Central And Eastern Europe (CEE) Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

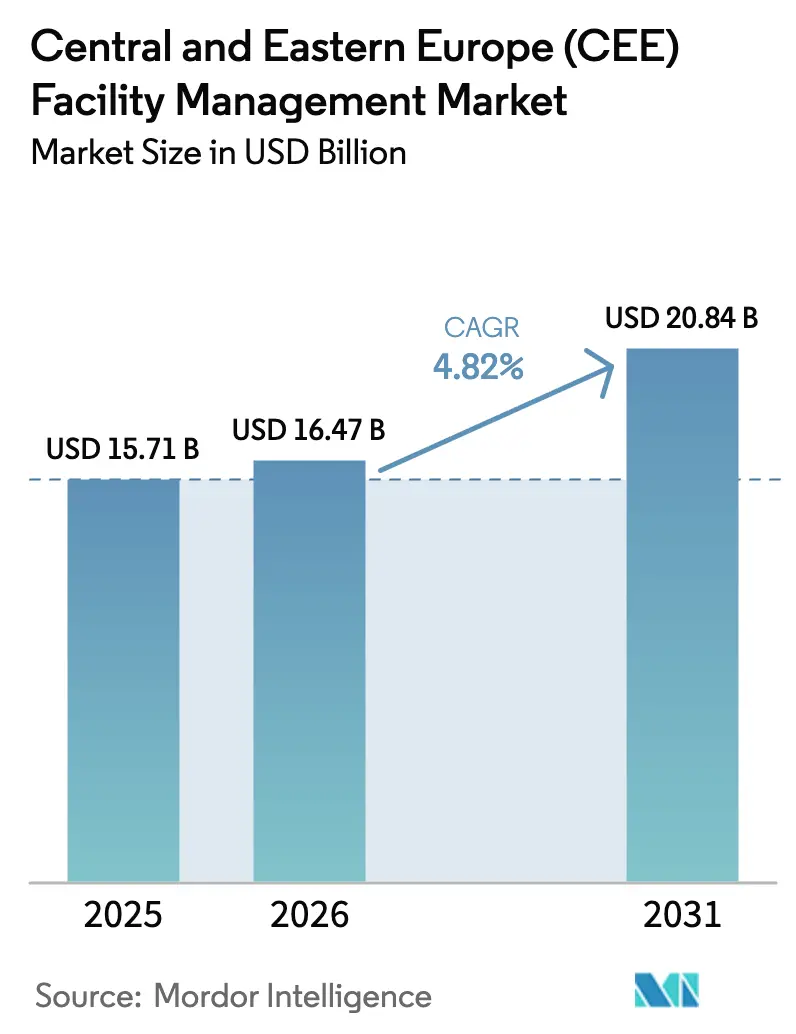

| Base Year Market Size (2025) | USD 15.71 Billion |

| Market Size (2026) | USD 16.47 Billion |

| Market Size (2031) | USD 20.84 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

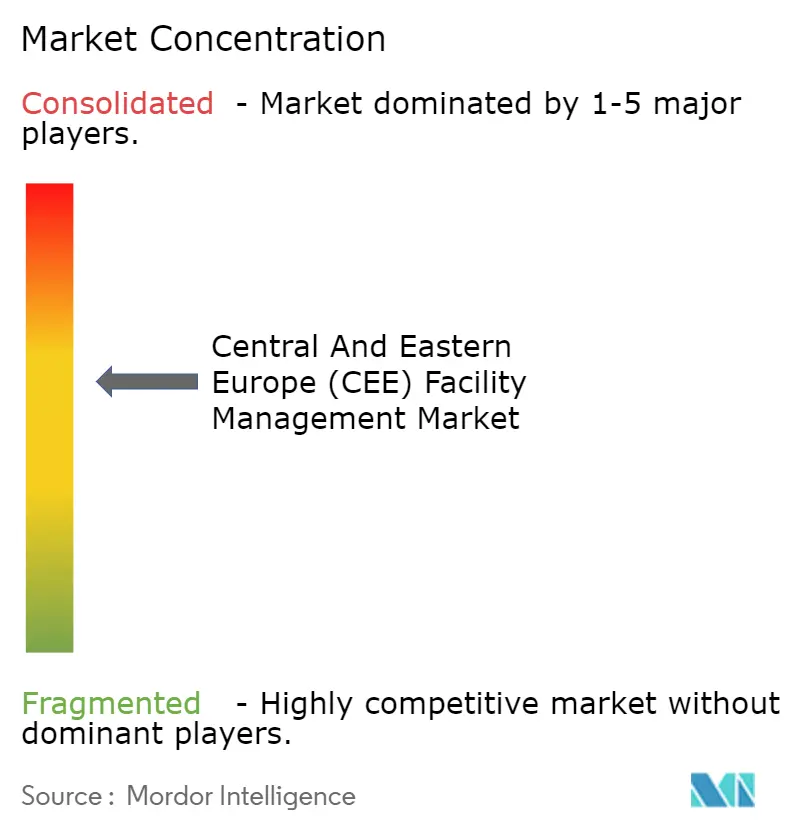

| Market Concentration | Medium |

Major Players_Facility_Management_Market_comapny_logog.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central And Eastern Europe (CEE) Facility Management Market Analysis by Mordor Intelligence

The CEE facility management market size is expected to grow from USD 15.71 billion in 2025 to USD 16.47 billion in 2026 and is forecast to reach USD 20.84 billion by 2031 at 4.82% CAGR over 2026-2031. This expansion is propelled by sustained infrastructure modernization, stringent EU-aligned efficiency rules, and the preference for outsourced, technology-enabled services that cut operating costs while ensuring regulatory compliance. Technology adoption, notably AI-driven predictive maintenance and IoT-enabled energy management, is moving the market toward data-led, performance-based contracts that help clients meet ESG targets.[1]European Investment Bank, “Two European companies are transforming IoT from Poland and Lithuania,” eib.org Consolidation among global and regional providers is intensifying but local specialists still capture niche contracts that demand on-the-ground expertise. Labor cost inflation and supply-chain volatility pose near-term pressures, yet the drive for energy savings and standardized service levels in commercial real estate keeps overall demand resilient.

Key Report Takeaways

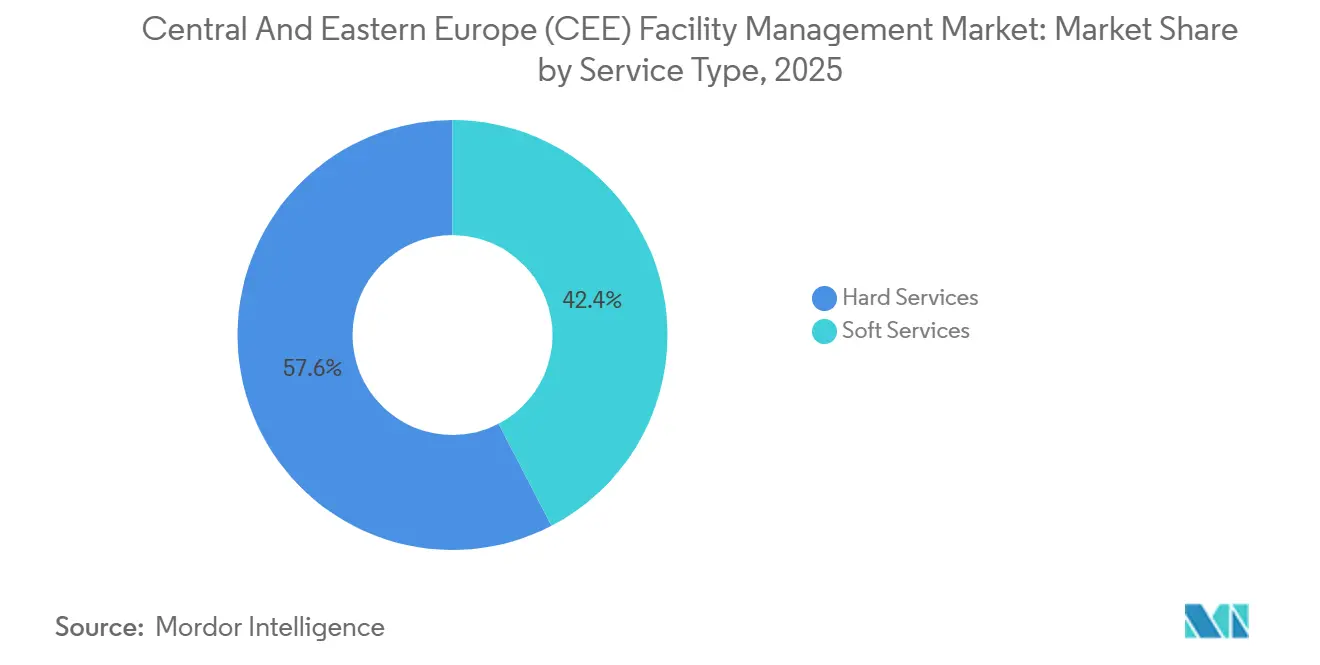

- By service type, hard services held 57.62% of the CEE facility management market share in 2025 while soft services are projected to grow at a 6.05% CAGR through 2031.

- By offering type, outsourced solutions commanded 64.20% of the CEE facility management market size in 2025 and are set to expand at a 6.78% CAGR between 2026 and 2031.

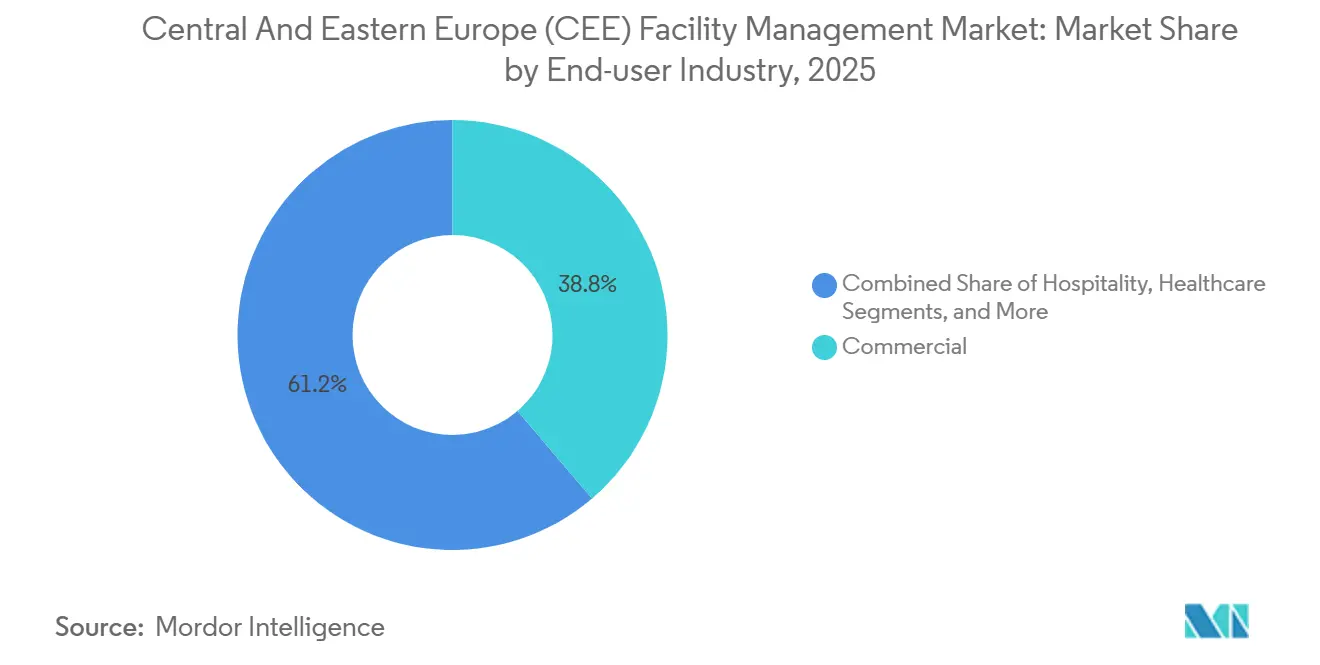

- By end-user industry, the commercial segment led with 38.76% of the CEE facility management market share in 2025 whereas the institutional and public infrastructure segment is forecast to post an 8.09% CAGR to 2031.

- By geography, Poland accounted for 55.10% of the CEE facility management market in 2025 and the Slovak Republic is expected to register the fastest 7.51% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Central And Eastern Europe (CEE) Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Infrastructure Development | +1.2% | Poland, Czech Republic, Romania | Medium term (2-4 years) |

| Rising Outsourcing in Building Management | +1.5% | Global CEE region | Short term (≤ 2 years) |

| Heightened Safety and Security Needs | +0.8% | Urban centers across CEE | Short term (≤ 2 years) |

| Technological Advancements in Facility Management | +1.1% | Poland, Czech Republic, Hungary | Medium term (2-4 years) |

| Expansion of Commercial Real Estate with International Tenants | +0.9% | Major cities: Warsaw, Prague, Budapest | Medium term (2-4 years) |

| Growing Emphasis on ESG Compliance and Energy-Efficient Operations | +1.0% | EU-aligned CEE countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Infrastructure Development

Government-backed construction programs, new building codes, and foreign direct investment are reshaping service demand across the CEE facility management market. Poland’s technical conditions that took effect in August 2024 introduced stricter energy-efficiency and spacing rules, prompting developers to seek specialist FM partners for asset compliance.[2]DWF Group, “Construction Insights May 2024: Poland,” dwfgroup.com The Czech Republic’s BIM requirement for public projects above USD 11.23 million starting 2025 is creating new revenue streams for data-rich lifecycle management services.[3]Ewelina Mitera-Kiełbasa and Krzysztof Zima, “BIM Policy in Eastern Europe,” bibliotekanauki.pl Romania’s USD 40.6 million EIB-financed university campus upgrade underscores broader public-sector modernization that relies on integrated FM to manage complex utilities and safety systems. Large industrial investments, such as onsemi’s USD 2 billion semiconductor plant in the Czech Republic, are further lifting demand for high-specification hard services. The cumulative effect is a steady pipeline of assets needing long-term technical stewardship that fuels market growth.

Rising Outsourcing in Building Management

Regulatory complexity and standardized service expectations are accelerating the switch from in-house teams to professional providers across the CEE facility management market. Hungary’s amended energy-efficiency law, which doubles mandatory savings to 1.4% per year from 2025, is compelling asset owners to tap external expertise that can implement specialized retrofits at scale. Poland’s digitalized work-permit regime effective June 2025 eases cross-border labor deployment, helping multinational FM firms mobilize skilled technicians quickly. Region-wide adoption of the EU Minimum Wage Directive is harmonizing pay structures and amplifying economies of scale that favor large, integrated vendors. High-value multi-site wins exemplified by ISS’s 7-year contract for the UK Department for Work and Pensions highlight the cost and performance advantages driving outsourcing momentum.

Heightened Safety and Security Needs

The security remit facing FM providers is widening from physical protection to include cybersecurity, structural safety, and emergency preparedness. The EU AI Act, effective from August 2024, categorizes building security AI as high-risk, compelling providers to embed robust compliance protocols in surveillance and access-control deployments. Romania’s 2025 balcony-safety law, which mandates civil-liability insurance and load limits, illustrates how niche regulations expand FM service scope into previously unmanaged areas. IoT sensor rollouts by suppliers such as Kontakt.io are delivering energy savings of up to 35% while concurrently improving real-time threat detection. Healthcare, a highly regulated segment, is seeing rapid uptake of integrated security and infection-control packages that can meet stringent accreditation requisites.

Technological Advancements in Facility Management

AI, digital twins, and advanced IoT networks are propelling the CEE facility management market from reactive maintenance toward predictive, data-driven operations. Case studies from Ireland and Greece show the PHOENIX platform cutting energy use by 61% in commercial buildings, proof of scalable savings potential. Predictive HVAC algorithms are slashing downtime by 75% and halving repair lead times. Czech buildings already average annual efficiency gains of 1.5%, a figure expected to climb as automated controls proliferate. Digital twins allow continuous optimization of thermal comfort and asset longevity, delivering measurable returns for both landlords and tenants. Vendors that can demonstrate quantified performance improvements are winning competitive bids more frequently.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex and Varying Regulatory Frameworks for New Market Entrants | -0.7% | Cross-border operations in CEE | Medium term (2-4 years) |

| Sensitivity of FM Demand to Macroeconomic Indicators and Construction Cycles | -0.9% | All CEE countries | Short term (≤ 2 years) |

| Regulatory and Legislative Framework for Market Entrants | -0.5 | All CEE countries | Short term (≤ 2 years) |

| Impact of Macroeconomic Indicators on FM Demand | -0.1 | All CEE countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex and Varying Regulatory Frameworks for New Market Entrants

Cross-border expansion is slowed by disparate tax rules, permitting procedures, and labor codes, each requiring distinct compliance toolkits. Poland’s 2025 property-tax reform introduces separate definitions for buildings and structures, forcing FM firms to re-evaluate asset classifications and documentation processes. The Czech Republic’s new construction law adds compulsory energy-performance certificates at the occupancy stage, lengthening project timelines. Romania’s lease approvals on state-owned educational property now demand ministerial clearance, adding administrative overhead for FM bids on campus upgrades. Such divergence obliges multinational providers to maintain multiple legal teams, raising fixed costs and slowing market penetration.

Sensitivity of FM Demand to Macroeconomic Indicators and Construction Cycles

High interest rates, commodity-price swings, and supply-chain disruptions transmit quickly to facility management budgets. Research on construction contracts finds that price-escalation clauses and backend fees expose FM clients to hidden cost upsides that erode margins. Insurance premiums have risen in tandem with broader risk perceptions, as evidenced by Vienna Insurance Group’s 10.7% revenue growth in the CEE region for Q1 2025. Global guidance downgrades from providers such as Sodexo confirm how macro headwinds can temper service-sector revenue expansion. Although technology-based efficiency gains offset some pressure, cyclical volatility remains an inherent restraint on short-term demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Remain the Backbone of Modern Assets

Hard services anchored 57.62% of 2025 revenue, reflecting building-owner priorities around asset protection, mandatory inspections, and fire-safety system uptime. Poland’s post-2024 code revisions that mandate enhanced insulation and modern HVAC systems have spurred a wave of retro-commissioning contracts that keep the hard-services pipeline active. Predictive maintenance is shortening repair cycles and extending asset life, delivering the highest return on investment among service lines.

Soft services will outpace at a 6.05% CAGR as occupiers sharpen focus on workplace hygiene, security, and user experience. High-density office hubs in Warsaw, Prague, and Budapest are adopting smart-cleaning programs using telemetry data to align staffing to real-time occupancy, a shift that improves quality while trimming labor hours. Catering and reception services are being redesigned around hybrid work patterns, with modular menus and digital visitor management enhancing flexibility.

By Offering Type: Outsourcing Becomes Mainstream Across Property Classes

The outsourced model captured 64.20% of 2025 value and is projected to rise 6.78% annually as landlords and corporates view FM as a strategic lever rather than a cost center. Multi-disciplinary contracts bundle cleaning, technical, and security services under unified service-level agreements that emphasize uptime and ESG metrics. The CEE facility management market size for integrated contracts is set to expand fastest, supported by clients seeking single-invoice simplicity and data transparency.

Single and bundled FM offerings serve as entry paths for organizations with unique requirements or risk appetites. In-house teams persist in niche segments such as heritage sites where on-site knowledge and regulatory exemptions favor internal control. Nevertheless, technology investment needs and wage inflation continue to tilt the calculus toward professional partners that can spread costs across large portfolios.

By End-user Industry: Commercial Stock Leads, Public Assets Accelerate

Commercial real estate delivered 38.76% of 2025 revenue, anchored by Grade-A offices, logistics hubs, and data centers that demand premium uptime and certified sustainability. International occupiers drive uniform service expectations, making vendor consistency a critical differentiator. Retail landlords are upgrading common areas to attract footfall, feeding demand for advanced lighting, air-quality monitoring, and omnichannel visitor services.

Public-sector and institutional estates are the quickest risers with an 8.09% CAGR outlook as EU funds finance hospital, university, and transport-hub renewals. Energy-performance contracting, lifecycle management, and compliance reporting form the core scope of work. Healthcare campuses require high-frequency cleaning and specialized waste disposal, while universities seek space-usage analytics to optimize timetabling and utility bills. These needs position integrated providers to secure multi-year frameworks that underpin predictable cash flows.

Geography Analysis

Poland anchors the CEE facility management market with 55.10% revenue share in 2025, underpinned by its status as the region’s largest economy and most advanced commercial property hub. Regulatory reforms that favor outsourced models, combined with major urban redevelopment in Warsaw and regional centers, sustain a robust pipeline of hard and soft service contracts. Streamlined work-permit rules effective 2025 remove administrative friction for inbound technical specialists, adding further scale advantages for multinational providers.

The Slovak Republic is the fastest-growing geography at a 7.51% CAGR through 2031. EU structural funds directed at logistics parks and automotive manufacturing have created steady demand for energy-managed facilities. Institutional investors acquired USD 35.5 million of industrial stock in early 2025, signaling confidence in local real-asset fundamentals and the need for professional FM operations.

Hungary and Romania advance on the back of strict energy-saving mandates and public-infrastructure upgrades. Hungary’s higher annual saving target of 1.4% from 2025 lifts the addressable market for audit and retrofit services. Romania’s university-campus modernization financed by the EIB exemplifies expanding institutional opportunities. The Czech Republic benefits from large-scale foreign industrial projects like onsemi’s silicon-carbide facility, which demands specialist clean-room, utilities, and reliability programs.

Balkan and Baltic states show emerging potential as EU accession talks and green-deal funding direct capital toward transport corridors, smart ports, and modern healthcare estates. Russia’s share remains limited due to geopolitical uncertainties and restricted capital inflows, leading most international FM providers to concentrate on EU-aligned territories.

Competitive Landscape

The market is moderately fragmented, with the top five providers accounting for roughly 35% of regional revenue. Global giants ISS, Sodexo, and CBRE leverage scale, technology investment, and standardized processes to win cross-border accounts. CBRE’s 2025 consolidation of its Enterprise, Local, and Property Management operations into the Building Operations and Experience segment strengthens its single-platform proposition and widens client wallet share.

Regional specialists maintain strong footholds through cultural familiarity and niche expertise, particularly in sectors like manufacturing clean rooms, healthcare campuses, and municipal utilities where local regulations are intricate. Partnerships between tech innovators such as Kontakt.io and mainstream FM firms illustrate how data-centric solutions are enhancing competitive differentiation via demonstrable cost savings.

Mergers and acquisitions remain a key route to geographic expansion. Wood & Company’s 2024 entry into Polish property management shows how asset-acquisition strategies and FM service provision increasingly intersect. Providers are also hiring senior ESG and digital-innovation executives to institutionalize sustainability and analytics capabilities that clients now consider baseline requirements.

Central And Eastern Europe (CEE) Facility Management Industry Leaders

Strabag SE

Bilfinger SE

Dussmann Group

SIMACEK GmbH

OKIN Facility (OKIN Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: EY assisted Solida Capital in acquiring the Victoria Center office building in Bucharest, highlighting continuous foreign capital inflow into assets that require professional FM stewardship.

- January 2025: CBRE Group formed the Building Operations & Experience unit after its USD 800 million Industrious acquisition, unifying its FM and property-management services.

- January 2025: Sodexo acquired CRH Catering, broadening its soft-services portfolio in North America and reinforcing global integrated-service competence.

- June 2024: onsemi selected the Czech Republic for a USD 2 billion end-to-end silicon-carbide production plant, creating long-term demand for high-spec FM.

Central And Eastern Europe (CEE) Facility Management Market Report Scope

Facility management services involve building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management and soft facility management spheres.

The study tracks the facility management (FM) industry-related trends in CEE by analyzing the industry turnover accrued through end-user contracts by the service providers. The study tracks the revenues accrued from services offered for building operation and maintenance (mechanical and electrical services, heating and ventilation, plumbing, building services control and management systems, building fabric portable application testing, fire protection systems, fire alarm and detection systems), environmental management (energy management services, waste management, recycling services), IT and Telecommunication (establishment and maintenance of IT systems, the introduction of software packages), support services (cleaning, catering, vending, courier services, laundry services, post room staffing and management, reception staffing, security) and property management (space planning and design, asset management, property acquisitions and disposals, relocation management).

The Central and Eastern Europe (CEE) facility management market is segmented by offering (Hard FM, Soft FM), type (In-house Facility Management, Outsourced Facility Management), country (Poland (current market scenario and share of outsourced FM), end user (commercial buildings, retail, government and public entities), Hungary (current market scenario and share of outsourced FM), end user (commercial buildings, retail, government and public entities), Romania (current market scenario and share of outsourced FM), end user (commercial buildings, retail, government and public entities), Slovak Republic (current market scenario and share of outsourced FM), end user (commercial buildings, retail, government and public entities), Slovenia (current market scenario and share of outsourced FM), end user (commercial buildings, retail, government and public entities), Czech Republic (current market scenario and share of outsourced FM), end user (commercial buildings, retail, government and public entities), Turkey (current market scenario and share of outsourced FM), end user (commercial buildings, retail, government and public entities), Bosnia, Serbia, Croatia, Russia). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

| Commercial (IT and Telecom, Retail and Warehouses) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| Poland |

| Hungary |

| Romania |

| Slovak Republic |

| Slovenia |

| Czech Republic |

| Bosnia and Herzegovina |

| Serbia |

| Croatia |

| Russia |

| Rest of Central and Eastern Europe |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Country | Poland | |

| Hungary | ||

| Romania | ||

| Slovak Republic | ||

| Slovenia | ||

| Czech Republic | ||

| Bosnia and Herzegovina | ||

| Serbia | ||

| Croatia | ||

| Russia | ||

| Rest of Central and Eastern Europe | ||

Key Questions Answered in the Report

What is the current size of the CEE facility management market?

The market is valued at USD 16.47 billion in 2026 and is projected to reach USD 20.84 billion by 2031.

Which service type dominates spending?

Hard services lead with 57.62% of 2025 revenue as owners prioritize asset integrity and regulatory compliance.

Why is outsourcing growing so quickly?

Regulatory complexity, standardized ESG requirements, and technology investment needs are prompting organizations to shift from in-house teams to specialized FM providers.

Which country is expanding the fastest?

The Slovak Republic is set to grow at a 7.51% CAGR between 2026 and 2031 due to manufacturing and logistics investment backed by EU funds.

How are technology trends shaping the industry?

AI-driven predictive maintenance, IoT-enabled energy management, and digital twins are lowering downtime and energy costs, making data-driven FM contracts increasingly mainstream.

What is the outlook for integrated facility management contracts?

Integrated contracts, already 64.20% of revenue in 2025, are forecast to expand at 6.78% annually as clients seek single-source solutions with performance guarantees.

Page last updated on: