Blockchain IoT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

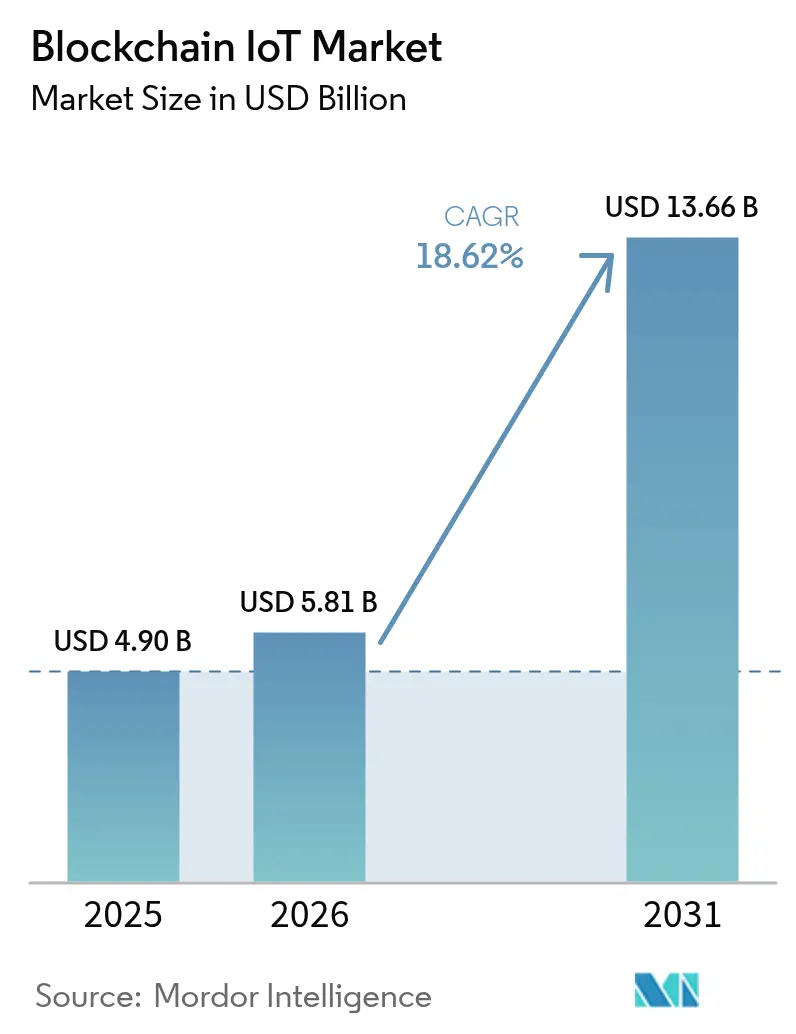

| Market Size (2026) | USD 5.81 Billion |

| Market Size (2031) | USD 13.66 Billion |

| Growth Rate (2026 - 2031) | 18.62% CAGR |

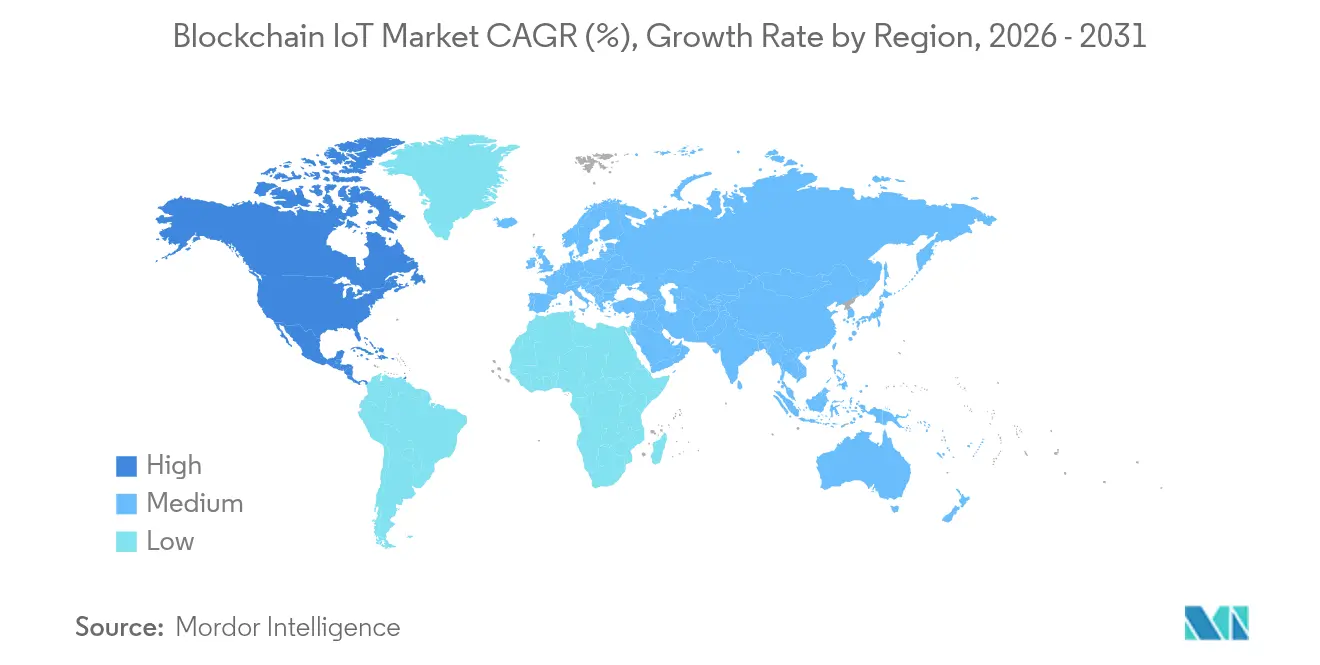

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

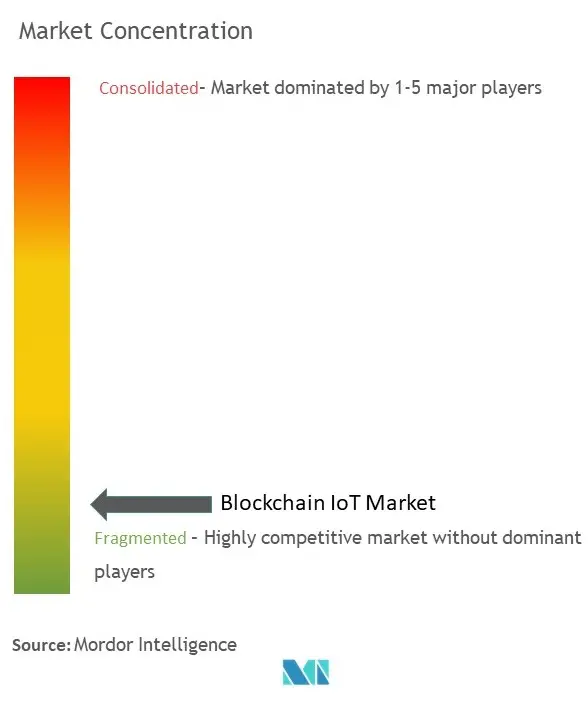

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain IoT Market Analysis by Mordor Intelligence

The Blockchain IoT Market size was valued at USD 4.90 billion in 2025 and estimated to grow from USD 5.81 billion in 2026 to reach USD 13.66 billion by 2031, at a CAGR of 18.62% during the forecast period (2026-2031).

Escalating cyber-attacks on connected devices, tightening supply-chain transparency mandates, and enterprise demand for tamper-proof data flows reinforce rapid adoption. Layer-2 roll-ups and edge-native consensus engines lower latency limits that once restrained industrial use, while Decentralized Physical Infrastructure Networks (DePIN) create token-driven business models that monetise idle sensor capacity. Hardware spending leads short-term growth as organisations embed secure elements, yet infrastructure services generate the strongest mid-term upside as firms shift from monolithic to modular blockchain stacks. Regulatory clarity in North America and the European Union accelerates deployments, but energy and compute constraints on low-cost devices remain a drag.

Key Report Takeaways

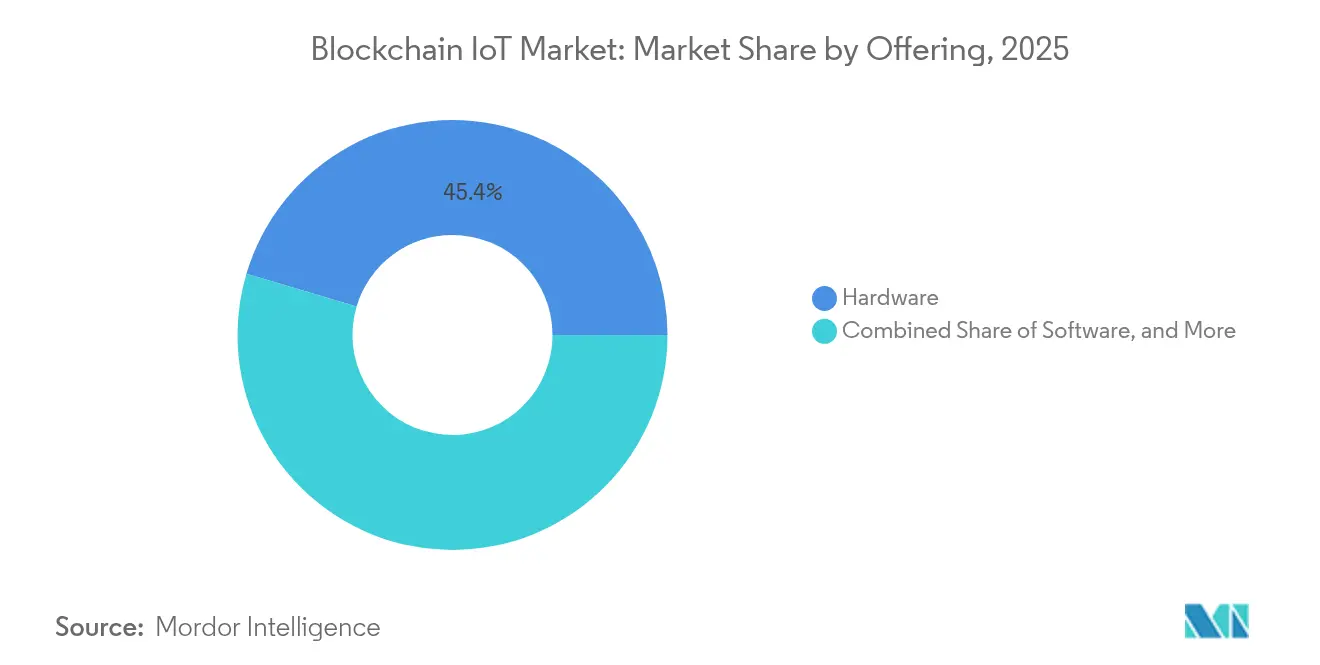

- By offering, hardware captured 45.40% revenue share of the blockchain IoT market in 2025; infrastructure solutions are projected to grow at a 20.90% CAGR through 2031.

- By application, asset tracking held 30.85% of the blockchain IoT market share in 2025, while smart contracts and automation are expected to advance at a 23.10% CAGR to 2031.

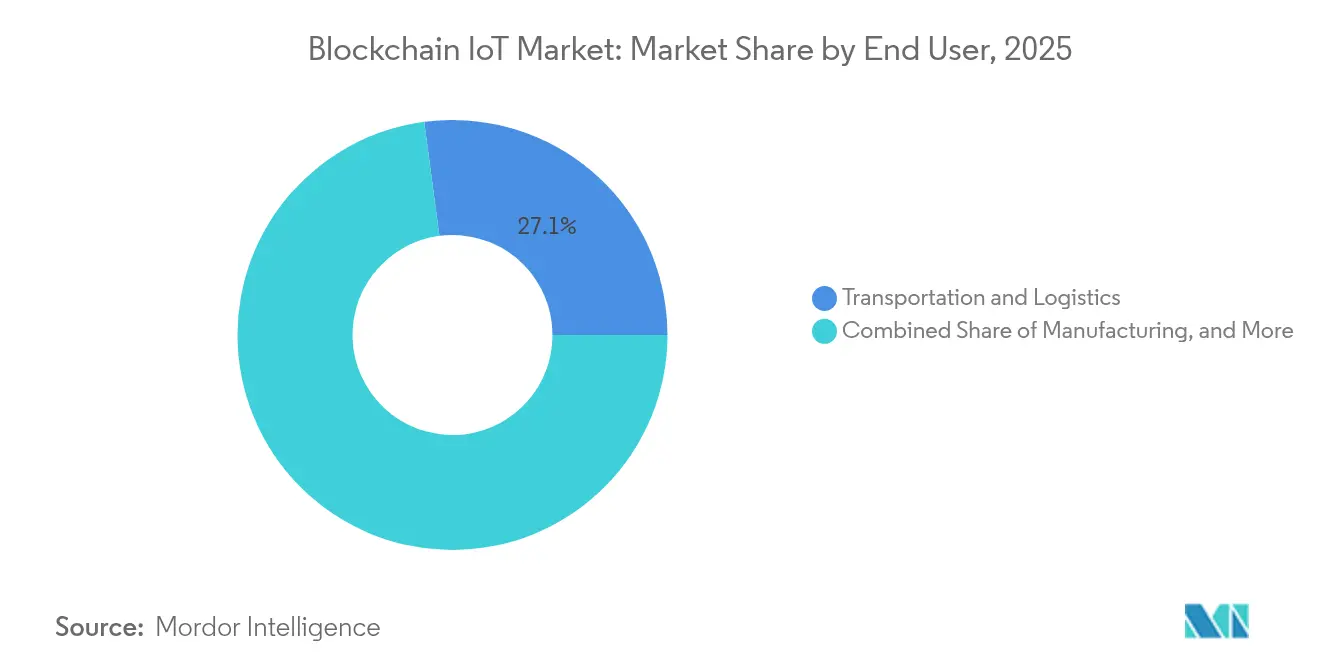

- By end user, transportation and logistics led with a 27.10% share in 2025; smart cities and government are forecast to expand at a 21.90% CAGR through 2031.

- By application, asset tracking held 30.85% of the blockchain IoT market share in 2025, while smart contracts and automationDriver (~) % Impact on CAGR Forecast Geographic Relevance Impact Timeline

- Surge in IoT-centric cyber-attacks elevating demand for tamper-proof ledgers +4.20% Global, acute in North America & the EU Short term (≤ 2 years)

- Acceleration of supply-chain transparency mandates (ESG, eIDAS 2.0, US FSLMDA) +3.80% North America & EU primary, APAC emerging Medium term (2–4 years)

- Edge-computing investments coupled with Layer-2 roll-ups for low-latency consensus +3.10% APAC core, spill-over to North America Medium term (2–4 years)

- Standardization of device identities via DID / Verifiable Credentials frameworks +2.90% Global, led by the IEEE consortium Long term (≥ 4 years)

- Emergence of DePIN token-incentivized sensor networks +2.60% US, EU early, scaling fastest in APAC smart-city clusters Medium term (2–4 years)

- Digital-twin monetization through on-chain provenance tokens +2.40% Global industrial manufacturing ecosystems Long term (≥ 4 years)

- advance at a 23.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blockchain IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in IoT-centric cyber-attacks elevating demand for tamper-proof ledgers | +4.20% | Global, acute in North America & the EU | Short term (≤ 2 years) |

| Acceleration of supply-chain transparency mandates (ESG, eIDAS 2.0, US FSLMDA) | +3.80% | North America & EU primary, APAC emerging | Medium term (2–4 years) |

| Edge-computing investments coupled with Layer-2 roll-ups for low-latency consensus | +3.10% | APAC core, spill-over to North America | Medium term (2–4 years) |

| Standardization of device identities via DID / Verifiable Credentials frameworks | +2.90% | Global, led by the IEEE consortium | Long term (≥ 4 years) |

| Emergence of DePIN token-incentivized sensor networks | +2.60% | US, EU early, scaling fastest in APAC smart-city clusters | Medium term (2–4 years) |

| Digital-twin monetization through on-chain provenance tokens | +2.40% | Global industrial manufacturing ecosystems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in IoT-centric cyber-attacks elevating demand for tamper-proof ledgers

Exploding malware volumes force enterprises to embed security at the protocol level. A lightweight blockchain consensus achieved 95.2% malicious-device detection with 15% higher throughput and 20% lower latency than centralised models. Chief information security officers increasingly regard distributed ledgers as mandatory for zero-trust architectures.

Acceleration of supply-chain transparency mandates

Regulations such as the US Federal Supply Chain Localisation and Manufacturing Development Act and EU eIDAS 2.0 oblige verifiable provenance. California’s DMV moved 42 million car titles on-chain, proving large-scale public deployment viability.

Edge-computing investments with Layer-2 roll-ups

Delegated proof-of-stake chains processed over 4,000 tps on industrial edge nodes without sacrificing cryptographic integrity.[2]Research Team, “High-Throughput Edge Blockchains,” Nature, nature.comSharding across micro-data-centres positions the blockchain IoT market for real-time robotics and predictive-maintenance workloads.

Standardisation of device identities via DID / VCs

An IEEE working group involving Bosch, Ericsson and Lenovo is finalising a Decentralised Identifier framework for cross-chain IoT authentication.[1]Standards Committee, “Decentralized Identifier Framework for IoT,” IEEE, ieee.orgInteroperable credentials dismantle proprietary silos, boosting ecosystem liquidity and developer uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited on-device computing power for cryptographic workloads | -2.80% | Global, acute in cost-sensitive IoT deployments | Short term (≤ 2 years) |

| Rising energy cost for Proof-of-Work / Proof-of-History edge nodes | -2.10% | Energy-intensive regions, industrial applications | Medium term (2–4 years) |

| Fragmented interoperability across blockchain protocols and IoT standards | -1.90% | Global, multi-protocol brownfield legacy estates | Medium term (2–4 years) |

| Regulatory ambiguity surrounding tokenized machine data ownership | -1.60% | US/EU highest legal exposure | Medium → Long term (3–5+ years) |

| Source: Mordor Intelligence | |||

Limited on-device computing power for cryptographic workloads

Proof-of-Work tests on micro-controllers showed untenable energy draw, pushing vendors toward offloaded or hardware-accelerated hashing. FPGA SHA-256 cores cut dynamic power nearly 1,000-fold versus software. Cost barriers split the market between premium blockchain-capable devices and lightweight authenticators.

Rising energy cost for consensus edge nodes

Projected AI electricity demand of 23 GW by 2025 competes directly with distributed ledger workloads.[3]J. G. Miller, “AI Electricity Demand Forecast,” Foreign Affairs, foreignaffairs.com Industrial operators are pivoting to Proof-of-Stake schemes that lower energy use by 99%, despite reduced decentralization guarantees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Dominance Drives Infrastructure Innovation

Hardware held 45.40% share of the blockchain IoT market in 2025, anchored by secure elements and cryptographic co-processors that safeguard device keys. The segment safeguards the blockchain IoT market size against firmware tampering across industrial robots and connected vehicles. Infrastructure, spanning Layer-2 roll-ups and edge validators, is projected to expand at 20.90% CAGR as enterprises migrate from pilot clouds to production-grade networks. Software platforms complete the stack by masking ledger complexity through API gateways.

The infrastructure boom reflects the maturity of blockchain-as-a-service portfolios from hyperscalers that bundle orchestration, compliance, and monitoring. Public chains struggle to match deterministic latency thresholds, so private or consortium-ledgers dominate mission-critical workloads. Hybrid architectures fuse on-prem edge clusters with public settlement layers, trading full decentralisation for deterministic performance. Token-incentivised gateways reward operators for bandwidth and compute contributions, nurturing a self-financing backbone that underpins future growth of the blockchain IoT market.

By Application: Asset Tracking Leads, Smart Contracts Accelerate

Asset tracking commanded 30.85% of the blockchain IoT market share in 2025 through mandated provenance across pharma, aerospace, and luxury goods. Verified location and temperature logs underpin recall avoidance and counterfeit mitigation. Smart contracts and automation should record a 23.10% CAGR to 2031, enlarging the blockchain IoT market size as firms convert static ledgers into autonomous process engines that trigger payments and warranty claims.

Data-security suites remain steady as baseline defences, while predictive-maintenance offerings monetise verified equipment logs to extend service intervals. Digital-twin tokens introduce secondary-market liquidity for refurbished machinery, translating operational transparency into capital efficiency. Over time, bundled platforms that unite multiple use cases outperform point solutions, supporting long-run stickiness within the blockchain IoT market.

By End User: Transportation Dominance Challenged by Smart-City Surge

Transportation and logistics led with 27.10% revenue in 2025, leveraging tamper-proof e-bill-of-lading and cold-chain monitoring. Yet smart-city and government programmes are forecast to grow at 21.90% CAGR, propelled by municipal identity wallets and on-chain public-service logs. The resulting re-ordering diversifies the blockchain IoT market, lessening over-reliance on supply-chain budgets.

Manufacturing sustains double-digit momentum under Industry 4.0 retrofits, embedding verifiable process data into quality audits. Energy and utilities experiment with transactive-grid pilots that share surplus rooftop power, while healthcare players secure patient-generated sensor data through zero-knowledge proofs. Agricultural uptake is nascent but rising where provenance premiums justify device costs.

Geography Analysis

North America retained 35.60% of the blockchain IoT market revenue in 2025, aided by the US FSLMDA and deep venture funding pools. Federal and state pilots—such as 42 million blockchain-verified car titles—canonicalise ledger usage in public registries. Canadian utilities deploy peer-to-peer energy marketplaces, whereas Mexican exporters adopt provenance ledgers to satisfy USMCA traceability clauses.

APAC posts a 19.23% CAGR outlook to 2031, anchored by China’s goal of 3.6 billion cellular IoT links by 2027 . Japan spearheads blockchain-IoT interoperability standards, South Korea couples 5G and distributed ledgers in smart-city grids, and India pilots blockchain in crop-insurance schemes. Australia applies verified sensing to mining compliance.

Europe gains from the Markets in Crypto-Assets Regulation and eIDAS 2.0, supplying robust legal scaffolding for cross-border device identity. Germany champions industrial roll-outs, the Netherlands tracks port cargo, and France digitises luxury supply chains. The European Data Protection Board’s 2025 guidelines detail privacy-by-design ledger architectures

The Middle East and Africa leverage blockchain to leapfrog legacy grids, piloting smart-meter roll-outs and drone-based asset inspection. Selected South-American mines record ESG metrics on-chain to secure premium export pricing.

Regulatory Landscape

Regulation for blockchain-enabled IoT is taking shape across IoT architecture standards, DLT guidance, and sector rules for data sharing and smart-contract behavior. ITU-T has published blockchain-IoT focused guidance, including ITU-T Supplement 88 (January 2025) on applicability cases of blockchain in IoT and ITU-T Recommendation Y.4227 (2024) on requirements for IoT systems to support blockchain integration. ISO/IEC has also updated the IoT systems reference architecture through ISO/IEC 30141:2024, which is increasingly used as a baseline for designing interoperable device-to-cloud architectures that incorporate ledger-based integrity controls.

In Europe, compliance work is clustering around privacy-by-design and operational controls for smart contracts used in data sharing. The EU Data Act introduces EU-level requirements for smart contracts in data sharing agreements, applicable from September 2025, which pushes IoT and platform providers to implement controllability measures such as safe termination and consistency safeguards in contract automation. On privacy, the European Data Protection Board adopted Guidelines 02/2025 (Version 2.0) for processing personal data through blockchain technologies on 07 July 2026, clarifying GDPR obligations for immutable ledgers and reinforcing the need for off-chain processing, encryption, and privacy-preserving designs when blockchain records can relate to identifiable device owners or operators.

Value Chain Analysis

The blockchain IoT value chain begins with device and edge hardware suppliers, including sensors, gateways, secure elements, and cryptographic accelerators, along with connectivity providers. It then passes through IoT platforms and middleware, covering device management, data ingestion, and API gateways, before moving into blockchain infrastructure layers such as public chains, private or consortium ledgers, Layer-2 systems, and node operations. Application integrators translate these building blocks into asset tracking, automation, and integrity solutions for end users.

A recurring operating pattern is hybridization, where high-frequency IoT telemetry is stored off-chain in enterprise repositories and hashes, signatures, and key events are anchored on-chain to support tamper evidence, auditability, and cross-party trust without creating prohibitive latency or storage overhead. Interoperability and standards alignment increasingly shape where value concentrates and where bottlenecks form. ISO/TS 23516:2026 (published March 2026) provides a framework for interoperability between DLT systems and external entities, while IEEE 3221.01-2025 (approved March 2025) addresses cross-chain transaction consistency, reducing fragmentation across blockchain protocols that limits end-to-end visibility across multi-party IoT estates. Standards that focus on supply-chain authenticity and integrity, such as ISO 22373:2025 (published November 2025), also push hardware-rooted trust and standardized event schemas upstream, increasing demand for approaches that consortium participants can share.

Competitive Landscape

The blockchain IoT market remains moderately fragmented. IBM pairs Hyperledger Fabric with Red Hat OpenShift to bundle containerised edge nodes, winning aviation parts traceability contracts. Microsoft embeds Confidential Computing enclaves in Azure Sphere to secure device roots of trust and recently partnered with Schneider Electric on predictive-maintenance ledgers. Cisco integrates blockchain into its IoT Control Center, targeting telecom carriers that monetize managed connectivity.

Emerging specialists pursue energy-efficient consensus chips and cross-chain routers. Helium-style DePIN operators tokenise last-mile connectivity, challenging telecom incumbents with community hotspots. Standards bodies such as IEEE level the playing field by codifying interoperable identity frameworks that commoditise baseline functions, shifting competition to value-added analytics and SLA guarantees.

Strategic investments shape the field. Bosch earmarked EUR 2.5 billion for blockchain-AI convergence, focusing on automated driving stacks. Honeywell collaborates with Verizon to connect smart meters over 5G, marrying near-real-time tariffs with blockchain-verified readings . Such cross-sector alliances highlight the shift from proof-of-concepts to production ecosystems.

Blockchain IoT Industry Leaders

IBM Corporation

Microsoft Corporation

Intel Corporation

Cisco Systems Inc.

Amazon Web Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space is concentrated at the intersection of device identity, zero-touch onboarding, and compliance-grade data sharing, where enterprises are seeking interoperable building blocks rather than bespoke pilots. Existing standards provide a path to packaged functionality, including ITU-T X.1353 (September 2024), which outlines a security methodology for zero-touch deployment of massive IoT using blockchain, and IEEE 3219-2023 (published April 2026), which defines a blockchain-based zero-trust access control framework for heterogeneous IoT interoperability. Together, these references support opportunities for vendors that productize credential lifecycle management, device attestation, and policy enforcement into modular stacks intended to operate across multiple ledgers and IoT platforms.

Another near-term opportunity sits in compliance-driven traceability and multi-party provenance that uses blockchain as an integrity layer while keeping operational data scalable and private. The EU Data Act (applicable September 2025) is increasing attention on governed smart contracts in data sharing agreements, and European Commission work on supply chain transparency infrastructure is visible in its June 2026 proposal (COM/2026/504) for a Business-to-Business Semiconductor Supply Chain Platform, framed as a digital twin for transparency and crisis management. Alongside this policy pull, commercialization signals are showing up around hardware-anchored identity and machine-to-machine economies, including WISeKey SEALCOIN AGs April 2026 Spacedrop initiative built on hardware-based identity with Hedera DLT. Demand centers that align with hybrid on-chain or off-chain constraints also remain prominent, particularly logistics provenance and regulated-industry traceability, where integrity guarantees and confidentiality requirements must be balanced.

Recent Industry Developments

- July 2026: Keysight Technologies was selected by the European Space Agency to lead a three-year program with satellite operator Sateliot to develop blockchain-anchored anomaly detection and security for 5G non-terrestrial networks. The award connects blockchain trust layers with satellite IoT connectivity, broadening the addressable set of high-latency, wide-area IoT deployments where integrity and authentication are difficult to centralize.

- April 2026: IBM expanded its FedRAMP portfolio with authorization of 11 software solutions, including watsonx, supported by its strategic collaboration with AWS. The added authorizations strengthen IBM and partners ability to place blockchain-IoT adjacent workloads into regulated public-sector environments where compliance-ready cloud controls often decide vendor selection.

- September 2024: ITU published Recommendation ITU-T X.1353, defining a security methodology for zero-touch deployment of massive IoT using blockchain. The guidance provides a standards-backed pathway for automating credentialing and provisioning at scale, supporting blockchain-enabled device identity frameworks that reduce operational friction in large IoT rollouts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending on blockchain-based platforms, software, and related services that are deployed to secure, verify, and automate data and transactions across IoT devices and connected systems.

Scope exclusions: Pure IoT hardware-only revenue, generic cybersecurity products without blockchain functionality, and cryptocurrency trading activity are excluded from this sizing.

Segmentation Overview

- By Offering

- Hardware

- IoT Sensors and Actuators

- Gateways and Edge Devices

- Connectivity Modules

- Blockchain Chipsets

- Software

- Middleware Platforms

- Smart-Contract Management

- Identity and Access Management

- Analytics and Visualization

- Infrastructure

- Public Chains

- Private/Consortium Chains

- Cloud and Edge Services

- Hardware

- By Application

- Data Security

- Smart Contracts and Automation

- Data Communication and Integrity

- Asset Tracking and Management

- Predictive Maintenance

- Other Niche Applications

- By End User

- Manufacturing

- Energy and Utilities

- Transportation and Logistics

- Building Management and Smart Facilities

- Retail and eCommerce

- Smart Cities and Government

- Healthcare and Life Sciences

- Agriculture

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To build the initial structure, we map how blockchain is used inside IoT environments, then we collect reference indicators that can be checked across regions. Public sources are used to anchor the wider digital and connected-device context, such as data from the International Telecommunication Union (ITU), the World Bank, OECD digital economy datasets, NIST publications, and ENISA reports on security practices.

We also review supporting material like standards and guidance from bodies such as ISO and IEEE, plus peer-reviewed papers that discuss blockchain performance limits for device networks. On top of that, we use company filings, earnings transcripts, investor presentations, and credible press to understand adoption patterns, typical deployment models, and pricing direction for enterprise software. Paid subscriptions are used selectively for company financials and intelligence, patent lookups, and news and financial screening to avoid missing product launches or partnership signals. The examples above are not exhaustive, and we referenced many other public documents and datasets for data collection and cross-checks.

Primary Interviews and Surveys

Primary work is used to confirm what is actually being bought and deployed, and how spend moves between pilots and scaled rollouts. We speak with solution providers, system integrators, and end-user teams running connected operations across APAC, EMEA, and the Americas, and then the inputs are used to fill gaps around pricing, buyer budgets, and adoption timing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 15% | APAC: 39% |

| Mid tier: 52% | Functional/Unit leaders: 39% | EMEA: 36% |

| Smaller Players: 15% | Managers: 46% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts by reconstructing demand from the IoT digitalization pool, then applying adoption and spending ratios for blockchain-enabled device networks by region and major end-use settings. We state the top-down approach once because it stays practical for this space, where many deployments are bundled into broader digital programs. Selective bottom-up checks are then used to keep totals realistic, including sampled deal sizes, service intensity per deployment, and cross-checks against provider exposure.

Key inputs in the model include the installed base growth of connected devices, enterprise adoption of distributed ledger features for identity and data integrity, smart contract usage in machine-to-machine workflows, typical implementation and integration hours, and cloud versus on-premises preference where it changes budgets. When data is sparse for a niche use case, we keep assumptions conservative and validate them through follow-up calls with practitioners rather than forcing a detailed supplier roll-up.

For forecasting, we use scenario analysis supported by regression-style sensitivity checks. The main drivers are device growth, security and compliance pressure, and the maturity of enterprise blockchain tooling. The forecast is adjusted only after the driver outlook is agreed across interview feedback and desk signals, so the path from assumptions to outputs remains traceable.

Data Validation & Update Cycle

Validation is done by comparing outputs against independent signals, including enterprise software spending direction, IoT rollout activity, and the pace of blockchain production adoption discussed in public filings. Outliers are investigated by drilling into region, use case, and pricing assumptions, followed by peer review of the math and logic before sign-off.

The report is refreshed annually, and interim updates are triggered when a material event changes the demand picture, such as a regulatory push, a large enterprise rollout wave, or a clear pricing reset in implementation services. Before delivery, an analyst runs a fresh consistency pass so clients get an updated view aligned to the latest available information.

Mordor Intelligence's Blockchain IOT Market Sizing Compared With Other Published Estimates

Published market numbers for blockchain IoT can look far apart because the market can be framed in more than one way, and because researchers do not always use the same spending boundary. Differences also come from the base year selected, how fast adoption is assumed to move from pilots to scaled deployments, and whether price erosion in software is applied evenly across regions.

Cryptocurrency and token-trading related revenue is excluded because it sits outside Mordor Intelligence's blockchain IoT scope, and that single exclusion often explains why some public figures appear much larger even when the wording sounds similar. Gaps also show up when estimates include IoT hardware revenue, count general cybersecurity spend as blockchain-enabled, or use aggressive adoption curves without checking them against integration capacity and real project timelines.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.81 B (2026) | |

| Industry Research House A | USD 0.51 B (2023) | Uses an earlier base year and a narrower revenue capture that leans toward recorded blockchain IoT software revenues, which can undercount integration and managed services tied to deployments. |

| Industry Research House B | USD 1.46 B (2024) | Counts a different base year and tends to apply a faster adoption ramp, which can lift totals if pilots are assumed to convert to scaled rollouts sooner than field feedback indicates. |

The table shows that the spread is mainly driven by year alignment and what is treated as deployable blockchain IoT spend versus adjacent technology revenue. By keeping inputs tied to observable device rollout signals and validated service intensity assumptions, our estimate stays easy to replicate and explain, even when public sources point to different totals.

Key Questions Answered in the Report

What is the current size of the blockchain IoT market?

The blockchain IoT market is valued at USD 5.81 billion in 2026 and is projected to hit USD 13.66 billion by 2031, reflecting an 18.62% CAGR.

Which region leads the blockchain IoT market?

North America holds 35.60% share in 2025 owing to supportive regulation and mature enterprise adoption.

Which application segment is growing fastest?

Smart contracts and automation post a 23.10% CAGR through 2031 as firms shift to autonomous, rules-based workflows.

What is the biggest restraint on adoption?

Limited compute capacity on low-power IoT devices reduces feasibility of on-device cryptographic operations, subtracting an estimated 2.8% from forecast CAGR.

Why are Layer-2 roll-ups important for blockchain IoT?

They boost throughput to industrial thresholds (>4,000 tps) while keeping latency low, enabling real-time control workloads.

How fragmented is the vendor landscape?

Top players IBM, Microsoft, Cisco, Bosch and Honeywell account for roughly 60% combined revenue, indicating moderate concentration with active specialist competition.

Page last updated on: