Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

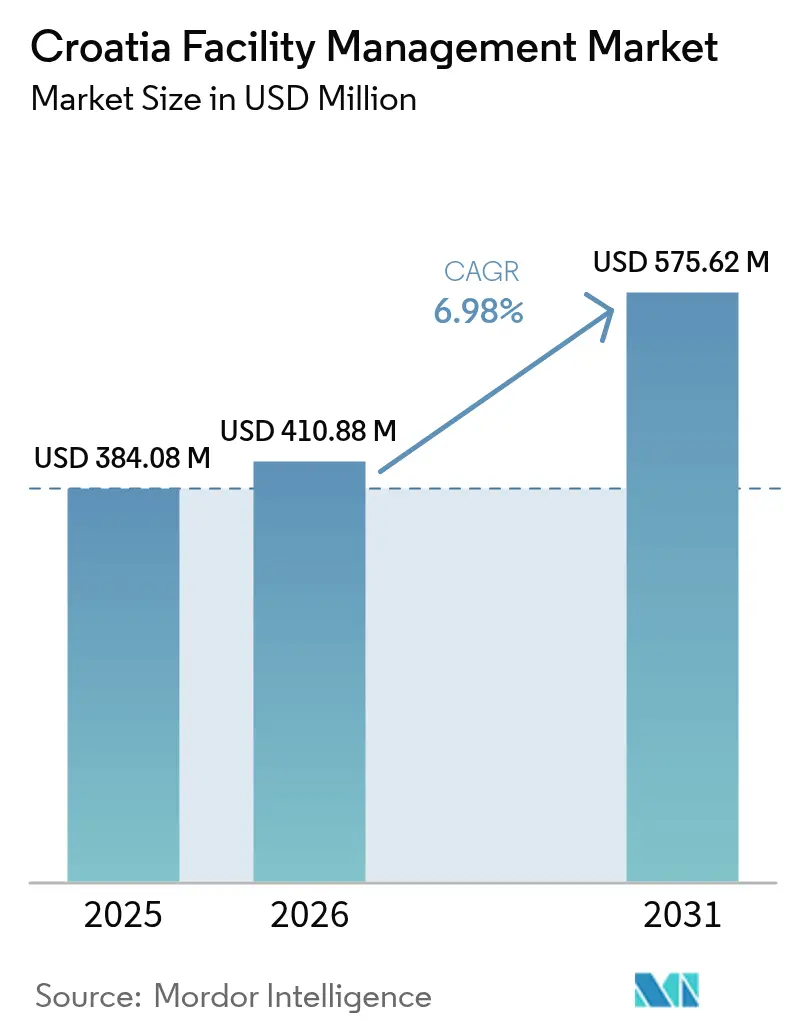

| Base Year Market Size (2025) | USD 384.08 Million |

| Market Size (2026) | USD 410.88 Million |

| Market Size (2031) | USD 575.62 Million |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

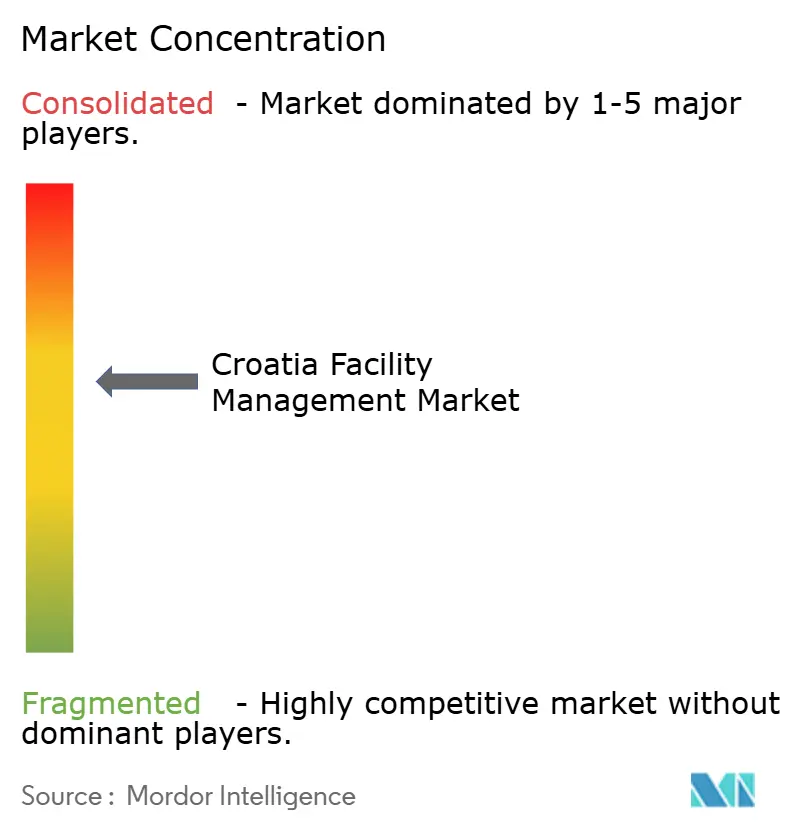

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Croatia Facility Management Market Analysis by Mordor Intelligence

The Croatia facility management market size was valued at USD 384.08 million in 2025 and estimated to grow from USD 410.88 million in 2026 to reach USD 575.62 million by 2031, at a CAGR of 6.98% during the forecast period (2026-2031). Mandatory energy-performance retrofitting, the euro’s adoption, and rising cross-border investment have raised the baseline for building-performance standards. Larger tenants now insist on outcome-based contracts that link vendor fees to energy, safety, and service-quality metrics, encouraging owners to outsource specialist tasks and accelerating digital-tool deployment.[1]European Investment Bank, “Croatia’s Investment Momentum Remains Strong in 2024,” eib.org Public-sector recovery-plan grants earmarked EUR 789 million (USD 891 million) for renovations, ensuring a multi-year pipeline of hard-service projects that include HVAC upgrades, fire-safety retrofits, and smart-meter rollouts. At the same time, tourism’s rebound and hotel pipeline expansion have fueled demand for hospitality-grade cleaning, security, and guest-technology support. Cost pressures from volatile VAT and property-tax reforms are pushing providers to adopt IoT-enabled maintenance tools that cut unplanned downtime and secure margin stability.

Key Report Takeaways

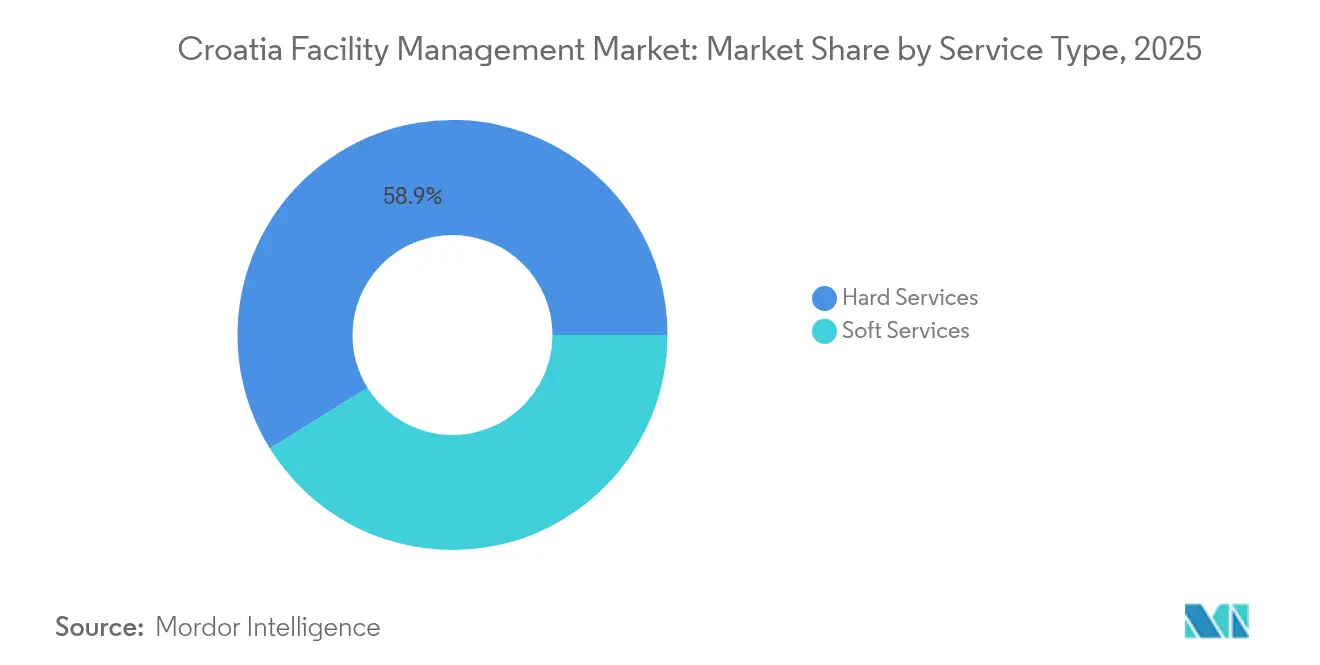

- By service type, hard services held 58.85% of Croatia's facility management market share in 2025, whereas soft services are projected to expand at an 8.27% CAGR through 2031.

- By offering type, the outsourced model commanded 62.05% share of the Croatia facility management market size in 2025 and is forecast to register a 7.7% CAGR to 2031.

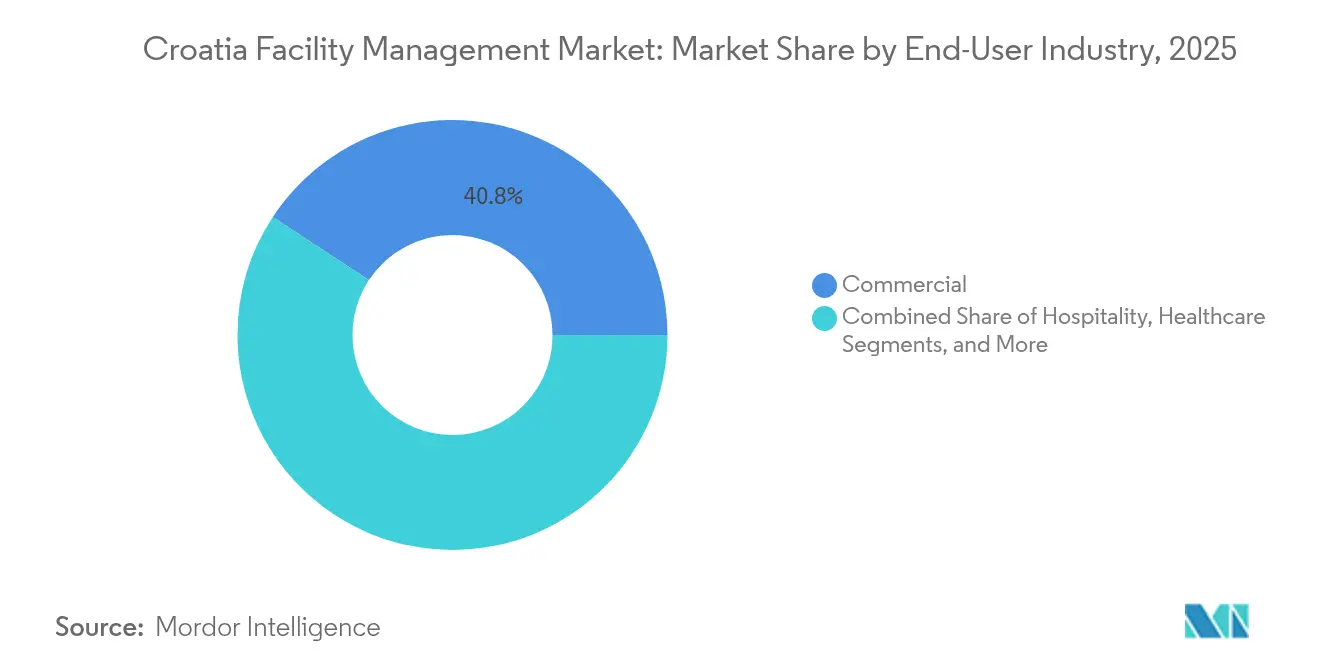

- By end-user industry, commercial facilities contributed 40.75% revenue in 2025; institutional and public infrastructure is the fastest-growing segment, advancing at a 7.56% CAGR during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Croatia Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of commercial real estate and mixed-use developments | +1.2% | National, with a concentration in Zagreb, Split, and coastal tourist areas | Medium term (2-4 years) |

| Growth of the tourism and hospitality sector boosts FM demand | +1.5% | Coastal regions, Zagreb, and major tourist destinations | Short term (≤ 2 years) |

| Increasing adoption of integrated FM contracts by the public sector | +0.9% | National, with early adoption in the Zagreb and Split municipalities | Medium term (2-4 years) |

| Mandatory energy-performance retrofitting under updated EU directives | +1.8% | National, with a priority focus on public buildings and commercial properties | Long term (≥ 4 years) |

| Nearshoring-driven rise of specialized R&D hubs requiring tailored FM services | +0.7% | Zagreb, Split, and emerging technology corridors | Long term (≥ 4 years) |

| Smart-city PPP pilots in Zagreb and Split, embedding FM platforms | +0.4% | Zagreb and Split metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Commercial Real Estate and Mixed-Use Developments

Property prices in Croatia rose about 10% year-on-year in 2025, outpacing many EU peers and encouraging developers to launch multi-tower projects around Zagreb’s City Island and Split’s waterfront. Foreign investors accounted for 37.5% of transactions, bringing international lease standards that require ISO-aligned maintenance logs and 24-hour equipment uptime. Facility managers with predictive-maintenance platforms tend to win tenders by promising faster fault resolution, lower energy use, and transparent KPI dashboards. Concentrated building activity in the two largest cities gave vendors critical mass, letting them pool specialist technicians and negotiate bulk pricing on sensors and spare parts, which in turn lifted profitability.

Growth of Tourism and Hospitality Sector Boosting FM Demand

International arrivals from Germany, Poland, France, and the USA surged through summer 2025, returning Adriatic occupancy close to record highs. Global hotel brands accelerated flag rollouts: Hyatt opened the 133-room Hyatt Regency Zadar, while Accor debuted the 193-room Pullman Zagreb, both in May 2025. These assets require round-the-clock HVAC tuning, food-safety protocols, and guest-tech support that meet brand audit criteria. Domestic operator Valamar completed a nationwide deployment of Flexkeeping’s AI-driven housekeeping engine in July 2025, cutting response times and elevating guest-satisfaction scores. Such benchmarks are compelling smaller hotels and marinas to outsource soft services to vendors that can guarantee similar performance.

Increasing Adoption of Integrated FM Contracts by Public Sector

Recovery and Resilience Facility funds prompted ministries and municipalities to bundle cleaning, security, and technical tasks under single, multi-year agreements. The Čakovec administrative building retrofit, finished in March 2025, delivered 80% electricity and 56% gas savings after deploying a unified energy management platform. Zagreb’s EUR 9.3 million “Bajs” bike-sharing network embeds predictive maintenance obligations in its concession, making uptime a payment trigger. Vendors capable of real-time monitoring and compliance reporting now win a growing share of public bids.

Mandatory Energy-Performance Retrofitting Under Updated EU Directives

EU directives earmarked EUR 789 million (USD 891 million) for Croatian renovations, obliging owners to install smart meters, rooftop solar, and advanced HVAC systems. The Čakovec project showcased pyrolysis wood furnaces and solar collectors integrated with IoT sensors, underscoring the multi-disciplinary skills hard-service firms must supply. Ten-year payback horizons encourage owners to sign bundled design-build-operate contracts, ensuring steady fee streams for qualified vendors over the asset life.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| A fragmented supplier base is limiting standardization and scalability | -0.8% | National, with particular challenges in smaller cities and rural areas | Medium term (2-4 years) |

| Low technology maturity among local FM SMEs is hindering digital ROI | -1.1% | National, with concentration among smaller regional providers | Short term (≤ 2 years) |

| Price-driven tendering culture suppressing service quality and margins | -0.6% | National, particularly affecting public sector contracts | Medium term (2-4 years) |

| Volatile VAT and municipal tax regimes are increasing cost uncertainty | -0.9% | National, with varying impact based on municipal policies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Supplier Base Limiting Standardization and Scalability

More than 70% of facility-management entities employ under 50 staff, according to the 2024 construction collective agreement.[2]Narodne Novine, “Kolektivni Ugovor za Graditeljstvo,” narodne-novine.nn.hr Limited scale hampers investment in CAFM software, certified training, and ESG reporting. Service quality, therefore, varies widely outside Zagreb and Split, where many micro-firms rely on manual checklists and reactive maintenance. Corporate occupiers struggle to extend standardized procedures across multi-city portfolios, slowing national rollouts of smart-building practices.

Low Technology Maturity Among Local FM SMEs Hindering Digital ROI

Statutory minimum wages and a 42-hour workweek consume most operating budgets, leaving scant capital for sensors or analytics. Even where IoT pilots launch, data seldom translates into preventive-maintenance savings because smaller providers lack analytics staff. Global contractors, conversely, link occupancy sensors with automated work-orders, reducing average fault-response time by over 25% on embassy and hotel portfolios. This digital divide has produced a two-tier market in which technology leaders secure long-term integrated contracts, while laggards compete mainly on price for short-cycle tasks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Compliance Excellence

Hard services accounted for 58.85% of 2025 revenue as owners raced to meet EU retrofit deadlines and align with corporate ESG targets. Assets entering operation in 2025 contained smart meters, BMS interfaces, and low-carbon fire-suppression systems; maintaining these components requires multi-disciplinary engineers certified in energy management as portfolio-wide energy dashboards become audit staples, hard-service vendors that can verify kilowatt-hour reductions secure bonus payments and contract renewals, expanding the Croatia facility management market.

Soft services, while smaller in value, are forecast to grow at an 8.27% CAGR through 2031 on the back of tourism expansion and rising workplace-experience standards. Hotels are embedding robotics for corridor vacuuming, while corporate offices roll out antimicrobial protocols and sensor-based washroom restocking. Vendors able to merge cleaning, concierge, and security under a single KPI increase stickiness within mixed-use campuses that integrate retail, office, and residential tenants around Zagreb’s central business zone.

By Offering Type: Outsourcing Accelerates Market Consolidation

Outsourced delivery models controlled 62.05% of Croatia's facility management market share in 2025, reflecting owner preference for lean balance sheets and transparent cost benchmarks. Multi-service and fully integrated FM agreements, often spanning five years or more, now dominate public-sector tenders. These contracts transfer energy-performance risk to vendors, who deploy IoT sensors and building analytics to safeguard margins. The resulting data troves let providers benchmark asset uptime and negotiate dynamic pricing.

In-house teams persist in heavy-industry and defense-related facilities that require security clearances and proprietary know-how. Yet rising labor costs—cemented by the 2024 collective agreement—are nudging even these owners to carve out non-core tasks such as landscaping or cafeteria operations. Bundled and single-service outsourcing options therefore serve as transitional models, smoothing the shift toward fully integrated contracts as owners build trust in performance-based frameworks.

By End-User Industry: Commercial Leadership Faces Institutional Challenge

Commercial estates delivered 40.75% of revenue in 2025, buoyed by multinational tenants establishing near-shoring R&D labs. Grade-A offices in Zagreb advertise WELL and BREEAM plaques, compelling facility managers to maintain indoor-air-quality dashboards and wellness amenities. Retail parks and logistics hubs likewise rely on IoT lighting and predictive asset management to contain utility costs, reinforcing the case for outsourcing to tech-savvy providers. The Croatia facility management market size for commercial stock is therefore positioned for steady expansion as new mixed-use districts come online.

Institutional and public-infrastructure assets, though smaller today, represent the fastest-growing segment at a 7.56% CAGR. Schools, hospitals, and municipal offices tapped Recovery-Facility grants to fund deep renovations that demand long-term O&M oversight tied to energy and safety metrics. Vendors with heritage-property expertise are also winning libraries and museum contracts that couple preservation requirements with modern climate-control standards.

Geography Analysis

Zagreb retained the largest regional share in 2025 thanks to its role as the capital, headquarters hub, and test-bed for smart-city pilots such as the “Bajs” bike-sharing network. Commercial towers around Novi Zagreb rely on cloud-based CAFM systems that integrate lift telemetry, fire-panel alerts, and air-quality sensors. Such complexity favors multi-disciplinary vendors capable of providing 24-hour help-desk support.

Split ranked second, propelled by tourism and an emerging tech cluster. Urban-climate modeling published in April 2025 highlighted rising heat-island stress, driving demand for reflective roofs, adaptive shading, and intelligent cooling set-points managed by facility teams. Waterfront revamps bundle marina, retail, and condo spaces, which in turn require integrated security and guest-services staffing across peak seasons.

Coastal counties in Istria and Dalmatia formed the highest-growth corridor. Land prices appreciated 10–13% annually through early 2025, reinforcing the need for energy-efficient operations that shield occupancy costs. Hotels, campsites, and marinas increasingly adopt smart-sensor mooring and e-booking platforms, pushing facility managers into hybrid IT-engineering roles. On islands, seasonal load swings compel flexible staffing models in which vendors ramp labor pools each summer and scale back during winter, a niche only a handful of providers have mastered so far.

Competitive Landscape

Global groups—CBRE, Atalian Global Services, and Savills—leveraged regional hubs to secure embassy, hotel, and multinational portfolios, offering tenants unified reporting dashboards across Central Europe. Domestic leaders such as BFM d.o.o, PRS-FM d.o.o., and Apleona HSG d.o.o. relied on local-knowledge advantages, tight labor networks, and Croatian-language help desks to protect municipal and healthcare accounts. Collectively, the five largest firms controlled a majority of nationwide turnover, signaling moderate concentration.

Technology capability became the prime differentiator during 2024-2025. Flexkeeping’s AI housekeeping engine, deployed across Valamar’s chain in July 2025, automated task dispatch and delivered real-time guest-room status, setting a new benchmark.[4]Hospitality Net, “Flexkeeping Elevates Guest Personalization at Valamar,” hospitalitynet.org CBRE acquired a Zagreb-based MEP contractor to deepen hard-service depth, while Atalian formed a joint venture with an energy-services firm to bid on deep-retrofit packages. Workforce shortages remained acute; leading vendors funded vocational courses with trade schools to lift apprenticeship intake and comply with collective-agreement wage ladders.

M&A prospects are rising as small family-owned firms confront succession gaps and mounting digital-investment needs. Buyers value firms holding ISO 14001 and ISO 45001 certificates, given public-sector bids now award points for environmental and occupational-health credentials. Successful integrations will depend on harmonizing pay scales and migrating disparate work-order platforms onto single CAFM backbones, a process global acquirers can fund through scale synergies.

Croatia Facility Management Industry Leaders

Atalian Global Services

Apleona HSG d.o.o.

BFM d.o.o

CBRE Group, Inc

Asura Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Flexkeeping completed the nationwide rollout of its Automated Services engine across Valamar’s hotel portfolio, boosting housekeeping productivity through AI-driven task allocation.

- May 2025: Hyatt opened the 133-room Hyatt Regency Zadar, its first Croatian property, incorporating advanced BMS and energy-recovery ventilation.

- May 2025: Zagreb City Council signed a EUR 9.3 million (USD 10.5 million) contract for the “Bajs” bike-sharing network, embedding predictive maintenance clauses.

- March 2025: Croatia’s property-tax reform introduced rates from 3% on permanent residences to 5% on commercial assets, prompting landlords to seek professional FM cost-optimization.

Croatia Facility Management Market Report Scope

The study tracks the facility management (FM) industry-related trends in Croatia by analyzing the industry turnover accrued through end-user contracts by the service providers.

The Croatia facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What growth rate is expected for the Croatia facility management market between 2026 and 2031?

The market is projected to grow at a 6.98% CAGR, rising from USD 410.88 million in 2026 to USD 575.62 million in 2031.

Which service category leads Croatian facility management revenues today?

Hard services, including asset maintenance and energy systems, held a 58.85% share in 2025, reflecting strict EU retrofit mandates.

Why are outsourced contracts expanding faster than in-house delivery?

Owners prefer outsourced models for cost transparency and access to specialized skills, driving a 7.7% CAGR for outsourced services.

How do EU energy rules affect facility-management demand?

Recast directives allocated EUR 789 million for Croatian retrofits, increasing demand for vendors certified in energy-efficient building operations.

Which end-user sector shows the fastest growth through 2031?

Institutional and public-infrastructure facilities are set to expand at a 7.56% CAGR as government grants fund deep renovations.

What technologies are redefining facility management in Croatia?

IoT sensors, AI-driven housekeeping, and ESG compliance dashboards are helping leading providers cut downtime and meet stricter reporting standards.

Page last updated on: