Blockchain Identity Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.51 Billion |

| Market Size (2031) | USD 47.97 Billion |

| Growth Rate (2026 - 2031) | 49.08% CAGR |

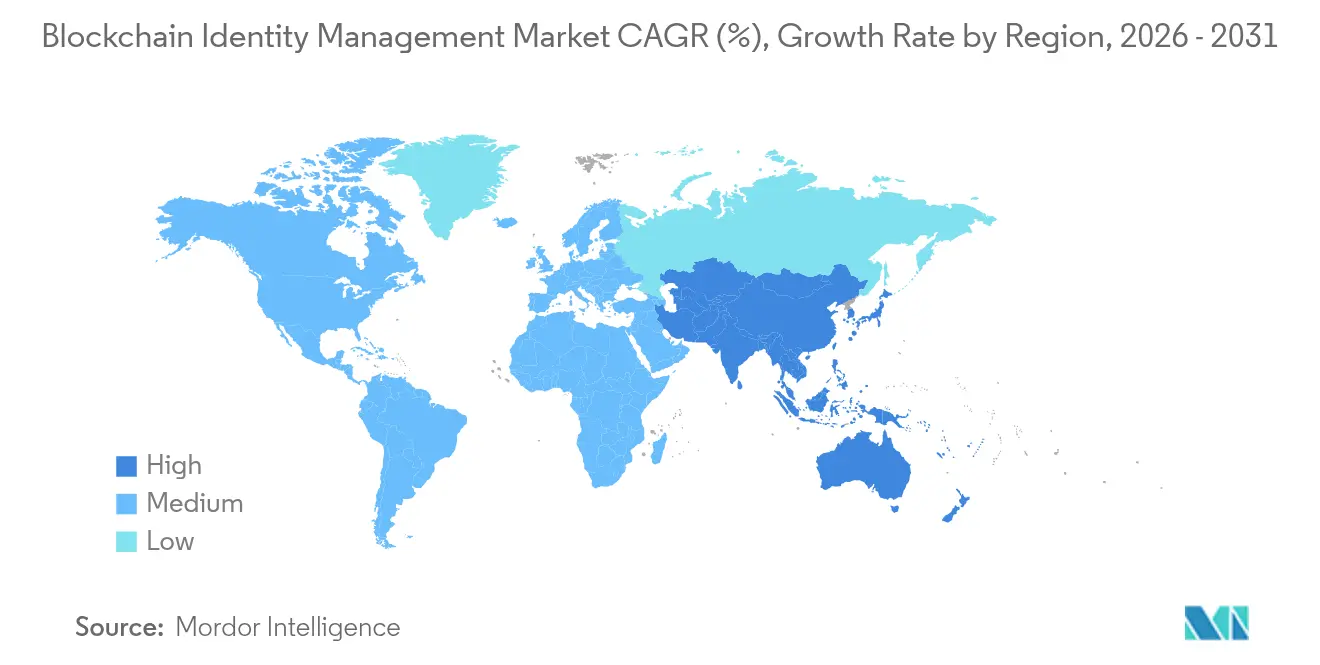

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain Identity Management Market Analysis by Mordor Intelligence

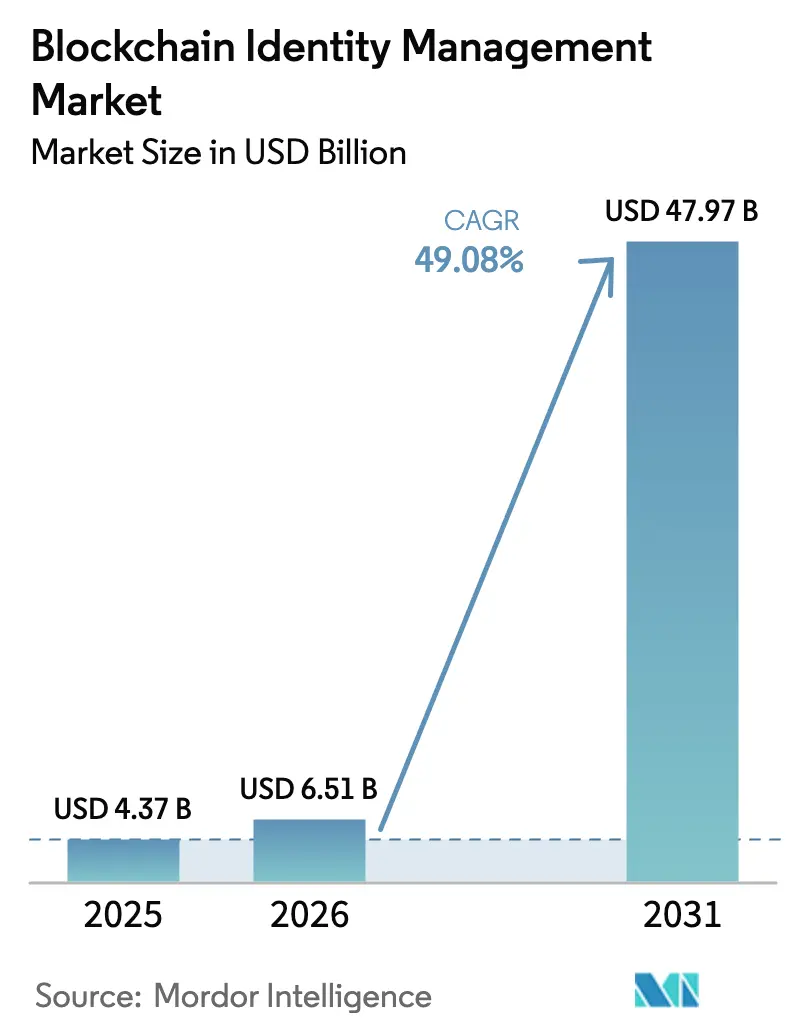

The Blockchain Identity Management Market size was valued at USD 4.37 billion in 2025 and estimated to grow from USD 6.51 billion in 2026 to reach USD 47.97 billion by 2031, at a CAGR of 49.08% during the forecast period (2026-2031).

This sharp up-curve stems from the collision of tightening digital-ID regulations, falling cryptographic-proof costs, and the maturation of enterprise-grade distributed-ledger stacks, which together propel solution roll-outs across finance, healthcare, government, and Web3 commerce. Continuous revelations of credential theft—well above 16 billion compromised passwords—further erode confidence in siloed, centralized directories and push buyers toward decentralized, verifiable-credential architectures that anchor consent and authentication events on tamper-resistant ledgers. Solution vendors are using zero-knowledge proof (ZKP) engines to satisfy privacy law while exposing only the minimal attributes a relying party needs, a design that materially lowers onboarding drop-off and fraud loss. Government wallet mandates, typified by Europe’s eIDAS 2.0 rule, supply an assured end-user base and act as an accelerant for adjacent commercial use cases. Venture capital momentum remains firm, with blockchain identity start-ups netting nine-figure rounds despite a broader technology funding slowdown.

Key Report Takeaways

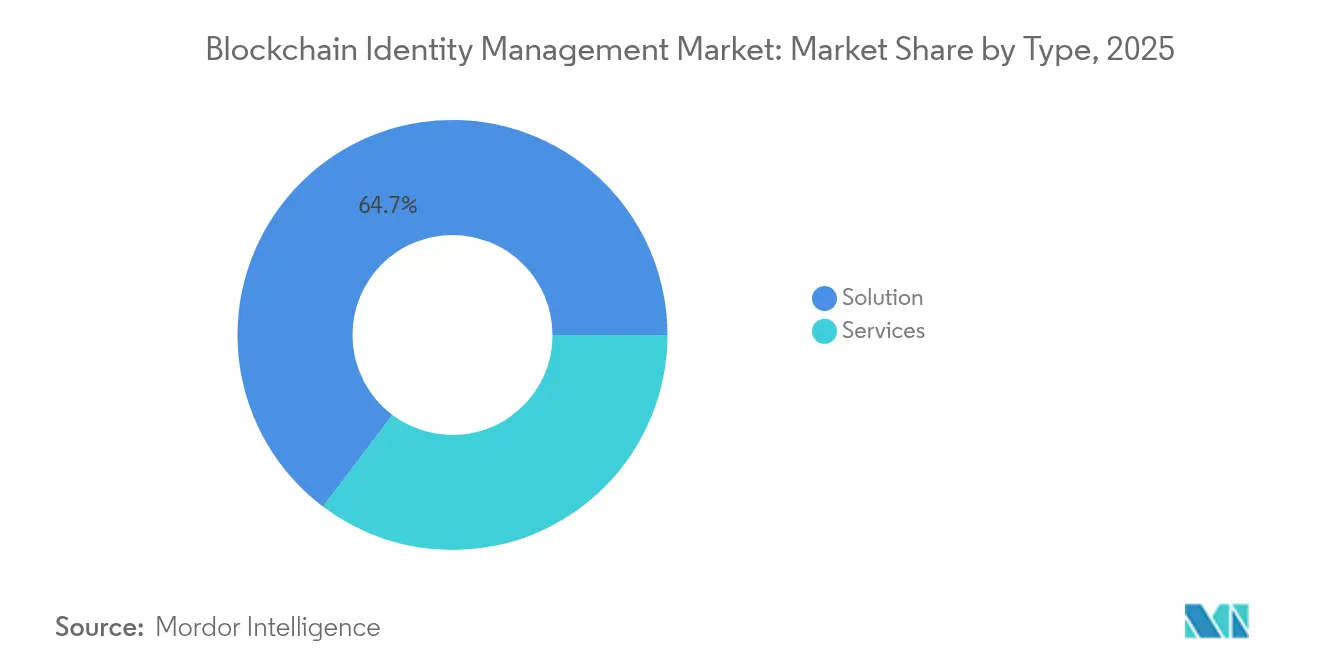

- By type, solutions held 64.73% of the blockchain identity management market share in 2025; services are projected to expand at a 53.49% CAGR through 2031.

- By provider, the application-provider segment led with 47.05% revenue in 2025, while middleware providers are tracking a 55.24% CAGR to 2031.

- By end-user, financial services commanded 31.12% share of the blockchain identity management market size in 2025; healthcare is forecast to grow at 57.23% CAGR over 2026-2031.

- By geography, North America contributed 42.10% of 2025 revenue, whereas Asia-Pacific is set to record the fastest 56.41% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Blockchain Identity Management Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising regulatory mandates for digital KYC and AML compliance | +8.5% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| Surge in self-sovereign identity (SSI) pilots by financial institutions | +7.2% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Growth of Web3 wallets integrating verifiable credentials | +6.8% | Global, led by North America and APAC | Medium term (2-4 years) |

| Expansion of national e-ID programs adopting blockchain back-ends | +9.1% | EU core, APAC expansion, selective North America adoption | Long term (≥ 4 years) |

| Tokenization of patient consent records in precision medicine | +4.3% | North America and EU, with spillover to developed APAC markets | Long term (≥ 4 years) |

| Demand for privacy-preserving reusable age-verification in metaverse retail | +3.7% | Global, concentrated in digital-native demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Regulatory Mandates for Digital KYC and AML Compliance

Financial institutions confront stringent new KYC and AML rules that insist on cryptographically provable identity checks capable of audit-grade traceability. United States regulators are expanding Customer Identification Program coverage to investment advisers, while the European Banking Authority tightens screening rules for virtual-asset service providers. Central-bank digital currency (CBDC) pilots in India and Brazil embed blockchain identity layers so regulators can view provenance without breaching user privacy.[1]IndusInd Bank, “Successful CBDC Pilot Execution,” indusind.com The convergence of CBDC rollout schedules and privacy-preserving ZK tooling elevates blockchain identity from proof-of-concept to budget-line item, adding sustained lift to the blockchain identity management market.

Surge in Self-Sovereign-Identity Pilots by Financial Institutions

Large banks are testing self-sovereign identity (SSI) to slash the USD 35 billion annual KYC spend caused by redundant data collection. HSBC and Deutsche Bank have piloted SSI wallets that allow customers to reuse credentials across lending, payments, and insurance channels, cutting onboarding times from days to minutes while leaving raw personal data under user custody. Early pilots demonstrate that credential reuse can halve per-customer due-diligence costs, creating a compelling payback window and deepening demand for enterprise middleware that bridges decentralized identifiers (DIDs) and core banking systems.

Growth of Web3 Wallets Integrating Verifiable Credentials

Consumer crypto wallets are evolving into multifaceted digital-ID containers. Google’s 2025 upgrade to Wallet lets users prove legal age to online merchants through an elliptic-curve ZKP that reveals nothing except “over-18” status, a dramatic privacy gain now accessible to hundreds of millions of Android users.[2]Google LLC, “New Android Features for Summer 2025,” blog.google ConsenSys quickly followed by purchasing Web3Auth, thereby embedding email and social-login recovery in MetaMask to reduce the 35% wallet-loss problem cited by exchanges. As wallets merge payments, NFTs, and verifiable credentials, they become a default gateway into blockchain identity services, giving wallet providers disproportionate influence over the blockchain identity management market.

Expansion of National e-ID Programs Adopting Blockchain Back-ends

The European Union’s eIDAS 2.0 statute obliges all 27 member states to issue digital wallets that support cross-border services no later than 2026, effectively guaranteeing a massive addressable population for decentralized IDs.[3]European Commission, “Regulation (EU) 2024/1123 on a European Digital Identity,” europa.eu Malaysia’s MyDigital ID and Australia’s Digital ID Act 2024 replicate the model in Asia-Pacific, offering private-sector accreditation paths that let banks and telecoms become credential issuers. These government rollouts set uniform technical artifacts—schema, signing algorithms, validation endpoints—that de-risk vendor selection for enterprises and open bidding pipelines worth hundreds of millions of dollars.

Restraints Impact Analysis of Blockchain Identity Management Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability gaps among DID, VC, and legacy IAM stacks | -4.2% | Global, particularly affecting enterprise adoption | Short term (≤ 2 years) |

| Uncertain global data-protection harmonization (GDPR vs. other regimes) | -3.8% | Global, with regulatory fragmentation between EU, US, and APAC | Medium term (2-4 years) |

| Latency penalties of zero-knowledge proof (ZKP) orchestration at scale | -2.9% | Global, affecting real-time applications | Medium term (2-4 years) |

| Carbon-footprint scrutiny of public-chain identity projects | -1.7% | EU and North America, expanding to ESG-conscious markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps Among DID, VC, and Legacy IAM Stacks

Enterprises wedded to SAML, OAuth, or Active Directory face steep integration toil when layering W3C-style DIDs and verifiable-credential (VC) flows. Systems integrators report multi-million-dollar middleware budgets to reconcile decentralized revocation registries with conventional certificate authorities. Healthcare exemplifies the challenge: electronic-health-record vendors must meet HIPAA logging rules yet map them onto patient-controlled wallets, a feat only a handful of platforms can deliver at scale. Lack of cross-stack interoperability slows procurement and motivates buyers to favor hybrid models that still depend on centralized directories, muting near-term uptake in the blockchain identity management market.

Uncertain Global Data-Protection Harmonization

The immutable traits of public ledgers collide with “right to erasure” clauses in GDPR, while the forthcoming US American Privacy Rights Act proposes variant consent and redress conditions. Multinationals fear conflicting enforcement that could force data sharding by region, undercutting the universal-credential promise. Vendors are responding with “selective disclosure” and “off-chain storage” patterns, yet the regulatory fog makes boards hesitant to green-light multi-jurisdiction deployments, trimming a few percentage points off the forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Blockchain Identity Management Market Segment Analysis

By Type:

Solutions Underpin Market Revenue MomentumSolutions accounted for 64.73% of 2025 revenue, confirming buyer appetite for end-to-end stacks that wrap credential issuance, wallet SDKs, ZKP engines, and governance tooling into one commercial contract. Most deployments bundle at least two conformance profiles—W3C-VC and ISO/IEC 18013-5—to maximize cross-jurisdiction acceptance. In 2025, leading hospital networks in Germany and Spain issued over 3 million patient-consent tokens on Hyperledger Fabric, illustrating how sector-specific builds can proceed without public-chain reliance. Public-permissionless approaches continue to gain mindshare because chains such as Tezos and Algorand cut energy cost per transaction by double-digit factors compared with first-generation proof-of-work networks, aligning with ESG mandates. The blockchain identity management market size for solution offerings is on track to expand at a 46.7% CAGR, adding more than USD 10 billion by 2031.

Services, meanwhile, register the fastest 53.49% growth as CIOs outsource node-ops, credential lifecycle, and trust-framework governance. Integration specialists build connectors from decentralized registries into HR, CRM, and ERP suites, a task in high demand because fewer than 8% of enterprises possess in-house cryptographic engineering capacity. Managed-service contracts frequently include service-level agreements for uptime on validator clusters and escrowed key-custody to satisfy audit committees. As a result, services are expected to capture nearly one-third of total blockchain identity management market revenue by 2031, easing the entry barriers for mid-market organizations that would otherwise defer adoption.

By Provider:

Application Providers Secure Distribution AdvantageApplication providers controlled 47.05% sales in 2025, a lead owed to their embedded presence in workflow software where identity events fire: loan origination, mobile checkout, patient onboarding. Okta’s decision to weave verifiable-credential exchange into its IAM cloud in 2025 illustrates how incumbents are co-opting decentralized-ID functionality rather than ceding ground to upstarts. The blockchain identity management market enjoys spillover when thousands of Okta customers can toggle a pilot through a configuration panel instead of footing a green-field project.

Middleware specialists, though starting from a smaller base, are advancing at 55.24% CAGR by offering protocol bridges between DIDComm, SAML, and proprietary token formats. Their revenue model—API usage fees—scales linearly with credential calls, so fintech and e-commerce traffic drive sizable annuities. Infrastructure providers focus on consensus and key management, with bare-metal validation and hardware security module leasing forming new service lines. Collective competition intensifies but also raises the interoperability bar, ultimately stabilizing integration pain points that had previously curbed the blockchain identity management market’s velocity.

By End-user:

BFSI Holds the Lion’s Share while Healthcare SurgesBanking, financial services, and insurance (BFSI) owned 31.12% revenue in 2025, supported by stringent know-your-customer reporting and the parallel rise of programmable money rails. When India’s IndusInd Bank settled carbon-credit trades via CBDC interlinked with blockchain-proofed identities, it demonstrated real-time regulatory visibility and carbon-tracking in one flow—capabilities legacy directories cannot provide. For global banks, each credential reused across product lines jams incremental fraud risk and culminates in lower capital reserves set aside for non-performing exposures.

Healthcare grows fastest at 57.23% CAGR, reflecting payer and provider hunger to exchange electronic health records under stringent privacy regimes. A 2025 Nature study documented a 30% cut in duplicate lab testing after blockchain-anchored consent eliminated data-silo lock-in. The blockchain identity management market size for healthcare is projected to surpass USD 8.21 billion by 2031. Government and public-sector programs run pilot wallets for cross-agency benefit delivery, while telecom operators test SIM-bound DIDs for device attestation, signaling a broader commercial foundation.

Geography Analysis

North America Blockchain Identity Management Market

North America retained 42.10% of 2025 spend, underpinned by federal proof-of-identity frameworks and venture funding depth. The United States appropriated USD 185 million in FY 2025 for digital-identity infrastructure grants, seeding deployments in driver-license agencies and Medicare portals. Google’s Wallet upgrade placed privacy-preserving age verification into the hands of over 240 million Android users, cementing mainstream familiarity with blockchain-backed claims. Canada’s pan-Canadian Trust Framework revision allows provincial health cards to become root credentials in verifiable-credential graphs, boosting inter-province telehealth trust. Mexico is joining a trilateral pilot that lets migrant workers present blockchain credentials to cross-border employers within minutes, highlighting the regional network effect. With such institutional backing, the blockchain identity management market in North America remains the largest single-region pool by 2031.

APAC Blockchain Identity Management Market

Asia-Pacific records the steepest slope, clocking a 56.41% CAGR through 2031. Singapore’s Singpass handled 350 million verifiable-credential transactions in 2025 on a population of 5.9 million, providing empirical proof of high-volume feasibility. Malaysia’s MyDigital ID is moving from pilot to nationwide issuance, including a cross-border alignment layer with ASEAN member states. Australia’s Digital ID Act opens accreditation so private banks and telcos can issue or verify credentials, sparking a competitive service marketplace. India combines its CBDC pilot and Aadhaar revamp to create programmable subsidies locked to self-sovereign wallets. These multipronged policies funnel substantial budget and public acceptance into the blockchain identity management market, ensuring APAC overtakes Europe in annual incremental revenue by 2028.

Competitive Landscape

The blockchain identity management market is moderately concentrated. IBM, Microsoft, and Oracle package credential issuance and verification inside their cloud portfolios, exploiting scale and procurement convenience. IBM’s 2025 release of Identity Ledger Service added built-in selective-disclosure ZKPs, enabling Fortune 500 clients to deploy live wallets in under six weeks. Microsoft built Entra Verified ID into Office 365 tenants, moving decentralized identity from optional to default in workplace collaboration. Oracle fused its identity graph with banking KYC modules, expediting compliance for tier-one banks.

Specialist vendors differentiate on agility and Web3 alignment. Dock Labs offers open-source SDKs and a permissionless ledger optimized for identity payloads under 2 kB, achieving sub-second issuance latency. Civic Technologies launched Civic Pass Managed, letting developers embed reusable credentials in dApps without deep cryptography knowledge. ConsenSys spent USD 200 million across two acquisitions—Web3Auth for social recovery and HAL for low-code workflow triggers—building a vertically integrated Web3 wallet stack. Humanity Protocol reached unicorn status by binding palm-print biometrics to ZK-proofs, chasing the Sybil-resistance opportunity in on-chain governance.

Blockchain Identity Management Industry Leaders

International Business Machines Corporation

Microsoft Corporation

Rapid Innovation

LeewayHertz

1Kosmos

- *Disclaimer: Major Players sorted in no particular order

Blockchain Identity Management Market Companies Covered in this Report

- International Business Machines Corporation

- Microsoft Corporation

- Rapid Innovation

- LeewayHertz

- 1Kosmos

- SoluLab

- Thales Group

- Okta Inc.

- ConsenSys (uPort)

- Dock Labs

- Oracle Corporation

- Blockchain Helix

- Hu-Manity.co

- Civic Technologies

- Ping Identity

- NEC Corporation

- R3

- Ontology

- SelfKey

- Evernym

Recent Industry Developments in Blockchain Identity Management Market

- June 2025: ConsenSys acquired Web3Auth to enhance MetaMask recovery, mitigating seed-phrase loss for 35% of wallet users.

- June 2025: Moca Foundation launched Moca Chain, an EVM-compatible L1 focused on privacy-preserving identity, backed by Animoca Brands.

- March 2025: SEALSQ Corp invested in Wecan Token and teamed with Solana to anchor sensitive data such as land registries using Solana Attestation Service.

- February 2025: Civic rolled out Civic Pass Managed, giving developers turnkey reusable‐credential integration while staying GDPR-aligned.

Global Blockchain Identity Management Market Report Scope

Blockchain enables more secure management and storage of digital identities by providing unified, interoperable, and tamper-proof infrastructure. It can create a unified, interoperable system where one's digital identity documents can be used across multiple platforms.

The blockchain identity management market is segmented by type (solution, services), by provider (application provider, middleware provider, infrastructure provider), by end-user (BFSI, IT and telecom, retail and e-commerce, media and entertainment, healthcare, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Segmentation Overview

| Solutions | Public/Permissionless Platforms |

| Private/Permissioned Platforms | |

| Services | Consulting and Integration |

| Support and Managed Services |

| Application Provider |

| Middleware Provider |

| Infrastructure Provider |

| BFSI |

| IT and Telecom |

| Retail and E-commerce |

| Media and Entertainment |

| Healthcare |

| Government and Public Sector |

| Other End-users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Type | Solutions | Public/Permissionless Platforms | |

| Private/Permissioned Platforms | |||

| Services | Consulting and Integration | ||

| Support and Managed Services | |||

| By Provider | Application Provider | ||

| Middleware Provider | |||

| Infrastructure Provider | |||

| By End-user | BFSI | ||

| IT and Telecom | |||

| Retail and E-commerce | |||

| Media and Entertainment | |||

| Healthcare | |||

| Government and Public Sector | |||

| Other End-users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the blockchain identity management market?

The market stands at USD 6.51 billion in 2026 and is projected to reach USD 47.97 billion by 2031 at a 49.08% CAGR.

Which segment generates the most revenue?

Solution packages that bundle credential issuance, ZKP engines, and governance tooling generate 64.73% of 2025 revenue.

Which end-user industry is growing fastest?

Healthcare leads growth with a 57.23% CAGR, fueled by blockchain-based electronic-health-record sharing and consent tokenization.

Why is Asia-Pacific the fastest-growing region?

APAC growth at 56.41% CAGR is driven by national digital identity programs in Singapore, Malaysia, Australia, and ongoing CBDC pilots in India.

Page last updated on: