Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

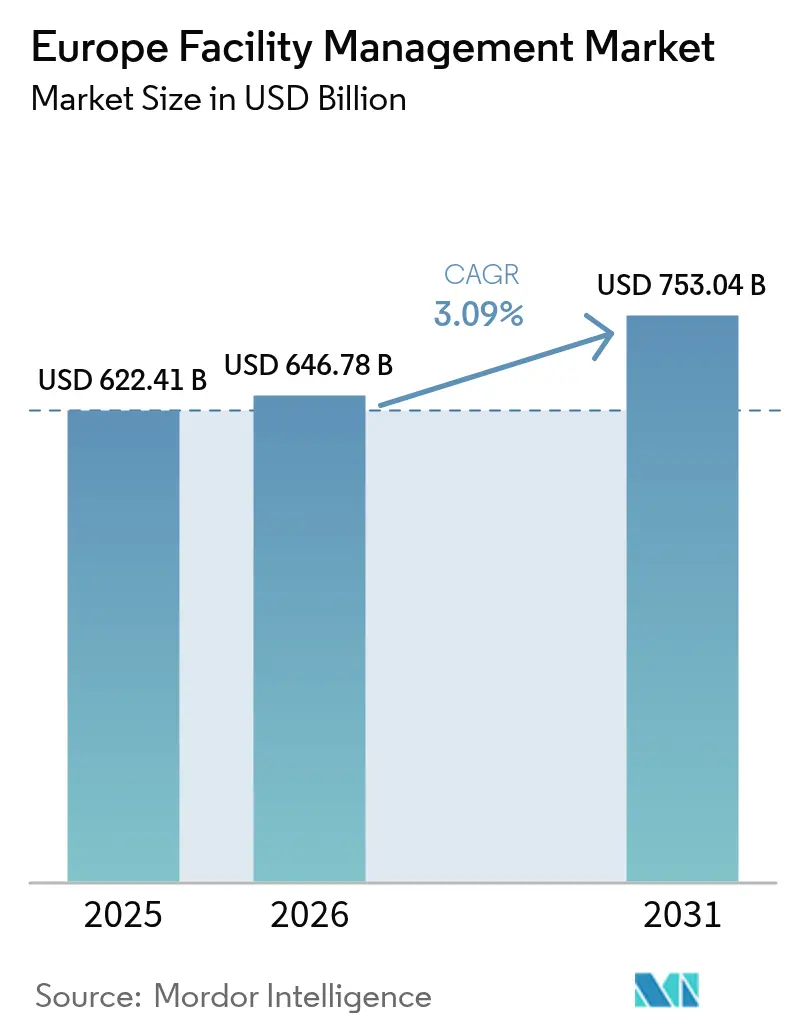

| Base Year Market Size (2025) | USD 622.41 Billion |

| Market Size (2026) | USD 646.78 Billion |

| Market Size (2031) | USD 753.04 Billion |

| Growth Rate (2026 - 2031) | 3.09% CAGR |

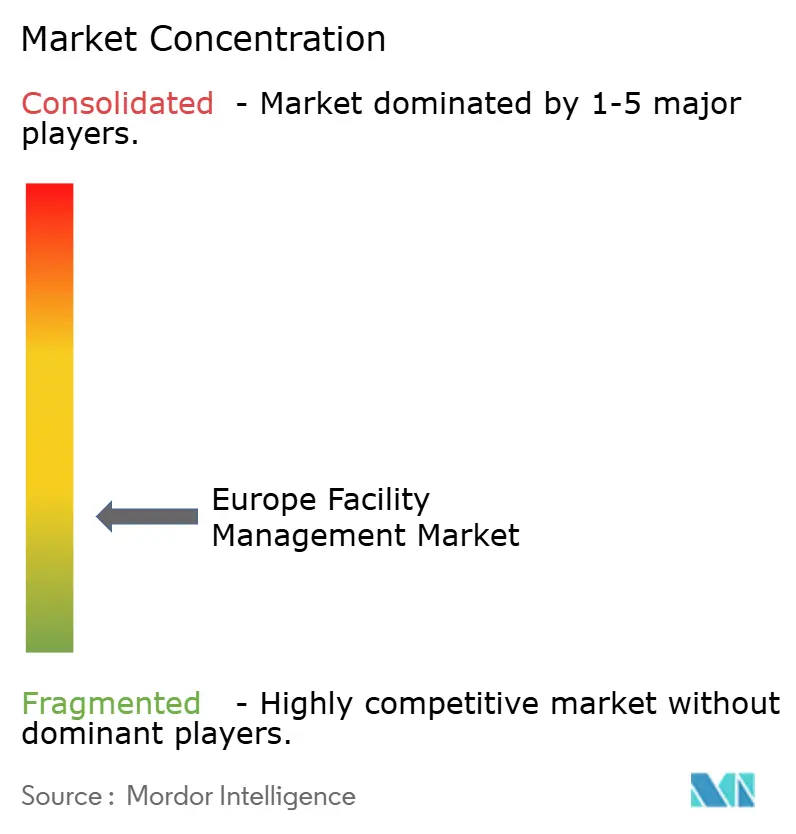

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Facility Management Market Analysis by Mordor Intelligence

The Europe Facility Management Market size is expected to increase from USD 622.41 billion in 2025 to USD 646.78 billion in 2026 and reach USD 753.04 billion by 2031, growing at a CAGR of 3.09% over 2026-2031. A steady expansion reflects the sector’s shift from cost-driven maintenance toward data-enabled performance services, tighter energy-efficiency mandates, and widening public-sector outsourcing. Hard services remain the industry’s anchor as ageing building systems require intensive mechanical, electrical, and plumbing care, while soft services accelerate on the back of health, wellness, and experience-oriented workplaces. Rising energy prices since the Russia-Ukraine conflict have pushed clients to favor optimization contracts over time-and-materials tasks.[1]European Central Bank, “Energy Price Developments in and out of the COVID-19 Pandemic,” ecb.europa.eu Outsourcing gains scale as ESG reporting rules and the complexity of digital technology demand specialized know-how. Private-equity interest, typified by Techem’s USD 7.2 billion transaction, underlines confidence in the segment’s recurring-revenue profile.

Key Report Takeaways

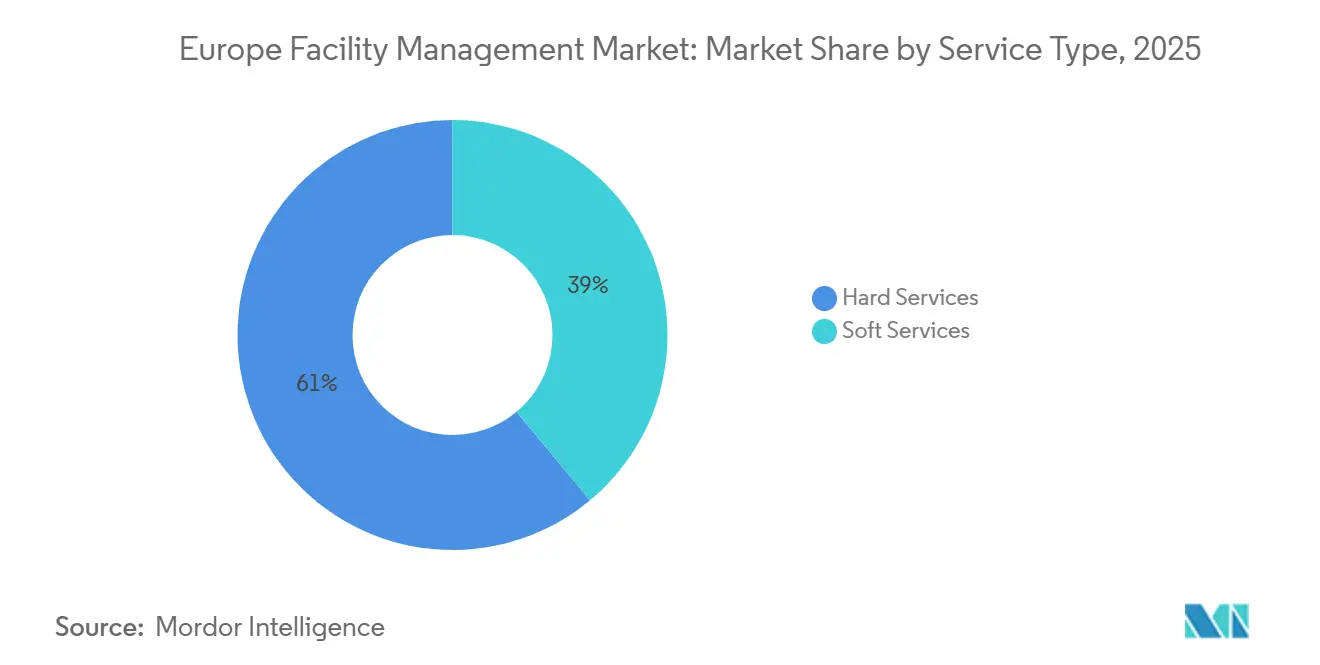

- By service type, hard services led with 61.05% revenue share in 2025; soft services are projected to expand at a 4.61% CAGR through 2031.

- By offering type, the in-house model retained a 56.80% share in 2025, while outsourced services are set to grow at a 4.86% CAGR during 2026-2031.

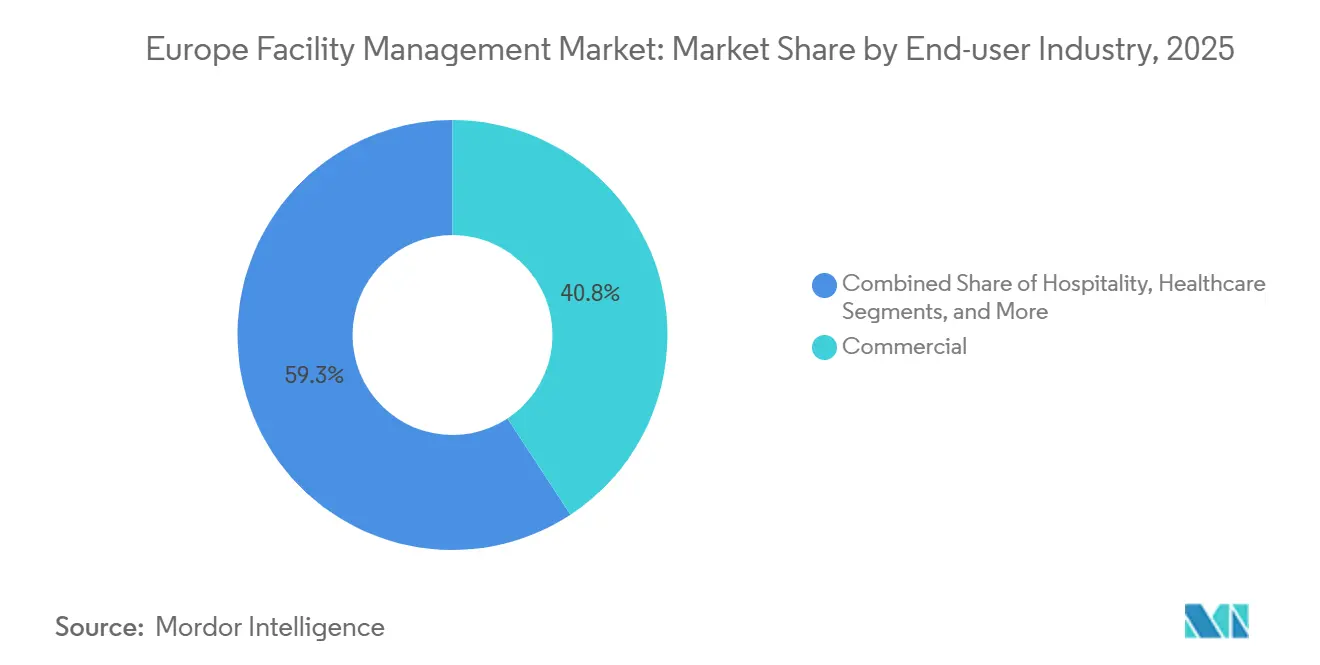

- By end-user industry, the commercial sector accounted for 40.75% of revenue in 2025; institutional and public infrastructure is forecast to advance at a 4.45% CAGR to 2031.

- By country, Germany commanded a 31.65% share in 2025, whereas Slovenia is expected to post the fastest 4.95% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging building stock driving retrofit spending | +0.8% | Germany, France, UK; spillover Eastern Europe | Long term (≥ 4 years) |

| Public-sector outsourcing after fiscal austerity | +0.6% | UK, Nordics, Southern Europe | Medium term (2-4 years) |

| Energy-price volatility steering energy-optimization FM | +0.4% | Highest in Germany, industrial belts | Short term (≤ 2 years) |

| ESG reporting mandates requiring data-driven FM | +0.3% | EU-wide; early in Netherlands, Germany, France | Medium term (2-4 years) |

| Health and safety certification demand | +0.2% | Global; strong in healthcare, hospitality | Short term (≤ 2 years) |

| Private-equity consolidation fueling integrated FM | +0.1% | Western Europe core; CEE expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Building Stock: Retrofit-Driven FM Spending

Three-quarters of the European building stock is more than 50 years old, creating sustained demand for comprehensive retrofit programmes that bundle technical maintenance with energy upgrades.[2]European Environment Agency, “Addressing the Environmental and Climate Footprint of Buildings,” eea.europa.eu Performance-contract models such as Centrica’s 15-year deal at St George’s University Hospitals, which cuts 6,000 tonnes of carbon and saves USD 1.1 million annually, illustrate the financial viability of retrofit-oriented facility services. German and French portfolios face the greatest urgency as Nearly-Zero-Energy Building standards tighten, pushing facility managers to integrate IoT sensors, predictive maintenance, and energy-performance analytics during refurbishments. The European Investment Bank estimates a EUR 185 billion yearly funding gap for energy efficiency, positioning facility service providers as key intermediaries for capital access.

Public-Sector Outsourcing Momentum Post-Fiscal Austerity

Government departments are transferring multi-service bundles to external providers to meet efficiency targets and ESG disclosure obligations. The UK Department for Work and Pensions awarded ISS a seven-year contract worth USD 175 million per year, consolidating cleaning, catering, and technical maintenance under one roof. Nordic and German municipalities follow suit, evidenced by VINCI Facilities’ decade-long framework with Lincolnshire County Council that prioritises collaborative energy management. Health-care estates are prominent adopters as 24/7 operations, infection control, and high-energy HVAC loads demand specialist support.

Energy Price Volatility Accelerating Energy-Optimisation Services

Wholesale electricity and gas peaks during 2024 opened a path for AI-enabled optimisation contracts that guarantee consumption cuts. Vodafone’s Düsseldorf campus achieved a 23% HVAC energy drop by deploying Recogizer’s self-learning controls, saving 5.5 GWh annually. Facility managers now bundle energy analytics, procurement advisory, and demand-response alignment into service scopes. Industrial clients replicate the approach; ABB reports 20% energy savings at its Stonehouse site via integrated resource monitoring.

ESG Reporting Mandates Requiring Data-Driven Solutions

The Corporate Sustainability Reporting Directive expands mandatory sustainability disclosures to tens of thousands of firms, driving uptake of platforms that capture utility, waste, and emissions data in real time. Providers such as BuildingMinds integrate GRESB, SFDR, and EU-Taxonomy rules into single dashboards. Hotel operators like Leonardo target net-zero 2040 pathways that hinge on granular facility metrics supplied by FM partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic pressures (inflation, cost optimisation) | -0.3% | Highest in Southern and Eastern Europe | Short term (≤ 2 years) |

| Fragmented EU regulatory regimes | -0.2% | EU-wide; cross-border issues | Long term (≥ 4 years) |

| Limited PropTech interoperability | -0.1% | Western Europe core | Medium term (2-4 years) |

| Cybersecurity risks to connected buildings | -0.1% | Digitally advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Pressures (Inflation, Cost Optimisation)

Rising labour, material, and energy inputs prompt clients to renegotiate contracts, curbing discretionary FM spend. CBRE notes that while 35% of organisations raised FM budgets in 2023, 29% still listed supply-chain disruption as the top threat. Sodexo’s European business recorded only 2.1% organic growth for the first half of fiscal 2025 as healthcare clients delayed tenders. Margin pressure is acute in Southern and Eastern Europe, where price sensitivity drives commoditisation.

Fragmented EU Regulatory Regimes Hindering Standardised Delivery

Divergent health-and-safety, labour, and energy codes oblige providers to maintain multiple compliance frameworks, raising costs and limiting cross-border scale economies. Cleanroom specifications, for example, vary between GMP Annex 1 and national rules, complicating pharmaceutical-site servicing. Customisation also slows digital platform roll-outs because software must align with country-specific regulations rather than standard EU templates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technical Upkeep Anchors Growth

Hard services hold 61.05% of the European facility management market in 2025, underlining the necessity of MEP, HVAC, and fire-safety upkeep across an ageing building base. Persistent retrofit activity keeps the European facility management market size for hard services expanding despite moderate industry growth. Predictive asset management gains traction as clients look to extend equipment life cycles and comply with energy-use regulations.

Soft services, though smaller, deliver a 4.61% forecast CAGR as employee-experience strategies prioritise advanced cleaning, concierge, and security packages. Hybrid work drives demand for space booking, flexible catering, and touchless access control, threading technology through traditional frontline functions. Integration opportunities arise where soft-service data, such as footfall analytics, feed back into energy algorithms, further embedding providers in client operational planning.

By Offering Type: Outsourcing Outpaces In-House Control

While in-house teams still oversee 56.80% of facilities' spend in 2025, the outsourced slice of the European facility management market expands at a 4.86% CAGR to 2031 as corporations pursue specialised compliance and digital capabilities. Integrated FM packages are gaining favour because they consolidate vendor oversight and better align with ESG reporting workflows.

Single-service outsourcing endures in settings that require niche technical expertise, fire-system testing, or cleanroom validation, whereas bundled contracts suit multi-site portfolios seeking cost coordination without full integration. The European facility management market share for outsourcing lifts further when providers demonstrate AI-enabled energy dashboards, compliance indices, and robotics solutions, as shown in Sodexo’s five-year HMRC award covering 24 UK sites.

By End-user Industry: Commercial Holds Lead, Public Infrastructure Rises

Commercial buildings contribute 40.75% of 2025 revenue, yet their service mix changes as office footprints shrink and logistics hubs proliferate. Facility managers deploy occupancy sensors, automated lighting, and cloud-based BMS to boost utilisation and cut energy in mixed-use portfolios. Retail and warehouse operators adopt similar toolkits as e-commerce reshapes delivery timelines and temperature-controlled storage.

Institutional and public-infrastructure estates grow at a 4.45% CAGR through 2031, reflecting a shift toward outsourced models that capture efficiency gains for budget-constrained authorities. Schools and hospitals now require granular energy and waste data to meet decarbonisation targets; transportation hubs need resilient maintenance schedules to handle fluctuating passenger volumes. Providers with proven health-care protocols and energy-performance contracts hold an edge.

Geography Analysis

Germany accounts for 31.65% of the European facility management market in 2025, supported by a vast industrial base, rigorous building regulations, and advanced digital adoption. Technical building management is projected to add 8.6% revenue in 2026 as manufacturers invest in energy monitoring and predictive maintenance. Leading firms such as Dussmann and Apleona report record integrated-service sales, underlining continued market professionalization.

Slovenia, with a 4.95% forecast CAGR, benefits from EU accession-driven infrastructure upgrades and harmonised regulation that raise outsourcing demand. France leverages strong IoT penetration to embed smart-building platforms in corporate estates, while Italy’s healthcare modernisation fuels specialised FM uptake. The UK retains a sizeable share due to mega public-sector contracts despite regulatory divergence. Nordic providers, exemplified by Coor’s extension with PostNord, show high service sophistication and ESG alignment. Emerging Eastern and Southern European economies close the gap through EU funding windows and foreign direct investment, expanding the European facility management market footprint.

Competitive Landscape

The European facility management market is moderately fragmented: global integrators ISS, Sodexo, and Dussmann compete with regional champions and niche technical specialists. Private-equity consolidation raises competitive stakes; TPG and GIC’s USD 7.2 billion Techem buyout adds a digitally focused heavyweight in sub-metering and energy services. Strategic alliances between technology vendors and FM firms accelerate. Schneider Electric’s stake in Planon broadens smart-building software reach for both partners.

Scale provides pricing leverage, yet regulatory complexity preserves space for local experts with deep code knowledge. ESG data provision emerges as a premium differentiator, encouraging integrators to embed analytics platforms and hire sustainability professionals. Robotics for cleaning and inspection slowly shifts labour profiles, amplifying capital-investment needs and widening capability gaps between leaders and smaller players.

Europe Facility Management Industry Leaders

Mitie Group PLC

Emcor Facilities Services WLL

Atlas FM Ltd.

G4S Facilities Management UK Ltd.

ISS Global

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sodexo posted EUR 12.5 billion (USD 14.3 billion) revenue for H1 FY 2025; European FM rose 2.1%, prompting efficiency measures.

- February 2025: Gecina earmarked EUR 500 million (USD 573.38 million) capex for three flagship retrofit projects and reported a 4.2% energy-consumption cut versus 2019.

- January 2025: Coor renewed its Nordic integrated-FM contract with PostNord, reinforcing its regional leadership.

- January 2025: KONE recorded 1.3% sales growth to EUR 11.1 billion (USD 12.73 billion), driven by service and modernisation demand in ageing European lifts.

Europe Facility Management Market Report Scope

Facility management (FM) incorporates many disciplines to ensure the built environment's functionality, safety, comfort, and efficiency by integrating people, processes, places, and technology. FM service providers contribute to the business's bottom line by maintaining an organization's most significant and valuable assets, such as property, equipment, and buildings.

The facility management market in Europe is segmented by type of facility management (in-house facility management, outsourced facility management [single FM, bundled FM, and integrated FM]), end user (commercial buildings, retail, government and public entities, and manufacturing and industrial), and country. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Slovenia |

| Rest of Europe |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Slovenia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe facility management market?

The market is valued at USD 646.78 billion in 2026.

How fast is the Europe facility management market expected to grow?

It is projected to register a 3.09% CAGR, reaching USD 753.04 billion by 2031.

Which service segment holds the largest share?

Hard services account for 61.05% of revenue, reflecting the priority on technical infrastructure upkeep.

Which geography is expanding the fastest?

Slovenia leads regional growth with a forecast 4.95% CAGR over 2026-2031.

Why is outsourcing gaining popularity in European facility management?

Complex ESG rules and advanced digital-technology requirements push organisations to seek specialised providers, driving outsourced services at a 4.86% CAGR.

How are energy-price fluctuations affecting facility services?

Volatile gas and electricity costs increase demand for energy-optimisation contracts that deliver measurable consumption reductions.

Page last updated on: