favors scientifically validated products, reinforcing the commitment of China's cosmetics industry to transparent sourcing and measurable performance.

By Distribution Channel: Digital Commerce Firmly on Top

In 2025, online retail stores accounted for 54.05% of China's cosmetic products market and are expected to surpass offline outlets with an 11.1% CAGR from 2026 to 2031. The availability of 24/7 shopping, the widespread use of mobile payments, and personalized product recommendations drive impulse purchases and subscription renewals. These platforms go beyond convenience by integrating augmented-reality try-ons, providing one-hour doorstep deliveries in major cities, and offering Buy Now Pay Later options to streamline the purchasing process. Beauty brands are leveraging these channels by introducing online-exclusive products and strategically timing limited releases with live-streamed festivals, ensuring a dynamic and engaging digital presence.

Simultaneously, brick-and-mortar stores are adapting to changing consumer preferences. Flagship boutiques are evolving into experiential spaces, featuring skin diagnosis labs and live-streamed influencer events to create a cohesive omnichannel experience. Specialty chains are implementing a “store as warehouse” model to enable same-day order fulfillment by consolidating inventory. In smaller towns, supermarkets are establishing beauty corners staffed with dermatology advisors to build trust among first-time cosmetics buyers.

Geography Analysis

Shanghai, Beijing, Guangzhou, and Shenzhen, China's Tier-1 cities, contribute significantly to premium turnover due to their higher disposable incomes, international tourism, and dense retail networks. These cities act as innovation hubs, testing concepts such as AI skin scanners and refill-station formats. Multinational corporations frequently launch limited editions in these markets, leveraging advanced shopper feedback to optimize nationwide rollouts. Simultaneously, domestic start-ups gravitate toward these cities to access venture capital, research and developments expertise, and efficient cross-border logistics.

Conversely, Tier-2 and Tier-3 cities are experiencing the fastest growth, driven by increasing incomes and greater digital penetration. Consumers in these regions demonstrate a pragmatic approach, balancing value-seeking behavior with an interest in niche products. E-commerce bridges the gap by delivering metropolitan product assortments to remote areas. Additionally, short-video platforms enhance local engagement by incorporating dialect subtitles and region-specific beauty tips. Offline retail is also expanding, with brands like Sephora and domestic specialty retailers introducing compact store formats in provincial capitals to strengthen brand equity and provide tactile experiences unavailable online.

Free-trade zones and border cities form a distinct market segment that benefits from cross-border e-commerce through duty-free pricing and simplified customs procedures. International brands use bonded warehouses to test products and assess market demand before obtaining full import licenses. Regulatory bodies are aligning cross-border e-commerce and general trade regulations to reduce compliance differences and enhance transparency. The diverse regional markets in China require companies to carefully segment their marketing approaches and product offerings, reflecting the complex nature of the country's cosmetic products market.

Regulatory Landscape

China's cosmetics market is regulated by the National Medical Products Administration (NMPA). The Cosmetic Supervision and Administration Regulation (CSAR) raises requirements on safety assessment, efficacy substantiation, and ingredient transparency for both domestic and imported products. In November 2025, the NMPA issued the Opinions on Deepening the Reform of Cosmetics Regulation and Promoting High-Quality Industry Development (Guoyaojian Zhuang No. 18), signaling a multi-year reform agenda through 2030 and beyond.

Value Chain Analysis

The China cosmetics value chain spans ingredient and chemical suppliers, packaging providers, brand owners, and a large ODM/OEM base that formulates and manufactures finished products for domestic and multinational labels. Manufacturing and product development are increasingly organized around industrial clusters and service ecosystems that combine R&D enablement with scale production, illustrated by platforms linked to zones such as Shanghai's Oriental Beauty Valley, which coordinates upstream and downstream resources for cosmetics companies.

Downstream routes to market are led by online-first commerce models and supported by specialty retail and mass retail, while compliance functions sit alongside the chain as a critical workflow for product filing/registration, testing, and labeling. The operating environment is pushing value-chain upgrading toward higher technical documentation capability and faster iteration on compliant formulas, reinforced by NMPA actions in 2025-2026 that prioritize risk-based management and ingredient pathway clarity. Trade frictions and tariff exposure on China-linked sourcing have also increased focus on localized procurement, supplier consolidation, and tighter quality control across the domestic supply network.

Competitive Landscape

The Chinese cosmetic products market is moderately consolidated, with multinational corporations and local players vying for market share. Global leaders such as L'Oréal SA, Shiseido Co. Ltd, and Estée Lauder Companies Inc. leverage their extensive brand portfolios and robust distribution networks to maintain dominance. In contrast, domestic companies like Yatsen Group capitalize on their deep understanding of local consumer preferences and agile business models to strengthen their position. Strategic collaborations with influencers and Key Opinion Leaders (KOLs) have become pivotal for brand development and market expansion. Companies are allocating significant resources to enhance their digital presence, focusing on e-commerce platforms and social media marketing. The market is characterized by ongoing product innovations, particularly in the premium and natural cosmetics categories, aimed at catering to specific consumer segments.

Local players, Florasis, Perfect Diary, and Mary Kay (China) Co., Ltd., demonstrate expertise in digital storytelling, building influencer partnerships, and maintaining agile supply chains. During the 2024 11-11 festival, these domestic brands surpassed traditional leaders, highlighting the transformative impact of social commerce. Start-ups utilize contract manufacturers to swiftly develop formulations tailored to niche audiences, such as acne-prone teenagers or menopausal women, and scale successful products nationally with the support of venture funding. Furthermore, domestic companies are leveraging tariff challenges that increase the landed costs of imported goods, further strengthening their market position.

Companies in the market are focusing on sustainability initiatives and technological advancements to gain competitive advantages. In terms of sustainability, organizations are testing refillable packaging solutions to reduce plastic waste and environmental impact. The implementation of blockchain technology enables companies to track ingredients throughout the supply chain, ensuring transparency and authenticity of raw materials. Companies are also developing artificial intelligence applications for precise skin analysis, which provide personalized product recommendations to consumers. Additionally, organizations are leveraging advanced data analytics capabilities to analyze consumer behavior patterns and optimize product offerings at the postal code level. This granular approach to data analysis allows companies to create targeted promotional campaigns based on specific regional preferences and purchasing patterns, ultimately improving market penetration and sales effectiveness.

China Cosmetic Products Industry Leaders

-

L'Oréal S.A.

-

Shiseido Co. Ltd

-

Estée Lauder Companies Inc

-

Procter & Gamble Co.

-

Coty Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory reforms and clearer technical pathways create whitespace for faster compliant innovation, particularly in efficacy-driven skincare and differentiated actives. In June 2026, the NMPA released Announcement No. 59, narrowing the higher-risk new cosmetic ingredient classifications from 10 categories to 5 (effective July 15, 2026), while May 2026 updates added new standards and test methods to the Safety and Technical Standards for Cosmetics (with elements effective July 1, 2026). Together, these measures support brands and manufacturers that can build strong dossiers, run validated testing, and translate ingredient claims into compliant efficacy narratives.

Operationally, investment into China-based supply chain and digital manufacturing capabilities is opening opportunities for shorter lead times, higher QC consistency, and more agile omnichannel fulfillment. In April 2026, The Estee Lauder Companies launched a China Fulfillment Center and Group Open Innovation (GOI) Center in Minhang, Shanghai, featuring automated goods-to-person picking and 24/7 lights-out operations, reflecting how logistics and innovation infrastructure are being localized for China demand patterns. On the manufacturing side, L'Oreal China inaugurated the UPX Phase II smart manufacturing workshop at its Suzhou plant in June 2026 with AI-driven quality inspection, raising the bar for contract manufacturing partnerships and for domestic brands seeking scalable, higher-assurance production for online-led launches.

Recent Industry Developments

- July 2026: L'Oreal China inaugurated the UPX Phase II smart manufacturing workshop at its Suzhou plant as part of a broader upgrade to its China supply chain. The move deepens smart production capabilities, including AI-driven quality inspection, supporting faster scale-up and tighter batch consistency for high-volume online demand.

- June 2026: Beijing Liyuan listed its 35% stake in the Shiseido Liyuan Cosmetics joint venture for sale on the China Beijing Equity Exchange. The potential ownership change highlights continued restructuring among multinational-local operating models in China, with implications for brand control, channel execution, and local decision speed.

- April 2024: Fenty Beauty launched in Mainland China through Sephora stores, signaling a major entry for a global premium cosmetics brand into the mainland market.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the retail value of cosmetic make-up products sold in China, tracked across mass and premium positioning and across the major selling channels.

Scope exclusions: Hair care, skin care, bath and shower, deodorants, and other broader personal care items are excluded even when they are sold by the same beauty brands.

Segmentation Overview

-

By Product Type

- Facial Cosmetics

- Eye Cosmetics

- Lip and Nail Make-up Products

-

By Category

- Premium

- Mass

-

By Ingredient Type

- Natural/Organic

- Conventional/Synthetic

-

By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, build the historical context, and collect anchor indicators that can be checked year over year. We mainly relied on public sources such as China NMPA and related CSAR regulatory releases, China National Bureau of Statistics retail sales series, China Customs trade statistics where relevant, and trade association updates such as those from fragrance and cosmetics bodies.

Along with this, we reviewed brand and retailer public filings, investor presentations, product launch announcements, and reputed press coverage to understand pricing direction, channel shifts, and promotional intensity. A paid subscription covering company financials and another covering patent and innovation activity were used selectively to cross-check revenue exposure and new product cadence. The sources listed here are illustrative rather than exhaustive, and many other references were also used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to validate what desk research cannot clearly show, especially around channel mixes, typical price ladders, and how fast new formats are being adopted in different parts of China. We spoke with a spread of manufacturers, distributors, retailers, and industry specialists across the main demand centers and also the faster-growing lower-tier city markets, and then the feedback was used to fine-tune assumptions and resolve data gaps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | |

| Mid tier: 51% | Functional/Unit leaders: 42% | |

| Smaller Players: 15% | Managers: 45% |

Market-Sizing & Forecasting

Sizing started with a top-down reconstruction of the China make-up demand pool by linking national beauty and cosmetics retail signals to the specific product scope covered in this report, and then splitting the total by channel and price tier using observed mix shifts. To keep the outputs realistic, the totals were corroborated with selective bottom-up checks like sampled brand sales exposure, store level throughput logic for key channels, and typical ASP times volume sanity checks for a limited set of product lines.

Inputs used in the model include, for example, cosmetics retail sales trends, online penetration and conversion signals for beauty shopping, premiumization direction in pricing, the pace of new product registrations and compliant launches, and the channel rebalancing between specialty stores, supermarkets, and online retail. For forecasting, we used scenario analysis supported by short variable-based projections, and each driver was stress-tested with primary feedback so the growth path stays consistent with what industry participants expect.

Where bottom-up reference points were missing for smaller brands or informal selling routes, gaps were handled through conservative mix assumptions and then rechecked against the implied per-capita spend and channel shares, before the final market totals were locked.

Data Validation & Update Cycle

Outputs were cross-verified through triangulation across demand indicators, channel level sense checks, and pricing progression checks so the market direction is not driven by any single series. When a metric moved sharply, the driver was traced back, and the assumption was challenged through a second internal review and, if needed, follow-up outreach to primary respondents.

The model is reviewed in multiple steps before sign-off, including variance checks against past editions and against independent signals like retail sales momentum and channel mix trends. Reports are refreshed annually, and interim updates are made when material events occur, such as regulation changes or large channel disruptions. Before delivery, a fresh final pass is completed so clients receive the latest updated view.

Mordor Intelligence's China Cosmetics Products Market Market Size Versus Other Published Estimates

Published market sizes for China cosmetics can look far apart, even when the titles sound similar, because the underlying product boundary and the selling stage being measured are not always aligned. Differences also come from how channels are treated, which year is used as the base, and whether pricing is modeled as an average retail tag or as realized selling price after promotions.

In this market, the biggest spread usually comes from whether skin care and broader personal care are bundled into the same number, and whether cross-border and travel retail are counted in the same way as domestic retail. Currency conversion timing, the way premiumization is applied to future ASPs, and how often assumptions are refreshed can also move the total up or down.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.95 B (2025) | |

| Global Consultancy A | USD 41.31 B (2025) | Uses a broader cosmetics and personal care definition that typically includes skin care and hair care, so the value pool is much larger than make-up only, and channel coverage is often reported at an aggregate level. |

| Industry Research Group B | USD 9.56 B (2024) | Uses a different base year and may apply a wider product basket within beauty categories, plus higher assumed growth in emerging channels, which can shift year-on-year comparability. |

The table shows the widest gap is driven by what is counted as cosmetics, and under Mordor Intelligence's scope only facial cosmetics, eye cosmetics, and lip and nail make-up are included rather than skin care, hair care, and other personal care categories. After scope and year are aligned, the remaining spread is usually explained by how online discounting is translated into realized ASPs and by how frequently channel mix assumptions are refreshed through interviews and ongoing checks.

Key Questions Answered in the Report

What is the current size of the China cosmetics market?

The China cosmetics market size is USD 10.84 billion in 2026.

How fast is the market expected to grow?

It is projected to expand at a 8.9% CAGR, reaching USD 16.61 billion by 2031.

Which product segment holds the largest share?

Facial cosmetics led with 50.92% of 2025 sales.

Which distribution channel is growing the fastest?

Online retail stores are advancing at an 11.1% CAGR through 2031.

Page last updated on: