Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

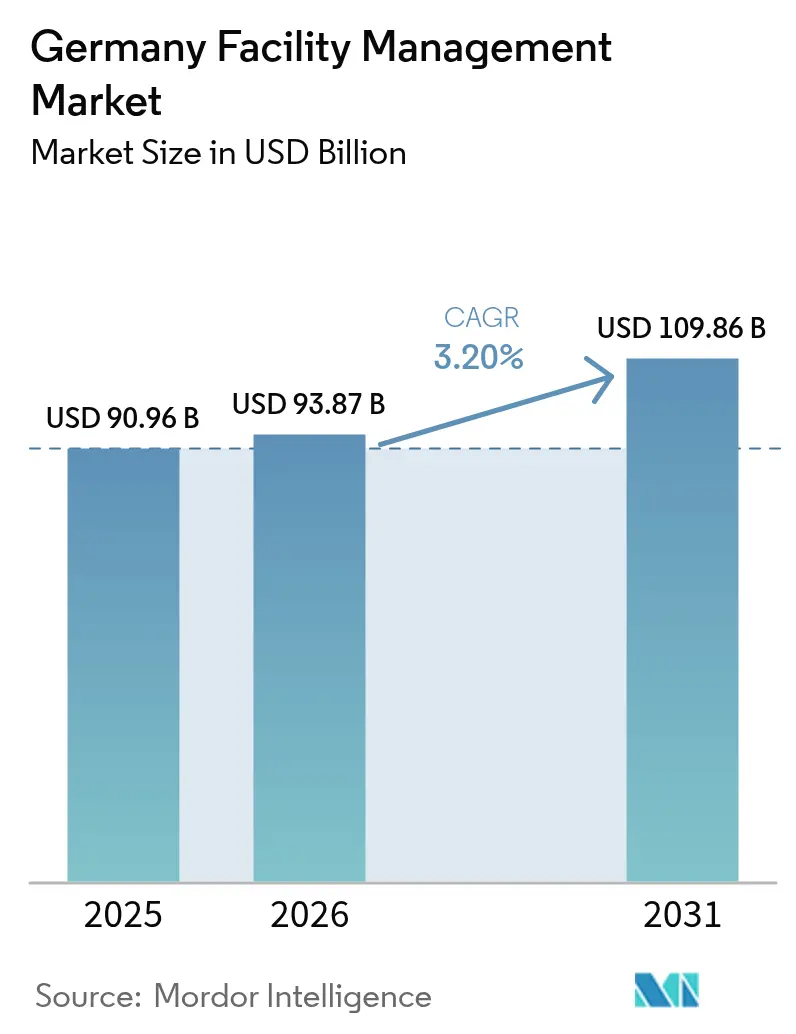

| Base Year Market Size (2025) | USD 90.96 Billion |

| Market Size (2026) | USD 93.87 Billion |

| Market Size (2031) | USD 109.86 Billion |

| Growth Rate (2026 - 2031) | 3.20% CAGR |

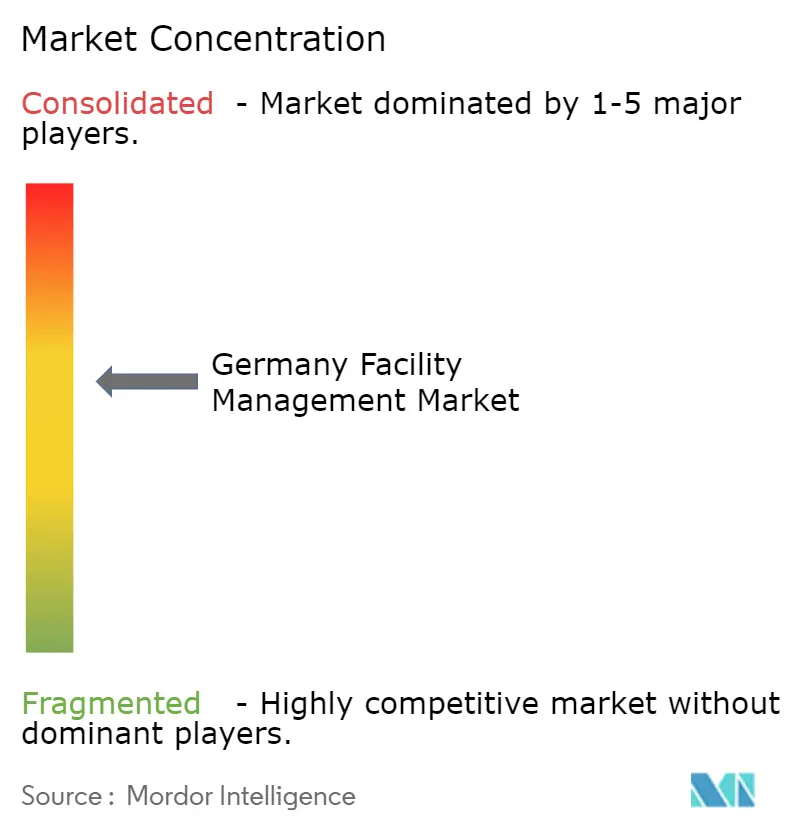

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Facility Management Market Analysis by Mordor Intelligence

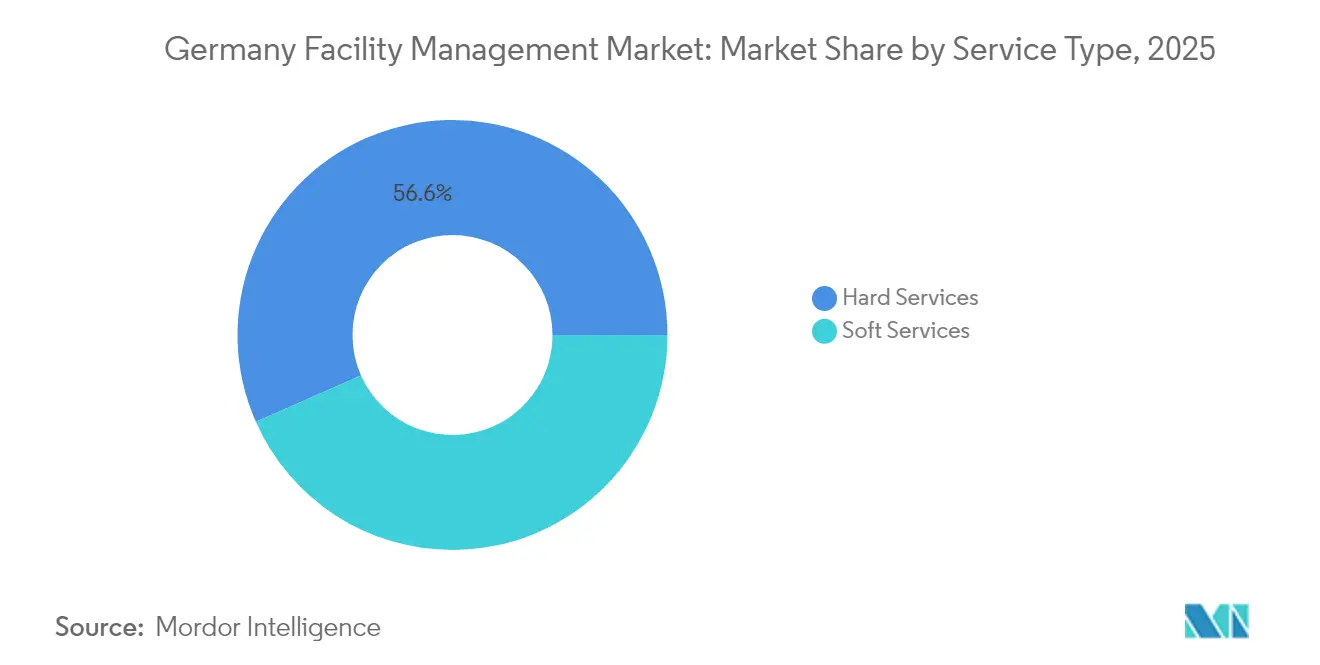

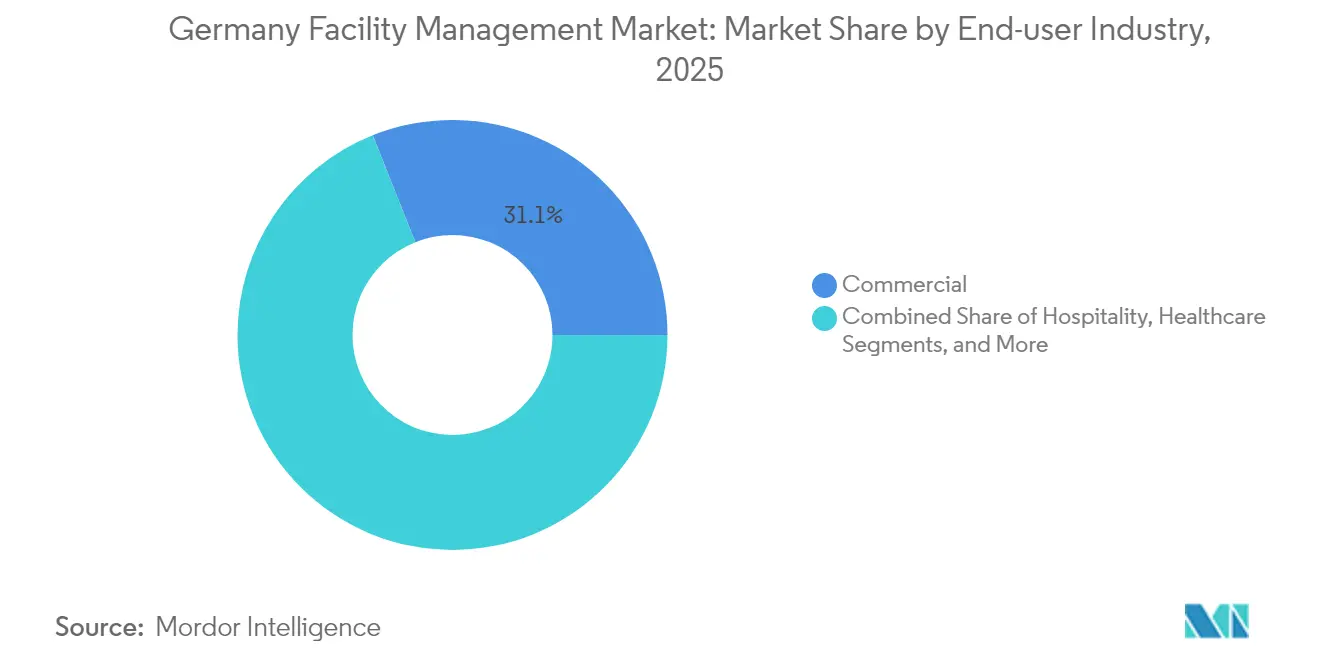

The Germany facility management market size was valued at USD 90.96 billion in 2025 and estimated to grow from USD 93.87 billion in 2026 to reach USD 109.86 billion by 2031, at a CAGR of 3.20% during the forecast period (2026-2031). This stable trajectory reflects the sector’s ability to withstand Germany’s longest recession since 2002 while supporting mandatory upgrades required by the Gebäudeenergiegesetz (GEG) and other energy-efficiency statutes. Hard Services continue to command spending because building operators must retrofit HVAC and MEP systems to satisfy the 65% renewable-heat rule, whereas Soft Services are growing faster as occupiers pivot toward wellness and hybrid-workplace programs. Outsourcing momentum persists on the back of integrated contracts that pool multiple functions under one provider, even though in-house teams still dominate. Commercial real estate leads demand; however, healthcare, education, and other public assets are expanding quickly as stimulus funding modernizes critical infrastructure. Fragmented competition and chronic skilled-labor shortages reinforce the need for digitization, automation, and ESG-driven value propositions across the Germany facility management market.

Key Report Takeaways

- By service type, Hard Services held 56.62% of the Germany facility management market share in 2025, while Soft Services are projected to post the fastest 5.29% CAGR through 2031.

- By offering type, in-house models accounted for 58.95% of the Germany facility management market size in 2025, whereas outsourced contracts are anticipated to expand at a 3.97% CAGR by 2031.

- By end-user industry, commercial facilities captured 31.05% revenue share in 2025, yet institutional and public infrastructure assets are forecast to record a 5.11% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Energy Efficiency Regulations | +1.2% | Germany nationwide, with early implementation in major metros | Medium term (2-4 years) |

| ESG Compliance Momentum | +0.8% | Germany nationwide, with spillover to EU markets | Long term (≥ 4 years) |

| Digital Transformation and Smart Buildings | +0.6% | Germany core cities, expanding to secondary markets | Medium term (2-4 years) |

| Workforce Automation Momentum | +0.4% | Germany nationwide, concentrated in industrial regions | Long term (≥ 4 years) |

| Growing Adoption of Green Building Certifications | +0.3% | Germany major cities, expanding to regional markets | Medium term (2-4 years) |

| Health and Wellness Oriented Facility Standards | +0.2% | Germany nationwide, with focus on commercial sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Energy Efficiency Regulations

The Gebäudeenergiegesetz requires new heating systems installed from 2024 to derive at least 65% of heat from renewable sources, pushing operators to upgrade boilers, chillers, and distribution networks. HVAC units exceeding 12 kW must pass periodic energy inspections by certified experts, and owners face fines when deadlines lapse.[1] buzer.de, “Energetische Inspektion von Klimaanlagen,” buzer.deComplementary rules under the Energy Efficiency Act oblige enterprises to deploy energy-management systems covering 90% of consumption and to publish reduction roadmaps. These mandates elevate demand for monitoring sensors, analytics dashboards, and performance contracting services that guarantee savings. Service providers able to bundle auditing, retro-commissioning, and financing options gain a competitive advantage in the Germany facility management market.

ESG Compliance Momentum

The Corporate Sustainable Reporting Directive will triple the number of German entities producing non-financial statements, reaching nearly 15,000 by 2026. [2]ICLG, “Environmental, Social & Governance Law Germany 2025,” iclg.comICLG, “Environmental, Social & Governance Law Germany 2025,” iclg.com Buildings contribute around 30% of national CO₂ emissions, making facility operations a high-impact target. DGNB’s “double materiality” lens obliges firms to disclose how their activities affect people and planet and how sustainability risks affect revenues. In response, providers now embed CO₂ baselines, renewable sourcing plans, and waste-reduction KPIs into service-level agreements. High-profile appointments, such as ISS naming a Group Head of ESG, underline how credentials drive bid evaluation and project awards. This alignment is nudging the Germany facility management market toward outcome-based pricing tied to verified emissions cuts.

Digital Transformation and Smart Buildings

IoT platforms that unify meters, sensors, and legacy automation protocols are scaling throughout premium offices, logistics hubs, and mixed-use campuses. Start-ups such as metr deploy interoperable gateways that capture heating, water, and air-quality data across heterogeneous equipment fleets, allowing centralized analytics and remote optimization. Academic trials have recorded 24.52% average energy savings and 8.12 tons of CO₂ reductions per building when AI-guided set-points adjust boiler and valve operation in real time. Siemens and Stadtwerke Stuttgart demonstrated that coupling PV, battery storage, and heat pumps with grid-aware control trims electricity bills up to 30% while easing peak-load stress. Yet 60% of German buildings were erected before 1995 and still house proprietary controls that impede plug-and-play upgrades, so brownfield integration remains a core technical hurdle.

Workforce Automation Momentum

Germany has more than 150,000 open positions in construction-related trades, and the metal-electrical cluster alone counts 110,000 vacancies vital to building services. Robotic cleaners, autonomous lawn mowers, and kitchen cobots already supplement stretched teams in hospitals and campuses; Sodexo’s program at Tübingen University Hospital highlights efficiency gains in catering workflows. Facility management firms now allocate sizable budgets to internal academies that cross-train staff on connected devices, cybersecurity basics, and predictive-maintenance protocols. As demographic trends signal a shrinking labor pool, adoption of sensor-triggered work orders, AR-assisted inspections, and centralized command centers will accelerate across the Germany facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Implementation Costs | -0.7% | Germany nationwide, with higher impact in SME segments | Short term (≤ 2 years) |

| Cybersecurity and Data Privacy Concerns | -0.4% | Germany nationwide, with focus on critical infrastructure | Medium term (2-4 years) |

| Fragmented Vendor Ecosystem and Pricing Pressure | -0.3% | Germany nationwide, with concentration in competitive metros | Medium term (2-4 years) |

| Legacy Building System Interoperability Challenges | -0.2% | Germany nationwide, with higher impact in industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Implementation Costs

Energy-positive retrofits, advanced sensors, and on-site renewables often require capital outlays that stretch budgets during a downturn. The property sector saw deal volumes fall 52% to EUR 31.7 billion (USD 36.94 billion) in 2023, tightening credit for large upgrades.[3] Emova "Building Energy Act 2025 – new requirements and funding opportunities," emova.de Owners worry that GEG-mandated boiler replacements might raise rents, provoking tenant resistance and delaying project approvals. Construction spending is projected to contract by 3.5% in 2025, so phased roll-outs, leasing models, and public grants become essential financing levers. Without these supports, some operators may defer or scale back technology investments, muting growth potential for the Germany facility management market in the near term.

Cybersecurity and Data Privacy Concerns

Smart devices broaden attack surfaces, and Germany’s strict GDPR regime amplifies risk perception. Academic work from the University of Regensburg stresses the need for standardized threat-intelligence formats to protect complex, multi-vendor estates. Operators of HVAC and refrigeration assets must also comply with new logging obligations under the revised F-Gas Regulation effective 2024, adding layers of data governance complexity. Many critical-infrastructure owners still prefer on-premise servers to cloud platforms, sacrificing scalability for perceived sovereignty. Hesitancy slows adoption of predictive analytics that could otherwise cut downtime and utility costs across the Germany facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technical Dominance Holds as Wellness Gains Traction

Hard Services contributed 56.62% of 2025 revenue because regulatory compliance tasks such as HVAC retro-commissioning and electrical safety inspections demand deep engineering know-how. Mechanical, electrical, and plumbing teams schedule thermographic surveys, balance hydronic circuits, and tune building-automation logic to align with GEG thresholds. Asset-management consultancies overlay life-cycle planning on an aging real-estate stock where 60% of properties exceed 30 years. As the Germany facility management market size for Hard Services tightens around legally enforceable performance targets, suppliers invest in sensor-equipped toolkits and cloud analytics that speed issue detection and track warranty claims.

Soft Services, forecast at a 5.29% CAGR, mirror employers’ focus on occupant well-being. Heightened cleaning standards integrate UV-C disinfection robots for after-hours sweeps, while hospitality-grade front-of-house teams curate hybrid-work experiences through flex-desk management apps. Security guards increasingly deploy AI-enabled video analytics that distinguish safety breaches from routine events. Sodexo’s robotic kitchen use case shows how automation raises throughput in healthcare catering without compromising nutrition. The growing appetite for tech-infused Soft Services suggests that their Germany facility management market share will rise steadily through 2031, even though value creation remains tethered to wellness metrics more than mandated compliance thresholds.

By Offering Type: Outsourcing Narrows the Control Gap

Historically, German enterprises retained 58.95% of services in-house to preserve direct oversight and unionized labor structures. Manufacturing plants in North Rhine-Westphalia and Baden-Württemberg exemplify vertically integrated maintenance shops that calibrate production-critical utilities alongside facility tasks. Yet the expanding rulebook covering energy efficiency, ESG reporting, and occupational health overwhelms internal teams, especially where vacancies persist. Outsourced contracts, already advancing at a 3.97% CAGR, bundle multiple scopes under key performance indicators that track uptime, CO₂ savings, and user-satisfaction scores. The sale of Apleona to PAI Partners injected fresh capital for digital platforms and regional expansion, signalling that scale and specialization increasingly tilt the Germany facility management market toward external providers.Integrated FM stands out inside the outsourcing mix because single master agreements reduce vendor fragmentation and simplify governance. Bundled FM appeals to mid-sized owners that want cost relief yet are not ready for full integration. Single-service contracts remain useful for niche functions such as vertical transportation or landscaping in heritage sites where specific certifications apply. As providers enhance energy-consultancy, BIM-enabled asset management, and carbon accounting within package deals, in-house share may erode further over the forecast horizon.

By End-User Industry: Commercial Core While Public Assets Accelerate

Commercial buildings captured 31.05% revenue in 2025 as finance, technology, and retail tenants concentrated in Frankfurt, Berlin, and Munich resumed leasing momentum. The office market registered 704,000 m² of turnover in Q1 2025, an annual jump of 16% that revitalized demand for daily operations, fit-out coordination, and green-lease compliance. Data-center expansions by cloud providers intensify requirements for redundant power, precision cooling, and real-time monitoring. Warehousing networks supporting e-commerce rely on integrated security patrols and automated material-handling upkeep. These diverse needs guarantee a stable anchor for the Germany facility management market despite cyclical swings.

Institutional and public infrastructure assets represent the fastest-growing slice, forecast at 5.11% CAGR. Federal healthcare modernization funnels funds into hospitals, rehabilitation centers, and elder-care homes. Real-estate investment in healthcare reached EUR 1.68 billion (USD 1.96 billion) in the last published cycle, and occupancy-based HVAC fault detection, sterilization workflows, and patient-comfort analytics shape FM scopes. Government agencies refurbish administrative campuses to hit net-zero targets, while educational boards upgrade ventilation and lighting to support digital classrooms. Transport facilities—from rail depots to regional airports—seek concession partners capable of 24/7 safety assurance and lifecycle cost optimization. These programmatic investments diversify revenue streams and lift overall resilience of the Germany facility management market.

Geography Analysis

Metropolitan clusters command a disproportionate share of contracts because they house dense commercial stock, multinational headquarters, and early adopters of smart-building retrofits. Frankfurt led Q1 2025 office turnover at 204,000 m², up 71% year on year, followed by Munich at 137,000 m² and Hamburg at 111,000 m². Owners in these cities fast-track IoT rollouts and install rooftop photovoltaics paired with battery storage, widening the technical FM scope. Local energy agencies disseminate subsidies that offset capex for heat-pump conversions, tilting project pipelines toward integrated providers. Consequently, the Germany facility management market sees high bidding intensity and ambitious performance clauses inside these urban centers.

Industrial heartlands such as North Rhine-Westphalia and Baden-Württemberg display elevated demand for mechanical services tied to process cooling, compressed-air reliability, and machine-hall ventilation. Yet acute labor shortages in metal and electrical trades hamper self-performing models, nudging factories to co-source engineering tasks. Service firms offering robotics expertise and predictive-maintenance algorithms find receptive clients, particularly where downtime threatens export schedules. Policy packages that bankroll semiconductor fabs and battery-cell plants widen the regional FM addressable market.

Secondary and tertiary municipalities witness incremental uptake as public-sector grants for social housing and climate adaptation become available. Smaller local authorities lean on outcome-based contracts to bridge skill gaps, allowing providers to roll out standardized toolkits originally perfected in major metros. Building-law amendments assign earlier renewable-heat deadlines to larger cities, but staggered compliance timetables ensure that demand waves ripple into rural districts through 2030. This phased structure underpins a steady regional expansion path for the Germany facility management market.

Regulatory Landscape

Germany's regulatory framework is tightening around energy performance, digital monitoring, and resilience, which is directly shaping hard FM scopes. Under the Building Energy Act (GEG), non-residential buildings meeting defined thresholds must implement ongoing energy monitoring and technical commissioning management for heating and cooling systems, and certain large systems are required to install building automation and control systems compliant with at least automation grade B (DIN V 18599-11) under Section 71a.

In 2026, security and digital-compliance obligations expanded for operators and service providers supporting critical and data-intensive facilities. The Act for Critical Facilities (KRITIS-DachG) entered into force on March 17, 2026, implementing the EU CER Directive and requiring in-scope companies to register with the Federal Office of Civil Protection and Disaster Assistance (BBK) and the Federal Office for Information Security (BSI) by July 17, 2026. Separately, the AI Market Surveillance and Innovation Promotion Act (KI-MIG) adopted in June 2026 designates the Bundesnetzagentur (BNetzA) as the central market surveillance authority for the EU AI Act, with high-risk AI obligations taking effect on August 2, 2026. That timeline lifts governance requirements for FM workflows that deploy AI-enabled monitoring, dispatching, or predictive maintenance in regulated environments.

Value Chain Analysis

The Germany facility management value chain runs from asset owners and occupiers (commercial real estate, industrial sites, healthcare, education, and public infrastructure) to consulting and compliance services such as energy audits, commissioning management, and ESG and reporting support, and then to execution partners covering hard and soft services. Technical subcontractor networks cover HVAC, MEP, fire and life safety, refrigeration, and building-automation specialists, while OEMs and platform providers supply BMS/IoT layers, sensors, gateways, and analytics that connect OT equipment with enterprise IT systems.

A growing share of value is accruing to providers that run digital platforms and managed services rather than only labor-led delivery. Siemens launched Asset Performance Advanced in March 2026, integrated with the Building X platform, which points to upstream-to-downstream convergence where equipment intelligence, AI-enabled diagnostics, and managed building services sit at the center of delivery. Downstream, end users in logistics and campuses are testing automation as part of service execution, including Otto Group's May 2026 pilot of a robotic coordination layer to manage robot fleets in real time at its Lohne logistics center. Trade association guidance is also becoming a more visible input into service design, such as GEFMA's release of GEFMA 984-5 on climate adaptation in July 2026, which frames how FM organizations translate extreme-weather risks into maintenance planning, retrofits, and continuity processes.

Competitive Landscape

Private-equity ownership is reshaping the field; PAI Partners’ acquisition of Apleona brought fresh investment for digital twins and pan-European synergies. Dussmann Group surpassed EUR 3 billion (USD 3.50 billion) in sales after extending technical FM, food services, and security within bundled packages. ISS advanced consolidation by purchasing gammaRenax, adding 1,800 staff and a hospitality portfolio across Switzerland, which complements German contracts that emphasize ESG stewardship.

Technology partnerships proliferate. Siemens aligns with municipal utilities to integrate building management, renewable assets, and grid services, translating into operational savings up to 30% . Start-ups like Metr Secure Ventures with landlords seeking transparent, device-agnostic data flows. The Building Technology sector’s stable EBITDA multiples around 8.9x reflect investor conviction that automation and sustainability will unlock margin expansion. Providers that embed cybersecurity layers and real-time analytics differentiate in tender evaluations, reinforcing a capability gap between digital leaders and late adopters inside the Germany facility management market.

White-space opportunities center on outcome-based contracts tied to verified CO₂ reductions, indoor-air quality, and user-experience metrics. Tight labor supply motivates firms to deploy AI scheduling tools and VR training modules that amplify technician productivity. As large incumbents integrate ESG disclosures into annual reports and bond frameworks, smaller peers may struggle to fund comparable upgrades, furthering consolidation momentum.

Germany Facility Management Industry Leaders

-

Strabag SE

-

Bilfinger SE

-

Dussmann Group

-

Compass Group PLC

-

Wisag Facility Service Holding GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Technology-led integrated FM is moving from point solutions into unified operational backbones that combine CMMS, compliance workflows, and energy optimization across portfolios. In 2026, Planon launched a platform positioned around data center operational resilience, incorporating CMMS, compliance, and energy-related workflows, and Siemens expanded Building X with Asset Performance Advanced to operationalize predictive maintenance and more autonomous building operations.

Connectivity and regulated building automation requirements are creating additional whitespace for device-agnostic monitoring, cybersecurity-aligned operations, and OT/IT modernization services. VATM and Dialog Consults' 2026 telecoms market analysis cites 96 million M2M SIM connections in Germany by end-2026, which underlines the scale of machine connectivity available for metering, condition monitoring, and remote service dispatch across distributed assets. At the asset level, data-center and AI-compute buildouts are translating into higher-spec technical FM needs: in June 2026, SPIE started development of the 16 MW FRA7 data center in Rosbach vor der Hohe with integrated building automation, energy monitoring, and waste heat recovery, reinforcing demand for providers that can operate critical environments under strict availability, energy, and reporting requirements.

Recent Industry Developments

- July 2026: Bilfinger acquired a digital platform from Zentur.io GmbH, effective July 1, 2026, to expand its digital service portfolio for the energy sector. The transaction strengthens Bilfinger's ability to deliver software-enabled service models that overlap with technical facility management needs such as monitoring, analytics, and remote support. It also highlights the increasing role of platform capabilities in winning complex, regulated customer environments.

- June 2026: STRABAG PFS extended its technical facility management contract for the Federal Ministry of Finance (BMF) in Berlin for five years, covering 134,300 square meters. Multi-year public-sector renewals support revenue visibility and reinforce incumbent positioning in compliance-heavy, security-sensitive buildings. The scope also points to sustained demand for scaled technical FM delivery in government real estate portfolios.

- April 2026: STRABAG PFS won a technical facility management contract for German Aerospace Centre (DLR) locations in Oberpfaffenhofen and Augsburg, incorporating its eco2state service line with AI-supported maintenance. The award reflects buyer preference for data-driven maintenance and energy-oriented service concepts within technical FM. It also shows how AI-enabled workflows are being embedded into operational delivery for high-value, mission-critical sites.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, we define facility management in Germany as the paid services used to operate, maintain, and support buildings and sites across commercial, public, and industrial properties, covering day-to-day technical upkeep and people-facing services.

Scope exclusions: pure construction and major refurbishments, as well as standalone equipment sales without an ongoing service component, are not counted.

Segmentation Overview

-

By Service Type

-

Hard Services

- Asset Management

- MEP and HVAC Services

- Fire Systems and Safety

- Other Hard FM Services

-

Soft Services

- Office Support and Security

- Cleaning Services

- Catering Services

- Other Soft FM Services

-

Hard Services

-

By Offering Type

- In-house

-

Outsourced

- Single FM

- Bundled FM

- Integrated FM

-

By End-user Industry

- Commercial (IT and Telecom, Retail and Warehousing)

- Hospitality (Hotels, Eateries, Restaurants)

-

Institutional and Public Infrastructure (Govt, Education, Transport)

- Retail and Warehousing

- Healthcare (Public and Private Facilities)

- Industrial and Process (Manufacturing, Energy, Mining)

- Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the demand context and to anchor assumptions to visible signals. We relied on public sources such as Destatis for building and labor statistics, the German Federal Ministry for Economic Affairs and Climate Action for policy direction, the Federal Institute for Occupational Safety and Health for workforce indicators, and the European Commission and Eurostat for economy and inflation references.

To convert these signals into sizing inputs, we also reviewed company annual reports and investor decks, press and trade association releases (including German real estate and building operator groups), and public procurement portals for recurring service tenders. Where needed, we complemented this with paid subscriptions that compile company financials and news, and an import/export shipment level database to sanity check cost movements for selected consumables used in soft services. These sources are not exhaustive, and many other public and paid references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work was used to verify outsourcing behavior and service scope, and to pressure test the pricing and volume levers behind hard and soft services. We spoke with a mix of facility service providers, subcontractors, large property operators, and buyers across office, industrial, healthcare, and public infrastructure, so assumptions could be checked from both the supply and demand sides. Coverage was kept balanced across Germany, and follow-up outreach was triggered when desk signals and interview feedback did not match on rates, staffing, or contract structure.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 20% | |

| Mid tier: 41% | Functional/Unit leaders: 39% | |

| Smaller Players: 20% | Managers: 41% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where property stock and occupied space are converted into a spend pool using service intensity and outsourcing penetration by end user, then mapped into hard and soft service splits. The totals are subsequently cross-checked with selective bottom-up approximations, such as sampled contract values by service line, channel checks with subcontracting shares, and simple ASP x headcount logic for labor-heavy activities, which are then used to adjust outliers.

A few inputs carry most of the weight in Germany, including the mix of outsourced versus in-house delivery, wage and benefit inflation for cleaning and security roles, energy-efficiency-driven maintenance cycles tied to building upgrades, the share of integrated and bundled contracts, and occupancy trends across offices and public facilities. When a bottom-up check is missing for a niche service, we fill the gap using the closest-service ratios and then validate it through an extra round of expert calls. Forecasts are built using scenario analysis anchored to macro indicators and contract renewal patterns, with the final path selected based on what interviewees expected for staffing availability, pricing pass-through, and outsourcing appetite.

Data Validation & Update Cycle

Outputs are triangulated across independent signals, so the model is compared against visible labor trends, tender activity, and reported growth commentary from major service providers. Variance checks are run at each step, and anomalies are reviewed to confirm whether they came from one-off contracts, unusual pricing, or a temporary shift in demand. Before sign-off, another analyst reviews the logic and recalculates key steps, and then we re-contact selected interviewees when major assumptions move.

The report is refreshed once a year, and interim updates are made when material events occur, such as major policy changes, sharp wage movements, or notable shifts in outsourcing. Right before delivery, we do a final pass so clients receive the most current view supported by the latest available data.

Mordor Intelligence's Germany Facility Management Market Estimate Compared With Other Published Estimates

Published market sizes for Germany facility management can look far apart, even when they use similar words, because the underlying scope and the way spend is counted often changes by publisher. Differences usually come from what is included as facility management, whether in-house activity is valued, how integrated contracts are treated, and which year and currency conversion timing is applied.

The main gap comes from whether the number represents the full facility management spend or only the outsourced facility services turnover. Mordor Intelligence counts both in-house and outsourced delivery across hard and soft services and keeps the split consistent by end user. Another driver is pricing, since some estimates lean on headline inflation or wage indices without checking if pass-through is capped in multi-year contracts. Finally, refresh cadence matters, since rapid labor cost changes can shift soft services values quickly if the assumptions are not revalidated with recent buyer and provider feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 90.96 B (2025) | |

| Industry Association A | USD 75.20 B (2024) | Represents outsourced facility services turnover for a defined company set, which can exclude in-house delivery and understate hard services performed within large owner-operators. |

| Trade Journal B | USD 98.50 B (2025) | Uses broader real estate operations spend and applies generalized price escalation, which can over-count adjacent property services and miss contract-level caps and renegotiation timing. |

The spread in the table largely traces back to scope and how service spend is assigned, rather than to a single math error. By keeping the service basket tied to repeatable demand drivers (occupied space, service intensity, outsourcing share, and wage-led pricing) and then validating it with buyer and provider checks, we end up with a value that is easier to reconcile across years and easier to defend on a client call.

Key Questions Answered in the Report

What is the current value of the Germany facility management market?

The Germany facility management market size stands at USD 93.87 billion in 2026 and is expected to rise to USD 109.86 billion by 2031.

Which service type holds the largest share?

Hard Services lead with 56.62% of 2025 revenue, underpinned by mandatory energy-efficiency upgrades and technical infrastructure needs.

Why is outsourcing growing in Germany’s facility management sector?

Outsourcing expands at a 3.97% CAGR because escalating regulatory complexity and skilled-labor shortages push owners toward integrated service partners.

Which end-user group is expanding the fastest?

Institutional and public infrastructure assets, including healthcare and education, show the highest growth at a projected 5.11% CAGR through 2031.

Page last updated on: