Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

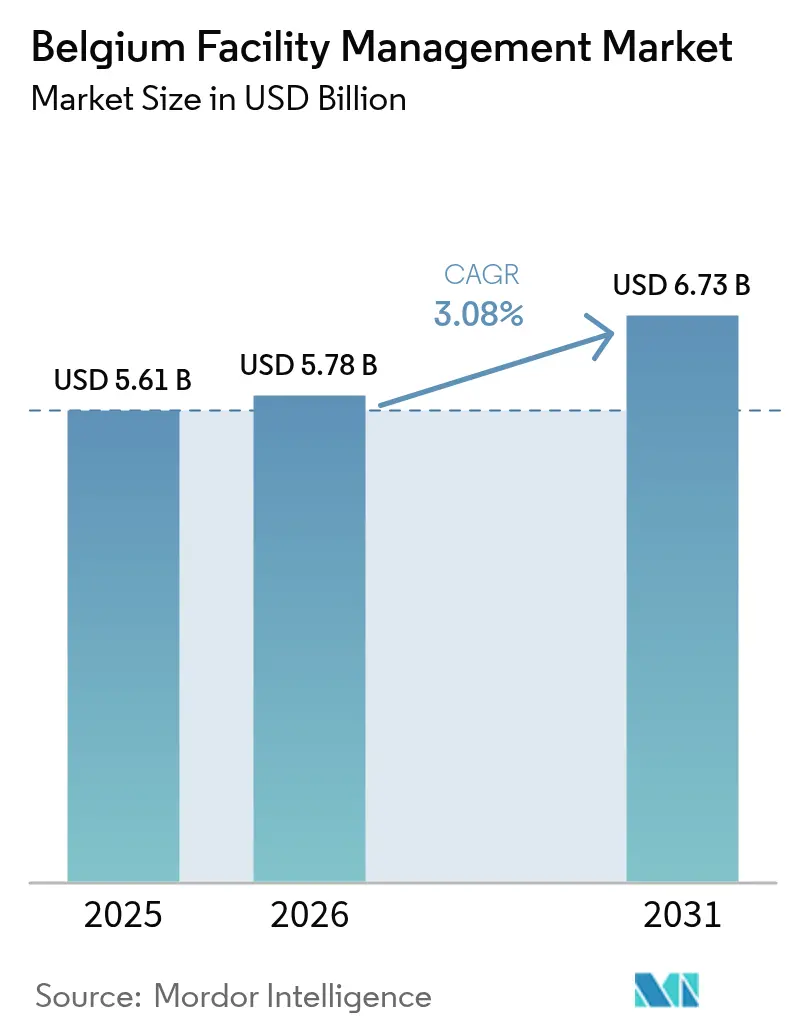

| Base Year Market Size (2025) | USD 5.61 Billion |

| Market Size (2026) | USD 5.78 Billion |

| Market Size (2031) | USD 6.73 Billion |

| Growth Rate (2026 - 2031) | 3.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Facility Management Market Analysis by Mordor Intelligence

Belgium facility management market size in 2026 is estimated at USD 5.78 billion, growing from 2025 value of USD 5.61 billion with 2031 projections showing USD 6.73 billion, growing at 3.08% CAGR over 2026-2031. Demand growth is fuelled by mandatory efficiency upgrades under the EU Energy Performance of Buildings Directive, steady retro-commissioning of an ageing commercial estate, and the migration from single-service contracts to bundled and integrated models that promise auditable sustainability outcomes. Outsourcing dominates service delivery as large occupiers in Brussels and Antwerp prioritise core-business focus, while technology adoption-IoT sensors, AI analytics and smart-building platforms-improves uptime and lowers energy baselines amid construction-price inflation that climbed 3.5% in 2023. Competitive intensity is moderate: a mix of multinationals and regional specialists compete on multilingual compliance, carbon reporting credentials and workforce depth.

Key Report Takeaways

- By offering type, outsourced services captured 61.85% of the Belgium facility management market share in 2025 and are expanding at a 3.26% CAGR through 2031.

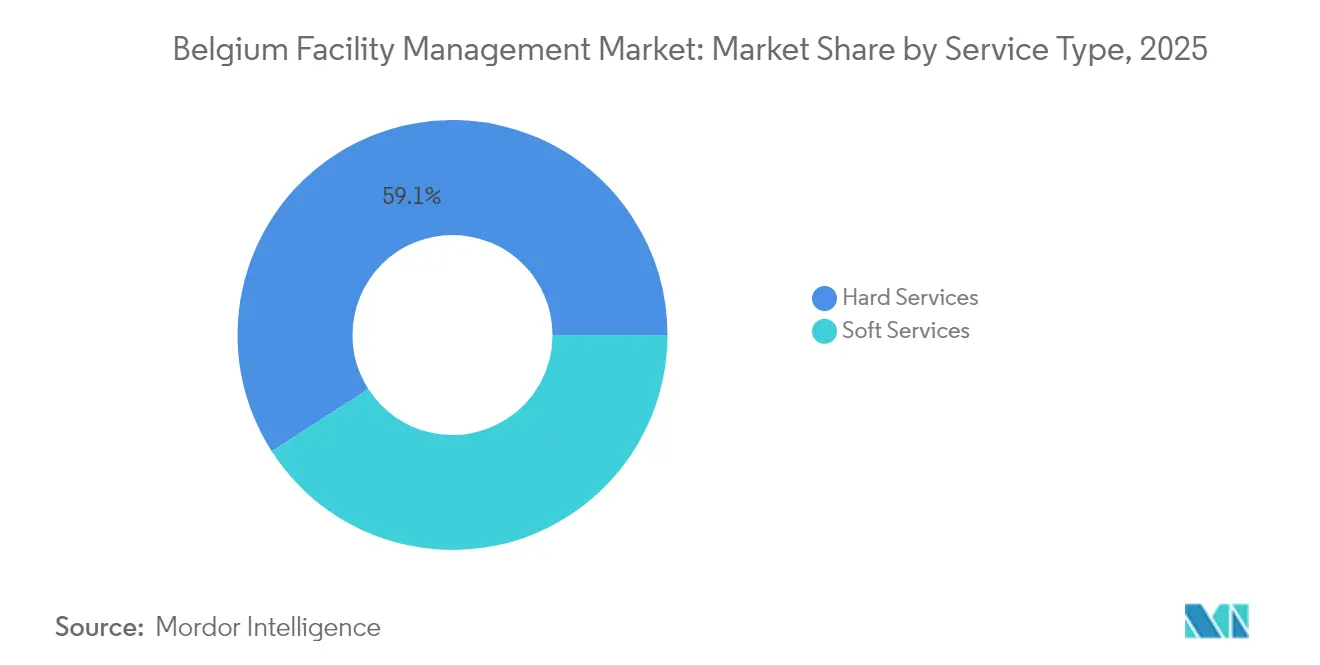

- By service type, hard services accounted for 59.10% of the Belgium facility management market size in 2025, while soft services are forecast to post the fastest 3.39% CAGR to 2031.

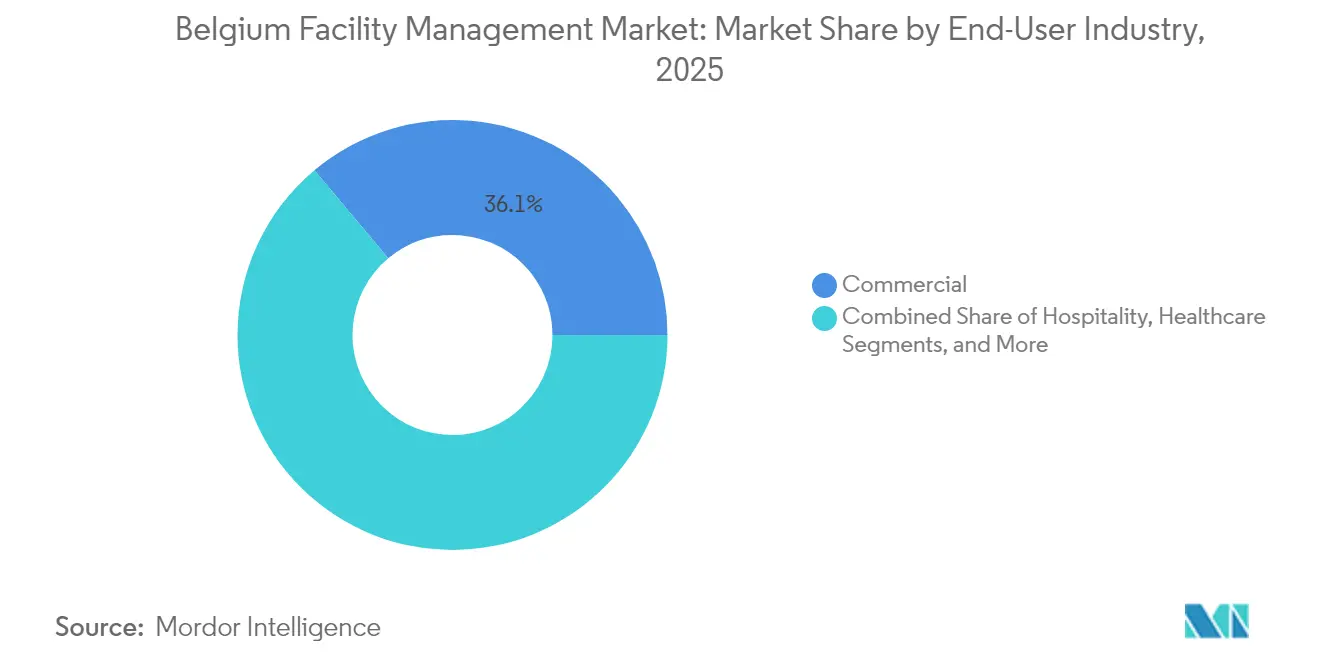

- By end-user industry, the commercial segment led with 36.10% revenue in 2025; institutional and public infrastructure is projected to expand at a 3.33% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Belgium Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing of non-core business functions | +0.8% | Brussels and Antwerp corridors | Medium term (2-4 years) |

| Demand for integrated FM services | +0.6% | Nationwide; early uptake in commercial and healthcare | Medium term (2-4 years) |

| Workplace-experience and employee wellbeing focus | +0.4% | Urban centres | Short term (≤ 2 years) |

| IoT, AI and smart-BMS penetration | +0.5% | Brussels and Flemish tech clusters | Long term (≥ 4 years) |

| EU EPBD-driven energy retrofits | +0.7% | Brussels Capital and Wallonia | Medium term (2-4 years) |

| Outcome-based contracts under EU CSRD | +0.3% | Large enterprise campuses | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing outsourcing of non-core business functions

Belgian corporates are accelerating the transfer of soft and technical services to strategic suppliers to unlock management bandwidth and hedge regulatory risk. Sodexo’s local arm recorded EUR 6.4 billion sales in Q1 2025, with outsourcing demand across food and facilities lifting organic growth to 4.6%. [1]Sodexo, “Q1 Fiscal 2025 Revenues,” sodexo.com Multilingual compliance burdens, intensified by workplace-health protocols and carbon-reporting audits, make specialised partners more cost-effective than in-house teams. Financial-services and tech tenants, weighed down by CSRD disclosure rules, are leading the flight to contract models that guarantee data-ready energy dashboards. As a result, the Belgium facility management market registers rising contract durations and higher bundled-service densities, which underpin predictable fee streams for providers. This structural pivot cements outsourcing as a principal expansion lever for the Belgium facility management market over the medium term.

Rising demand for integrated facility management services

Clients are consolidating cleaning, maintenance, catering and energy oversight under single-provider governance to cut transaction costs and secure unified KPIs. SPIE Belgium’s ten-year multi-site deal with Befimmo spans preventive maintenance, modernisation and performance analytics across three office parks. [2]SPIE, “Befimmo Office Complexes Maintenance,” spie.comSuch contracts allow real-time re-allocation of field staff and enable synergies in consumables procurement. Integrated delivery is especially prized in the healthcare and high-tech manufacturing estates where downtime penalties are steep. For suppliers, deeper wallet share raises switching barriers and stabilises margins despite wage inflation. Consequently, integrated models are set to elevate average revenue per contract and support steady CAGR momentum for the Belgium facility management market.

EU EPBD-mandated energy retrofits

The directive obliges non-residential buildings to meet 100 kWh/m²/year by 2050, prompting staged renovation waves every five years. [3] Flanders alone targets 95,000 deep-dwellings annually, translating into a EUR 200 billion outlay through 2050. Facility management providers secure retrofit programme management, post-occupancy measurement and verification, and long-term asset-performance monitoring. Although inflation lifted construction-input prices to an index of 140.59 in April 2024, [3]Belgium Federal Public Service Economy, “Mercuriale – Index I 2021,” economie.fgov.be IoT-enabled energy dashboards offset cost pressures by evidencing savings. The Belgium facility management market benefits from these legally driven projects, creating resilient demand across the value chain.

Technological advancements in IoT, AI and BMS

Sensor networks and AI diagnostics are cutting unplanned downtime and lowering HVAC electricity use in smart buildings by an average 36.8 kW. In Brussels, a Bluetooth-mesh lighting retrofit spanning 2,000 m² and 50 zones automated occupancy-based dimming and daylight harvesting. BESIX and Proximus’ “living lab” headquarters run AI algorithms that tune chillers and integrate photovoltaic inputs. These cases prove the ROI of predictive maintenance and energy orchestration, encouraging FM providers to bundle digital twins and analytics subscriptions into long-term contracts. Digital capability therefore constitutes a pivotal driver that will reinforce the growth trajectory of the Belgium facility management market well beyond 2029.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour shortages and skill gaps | –0.5% | Nationwide; acute in Flanders | Short term (≤ 2 years) |

| High upfront cost of tech integration | –0.3% | SME providers countrywide | Medium term (2-4 years) |

| Fragmented public procurement and price compression | –0.2% | Regional authorities | Medium term (2-4 years) |

| Multilingual compliance and union complexity | –0.4% | Brussels bilingual zone | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labour shortages and skill gaps

Belgium posted 54,852 cross-border worker declarations in construction during 2021, equalling 17% of sectoral employment. Yet only one-third of the 19,000 labour migrants who arrived in 2023 remain after five years, worsening attrition in cleaning and technical trades. The statutory minimum wage of EUR 1,879.13 (USD 2,013) and sector-specific collective agreements are driving payroll costs higher. Providers shoulder overtime premiums to meet SLAs, while automation roll-outs stall because frontline technicians lack digital-maintenance skills. Labour scarcity therefore drags on service-quality scalability and restrains short-term growth in the Belgium facility management market.

Multilingual compliance and union regulations

Companies must produce employment, safety and wage records in Dutch, French and German, while Brussels imposes bilingual service obligations for every public-facing function. The tri-layer governance model forces FM suppliers to juggle federal, regional and municipal rules, each policed by active sector unions. Administrative overhead and penalty risk deter small providers from bidding on public tenders, consolidating volume in larger incumbents but narrowing overall supplier diversity. This compliance drag subtracts momentum from the Belgium facility management market, particularly in long-term public-sector frameworks where price is fixed yet documentation costs rise annually.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Asset-intensive demand sustains hard-service dominance

Hard services retained 59.10% of the Belgium facility management market share in 2025 as ageing HVAC, fire-safety and electrical assets across office towers and transport hubs required lifecycle upgrades. Belgium’s renovation roadmap sets interim milestones every five years, ensuring recurring demand for condition-based maintenance, retrofit design and commissioning audits. Providers with deep MEP and energy-performance credentials secure multi-year frameworks that bundle statutory inspections with sensor-enabled predictive maintenance, insulating revenues from cyclical vacancy swings. Nevertheless, the soft-service segment is forecast to outpace at a 3.39% CAGR as occupiers elevate workplace experience scores to strengthen talent retention in a tight labour market. High-frequency cleaning, front-of-house reception and hybrid-office support comprise the fastest-growing sub-clusters, amplified by infection-control protocols in corporate campuses. Facilicom’s deployment of cobotic cleaning units and bio-based detergents illustrates how automation offsets wage pressure while improving ESG ratings.

Rapid adoption of smart-restroom sensors, digital wayfinding and AI-driven security analytics further blurs the boundary between hard and soft lines, prompting integrated service playbooks. Soft-service growth also benefits from the rebound in conference and hospitality events that lift catering and concierge hours. Consequently, service portfolios are converging: vendors couple asset stewardship with employee-experience platforms and deliver both through a single help-desk interface. That convergence aligns with tenant pressure for transparent carbon footprints, pushing providers to evidence cleaning-chemical toxicity, fleet emissions and HVAC kWh in one dashboard. The interplay of regulatory compliance, digitalisation and wellbeing priorities therefore keeps both service classes essential to the Belgium facility management market.

By Offering Type: Outsourcing cements structural lead

Outsourced contracts represented 61.85% of the Belgium facility management market size in 2025, and the segment is charted to expand at 3.26% CAGR to 2031 as corporates rationalise supplier rosters and pivot to operating-expense models. Bundled and integrated offerings lead new wins because they aggregate disparate SLAs into single key-performance indicators, easing CSRD audit preparation. Global majors leverage supply-chain scale to hedge material inflation and satisfy trade-union wage escalators without eroding margins. Concurrently, hybrid models emerge in healthcare and sensitive-infrastructure sites where clients retain strategic control of security or clinical engineering but offload cleaning, catering and energy-monitoring to specialist subcontractors. These hybrids still feed the outsourcing ledger because external providers capture the bulk of spend on technical expertise and compliance tooling.

In-house management remains viable among small public-sector bodies and niche industrial plants that prefer direct labour contracts for cultural or security reasons. However, rising digital-skill requirements, multilingual recordkeeping and asset-monitoring technologies inflate fixed staff budgets, nudging late adopters toward managed-service pilots. Technology giants in Flanders, for example, have shifted cafeteria and building-automation oversight to ISS under outcome-based metrics, freeing technicians to focus on core R&D. As embedded suppliers deepen strategic ties, exit barriers expand, reinforcing the long-term ascendancy of outsourced delivery within the Belgium facility management market.

By End-User Industry: Commercial real estate still leads but institutional demand escalates

The commercial office domain generated 36.10% of 2025 revenue, anchored by EU institutions and multinational headquarters clustered in Brussels’ European Quarter. Corporate landlords seek green-lease alignment and WELL-certification, channelling investment toward air-quality sensors, circadian lighting and waste-segregation regimes. This appetite supports premium-priced integrated contracts that couple asset uptime with occupant-satisfaction analytics. Conversely, the institutional and public-infrastructure segment is on track to deliver the fastest 3.33% CAGR thanks to a EUR 30 billion national renovation programme earmarked for schools, hospitals and municipal facilities. Energy-performance contracting, backed by performance-guarantee insurance, opens multi-decade cashflows for FM firms skilled in metering and lifecycle-cost modelling.

Healthcare presents stringent infection-control demands: ATP swab studies across nine cross-border hospitals found 37.7% of tested surfaces fell outside “clean” thresholds, elevating the role of science-based cleaning protocols. Industrial and process facilities, concentrated in Antwerp’s petrochemical belt and Wallonia’s manufacturing clusters, require predictive maintenance and statutory pressure-vessel inspections. Hotel and large-format dining outlets, boosted by international conferences, favour guest-centric soft-service menus including pop-up catering and smart-locker logistics. Sports arenas and mixed-use entertainment precincts round out the opportunity pipeline as Belgium bids for pan-European events. Together, these diverse demand nodes ensure balanced revenue exposure for the Belgium facility management market across cyclical sectors.

Geography Analysis

Brussels Capital Region anchors the Belgium facility management market with the densest inventory of premium offices, EU agencies and transport interchanges. Bilingual statutory requirements add procedural complexity, incentivising occupiers to outsource to multilingual providers that maintain dual-language documentation. Ongoing EUR 30 billion retrofit mandates covering insulation, HVAC upgrading and façade optimisation guarantee a steady retrofit workstream into the next decade. Flanders is the fastest-growing territorial market; its tech corridors stretching from Ghent to Leuven host biotech incubators and semiconductor fabs that require ISO-class cleanrooms and high-availability utilities. Labour mobility programmes attracted 19,000 migrants in 2023, heightening multilingual workforce services and raising demand for employee-wellbeing amenities.

Wallonia’s market, while smaller, is diversified across logistics parks, healthcare campuses and legacy heavy-industry conversions seeking carbon-neutral refurbishment. Public-sector procurement there favours local SMEs but often splits contracts, leading to price compression and opportunities for integrators to aggregate scopes. Across all three regions, facility managers must incorporate CSRD-compliant carbon accounting, driving a uniform shift to sensor-based monitoring platforms. Belgium’s A2 sovereign-risk and A1 business-climate ratings underpin investor confidence and long-term concession financing for FM operators. Consequently, the Belgium facility management market maintains a balanced regional growth profile, with policy-led renovation in Brussels and Wallonia complemented by tech-sector expansion in Flanders.

Regulatory Landscape

Belgium facility management demand is shaped by EU and national requirements spanning building energy, workplace safety, indoor environmental quality, and digital compliance. The EU Energy Performance of Buildings Directive (EPBD) continues to anchor retrofit-led technical FM scopes (energy audits, commissioning, metering and verification). At the same time, operators of enclosed public places must comply with Belgiums indoor air quality framework under the Law of 6 November 2022, which scales obligations through 2037 and strengthens the business case for IAQ monitoring, ventilation performance checks, and documented maintenance regimes.

Digital and administrative compliance is tightening in parallel. From 1 January 2026, Belgium mandates structured B2B electronic invoicing with Peppol as the default standard, pushing FM providers to standardize billing and subcontractor flows for multi-site, multi-service contracts. For connected buildings and critical sites, cybersecurity and incident governance under NIS2-relevant obligations, together with oversight from the Belgian Institute for Postal Services and Telecommunications (BIPT), reinforces supplier due diligence for IoT, BMS, and remote-monitoring stacks, particularly when FM providers operate or manage networked systems in client environments.

Value Chain Analysis

The Belgium facility management value chain begins with building owners and occupiers (commercial landlords, public bodies, industrial and logistics operators) defining service scope and compliance requirements. It then moves to lead FM contractors (single, bundled, or integrated), which design SLAs, mobilize delivery teams, and manage subcontractors. Upstream inputs include labor (technical trades and cleaning), equipment and consumables, and, increasingly, digital layers such as FMIS/CMMS, BMS integration, IoT sensors, and cybersecurity controls. Platform providers and integrators connect data from assets to help desks, scheduling, and performance reporting that supports energy and ESG disclosures.

Execution relies on on-site technicians, mobile field services, and specialist partners (HVAC, fire and life safety inspections, security, waste, catering) coordinated through service desks and command centers. Downstream, outcomes are verified through KPI reporting, regulatory documentation (workplace safety, air quality, energy performance), and financial settlement, with standardized e-invoicing workflows taking effect from 2026. Bottlenecks remain concentrated in skilled-labor availability and in the integration effort needed to connect legacy building systems into unified dashboards, which elevates the role of solution partners able to integrate SAP/enterprise systems with operational technology and automate workflows at multi-site customers.

Competitive Landscape

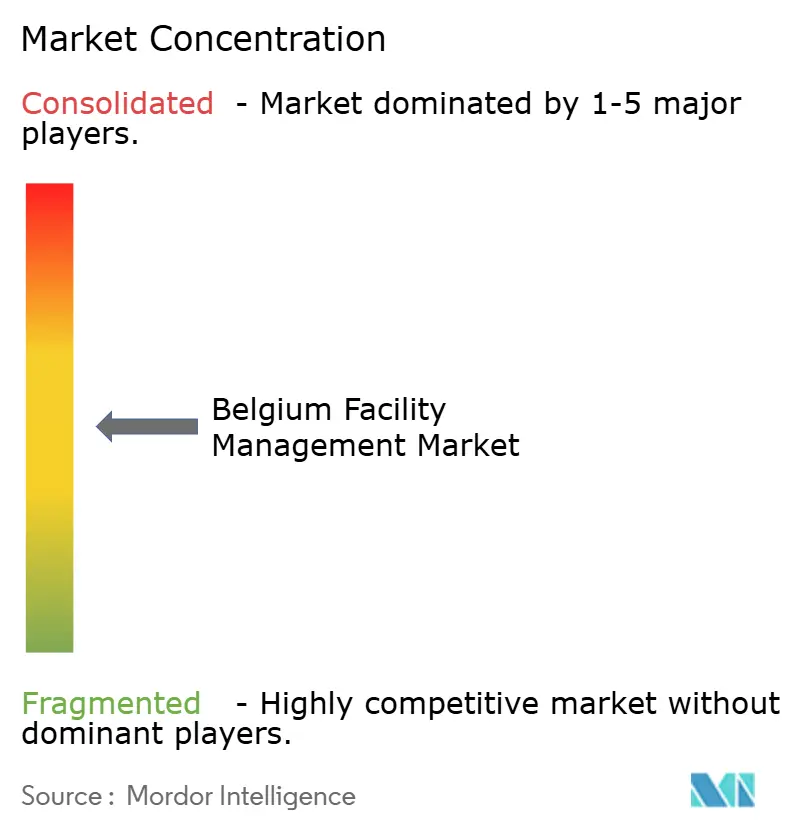

The Belgium facility management market is moderately fragmented: the top five players-ISS, Sodexo, CBRE, SPIE Belgium and Equans-collectively command just below 50% revenue, while a long tail of domestic specialists services municipal and SME portfolios. Multinationals leverage central purchasing and digital-platform investments to satisfy stringent SLAs across multilingual sites. ISS’s 7-year UK Department for Work and Pensions contract, valued at DKK 1.2 billion annually, demonstrates the group’s capacity to mobilise large public contracts and cross-deploy expertise to Belgium. Sodexo’s acquisition spree in convenience solutions diversifies footfall-driven services that can be replicated in Belgian hybrid-office cafeterias.

Regional specialists differentiate through niche engineering depth and rapid response times. SPIE Belgium’s IoT-enabled command centre coordinates preventive tasks across 500+ assets, delivering real-time status dashboards that satisfy CSRD article requirements . Facilicom pilots autonomous vacuum bots and algae-based cleaning agents, appealing to occupiers chasing WELL or BREEAM credits. M&A reshapes the field: Bouygues’ EUR 7.1 billion buy-out of Equans in 2022 created a 74,000-employee multi-technical giant, adding competitive heft in Belgian tenders.

Technology is the new battleground: cloud-native CMMS, AI fault prediction and real-time energy analytics allow providers to pitch outcome-based models that guarantee kilowatt-hour reductions. Those able to bundle financing for deep retrofit alongside operations win programme-management mandates under EPBD, locking rivals out for a decade. ESG advisory add-ons grow in importance; BESIX RED’s ESG Impact Report underscores market expectation for transparent social and environmental metrics from FM suppliers. This convergence of engineering, digital and sustainability skillsets defines competitive advantage in the Belgium facility management market.

Belgium Facility Management Industry Leaders

Serco Europe

ISS World Belgium

Savills

Vinci Facilities Limited Belgium

Facilicom Solutions

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Public-sector digitalization and automation programs create a tangible demand lane for FMIS modernization and workflow automation in Belgium. In Flanders, policy direction includes a mandate to automate 70% of viable facility processes by 2027, and Het Facilitair Bedrijf moved in January 2026 to operationalize a new FMIS while integrating AI use cases into facility processes. These steps increase procurement visibility for standardized request intake, work-order automation, and analytics-ready asset data, widening whitespace for providers that bundle software-enabled service desks, field-force orchestration, and auditable reporting into integrated FM contracts for government and adjacent institutional portfolios.

Compliance-driven technical scopes also broaden opportunities where FM contractors connect building operations with security and reporting requirements. EPBD-linked retrofit workstreams, indoor air quality obligations for enclosed public places, and NIS2-related cybersecurity expectations for connected building systems are shifting RFPs toward vendors that can combine hard FM delivery with data governance, secure remote monitoring, and measurable outcomes (energy baselines, IAQ indicators, maintenance traceability). Smart-building automation pilots pursued by bodies such as VLAIO and VEB further encourage retrofit-friendly sensor deployment and building-automation upgrades in existing public buildings, supporting solution ecosystems around IoT installation, BMS integration, and performance contracting administration.

Recent Industry Developments

- May 2026: Serco confirmed ongoing delivery of integrated facility management services at the Meerdaal military base for the Belgian Ministry of Defence. The activity reinforces defense as a sticky, compliance-heavy end-user where 24/7 readiness, security procedures, and multi-service coordination favor large IFM providers and long-duration outsourcing models.

- December 2025: ISS announced a further expansion of a multi-country contract with a financial services customer. The expansion highlights how large clients consolidate suppliers across geographies and broaden scope under integrated facilities services, raising competitive pressure on smaller single-service vendors in enterprise tenders.

- August 2024: SPIE Belgium won a 10-year technical facility management contract covering three Befimmo office complexes. The long-term mandate strengthens the role of performance-oriented technical FM in commercial real estate portfolios, including preventive maintenance and modernization programs supported by analytics and centralized coordination.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Belgium facility management market covers outsourced services that keep buildings and sites running day to day, including operational support, upkeep, and workplace services delivered under contract.

Scope exclusions: In-house facility teams and purely one-off construction or major renovation work are excluded where they are not part of an ongoing facility service contract.

Segmentation Overview

- By Service Type

- Hard Services

- Asset Management

- MEP and HVAC Services

- Fire Systems and Safety

- Other Hard FM Services

- Soft Services

- Office Support and Security

- Cleaning Services

- Catering Services

- Other Soft FM Services

- Hard Services

- By Offering Type

- In-house

- Outsourced

- Single FM

- Bundled FM

- Integrated FM

- By End-user Industry

- Commercial (IT and Telecom, Retail and Warehouses, etc.)

- Hospitality (Hotels, Eateries, Large-scale Restaurants)

- Institutional and Public Infrastructure (Govt, Education, Transportation)

- Healthcare (Public and Private Facilities)

- Industrial and Process (Manufacturing, Energy, Mining)

- Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market model and to pin down Belgium-specific demand signals before the numbers were finalized. We referred to public sources such as Statbel releases, Eurostat structural business statistics, National Bank of Belgium publications, and EU public procurement portals that show tender activity and contract values.

Along with that, we reviewed annual reports and investor presentations of service providers and large buyers, plus relevant association pages and reputable press, to understand outsourcing patterns and contract length norms. Where needed, paid subscriptions for company financials and intelligence, news and financials, and global contracts and tenders were used to cross-check revenue exposure to Belgium and to track large multi-year awards. These sources are not exhaustive, and additional documents were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating how the facility management wallet is split across services and end users in Belgium, and on testing price and volume assumptions against real buying behavior. We spoke with a mix of service providers, subcontractors, and procurement or site operations contacts across commercial, industrial, and public facilities, so gaps from desk findings could be closed and assumptions could be triangulated with on-ground realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 18% | |

| Mid tier: 48% | Functional/Unit leaders: 33% | |

| Smaller Players: 19% | Managers: 49% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where national services output and outsourcing intensity were first used to reconstruct the addressable FM spend pool, which was then adjusted to match contract-delivered revenues. Once that ceiling was set, selective bottom-up checks were run using sampled provider revenues in Belgium, typical contract values, and observed staffing intensity for large sites. Totals were then corrected where the two views disagreed.

Key inputs included the active building stock and utilization in offices, industrial sites, and public facilities, the share of outsourced versus in-house delivery, average contract duration and renewal patterns, wage inflation for labor-heavy services, and energy and compliance-driven maintenance intensity. Forecasts were built using scenario analysis supported by a short set of drivers that can be refreshed annually, mainly outsourcing rate movement, price progression by service type, and expected activity levels in commercial real estate and public budgets. When bottom-up information was missing for smaller local providers, we filled the gap using calibrated revenue per employee ranges and channel checks, and then rebalanced results back to the demand pool constraints.

Data Validation & Update Cycle

Validation was done in steps so the final value is not dependent on one data stream. We compared model outputs against independent signals like major contract announcements, procurement volumes, and the implied revenue intensity per square meter for different facility types, and then investigated any outliers before sign-off.

A second analyst review was used to challenge the main drivers, especially outsourcing share, pricing, and end-user mix, followed by targeted re-contact with experts when variances were still high. Reports are refreshed annually, with interim updates when material events occur that can change pricing, labor availability, or demand from major end users. Right before delivery, we perform a fresh check so clients receive the latest updated view.

Mordor Intelligence's Belgium Facility Management Market Sizing Compared With Other Published Estimates

Published market sizes for Belgium facility management can differ quite a bit, even when the topic sounds similar. In practice, the gaps usually come from what is counted as facility management revenue, how much in-house activity is assumed to be outsourced, and which price movements are used for multi-year contracts.

By tracking contract-award values, outsourcing rate shifts, and service-level price resets, Mordor Intelligence keeps the estimate tied to contracted FM revenue in Belgium, which is different from approaches that blend in broader building services or use aggressive price escalation without procurement checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.61 B (2025) | |

| Industry Association B | USD 9.08 B (2024) | Often represents a broader facilities function spend view, which can fold in in-house delivery and adjacent workplace or real estate costs, and it may not separate contracted FM revenue from internal budgets. |

| Regional Consultancy A | USD 6.25 B (2026) | Can assume faster outsourcing and price growth across the forecast window, and may apply uniform inflation to all service lines even when renewals and indexation differ by contract type. |

The spread in the table mainly reflects scope boundaries and how pricing and outsourcing are handled year to year. Our approach stays repeatable because the sizing steps are anchored to observable demand signals, followed by cross-checks against provider exposure and tender-led reality checks before the final number is locked.

Key Questions Answered in the Report

What is the current value of the Belgium facility management market?

The Belgium facility management market size was USD 5.78 billion in 2026 and is projected to reach USD 6.73 billion by 2031.

Which service type generates the most revenue?

Hard services, covering MEP, HVAC and asset management, accounted for 59.10% of 2025 revenue.

Why are outsourced contracts growing faster than in-house models?

Outsourcing reduces multilingual compliance burdens and bundles carbon-reporting tasks, pushing outsourced market share to 61.85% in 2025 with a 3.26% CAGR outlook.

How do EU regulations influence market demand?

The EPBD and CSRD compel owners to retrofit buildings and disclose carbon performance, creating steady pipelines for energy-efficient FM services.

Which Belgian region offers the highest growth potential?

Flanders is forecast to record the fastest 3.42% CAGR due to its expanding tech corridors and large-scale renovation targets.

What technologies are changing facility management delivery?

IoT sensors, AI fault-prediction tools and cloud-based energy dashboards cut HVAC energy use and enable outcome-based contracts, bolstering provider competitiveness.

Page last updated on: