Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.34 Billion |

| Market Size (2026) | USD 3.46 Billion |

| Market Size (2031) | USD 4.11 Billion |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

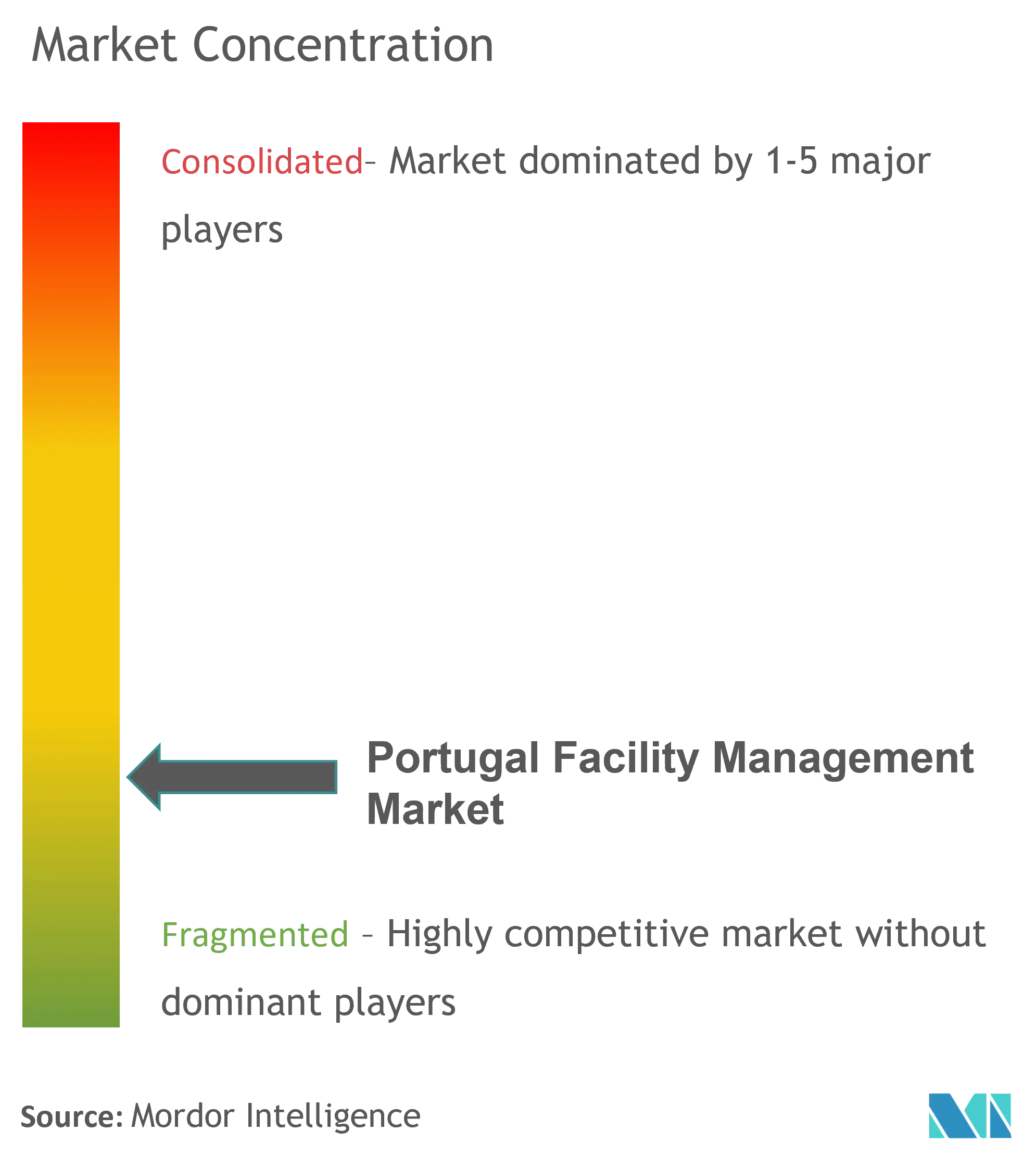

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Facility Management Market Analysis by Mordor Intelligence

The Portugal facility management market size was valued at USD 3.34 billion in 2025 and estimated to grow from USD 3.46 billion in 2026 to reach USD 4.11 billion by 2031, at a CAGR of 3.53% during the forecast period (2026-2031). Growth has moderated as facility management services moved from an emerging offering to a standardized operational outlay for most organizations. Stricter energy-efficiency rules, a national building-renovation program targeting 69% of the stock by 2030, and steady infrastructure investment pipelines such as the EUR 1 billion (USD 1.16 billion) Porto Metro 3.0 expansion have generated predictable contract flows. At the same time, chronic labour shortages and persistent wage inflation in technical trades are pushing service providers toward efficiency-oriented technologies rather than rapid territorial expansion. Consolidation remains the dominant competitive theme, with international majors defending share while local technology specialists leverage IoT-driven systems to offer incremental performance gains.

Key Report Takeaways

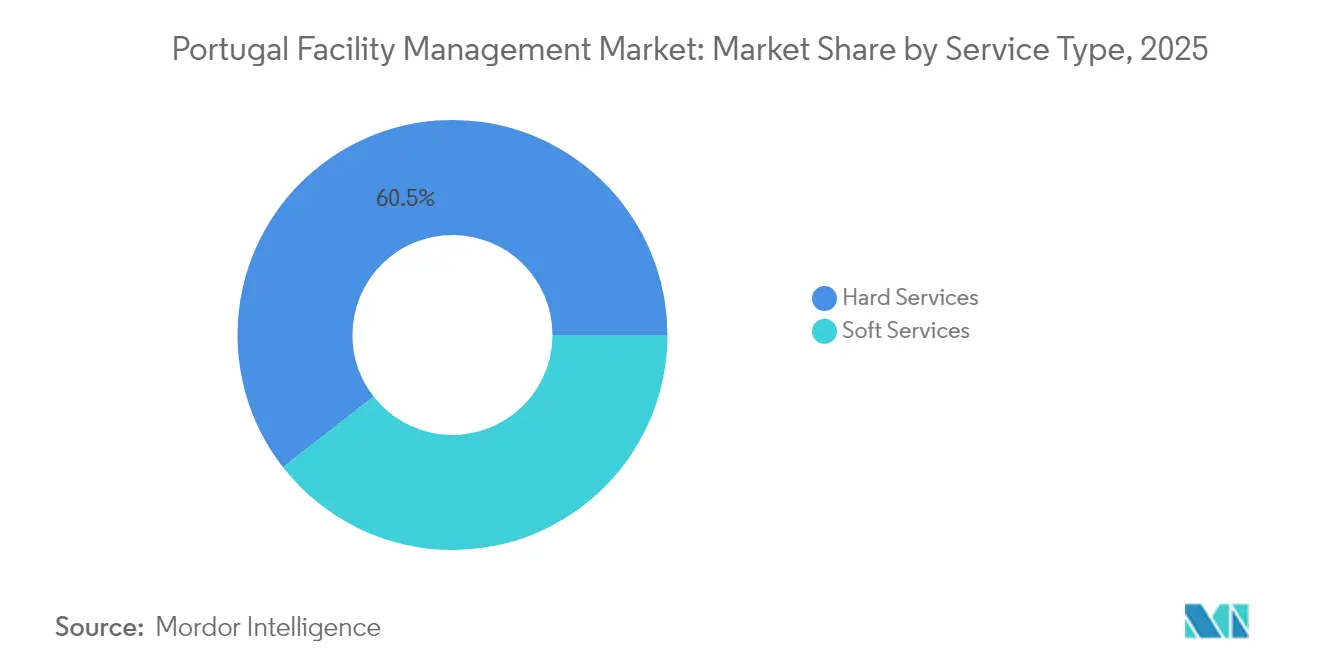

- By service type, Hard Services led with 60.55% of the Portugal facility management market share in 2025.

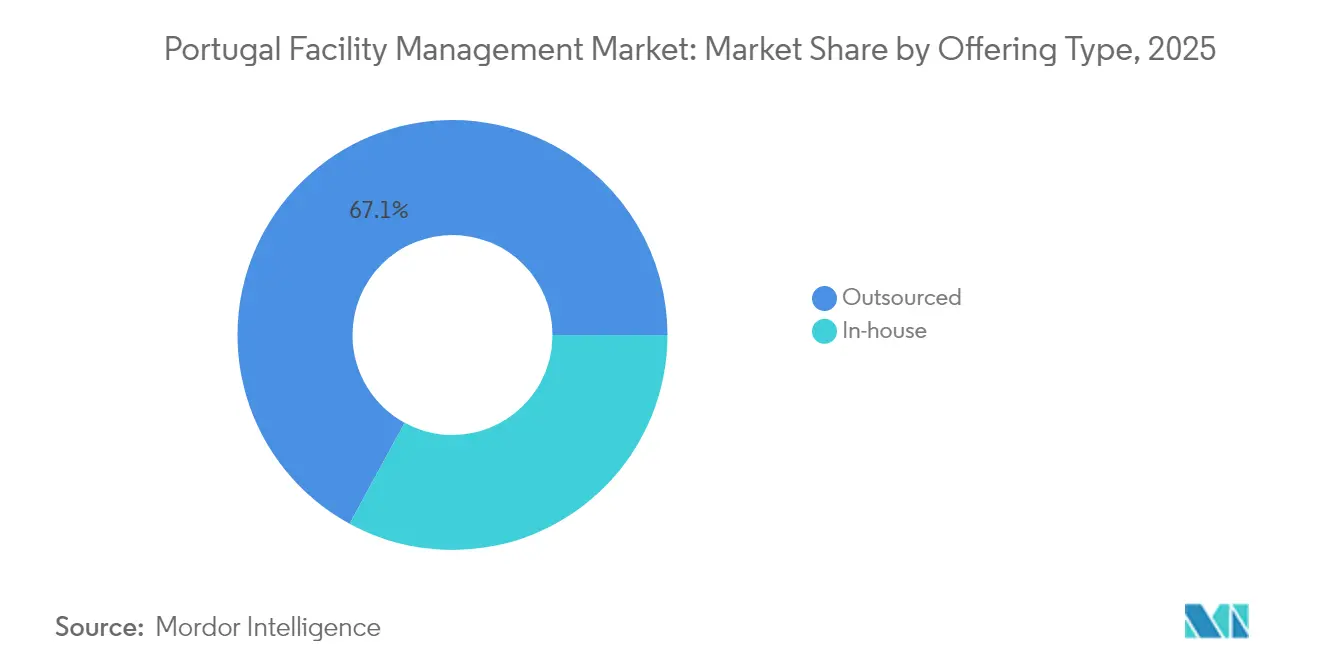

- By offering type, the Outsourced model accounted for 67.05% of the Portugal facility management market size in 2025 and is advancing at a 4.66% CAGR through 2031.

- By end-user, the Commercial segment generated 40.25% revenue share of the Portugal facility management market in 2025, while Institutional and Public Infrastructure is projected to expand at a 4.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Portugal Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and population growth in key Portuguese metros | +0.8% | Lisbon, Porto, Amadora, Braga, Coimbra | Medium term (2-4 years) |

| National infrastructure-pipeline investment across transport, energy, and social assets | +1.1% | National, with a concentration in the Lisbon-Porto corridor | Long term (≥ 4 years) |

| Stricter labour and occupational-safety regulations are raising compliance-driven FM demand | +0.7% | National | Short term (≤ 2 years) |

| Technology-led adoption of integrated FM (IoT, BMS, predictive analytics) | +0.9% | Urban centers, industrial zones | Medium term (2-4 years) |

| EU Green Deal energy-efficiency mandates accelerating retrofit FM services | +0.6% | National, EU-wide alignment | Long term (≥ 4 years) |

| Surging demand for ESG-compliant, data-driven FM to achieve green-building certifications | +0.5% | Commercial districts, corporate headquarters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urbanization and population growth in key Portuguese metros

Between 2025 and 2030, Lisbon and Porto continued to attract residents and corporate activity, together accounting for more than 40% of national GDP. New mixed-use projects clustered around transport corridors created a steady stream of mechanical, electrical, and plumbing (MEP) contracts rather than episodic spikes in demand. Occupiers increasingly favoured multi-year integrated agreements to maintain predictable cost structures, reinforcing the Portugal facility management market’s shift toward maturity. Dense metropolitan footprints also allowed providers to pool technicians and route service calls efficiently, partly offsetting skilled-labour scarcity. Service portfolios in these metros now standardize sustainability audits, reflecting tenant expectations for certified energy performance.

National infrastructure-pipeline investment across transport, energy, and social assets

Public-sector investment plans supplied the market’s longest visibility horizon. The Recovery and Resilience Plan earmarked EUR 143 million (USD 161 million) annually through 2050 for building upgrades, while flagship projects such as Porto Metro 3.0 and the Alcochete airport site embedded long-term facilities requirements into concession contracts.[1]Ayesa, “Ayesa wins new contracts for Porto Metro 3.0,” aysa.com High-speed rail electrification programs executed by Infraestruturas de Portugal further extended the pipeline of technical maintenance work. These undertakings strengthened the Portugal facility management market by locking in multi-year revenue rather than stimulating speculative supply.

Stricter labour and occupational-safety regulations raising compliance-driven FM demand

The Working Conditions Authority intensified inspections during 2024-2025, elevating non-compliance penalties for fire safety systems, indoor-air quality, and hazardous-material handling. The impending Construction Code, due in 2026, consolidated 100 separate statutes into a single framework that places clear accountability on facility owners for ongoing conformity. Clients, therefore, shifted from transactional fixes to preventative compliance programmes, favouring providers with integrated expertise across HVAC, fire systems, and workplace health. Consequently, contract renewal cycles lengthened, anchoring the Portugal facility management market around regulatory routine rather than discretionary spending.

Technology-led adoption of integrated FM (IoT, BMS, predictive analytics)

Measured digitization replaced the early-stage experimentation of the previous decade. IoT sensors embedded in building-management systems produced 20% energy savings in a Lisbon public-sector pilot, illustrating the incremental yet bankable returns that facility owners now expect. Predictive-maintenance trials at Renault Cacia’s plant trimmed maintenance costs by about 25%, encouraging industrial occupiers to negotiate outcome-based SLAs. Portuguese software vendors such as Infraspeak channelled their EUR 18 million (USD 20.88 million) Series B proceeds into collaboration features rather than expansionary marketing, underscoring the market’s operations-first mentality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic fluctuations and real estate market uncertainty | -0.6% | National, with higher impact in Lisbon and Porto | Short term (≤ 2 years) |

| Skilled labour shortages and wage inflation in technical trades | -0.9% | National, particularly acute in the construction and technical sectors | Medium term (2-4 years) |

| A highly fragmented vendor landscape is limiting standardisation and scale | -0.4% | National | Medium term (2-4 years) |

| Rising insurance and compliance costs for ageing building stock | -0.3% | Urban centers with older building stock | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled labour shortages and wage inflation in technical trades

Portugal reported an 80,000-person shortfall in construction and allied technical roles during 2024-2025, lifting average janitorial and handyman rates to EUR 8-15 (USD 9-17) per hour in major cities.[2]The Portugal News, “Portugal has a chronic lack of labour,” theportugalnews.com Service providers responded by upskilling existing staff and adopting remote-monitoring tools to reduce truck rolls, but elevated wage bases eroded margins on lower-complexity contracts. Market-entry barriers rose, cushioning incumbent shares yet capping the Portugal facility management market’s headline expansion until the vocational-training pipeline recovers.

Economic fluctuations and real-estate market uncertainty

After rent caps expired, housing rents climbed 6.94% in 2024, while construction costs added 4.3% by December of the same year. Developers slowed speculative builds, dampening near-term demand for fit-out services. Although GDP is expected to grow 2.1-2.3% in 2025, interest-rate volatility keeps corporate real-estate decision-making conservative. Contract renewals continue, but portfolio expansions are modest, tempering growth in Portugal facility management market revenues over the next two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering Type: Outsourced Model Embeds Majority Preference

Organizations outsourced 67.05% of facility-management spend in 2025, a share projected to edge up as labour tightness persists. Owners perceived integrated-service bundles as the most reliable hedge against compliance risk, catalysing a 4.66% CAGR for outsourced agreements within the Portugal facility management market size through 2031. Banks, telecom operators, and energy utilities renewed five-year frameworks that couple technical upkeep with space-management analytics, expecting contractors to deliver energy-intensity improvements aligned with EU taxonomy disclosures.

In-house teams retained strategic control over corporate real estate portfolios but shed non-core chores such as boiler servicing and waste segregation. Rising insurance premiums for ageing stock incentivised boardrooms to transfer liability to specialist vendors with robust process certifications. Nevertheless, certain public-sector agencies preserved mixed models to protect local employment; such arrangements contribute to the remaining 32.95% share but seldom reverse the broader outsourcing trajectory in the Portugal facility management market.

By End-user Industry: Commercial Core, Public Infrastructure Upside

The Commercial arena delivered 40.25% of Portugal's facility management market revenue in 2025, reflecting a service-economy structure centred on offices, data centres, and retail hubs. Data-sovereignty legislation spurred domestic hosting demand, keeping facilities such as the 1.2 GW SINES campus under intensive 24/7 technical-maintenance regimes. ESG screening by multinational tenants ensured that green-building audits now stand as a contractual baseline, converting specialist certifications from differentiators into prerequisites.

Institutional and Public Infrastructure, covering hospitals, universities, and rail assets, is forecast to be the fastest riser at a 4.74% CAGR to 2031. Hospital de Lisboa Oriental and multiple PPP healthcare renewals feed multi-disciplinary contracts blending MEP, sterile-environment cleaning, and fleet management. Education campuses, meanwhile, repurpose pandemic ventilation upgrades into permanent energy-efficiency projects. The steady pipeline of EU-funded projects makes the Portugal facility management market particularly resilient within this end-user slice.

By Service Type: Hard Services Sustain Structural Primacy

Hard Services held 60.55% of Portugal's facility management market share in 2025 and underpinned most mandatory compliance spending, while Soft Services advanced at a 4.92% CAGR to 2031 on hygiene and workspace-experience upgrades. The concentration of EU energy-efficiency mandates funnelled capital toward HVAC, MEP retrofits, and fire-system checks, embedding Hard-Service budgets into owner OPEX lines. Portugal's facility management market size associated with asset management surged alongside the EUR 1 billion (USD 1.16 billion) Porto Metro extension, which inserted multi-decade maintenance contracts into transit concessions.

Soft-Service providers leveraged regulatory requirements for formal employment contracts in cleaning and security to transition informal operators into professional networks. Technology infusion-such as robot scrubbers guided through Infraspeak’s maintenance platform-raised productivity per cleaner, partially offsetting higher wages. Hybrid working patterns sustained modest call-off demand for concierge and mailroom support, keeping segment revenues on a predictable ascent rather than the rapid spikes experienced in pandemic-era sanitization cycles.

Geography Analysis

Portugal's facility management market activity remained concentrated along the Lisbon-Porto axis, which absorbed roughly 59% of the national spend in 2025. Lisbon’s stock of government buildings, corporate HQs, and mixed-use developments cemented its lead; ESG compliance and ISO-41001 certification are now embedded in most renewal tenders, raising technical complexity and average contract values. Porto benefited from Metro 3.0 civil works and its software-startup ecosystem, which championed predictive-maintenance pilots to showcase exportable solutions.

Secondary urban clusters such as Braga, Coimbra, and Amadora drew university-linked R&D funding that flowed into smart-campus initiatives. Projects under the Aveiro Tech City Living Lab illustrated how mid-sized municipalities deployed AI for traffic-safety analytics and waste-collection routing, thereby opening niches for regional FM firms skilled in sensor integration. Along the Algarve coast, hospitality-driven seasonality sustained cyclical peaks for housekeeping and HVAC servicing. However, operators increasingly locked in 12-month retainers to guard against labour shortages during high season, smoothing revenue curves. Industrial zones such as Sines anchored specialized contracts on power-density management, water-treatment oversight, and substation maintenance. Rural regions, though fragmented, began to receive energy-retrofit grants that bundled FM clauses for long-term monitoring, broadening Portugal facility management market penetration outside metropolitan cores.

Competitive Landscape

Competitive dynamics reflected a mature, efficiency-oriented arena. ISS preserved its leading share through multi-country frameworks, including a 7-year, DKK 1.2 billion (USD 0.19 billion) annual deal with the UK Department for Work and Pensions, giving the group scale to leverage offshore procurement on Portuguese contracts.[4]ISS A/S, “ISS to mobilise landmark contract with DWP,” issworld.com Sodexo maintained a measured 2.1% organic growth in Europe, illustrating how incumbents prioritised contract optimization over aggressive rollout.

Local technology specialists intensified horizontal alliances rather than direct share grabs. Infraspeak channelled its EUR 18 million (USD 20.92 million) investment toward API integrations with BMS hardware, enabling incumbents to embed real-time telemetry into legacy work-order systems. NextBITT allocated EUR 5 million (USD 5.81 million) to carbon-footprint modules, positioning itself as a compliance engine amid growing CSRD reporting obligations.

M&A unfolded selectively: Samsic’s purchase of Pro Impec strengthened janitorial depth, while international energy-service conglomerates eyed data-centre cooling opportunities. Vendor selection criteria increasingly centred on ESG credentials—only 7% of Portuguese offices had third-party environmental labels in 2024, well below the 22% European norm, creating a value gap for certifications within the Portugal facility management market.

Portugal Facility Management Industry Leaders

Infraspeak

Apleona GmbH

TDGI SA

BMG-Services

NextBITT

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: EDP reached 15 GW of contracted PPA capacity worldwide, with over 20% earmarked for data-centre supply, intertwining energy and FM service scopes.

- February 2025: ISS announced a share-buyback programme capped at DKK 2.5 billion, signalling financial resilience that underpins Portuguese operations.

- January 2025: NextBITT invested EUR 5 million in energy-management modules to help firms meet EU environmental-reporting rules.

- November 2024: Sodexo agreed to acquire CRH Catering, reinforcing its North American convenience-food reach while confirming a focus on core services.

Portugal Facility Management Market Report Scope

Facility management (FM) incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology.

The Portugal facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehousing) |

| Hospitality (Hotels, Eateries and Restaurants) |

| Institutional and Public Infrastructure (Government, Education, Transport) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehousing) | |

| Hospitality (Hotels, Eateries and Restaurants) | ||

| Institutional and Public Infrastructure (Government, Education, Transport) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

Key Questions Answered in the Report

What is the current size of the Portugal facility management market?

The Portugal facility management market size reached USD 3.46 billion in 2026 and is projected to hit USD 4.11 billion by 2031.

Which service segment holds the largest share?

Hard Services dominated with 60.55% of Portugal facility management market share in 2025, thanks to mandatory MEP and fire-safety compliance.

Why is outsourcing preferred over in-house models?

A 67.05% share in 2025 reflected employers’ need for specialist skills amid labour shortages and rising regulatory complexity.

Which end-user sector will grow fastest by 2031?

Institutional and Public Infrastructure is expected to post a 4.74% CAGR as EU-funded modernization projects roll out.

How are technology trends shaping the market?

IoT-enabled BMS and predictive maintenance have delivered energy savings of around 20% in pilot sites, making data-driven FM a procurement staple.

What is the main barrier to faster market growth?

An 80,000-person deficit in technical trades is inflating wages and constraining capacity expansion across service providers.

Page last updated on: