Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

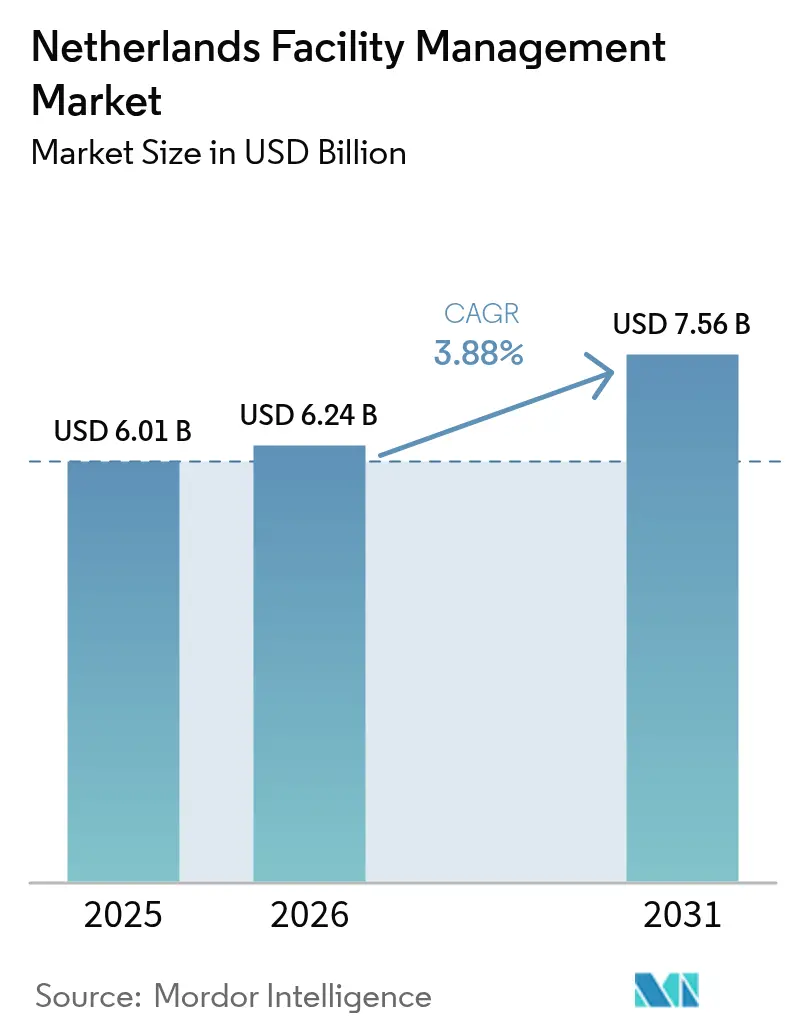

| Base Year Market Size (2025) | USD 6.01 Billion |

| Market Size (2026) | USD 6.24 Billion |

| Market Size (2031) | USD 7.56 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

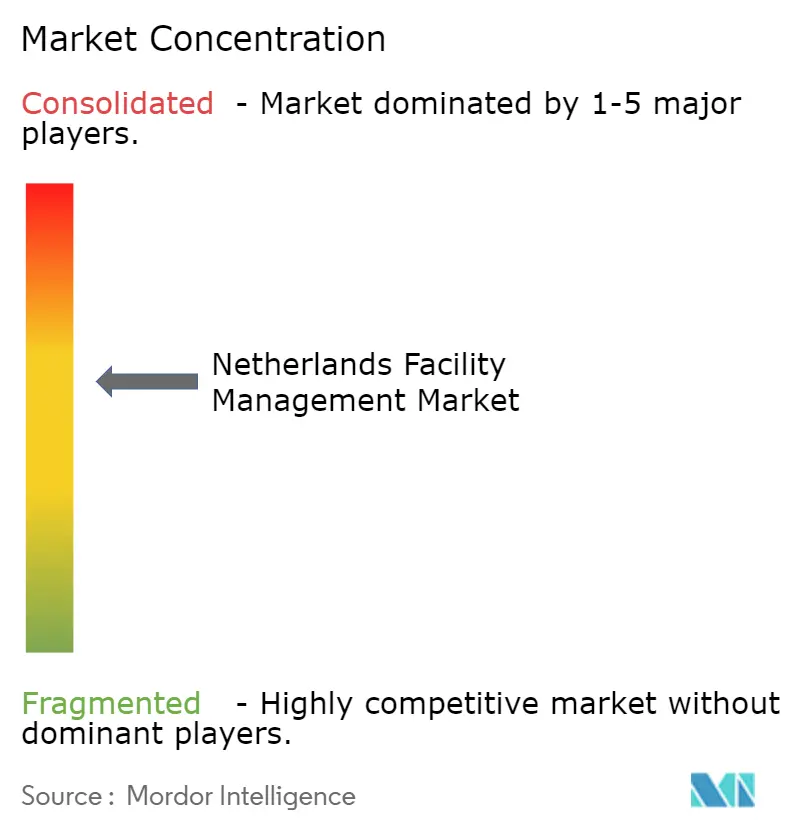

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Facility Management Market Analysis by Mordor Intelligence

The Netherlands facility management market size was valued at USD 6.01 billion in 2025 and estimated to grow from USD 6.24 billion in 2026 to reach USD 7.56 billion by 2031, at a CAGR of 3.88% during the forecast period (2026-2031). This trajectory signals a mature yet steadily expanding arena where decarbonization mandates, digital building platforms, and hybrid working patterns combine to generate recurrent demand. Spending shifts toward outcome-based contracts, together with the 2025 launch of the Corporate Sustainability Reporting Directive (CSRD), are encouraging firms to procure integrated solutions that document Scope 1-3 emissions and verify energy-efficiency paybacks. Providers able to embed IoT sensors, AI analytics, and digital-twin oversight into core hard-service routines are capturing share as asset owners target operating-cost reductions and BREEAM-NL certification premiums. Inflationary pressure on wages and materials is simultaneously nudging clients to outsource non-core activities, pushing the outsourced slice of the Netherlands facility management market past two-thirds of overall revenues. Competitive intensity remains moderate; multinationals leverage scale while regional specialists win on local labor networks and project agility.

Key Report Takeaways

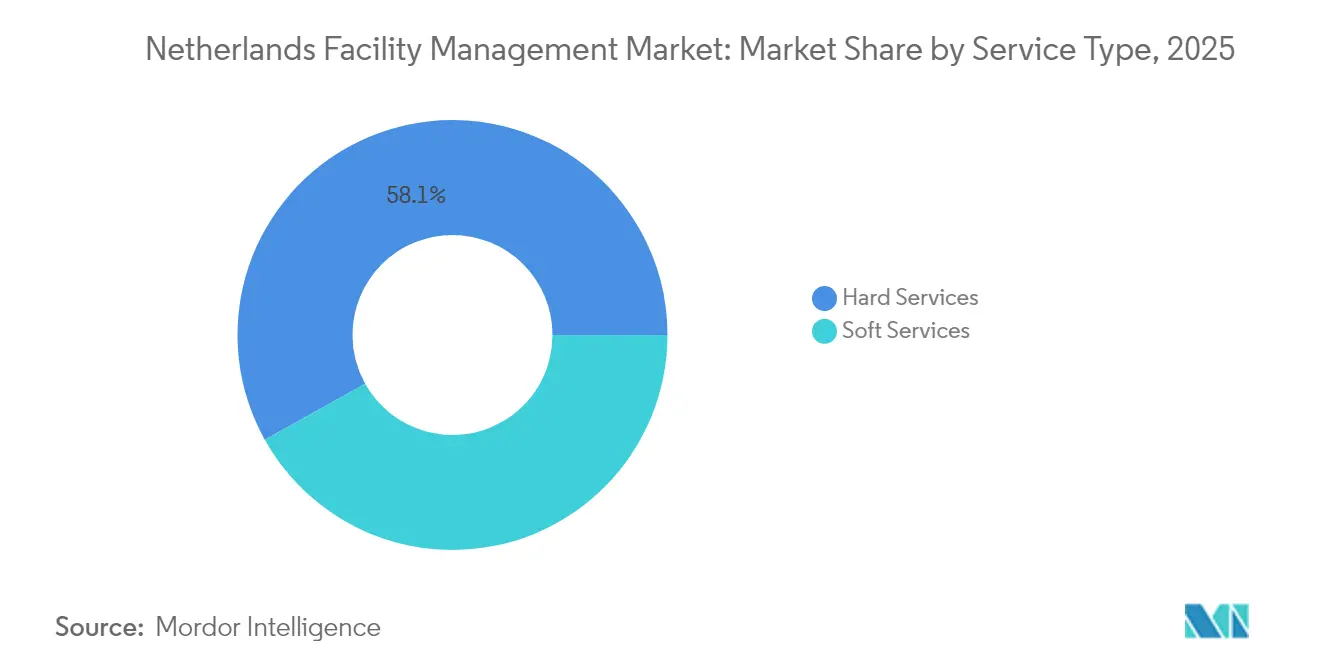

- By service type, hard services led with 58.10% of Netherlands facility management market share in 2025 while soft services are advancing at a 4.02% CAGR through 2031.

- By offering, the outsourced model accounted for 65.35% of the Netherlands facility management market size in 2025 and is projected to post a 3.92% CAGR to 2031.

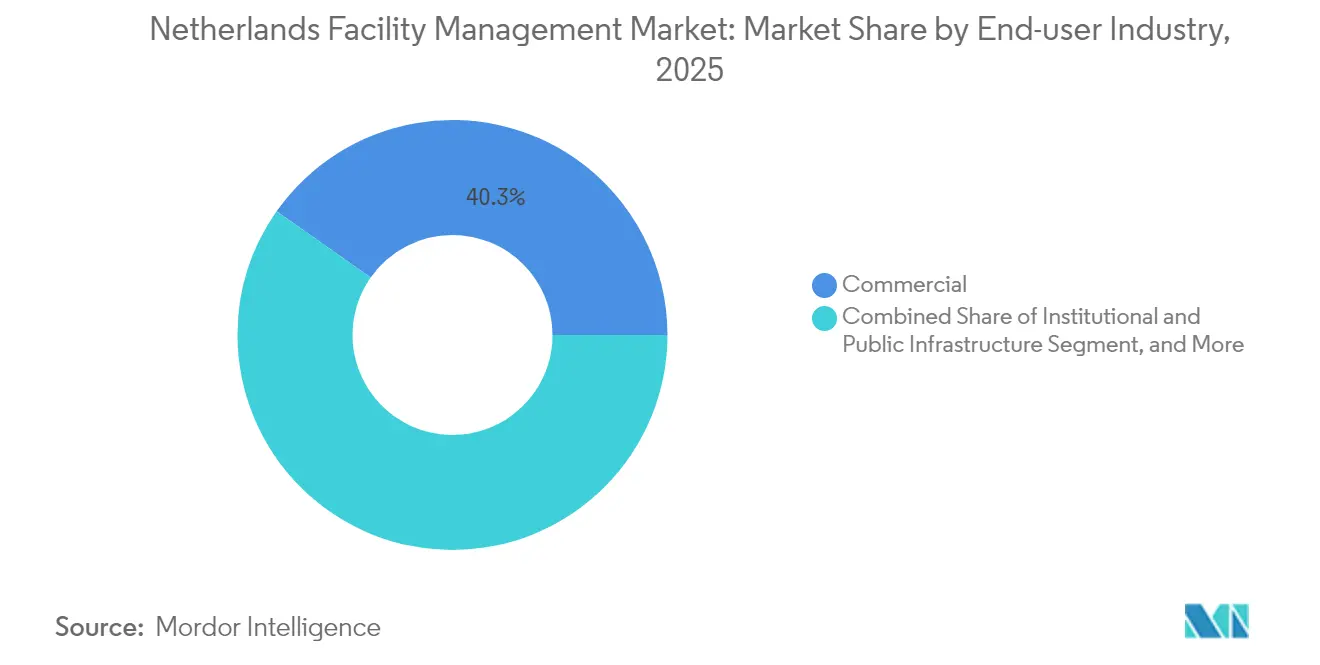

- By end-user industry, commercial facilities commanded 40.25% of the Netherlands facility management market size in 2025, whereas institutional and public infrastructure segments are expanding at a 4.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability Drives Transformation in Facility Operations | +0.8% | National, with concentration in Amsterdam, Rotterdam, The Hague | Medium term (2-4 years) |

| Technology Integration Reshapes Service Delivery | +0.7% | National, with early adoption in Zuidas and Eindhoven tech corridors | Short term (≤ 2 years) |

| Hybrid Working Transforms Space Utilization | +0.6% | National, with highest impact in Amsterdam and Utrecht office markets | Short term (≤ 2 years) |

| Rising Outsourcing Trend Reshapes Service Models | +0.5% | National, with government sector leading adoption | Medium term (2-4 years) |

| Circular Economy Regulations Foster Demand for Resource-Efficient FM | +0.4% | National, with construction sector concentration | Long term (≥ 4 years) |

| Aging Building Stock Spurs Renovation and Maintenance Outsourcing | +0.9% | National, with 425,000 buildings requiring foundation repairs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability Drives Transformation in Facility Operations

Mandatory Energy Label C for offices above 100 m² has turned regulatory compliance into the single largest catalyst for the Netherlands facility management market.[1]Loyens & Loeff, “Energy Labels Required for Office Buildings as of 2023,” loyensloeff.com Facility managers must implement measures with paybacks under 10 years, accelerating demand for energy audits, heat-pump retrofits, and building-fabric upgrades. BREEAM-NL certifications now influence asset valuations across prime districts, motivating owners to embed continuous commissioning and waste-minimization clauses in contracts.[2]Dutch Green Building Council, “Wat is BREEAM-NL,” breeam.nl The CSRD roll-out in 2025 obliges roughly 2,500 Dutch companies to disclose ESG KPIs, placing facility data capture at the heart of corporate reporting.[3]Coolset, “Dutch Implementation Proposal of the CSRD,” coolset.com Suppliers therefore promote green cleaning chemicals, circular-economy materials, and ISO 14001 workflows as differentiators. In parallel, government allocations of EUR 1 billion for emission-free construction stimulate retrofits that prioritize low-carbon concrete, modular façades, and cradle-to-cradle asset management.[4]Atradius, “Nederlandse bouwsector groeit 1.6% in 2025,” atradius.nl

Technology Integration Reshapes Service Delivery

IoT gateways connected to HVAC, lighting, and security assets deliver live telemetry that underpins predictive maintenance, cutting failure-related call-outs by up to 35% in pilot portfolios. Buildings such as The Edge in Amsterdam demonstrate electricity consumption 70% lower than comparable offices after digitized controls, occupancy analytics, and AI-driven optimization went live. Providers extend these learnings via digital-twin platforms capable of simulating alternative retrofit scenarios and benchmarking carbon footprints against BENG norms. Investment moves-Edge’s stake in TPEX International or IFS’s acquisition of ULTIMO-underscore how software ecosystems are becoming core to Netherlands facility management market competitiveness. Contracts are shifting from prescriptive task lists to outcome-based agreements promising kWh-savings or uptime thresholds, aligning supplier remuneration with measurable performance metrics.

Hybrid Working Transforms Space Utilization

Dutch office attendance stabilized near 56% in 2024, down from pre-pandemic peaks yet up from 2022 troughs. Government workforce surveys reveal 36% of employees prefer onsite presence only twice weekly, prioritizing work-life balance and commute reduction. These patterns compel facility teams to toggle air-handling volumes, cleaning routes, and security staffing in line with daily occupancy data. Space-booking apps, desk sensors, and digital reception kiosks enable service scaling that prevents resource wastage without sacrificing user experience. Soft-service suppliers are broadening mandates to include WELL-standard air quality monitoring and ergonomic furniture rotation, embedding employee satisfaction scores into KPIs. The result is a Netherlands facility management market where client value is judged by wellness metrics as much as by square-meter cleanliness.

Aging Building Stock Spurs Renovation and Maintenance Outsourcing

An estimated 425,000 properties across the country suffer subsidence-related foundation damage, creating sustained structural remediation outlays that favor external specialist contractors. Buildings erected before 1980 often rely on obsolete HVAC and electrical systems that fall short of current BENG and MPG efficiency rules, driving multi-year modernization pipelines. Because many owners lack in-house engineering depth, integrated facility managers capture long-term contracts covering structural repairs, façade renewal, and lifecycle asset planning. Funding support through the National Heat Fund and energy-saving grants further enlarges project scope. Consequently, capital-project advisory services are converging with traditional maintenance lines, broadening revenue bases for the Netherlands facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Costs Pressure Operational Efficiency | -0.4% | National, with highest impact in Amsterdam and Rotterdam metropolitan areas | Short term (≤ 2 years) |

| Labor Shortages Challenge Service Delivery | -0.6% | National, with critical shortages in skilled manual labor | Medium term (2-4 years) |

| Fragmented Supplier Ecosystem Limits Standardization | -0.3% | National, with regional variations in service quality | Medium term (2-4 years) |

| Stringent Tendering Processes Favor Lowest Bids Over Quality | -0.2% | National, with government sector concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Costs Pressure Operational Efficiency

Construction inflation eased in 2025 yet remains above historic norms after a 2.8% sector contraction in 2024 and a modest 1.6% rebound forecast this year. Facility managers now juggle elevated wage agreements, higher insurance premiums, and escalating material prices linked to global supply volatility. Simultaneously, compliance costs for CSRD reporting and Energy Performance Certificates raise overheads. Firms respond by automating workflow scheduling, clustering service routes, and renegotiating energy tariffs through collective-buying pools. Outcome-based pricing that ties fees to energy-savings ratios helps shield margins while justifying capital-expenditure outlays. Nevertheless, cost headwinds trim overall Netherlands facility management market CAGR by an estimated 0.4 percentage points.

Labor Shortages Challenge Service Delivery

McKinsey projects Dutch labor gaps could reach 1.4 million positions by 2030, with 100,000 vacancies in skilled manual roles foundational to facilities trade services. Tight talent pools inflate wages for electricians, HVAC technicians, and cleaning operatives, prompting providers to adopt robotics (e.g., autonomous scrubbers) and smart-glasses field support to stretch existing headcounts. Enforcement against false self-employment pushes freelancers toward salaried arrangements, pressuring small subcontractors reliant on flexible labor. Large multinationals answer with in-house academies, apprenticeship alliances, and migrant recruitment pipelines, yet onboarding lags still jeopardize tender compliance. Persistent shortages subtract a 0.6 percentage-point drag from the Netherlands facility management market growth outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Infrastructure Modernization

Hard services generated 58.10% of Netherlands facility management market share in 2025 on the back of structural remediation, HVAC upgrades, and fire-system lifecycle programs. The Netherlands facility management market size tied to hard services benefits from government subsidy schemes rewarding heat-pump adoption and low-carbon materials. Providers integrate IoT sensors into chillers and boilers to shift from reactive to predictive repairs, curbing downtime penalties and extending asset life. Aging post-war housing blocks and subsidence-affected canalside properties require foundation-jack stabilization, a niche where local specialists partner with larger FM integrators to meet safety timelines. Over the forecast, spending transitions from one-off refurbishments to rolling performance contracts that guarantee kilowatt reductions.

Soft services, while smaller, are forecast to grow 4.02% annually as hybrid working elevates employee-experience KPIs. Smart-dispensing cleaning robots help providers manage labor scarcity while ensuring consistent hygiene across fluctuating occupancy profiles. Concierge, catering, and security packages increasingly bundle wellness analytics to score biophilic design elements and indoor-air parameters against WELL benchmarks. The convergence of data streams allows suppliers to cross-sell energy coaching and waste-segregation advisory within their soft-service remit, cementing integrated positioning inside the Netherlands facility management market.

By Offering Type: Outsourcing Accelerates Through Specialization

Outsourced contracts captured 65.35% of Netherlands facility management market size in 2025 and are slated to climb at a 3.92% CAGR through 2031 as clients divest non-core support functions. Integrated FM (IFM) packages dominate new tenders, blending technical maintenance, soft services, and ESG reporting under single master agreements. Multinational landlords prize IFM providers that maintain ISO 55000 asset-management credentials and deliver cross-border governance compliance, including DORA cyber-resilience stipulations. Bundled FM contracts remain popular among mid-market portfolios seeking price efficiency through volume pooling, whereas single FM retains relevance for mission-critical environments such as data centers requiring domain-specific technicians.

In-house models persist within heavily regulated sectors like defense or nuclear medicine, yet budget austerity and skills constraints drive hybrid solutions where strategic oversight stays internal while field operations shift to external partners. As-a-service pricing structures-ranging from “lighting-as-a-service” to “energy-savings-as-a-service”-gain ground, shifting capital expenditures onto providers’ balance sheets. These structures align cost with measurable benefits, reinforcing the competitive moat of experienced suppliers inside the Netherlands facility management market.

By End-user Industry: Commercial Sector Leads While Public Infrastructure Accelerates

Commercial real estate, spanning offices, retail, and data hubs, accounted for 40.25% of Netherlands facility management market size in 2025, reflecting heavy demand for tenant-experience upgrades and net-zero carbon roadmaps. Landlords in Amsterdam’s Zuidas adopt digital twins to manage ventilation in real time, while retail chains deploy centralized BMS platforms to optimize refrigeration loads. IT, telecom, and co-working operators contract IFM providers able to deliver 24/7 uptime plus robust cybersecurity frameworks.

Institutional and public-infrastructure segments post the fastest expansion at 4.46% CAGR to 2031, buoyed by municipal circular-economy ordinances requiring resource-efficient maintenance of schools, hospitals, and transport nodes. Healthcare facilities adopt smart-ward cleaning robots and negative-pressure HVAC retrofits to meet infection-control guidelines, while the Ministry of Infrastructure’s renovation of waterways invites long-term FM alliances covering lock automation and predictive component swap-outs. Industrial sites demand intersectional expertise across safety, ATEX compliance, and energy management, creating high-margin niches for vertically specialized providers in the Netherlands facility management industry.

Geography Analysis

Amsterdam, Rotterdam, The Hague, Utrecht, and Eindhoven anchor more than two-thirds of Netherlands facility management market revenue, owing to dense commercial floorplates and advanced sustainability codes. Amsterdam’s Edge-led smart-building cluster sets energy benchmarks that ripple across national portfolios, reinforcing demand for high-tech FM services. Rotterdam’s port complex and petrochemical sites require integrated asset-integrity support blending corrosion monitoring, fire safety, and environmental permits. The Hague’s concentration of ministries drives security-cleared service contracts focusing on access control and classified waste disposal.

Beyond the Randstad, secondary hubs such as Groningen embrace standardized IFM solutions to maximize economies of scale across university campuses and energy-transition labs. Nationwide, 425,000 units of foundation-affected housing spur remediation frameworks funded partly through regional subsidies, distributing work evenly across provinces. Public-sector renovation aims to create 120,000 new homes by repurposing existing stock by 2030, further widening the Netherlands facility management market footprint.

Compact geography allows suppliers to centralize help-desk operations while deploying mobile engineering pods capable of reaching any major city within 90 minutes, compressing response-time SLAs. The government’s EUR 1 billion budget for clean construction technologies encourages providers to extend low-emission machinery and electric vehicle fleets, ensuring compliance across all Dutch regions. Climatic challenges such as sea-level rise and increased precipitation accelerate maintenance on dikes and pumping stations, reinforcing the strategic role of facility managers in national resilience planning.

Competitive Landscape

The Netherlands facility management market balances scale economies of global groups with the domain depth of regional specialists. ISS, Sodexo, and CBRE leverage multinational procurement, proprietary tech stacks, and cross-sector expertise to secure complex IFM mandates. Facilicom, Vebego, and Unica differentiate on local labor networks, circular-economy know-how, and sector-specific engineering. Mid-tier outfits such as Asito and Dolmans exploit niche verticals—air-terminal clean-ing or heritage-building maintenanceunattractive to larger rivals.

Digital capability increasingly dictates win probabilities. ISS’s cloud-based data lake harmonizes energy and occupancy metrics across 1,600 properties after its 2024 acquisition of gammaRenax, reinforcing European service depth Vebego’s 2023 turnover of EUR 1.48 billion funds expansion of robotics pilots and brand consolidation strategies aimed at unified customer touchpoints. IFS’s purchase of ULTIMO embeds SaaS EAM into field-service scheduling, promising predictive insights that unlock 18% global EAM market share under the combined entity.

Strategic alliances flourish: Edge collaborates with TPEX International to manage 1,000 high-performance buildings via digital twins, while Renew Holdings’ Full Circle takeover primes entry into onshore-wind maintenance. ESG consulting bolt-ons and AI-powered analytics platforms represent prized acquisition targets as buyers seek differentiated IP. Despite consolidation sparks, market fragmentation endures, granting agile local providers capacity to outmaneuver larger peers on bespoke, short-cycle projects within the Netherlands facility management market.

Netherlands Facility Management Industry Leaders

Apleona GmbH

Vebego International BV

Hago Netherlands BV

DW Facility Group BV

Fortrus

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Renew Holdings PLC acquired Full Circle Group Holding B.V. for EUR 60 million, adding a technology-enabled wind-farm maintenance platform operating from Amersfoort.

- February 2025: IFS completed its acquisition of Netherlands-based ULTIMO, expanding flexible SaaS asset-management solutions across 2,000 clients.

- January 2025: Dutch government submitted the CSRD implementation bill to the House of Representatives, formalizing extensive sustainability reporting obligations.

- January 2025: BESIX and Proximus delivered an AI-optimized smart-building headquarters in Dordrecht featuring advanced automation and energy-management systems.

Netherlands Facility Management Market Report Scope

Facility management (FM) incorporates many disciplines to ensure the built environment's functionality, safety, comfort, and efficiency by integrating people, process, place, and technology. Facility management includes management methods and techniques for building operations and maintenance, support services, environmental management, and property management for an organization, along with overall harmonization of the work environment in an organization standardizing services, and streamlining processes for end users.

The Netherlands facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehousing) |

| Hospitality (Hotels, Eateries and Restaurants) |

| Institutional and Public Infrastructure (Government, Education, Transport) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehousing) | |

| Hospitality (Hotels, Eateries and Restaurants) | ||

| Institutional and Public Infrastructure (Government, Education, Transport) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Netherlands facility management market?

The Netherlands facility management market size is USD 6.24 billion in 2026, with a projected CAGR of 3.88% to 2031.

Which service category leads market revenues?

Hard services dominate with 58.10% of Netherlands facility management market share due to pervasive infrastructure modernization needs.

How important is outsourcing in Dutch facility operations?

Outsourced models account for 65.35% of revenues and are expected to continue growing as compliance complexity and technology requirements rise.

Which end-user segment is expanding quickest?

Nstitutional and public-infrastructure facilities show a 4.46% CAGR, outpacing commercial and industrial segments on the back of sustainability mandates.

What technologies are reshaping facility management in the Netherlands?

IoT sensors, AI-driven analytics, and digital-twin platforms enable predictive maintenance, energy optimization, and outcome-based contracts across leading portfolios.

Page last updated on: