Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.05 Billion |

| Market Size (2026) | USD 13.62 Billion |

| Market Size (2031) | USD 16.89 Billion |

| Growth Rate (2026 - 2031) | 4.40% CAGR |

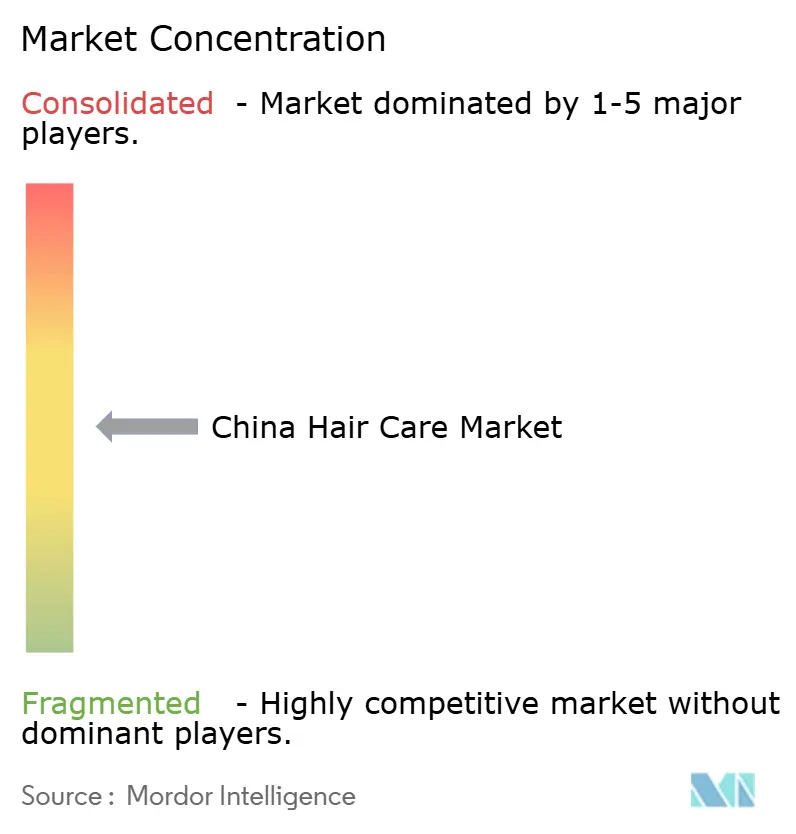

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Hair Care Market Analysis by Mordor Intelligence

The China Hair Care Market size was valued at USD 13.05 billion in 2025 and estimated to grow from USD 13.62 billion in 2026 to reach USD 16.89 billion by 2031, at a CAGR of 4.40% during the forecast period (2026-2031). This growth trajectory positions China as a critical battleground where digital commerce innovation intersects with evolving consumer preferences for premium, efficacy-driven formulations. The market's expansion occurs against a backdrop of regulatory modernization through the National Medical Products Administration's Cosmetics Supervision and Administration Regulation, which has fundamentally restructured how hair care products enter and compete in Chinese markets [1]Source: Cosmetics Supervision and Administration Regulation (CSAR), "How hair care products enter and compete in Chinese markets", english.nmpa.gov.cn. Competitive play increasingly centers on data-rich influencer partnerships that convert social engagement into instant checkouts. Distribution-channel diversification, particularly in lower-tier cities reached through livestream selling, expands total addressable demand even as urban shoppers trade up. Demand for premium products is surging as younger consumers, especially Gen Z, embrace multi-step "skincare-style" hair routines and sophisticated scalp care, with men in second-tier cities adopting new treatment formats. Product innovation featuring clean, vegan, and traditional Chinese medicine ingredients is addressing concerns around pollution and hair loss, while digital marketing and social commerce—especially live-stream selling on platforms like Douyin—fuel product discovery and market expansion. These consumer trends, alongside rapid growth in both mid-range and high-end segments and a strong emphasis on health, efficacy, and personalized solutions, are underpinning the robust trajectory of China's hair care market in 2025.

Key Report Takeaways

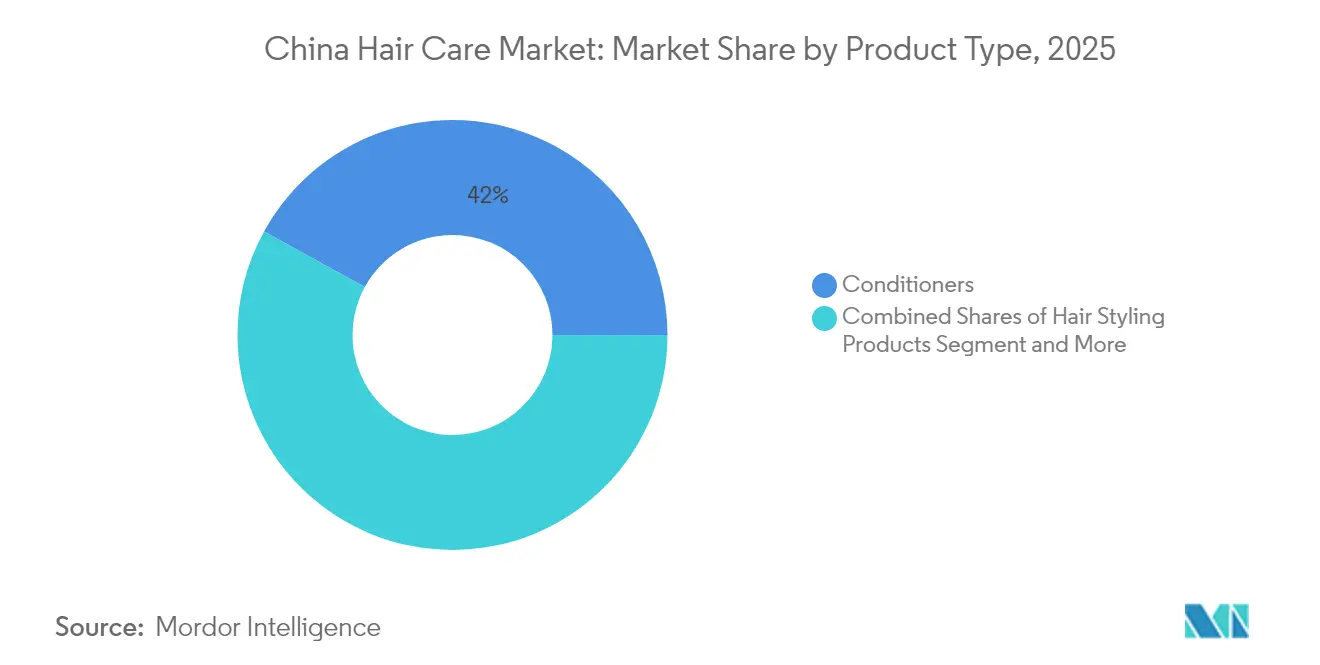

- By product type, conditioners led with 42.01% revenue share in 2025; hair styling lines are projected to expand at a 4.86% CAGR through 2031.

- By category, conventional and synthetic formats accounted for 74.03% of the China hair care products market share in 2025, while natural and organic ranges post the fastest growth at a 5.94% CAGR to 2031.

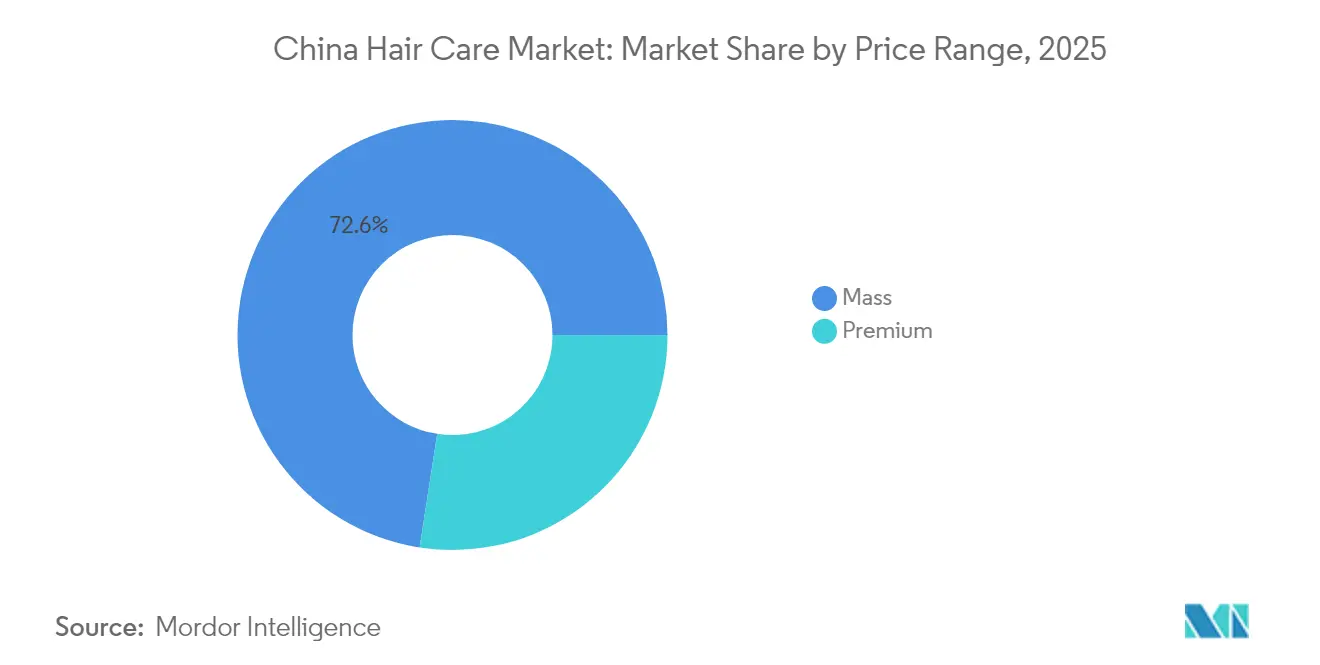

- By price range, mass offerings held 72.56% of the China hair care products market size in 2025; the premium tier records a 5.05% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured 35.05% share in 2025, whereas online retail platforms register the strongest momentum with a 5.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Focus on Scalp Care and Anti-Dandruff Solutions | +0.8% | National, with concentration in tier-1 cities | Medium term (2-4 years) |

| Accelerating Demand for Premium and Luxury Hair Care Offerings | +0.7% | Tier-1 and tier-2 cities, expanding to lower tiers | Long term (≥ 4 years) |

| Impact of Digital Marketing and Social Media on Product Adoption | +0.6% | National, strongest in urban areas | Short term (≤ 2 years) |

| Expanding Market for Hair Color Products | +0.5% | Urban areas, particularly among Gen Z consumers | Medium term (2-4 years) |

| Growing Consumer Preference for Natural and Clean Label Ingredients | +0.4% | Tier-1 cities, spreading to tier-2 markets | Long term (≥ 4 years) |

| Evolution of Multi-Benefit Hair Care Products | +0.3% | National, across all consumer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Focus on Scalp Care and Anti-Dandruff Solutions

Scalp health has emerged as the primary growth catalyst, transforming from a niche concern into mainstream wellness priority across Chinese consumers. The segment's momentum stems from clinical evidence linking scalp microbiome balance to overall hair health, driving demand for specialized treatments beyond traditional cleansing. CLEAR's April 2025 launch of the SCALPCEUTICALS PRO RANGE in Shanghai, backed by three global patents and validation from 200 dermatologists, exemplifies how brands are positioning scalp care as a scientific discipline rather than cosmetic enhancement. The premium scalp care market has expanded 190% with market size exceeding CNY 33 billion, indicating consumer willingness to invest in targeted solutions. This trend particularly resonates with younger demographics who view scalp health as preventive care, creating opportunities for brands that combine dermatological credibility with accessible pricing. Anti-dandruff formulations now incorporate advanced actives like selenium disulfide and piroctone olamine, moving beyond zinc pyrithione to deliver more sophisticated therapeutic benefits.

Accelerating Demand for Premium and Luxury Hair Care Offerings

Premiumization reflects China's broader consumption upgrade as disposable incomes rise, and consumers prioritize quality over quantity in personal care routines. The shift toward luxury positioning enables brands to capture higher margins while meeting sophisticated consumer expectations for ingredient transparency, sensory experience, and packaging aesthetics. In February 2024, Henkel's strategic acquisition of Vidal Sassoon's China operations demonstrates how multinationals are consolidating premium assets to compete more effectively against domestic challengers who increasingly occupy mid-market positions [2]Source: Henkel, "Henkel to acquire Vidal Sassoon in Greater China", henkel.com. Premium hair care benefits from the "skinification" trend, where consumers apply skincare evaluation criteria to hair products, seeking formulations with proven actives like hyaluronic acid, niacinamide, and peptides. This evolution creates differentiation opportunities for brands that can substantiate efficacy claims through clinical testing, particularly as NMPA regulations require stronger evidence for functional benefits. The premium segment's 5.12% CAGR outpaces overall market growth, indicating sustainable demand for higher-priced offerings that deliver measurable results.

Impact of Digital Marketing and Social Media on Product Adoption

Digital platforms have fundamentally restructured how Chinese consumers discover, evaluate, and purchase hair care products, with livestreaming commerce emerging as the dominant conversion mechanism. Xiaohongshu's influence extends beyond product discovery to trend creation, as beauty influencers demonstrate application techniques and share ingredient education that drives purchase decisions. The platform's 300+ million users, predominantly female and under 26, represent the core demographic for premium hair care adoption, making influencer partnerships essential for brand building. Douyin's integration of e-commerce functionality enables direct conversion from content consumption to purchase, reducing friction in the customer journey while providing brands with performance metrics that traditional retail channels cannot match. This digital transformation particularly benefits domestic brands that can respond quickly to trending ingredients or formats, as evidenced by the rapid adoption of solid shampoo bars and DIY hair coloring products following viral social media content. The challenge for international brands lies in adapting global campaigns to local digital ecosystems while maintaining brand consistency across platforms.

Expanding Market for Hair Color Products

Hair colorants represent a high-growth category driven by self-expression trends among younger consumers and the normalization of DIY coloring during and after COVID-19 lockdowns. The segment reached CNY 13.5 billion in 2019 with projections of CNY 18.2 billion by 2020, demonstrating strong consumer appetite for at-home coloring solutions. Regulatory complexity creates barriers to entry, as hair colorants fall under NMPA's special cosmetics category requiring registration rather than simple notification, but this same regulatory framework protects established players from low-quality competition. Product innovation focuses on convenience and safety, with foam and bubble formats gaining popularity alongside traditional cream formulations. The trend toward temporary and semi-permanent colors reflects consumer desire for experimentation without long-term commitment, creating opportunities for brands that can offer vibrant colors with gentle formulations. E-commerce platforms report strong growth in colorant sales, with Tmall recording 84% year-over-year increases in hair dye purchases, indicating robust demand that extends beyond traditional salon channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Consumer Awareness About Chemical Ingredients | -0.3% | Tier-1 cities, expanding to tier-2 markets | Long term (≥ 4 years) |

| Consumer Brand Loyalty Remains Low with Frequent Switching | -0.4% | National, particularly strong in online channels | Short term (≤ 2 years) |

| Environmental Impact of Product Packaging and Microplastics | -0.2% | Urban areas with higher environmental consciousness | Medium term (2-4 years) |

| Growing Adoption of Minimalist Hair Care Practices | -0.3% | Tier-1 cities, influenced by social media trends | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Awareness About Chemical Ingredients

Ingredient scrutiny has intensified as Chinese consumers become more sophisticated in evaluating product formulations, creating pressure on brands to reformulate away from controversial components like sulfates, parabens, and silicones. This awareness stems from increased access to international beauty information through social media and the influence of clean beauty movements from Western markets. The challenge for manufacturers lies in maintaining product performance while addressing consumer concerns about chemical safety, often requiring significant R&D investment to develop alternative formulations. NMPA's enhanced labeling requirements, which mandate full ingredient disclosure in descending order by weight, have amplified consumer ability to make informed choices based on formulation transparency. Brands that proactively communicate ingredient safety and provide educational content about formulation science can turn this trend into competitive advantage, while those relying on traditional marketing claims face increased skepticism from informed consumers.

Consumer Brand Loyalty Remains Low with Frequent Switching

The digital commerce environment facilitates easy brand switching as consumers can quickly compare products, read reviews, and experiment with new offerings without significant switching costs. This behavior is particularly pronounced among younger demographics who view hair care experimentation as part of personal expression rather than routine maintenance. E-commerce platforms amplify switching behavior by promoting discovery through algorithm-driven recommendations and influencer endorsements that introduce consumers to previously unknown brands. The proliferation of domestic brands offering competitive quality at lower price points has further eroded traditional brand loyalty, forcing international players to continuously justify premium positioning through innovation and marketing investment. Brands can combat switching behavior through subscription models, loyalty programs, and personalized product recommendations, but the fundamental shift toward experimental consumption patterns requires ongoing investment in customer acquisition rather than retention-focused strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conditioners Lead While Styling Surges

Conditioners dominate the product landscape with 42.01% market share in 2025, reflecting Chinese consumers' emphasis on hair health and damage repair over basic cleansing functions. This leadership position stems from the category's ability to deliver immediate sensory benefits that consumers can feel and see, making it easier to justify premium pricing compared to shampoos where differentiation is less apparent. Hair styling products emerge as the fastest-growing segment at 4.86% CAGR through 2031, driven by urbanization trends and professional appearance standards that require daily hair management. The styling category benefits from product innovation in heat protection, humidity resistance, and long-lasting hold formulations that address specific challenges in China's diverse climate conditions.

Shampoo products face commoditization pressure despite representing the largest volume category, as consumers increasingly view cleansing as a functional necessity rather than a premium experience. Hair loss treatment products command premium pricing but remain constrained by NMPA's special cosmetics registration requirements, which create regulatory barriers that protect established players while limiting new entrant competition. Hair colorants show strong growth potential particularly in DIY formats, though regulatory complexity requires significant investment in safety testing and efficacy validation. The "other product types" category includes emerging formats like scalp serums, hair masks, and leave-in treatments that capitalize on the skinification trend by applying skincare product concepts to hair care routines.

By Category: Conventional Dominance Faces Natural Challenge

Conventional and synthetic formulations maintain 74.03% market share in 2025, reflecting established consumer acceptance of proven ingredients and manufacturing cost advantages that enable competitive pricing. However, natural and organic products accelerate at 5.94% CAGR through 2031, indicating a fundamental shift in consumer preferences toward cleaner formulations despite higher price points. This growth trajectory suggests that natural products will capture increasing market share as supply chains mature and manufacturing costs decline through scale economies. The clean beauty trend gains momentum through social media education about ingredient safety and environmental impact, creating opportunities for brands that can communicate natural positioning authentically.

Regulatory frameworks currently lack formal recognition for "natural" or "organic" cosmetics categories in China, creating both opportunity and risk for brands making such claims. Companies must carefully substantiate natural claims to avoid regulatory scrutiny while building consumer trust through ingredient transparency and sustainable sourcing practices. The premium pricing associated with natural products creates margin opportunities for brands that can effectively communicate value propositions around safety, environmental responsibility, and efficacy. Conventional products retain advantages in performance consistency and regulatory predictability, but face increasing pressure to incorporate natural ingredients or develop hybrid formulations that combine synthetic efficacy with natural positioning.

By Price Range: Mass Market Stability Amid Premium Growth

Mass market products command 72.56% share in 2025, demonstrating the importance of accessible pricing in serving China's diverse economic landscape across tier-1 through tier-4 cities. This segment's stability reflects fundamental demand for basic hair care functionality at price points that accommodate varying disposable income levels throughout the country. Premium offerings grow at 5.05% CAGR through 2031, outpacing overall market expansion as consumers increasingly prioritize quality and efficacy over cost savings. The premium segment benefits from urbanization trends, rising disposable incomes, and social media influence that positions expensive products as status symbols and self-care investments.

Price segmentation increasingly correlates with distribution channels, as premium products find success through specialty retailers and e-commerce platforms that can provide detailed product information and customer reviews to justify higher costs. Mass market products maintain dominance in traditional retail channels like supermarkets and hypermarkets where purchase decisions often rely on brand recognition and promotional pricing. The growing middle class creates opportunities for mid-tier positioning between mass and premium segments, though this space faces intense competition from both domestic brands moving upmarket and international brands extending downmarket. Successful premium positioning requires consistent investment in product innovation, marketing, and retail experience to maintain differentiation from lower-priced alternatives.

By Distribution Channel: Digital Transformation Accelerates

Supermarkets and hypermarkets retain 35.05% market share in 2025, reflecting the continued importance of physical retail for routine hair care purchases where consumers value the ability to examine packaging and compare products directly. However, online retail stores surge at 5.29% CAGR through 2031, driven by livestreaming commerce, social platform integration, and the convenience of home delivery for bulky hair care products. This digital acceleration particularly benefits premium and specialized products that require detailed explanation and demonstration to communicate value propositions effectively. E-commerce platforms enable brands to reach consumers in lower-tier cities where physical retail presence may be limited, expanding addressable markets beyond traditional urban strongholds.

Specialty stores maintain relevance through expert consultation and product trial opportunities that online channels cannot replicate, though their growth remains constrained by higher operating costs and limited geographic reach. The "other distribution channels" category includes direct-to-consumer sales, salon retail, and emerging formats like subscription services that bypass traditional retail entirely. Digital transformation creates opportunities for brands to capture customer data, personalize marketing messages, and build direct relationships with consumers, though it also increases competition as barriers to market entry decline. Successful omnichannel strategies integrate online and offline touchpoints to provide seamless customer experiences while optimizing cost structures across different channel types.

Geography Analysis

China's hair care products market demonstrates significant regional variation in consumption patterns, with tier-1 cities like Beijing, Shanghai, Guangzhou, and Shenzhen driving premium product adoption while lower-tier markets provide volume growth opportunities through mass market positioning. The concentration of disposable income in major urban centers creates natural segmentation where international brands can command premium pricing for advanced formulations, while domestic brands leverage cost advantages to penetrate price-sensitive segments in smaller cities. Regional preferences also vary based on climate conditions, with humid southern regions driving demand for oil-control and anti-frizz products while northern areas prioritize moisturizing and damage repair formulations.

E-commerce platforms have democratized access to premium hair care products across geographic boundaries, enabling consumers in tier-3 and tier-4 cities to purchase international brands that previously required travel to major retail centers. This digital accessibility has accelerated market development in previously underserved regions while creating new competitive dynamics as local brands must compete with global offerings on the same platforms. Livestreaming commerce particularly benefits geographic expansion by providing product demonstration and expert consultation that traditionally required physical retail presence. The "sinking market" phenomenon, where urban consumption patterns spread to smaller cities through returning migrants and digital influence, creates growth opportunities for brands that can adapt premium positioning to local price sensitivities.

Distribution infrastructure improvements, including cold chain logistics and last-mile delivery capabilities, have reduced geographic barriers to market entry while enabling brands to maintain product quality across diverse climate conditions throughout China. Regulatory compliance remains consistent across regions through NMPA's centralized oversight, though local enforcement variations can create operational complexities for brands expanding beyond established markets. The integration of online and offline channels becomes particularly important in lower-tier cities where consumers may research products digitally but prefer to make initial purchases through physical retail to ensure product authenticity and quality.

Regulatory Landscape

China regulates hair care under the National Medical Products Administration (NMPA) through the Cosmetics Supervision and Administration Regulation (CSAR), classifying products as ordinary cosmetics or special cosmetics (notably hair dyes, perming products, and anti-hair loss products) with higher pre-market requirements for the latter. Compliance focuses on registrant or filing-person accountability for safety and truthful claims, with ingredient and sourcing disclosures managed through NMPA information service systems and increasing coordination with broader market supervision for advertising and labeling enforcement.

Regulatory modernization accelerated in late 2025, including NMPA Opinions (国药监妆〔2025〕18号, issued November 14, 2025) that prioritize reducing or waiving animal testing for certain categories such as perming products and non-oxidative hair dyes, supporting innovation and cross-border trade readiness. In December 2025, the NMPA initiated a pilot program for electronic labels to improve transparency and post-market oversight, reinforcing a digital-first compliance expectation for brands and manufacturers operating in China.

Competitive Landscape

China's hair care products market exhibits moderate concentration with established international players maintaining leadership through brand recognition, distribution scale, and R&D capabilities, while domestic challengers gain ground through digital-native strategies and localized product development. Market dynamics favor companies that can effectively navigate NMPA's regulatory requirements while building consumer trust through ingredient transparency and efficacy validation.

The competitive environment intensifies as traditional barriers to entry decline through e-commerce platforms and contract manufacturing availability, enabling new brands to reach consumers directly without extensive retail partnerships. Strategic differentiation increasingly centers on technological innovation, with companies investing in scalp diagnostics, personalized formulations, and sustainable packaging to create competitive moats that extend beyond traditional marketing approaches. Patent activity accelerates in areas like delivery systems, active ingredients, and manufacturing processes, as evidenced by CLEAR's three global patents for anti-dandruff formulations that provide regulatory protection and scientific credibility.

Opportunities emerge in specialized segments like men's grooming, children's formulations, and therapeutic treatments where regulatory barriers create natural protection for early movers willing to invest in compliance and clinical validation. The integration of artificial intelligence for personalized product recommendations and supply chain optimization becomes a competitive necessity as consumer expectations for customization and convenience continue to rise. Companies that focus on developing clean and sustainable formulations within these specialized segments gain significant market advantage, particularly as consumers become more ingredient-conscious. Additionally, the rising demand for multi-functional products that combine treatment and preventive properties creates new opportunities for product innovation and market expansion.

China Hair Care Industry Leaders

-

Procter & Gamble

-

Unilever

-

L’Oréal S.A.

-

Beiersdorf AG

-

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Scalp care and dermatology-adjacent positioning remain a core whitespace, supported by visible brand actions that blend clinical narratives with premium cues, such as CLEAR introducing its SCALPCEUTICALS PRO RANGE in Shanghai in 2025 with dermatologist involvement and patented technologies. Another opportunity area sits in special-cosmetics categories where registration complexity acts as a moat (for example, hair dyes and anti-hair loss products), favoring companies that can sustain testing, claims substantiation, and end-to-end documentation under CSAR while converting that compliance into consumer trust on social and e-commerce channels.

Go-to-market and operating-model opportunities are concentrated in social commerce and omnichannel execution beyond tier-1 cities, where online discovery converts quickly via livestreaming and brands can build repeat purchase through data-driven personalization. China-based scale players are also demonstrating distribution playbooks that combine platform dominance with offline reach, illustrated by Fandow describing a dual-engine approach for KONO across Douyin and more than 25,000 retail outlets. On the supply side, inland clusters and cross-border e-commerce capabilities are upgrading the ecosystem around hair-related categories (including Xuchangs large base of wig enterprises using platforms such as TikTok Shop and Amazon), creating partnership and sourcing options for brands expanding portfolios across hair care, color, and adjacent hair aesthetics.

Recent Industry Developments

- July 2026: Kao announced that its Liese hair color series featuring newly developed H-Linx TECH will roll out across seven Asian countries and regions, including China, starting in August 2026. The move strengthens Kaos color portfolio in China with a technology-led proposition and adds competitive pressure in DIY and at-home color where innovation cycles are fast.

- April 2025: Unilever launched the CLEAR SCALPCEUTICALS PRO RANGE in Shanghai and positioned it around patented scalp-repair technologies and dermatologist collaboration. This reinforced the premium, science-backed scalp-care direction in China and raised the bar for efficacy narratives and claims substantiation in anti-dandruff and scalp-treatment segments.

- December 2024: Keune Haircosmetics expanded into China as part of its broader Asia growth strategy in professional hair care. The entry increased competitive intensity in salon-linked and professional-grade channels, where education, performance credibility, and distribution partnerships shape brand adoption.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the China hair care market is defined as the value of products bought for routine hair and scalp cleansing, conditioning, treatment, coloring, and styling, across retail and salon-linked purchase points, measured in current USD.

Scope exclusions: We exclude hair tools and appliances, wigs and extensions, and professional salon service revenue that is not tied to product sales.

Segmentation Overview

-

By Product Type

- Shampoo

- Conditioner

- Hair loss treatment products

- Hair Colorants

- Hair Styling Products

- Other Product Types

-

By Category

- Natural/Organic

- Conventional/Synthetic

-

By Price Range

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/ Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the base structure of the model and to anchor assumptions that can be checked independently. We mainly reviewed public statistics and rules that affect cosmetics and personal care in China, then translated them into demand and pricing signals that fit the hair care category.

Sources referenced include, for example, the National Bureau of Statistics of China for consumer and retail indicators, China Customs for import and export signals relevant to finished products and key inputs, the National Medical Products Administration for regulatory updates and compliance themes, and publicly available publications from groups such as the Personal Care Products Council and other personal care associations. We also used company annual reports, investor presentations, earnings commentary, and reputable press coverage, supported by paid subscriptions for company financial intelligence, news and financials, and patent databases to track innovation intensity and claim trends. This list is illustrative and not exhaustive, since many other public documents were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test what we saw in public data, especially on pricing ladders, channel mix shifts, and how fast premium and mass products are moving in different city tiers. We spoke with a mix of manufacturers, distributors, retailers, and salon channel participants, and then aligned their inputs into one consistent view of volumes, typical pack sizes, and promotion intensity across China.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | |

| Mid tier: 52% | Functional/Unit leaders: 35% | |

| Smaller Players: 18% | Managers: 51% |

Market-Sizing & Forecasting

Sizing starts with a top-down rebuild of the demand pool using China personal care spend direction, hair care category share signals, and channel-level retail movement indicators, and then converting those into value using observed price bands. Once that anchor is set, we corroborate it with selective bottom-up approximations, such as sampling brand and retailer price ladders, checking typical SKU throughput by channel, and rolling up a limited set of supplier and distributor revenue disclosures to adjust the final totals.

Key inputs used in the model include average selling price movement by mass and premium tiers, online versus offline channel mix, share shift toward treatment and scalp-care products, frequency of promotions and bundle packs, and urbanization driven demand differences across city tiers. For forecasting, scenario analysis is used, and then the final curve is guided by expert consensus on how pricing, premiumization, and e-commerce penetration are expected to evolve over the forecast window. When bottom-up checks have gaps, we fill them using conservative ranges from interviews and then test the impact by re-running the model under alternate price and mix assumptions.

Data Validation & Update Cycle

Outputs are validated through cross-checks against independent signals, such as reported beauty and personal care retail trends, channel expansion patterns, and observable pricing moves in major online storefronts and modern trade. If a variance looks high, we recheck the underlying drivers, and trigger follow-up calls to confirm whether the change is real or a data timing issue.

Before sign-off, the model and assumptions go through multi-step analyst reviews that focus on outliers, currency consistency, and year-on-year reasonableness by category and channel. The report is refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is done so clients receive the most current view.

Mordor Intelligence's China Hair Care Market Market Size Compared Against Other Published Estimates

It is normal to see different market size numbers for China hair care because publishers do not always count the same product set, sales channels, or pricing basis, even when the title looks similar. Variances also come from whether a study uses retail value, manufacturer sales value, or a blended view, and whether the year is treated as actuals or partly forecasted.

Some estimates expand the scope by adding adjacent beauty categories or by treating salon services and tools as part of hair care. The table highlights that spread. In Mordor Intelligence's case, only hair care product value is counted, and tools, wigs, and non-product salon service revenue are excluded to keep the total tied to repeatable demand and price inputs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.05 B (2025) | |

| Industry Publisher A | USD 15.55 B (2025) | Uses a broader retail-value interpretation that can pull in a wider set of hair-related purchases and regional rollups, which tends to lift the 2025 total versus a product-only count. |

| Industry Publisher B | USD 5.10 B (2025) | Likely reflects a narrower coverage or a different value layer (for example, selected channels, tracked brands, or manufacturer-level revenue), which typically undercounts premium online sales and the long tail of SKUs. |

Taken together, the comparison suggests that the biggest drivers are scope and the value layer being measured, followed by how pricing and channel mix are refreshed for the base year. By keeping assumptions traceable to category mix, channel shares, and price tiers, the approach gives decision-makers a number that can be rechecked and updated in a practical way.

Key Questions Answered in the Report

How big is the China hair care products market in 2026?

It is valued at USD 13.62 billion and is set to grow at a 4.40% CAGR to 2031.

Which product category grows fastest within China’s hair care segment?

Hair styling products post the quickest expansion at a 4.86% CAGR through 2031.

What drives premium hair-care demand in China?

Rising disposable incomes, “skinification” of routines, and social-media influence push consumers toward clinically proven, higher-priced formulations.

How significant is e-commerce for Chinese hair care sales?

Online channels grow at a 5.29% CAGR, powered by livestreaming and integrated social-commerce checkout features.

Page last updated on: