Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 73.31 Billion |

| Market Size (2026) | USD 75.09 Billion |

| Market Size (2031) | USD 84.67 Billion |

| Growth Rate (2026 - 2031) | 2.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Facility Management Market Analysis by Mordor Intelligence

The France facility management market size was valued at USD 73.31 billion in 2025 and is estimated to grow from USD 75.09 billion in 2026 to reach USD 84.67 billion by 2031, at a CAGR of 2.43% during the forecast period (2026-2031). Demand is shifting toward bundled and integrated contracts as the Tertiary Decree’s 40% energy-reduction mandate, the 2026 Energy Performance Certificate (EPC) enforcement, and the Building Automation and Control Systems Decree reshape compliance obligations. Persistent labor shortages, especially for HVAC and multi-technical trades, are accelerating investment in IoT sensors, predictive maintenance, and digital dashboards that let providers deliver more output with fewer technicians. Price pressure is easing as inflation moderates, yet fixed-price contracts must now factor in future carbon costs ahead of the EU ETS2 launch in 2027. Consolidation is evident after ONET acquired ISS France operations in 2024, while global players such as Sodexo, VINCI Facilities, and Veolia leverage scale, self-delivery, and data analytics to guard margins in the France facility management market.

Key Report Takeaways

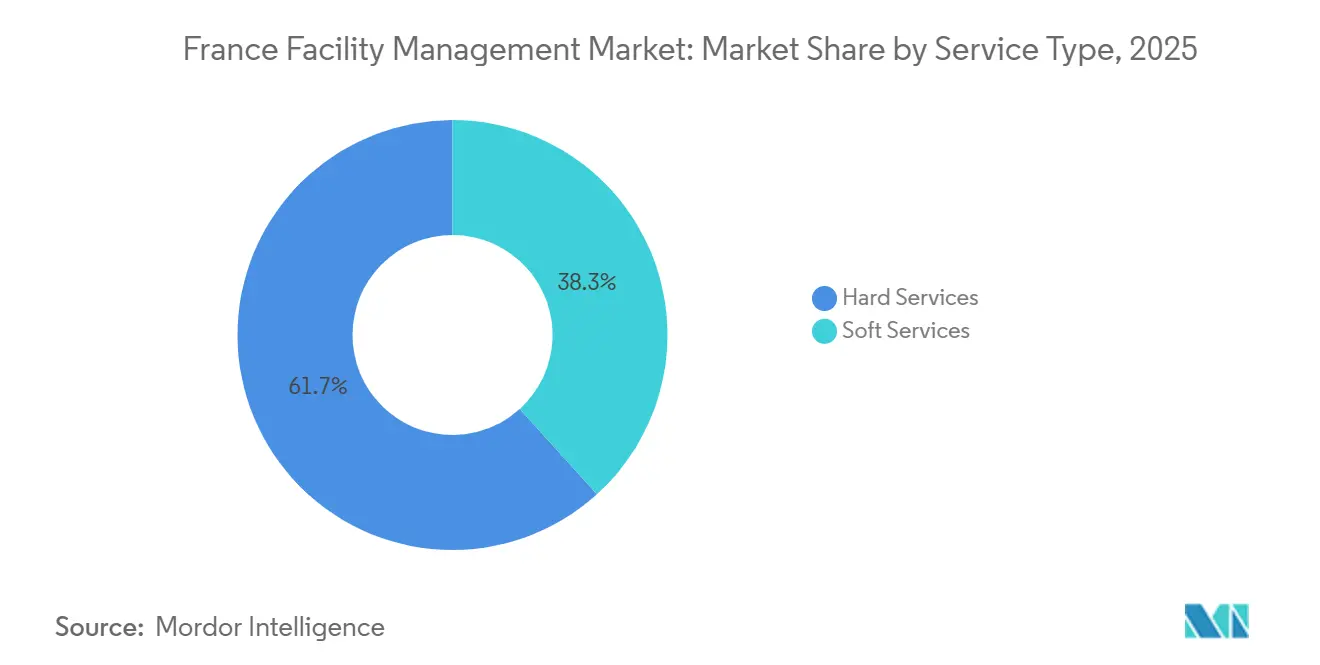

- By service type, hard services led with 61.73% of France facility management market share in 2025. Soft services are forecast to advance at a 2.57% CAGR through 2031.

- By offering type, in-house models retained 66.59% share in 2025; outsourced integrated facility management is projected to expand at a 2.82% CAGR over 2026-2031.

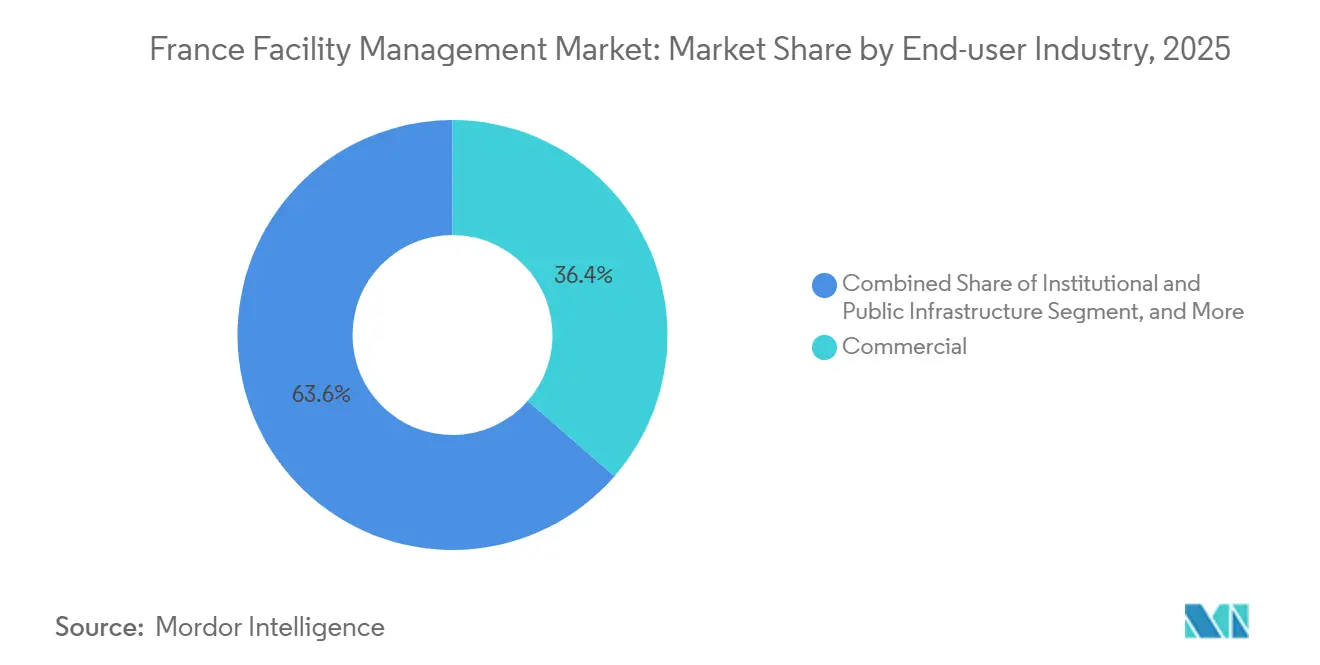

- By end-user, commercial real estate held a 36.42% share of the France facility management market size in 2025 and is poised to grow at a 2.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological Advancements in Building Management Systems | +0.6% | Paris, Lyon, Marseille, Lille, Toulouse metro areas | Medium term (2-4 years) |

| Mandated Energy Performance Certificates Enforcement from 2026 | +0.5% | National, stricter in Île-de-France | Short term (≤ 2 years) |

| Growth of the Real Estate Sector | +0.4% | Paris, Lyon, Marseille, secondary cities | Medium term (2-4 years) |

| Increasing Emphasis on Green Building Practices | +0.3% | National, led by HQE projects | Long term (≥ 4 years) |

| Post-Pandemic Hybrid Work Models Driving Flex-Space Servicing | +0.3% | Major commercial hubs | Short term (≤ 2 years) |

| Rising Adoption of Integrated FM Contracts | +0.2% | National multi-site portfolios | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Building Management Systems

The BACS Decree requires automation in all non-residential buildings over 290 kW by 2025 and 70 kW by 2027, forcing owners to add IoT sensors, real-time energy tracking, and anomaly detection platforms.[1]Christophe Marvillet, “Applying the BACS Decree to Commercial and Industrial Buildings,” Techniques de l'Ingénieur, techniques-ingenieur.fr Providers deploy cloud analytics that merge HVAC, lighting, and water data into unified dashboards. Eiffage’s AI engine lowered prediction error on a high-speed rail network to 4% for one-month horizons, showing predictive maintenance is maturing. Orange Business Services and Sensinov have documented 30-48% energy savings in pilots that couple LoRaWAN devices with centralized controls. These outcomes help the France facility management market satisfy performance guarantees despite labor gaps.

Growth of the Real Estate Sector

Paris office vacancy hit 8.1% in Q3 2024, yet flexible office take-up jumped 15%, creating a two-speed landscape. Traditional landlords focus on cost-cutting and ESG retrofits, while coworking operators require daily service adjustments triggered by occupancy sensors. Government portfolios, 90 million m² managed by France Domaine, face the same 60% reduction mandate, lining up long-duration retrofit contracts. Capital is selective: investment volumes fell 19% year-on-year to EUR 7.8 billion (USD 8.35 billion) in 2024, rewarding assets that already embed smart FM tools.[2]CBRE Research, “EMEA Flexible Office Market Report 2024,” cbre.com

Increasing Emphasis on Green Building Practices

HQE certification now covers more than 1,000 buildings, and RE2020 carbon caps tighten again in 2025, 2028, and 2031.[3]Alliance HQE-GBC, “HQE Certification,” hqe-gbc.org Energy performance contracts offered by Equans and Bouygues Énergies et Services tie provider fees to verified consumption cuts. The requirement to justify target modulation through energy studies opens advisory revenue for audits and payback analysis. As lifecycle carbon metrics become bid qualifiers, digital twins and embodied-carbon dashboards differentiate bids in the France facility management market.

Mandated Energy Performance Certificates Enforcement from 2026

France tightened EPC rules in 2025, adding QR codes for instant audits and escalating fines up to EUR 7,500 (USD 8,025) per legal entity. Owners must report consumption on the OPERAT portal and hit 40% savings by 2030 or meet absolute targets set by the Tertiary Decree.[4]France Stratégie, “Jobs and Skills Needs for 2030: Energy Efficiency Renovation of Buildings,” strategie.gouv.fr Hotels will post A-to-E environmental grades from 2026, broadening demand for carbon accounting, data normalization, and supplier screening. Facility managers that bundle energy studies, retrofits, and performance monitoring gain a compliance premium in the France facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Market Constraints and Skills Shortage | -0.4% | Île-de-France, Lyon, Marseille | Long term (≥ 4 years) |

| Economic Fluctuations and Inflationary Pressures | -0.3% | National, construction exposed | Medium term (2-4 years) |

| High Market Fragmentation Limiting Economies of Scale | -0.2% | Cleaning and single-service segments | Long term (≥ 4 years) |

| Imminent Carbon-Tax Pass-Through Risks on FM Contract Margins | -0.2% | Energy-intensive facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labor Market Constraints and Skills Shortage

France Stratégie estimates 170,000-250,000 additional workers are needed by 2030 to meet renovation goals INSEE found 27% of construction firms lacked labor in October 2025, hampering envelope upgrades. Cleaning jobs face high turnover, with an average worker age of 43 and widespread musculoskeletal issues. Providers are responding with robotics, route-optimization apps, and cross-training into catering or logistics, yet persistent scarcity raises wage costs and strains France facility management market profitability.

Economic Fluctuations and Inflationary Pressures

Construction contracted 3.9% in 2024 and order books sank to -33 in November 2025, the weakest since 2016. IPEA climbed to 118.0 in Q3 2025, led by HVAC sub-indices above 122, while labor costs rose with each minimum-wage revision. Clients hesitate to fund retrofits amid weak demand, pushing providers to absorb cost increases or risk non-renewal. Banque de France’s January 2026 survey shows near-term construction activity still negative, signaling a slow pipeline for new FM contracts .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Retain Lead as Soft Services Accelerate

Hard services captured 61.73% of the France facility management market in 2025, anchored by multi-technical maintenance, MEP compliance, and the BACS-driven retrofit surge. Providers such as SPIE Facilities and Equans manage nationwide agency networks that embed predictive analytics into HVAC and electrical upkeep. AI models cut reactive interventions by flagging drift in vibration or temperature data a month in advance, protecting uptime on aging assets. Fire-safety testing has intensified under ERP and IGH rules, adding steady audit revenue.

Soft services are projected to grow at a 2.57% CAGR, lifted by hybrid work patterns that require occupancy-based cleaning, variable catering, and modular security. The cleaning sector generated EUR 21 billion (USD 22.47 billion) in 2025 across 15,000 companies, yet 85% employ fewer than 50 staff, limiting technology adoption. Environmental labeling in hotels from 2026 pushes catering firms to source organic menus, while security specialists expand into remote monitoring that integrates with building IoT stacks. These shifts expand wallet share for providers that can bridge hard and soft scopes within the France facility management market size.

By Offering Type: Outsourcing Momentum Builds on Compliance Complexity

In-house delivery still held 66.59% share in 2025, especially inside public hospitals and heavy-industry campuses where institutional knowledge of process utilities is critical. Yet huge backlogs, EUR 25 billion (USD 26.75 billion) in hospitals alone, require capital and expertise unavailable internally, nudging administrators toward mixed models that pair internal clinical engineering with outsourced energy contracts .

Outsourced solutions will rise at a 2.82% CAGR as single-service contracts consolidate into bundled and integrated facility management formats. Atalian’s 85% self-delivery and eight-year average tenures show how embedded digital cockpits and energy dashboards lock in clients.[5]Atalian Group, “Annual Results 2024,” atalian.com The World Bank’s Paris office tender, which demanded USD 60 million in provider revenue, underlines how bid thresholds now screen out small specialists. Performance-based fee structures tied to EPC targets shield margins once carbon pricing advances, accelerating the shift toward integrated models within the France facility management market.

By End-User Industry: Commercial Real Estate Dominates, Healthcare Faces Backlog

Commercial buildings commanded 36.42% of France facility management market share in 2025 and should grow at 2.48% CAGR as landlords retrofit space to win ESG-minded tenants. Flexible office demand climbed 15% in 2024, prompting operators to deploy real-time cleaning dispatch and sensor-linked catering. Retail portfolios turn to centralized BMS platforms, Sensinov reports up to 48% energy savings in 350 stores, to manage refrigeration loads.

Healthcare facilities confront a EUR 25 billion (USD 26.75 billion) maintenance gap plus stricter infection-control and fire-safety rules. The Ségur de la Santé program allocates EUR 19 billion (USD 20.33 billion) for upgrades but still leaves room for energy-performance contracts that wrap HVAC modernization with guaranteed savings. Industrial sites adopt AI-enabled predictive maintenance to cut downtime that can erase 11% of turnover, as Orange’s digital twin pilot illustrates. Outcome-based contracts that tie fees to uptime and kilowatt-hour reductions are spreading through these capital-intensive sectors of the France facility management market share.

Geography Analysis

Île-de-France remains the epicenter of the France facility management market. Paris posted 8.1% office vacancy in 2024, yet La Défense still generates large retrofit projects aimed at EPC compliance. Government real-estate holdings cluster in the region, and a 25-year concession to run the district-heating network from 2027 underscores the pipeline for long-run multi-technical contracts.

Regional hubs such as Lyon and Marseille host heavy manufacturing clients. Veolia’s preventive-maintenance pact with Renault Trucks in Lyon covers HVAC, water loops, and high-voltage systems, showcasing integrated models beyond the capital. Lille and Toulouse face similar aging-stock challenges; rising enforcement of EPC rules pulls in digital audits and phased retrofit scopes to hit the 2030 40% energy-cut mandate.

Secondary towns and rural communes show lower outsourcing penetration, with many schools and municipal buildings still self-managed. Yet France Stratégie forecasts up to 250,000 extra renovation jobs by 2030, and its reindustrialization scenario adds as many as 740,000 industrial positions, spreading demand to new geographies. Providers able to mobilize mobile teams and remote monitoring tech will capture these dispersed opportunities in the France facility management market size.

Competitive Landscape

The top 10 cleaning firms control 43% of revenue, signaling moderate concentration, while the long tail of 12,000 micro-companies keeps price competition fierce. ONET’s 2024 takeover of ISS France expanded its footprint and client roster, reflecting a consolidation trend. Atalian, backed by private equity, recorded EUR 2.011 billion (USD 2.24 billion) revenue in 2024 with 71% from France and 44,000 staff, and leverages its ERGELIS energy platform to deliver 14-45% savings depending on asset class.

VINCI Facilities, Eiffage, and Bouygues Énergies et Services use construction heritage to cross-sell multi-technical maintenance and EPC-linked retrofits. Eiffage’s AI algorithm for rail assets demonstrates deep data science capability, giving it an edge in outcome-based bids. Veolia wraps FM into broader water, waste, and energy services, winning industrial portfolios like PSA Group sites through single-provider utility management.

Mid-tier contenders such as Seris Group, Samsic Facility, and DEF Network focus on retail or hospitality niches and adopt SaaS BMS solutions from Sensinov to stay competitive without heavy capex. Technology vendors thus act as force multipliers, enabling smaller firms to enter integrated contracts and widening competitive intensity across the France facility management market.

France Facility Management Industry Leaders

Sodexo Group

VINCI Facilities

Atalian Group

L'Agence du Panier

AItenders

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: VINCI Facilities won a EUR 237 million (USD 253.6 million) multi-technical contract for the Romainville-Bobigny waste-to-energy plant, reinforcing its circular-economy positioning.

- December 2025: Paris approved the Dalkia-Eiffage-RATP Solutions Ville consortium for a 25-year district-heating concession starting Jan 2027.

- November 2025: Eiffage Énergie Systèmes launched an AI predictive-maintenance tool for railway infrastructure, reporting 4% one-month prediction error.

- May 2025: Sodexo’s Entegra purchased Agap'pro to deepen French food-procurement reach for catering contracts.

France Facility Management Market Report Scope

Facility management encompasses multiple disciplines to ensure the functionality of the built environment by integrating people, places, processes, and technology. Also, facility management is the coordination of a facility's operations to make the organization more effective at what it does. Facility management is applied in various industry verticals like retail, education, and healthcare, among others, as per the needs of the business.

The France Facility Management Market Report is Segmented by Service Type (Hard Services [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Services [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), Offering Type (In-house, and Outsourced [Single Facility Management, Bundled Facility Management, and Integrated Facility Management]), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-house | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-user Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-house | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-user Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the projected value of the France facility management market in 2031?

It is forecast to reach USD 84.67 billion by 2031, growing at a 2.43% CAGR from 2026.

Which service category is expanding fastest?

Soft services, including cleaning, catering, and security, are expected to post a 2.57% CAGR over 2026-2031.

Why are integrated facility management contracts gaining traction?

Owners seek single-point accountability for meeting the Tertiary Decree's energy-cut targets and for handling complex compliance reporting.

How does the labor shortage affect providers?

Scarcity of skilled HVAC and multi-technical workers raises wage costs and pushes firms to adopt IoT automation and robotics to maintain service levels.

Which region drives the highest demand?

Île-de-France generates the largest concentration of projects thanks to dense commercial stock, government estates, and large infrastructure concessions.

What risks do fixed-price FM contracts face from 2027?

The EU ETS2 will add carbon costs to building operations, so providers are embedding pass-through clauses or switching to performance-based fee structures.

Page last updated on: