Blockchain-as-a-Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

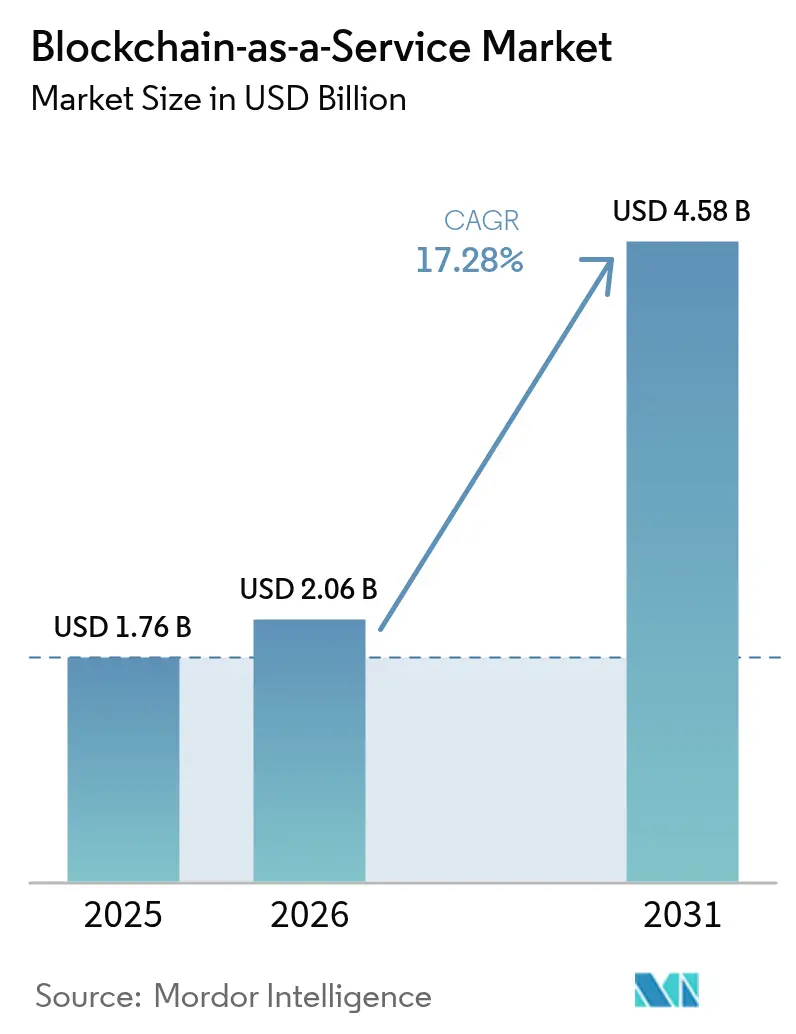

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 4.58 Billion |

| Growth Rate (2026 - 2031) | 17.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain-as-a-Service Market Analysis by Mordor Intelligence

The Blockchain-as-a-Service market size is expected to grow from USD 1.76 billion in 2025 to USD 2.06 billion in 2026 and is forecast to reach USD 4.58 billion by 2031 at 17.28% CAGR over 2026-2031. The Blockchain-as-a-Service market is gaining momentum as enterprises move from small-scale proofs of concept toward production deployments, spurred by clearer regulations and cloud providers that embed distributed-ledger tools within broader infrastructure bundles. Central-bank digital-currency pilots, especially the Bank for International Settlements’ mBridge project, are generating downstream demand for enterprise blockchain platforms.[1]Bank for International Settlements, “Project mBridge: Minimum viable product,” bis.org Cloud hyperscalers’ bundled offerings reduce procurement friction, while regulatory frameworks such as the European Union’s Markets in Crypto-Assets regulation legitimize enterprise spending.[2]European Union, “Markets in Crypto-Assets Regulation,” eur-lex.europa.eu North American sandbox programs and Asia Pacific’s state-funded tokenization initiatives further accelerate uptake. At the same time, ongoing talent shortages and protocol-level interoperability gaps remain watchpoints that could temper short-term growth.

Key Report Takeaways

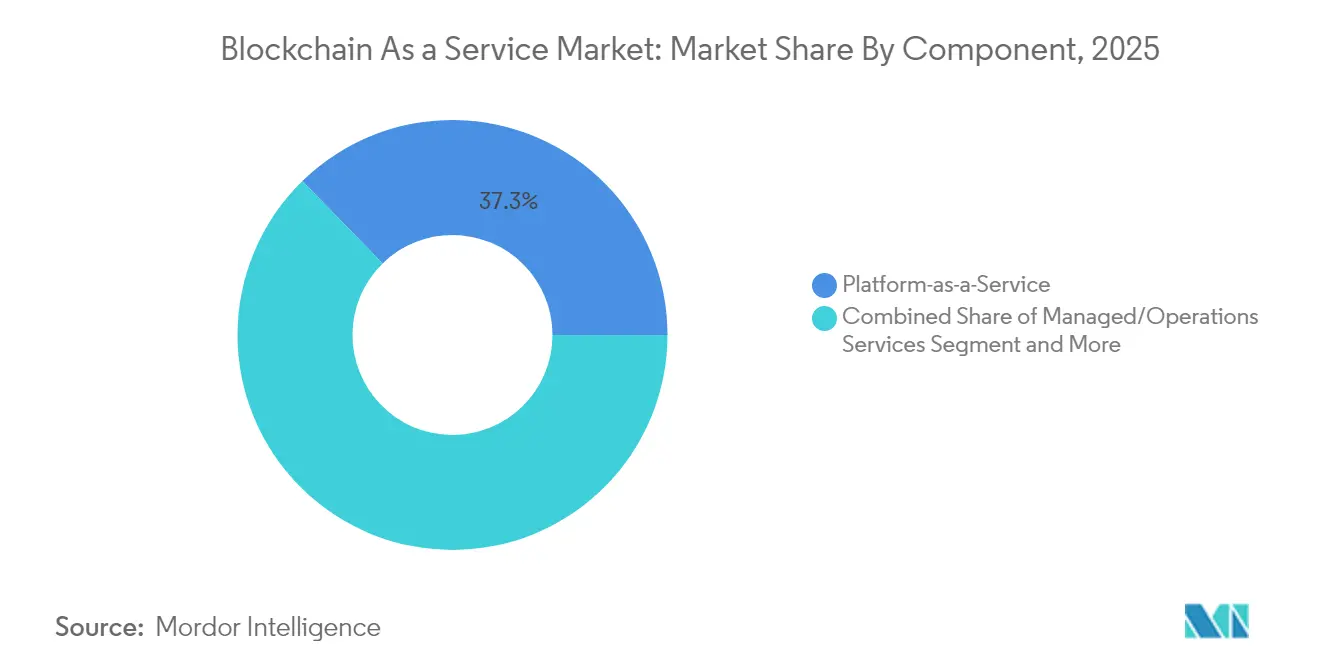

- By component, Platform-as-a-Service led with 37.30% revenue share in 2025, whereas Managed Services is forecast to expand at a 19.25% CAGR through 2031.

- By deployment model, Public Cloud captured 62.20% of the Blockchain-as-a-Service market share in 2025; Hybrid Cloud is projected to rise at a 21.35% CAGR to 2031.

- By organization size, Large Enterprises accounted for 60.60% of the Blockchain-as-a-Service market size in 2025, while Small and Medium Enterprises recorded the quickest growth at 23.90% CAGR.

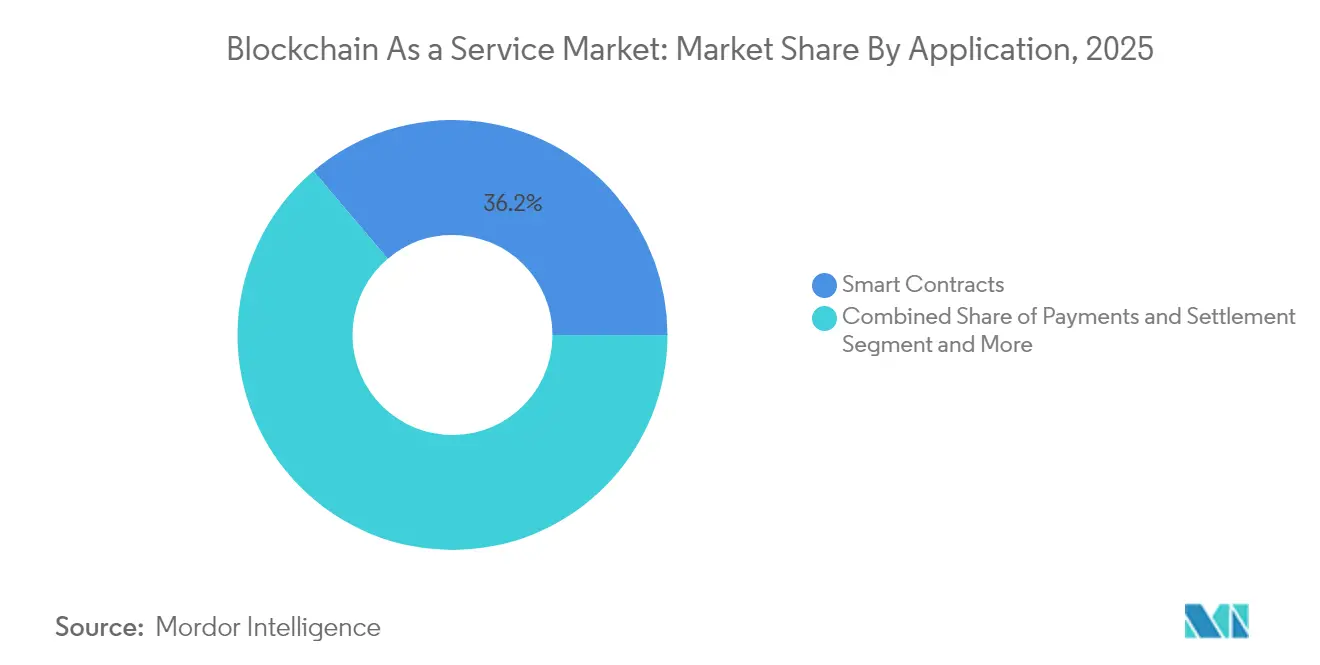

- By application, Smart Contracts commanded 36.20% of revenue in 2025, and Digital Identity and KYC is poised for a 24.70% CAGR through 2031.

- By end-user vertical, Banking, Financial Services, and Insurance held a 33.10% share in 2025; Healthcare and Life Sciences advanced fastest at 25.05% CAGR.

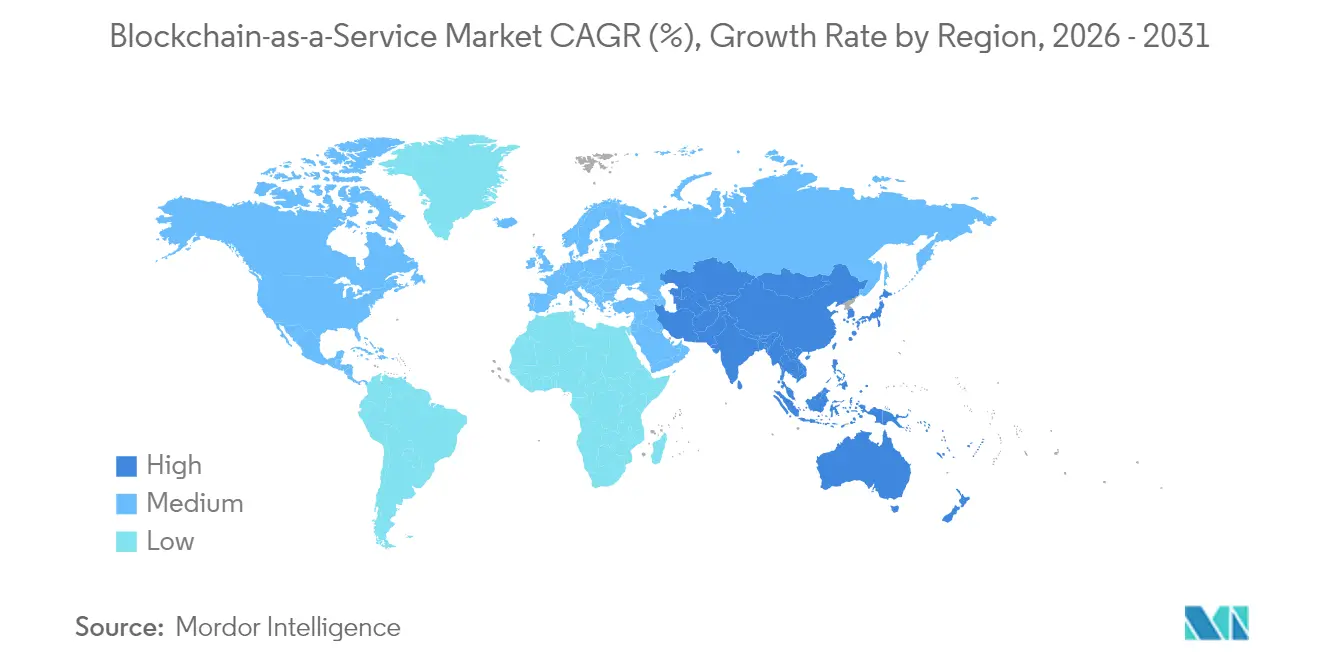

- By geography, North America led with a 40.40% share in 2025, whereas Asia Pacific shows the steepest trajectory at 18.20% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blockchain-as-a-Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for tamper-proof data integrity across regulated industries | +3.2% | Global, with concentration in North America and EU | Medium term (2–4 years) |

| Cloud hyperscalers bundling BaaS into broader X-as-a-Service stacks | +2.8% | Global, led by North America, expanding to APAC | Short term (≤ 2 years) |

| Gradual regulatory clarity on tokenization and stablecoins | +2.1% | EU, selective US jurisdictions | Medium term (2–4 years) |

| Central-bank sandbox programs sourcing BaaS back-ends | +1.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Explosion of enterprise-grade blockchain pilots post-2024 | +1.7% | Global | Short term (≤ 2 years) |

| Scope-3 emissions auditing via sustainability ledgers | +1.4% | EU, voluntary North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for tamper-proof data integrity across regulated industries

Health, finance, and pharmaceuticals increasingly adopt blockchain to meet stringent audit-trail and provenance mandates. Change Healthcare’s Hyperledger Fabric deployment already processes about 50 million daily transactions while preserving immutable logs.[3]Hyperledger Foundation, “Change Healthcare case study,” hyperledger.org European pharmaceutical rules that track medicine provenance drive similar uptake. Financial institutions cut compliance workloads by recording regulatory data on chains that regulators deem trustworthy under MiCA. These sector mandates position the Blockchain-as-a-Service market as a compliance enabler, particularly as auditors begin to prefer immutable records over traditional databases. Demand, therefore, scales with every new data-integrity policy in advanced economies.

Cloud hyperscalers bundling BaaS into broader X-as-a-Service stacks

Microsoft integrates blockchain, AI, and IoT on Azure, letting clients activate ledgers through familiar portals and existing contracts. Amazon Web Services and Google Cloud follow, while Kaleido’s Azure tie-up offers more than 500 pre-built APIs that snap into enterprise tools. Bundling cuts procurement cycles, especially for mid-market firms without deep cryptography skills, and keeps operating costs variable instead of capital-intensive. This packaging strategy keeps the Blockchain-as-a-Service market visible to every customer managing cloud workloads, making adoption an incremental, rather than transformative, decision.

Gradual regulatory clarity on tokenization and stablecoins

EU MiCA rules effective December 2024, describe licensing, capital, and disclosure obligations for stablecoin issuers, which reassures banks exploring on-chain settlement. Mastercard’s 2025 deal with Fiserv to embed FIUSD across its card network highlights how clear guardrails unlock mainstream pilots. Central-bank experiments such as BIS Project Agorá give private providers technical blueprints for compliant back-end services. Each milestone reduces legal uncertainty, spurring enterprises to commit multi-year budgets.

Central-bank sandbox programs sourcing BaaS back-ends

The Hong Kong Monetary Authority’s Project Ensemble invites commercial ledgers to provide wholesale settlement rails. Thailand’s Retail CBDC pilot and the Bank of England’s Digital Securities Sandbox set interoperability and performance benchmarks that Blockchain-as-a-Service vendors must meet. Compliance within these sandboxes signals quality to commercial users, creating a pipeline of reference deployments across Asia Pacific and beyond.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented standards and protocol interoperability gaps | -2.4% | Global, more acute for multi-region rollouts | Medium term (2–4 years) |

| Talent shortage in distributed-ledger engineering | -1.8% | Global, acute in North America and EU | Long term (≥ 4 years) |

| Uncertain jurisprudence on smart-contract enforceability | -1.3% | Global, varying by jurisdiction | Long term (≥ 4 years) |

| Rising cloud spend scrutiny dampening POC budgets | -1.1% | Global, cost-sensitive enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented standards and protocol interoperability gaps

IEEE and ISO continue to draft frameworks, yet no universal plug-and-play standard exists, forcing enterprises to custom-build cross-chain connectors iso.org. Sensors-journal research shows such architectures add complexity and new attack surfaces. Multinationals therefore hesitate to scale pilots across borders, which slows cumulative contract flow into the Blockchain-as-a-Service market. Until dominant interoperability protocols mature, vendors must allocate road-map resources to proprietary bridges that elevate costs and lengthen implementation timelines.

Talent shortage in distributed-ledger engineering

Blockchain roles in the United States command mean salaries near USD 146,250, reflecting scarcity.[4]Algorand Foundation, “Blockchain developer salary report,” algorand.foundationCryptography, consensus, and smart-contract skills remain rare in mainstream computer-science programs, so enterprises over-rely on small pools of senior engineers. Project delays and consultant premiums inflate the total cost of ownership, especially for small firms. This bottleneck affects the Blockchain-as-a-Service industry globally and is likely to persist beyond 2028 because university pipelines lag commercial demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Managed Services Scale Faster Than Core Platforms

Platform-as-a-Service contributed 37.30% revenue in 2025, underpinned by integrated development environments and configurability that attract large corporations. Managed Services, however, grows fastest at 19.25% CAGR as organizations seek turnkey operations, security patching and 24/7 uptime without running nodes themselves. Large multinational treasury teams cite tangible savings; Siemens cut bank accounts by half and saved USD 20 million each year after migrating to managed ledgers for cross-border liquidity. Consulting and implementation work remains essential to bridge legacy ERP systems and to meet sector-specific regulations in finance and healthcare.

Enterprises also adopt Infrastructure-as-a-Service when they need granular control over consensus settings yet still prefer cloud billing. Meanwhile, software-as-a-service toolkits expose APIs that abstract smart-contract compilation, lowering entry barriers for small developers. Rising compliance workloads make immutable audit trails a default requirement, so even risk-averse boards now approve subscriptions. This persistent demand anchors the Blockchain-as-a-Service market across both greenfield and brownfield deployments.

By Deployment Model: Hybrid Cloud Balances Control and Flexibility

Public Cloud captured 62.20% of the Blockchain-as-a-Service market share in 2025 because hyperscalers provide elasticity and high service-level agreements. Still, Hybrid Cloud is on track for a 21.35% CAGR as financial institutions and pharmaceutical firms hold sensitive data on-premises to satisfy residency laws under MiCA and similar policies. Hybrid topologies keep production chains behind firewalls while using public cloud for development sandboxes, which speeds iteration.

Private Cloud persists where data sovereignty or classified workloads prohibit any external infrastructure. The European Union’s new operational-resilience rules further motivate contingency planning, making hybrid designs attractive. As a result, the Blockchain-as-a-Service market sees consistent architectural diversity: enterprises swap workloads between environments in response to cost audits or new compliance directives, ensuring long-run demand for orchestration tools.

By Organization Size: SMEs Harness User-Friendly Platforms

Large Enterprises generated 60.60% of the Blockchain-as-a-Service market size in 2025, reflecting deep budgets and multi-region supply chains. Small and Medium Enterprises, though, expand adoption at 23.90% CAGR thanks to template-driven platforms and managed nodes that hide complexity. Mid-sized importers can now trace shipments on a consortium ledger without recruiting cryptographers. Research shows blockchain can cut infrastructure costs by 43% in supply-chain scenarios, savings that resonate with cash-focused SMEs.

Enterprise pioneers such as Walmart demonstrated how traceability slashes recall times from days to seconds. SMEs emulate these benefits on narrower scopes, for example single-product lines. Cloud subscription pricing aligns with variable demand, allowing gradual expansion instead of disruptive capex. Talent shortages remain a challenge, but marketplace plug-ins and no-code smart-contract tools continue to lower the threshold for entry.

By Application: Digital Identity Advances at High Speed

Smart Contracts retained 36.20% revenue in 2025, underpinning automated invoicing, escrow and compliance verification workflows. Digital Identity and KYC accelerates at a 24.70% CAGR through 2031 because regulators tighten customer-due-diligence rules. The United Nations’ 2024 digital-ID rollout confirmed blockchain’s suitability for interoperable credentials across agencies. Supply-chain traceability also climbs as sustainability reporting and consumer provenance demands rise.

Payments and settlement workflows benefit from central-bank pilots that require robust ledger infrastructure. Stablecoin integrations such as Mastercard’s FIUSD project showcase live payment volumes on permissioned chains. Governance, risk and compliance applications close the loop by automating reporting, using immutable logs to speed audits and reduce manual reconciliations. Combined, these use cases diversify the Blockchain-as-a-Service market and cushion it against single-segment downturns.

By End-User Vertical: Healthcare Leads Growth Curve

Banking, Financial Services and Insurance owned 33.10% revenue in 2025, leveraging blockchain for 24/7 cross-border payments, trade-finance document tracking and digital-asset custody. Citi’s Token Services for Cash illustrates how tokenized deposits streamline treasury operations and meet near-time settlement demands. Healthcare and Life Sciences exhibits a 25.05% CAGR through 2031 as regulators enforce end-to-end drug traceability and push for interoperable patient records.

Manufacturing and energy companies implement ledgers to verify equipment provenance and carbon-credit transactions, aligning with emerging Scope-3 reporting duties. The public sector explores citizen ID, voting, and land registry pilots to cut fraud and improve transparency. Each vertical’s regulatory pain points map neatly to blockchain attributes, ensuring broad adoption momentum inside the Blockchain-as-a-Service market.

Geography Analysis

North America continued to dominate in 2025 with a 40.40% Blockchain-as-a-Service market share, buoyed by deep venture funding such as Digital Asset’s USD 135 million round led by Goldman Sachs and Citadel. US-based hyperscalers integrate ledger tools into mainstream cloud menus, allowing quick uptakes among existing clients. Regulatory sandboxes in several states accelerate production pilots, though nationwide policy fragmentation still injects compliance uncertainty that slows multi-state rollouts.

Asia Pacific records the steepest growth at an 18.20% CAGR through 2031. Government-backed CBDC and tokenization projects in Singapore and Hong Kong create visible proof points, drawing banks and fintechs onto commercial platforms. Manufacturing hubs across Japan, South Korea and China deploy blockchains for supply-chain and sustainability reporting use cases, leveraging intra-Asia trade corridors. Regional talent pools expand through university blockchain labs, helping offset developer shortages seen elsewhere.

Europe benefits from MiCA’s uniform rules that became fully effective in December 2024. Automotive, luxury and food companies implement provenance solutions to satisfy regulators and consumers, exemplified by Renault’s XCEED supply-chain systeM. The European Central Bank’s advocacy for digital-assets market integration encourages banks to modernize back offices with distributed-ledger infrastructure, sustaining near-term contract flow. Emerging markets in the Middle East and Africa experiment with blockchain for financial inclusion and carbon credit registries, yet overall adoption remains nascent due to limited technical capacity.

Regulatory Landscape

Regulation for Blockchain-as-a-Service (BaaS) is tightening around crypto-asset services, data protection, and cross-border operational standards, which is shifting BaaS procurement toward vendors that can evidence controls for regulated production deployments. In the European Union, Regulation (EU) 2023/1114 (MiCA) moved the market toward licensing, disclosure, and governance requirements for crypto-asset service providers, with a mandatory authorization deadline of 01 July 2026. That timeline has made compliance-ready hosting, monitoring, and audit logging more central in enterprise buying decisions.

Standards activity is also becoming a practical procurement filter for BaaS platforms and managed services. ISO published ISO/TS 23516:2026 (12 March 2026) on interoperability frameworks for blockchain and distributed ledger technology, while China released GB/T 47677.1-2026 (25 May 2026, implemented from 01 September 2026) specifying general technical requirements for BaaS operations. In the United States, NIST issued the initial public draft of IR 8500A (19 May 2026) on blockchain-based secure software asset management (BloSS@M), and the U.S. Congress introduced H.R. 1664 (Deploying American Blockchains Act). Together, these actions point to continued policy focus on national coordination and best practices, which feeds into enterprise risk assessments for BaaS deployments.

Value Chain Analysis

The BaaS value chain begins with infrastructure and hosting, including hyperscaler cloud and bare-metal providers. It then moves through blockchain middleware such as node and RPC management, orchestration layers, rollup-as-a-service, and oracle and key-management services, before reaching enterprise application layers spanning smart contracts, traceability, digital identity and KYC, payments and settlement, and governance, risk, and compliance.

Value creation is concentrating in orchestration and managed operations, where customers face scaling, security hardening, and integration challenges. Deutsche Telekom MMS joining the NEAR ecosystem Enterprise Node Operator program (November 2024), Reliance Jio partnering with Polygon Labs to integrate blockchain infrastructure into network services (January 2025), and stc Bahrain partnering with Nirvana Labs to extend Web3 hosting capabilities into its data centers (January 2025) show how infrastructure and middleware are being tied to industry use cases. Persistent bottlenecks around interoperability and production performance are also pushing adoption toward managed architectures and RaaS-style abstractions that reduce operational overhead and support predictable service levels for regulated workflows.

Competitive Landscape

The Blockchain-as-a-Service market shows moderate fragmentation. Hyperscalers compete on breadth: IBM claims more than 14,000 blockchain-related patent filings with 10,000 granted, fortifying its IP moat. Microsoft Azure and Amazon Web Services embed ledgers into developer-tool pipelines, locking in users through integrated identity, analytics, and security services. Specialized vendors such as Kaleido and R3 focus on low-code orchestration and compliance modules that cater to regulated sectors.

Financial institutions increasingly take equity stakes in infrastructure firms. Deutsche Bank joined JPMorgan and Standard Chartered in Partior’s USD 80 million Series B to secure influence over multi-currency settlement networks. Technology differentiation gravitates toward throughput, with Teranode architecture demonstrating 3 million transactions per second via horizontal sharding Vendors also explore blockchain-AI convergence for real-time fraud analytics and automated contract summarization. Despite consolidation pressure, plentiful niche opportunities remain in cross-chain gateways and ESG data orchestration, keeping competitive intensity high

Blockchain-as-a-Service Industry Leaders

Microsoft Corporation

Hewlett-Packard Enterprise

IBM Corporation

SAP SE

Stratis

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace centers on production-grade managed infrastructure for regulated financial workflows. Institutions want blockchain capabilities embedded into familiar rails and operational models, rather than standalone proofs of concept. In 2026, named initiatives reflect this shift: OP Labs launched OP Enterprise (January 2026) as a production-grade managed blockchain infrastructure offering, SWIFT progressed its blockchain-based shared ledger to MVP implementation (March 2026) for tokenized deposit payments interoperability, and JPMorgan expanded Kinexys to support additional Asia-Pacific currencies (June 2026). These changes widen the addressable requirement for BaaS across identity, observability, key management, and policy controls aligned with bank-grade settlement and treasury use cases.

Opportunities also expand around custody, tokenization, and multi-party settlement integrations that rely on hybrid architectures and clear governance. BNY's collaboration with Finstreet Limited and ADI Foundation in Abu Dhabi Global Market (May 2026) highlights institutional demand for custody and market infrastructure, while DTCC commencing live production trading of tokenized securities (July 2026) shows tokenization concepts moving into real-market trading. For BaaS vendors, these proof points translate into demand for managed environments that support permissioned networks, compliance and reporting modules, and interoperability tooling to connect legacy systems with tokenized instruments and cross-border payment workflows.

Recent Industry Developments

- July 2026: Alchemy launched Validator-as-a-Service for the permissioned Canton network, taking on node operations and associated fee management for institutional participants. The release pushes BaaS deeper into capital-markets style networks where operational reliability and standardized controls are procurement prerequisites for financial institutions.

- June 2026: Blockchain.com announced an expansion of its institutional operations into Brazil, positioning a cross-border liquidity and settlement solution for enterprise customers. The move broadens competitive coverage in a major Latin American market where institutions are seeking managed infrastructure for payments and settlement workflows.

- June 2025: Mastercard partnered with Fiserv to embed the FIUSD stablecoin across its global payment rails, enabling programmable on-chain commerce. By linking a mainstream card network with stablecoin-based settlement capabilities, the partnership supported enterprise pilots that rely on managed blockchain services for compliance, integration, and transaction orchestration.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from cloud-delivered blockchain capabilities that help organizations build, deploy, and run blockchain networks and applications without owning the underlying infrastructure. It includes platform access, tooling, and provider-delivered services that support setup, integration, and ongoing operations.

Scope exclusions: We exclude on-premises self-hosted blockchain software that is sold as a standalone license and not delivered as a managed cloud service.

Segmentation Overview

- By Component

- Platform-as-a-Service (PaaS)

- Infrastructure-as-a-Service (IaaS)

- Software-as-a-Service (SaaS) SDKs and APIs

- Consulting and Implementation Services

- Managed/Operations Services

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Smart Contracts

- Supply-Chain Traceability

- Digital Identity and KYC

- Payments and Settlement

- Governance, Risk and Compliance

- Others

- By End-User Vertical

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- IT and Telecom

- Retail and E-commerce

- Manufacturing

- Energy and Utilities

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- GCC (Saudi Arabia, UAE, Qatar, etc.)

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public signals that track enterprise cloud adoption and where blockchain pilots are moving into production. We refer to World Bank and OECD material for macro and digital-economy context, and we use NIST-related standards references as adoption cues that influence enterprise requirements.

To avoid drifting into adjacent categories, we also scan ISO materials and peer-reviewed journals that discuss permissioned networks, smart contracts, and interoperability. For commercial visibility, we then review public company filings, earnings call transcripts, investor presentations, and reputable press coverage to map product packaging, monetization patterns, and common contract structures used for managed blockchain offerings. In parallel, we use a paid subscription for company financials and news to track funding cycles, major contract announcements, and product launches that can change near-term demand. The sources listed here are illustrative, and other public references were also used to collect data, validate assumptions, and clarify unclear points.

Primary Interviews and Surveys

Primary conversations confirm what buyers actually pay for in a BaaS contract and how adoption differs by regulated industries, cloud preference, and deployment complexity. We speak with platform providers, systems integrators, and enterprise users, so pricing logic, attach rates for managed services, and renewal behavior can be checked across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 50% |

| Mid tier: 58% | Functional/Unit leaders: 39% | EMEA: 30% |

| Smaller Players: 15% | Managers: 49% | Americas: 20% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where cloud service spending and enterprise blockchain adoption signals are translated into an addressable demand pool for managed blockchain delivery. Once the demand pool is formed, it is narrowed using market-specific inputs such as the share of permissioned deployments, typical project-to-production conversion rates, average contract tenures, and the split between platform fees and implementation plus operations services. Building the path step by step helps make it clear what is counted and why.

To keep totals realistic, selective bottom-up checks are used, such as sampling common subscription price points, estimating active enterprise deployments by vertical, and validating service attach rates through channel feedback. Gaps that show up in smaller geographies or early-stage buyer cohorts are handled with conservative proxies, then re-tested in follow-up calls. For forecasting, scenario analysis is used with a base case anchored to expert expectations on cloud migration pace, regulatory and compliance demand, and integration workload trends, which then informs how quickly revenues scale year by year.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as enterprise cloud adoption direction, frequency of production deployments, and the pace of announced blockchain partnerships that translate into commercial contracts. If a country, vertical, or service line shows an unusual jump, the assumptions are reviewed again and the relevant inputs are stress-tested before sign-off. A second analyst review is completed to ensure calculations, currency handling, and time-series logic remain consistent.

The report is refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes, pricing shifts, or large contract wins that can move the near-term outlook. Before delivery, a final pass is done so the client receives the latest updated view and the narrative stays aligned with the data tables.

Mordor Intelligence's Blockchain As A Service Market Size Measured Against Other Published Estimates

Published market values for blockchain as a service can vary widely because scope is defined differently and the year used for sizing is not always the same. Differences also come from how providers treat bundled cloud charges, services revenue, and currency timing, which can change totals even when the description sounds similar.

Some published figures roll a broad set of blockchain-related cloud and consulting revenues into one number, which can push the total beyond pure BaaS contracts. For Mordor Intelligence, the count is limited to BaaS revenue tied to delivering blockchain capabilities as a managed cloud service, and adjacent blockchain technology spending that is not sold as a service is kept out.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.06 B (2026) | |

| Global Consultancy A | USD 3.25 B (2024) | Uses a different base year and assumes faster early adoption, and the service basket appears to include broader deployment and advisory revenues that may overlap with non-BaaS blockchain programs. |

| Industry Publisher B | USD 11.30 B (2024) | Applies a wide definition that can bundle development tools, infrastructure services, and consulting solutions under one umbrella, which increases the chance of double counting across platform fees and services. |

The spread across the table is mainly explained by year alignment and what is bundled into the service basket. With the scope tied to managed cloud delivery, and then cross-checking price and adoption assumptions with practitioner feedback, the final number stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current value of the Blockchain-as-a-Service market?

The market is valued at USD 2.06 billion in 2026 and is projected to reach USD 4.58 billion by 2031.

Which segment grows fastest within the Blockchain-as-a-Service market?

Managed Services shows the highest component-level growth at a 19.25% CAGR through 2031.

Why is Hybrid Cloud deployment accelerating?

Enterprises adopt Hybrid Cloud to keep sensitive data on-premises for regulatory reasons while using public cloud capacity for development and scaling, driving a 21.35% CAGR.

Which region offers the strongest growth outlook?

Asia Pacific expands at an 18.20% CAGR due to government-backed CBDC pilots and large-scale tokenization projects in markets such as Singapore and Hong Kong.

What are the main restraints hindering market expansion?

Fragmented interoperability standards and a global shortage of skilled blockchain engineers remain the primary constraints, reducing the forecast CAGR by a combined 4.2%.

How concentrated is competition in the Blockchain-as-a-Service market?

The space scores 4/10 for concentration, with cloud hyperscalers leading but many specialist vendors still capturing significant shares.

Page last updated on: