ASEAN Sensitive Skin Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

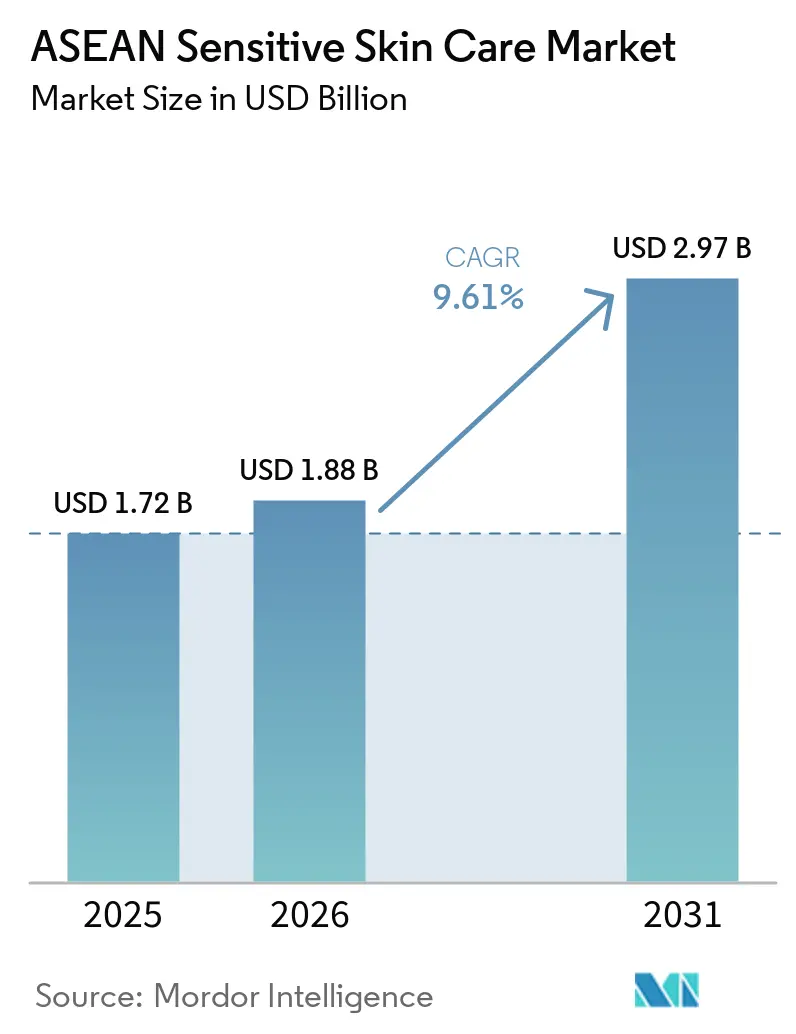

| Base Year Market Size (2025) | USD 1.72 Billion |

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.97 Billion |

| Growth Rate (2026 - 2031) | 9.61% CAGR |

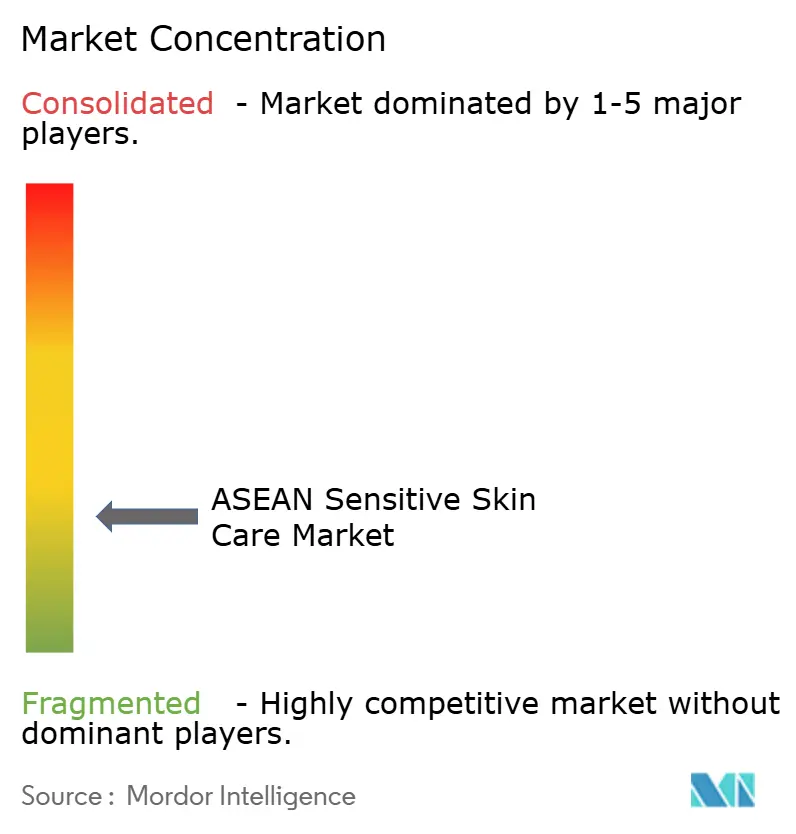

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

ASEAN Sensitive Skin Care Market Analysis by Mordor Intelligence

ASEAN sensitive skincare market size in 2026 is estimated at USD 1.72 billion, growing from 2025 value of USD 1.88 billion with 2031 projections showing USD 2.97 billion, growing at 9.61% CAGR over 2026-2031. Increasing digital engagement among the region’s young population, the introduction of mandatory halal certification in Indonesia by October 2026, and stricter ASEAN-wide ingredient regulations are driving changes in product formulations and encouraging innovation. While moisturizers and creams remain popular, serums and essences are gaining traction as consumers prefer targeted solutions supported by dermatological research. The market shows a split in demand, with mass-market products maintaining their appeal and premium products growing quickly, driven by affluent consumers who prioritize scientifically proven ingredients like fermented camellia seed extract, discovered by Shiseido in 2024. Rising pollution and humidity in tropical urban areas are also increasing the need for barrier-repair and anti-inflammatory products, making sensitive skincare a necessity rather than just a cosmetic choice. The ASEAN sensitive skincare market is moderately concentrated, with the top 5 companies holding a significant share, leaving opportunities for smaller, agile players to enter the market.

Key Report Takeaways

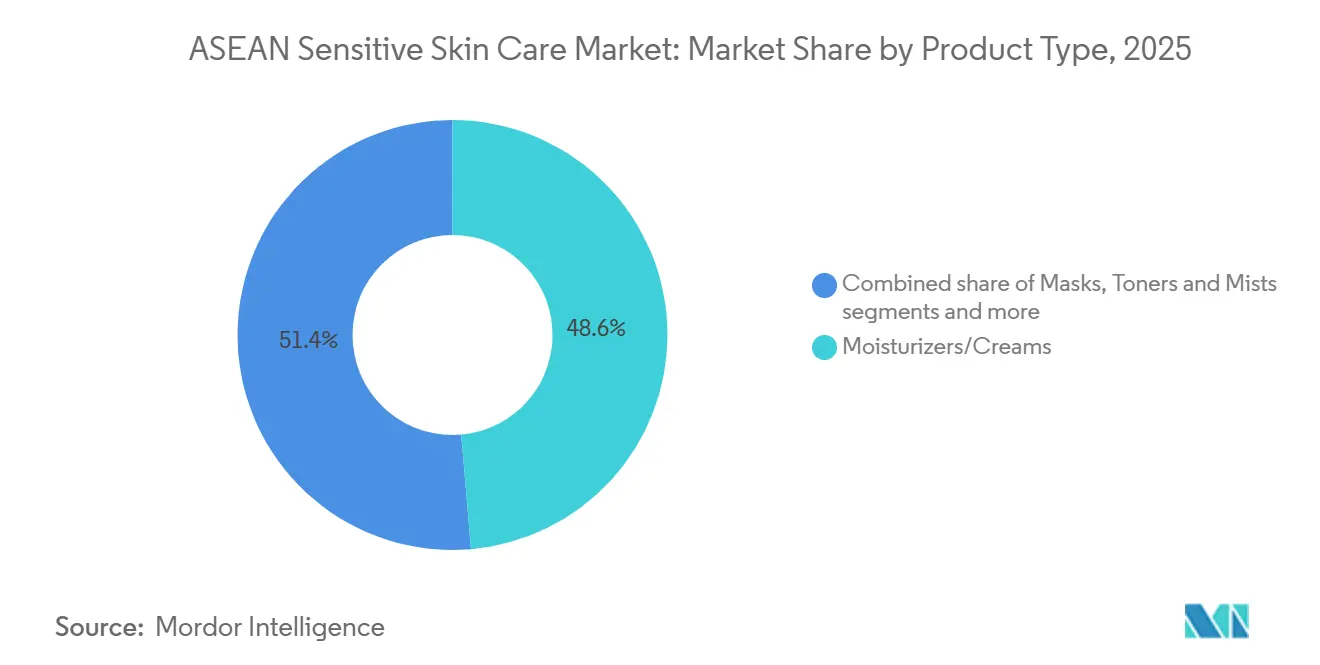

- By product type, moisturizers/creams commanded 48.62% of the ASEAN sensitive skincare market share in 2025, whereas serums and essences are advancing at a 11.70% CAGR through 2031.

- By price range, the mass segment accounted for 66.89% of the ASEAN sensitive skincare market size in 2025, while premium products are projected to expand at a 10.41% CAGR through 2031.

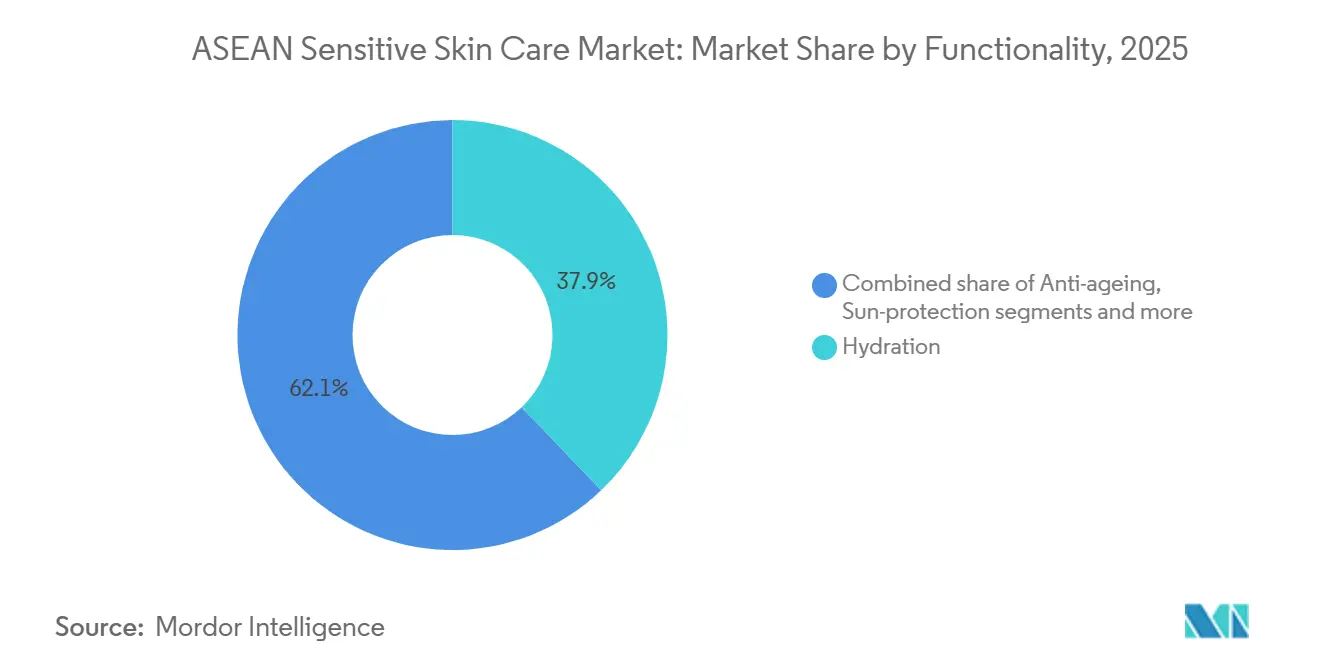

- By functionality, hydration products accounted for a 37.85% share of the ASEAN-sensitive skincare market in 2025, and sun-protection solutions are projected to grow at an 11.27% CAGR through 2031.

- By distribution channel, health and beauty stores led with a 27.18% revenue share in 2025; online retail stores are expected to grow at a 10.60% CAGR through 2031.

- By geography, Indonesia accounted for a 35.28% share of the ASEAN sensitive skincare market size in 2025, and the Vietnam is projected to progress at a 11.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Sensitive Skin Care Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of skin sensitivities | +1.8% | Impact in Indonesia, Thailand, Malaysia | Medium term (2-4 years) |

| Growing influence of social media and beauty influencers | +1.5% | Indonesia, Philippines, Thailand core, spillover to Vietnam | Short term (≤ 2 years) |

| Growing consumer awareness of ingredients | +1.2% | Singapore, Malaysia lead, expanding to Indonesia, Thailand | Medium term (2-4 years) |

| Cultural adoption of multi-step and personalized routines | +1.0% | Thailand, Philippines, Vietnam with K-beauty influence | Long term (≥ 4 years) |

| Focus on halal-certified and ethical skincare | +0.9% | Indonesia dominant, Malaysia secondary, Muslim-majority areas | Long term (≥ 4 years) |

| Increased product innovation | +0.7% | Singapore, Thailand innovation hubs, regional distribution | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of skin sensitivities

The increase in skin sensitivity issues across ASEAN is largely tied to environmental factors such as worsening air pollution in urban areas, consistently high humidity levels, and sudden temperature changes, especially in tropical cities. Health reports from Southeast Asian ministries highlight a growing number of dermatological cases, including conditions like atopic dermatitis, contact eczema, and rosacea. For example, a study by PubMed Central National Center for Biotechnology Information revealed a 33.7% prevalence of atopic dermatitis in Thailand as of 2023[1]Source: PubMed Central National Center for Biotechnology Information, "Epidemiology of adult patients with atopic dermatitis in AWARE 1: A second international survey", pmc.ncbi.nlm.nih.gov. These environmental and pollution-related factors have shifted sensitive skincare from being a cosmetic choice to a necessity for many. This has led to a rising demand for skincare products formulated with anti-inflammatory ingredients and antioxidants. Consumers are increasingly seeking solutions that not only improve skin health but also provide protection against these external stressors.

Growing influence of social media and beauty influencers

The growing impact of social media and beauty influencers on platforms like TikTok, Instagram, and regional live-commerce channels is playing a major role in shaping the buying habits of Gen Z consumers in ASEAN countries. These young consumers are highly influenced by endorsements from influencers, often making quick purchase decisions based on their recommendations. In response to this trend, Vietnam has implemented regulatory measures to monitor cosmetic sales on social platforms, recognizing their significant influence on driving product popularity and sales. This has created a dynamic environment where manufacturers need to stay ahead by predicting and responding to emerging ingredient trends. Thailand's high level of digital connectivity, with 90% internet penetration as of 2024 according to the World Bank, amplifies the reach and effectiveness of social media marketing, making it a critical tool for engaging with consumers in the ASEAN sensitive skincare market[2]Source: World Bank, "Individuals using the Internet (% of population) - Thailand", worldbank.org.

Cultural adoption of multi-step and personalized routines

The ASEAN sensitive skincare market is experiencing growth as consumers increasingly adopt multi-step and personalized skincare routines, especially in urban areas where skincare is viewed as both self-care and a way to maintain healthy skin. Influences from countries like South Korea and Japan, known for their advanced skincare practices, have popularized routines such as double cleansing, toner layering, and using products with specific active ingredients. This shift has driven demand for products that are fragrance-free and hypoallergenic, catering to concerns like redness, dryness, and post-acne inflammation. Brands in the region, such as Thailand’s BK Acne, have responded by introducing product lines specifically designed for sensitive skin. These products often feature minimalist packaging and include active ingredients like panthenol, cica, and ceramides.

Focus on halal-certified and ethical skincare

The ASEAN sensitive skincare market is increasingly influenced by halal compliance and ethical considerations, which are becoming critical factors for consumers. According to the Australian Government, Indonesia's mandatory halal certification law, set to be fully implemented by October 2026, is driving significant changes in the skincare industry[3]Source: Australian Government, "Complying with Indonesian halal requirements", dfat.gov.au. Companies are now focusing on ensuring transparency in ingredient sourcing, manufacturing processes, and product labeling to meet these requirements. At the same time, there is a growing demand for products that are cruelty-free, vegan, and environmentally sustainable, especially in countries like Malaysia and Brunei. In these regions, consumers are linking religious purity with environmental responsibility, leading to a preference for skincare products that align with both ethical and halal standards.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of counterfeit products | -1.4% | Thailand, Philippines enforcement challenges, regional spillover | Short term (≤ 2 years) |

| High price of skincare products | -1.1% | Indonesia, Vietnam price-sensitive markets, mass segment impact | Medium term (2-4 years) |

| Sourcing challenges for certified ingredients | -0.8% | Supply chains affecting Singapore, Malaysia distribution hubs | Long term (≥ 4 years) |

| Climate and environmental stressors worsen product performance | -0.6% | Tropical ASEAN regions, storage and efficacy challenges | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

The rise of counterfeit skincare products in ASEAN is becoming a major challenge for the sensitive skincare market, especially with the rapid growth of e-commerce, which is expected to significantly boost the region's GDP. Online platforms have become a hotspot for counterfeit goods, offering fake products at much lower prices. This not only harms genuine brands but also misleads consumers. These counterfeit items often contain unregulated synthetic ingredients, increasing the risk of skin irritation and allergic reactions. In March 2025, the Chamber of Cosmetics Industry of the Philippines (CCIP) and 18 member companies signed an agreement to tackle online cosmetic counterfeiting, according to the Intellectual Property Office of the Philippines[4]Source: Intellectual Property Office of the Philippines, "CCIP, 18 cosmetics companies join E-Commerce MOU", ipophil.gov.ph. In April 2025, the National Bureau of Investigation (NBI) and Intellectual Property Rights Division (IPRD) seized 18,889 counterfeit items worth PHP 15 million in Manila, as reported by NBI Gov Philippines[5]Source: NBI Gov Philippines, "NBI Seizes Counterfeit Products", nbi.gov.ph. These actions emphasize the need for stronger regional regulations and anti-counterfeit measures to ensure consumer safety and protect brand reputation.

High price of skincare products

The high cost of producing sensitive skincare products, especially those made with organic, halal-certified, and dermatologist-approved ingredients, continues to limit their reach in price-sensitive ASEAN countries like Indonesia and Vietnam. Ethical sourcing and certifications increase production costs, often making these products too expensive for middle-income consumers. Currency fluctuations in the region add to the challenge by raising the cost of imported ingredients and packaging. As a result, some brands reduce formulation quality or innovation, which limits the growth of premium sensitive skincare products among budget-conscious consumers. Brands like Paula’s Choice and La Roche-Posay, known for their sensitive-skin-focused products, often sell at higher prices ranging from USD 25–40 per product, making them desirable but less affordable for the mass market in ASEAN.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Serums and Essence Drive Premiumization Shift

Moisturizers/creams held the largest share of the ASEAN sensitive skincare market in 2025, accounting for 48.62%. These products remain popular due to their ability to provide hydration and protect the skin barrier, which is especially important in the region's humid climate. While other products like cleansers, masks, and toners are also part of skincare routines, they have not surpassed the widespread use of moisturizers and creams. These traditional hydration products continue to be the foundation of daily skincare for individuals with sensitive skin, offering a reliable solution for maintaining skin health in challenging environmental conditions.

Serums and essences are expected to grow significantly, with a projected CAGR of 11.70% through 2031. This growth is driven by advancements in nano-encapsulation technology, which helps preserve the potency of active ingredients, and by increased consumer awareness through influencer-led education on targeted skincare routines. These products are gaining popularity as they offer lightweight formulations that are suitable for tropical climates while delivering concentrated benefits like antioxidants and ceramides. Future product launches are likely to focus on innovative delivery systems that address specific skin concerns, further expanding the market for premium sensitive skincare solutions in the ASEAN region.

By Price Range: Premium Acceleration Despite Mass Dominance

In 2025, mass-tier products dominated the ASEAN sensitive skincare market, capturing 66.89% of the market share. This indicates a strong preference for affordable skincare solutions, particularly in countries like Indonesia, Vietnam, and the Philippines, where price sensitivity is high. Consumers in these regions prioritize halal-certified and budget-friendly products, which have gained their trust and loyalty. These products cater to the needs of a large population seeking effective yet economical skincare options, making them the most popular choice in the market.

Premium products, on the other hand, are projected to grow at a CAGR of 10.41% by 2031, fueled by increasing disposable incomes and a rising interest in advanced, science-backed skincare solutions. Consumers are becoming more willing to spend on high-quality products that deliver visible and proven results. The introduction of smaller packaging sizes and subscription-based models has further enhanced the accessibility of premium products, making them appealing to a broader audience. This trend reflects a gradual shift in consumer behavior, with more individuals upgrading to premium offerings for better skincare benefits.

By Functionality: Anti-Aging Emerges as Growth Driver

Hydration solutions dominated the ASEAN sensitive skincare market in 2025, accounting for 53.21% of the market share. This strong demand is driven by the region's hot and humid climate, combined with rising pollution levels and the widespread use of air conditioning, which often leaves skin dehydrated. Consumers are prioritizing products that restore moisture balance as a basic skincare need. While hydration products lead the market, other categories like whitening, acne care, and barrier-repair solutions are also gaining traction, though they contribute less to overall sales volumes. These secondary categories are gradually expanding as consumers diversify their skincare routines to address specific concerns.

Sun Protection products are expected to grow at a steady CAGR of 11.27% through 2031, fueled by younger urban consumers who are starting preventive skincare routines earlier. Millennials, in particular, are showing interest in products with advanced formulations, such as those containing fermented botanical extracts like Shiseido’s Camellia-derived actives, which target aging skin cells. This trend is expanding the market for therapeutic skincare solutions. Hybrid products like sunscreens with anti-pollution benefits are gaining popularity, as they address external factors contributing to premature aging. These innovations are expected to drive further growth in the anti-aging segment, making it a key area of focus for manufacturers in the ASEAN sensitive skincare market.

By Distribution Channel: Digital Commerce Transformation

Online Retail Stores accounted for 31.63% of the ASEAN sensitive skincare market share in 2025. These outlets remain popular due to established shopping habits and the ability to test products in-store, which is particularly important for consumers with sensitive skin. Health and beauty chains also play a significant role by offering personalized advice and product recommendations. Pharmacies, on the other hand, are trusted for their association with dermatologist-recommended products, making them a key channel for sensitive skincare items. Together, these physical retail formats continue to dominate the market by providing accessibility and trust to consumers.

Online retail stores are expected to grow at a 11.17% CAGR through 2031, driven by advancements in digital technology and changing consumer preferences. Features like livestream shopping, mobile payment options, and AI-powered skin analysis tools are making online platforms more appealing. These innovations allow consumers to make informed decisions from the comfort of their homes. Services like click-and-collect and virtual consultations are bridging the gap between online and offline shopping, offering both convenience and expert guidance. This shift toward digital channels is expected to significantly expand the market, creating a strong omnichannel presence for sensitive skincare products.

Geography Analysis

Indonesia held a significant 35.28% share of the ASEAN sensitive skincare market in 2025. This dominance is attributed to its large female population of 146.4 million, as of August 2025, and government initiatives aimed at reducing beauty imports by 35% by 2028 through increased local production. Local brands, such as Wardah, are expanding their online presence and regional reach, while international companies are adjusting their supply chains to meet halal certification requirements. These factors are driving market growth and creating opportunities for both domestic and global players to thrive in the region.

Vietnam is the fastest-growing market in the ASEAN sensitive skincare sector, with a projected CAGR of 11.17% through 2031. This growth is supported by robust regulatory frameworks that streamline product approvals and safeguard intellectual property. Malaysia is also benefiting from similar regulations, which ensure ingredient standardization and facilitate the regional launch of products. In Thailand, efforts by customs authorities and brands to reduce counterfeit products are helping to improve consumer trust. The recovery in tourism is driving demand for travel-sized, sensitive skincare products, thereby contributing to market expansion.

Other markets like Thailand, Vietnam, and Singapore are also showing strong growth potential due to increasing consumer awareness and the rapid development of e-commerce platforms. In the Philippines, ongoing measures to tackle counterfeit products are enhancing market transparency, although educating consumers remains a priority. Vietnam’s new social commerce regulations are helping to improve digital safety and consumer standards. Meanwhile, emerging markets such as Cambodia and Laos offer untapped opportunities for brands focusing on mobile-first strategies and affordable, halal-certified sensitive skincare products.

Competitive Landscape

The ASEAN sensitive skincare market is moderately concentrated, with the top 5 companies holding approximately 45% of the market share. This leaves room for smaller, agile players to enter and compete. Shiseido utilizes its VOYAGER AI platform to analyze extensive data, enabling faster development of sensitive-skin serums designed specifically for tropical climates. Similarly, L'Oréal employs its Cell BioPrint technology, a portable proteomics lab, to create personalized skincare regimens, positioning itself as a leader in combining diagnostics with product innovation.

Collaborations and partnerships are becoming increasingly important in the ASEAN sensitive skincare market as brands look to expand their presence and meet the unique needs of local consumers. For example, Kao has joined forces with Thailand’s C.P. Group to open SENSAI’s first store in Indonesia, reflecting the growing demand for premium skincare products in the region. This partnership caters to the rising preference for high-quality, luxury skincare solutions among consumers. Similarly, Kosé’s acquisition of Puri Beauty underscores the value of incorporating local traditions into product development.

Innovation in the market is focused on areas such as climate-adaptive formulations, pollution protection, and time-release active ingredients. Local startups are gaining attention by emphasizing halal-certified products and transparent sourcing practices, although challenges in scaling due to ingredient supply issues persist. To address this, multinational companies are setting up open-innovation accelerators in Singapore, offering funding and regulatory support to emerging ventures. This approach not only strengthens the ecosystem but also helps larger companies identify and adopt disruptive technologies.

ASEAN Sensitive Skin Care Industry Leaders

-

Beiersdorf AG

-

Unilever PLC

-

L'Oréal SA

-

Galderma (Cetaphil)

-

Rohto Pharmaceutical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Kosé-owned Carté HD expanded its presence by entering the Singapore market and announced plans to launch in Thailand the following year as part of its broader global expansion strategy. The brand aimed to cater to the growing demand for sensitive skincare products in the ASEAN region, leveraging its expertise in dermatological solutions.

- July 2024: Korean skincare brand Dr. Jart+ introduced its innovative product line to the Philippines. The launch marked a significant step in the brand's expansion strategy, aiming to cater to the growing demand for high-quality skincare solutions in the region.

- February 2024: Amorepacific expanded its international presence by launching its derma beauty brand, Aestura, in both Vietnam and Thailand. This strategic move aimed to tap into the growing demand for skincare products in these markets.

ASEAN Sensitive Skin Care Market Report Scope

Sensitive skin care products are specifically designed for those with sensitive skin and skin conditions. These products contain mild ingredients that do not aggravate existing skin issues and are gentle on the skin.

The ASEAN-sensitive skincare products market is segmented by product type, distribution channel, and country. Based on product type, the market is segmented into cleansers, creams & moisturizers, serums & essence, toners, and other classes. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, specialty stores, pharmacies, drug stores, online retail stores, and other distribution channels. Based on country, the market is segmented into Indonesia, Thailand, Singapore, Malaysia, Philippines, and the Rest of ASEAN.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Cleansers |

| Moisturizers/Creams |

| Serums and Essences |

| Masks |

| Toners and Mists |

| Other Product Types |

| Mass |

| Premium |

| Hydration |

| Anti-ageing |

| Whitening/Brightening |

| Acne-care |

| Sun-protection |

| Other Functionalities |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| Indonesia |

| Thailand |

| Philippines |

| Vietnam |

| Malaysia |

| Singapore |

| Rest of ASEAN |

| By Product Type | Cleansers |

| Moisturizers/Creams | |

| Serums and Essences | |

| Masks | |

| Toners and Mists | |

| Other Product Types | |

| By Price Range | Mass |

| Premium | |

| By Functionality | Hydration |

| Anti-ageing | |

| Whitening/Brightening | |

| Acne-care | |

| Sun-protection | |

| Other Functionalities | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Health and Beauty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | Indonesia |

| Thailand | |

| Philippines | |

| Vietnam | |

| Malaysia | |

| Singapore | |

| Rest of ASEAN |

Key Questions Answered in the Report

How big is the ASEAN sensitive skincare market in 2026?

The ASEAN sensitive skincare market size is USD 1.88 billion in 2026 with an 9.61% CAGR outlook to 2031.

Which product segment is growing the fastest?

Serums and essences are leading growth at a projected 11.70% CAGR through 2031 as consumers shift toward targeted, high-potency treatments.

Which distribution channel offers the greatest future upside?

Online retail stores show the highest growth potential at a 10.60% CAGR, powered by near-universal mobile internet use and livestream commerce popularity.

What is the competitive outlook for new entrants?

With a concentration score of 3, the market provides space for niche brands focusing on climate-adaptive, halal-certified, or AI-driven personalized solutions.

Page last updated on: