Blockchain In Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.4 Billion |

| Market Size (2031) | USD 68.23 Billion |

| Growth Rate (2026 - 2031) | 73.06% CAGR |

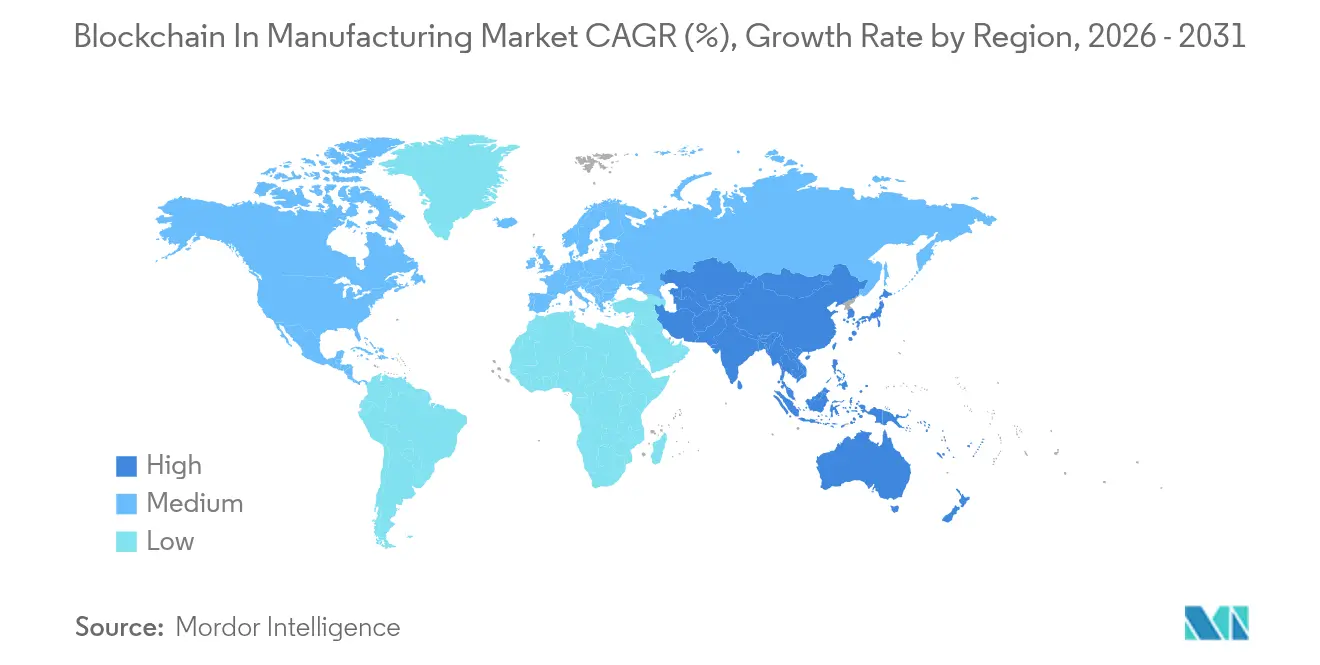

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain In Manufacturing Market Analysis by Mordor Intelligence

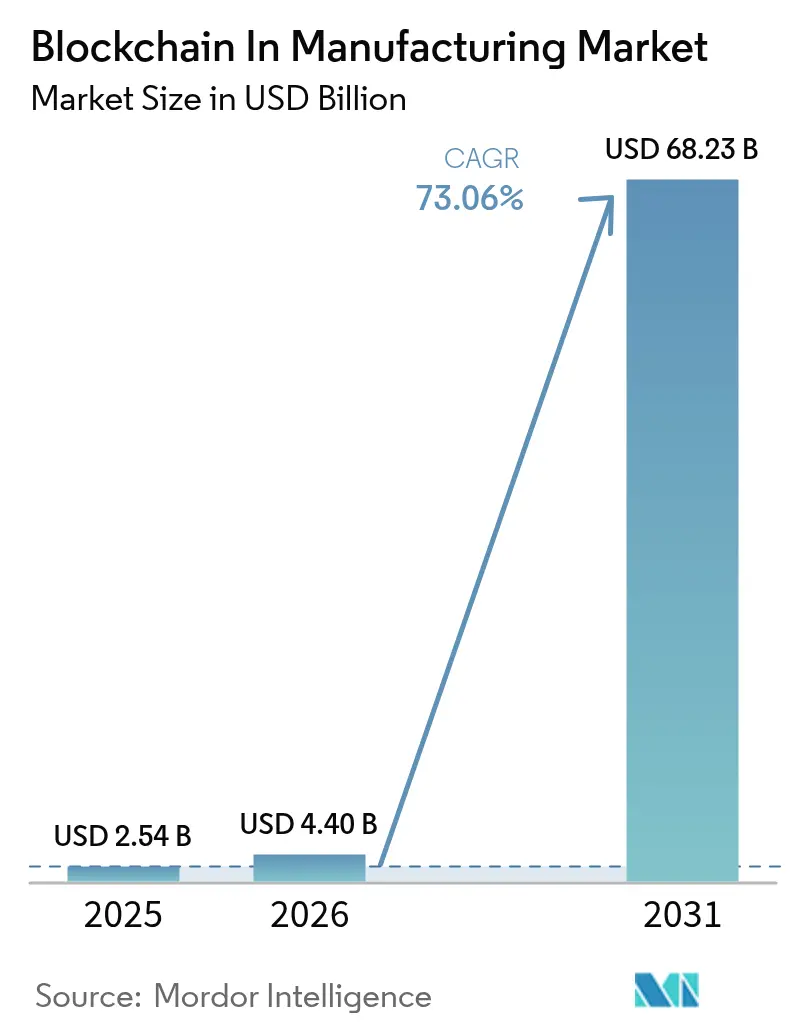

The Blockchain In Manufacturing Market size was valued at USD 2.54 billion in 2025 and estimated to grow from USD 4.4 billion in 2026 to reach USD 68.23 billion by 2031, at a CAGR of 73.06% during the forecast period (2026-2031).

Rising deployment of immutable ledgers for batch provenance, anti-counterfeiting, and equipment tokenization is accelerating the transition from pilot projects to enterprise-wide rollouts. Heightened regulatory scrutiny, especially under the Drug Supply Chain Security Act, is compelling manufacturers to adopt distributed ledgers that automate serialization and recall management. Equipment-as-a-service initiatives are unlocking new revenue streams, while cloud-based Blockchain-as-a-Service (BaaS) platforms lower entry barriers for small and mid-sized factories. Although fragmentation in standards and shortages of blockchain-skilled operational-technology talent temper near-term adoption, strategic partnerships between cloud hyperscalers and industrial OEMs are closing capability gaps.

Key Report Takeaways

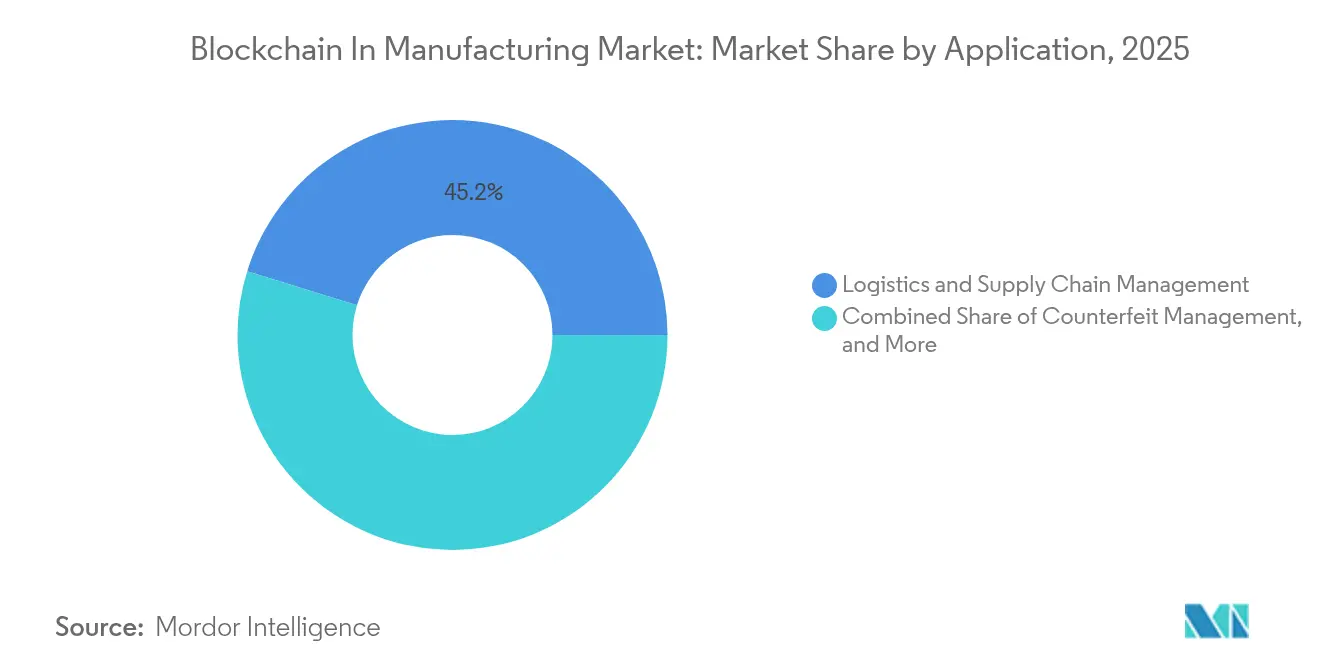

- By application, logistics and supply-chain management led with 45.20% of the blockchain in the manufacturing market share in 2025, whereas quality control and compliance applications are set to expand at a 74.20% CAGR through 2031.

- By end-user vertical, the automotive sector held 30.60% share of the blockchain in manufacturing market size in 2025, while the pharmaceutical and life sciences segment records the fastest CAGR at 75.60% to 2031.

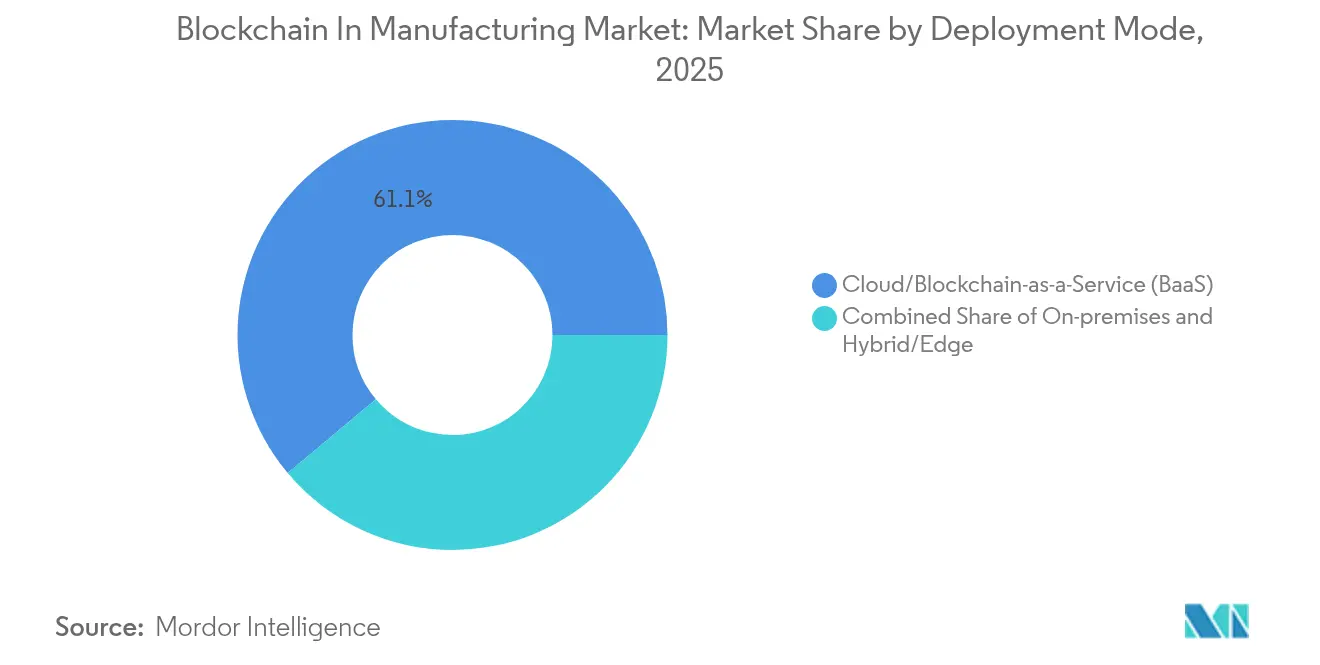

- By deployment mode, cloud-based BaaS platforms commanded 61.10% share of the blockchain in manufacturing market size in 2025; hybrid and edge approaches demonstrate the strongest 74.80% CAGR outlook.

- By blockchain type, private/permissioned led 57.80% of the blockchain in the manufacturing market share in 2025, whereas the public type of blockchain is set to expand at a 73.85% CAGR through 2031.

- By geography, North America accounted for 43.80% of the blockchain in manufacturing market share in 2025, whereas Asia Pacific is projected to advance at a 75.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Blockchain In Manufacturing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating adoption of BaaS across discrete manufacturing | +18.50% | Global, North America & Europe lead | Medium term (2–4 years) |

| Supply-chain provenance and traceability mandates | +16.20% | Global; strongest in North America & EU | Short term (≤ 2 years) |

| Demand for counterfeit mitigation in high-value components | +14.80% | Asia Pacific & North America | Medium term (2–4 years) |

| Tokenization enables equipment-as-a-service models | +12.30% | North America and Europe, spreading to the Asia Pacific | Long term (≥ 4 years) |

| Integration with additive manufacturing for secure part genealogy | +8.7% | North America and Europe | Long term (≥ 4 years) |

| Privacy-preserving zero-knowledge-proof pilots for IP protection | +5.9% | Global, high-IP industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Adoption of BaaS Across Discrete Manufacturing

Cloud-delivered BaaS now represents 61.8% of implementation preferences among discrete manufacturers, a share propelled by turnkey environments that eliminate the need for specialized node management. Microsoft’s integration of blockchain telemetry into its Fabric analytics suite allows users to query production-line events alongside enterprise data, reducing system-integration time by 35%[2]Microsoft Corp., “Microsoft Fabric Adds Blockchain Telemetry,” microsoft.com. Cost savings combine with simplified DevOps to ensure that BaaS gains traction in automotive, electronics, and industrial equipment factories that require rapid onboarding yet stringent uptime.

Supply-Chain Provenance and Traceability Mandates

The FDA extended its Food Traceability Rule deadline yet reaffirmed blockchain’s suitability for immutable lot-level reporting requirements. Parallel EU Digital Product Passport rules reinforce the need for distributed records across every product lifecycle phase. Pharmaceutical, aerospace, and consumer electronics producers are embedding serialization data onto shared ledgers to automate recall, thereby trimming manual audit costs by 28%.

Demand for Counterfeit Mitigation in High-Value Components

Counterfeiting exposes aerospace and automotive producers to multi-billion-dollar safety liabilities. Merck’s security-pigment markers combined with blockchain proofs cut fraudulent returns by 60% in pilot runs. As component pedigree moves on-chain, manufacturers report net revenue gains of 2-5% from diverted grey-market sales.

Tokenization Enabling Equipment-as-a-Service Models

Smart-contract-driven usage meters let OEMs shift from capital sales to performance-based billing. Pearson Packaging Systems achieved a 17% year-one margin uplift by monetizing runtime data captured on a permissioned ledger. Predictive maintenance alerts generated from tokenized digital twins reduced downtime by 22%, bolstering the business case for blockchain-enabled servitization.

Restraints Impact Analysis of Blockchain In Manufacturing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented standards and interoperability gaps | -12.40% | Global, pronounced in multi-vendor chains | Short term (≤ 2 years) |

| Limited blockchain talent in OT environments | -8.70% | Global, acute in Asia Pacific & emerging markets | Medium term (2–4 years) |

| Rising energy-use concerns for on-chain traceability | -6.3% | Europe & North America | Medium term (2–4 years) |

| Uncertainty around post-quantum security requirements | -4.8% | Global; defense & critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Standards and Interoperability Gaps

The absence of universal data models forces suppliers to build costly middleware bridges for each trading partner. GS1 and ISO working groups are drafting common schemas, yet adoption lags fast-moving implementation deadlines. Consortium-based pilots in automotive and chemicals signal progress but remain pockets rather than norms.

Limited Blockchain Talent in OT Environments

Deloitte’s 2025 Smart Manufacturing Survey shows 65% of factories cite blockchain skills scarcity as their primary hurdle, a rate higher than for AI or 5G deployments[1]Deloitte, “2025 Smart Manufacturing Survey,” deloitte.com . Bridging IT-OT cultures requires retraining control-system engineers in smart-contract logic, a process that stretches average pilot timelines by six months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Blockchain In Manufacturing Market Segment Analysis

By Application:

Quality Control Gains MomentumQuality control and compliance tools are projected to post a 74.20% CAGR to 2031, outpacing logistics management despite the latter’s 45.20% hold on the blockchain in manufacturing market share in 2025. Pharmaceutical firms running FDA serialization pilots report 30% faster deviation resolution when batch histories sit on a distributed ledger. Smart-contract workflows that auto-issue audit certificates replace paper record-keeping, cutting compliance hours by 40%. Second-wave applications include predictive maintenance logs and warranty adjudication, where immutable histories lower dispute rates. Counterfeit detection remains central as luxury-grade chemical tags feed authenticity hashes into public ledgers, enhancing consumer trust. As use cases multiply, the blockchain in the manufacturing market registers significant traction across both greenfield and brownfield plants.

Quality systems also form the backbone for emerging intellectual-property protection schemes in additive manufacturing, where zero-knowledge proofs confirm design compliance without revealing trade secrets. Electronic-component makers integrate on-device cryptographic signatures with the ledger, strengthening recall precision. This convergence of quality, compliance, and anti-counterfeiting accelerates enterprise interest in interoperable platforms, reinforcing the blockchain in the manufacturing market growth narrative.

By End-User Vertical:

Pharmaceutical AccelerationAutomotive factories dominated revenue with 30.60% in 2025, reflecting extensive part traceability obligations and mature Industry 4.0 investments. Nonetheless, life-sciences producers will expand the blockchain in the manufacturing market size for their segment at a 75.60% CAGR through 2031 as serialization, cold-chain tracking, and patient-level provenance become mandatory under global health regulations. Drug makers collaborating with IBM and Merck reported 25% faster recall execution during simulated audits. Aerospace and defense integrators adopt secure part genealogy ledgers for 3D-printed components, mitigating tampering risks. Consumer-electronics brands embed warranty tokens into products to streamline after-sales service, while food and beverage processors deploy farm-to-fork tracking to satisfy sustainability audits. Collectively, vertical diversification broadens the blockchain in the manufacturing industry footprint beyond early movers.

By Deployment Mode:

Hybrid Edge EmergenceCloud services captured 61.10% of 2025 revenue, illustrating strong early demand for managed stacks. Yet hybrid and edge frameworks will log a 74.80% CAGR to 2031 as factories embed lightweight nodes directly on equipment to meet sub-second latency thresholds. Siemens and Minima demonstrated that device-level validation upholds data integrity even when connectivity falters, an advantage crucial for high-speed robotics lines. Edge nodes process 90% of transactions locally before anchoring summaries to cloud chains, reducing bandwidth costs while preserving audit trails. On-premises installations persist where data sovereignty rules prevail, particularly in defense sectors, but their growth remains modest. The shift to hybrid architectures positions the blockchain in the manufacturing market for broader adoption across latency-sensitive operations.

By Blockchain Type:

Public Network Growth and Interoperability FocusPrivate and permissioned networks held 57.80% revenue share in 2025, driven by governance control requirements. Public chains, however, will expand at 73.85% CAGR as proof-of-stake frameworks ease energy burdens and zero-knowledge protocols conceal sensitive data on open ledgers. Firms leverage the liquidity and ecosystem tools of established public networks while anchoring confidential payloads off-chain. Consortium models fill the gap for sector-specific needs, such as automotive parts passports. Cross-chain bridges under development by standards bodies allow manufacturing events logged on private chains to synchronize with public ecosystems, creating unified visibility. As interoperability matures, stakeholders anticipate that public-network adoption will reshape cost structures and scalability expectations across the blockchain in the manufacturing market.

Geography Analysis

North America Blockchain In Manufacturing Market

North America held 43.80% of 2025 revenue owing to FDA mandates, established cloud infrastructure, and strong venture capital backing for ledger startups. Pharmaceutical serialization and aerospace part pedigree requirements drove early proofs that have since scaled to multi-plant deployments. State-level incentives further supported SME adoption.

APAC Blockchain In Manufacturing Market

Asia Pacific registers the highest 75.20% CAGR forecast between 2026 and 2031, reflecting sweeping digitization initiatives such as China’s industrial blockchain pilots and Japan’s Society 5.0 smart-factory roadmap. The Asian Development Bank’s Project Tridecagon showcases regional commitment to inter-bank distributed settlements that align with manufacturing export-credit flows. India’s electronics clusters and South Korea’s battery-supply chain agreements add momentum, catalyzing adoption by Tier-2 suppliers.

Europe Blockchain In Manufacturing Market

Europe emerges as a sustainability-centric adopter, leveraging Digital Product Passports to document carbon footprints and circular-economy metrics. Germany’s automotive OEMs employ joint ledgers to track recycled steel content, while France’s aerospace primes adopt blockchain to manage additive-manufacturing powders. Nordic manufacturers power permissioned networks with hydro and wind energy, addressing ESG expectations. Cross-border data-spaces projects promote interoperability, suggesting that regional implementations will converge under common governance as the blockchain in the manufacturing market matures globally.

Regulatory Landscape

Regulation and standardization are moving from pilots to more formal trust and assurance requirements that shape how manufacturers design and choose distributed-ledger implementations. In the European Union, Implementing Regulation (EU) 2025/2531 (adopted in December 2025) sets reference standards and specifications for qualified electronic ledgers under the eIDAS framework, pushing manufacturers and their trust service providers to align ledger governance, auditability, and technical controls with recognized specifications.

In the United States, policy attention is centering on competitiveness and supply chain resiliency use cases relevant to manufacturing. H.R. 1664, the Deploying American Blockchains Act of 2025, passed the House in June 2025 and directs the Department of Commerce to develop best practices for blockchain deployment, explicitly including supply chain resiliency and manufacturing applications. Alongside legislation, NIST continues to develop and test manufacturing traceability and blockchain-related approaches, positioning its work as a reference for implementation and risk management rather than a prescriptive compliance mandate.

Value Chain Analysis

The value chain starts with enabling layers such as industrial IoT and identity (data capture, device identity, and credentialing), blockchain platforms (public, permissioned, and consortium stacks), and integration services that connect ledgers to ERP, MES, PLM, and quality systems. Middleware, APIs, and data models translate shop-floor and supplier events into standardized records for use cases such as provenance, batch genealogy, anti-counterfeiting, and compliance documentation, with cloud BaaS providers and industrial system integrators packaging onboarding, node operations, and governance toolkits.

Downstream, manufacturers, Tier-1 and Tier-2 suppliers, logistics providers, and conformity assessment bodies contribute and consume shared records through consortium governance that defines membership, access control, and data retention. Bottlenecks cluster around interoperability between proprietary enterprise systems, protection of sensitive IP in multi-party ledgers, and cross-enterprise agreement on schemas and credentials. Efforts to reduce friction include standards and frameworks such as UNECEs UN Transparency Protocol for interoperable traceability data exchange, ISO work on trustworthy supply/value chains (ISO 22373:2025), and DLT-enabled electronic bills of lading processes (ISO 5909:2026).

Competitive Landscape

Competitive intensity is moderate with signs of consolidation as enterprises prefer end-to-end platforms. IBM, Microsoft, SAP, and Oracle integrate blockchain orchestration with ERP, IoT, and analytics suites, capturing 38% of 2024 platform billings. Their advantage rests on pre-existing enterprise contracts, turnkey compliance modules, and global cloud points of presence.

Specialists such as VeChain, Chronicled, and SyncFab carve niches in luxury goods, pharmaceutical traceability, and supplier discovery, respectively. They compete through domain depth and lighter-weight deployments. Strategic alliances bridge gaps; for example, IBM and Merck pilot FDA-compliant batch ledgers, and Zebra Technologies teams with Merck KGaA on M-Trust for counterfeit mitigation.

Emerging entrants pursue edge-native stacks, post-quantum cryptography, and zero-knowledge proofs. Siemens’ investment in device-resident nodes underscores OEM appetite for embedded ledgers. Patent filings by BMW and Ford reveal automakers’ focus on proprietary traceability workflows. Sustained R&D outlays and ecosystem alliances signal that platform breadth and standards influence will shape leadership in the blockchain in the manufacturing market through 2030.

Blockchain In Manufacturing Industry Leaders

IBM Corporation

Microsoft Corporation

Intel Corporation

Amazon Web Services, Inc.

Wipro Limited

- *Disclaimer: Major Players sorted in no particular order

Blockchain In Manufacturing Market Companies Covered in this Report

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Amazon Web Services Inc.

- Accenture PLC

- Wipro Limited

- Infosys Ltd

- Intel Corporation

- Advanced Micro Devices Inc.

- VeChain Technology

- Chronicled Inc.

- SyncFab

- Siemens AG

- Honeywell International Inc.

- General Electric

- R3 LLC

- ConsenSys

- Kaleido

- BlockApps Inc.

Market Opportunities and Future Outlook

Interoperability and cross-network coordination remain a key whitespace as manufacturers work to connect multi-tier supply chains that use different ledger stacks and non-DLT systems. ISO/TS 23516:2026, published in March 2026, provides an interoperability framework for blockchain and distributed ledger technologies, reinforcing the case for vendor-neutral integration layers, cross-chain data exchange, and standardized onboarding across suppliers. This supports opportunities in integration software, governance tooling, and data-model mapping that reduce the cost of scaling from single-enterprise pilots to multi-enterprise production networks.

Security- and compliance-led deployments also create room for solutions that bind equipment identity and production data to verifiable records, especially in IIoT and regulated product flows. Regional specifications such as DB21/T 4375-2026 define security requirements for blockchain applications in the Industrial Internet of Things, including equipment identity and production data storage, and complement traceability architectures such as the NIST IR 8536 manufacturing meta-framework for recording, linking, and querying provenance data. Recent manufacturing-facing implementations, including blockchain-enabled data sharing for ESG and product passport reporting, point to opportunities around digital product passport readiness, carbon and quality data exchange, and controlled data spaces that Tier-2 and Tier-3 suppliers with limited IT capacity can adopt.

Recent Industry Developments in Blockchain In Manufacturing Market

- July 2026: L&F established an ABB (AI, Big Data, Blockchain) smart factory at its Guji Plant 1, using a blockchain-based data space to manage life cycle assessment (LCA) information aligned to EU battery passport needs. The move links blockchain to ESG-grade production data sharing across upstream and downstream partners, raising the bar for standardized data exchange in battery materials manufacturing.

- June 2026: IBM, Red Hat, and Deloitte announced Project Lightwell to strengthen open source software supply chain trust against automated cyber threats. For manufacturers deploying blockchain platforms and connected OT/IT stacks, this collaboration elevates software provenance and integrity controls that influence procurement and deployment decisions for traceability and compliance systems.

- January 2026: Fujitsu began a demonstration experiment for green steel value flow using blockchain to enable safe data distribution and secure the environmental value attributes of green steel, with the trial running into February 2026. The project reinforces blockchain use in materials provenance and verifiable sustainability claims, which are increasingly tied to product passport and customer audit requirements.

Blockchain In Manufacturing Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the revenues linked to blockchain solutions used in manufacturing workflows, where distributed ledgers and smart contracts help track parts, verify provenance, improve compliance records, and support secure data sharing across the production value chain.

Scope exclusions: We exclude general crypto assets, consumer payments, and blockchain activity that is not tied to a manufacturing use case or a manufacturing-driven buyer budget.

Segments Covered in This Report

- By Application

- Logistics and Supply Chain Management

- Counterfeit Management

- Quality Control and Compliance

- Predictive Maintenance and Asset Tracking

- Smart Contracts for Procurement

- Other Applications

- By End-user Vertical

- Automotive

- Aerospace and Defense

- Pharmaceutical and Life Sciences

- Consumer Electronics

- Industrial Machinery

- Food and Beverage

- Other Verticals

- By Deployment Mode

- On-premises

- Cloud/Blockchain-as-a-Service (BaaS)

- Hybrid/Edge

- By Blockchain Type

- Public

- Private/Permissioned

- Consortium

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the manufacturing demand pool and the most common blockchain use cases that show up in supply chain traceability, anti-counterfeit controls, and audit readiness. We rely on public and official references such as the US Bureau of Labor Statistics for industrial output signals, the US International Trade Commission for trade flows that influence traceability needs, and standards bodies such as ISO for terminology and process requirements.

To keep assumptions grounded, we also review sources such as the World Bank and OECD for macro and industry indicators, and the World Economic Forum for published manufacturing and supply chain digitization themes. Company filings, earnings transcripts, and investor presentations help us understand how vendors position offerings, the typical contract structures, and where services are bundled with software. Select paid subscriptions are used only for structured company financials, patent-intensity checks, and shipment-level trade visibility where it helps verify directionally consistent volumes. These examples are not exhaustive, and many other public sources were also referenced for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary inputs are used to pressure-test adoption curves and price ranges with manufacturing users and solution providers, and we run follow-up calls when a number moves outside expected ranges. We speak with operations, supply chain, IT/security, and compliance stakeholders across APAC, EMEA, and the Americas so regional rollout patterns and regulatory readiness are reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 49% |

| Mid tier: 51% | Functional/Unit leaders: 43% | EMEA: 31% |

| Smaller Players: 18% | Managers: 45% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built from a top-down demand reconstruction where manufacturing digitization spend, traceability intensity in traded goods, and expected blockchain penetration are used to build a realistic spend pool by region. That number is then corroborated with selective bottom-up approximations, where we roll up a sampled set of manufacturing-focused solution revenues and validate implied volumes using typical project sizes and renewal patterns.

Key inputs used in the model include manufacturing output and PMI direction, cross-border shipment exposure for high-risk components, the share of regulated or recall-sensitive products, typical implementation and support pricing, and the pace of enterprise permissioned-network adoption versus pilots. Forecasts are produced using scenario analysis, with base, conservative, and aggressive adoption paths informed by interview feedback on procurement cycles, cybersecurity approval times, and integration effort. When bottom-up data is incomplete, gaps are handled through calibrated ranges by application maturity, and the midpoint is kept only after it matches independent signals from interviews and public indicators.

Data Validation & Update Cycle

Model outputs are checked against independent markers such as manufacturing IT spending direction, disclosed pipeline commentary, and the expected ratio of services to software in enterprise deployments. If growth in one region or application looks too steep, the drivers are re-tested and the inputs are sent through a second analyst review before sign-off.

The report is refreshed annually, and interim updates are made when major policy, funding, or technology shifts change adoption assumptions in a meaningful way. Before delivery, we do a final pass to re-check currency conversion timing, re-validate key variables, and confirm that the latest public and interview-led signals are reflected.

Mordor Intelligence's Manufacturing Blockchain Market Size Compared With Other Published Estimates

Published market numbers for blockchain in manufacturing often do not match because each study picks its own inclusion list and timing for when a deployment counts as revenue. Differences also come from currency conversion points, how services are treated, and whether pilot activity is assumed to convert to scaled rollouts.

Some external estimates appear to fold in broader blockchain technology spending that is not always tied to manufacturing-led budgets, and that choice pushes the headline value upward. In Mordor Intelligence, revenue is counted only when the buyer use case is manufacturing-specific (for example traceability, compliance records, or counterfeit control) and the scope does not absorb unrelated crypto, payments, or non-manufacturing blockchain programs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.54 B (2025) | |

| Industry Research Firm A | USD 4.44 B (2025) | Often uses a wider provider and offering set, which can include general blockchain platforms and adjacent enterprise blockchain spending that is not strictly manufacturing-use-case driven, and it may apply a slower ASP normalization for services over time. |

| Market Publisher B | USD 2.56 B (2024) | Uses a different base year and a segmentation structure that can mix manufacturing with other verticals, and the forecast path can change depending on whether pilots are treated as scaled deployments in the starting period. |

The spread in the table mainly comes from scope breadth, base-year selection, and how quickly pilot programs are assumed to turn into paid, recurring deployments. By keeping inclusion rules tied to manufacturing use cases and checking the result against practical pricing and adoption signals, the final number stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current size of the blockchain in the manufacturing market?

The blockchain in the manufacturing market is valued at USD 4.4 billion in 2026.

How fast will the market expand over the next five years?

Revenue is forecast to increase at a 73.06% CAGR, reaching USD 68.23 billion by 2031.

Which application segment is growing the quickest?

Quality control and compliance solutions show the highest growth, advancing at a 74.20% CAGR to 2031.

Why is Asia Pacific considered the most dynamic region?

Government-backed digitization programs in China, Japan, and India push Asia Pacific to a 75.20% CAGR through 2031.

Who are the leading technology providers in this space?

IBM, Microsoft, SAP, and Oracle lead platform revenues, while VeChain and Chronicled specialize in manufacturing-specific deployments.

What major hurdle could slow near-term adoption?

Fragmented interoperability standards pose the largest restraint, potentially trimming the CAGR impact by 12.4%.

Page last updated on: