Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.02 Billion |

| Market Size (2026) | USD 3.13 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

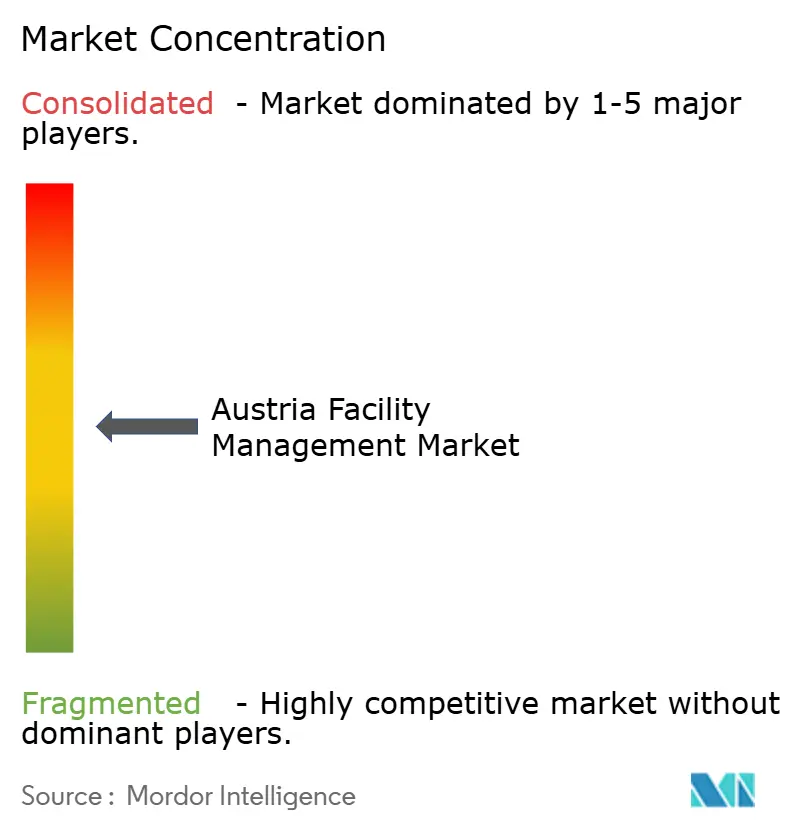

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Facility Management Market Analysis by Mordor Intelligence

Austria facility management market size in 2026 is estimated at USD 3.13 billion, growing from 2025 value of USD 3.02 billion with 2031 projections showing USD 3.74 billion, growing at 3.62% CAGR over 2026-2031. Vienna’s climate-neutrality mandate, an energy cost upsurge of 19% following the phase-out of temporary subsidies, and the construction sector’s tentative 0.2% rebound are shaping service demand profiles. A decisive pivot toward building automation, smart-meter rollouts, and performance-linked contracts is fostering sustained investment in hard services even as soft services dominate day-to-day budgets. Heightened regulatory scrutiny around energy performance, especially in healthcare facilities that account for 6.7% of national CO₂ emissions, is prompting corporates to bundle services under integrated frameworks. Meanwhile, labour shortages and the 3.90% wage hike effective January 2025 continue to squeeze margins, accelerating digital twin and predictive-maintenance adoption among leading vendors.[1]Covenant of Mayors, “Vienna’s Detox for an (Even) Happier City,” eu-mayors.ec.europa.eu

Key Report Takeaways

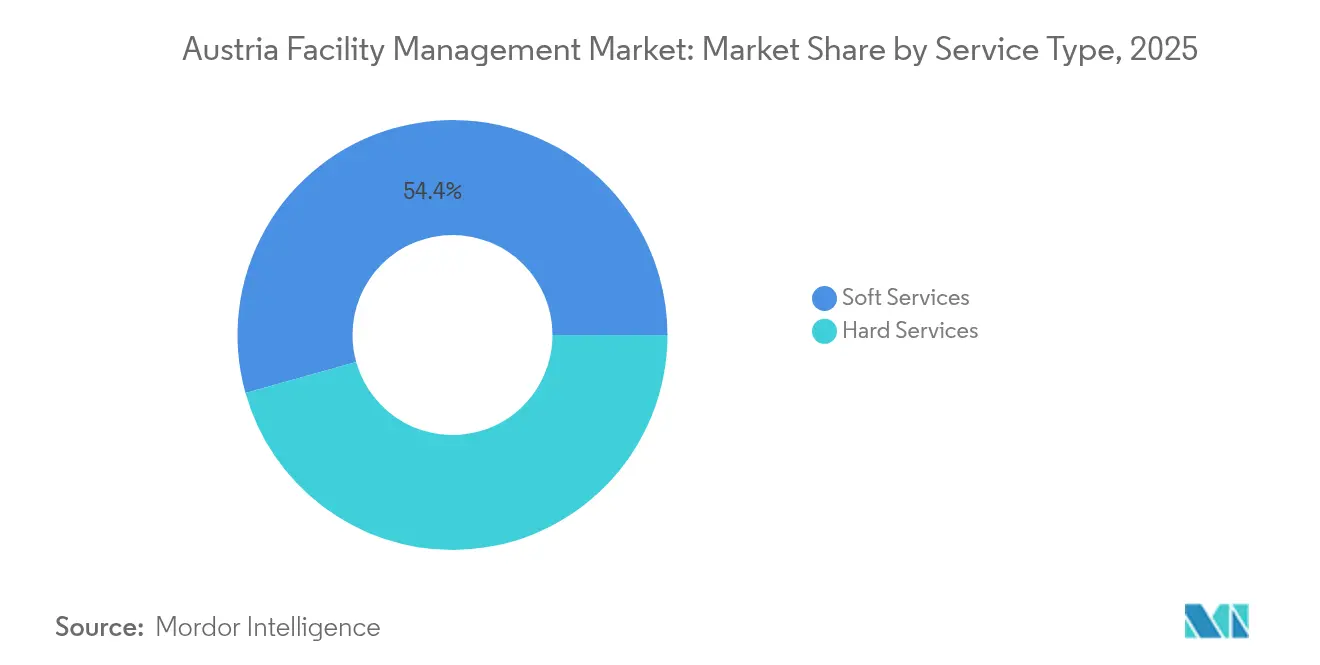

- By service type, soft services held 54.35% of the Austria facility management market share in 2025, while technical hard services are projected to expand at a 6.45% CAGR to 2031.

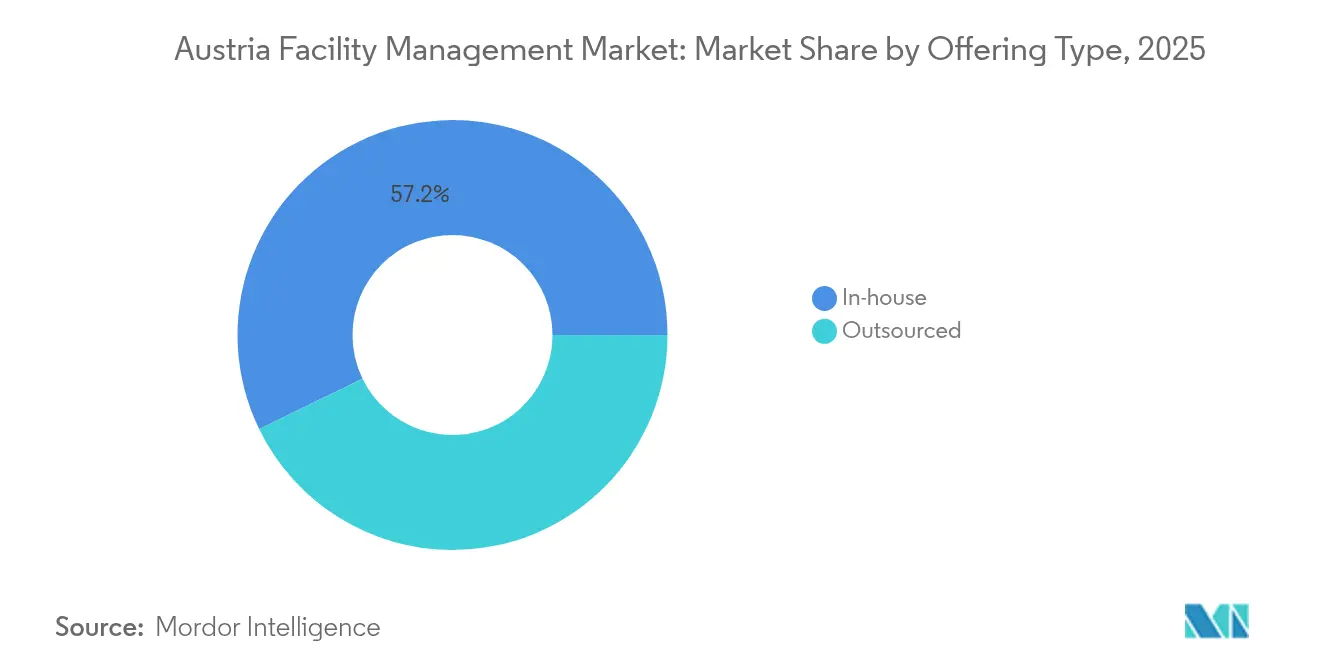

- By offering type, in-house delivery retained 57.20% share of the Austria facility management market size in 2025; integrated FM outsourcing is advancing at a 8.75% CAGR through 2031.

- By end-user Industry, the commercial segment accounted for 34.10% of the Austria facility management market in 2025, whereas healthcare is set to rise at a 7.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Current Occupancy Rates: Hybrid Work Models Reshape Space Utilization | 1.20% | Vienna, Graz, Linz metropolitan areas | Medium term (2-4 years) | |

| Profitability Rates of Major FM Players: Margin Pressure Drives Innovation | 0.80% | National, concentrated in commercial hubs | Short term (≤ 2 years) | |

| Workforce Indicators – Labor Participation: Skill Shortages Reshape Service Delivery | 0.60% | National, acute in Vienna and Salzburg | Long term (≥ 4 years) | |

| Urbanization and Population Growth in Major Metros: Density Drives Service Complexity | 0.90% | Vienna, Graz, Linz, Salzburg | Long term (≥ 4 years) | |

| Current Occupancy Rates: Hybrid Work Models Reshape Space Utilization | 1.20% | Vienna, Graz, Linz metropolitan areas | Medium term (2-4 years) | |

| Profitability Rates of Major FM Players: Margin Pressure Drives Innovation | 0.80% | National, concentrated in commercial hubs | Short term (≤ 2 years) | |

| Source: Mordor Intelligence | ||||

Current Occupancy Rates - Hybrid Work Models

Flexible-work policies are shrinking traditional office footprints yet increasing daily fluctuations in space usage, prompting operators to adopt IoT occupancy sensors and cloud scheduling tools. Enhanced cleaning frequency, touch-free access, and dynamic energy-load balancing are becoming standard service add-ons. Vienna’s Smart City agenda encourages FM firms to integrate real-time building data into municipal dashboards to optimise energy and mobility flows. Providers responding fastest are embedding workplace-as-a-service models that bundle space analytics, remote helpdesk, and maintenance fulfilment, turning fluctuating demand into a recurring-revenue stream.[2]Partium, “Partium x Wien Energie Case Study,” partium.io

Profitability Rates of Major Facility Management Players

A 3.90% baseline wage rise, and double-digit network-energy cost hikes have narrowed gross margins for most suppliers. Market leaders such as Dussmann lifted FM division sales 10.5% in 2023 by absorbing Janus Group’s healthcare portfolio and rolling out robotics-supported cleaning. Service providers are pooling procurement, automating back-office workflows, and piloting subscription-based energy-management modules that directly tie fees to consumption savings.[3]Wirtschaftskammer Österreich, “Kollektivvertrag Gewerbe, Handwerk und Dienstleistung 2025,” wko.at

Workforce Indicators - Labor Participation

Austria’s working-age population is on track to shrink 5-8% by 2030, aggravating shortages in HVAC, building automation, and technical cleaning. SIMACEK responds by widening Central-European recruitment funnels and running dual-education tracks with vocational schools. Growth in remote monitoring and predictive maintenance reduces onsite staffing dependency, yet the sector still invests heavily in AR-assisted repair guides and micro-credential programs to upskill existing teams.

Urbanization & Population Growth in Major Metros

Vienna targets a 35% greenhouse-gas reduction by 2030, embedding renewables and district-heating loops into dense mixed-use zones. Projects like the EUR 200 million Seestadt Aspern vocational campus deploy geothermal and photovoltaic systems that require life-cycle asset oversight. High-rise infill and transit-oriented development are expanding vertical-transport and façade-maintenance workloads, rewarding FM firms capable of bundling safety, energy, and community-engagement services into single contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortages: Demographic Headwinds Constrain Growth | -1.10% | National, acute in Vienna and technical centers | Long term (≥ 4 years) |

| Technology Adoption Costs: Investment Barriers Delay Transformation | -0.70% | National, concentrated in SME segment | Medium term (2-4 years) |

| Skilled Labor Shortages: Demographic Headwinds Constrain Growth | -1.10% | National, acute in Vienna and technical centers | Long term (≥ 4 years) |

| Technology Adoption Costs: Investment Barriers Delay Transformation | -0.70% | National, concentrated in SME segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages – Demographic Headwinds

Declining birth rates and retirements are eroding the talent pipeline, particularly for advanced BMS, HVAC, and fire-safety technicians. Providers lure scarce specialists with above-market wages and flexible rosters while investing in campus partnerships. Automation is filling gaps yet cannot fully replace competency in regulatory audits and complex retrofits, slowing project rollouts in sensitive facilities.

Technology Adoption Costs – Investment Barriers

Full-scale smart-building conversions cost EUR 50 000–500 000 per site and often exceed SME budget thresholds, stretching payback horizons beyond five years. Mandatory smart-meter deployment under the revised Electricity Economics Act illustrates the financial burden, with implementation costs of EUR 2.53 billion outweighing direct benefits. Leasing, energy-performance contracts, and staged retrofits are emerging as viable pathways, yet organizational inertia continues to delay transformative upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft Services Dominate Amid Technical Transformation

Soft services captured 54.35% of the Austria facility management market share in 2025 thanks to enduring demand for cleaning, security, and hospitality functions. The category remains indispensable in offices, healthcare, and hospitality, even as vendors face tighter margins from labour cost inflation. Cleaning leads the sub-mix, with robotics-assisted floor care and antimicrobial coatings extending contract scope. Security services increasingly integrate cloud CCTV, biometric access, and cyber-monitoring to protect hybrid offices and data centers. Catering retains relevance by aligning menus with ESG metrics and waste-recovery programs.

Hard services are on a steeper growth path, rising at a 6.45% CAGR through 2031. Within hard services, MEP and HVAC retrofits gain urgency as Vienna prepares to phase out gas heating by 2040, driving adoption of heat pumps and thermal-storage systems. Building-automation and IoT suites unlock predictive-maintenance value, lengthening asset life and lowering energy use. The Austria facility management market size for technical services is poised to widen as asset owners demand ESG reporting aligned to EU taxonomy thresholds. Fire-safety compliance, lift-maintenance digitization, and façade-access robotics round out high-growth niches. Together, the diverging trajectories of soft and hard services underscore a marketplace bifurcating between volume-driven routines and expertise-driven technical disciplines.

By Offering Type: Integrated Models Gain Traction

In-house teams still delivered 57.20% of total services in 2025, sustained by owner preference for direct oversight of statutory compliance and cultural alignment. Yet skill shortages and the complexity of ESG disclosure rules are exposing capability gaps that internal departments struggle to fill. Companies therefore lean on targeted outsourcing for energy audits, waste valorisation, and asset-condition surveys.

Integrated facility management (IFM) outsourcing is the fastest-advancing format, on track for a 8.75% CAGR. Multi-year, outcome-based contracts like the 25-year PORR-Apleona vocational school engagement are setting new benchmarks for value capture and lifecycle risk transfer. The Austria facility management market size for bundled and single-service contracts is consequently expected to plateau, nudging suppliers toward end-to-end offerings that weave soft and hard services into shared digital platforms. Providers scoring highest on sustainability metrics, data transparency, and innovation pipelines are thus emerging as preferred partners for corporates navigating regulatory change.

By End-User Industry: Healthcare Leads Growth Trajectory

Commercial real estate dominated with 34.10% share in 2025, supported by IT-telecom hubs, logistics parks, and mixed-use malls. However, hybrid work has thinned weekday footfall, prompting landlords to recalibrate cleaning rosters and energy-set points.

Healthcare is the fastest-growing vertical, projected at 7.05% CAGR through 2031 as demographic ageing and clinical-infrastructure modernisation spur demand for high-specification FM. Hospitals require continuous HVAC calibration, infection-control cleaning, and resilience audits tied to 24/7 operations. The Austria facility management market size serving healthcare facilities is further buoyed by the sector’s commitment to carbon-neutrality pathways, opening opportunities for renewable-heat integration and circular-procurement services. Hospitality, benefiting from 18.1% RevPAR growth in April 2025, remains a bright spot for energy-efficient refurbishments, while institutional estates maintain steady demand anchored in public-funding cycles. Industrial complexes and multi-housing schemes also require specialised FM as they decarbonise process loads and enhance tenant amenities.

Geography Analysis

Vienna is the epicentre of the Austria facility management market, combining dense public administration, healthcare campuses, and corporate headquarters. Smart-city investments drive pilots in district heating, waste-heat recovery, and AI-enabled mobility nodes, yielding fertile ground for service innovation. The Austria facility management market size linked to Vienna alone is expected to outpace the national average as fresh capital migrates toward smart-district retrofits and net-zero public buildings.

Graz and Linz form the second tier of demand. Graz’s move2zero strategy to decarbonise its bus fleet amplifies need for depot energy management and fleet-charging maintenance, while the city’s industrial R&D spine seeds opportunities in laboratory FM and cleanroom upkeep. Linz, with a steel-centric industrial base transitioning to hydrogen, requires integrated hard-service bundles to modernise heavy plant utilities. Salzburg, driven by tourism and cultural venues, leans on adaptive cleaning rotations and guest-experience technologies that align with peak visitor seasons.

Regional markets outside the metropolitan quartet remain fragmented yet promising, particularly where hospital networks and vocational campuses concentrate. Rural renewable-energy installations, including wind-repowering projects, add pockets of specialised FM demand for turbine, substation, and access-road maintenance. Collectively, the geographic mosaic underscores a need for providers with both nationwide reach and local cultural fluency.

Competitive Landscape

Austria’s facility management arena is moderately fragmented. ISS Österreich leverages a 7 000-strong workforce and data-driven KPIs to serve large commercial and institutional clients, sustaining revenue synergies across cleaning, catering, and technical services. SIMACEK, Austria’s largest privately held provider, generated more than EUR 200 million across Central Europe and continues to scale through technology partnerships and ESG reporting tools. Dussmann, fresh from a record EUR 3 billion group turnover, integrates robotics and green-energy retrofits to safeguard margins in a tight labour market.

Strategic differentiation tilts toward digitisation. Market leaders’ pilot digital twins, remote metering, and asset-health dashboards that shrink downtime and boost regulatory compliance. Mid-tier contenders bundle niche strengths-such as heritage-building conservation or high-security data-center protocols-into collaboration models with bigger integrators. Consolidation is expected to accelerate as smaller vendors grapple with capital-intensive technology mandates and wage inflation. Sustainable procurement, transparent Scope 3 reporting, and tenant-wellbeing metrics are emerging selection criteria in new tenders, favouring providers that embed ESG proof-points into contract SLA structures.[4]ISS Österreich, “Ihr Partner für integrierte Facility Services,” issworld.com

Austria Facility Management Industry Leaders

ISS Facility Services GmbH

Apleona GmbH

STRABAG Property & Facility Services GmbH

Sodexo Österreich

SIMACEK Facility Management Group GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Marriott International signed to convert five Austria Trend Hotels, adding 1 100 rooms to its national footprint.

- April 2025: A by Adina Vienna Danube opened 120 automated studios in Danubeflats tower.

- March 2025: Vonovia slated construction of 3 000 new energy-efficient flats with PV retrofits.

- January 2024: REWE Group announced 50 new stores and 200 refurbishments with sustainability focus.

Austria Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through its responsibility for maintaining what is often an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

Facility management services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services spheres.

Both in-house facility management and outsourced FM services are considered in the scope. The market for integrated facility management service (IFM), along with single and bundled services, is included in the outsourced FM services segment.

The Austria facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-User Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-User Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Austria facility management market?

It was valued at USD 3.13 billion in 2026.

How fast is the Austria facility management market expected to grow?

The market is forecast to post a 3.62% CAGR and reach USD 3.74 billion by 2031.

Which service category is expanding the quickest?

Technical hard services, growing at a 6.45% CAGR due to smart-building retrofits and energy-efficiency mandates.

Why is healthcare the fastest-growing end-user segment?

Ageing demographics and the sector’s drive toward carbon-neutral operations are boosting specialised FM demand.

What factors are pushing companies toward integrated outsourcing models?

Regulatory complexity, skill shortages, and the need for unified ESG reporting are encouraging adoption of integrated facility management contracts.

How are rising labor costs influencing FM providers?

A 3.90% salary rise, and ongoing talent shortages are spurring investment in automation and predictive maintenance to sustain profitability.

Page last updated on: