Blockchain In Telecom Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

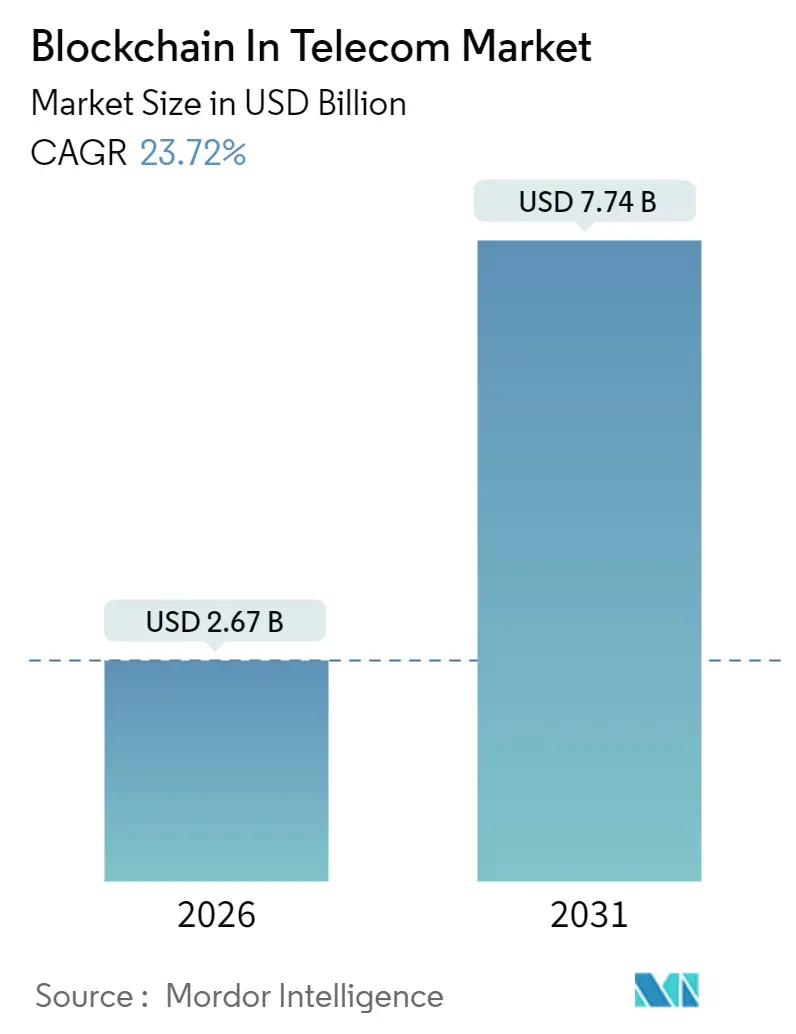

| Market Size (2026) | USD 2.67 Billion |

| Market Size (2031) | USD 7.74 Billion |

| Growth Rate (2026 - 2031) | 23.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain In Telecom Market Analysis by Mordor Intelligence

The blockchain in telecom market size reached USD 2.67 billion in 2026 and is projected to climb to USD 7.74 billion by 2031, advancing at a 23.72% CAGR during the forecast period. Momentum stems from carriers moving production workloads from isolated pilots to enterprise-grade deployments that streamline roaming settlement, combat fraud, and harden identity verification rails. Consortium-led standards, hyperscaler BaaS offerings, and 5G network-slicing mandates all shorten launch cycles, while the shift toward permissioned ledgers mitigates competitive secrecy concerns. North America’s caller-ID authentication rules, Asia-Pacific’s 5G rollouts, and Europe’s eSIM regulations anchor geographic demand. Service integration skills shortages, energy efficiency limits, and incomplete interoperability frameworks temper the growth trajectory but do not alter the market’s structural upswing. Vendor competition remains moderate as equipment makers, enterprise-software incumbents, and blockchain specialists pursue distinct niches without material overlap.

Key Report Takeaways

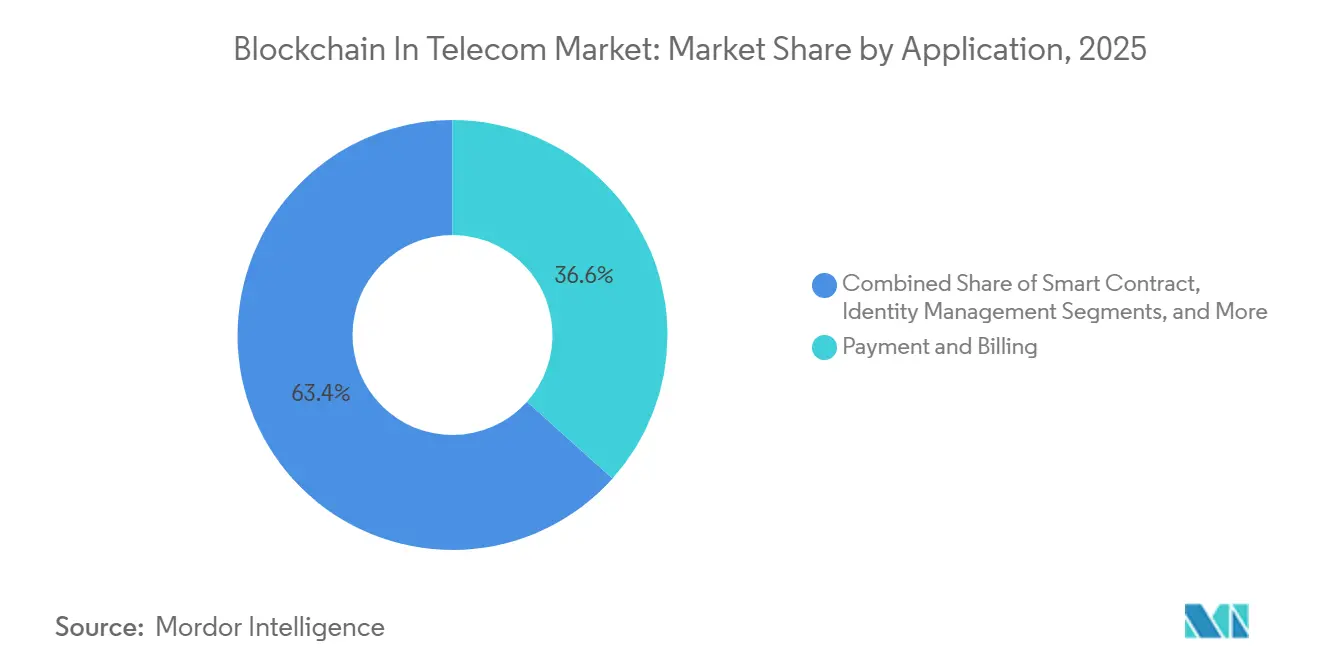

- By application, Payment and Billing held 36.63% revenue share in 2025, whereas Smart Contract use cases are set to expand at a 25.81% CAGR through 2031.

- By component, Platform captured 57.33% of revenue in 2025, while Services are forecast to accelerate at a 24.55% CAGR to 2031.

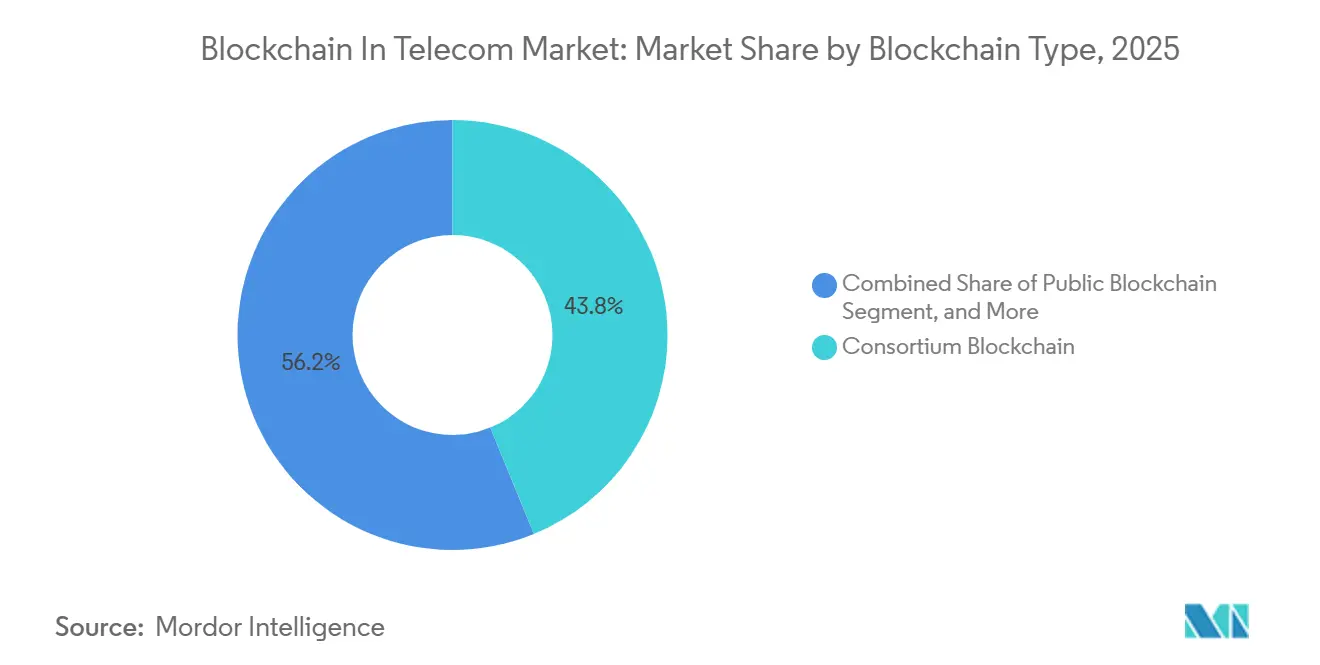

- By blockchain type, Consortium networks led with 43.82% share in 2025.

- By deployment type, Cloud accounted for 60.26% of installations in 2025 and is rising at a 26.03% CAGR.

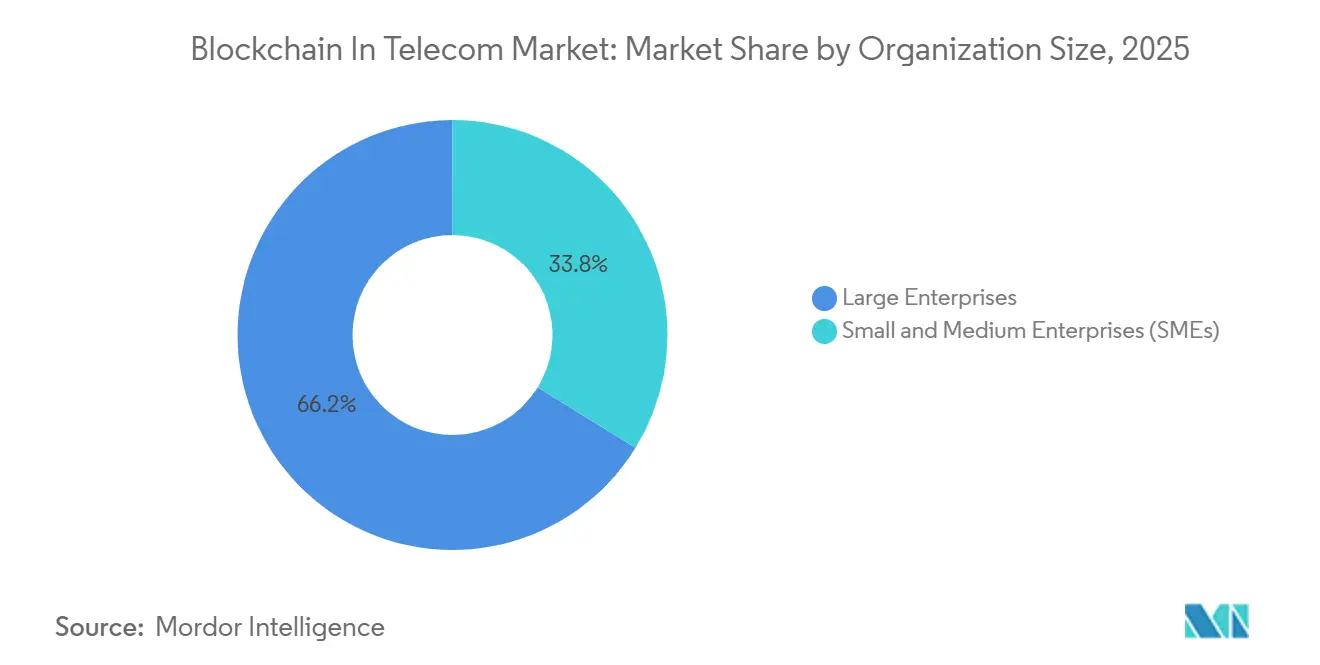

- By organization size, Large enterprises represented 66.21% spending in 2025; SMEs are forecast to expand at a 24.06% CAGR.

- By geography, North America commanded 37.12% revenue share in 2025, while Asia-Pacific is projected to post the fastest 28.17% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Blockchain In Telecom Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Focus on Telecom Fraud Mitigation | +4.2% | Global, with acute pressure in North America and Europe due to regulatory penalties | Medium term (2-4 years) |

| Rising Demand for Secure 5G Network Slicing | +3.8% | APAC core markets (China, South Korea, Japan), spill-over to Europe | Medium term (2-4 years) |

| Increasing Roaming-settlement Efficiency Initiatives | +2.9% | Global, led by GSMA member operators in Europe, Middle East, and APAC | Short term (≤2 years) |

| Regulatory Push for SIM and Device-identity Protection | +3.5% | North America and EU, expanding to Middle East and Africa | Long term (≥4 years) |

| Emergence of Telco-focused Blockchain-as-a-service (BaaS) | +4.1% | North America, Europe, and advanced APAC markets | Medium term (2-4 years) |

| Monetization of Carrier Edge Nodes via Blockchain Marketplaces | +2.7% | North America, Western Europe, and select APAC hubs (Singapore, South Korea) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Focus on Telecom Fraud Mitigation

Global fraud losses touched USD 39.89 billion in 2024, pushing operators to adopt immutable ledgers that record call-detail data at source and block SIM-box bypass in real time. The United States STIR/SHAKEN rules require cryptographic caller-ID signatures, and several Tier-1 carriers now trial blockchain registries because centralized databases invite credential-stuffing attacks. Ericsson’s pilot with Batelco cut roaming fraud 34% within six months, proving ledger-based shared intelligence delivers measurable gains. Fraud-mitigation needs favor consortium designs that let rivals share risk data without exposing proprietary subscriber records.

Rising Demand for Secure 5G Network Slicing

Network-slice contracts guarantee latency and bandwidth for autonomous vehicles or remote surgery. ITU-T standard Y.3087 sets distributed-ledger hooks for slice life-cycle logs, cementing blockchain as the trust layer for multi-operator SLAs. South Korea’s 2025 rule makes ledger logging compulsory in public-sector slices, accelerating adoption by SK Telecom and KT Corporation.[1]Ministry of Science and ICT, “5G Network Slicing Regulations,” MSIT, msit.go.kr Smart contracts also automate penalty payments once performance drifts, eliminating multi-week reconciliation cycles that eroded operator margins.

Increasing Roaming-settlement Efficiency Initiatives

ETSI’s PDL 030 specification for eSIM profile management elevates permissioned ledgers as the default platform to thwart SIM-swap fraud, which facilitated USD 68 million in cryptocurrency thefts in 2023. Zero-knowledge proofs now let operators meet KYC obligations while shielding user data. China’s licensing regime places blockchain identity platforms in the same critical-infrastructure tier as 5G base stations, tilting market share toward vetted domestic vendors.

Regulatory Push for SIM and Device-identity Protection

Carriers with idle edge sites convert spare compute into validator capacity, turning capex into yield. Deutsche Telekom earned EUR 1.2 million (USD 1.3 million) in 2024 staking rewards by running NEAR nodes, adding 0.5-1.0% incremental yield. Oracle and Microsoft embed telecom templates and compliance modules, shrinking deployment windows from months to weeks and attracting SME operators priced out of bespoke builds.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Industry-wide Interoperability Standards | -3.1% | Global, with acute friction in multi-vendor environments across Europe and APAC | Medium term (2-4 years) |

| Scalability and Energy-efficiency Concerns | -2.8% | Global, particularly in regions with carbon-pricing mandates (EU, California) | Long term (≥4 years) |

| High Integration Costs with Legacy OSS/BSS | -2.3% | Mature markets (North America, Europe) with entrenched legacy systems | Short term (≤2 years) |

| Limited Telco-grade Smart-contract Audit Expertise | -1.6% | Global, with talent concentrated in North America and select European hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Industry-wide Interoperability Standards

Only three of TM Forum’s 58 Open APIs cover blockchain, forcing carriers to bankroll bespoke middleware that translates transactions between Hyperledger Fabric and Ethereum sidechains. MEF’s orchestration spec defers ledger bindings until at least 2027, making early adopters fear stranded assets. IEEE’s interoperability project is still a draft, so operators hedge bets with parallel integrations that inflate operating costs and curb ROI.

Scalability and Energy-efficiency Concerns

Proof-of-Work chains draw more electricity than Argentina, breaching telecom Scope 2 carbon targets. Proof-of-Stake slashes energy use yet risks validator centralization, evidenced when four entities held 51% of Ethereum’s stake in 2024. Hyperledger Fabric’s 3,500 TPS ceiling compels carriers to batch settlement data, clashing with five-nines availability standards. Possible EU carbon tariffs on digital services from 2026 could penalize operators that fail to migrate to greener consensus models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Smart Contracts Automate Inter-carrier Settlements

Payment and Billing led revenue with a 36.63% share in 2025, but Smart Contract workflows are on track for a 25.81% CAGR as operators embed SLA logic directly into Solidity code in the blockchain in telecom market. The shift reflects recognition that blockchain’s advantage lies in automating roaming and spectrum-sharing agreements rather than mirroring legacy payment rails. Identity-management projects align with ETSI’s eSIM rules, and caller-ID registries anchored in blockchain deliver STIR/SHAKEN compliance, trimming fraud without central honeypots.

Emerging Connectivity Provisioning ledgers now port numbers in under 10 minutes in South Korea, versus 48 hours under legacy HLR systems. Network-slicing orchestration follows ITU-T Y.3087 guidance, logging every parameter change for legal defensibility. Oracle’s pre-built templates slash integration from nine months to six weeks, accelerating uptake among mid-tier carriers that lack deep OSS teams.

By Component: Services Surge as Audit Expertise Becomes Critical

Ledger platforms dominated 57.33% of 2025 revenue as operators sought architectural control in the blockchain in telecom market. However, Services are projected to post a 24.55% CAGR because fewer than 2,000 engineers combine telecom domain mastery and blockchain skills worldwide. Guardtime recorded a 340% jump in audit mandates, signaling that contract-security validation is becoming non-negotiable. Hardware nodes remain the smallest slice yet are indispensable for 5G edge scenarios needing sub-20-millisecond validation latency.

Consultancies and hyperscalers are filling the talent void. IBM and Accenture launched certification tracks in 2025, while AWS, Azure, and Google Cloud embed telecom governance packs that let carriers comply with GDPR, China’s Data Security Law, and other mandates straight out of the box. This feature set propels cloud platforms to grow 1.5 percentage points faster than on-premises builds.

By Blockchain Type: Consortia Balance Transparency with Secrecy

Consortium networks secured 43.82% revenue share in 2025 thanks to governance models that let competitors vote on upgrades while masking subscriber data through zero-knowledge proofs. Hybrid ledgers should deliver the fastest 23.96% CAGR by 2031 as operators adopt dual-layer architectures that store sensitive data on private sidechains while anchoring proofs to public chains for regulator audits.

Public chains remain limited to ancillary revenue plays, such as Deutsche Telekom’s NEAR validator nodes rather than core traffic handling. Private chains appeal to vertically integrated incumbents, such as AT&T, that seek internal process gains without relying on peer collaboration in the blockchain in telecom market.

By Deployment Type: Cloud Platforms Accelerate Time-to-Market

Cloud installations constituted 60.26% of 2025 deployments and are poised to advance at a 26.03% CAGR in the blockchain in telecom market. Azure Confidential Ledger, launched in 2024, dropped deployment cycles to eight weeks by integrating with Azure Active Directory and Key Vault, while Oracle moved to consumption-based pricing that aligns cost with transaction volume.

On-premises remains obligatory in countries with strict data-sovereignty laws, yet integration can stretch to 24 months. With 78% of new 2025 projects landing on hyperscalers, the economics favor cloud, especially when operators bundle blockchain with 5G edge nodes to monetize low-latency compute.

By Organization Size: SMEs Adopt API-first Services

Large operators directed 66.21% of spend in 2025, but SMEs will outpace them at a 24.06% CAGR through 2031. Twilio’s USD 0.02-per-lookup blockchain number-verification API enables carriers with under 5 million users to comply with STIR/SHAKEN without running their own nodes. Uniform regulatory pressures mean smaller players cannot postpone adoption, and API-based models cut total cost by up to 70% compared with bespoke builds.

Large incumbents will still invest heavily, yet entrenched OSS estates and multi-vendor complexity slow rollout. Middleware retrofits can run USD 5-10 million per deployment, explaining why Tier-1 operators post a slower 22.1% CAGR despite bigger absolute budgets in the blockchain in telecom market.

Geography Analysis

North America led with 37.12% revenue in 2025 after FCC caller-authentication rules compelled U.S. carriers to deploy ledger-based registries that cut robocalls by 28% within a year. Canada drafted parallel guidelines in 2025, and Mexico mandated blockchain number portability in 2024, trimming porting windows from 48 hours to six hours.[2]Instituto Federal de Telecomunicaciones, “Blockchain Number Portability Mandate,” IFT, ift.org.mx

Asia-Pacific will record the fastest 28.17% CAGR through 2031. Reliance Jio integrated blockchain into nationwide 5G slices, while South Korea’s compulsory ledger logging for public projects accelerates uptake. China issued 1,847 blockchain service licenses to telecom firms by late-2025, equating distributed ledgers with essential infrastructure. Japan’s Rakuten Mobile uses blockchain to timestamp spectrum-sharing events with incumbents, shortening dispute cycles from six weeks to three days.

Europe held 28.5% share in 2025, propelled by GDPR-aligned eSIM ledger standards from ETSI that Vodafone, Orange, and Deutsche Telekom embraced. Middle East and Africa posted a 25.3% CAGR, with South Africa’s blockchain SIM-registration mandate slashing fraudulent activations 41% in nine months.[3]Independent Communications Authority of South Africa, “SIM Registration Blockchain Mandate,” ICASA, icasa.org.za South America’s growth centers on Brazil, where Anatel’s portability reforms whittled transfer time to four hours.

Regulatory Landscape

Regulation and standards activity for blockchain in telecom is being shaped less by single-country rules and more by telecom-centric technical recommendations and industry governance frameworks that make permissioned DLT auditable, interoperable, and manageable across operators. ITU-T has published multiple DLT recommendations that map to telecom operating requirements, including F.751.8 (July 2023) on DLT frameworks aligned to regulatory needs such as privacy and accountability in permissioned environments, and Y.3210 (September 2024) supporting DLT integration into fixed, mobile, and satellite convergence architectures.

In 2025, ITU-T expanded the implementable guidance set with F.751.23 (March 2025) for DLT interoperability requirements, Y.2348 (March 2025) defining DLT-based functional architecture for network resource sharing, and F.751.24 (March 2025) specifying DLT-based authorization services. ITU-T M.3166.1 (October 2025) added protocol-neutral management interface requirements for blockchain systems (configuration, performance, fault, and log management), while GSMA governance and documentation for Blockchain for Wholesale Roaming provides an industry operating model to help carriers align multi-operator settlement and data-sharing designs to consistent controls.

Value Chain Analysis

The value chain starts with standards bodies and industry associations defining interoperable processes (GSMA Distributed Ledger Technology Group, ITU-T, ETSI ISG PDL), then moves to platform and infrastructure providers delivering permissioned ledger stacks and managed services (hyperscalers and enterprise software vendors). Telecom operators implement use cases across wholesale roaming settlement, fraud intelligence sharing, identity and eSIM-related workflows, and network resource sharing. System integrators and security specialists connect DLT to OSS/BSS, automate smart-contract driven settlement, and provide smart-contract assurance and operational monitoring aligned to telco-grade availability and audit requirements.

Downstream, carriers operationalize shared networks and data utilities through consortia, exchanges, and bilateral implementations that connect multiple operators, clearing agents, and roaming hubs. The chain increasingly includes roaming and settlement intermediaries aligning to GSMA BCE and wholesale roaming governance, plus specialized fraud and identity networks that share and consume indicators and attestations. Interoperability and integration remain the main friction points, since operator deployments span different stacks, requiring middleware, cross-chain communication layers, and privacy-preserving techniques (for example, zero-knowledge proofs) to keep shared ledgers compliant with data-protection obligations while enabling multi-party workflows.

Competitive Landscape

No vendor exceeds 12% share, yielding a moderately fragmented arena where equipment suppliers, enterprise-software providers, and blockchain natives seldom collide in the blockchain in telecom market. Huawei tops patent counts with 127 filings on low-latency consensus, while IBM focuses on smart-contract audit tooling. Deutsche Telekom’s validator strategy offers a third path: carriers monetizing spare capacity as blockchain infrastructure landlords.

Edge-computing monetization is the emergent battleground. Syntropy secures Border Gateway Protocol traffic via blockchain, addressing USD 2.8 billion in annual hijacking losses.[4]Syntropy Technologies, “Blockchain-based BGP Security,” Syntropy, syntropynet.com Hyperscalers threaten to compress software-vendor margins by bundling managed ledger services with compliance packs that small firms cannot replicate economically.

As ITU-T codifies more standards, risk-averse operators gravitate toward established vendors with turnkey integration. Yet niche firms that solve specific telecom pain points, such as contract audits or zero-knowledge subscriber proofs, retain room to expand alongside, rather than against, incumbents.

Blockchain In Telecom Industry Leaders

Blockchain Foundry Inc.

Huawei Technologies Co., Ltd

Microsoft Corporation

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity sits in wholesale roaming modernization, as carriers and roaming intermediaries move from legacy clearing and settlement toward BCE-aligned, auditable processes that can be automated with smart contracts. In March 2026, Syniverse announced it had become the first BCE agent to achieve GSMA BCE 2.0 compliance, which underscores how the ecosystem is formalizing operational and financial workflows that can be paired with ledger-based audit trails and automated reconciliation in multi-operator environments.

Another whitespace is the trust layer for 5G-advanced and Non-Terrestrial Networks (NTN), where telecom-grade security and anomaly detection must work across domains and providers. In July 2026, Keysight Technologies and Sateliot were selected by the European Space Agency for a three-year program focused on blockchain-anchored anomaly detection for 5G NTN, pointing to continued investment in DLT-backed assurance for satellite-cellular convergence. Standardization also reduces implementation ambiguity for operators and vendors: ITU-T published Y.2348 (March 2025) for DLT-based network resource sharing architecture and F.751.23/F.751.24 (March 2025) for interoperability and authorization, creating clearer design patterns for multi-party resource sharing, identity/authorization, and compliant cross-operator data exchange beyond single-operator pilots.

Recent Industry Developments

- July 2026: Keysight Technologies and Sateliot were selected by the European Space Agency for a three-year project to develop blockchain-anchored anomaly detection capabilities for 5G Non-Terrestrial Networks. The program ties blockchain trust and auditability to security monitoring for satellite-cellular convergence, a growing requirement for high-volume IoT connectivity across heterogeneous access networks.

- October 2025: Orange partnered with IBM to deploy blockchain roaming settlement across 18 African subsidiaries, targeting faster and more consistent dispute resolution across its intra-group wholesale footprint. The rollout highlights how operators are moving beyond pilots to multi-country operational deployments where shared ledger governance reduces reconciliation friction between affiliates and partners.

- August 2024: Microsoft launched Azure Confidential Ledger, adding managed, tamper-evident ledger capabilities integrated with core Azure identity and key management services. This lowered the barrier for telecom operators and their suppliers to deploy auditable, permissioned ledger components within existing cloud governance models, supporting faster implementation of settlement, identity, and compliance logging use cases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from blockchain platforms, related services, and enabling hardware used specifically for telecom workflows, such as identity, billing, fraud controls, and network operations, across public, private, consortium, and hybrid implementations.

Scope exclusions: Crypto trading, consumer wallets used only for investing, and non-telecom blockchain projects (such as pure banking or retail traceability) are not counted in this market.

Segmentation Overview

- By Application

- Identity Management

- Payment and Billing

- Smart Contract

- Connectivity Provisioning

- Fraud Management and Authentication

- Network Management and Slicing Orchestration

- By Component

- Platform

- Services

- Hardware Nodes and Gateways

- By Blockchain Type

- Public Blockchain

- Private Blockchain

- Consortium Blockchain

- Hybrid Blockchain

- By Deployment Type

- On-premises

- Cloud-based

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with getting the telecom and digital infrastructure context right, since blockchain adoption in this industry depends on network rollouts, compliance pressure, and enterprise digitization budgets. We referred to public sources such as ITU telecom indicators, national telecom regulators for licensing and subscriber metrics, FCC datasets for US market signals, and OECD digital economy statistics to anchor the demand environment.

To connect the technology piece, we also reviewed sources such as NIST publications on cybersecurity, ISO and ETSI material on security and telecom standards, and peer reviewed papers that discuss blockchain use cases in OSS/BSS and identity. Company filings, investor presentations, reputable press, and a paid subscription for company financials and news were used to confirm solution focus and commercial traction signals. This list is illustrative, and we also used other public sources for data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary inputs were used to pressure test assumptions that desk sources rarely spell out, especially what counts as telecom grade deployment versus pilots and bundled contracts. We spoke with people across operators, system integrators, and technology providers, and coverage was balanced across APAC, EMEA, and the Americas so regional maturity and pricing patterns could be checked consistently.

The respondent mix also helped us triangulate where blockchain projects are being operationalized versus where they remain in proof-of-concept or limited-service rollouts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 38% |

| Mid tier: 50% | Functional/Unit leaders: 31% | EMEA: 37% |

| Smaller Players: 14% | Managers: 57% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach, where telecom IT and network transformation spend signals are filtered into blockchain addressable pools by use case readiness (identity management, payment and billing, fraud management and authentication, connectivity provisioning, smart contracts, and network management). Those pools are then translated into value by applying adoption ranges and typical pricing structures for platform subscriptions, services effort, and hardware nodes and gateways.

To keep totals realistic, we corroborated the output using selective bottom-up approximations, including sampled deal values discussed in interviews, channel checks on platform and services mixes, and a sanity check of implied spend per operator for different regions. Key inputs used in the model included 5G and network slicing rollout pace, roaming and settlement modernization needs, fraud and authentication intensity, cloud migration levels in OSS/BSS, and the share of deployments shifting from on-premises to cloud-based setups. When bottom-up signals were missing for smaller countries, we used peer market proxies built from subscriber scale and operator count, then reviewed those assumptions with experts.

Forecasting relied on scenario analysis supported by a simple multivariate regression, where adoption and pricing were linked to the indicators above and then adjusted based on interview guidance on project conversion from pilots to production. Assumptions were kept transparent so a reader can repeat the math with updated inputs each year.

Data Validation & Update Cycle

Validation was done through multiple checks so outputs did not drift from real telecom spending behavior. We compared the modeled market values against independent signals such as telecom capex and IT spend trends, public network rollout indicators, and the expected mix of platform versus services revenue, and we investigated any sharp jumps before sign-off.

A second analyst review is completed for structure, math, and consistency across regions and deployment types, and experts are re-contacted when an assumption materially changes or when new evidence conflicts with earlier inputs. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulation changes or step shifts in telecom cloud adoption. Before delivery, a final pass is performed so the latest public information is reflected in both the numbers and the narrative.

Mordor Intelligence's Telecom Blockchain Market Size Compared With Other Published Estimates

Published market values for blockchain in telecom can look far apart even when they talk about similar use cases, because the year used, what gets counted as revenue, and the treatment of pilots versus production projects are not always aligned. Currency timing and whether services and enabling hardware are included also creates differences that are easy to miss if the scope is not spelled out.

Evidence like application level adoption (identity, payments and billing, OSS/BSS processes, and connectivity provisioning) and the expected platform to services mix are the checks that keep Mordor Intelligence tied to production deployments across platform, services, and hardware nodes and gateways. That is why some smaller 2024 point estimates and very high 2031 projections do not match this study period and scope choices.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.67 B (2026) | |

| Global Consultancy A | USD 1.20 B (2023) | Uses an earlier base year and a faster growth window (2024 to 2031), which can amplify totals when pilot activity is treated as scalable deployments and when pricing uplift is applied aggressively. |

| Research Aggregator B | USD 0.65 B (2024) | Starts from a smaller 2024 point estimate and applies a very high CAGR to 2031, and the write-up provides limited clarity on whether platform, services, and enabling hardware are all counted consistently across regions. |

The spread in the table mainly comes from base year selection and what is considered billable, telecom specific revenue versus broader or earlier stage activity. By keeping the scope anchored to telecom applications and verifying adoption and price logic with interviews, our estimate stays traceable to clear inputs that can be revisited as the market matures.

Key Questions Answered in the Report

What revenue level will the Blockchain in Telecom market reach by 2031?

Forecasts place the market at USD 7.74 billion by 2031, reflecting a 23.72% CAGR from 2026 to 2031.

Which application is growing fastest?

Which application is growing fastest?

Why do consortium blockchains dominate telecom deployments?

They balance data-sharing needs with confidentiality, capturing 43.82% revenue share in 2025.

How do cloud deployments compare with on-premises?

Cloud led with 60.26% of 2025 installations and is expanding at a 26.03% CAGR thanks to built-in compliance modules.

Which region will post the highest growth through 2031?

Asia-Pacific is expected to record a 28.17% CAGR, driven by 5G rollouts and supportive regulations.

What is the primary technical restraint?

Lack of interoperability standards trims CAGR by an estimated 3.1%, forcing operators to maintain costly middleware.

Page last updated on: