Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

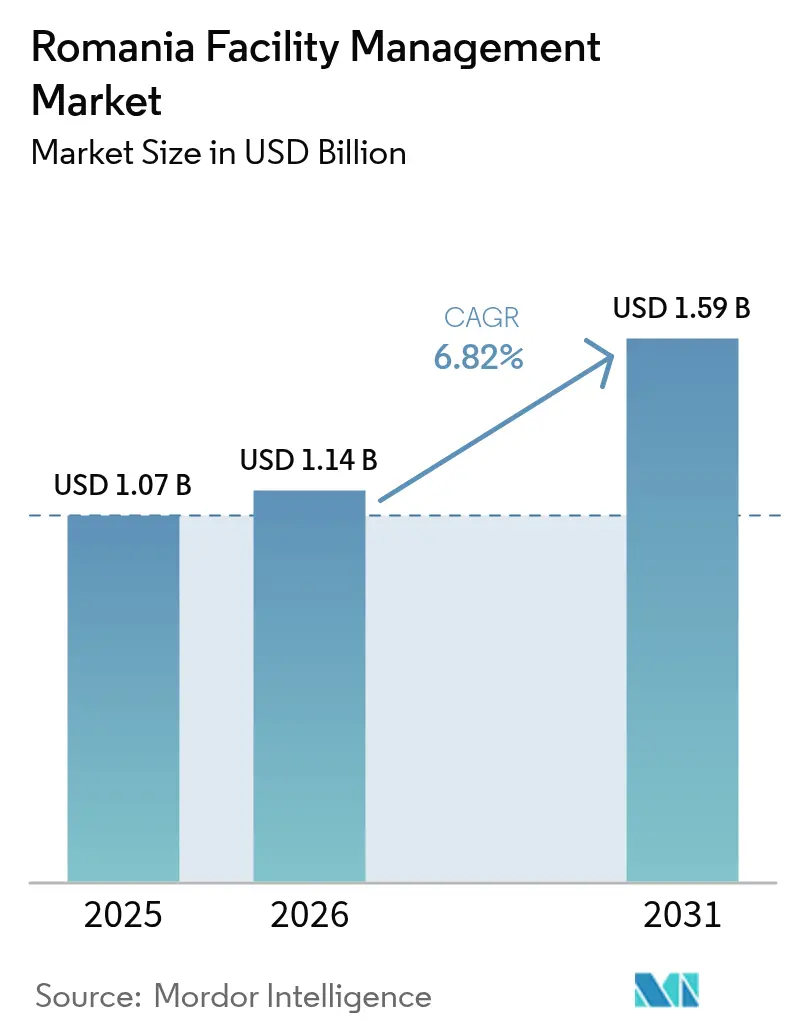

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.14 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

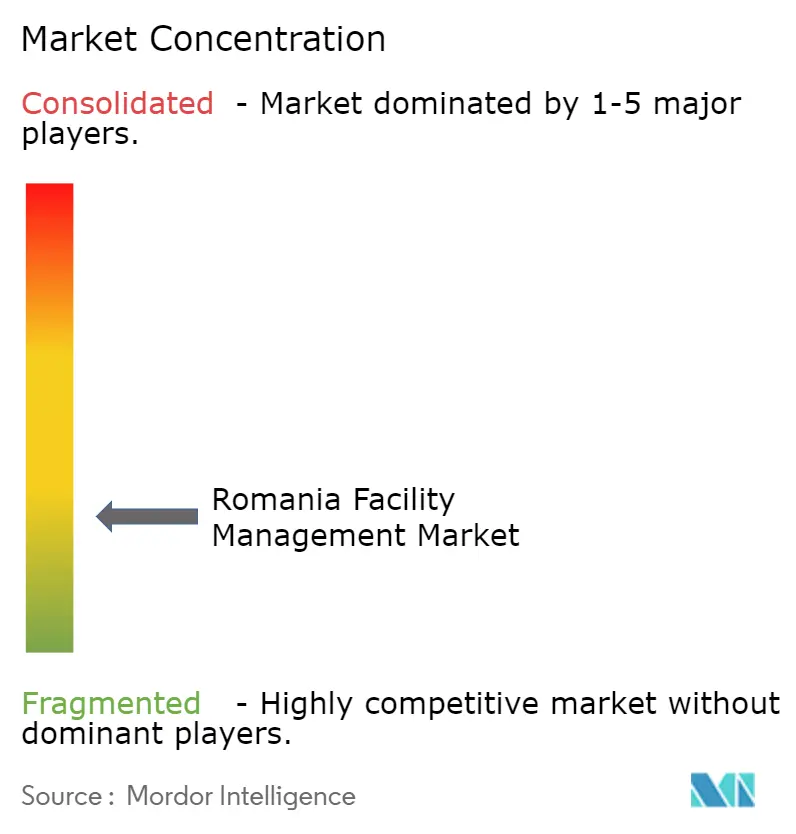

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania Facility Management Market Analysis by Mordor Intelligence

The Romania facility management market size is expected to grow from USD 1.07 billion in 2025 to USD 1.14 billion in 2026 and is forecast to reach USD 1.59 billion by 2031 at 6.82% CAGR over 2026-2031. The Romania facility management market is expanding as nearshoring inflows accelerate industrial construction, while EUR 29.2 billion in Recovery and Resilience Plan funding drives public-sector outsourcing. Energy-efficiency mandates, digital building technologies and outcome-based contracts are reshaping service scopes, prompting enterprises to seek integrated providers that manage both hard and soft tasks under a single agreement. The Romania facility management market also draws momentum from rising ESG commitments; developers are embedding IoT sensors, AI-enabled maintenance tools and green-building certifications to meet EU benchmarks. Competitive differentiation hinges on technology adoption, as volatile utility prices and looming inflation create cost-containment pressures that reward data-driven efficiency gains.

Key Report Takeaways

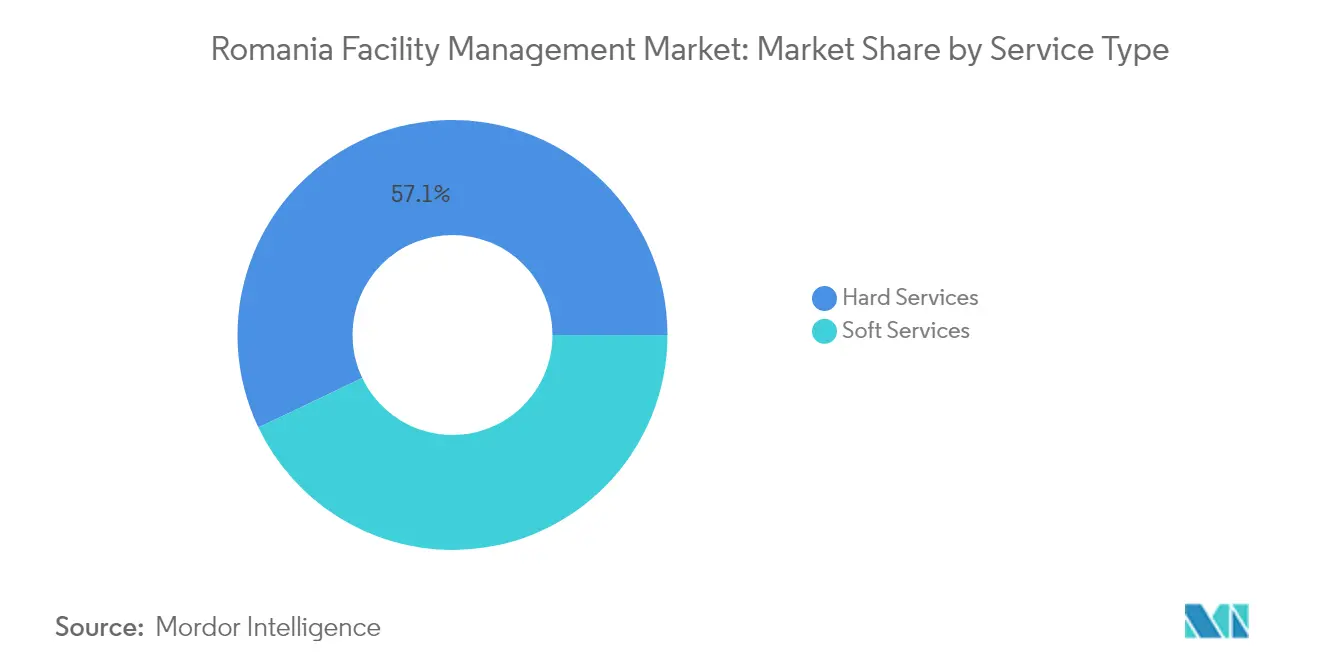

- By service type, hard services accounted for 57.08% of the Romania facility management market share in 2025, while soft services are forecast to grow at a 7.03% CAGR through 2031.

- By offering type, the outsourced segment commanded 62.85% of the Romania facility management market size in 2025 and is projected to expand at a 6.74% CAGR to 2031.

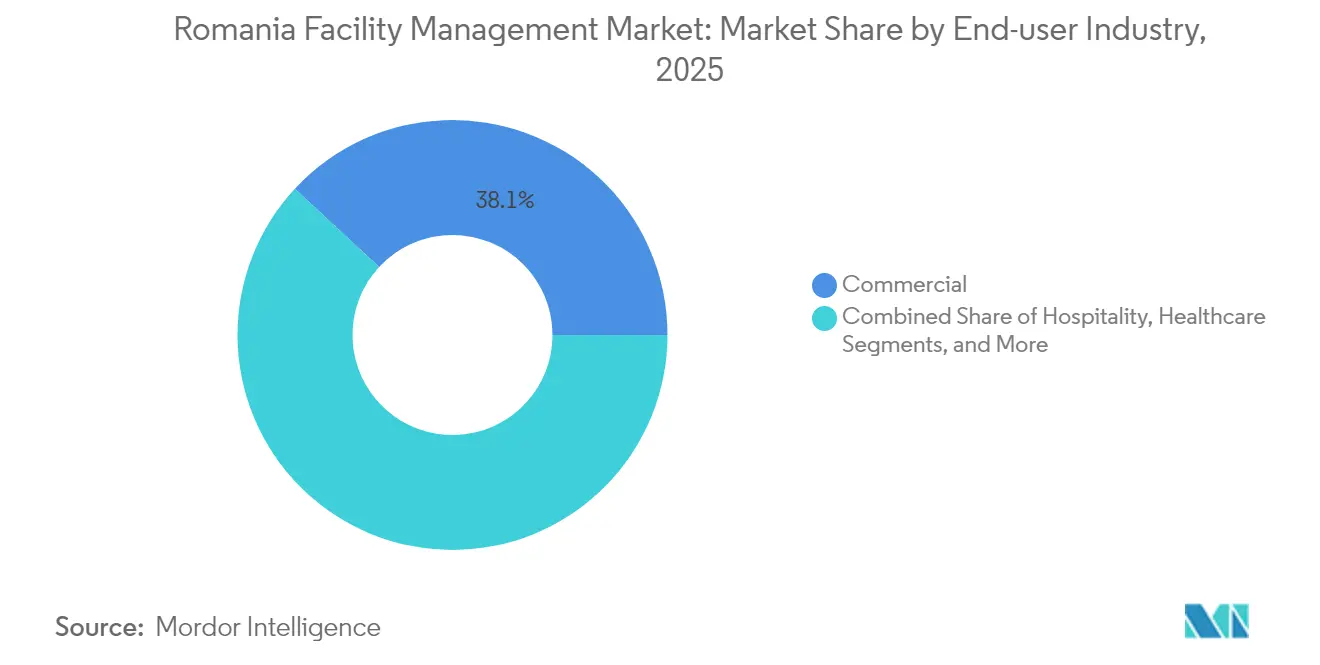

- By end-user industry, commercial facilities led with 38.10% share of the Romania facility management market size in 2025, whereas institutional and public infrastructure is advancing at an 8.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Romania Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising corporate outsourcing of non-core services | +1.8% | Bucharest, Cluj-Napoca, Timișoara | Medium term (2-4 years) |

| Growing adoption of integrated FM contracts | +1.5% | National, industrial corridors | Medium term (2-4 years) |

| Energy-efficiency and green-building mandates | +1.2% | National, EU-wide compliance | Long term (≥ 4 years) |

| EU RRF funding spurs public-sector outsourcing | +1.0% | Priority infrastructure regions | Short term (≤ 2 years) |

| Nearshoring-induced industrial expansion | +0.9% | Brașov, Timișoara, Constanța | Medium term (2-4 years) |

| Digitalization and IoT-enabled maintenance | +0.6% | Urban technology hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Corporate Outsourcing of Non-Core Services

Multinational manufacturers and technology firms increasingly relinquish in-house facilities teams to concentrate on core operations. Ford’s USD 300 million upgrade of its Craiova plant and Arctic’s EUR 37.8 million capacity expansion at Ulmi illustrate how production sites seek specialized MEP and fire-safety partners for compliance and uptime assurance. Outsourcing demand is most visible around Bucharest and Cluj-Napoca, where complex automated lines require predictive maintenance schedules aligned with ISO standards. Contract durations have lengthened beyond three years, reflecting client appetite for lifecycle cost certainty and service-level guarantees. Tier-one suppliers mirror this pattern, accelerating bundled hard-service deals that embed digital monitoring for energy, HVAC and critical utilities. The Romania facility management market benefits as global procurement teams recognise Romania’s engineering talent pool and competitive wage structure.

Growing Adoption of Integrated FM Contracts

Enterprises are consolidating disparate tasks-security, cleaning, catering, technical upkeep-into single multi-year frameworks. MKS Instruments’ 6,500 m² expansion in Bucharest deploys an integrated model so that cleanroom, utilities, and waste-handling teams share data flows and coordinated schedules.[1]MKS Instruments, “Relocation & Expansion of MKS Bucharest Romania Production Site,” mks.com Logistics developer CTP added almost 2 million m² of leases in 2024; most tenants requested bundled FM agreements covering energy optimisation, access control and landscaping. Integrated contracts cut transaction costs for clients while yielding continuous-improvement incentives for providers, who apply IoT platforms to predict faults, benchmark performance and issue consolidated KPI dashboards. The Romania facility management market thus sees a gradual shift from price-per-task quotes to outcome-based remuneration pegged to uptime, energy savings and occupant satisfaction indices.

Energy-Efficiency and Green-Building Certification Mandates

EU directives push facilities toward LEED and BREEAM labels, triggering demand for sensor-rich building-management systems. Genesis Property targets net-zero emissions by 2040, validating science-based targets and requesting suppliers to align on CO₂ reduction roadmaps. Romania’s Recovery Plan allocates EUR 1.2 billion for waste infrastructure and retrofits, propelling public authorities to embed energy audits and LED relighting into tenders. Facility managers now equip assets with sub-metering, air-quality probes and cloud analytics that fine-tune HVAC loads. Green mandates also influence material choices, requiring certified cleaning agents and recyclable consumables. Providers able to document carbon savings can charge premium rates, reinforcing a quality-over-price dynamic within the Romania facility management market.

EU RRF Funding Spurs Public-Sector Outsourcing

Recovery Facility grants accelerate healthcare and education projects that recruit private FM specialists. The European Investment Bank’s EUR 1 billion pipeline in 2024 underwrote hospital refurbishments and coastal-protection works that bundle maintenance, security and technical support in multi-year service contracts. Public buyers leverage outsourcing to access modern CAFM software without upfront capex and to comply with EU performance criteria. Outcome-linked payment schemes now reward providers for energy-intensity cuts, infection-control scores, and asset-availability thresholds. This mechanism shifts risk to contractors yet creates stable revenue streams, enhancing the attractiveness of the Romania facility management market for global vendors seeking predictable cash flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile utility costs increase contract risk | −1.2% | National, energy-intensive sites | Short term (≤ 2 years) |

| Highly fragmented supplier base | −0.8% | National, especially secondary cities | Medium term (2-4 years) |

| Lengthy digital permit approvals | −0.5% | National | Medium term (2-4 years) |

| Informal service providers intensify competition | −0.3% | Smaller municipalities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Utility Costs Increase Contract Risk

The National Bank projects a 15% hike in power bills after price caps lapse, forcing providers to renegotiate tariff pass-through clauses. Data-center operator ClusterPower installs efficient cooling achieving a 1.1 PUE to shield clients from spikes.[2]Cisco, “Cisco Case Study: ClusterPower,” cisco.com Nonetheless, thin-margin FM firms face liquidity strain when electricity and gas exceed budgeted thresholds. Some clients switch from fixed-rate to indexed contracts, demanding transparent metering and mid-term price reviews. Providers capable of on-site renewables or demand-response programs mitigate exposure and bolster competitiveness inside the Romania facility management market.

Highly Fragmented Supplier Base Limits Scale Efficiencies

Thousands of small firms compete mostly on price, hampering investment in robotics, CAFM platforms and staff training. The dispute between Bucharest’s Sector 1 and Romprest over waste-collection fees underscores inconsistent service quality and legal risks in a fragmented setting. [3]Ziare.com, “Ilie Bolojan… pretul salubrizarii din Sectorul 1,” ziare.comClients seeking nationwide coverage must orchestrate multiple micro-contracts, incurring coordination overheads. Fragmentation also delays technology diffusion, as smaller outfits cannot amortise AI or IoT deployments across sizeable portfolios. Consolidation opportunities remain substantial, especially for international groups with capital to acquire regional players and extend uniform standards within the Romania facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Infrastructure Modernization

Hard services captured 57.08% of the Romania facility management market in 2025, mirroring modernization needs across aging industrial lines and commercial complexes. Asset-management, HVAC and electrical maintenance contribute most revenue as factories such as STIHL’s new plant and Petrofac’s USD 270 million upgrade of the Ticleni oilfield require continuous uptime monitoring. The Romania facility management market size attributed to hard services is projected to rise alongside stricter fire-safety codes that boost demand for alarm testing and sprinkler retrofits.

Soft services, though smaller today, post the fastest expansion at a 7.03% CAGR as hotels, offices and retail chains seek enhanced occupant experiences. Radisson’s new Bucharest and Brașov properties and Hyatt Regency Aro Palace require hospitality-grade cleaning, front-of-house and catering packages. Robotic scrubbers launched by Tennant via its Cluj center exemplify how automation lifts productivity and sanitisation consistency. This momentum lifts the Romania facility management market as employers prioritise wellness, ESG reporting and labour-efficient soft services.

By Offering Type: Outsourced Solutions Dominate Market Evolution

The outsourced model accounted for 62.85% of the Romania facility management market share in 2025, highlighting corporate preference for specialised expertise and scalable resources. International groups leverage global supply chains to introduce predictive analytics and CAFM dashboards that smaller in-house teams cannot match. The Romania facility management market size linked to outsourced contracts is set to climb at 6.74% CAGR as bundled agreements replace fragmented task orders.

In-house operations persist in sensitive sectors such as defence or data sovereignty, but rising complexity pushes many organisations toward external partners. Single-service contracts remain relevant for niche requirements like ISO-class cleanrooms, yet bundled FM commands premium demand due to one-stop accountability. Outcome-based models further tilt the scale, with providers staking remuneration on energy savings and asset availability-features most cost-effective under outsourced structures.

By End-user Industry: Commercial Sector Leads While Public Infrastructure Accelerates

Commercial facilities, including IT offices, retail hubs and logistics warehouses, held 38.10% of spending in 2025, driven by Romania’s role as a regional e-commerce and BPO hub. Major parks such as VGP Brașov lure brands that outsource security, cleaning and technical upkeep for 24/7 operations. This segment of the Romania facility management market benefits from tight delivery schedules and the prevalence of outcome-linked SLAs that reward throughput and inventory accuracy.

Institutional and public infrastructure grows fastest at 8.63% CAGR, fuelled by EU-backed modernisation of schools, hospitals and coastal defences. Regina Maria’s EUR 18 million storage overhaul confirms private healthcare’s push for lean operations and hygiene compliance. Government ministries adopt private FM expertise to meet digital-permit, energy-audit and ESG deadlines, unlocking sizeable multiyear contracts that expand the Romania facility management market.

Geography Analysis

Bucharest generates around 39.60% of national demand, reflecting its dense office skyline, government precincts and transport hubs. Developments such as One Cotroceni Park-900 apartments and 70,000 m² of offices-embed SMART lighting, access control and waste-recycling systems requiring continuous FM oversight. The new Henri Coandă Airport terminal likewise specifies AI-enabled building-management suites that lengthen scope for technical services.

Cluj-Napoca, Timișoara and Brașov anchor secondary growth, buoyed by nearshoring lines for automotive, electronics and aerospace. BEIA Consult deploys IoT platforms that let facility teams adjust ventilation and energy loads in real time, aligning with clients’ carbon targets. Brașov’s logistics parks need integrated FM that spans yard management, security and PV maintenance, while Timișoara’s assembly plants prioritise predictive maintenance to minimise downtimes.

Constanța and the Black Sea corridor emerge as energy and logistics gateways. Hydrogen pilot projects and wind-energy service bases demand niche FM skills, including hazardous-substance handling and turbine-blade storage. Rural districts, supported by EU cohesion funds, begin outsourcing maintenance for schools and clinics, giving providers with nationwide reach the chance to extend the Romania facility management market footprint beyond urban cores.

Competitive Landscape

The market remains highly fragmented; no single operator holds more than 10% revenue, and hundreds of regional firms compete on price for soft services. International players such as ISS, Sodexo and Dussmann differentiate via CAFM suites, global procurement and ESG reporting. ISS’s USD 937 million nuclear services contract showcases capability to manage mission-critical assets.

Domestic champions like Romprest sustain municipal waste deals but face scrutiny over tariff disparities, underscoring governance risks. Coral Companies leverage pest-control know-how to secure industrial and hospitality clients, while Facilitec focuses on technical maintenance packages for energy sites. Foreign entrants scout acquisitions to gain regional portfolios and skilled technicians quickly.

Technology investment is the prime battleground. Dussmann channels EUR 40 million annually into digitisation, rolling out sensor networks that feed central AI engines to predict HVAC faults and optimise staffing rosters. Smaller firms experiment with SaaS CAFM platforms to narrow the gap, though capital constraints slow adoption. Market consolidation is expected as integrated service demands grow and clients favour suppliers that can guarantee uniform standards across Romania’s dispersed geography.

Romania Facility Management Industry Leaders

Vinci Facilities

HGC Facility Management Services SRL

B+N Referencia ZRT.

P. Dussmann Serv Romania S.R.L.

Sodexo SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: OMV Petrom began building a EUR 750 million sustainable aviation-fuel unit at Petrobrazi refinery, broadening technical FM demand in renewable assets.

- March 2025: The Ro-HydroHub EUR 140 million hydrogen R&D cluster launched, creating specialised FM needs in green energy facilities.

- February 2025: Radisson Hotel Group unveiled Radisson RED Bucharest Old Town and Radisson Blu Grand Mountain Resort Brașov, opening new soft-service contracts.

- December 2024: Romania signed a USD 2 billion deal to extend Cernavodă’s nuclear reactor life; AtkinsRéalis secured USD 937 million for project management, signalling high-skill FM opportunities.

Romania Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology.

The Romania facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Romania facility management market?

The market is valued at USD 1.14 billion in 2026 and is expected to reach USD 1.59 billion by 2031.

Which segment dominates the Romania facility management market?

Hard services lead with 57.08% share in 2025, reflecting intensive demand for technical maintenance across industrial and commercial facilities.

How fast is the outsourced facility management segment growing?

Outsourced contracts are projected to expand at a 6.74% CAGR between 2026 and 2031 as organisations focus on core businesses.

Which end-user industry is growing quickest?

Institutional and public infrastructure shows the fastest rise, advancing at an 8.63% CAGR due to EU-funded modernisation projects.

Why are integrated facility management contracts gaining popularity?

They simplify vendor management, enable bundled service delivery and support data-driven performance optimisation through centralised platforms.

How do energy-efficiency mandates influence facility management?

EU-aligned green-building requirements drive adoption of IoT sensors, automation and predictive analytics to cut energy use and meet sustainability goals.

Page last updated on: