Certificate Authority Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

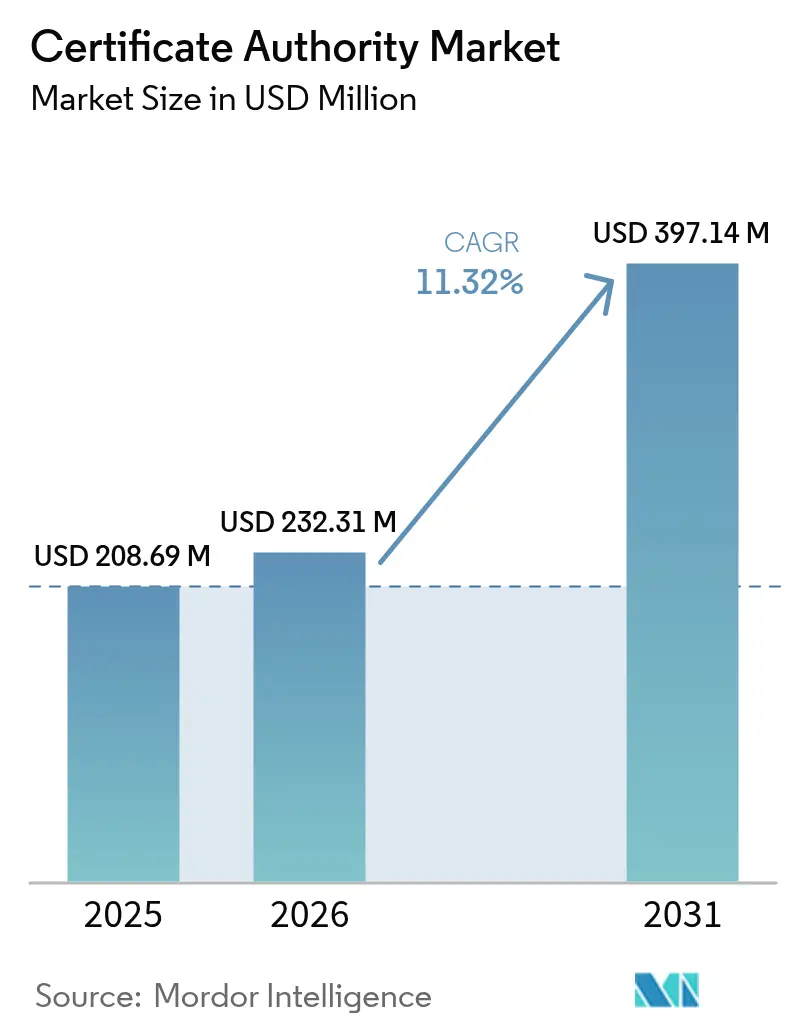

| Market Size (2026) | USD 232.31 Million |

| Market Size (2031) | USD 397.14 Million |

| Growth Rate (2026 - 2031) | 11.32% CAGR |

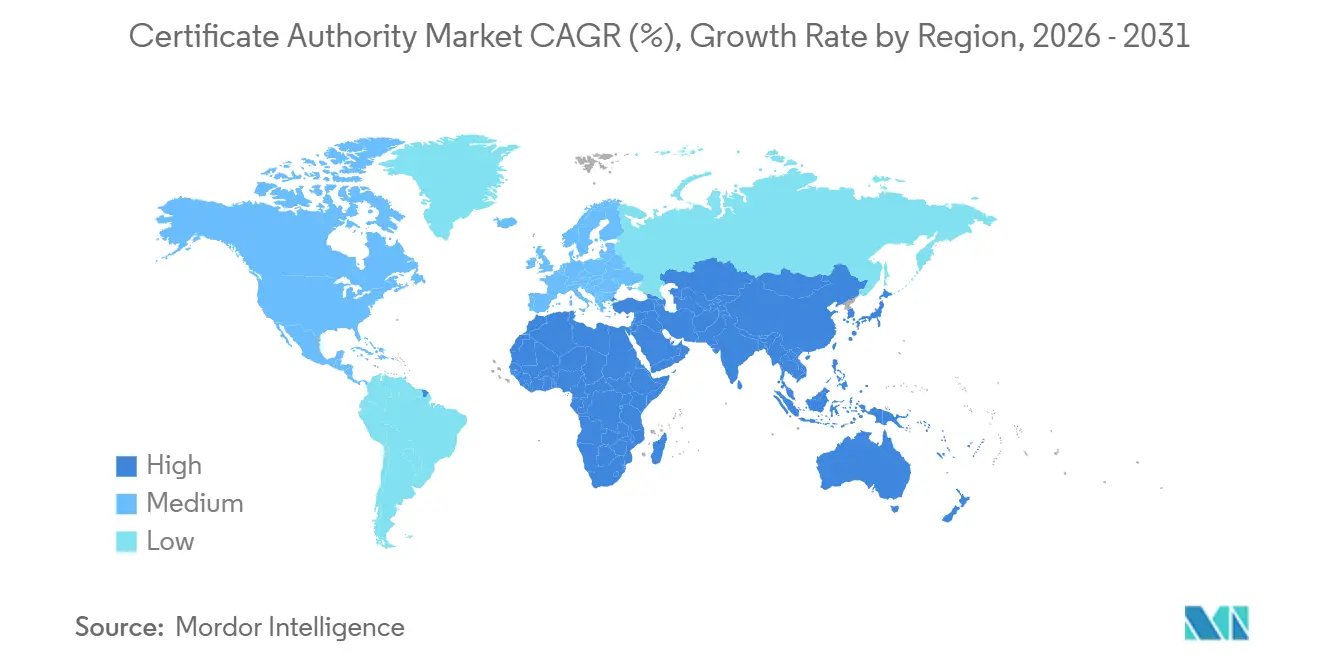

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Certificate Authority Market Analysis by Mordor Intelligence

The certificate authority market size is projected to be USD 208.69 million in 2025, USD 232.31 million in 2026, and reach USD 397.14 million by 2031, growing at a CAGR of 11.32% from 2026 to 2031. Near-continuous certificate renewals, soaring volumes of machine identities, and cloud-native delivery models are reshaping the certificate authority market. Browser vendors have shortened certificate validity, forcing enterprises to automate issuance, while post-quantum standards compel parallel migration planning. Hyperscalers now embed private and public CAs directly inside infrastructure-as-code workflows, compressing deployment cycles from days to seconds. Competition is intensifying as free domain-validation certificates, API-first issuance platforms, and industry-specific trust requirements converge, shifting revenue toward subscription contracts tied to automated renewal volumes.

Key Report Takeaways

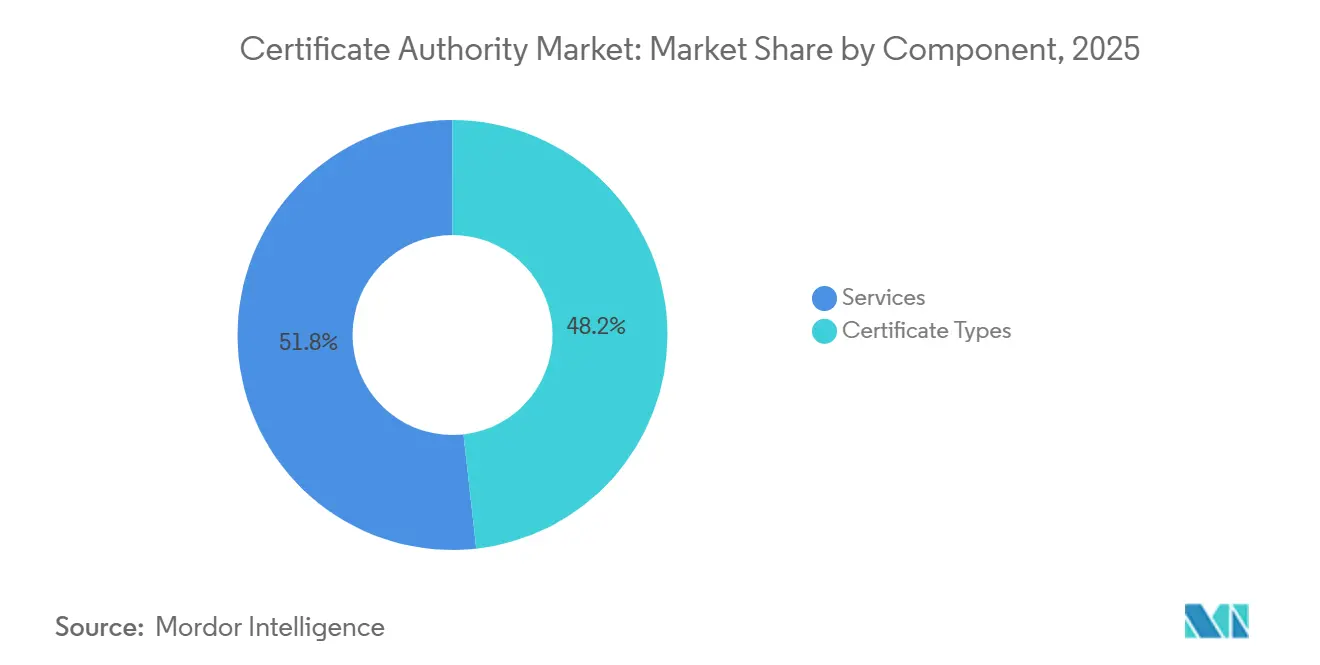

- By component, certificate types captured 48.24% of the certificate authority market share in 2025; services revenue is expected to lag as certificate types advance at an 11.71% CAGR through 2031.

- By organization size, large enterprises accounted for 63.47% of revenue in 2025, while small and medium enterprises are expanding at a 11.74% CAGR through 2031.

- By end-user vertical, BFSI led with a 28.91% share of the certificate authority market in 2025, whereas healthcare and life sciences are forecast to expand at a 12.36% CAGR through 2031.

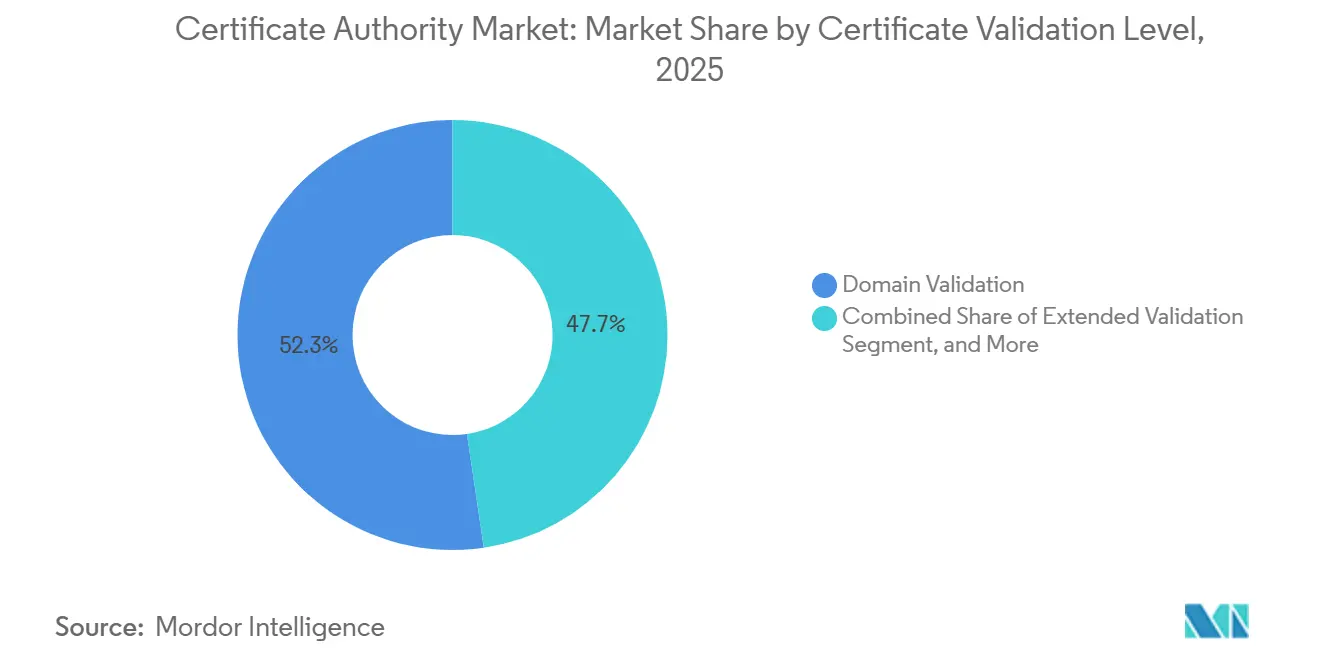

- By validation level, domain validation certificates accounted for 52.33% of the market in 2025, and extended validation certificates are rising at a 11.94% CAGR through 2031.

- By deployment model, cloud captured 57.83% of revenue in 2025 and is growing at a 11.78% CAGR over 2026-2031.

- By geography, North America commanded a 38.71% share in 2025, yet Asia-Pacific is registering the fastest regional CAGR at 12.39% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Certificate Authority Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulations and Compliance Mandates | +2.3% | Global, with early adoption in North America and EU | Short term (≤ 2 years) |

| Growing Awareness of Secure Web Access | +2.1% | Global | Medium term (2-4 years) |

| Expansion of Cloud-Based PKI Services | +1.9% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Surge in E-Commerce and Online Transactions | +1.8% | Global, with concentration in Asia-Pacific | Short term (≤ 2 years) |

| DevSecOps-Led Certificate Automation | +1.7% | North America, Europe | Long term (≥ 4 years) |

| Machine-Identity Demand in Zero-Trust Networks | +1.4% | Global, led by North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations and Compliance Mandates

Browser and platform owners are compressing certificate lifetimes at an unprecedented pace, with Ballot SC-063 proposing a 47-day maximum and Apple already enforcing a 45-day limit for several certificate classes.[1]SSL.com Team, “47-Day SSL/TLS Certificate Validity: What It Means for Your Business,” SSL.com, ssl.com PCI DSS 4.0 raises the compliance bar by tying payment processing authorization to automated certificate inventories and renewal alerts. In Europe, eIDAS 2.0 establishes a single market for qualified trust service providers, but it also introduces strict audit and liability rules that few issuers can meet. Healthcare regulators add further pressure; the FDA now requires medical device makers to embed firmware authentication and cloud connectivity certificates at the design stage. Together, these mandates make automated, policy-driven certificate management a board-level imperative rather than an optional security upgrade.

Growing Awareness of Secure Web Access

Modern browsers now block mixed content outright, turning HTTPS from a best practice into an operational prerequisite as Chrome recorded 95% of page loads over encrypted channels in 2025.[2]Google Transparency Report, “HTTPS Encryption on the Web,” Google, transparencyreport.google.com Certificate transparency logs process billions of public issuances each year, providing a near-real-time audit trail that deters mis-issuance and boosts user trust. Conversion-rate studies show e-commerce checkouts can lose 10-15% of sales when extended-validation indicators are absent, linking certificate choices directly to revenue. Remote learning and digital fundraising, two sectors that expanded sharply between 2020 and 2025, adopted SSL/TLS en masse to secure portals that replaced in-person interactions. As users internalize padlock cues as baseline hygiene, organizations without visible trust signals risk immediate reputational harm.

Expansion of Cloud-Based PKI Services

Hyperscalers now deliver public and private CAs as native cloud services, allowing developers to request certificates via API calls embedded in Terraform or CloudFormation scripts.[3]Google Cloud Product Page, “Certificate Authority Service,” Google Cloud, cloud.google.com Microsoft Cloud PKI ties certificate lifecycles to Azure Active Directory objects, merging authentication and encryption under a single policy engine. By 2025, Amazon Trust Services had issued certificates for more than 1 million domains, proving that scale is achievable without relying on the public CA root store. Entrust’s PKIaaS, launched in 2024, offers FIPS-validated hardware security modules in multitenant cloud environments, reducing capital expenses for enterprises retiring on-premises HSMs. While the shift slashes provisioning time from days to seconds, it also centralizes control within cloud platforms, increasing vendor lock-in risk and complicating cross-cloud migrations.

DevSecOps-Led Certificate Automation

A 47-day lifespan renders manual renewal cycles unworkable, pushing teams to embed certificate creation, testing, and revocation directly into CI/CD pipelines using tools such as cert-manager for Kubernetes. HashiCorp Vault’s PKI secrets engine issues short-lived certificates on demand, aligning credential lifetimes with container uptime and eliminating the need for long-term private-key storage. Teleport replaces static SSH keys with hourly certificates, shrinking the attack surface for infrastructure access. CloudBees added automated rotation steps to Jenkins pipelines, letting developers treat certificates as version-controlled artifacts subject to unit tests. Organizations with mature automation slash per-certificate costs and outage risks, while laggards face escalating compliance penalties and unplanned downtime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Security-Certificate Awareness in Emerging SMBs | -0.8% | Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Prevalence of Self-Signed Certificates | -0.6% | Global, concentrated in SMB segment | Short term (≤ 2 years) |

| Certificate Lifecycle Complexity at Hyperscale | -0.5% | Global, acute in large enterprises | Long term (≥ 4 years) |

| Regulatory Uncertainty on Post-Quantum Standards | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Security-Certificate Awareness in Emerging SMBs

Surveys in 2025 showed that 40% of SMB websites in India and Indonesia operated without SSL/TLS, citing cost and perceived complexity despite free options from Let’s Encrypt. Local IT resellers often charge USD 200-500 for manual installations, a prohibitive fee for firms earning under USD 50,000 annually. Documentation and support largely remain English-only, limiting uptake in Francophone Africa and parts of Southeast Asia. Government portals in these regions do not yet mandate HTTPS for business registration, removing the regulatory nudge that accelerated adoption in developed markets. The resulting trust gap constrains the expansion of the certificate authority market among the very businesses that stand to benefit most from online commerce.

Certificate Lifecycle Complexity at Hyperscale

Enterprises now manage portfolios exceeding 100,000 certificates across hybrid clouds, mainframes, and legacy applications, yet many still track expirations in spreadsheets, leading to public outages when unnoticed renewals lapse. Multiple root hierarchies and inconsistent policies complicate discovery, making it hard to standardize key lengths, algorithms, and revocation methods. Shorter lifetimes magnify the problem by tripling the number of annual renewals, stretching already limited security-operations headcount. Integrating lifecycle platforms with cloud IAM, container orchestration, and on-premise hardware security modules requires specialized expertise that many organizations lack. As visibility gaps persist, auditors and cyber-insurers now treat certificate governance as a critical control deficiency, creating financial and operational exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Automation Drives Certificate-Type Dominance

Certificate types held 48.24% of the certificate authority market share in 2025, a lead they are projected to retain as the sub-segment advances at an 11.71% CAGR through 2031. SSL/TLS certificates form the revenue core because every public-facing website now needs HTTPS, while code-signing certificates posted visibly faster unit growth after multiple 2024 supply-chain breaches highlighted the risk of unsigned binaries. Secure email certificates, once niche, are expanding in regulated healthcare and legal settings where S/MIME is mandated, and authentication client certificates are multiplying inside zero-trust networks that replace perimeter security with mutual TLS.

Services grow more slowly because enterprises now embed issuance and renewal directly into DevSecOps pipelines, shrinking demand for manual lifecycle outsourcing. Yet professional services remain vital for post-quantum migration planning, root-of-trust design, and cross-cloud hierarchy alignment, ensuring a continued, if smaller, services revenue pool. The revenue mix, therefore, tilts toward subscription contracts tied to automated renewal APIs, and vendors that bundle lifecycle orchestration with diverse certificate catalogs are best positioned to capture additional market share in the certificate authority market over the forecast period.

By Organization Size: SMB Acceleration Closes The Gap

Large enterprises captured 63.47% of the certificate authority market revenue in 2025, reflecting portfolios that easily exceed 100,000 active certificates across hybrid infrastructures. These organizations negotiate competitive volume pricing of less than USD 10 per certificate and deploy advanced policy engines to ensure the standardization of algorithms, certificate lifetimes, and key lengths across extensive multi-CA estates.

Small and medium enterprises are expanding at an 11.74% CAGR through 2031, the fastest pace among organization sizes, because SaaS providers and hosting platforms now automatically provision SSL/TLS certificates during onboarding. Free domain-validation options erode historic cost barriers, but awareness of extended validation and organization validation remains low, leaving an untapped pocket of certificate authority market share among SMBs. As browser warnings intensify and regulations trickle into emerging markets, automated issuance embedded in low-code website builders is expected to boost the SMB share of the overall certificate authority market.

By End-User Vertical: Healthcare Devices Boost Volumes

Banking, financial services, and insurance accounted for 28.91% of the certificate authority market share in 2025, driven by transaction signing, API authentication, and open-banking mandates that mandate mutual TLS. The critical need for seamless conversion-focused checkout processes, coupled with the increasing risk of regulatory penalties, is compelling banks and fintech companies to place a stronger emphasis on adopting high-assurance certificates. This strategic focus enables the preservation of premium pricing within this sector.

Healthcare and life sciences post the strongest 12.36% CAGR because the FDA now obliges device makers to embed certificates for firmware updates and secure telemetry. Each connected insulin pump or imaging modality represents a unique machine identity, alleviating the need for high-volume issuance that inflates the certificate authority market in healthcare faster than in any other vertical. Retail, telecom, and public-sector workloads follow closely, but none match the sheer surge of device certificates now embedded in connected medical equipment.

By Certificate Validation Level: Extended Validation Rebounds

Domain validation certificates held 52.33% of revenue in 2025, owing to ACME-enabled five-minute provisioning and zero manual paperwork. They continue to be the preferred choice for micro-sites, SaaS subdomains, and edge workloads, where the primary objective is to achieve exceptional speed and scalability. This preference persists even when it necessitates a certain level of compromise on brand assurance to meet performance demands.

Extended validation, although niche, is increasing at an 11.94% CAGR as financial institutions and high-traffic e-commerce sites re-adopt EV to counter sophisticated phishing and deepfake attacks. Organization validation sits between the two, offering faster issuance than EV yet higher assurance than DV, and is favored for B2B APIs. Ongoing browser interface changes may blur user-visible distinctions, but regulatory endorsements and insurance requirements are likely to preserve a revenue-relevant EV tier within the broader certificate authority market.

By Deployment Model: Cloud-Native Issuance Scales Rapidly

Cloud deployments accounted for 57.83% of certificate authority market revenue in 2025 and are growing at an 11.78% CAGR through 2031. Hyperscalers have incorporated certificate issuance capabilities directly into their infrastructure-as-code templates. This strategic integration allows developers to efficiently request certificates in conjunction with compute, storage, and networking resources, streamlining operations without requiring them to exit their CI/CD pipelines.

On-prem deployments are declining as a share of the certificate authority market, but they persist in industries with strict data-sovereignty laws or legacy SCADA environments. Hybrid models on-premises root CAs delegating to cloud subordinates are emerging as the pragmatic default for global enterprises seeking centralized policy control with elastic issuance capacity. Vendor lock-in and cross-cloud key portability will therefore shape procurement criteria as buyers look to protect long-term flexibility while still expanding the total certificate authority market for automated, short-lived credentials.

Geography Analysis

North America retained 38.71% of revenue in 2025, anchored by the United States' federal zero-trust mandates requiring device and workload certificates for every network segment. PCI DSS 4.0 enforcement added private-sector urgency, while Canada’s Pan-Canadian Trust Framework drove demand for cross-provincial identity credentials. Mexico’s fintech rules require mutual TLS for open-banking APIs, widening regional adoption beyond the United States. Together, these policies keep North America the largest absolute buyer of high-assurance certificates despite maturing penetration.

Asia-Pacific is advancing at a 12.39% CAGR, the fastest worldwide. China’s Financial Certification Authority issued more than 500 million certificates for e-commerce, banking, and public services by 2025, dwarfing regional peers. India’s Unified Payments Interface processes billions of API calls each day under Reserve Bank encryption mandates, requiring every participant bank to become a certificate subscriber. Japan’s Digital Agency upgrades the My Number Card ecosystem with qualified certificates, and South Korea pilots blockchain-based transparency logs to police mis-issuance. Cloud adoption, mobile wallets, and cross-border e-commerce are driving certificate volumes higher than in any other geography over the forecast horizon.

Europe sits between the two extremes, but regulatory depth makes it strategically vital. eIDAS 2.0, formalized in Regulation 2024/1183, forces every member state to accept qualified trust service providers across borders, expanding the addressable pool for high-assurance issuers. Germany tightened cryptographic baselines after 2024 vulnerabilities, while the United Kingdom’s post-Brexit framework obliges CAs to navigate dual rule sets. In South America, Brazil’s government-run PKI dominates issuance for tax and payroll filings, whereas Argentina and Chile move more slowly due to fragmented e-government budgets. Middle East and Africa growth relies on Gulf smart-government programs, but adoption in sub-Saharan Africa is still limited by bandwidth, cost, and low security awareness.

Competitive Landscape

The five largest commercial vendors, DigiCert, Sectigo, GoDaddy, GlobalSign, and Entrust, hold roughly 55-60% combined share, giving the sector a moderately consolidated profile. DigiCert’s USD 6.9 billion buyout by Clearlake Capital and TA Associates in 2024 signaled investor confidence in subscription revenue tied to automated renewals. Let’s Encrypt surpassed 4 billion active certificates in 2025, driving the marginal cost of domain validation products toward zero. As a result, premium growth now centers on high-assurance validation and lifecycle orchestration rather than basic issuance volume.

Hyperscalers are the most disruptive entrants. Amazon Trust Services provisions certificates solely for AWS workloads, Google Trust Services embeds issuance inside Google Cloud, and Microsoft Cloud PKI integrates with Azure Active Directory. These platforms shorten provisioning from hours to seconds and bundle costs into infrastructure bills, eroding the relevance of stand-alone CAs for cloud-native applications. Cloudflare’s SSL for SaaS further blurs the lines by enabling software vendors to outsource tenant-level certificate management, deepening vertical integration.

Strategic differentiation now depends on three levers: automation latency, post-quantum readiness, and domain expertise. Sectigo partners with chipmakers to embed device certificates during silicon fabrication, positioning for IoT scale, while Entrust focuses on the financial and government sectors, where regulation justifies premium pricing. Venafi and Keyfactor focus on machine-identity orchestration for Kubernetes and service-mesh traffic, capturing enterprises that issue millions of short-lived certificates per day. Browser root-program owners Google, Apple, Mozilla, and Microsoft retain veto power over issuance policy, demonstrated when Apple unilaterally adopted 45-day validity in 2025, quickly reshaping competitive economics. Private equity interest, nonprofit disruption, and hyperscaler integration, therefore, combine to keep rivalry intense even within a moderately concentrated field.

Certificate Authority Industry Leaders

DigiCert Inc.

Sectigo Ltd.

GoDaddy Group

GlobalSign K.K.

Asseco Data Systems SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DigiCert launched a Quantum-Ready Certificate Suite supporting hybrid classical-quantum algorithms, enabling enterprises to test migrations while retaining legacy compatibility.

- February 2026: SSL.com gained WebTrust certification for post-quantum issuance processes, becoming an early commercial CA with audited quantum-resistant operations.

- January 2026: Google Trust Services added private CA hierarchies within Google Cloud, removing the need for on-premise hardware security modules.

- January 2026: Buypass AS expanded to Nordic markets with eIDAS-qualified certificates for cross-border digital identity.

Global Certificate Authority Market Report Scope

The Certificate Authority Market Report is Segmented by Component (Certificate Types, and Services), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Vertical (BFSI, IT and Telecom, Retail and E-Commerce, Healthcare and Life Sciences, Government and Public Sector), Certificate Validation Level (Domain Validation, Organization Validation, Extended Validation), Deployment Model (On-Premise, and Cloud), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Certificate Types | SSL/TLS Certificates |

| Code-Signing Certificates | |

| Secure Email Certificates | |

| Authentication Client Certificates | |

| Services |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| IT and Telecom |

| Retail and E-Commerce |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Domain Validation |

| Organization Validation |

| Extended Validation |

| On-Premise |

| Cloud |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Certificate Types | SSL/TLS Certificates | |

| Code-Signing Certificates | |||

| Secure Email Certificates | |||

| Authentication Client Certificates | |||

| Services | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User Vertical | BFSI | ||

| IT and Telecom | |||

| Retail and E-Commerce | |||

| Healthcare and Life Sciences | |||

| Government and Public Sector | |||

| By Certificate Validation Level | Domain Validation | ||

| Organization Validation | |||

| Extended Validation | |||

| By Deployment Model | On-Premise | ||

| Cloud | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the certificate authority market expected to grow by 2031?

It is projected to expand from USD 232.31 million in 2026 to USD 397.14 million by 2031, registering an 11.32% CAGR over 2026-2031.

Which component currently drives the largest revenue share?

Certificate types, including SSL/TLS and code-signing certificates, captured 48.24% of revenue in 2025 and continue to outpace services.

Why is Asia-Pacific the fastest-growing region?

National PKI expansion in China, India’s payments modernization, and broad digital government investments are propelling a 12.39% regional CAGR through 2031.

What makes healthcare a rapid-growth end-user segment?

FDA guidance now requires medical devices to embed certificates for firmware authentication and secure communications, spurring a 12.36% CAGR for healthcare and life sciences.

How will shortened certificate validity affect enterprises?

Proposed 47-day lifetimes force automation of issuance and renewal, turning manual workflows into outage risks and favoring vendors with API-driven lifecycle platforms.

Are post-quantum certificates commercially available today?

Yes, vendors such as DigiCert and Cloudflare have launched hybrid classical-quantum certificates, letting organizations test migrations while staying compatible with existing clients.

Page last updated on: