Blockchain Supply Chain Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

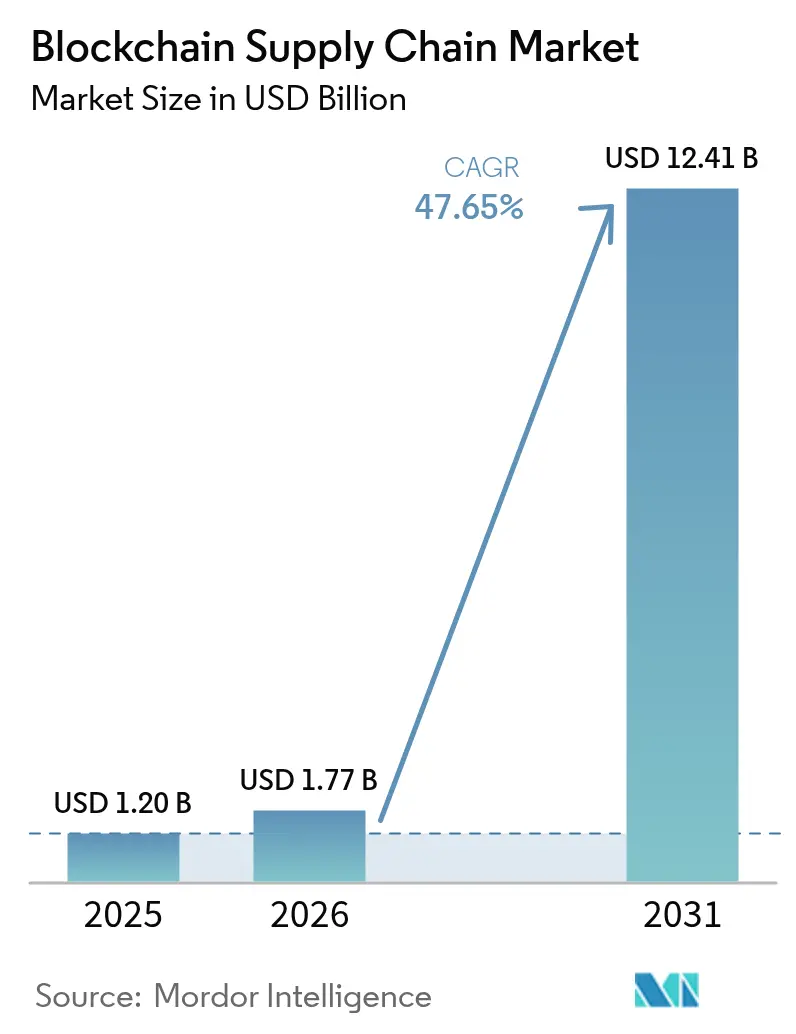

| Market Size (2026) | USD 1.77 Billion |

| Market Size (2031) | USD 12.41 Billion |

| Growth Rate (2026 - 2031) | 47.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain Supply Chain Market Analysis by Mordor Intelligence

The Blockchain Supply Chain Market size was valued at USD 1.20 billion in 2025 and estimated to grow from USD 1.77 billion in 2026 to reach USD 12.41 billion by 2031, at a CAGR of 47.65% during the forecast period (2026-2031). Stricter provenance regulations propel the expansion, mounting ESG disclosure pressures, and the inability of legacy systems to provide tamper-proof, end-to-end audit trails. Multi-tier transparency needs, token-driven cost-savings, and cloud deployment models further accelerate adoption. Technology suppliers are prioritizing interoperability and modular architectures, while enterprises increasingly view blockchain as the connective tissue unifying IoT, AI, and existing ERP systems. Demand is strongest in food, automotive, and high-value electronics, where real-time traceability mitigates recalls and counters gray-market diversion.

Key Report Takeaways

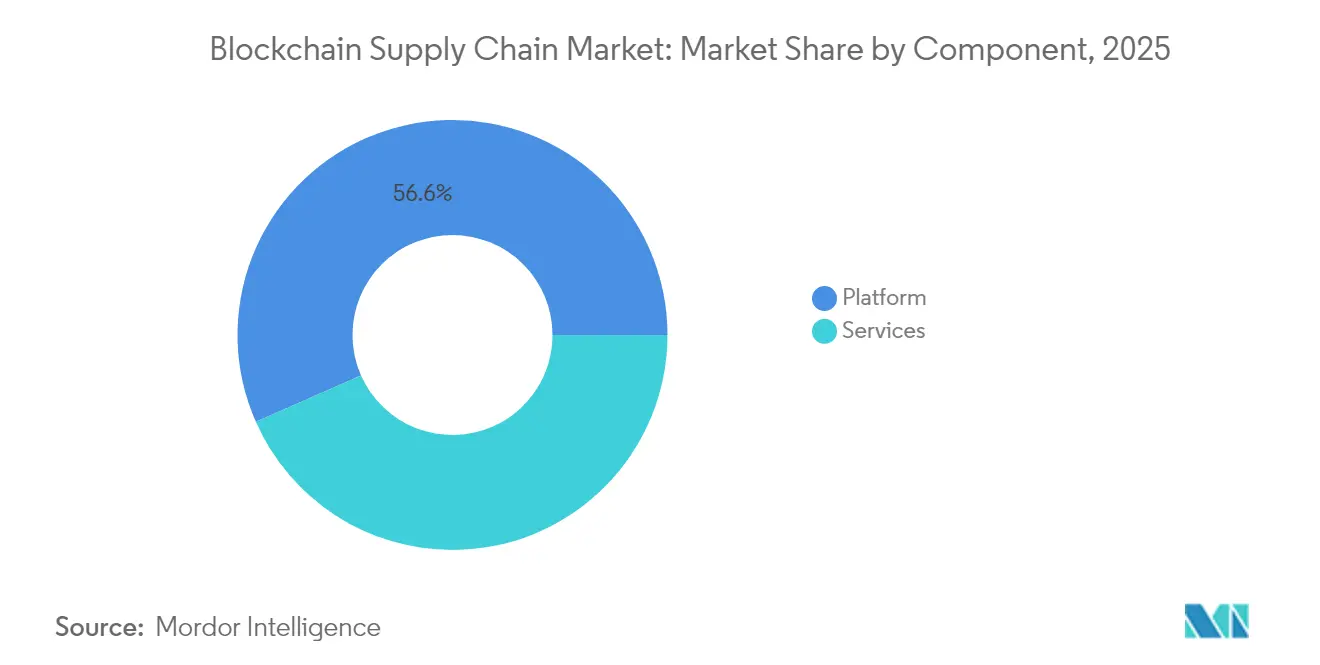

- By component, platform solutions led with 56.62% of the blockchain supply chain market share in 2025; service engagements are projected to rise at a 48.10% CAGR through 2031.

- By blockchain type, public networks held 42.10% revenue share in 2025, while hybrid models recorded the highest 49.20% CAGR to 2031.

- By deployment model, cloud captured 60.72% of the blockchain supply chain market size in 2025 and is advancing at a 49.40% CAGR through 2031.

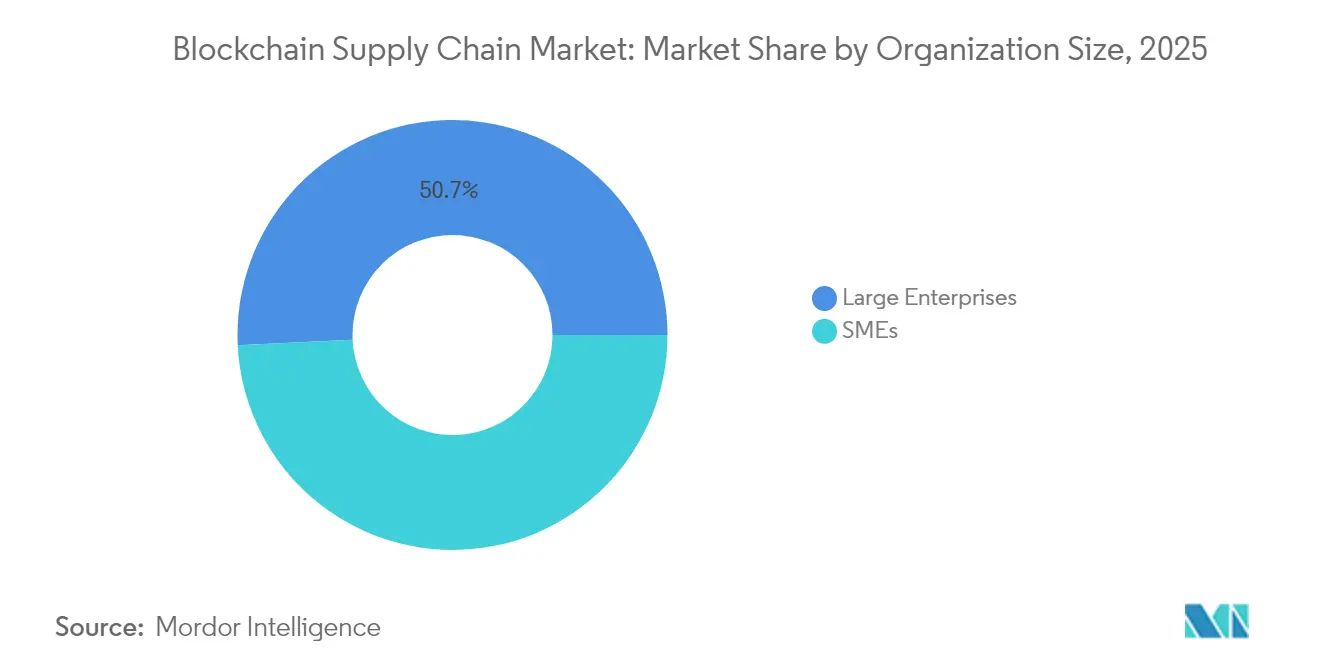

- By organization size, large enterprises controlled a 50.75% share in 2025; SMEs are poised for the quickest 50.10% CAGR through 2031.

- By application, product traceability accounted for 37.55% of 2025 revenue, whereas smart contracts are expanding at a 50.60% CAGR to 2031.

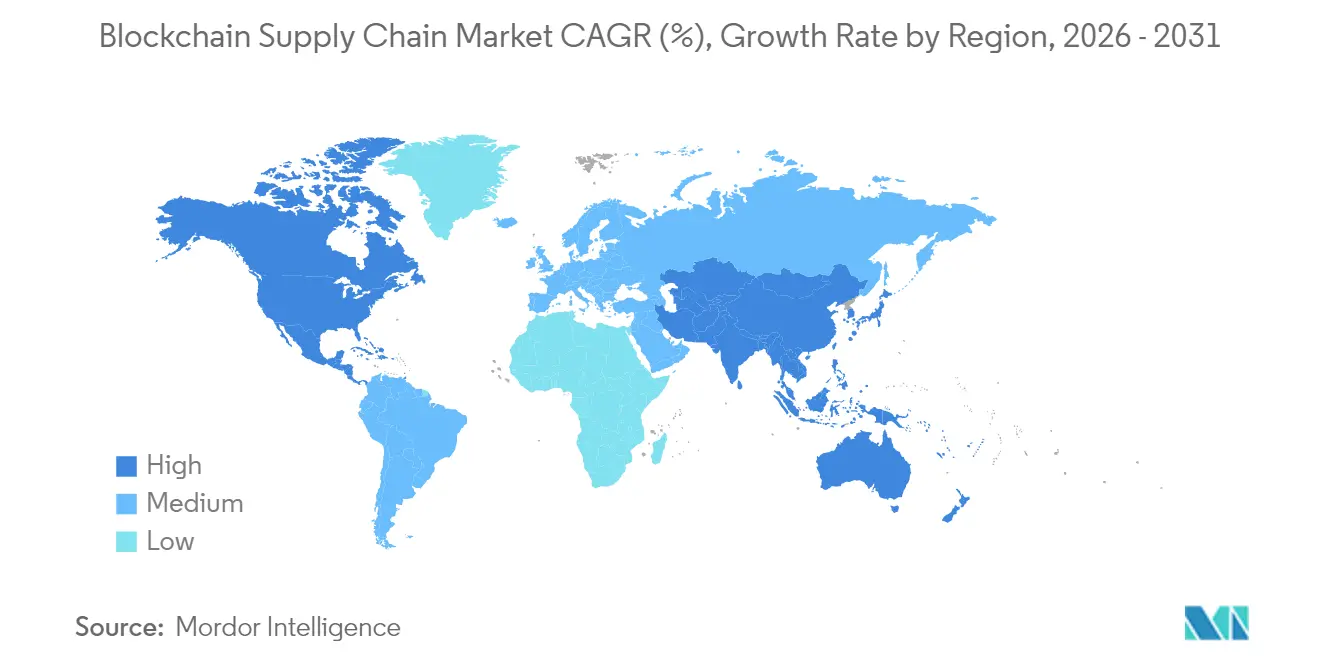

- By geography, North America dominated with a 39.15% share in 2025; Asia-Pacific is expected to surge at a 50.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blockchain Supply Chain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Augmented demand for secure, tamper-proof supply-chain transactions | +12.5% | North America, Europe, global spillover | Medium term (2-4 years) |

| Need for end-to-end transparency in multi-tier supply chains | +11.2% | APAC manufacturing hubs, global | Long term (≥ 4 years) |

| Cost-saving push from tokenized asset tracking and automated reconciliation | +9.8% | North America, Europe, expanding in APAC | Medium term (2-4 years) |

| Convergence of IoT sensors and blockchain for real-time asset tracking | +8.7% | APAC core, North America | Short term (≤ 2 years) |

| ESG-driven provenance auditing requirements | +7.3% | European Union leadership, global adoption | Long term (≥ 4 years) |

| Smart-insurance and parametric pay-outs for logistics | +6.1% | North America, Europe, APAC pilots | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Augmented Demand for Secure, Tamper-Proof Supply-Chain Transactions

Renault’s XCEED initiative processes more than 1 million compliance documents at up to 500 TPS, illustrating how immutable ledgers shift regulatory reporting from static spreadsheets to real-time verification [1]IBM, “Renault digital compliance network drives trusted data sharing,” ibm.com. The network spans multiple tier-one suppliers, cutting audit preparation cycles and strengthening collective risk oversight. Real-time certification reduces disruption response intervals, and embedded smart contracts eliminate roughly 40% of manual reconciliations. Confidential data is safeguarded through granular cryptographic keys, proving that privacy and transparency can co-exist on production-scale blockchains.

Need for End-to-End Transparency in Multi-Tier Supply Chains

Walmart’s food-safety program trimmed contamination source tracing from days to seconds, demonstrating how immutable records enhance recall accuracy and brand trust. DNV’s “My Story” QR codes link verified sustainability and quality data to individual items, giving consumers on-demand provenance proof [2]DNV, “My Story digital assurance,” dnv.com. The approach allows brands to transform transparency into a competitive advantage while regulators gain continuous visibility into high-risk nodes across product life cycles.

Cost-Saving Push from Tokenized Asset Tracking and Automated Reconciliation

Procurement teams report double-digit value leakage from invoice errors and price variances. Tokenizing goods transforms them into programmable assets, enabling self-executing smart contracts that settle once predefined milestones are met. IBM Food Trust users have observed up to 90% cycle-time cuts in invoice processing, with working-capital release accelerating as milestones are verified on-chain [3]IBM, “Food Trust overview,” ibm.com. Enterprise-grade tokenization modules baked into VeChain’s platform reduce technical lift for mid-sized suppliers.

Convergence of IoT Sensors and Blockchain for Real-Time Asset Tracking

AXONS’ FarmPro application, running on Amazon Managed Blockchain, supports 30,000 small farms across Southeast Asia by pairing field sensors with immutable records, boosting yields by up to 60% while trimming operating costs by 20% [4]Amazon Web Services, “FarmPro boosts yields for 30,000 farmers,” press.aboutamazon.com. Huawei Cloud’s Pangu 5.5 stack supplies synthetic lidar and video data that feed directly into blockchain-anchored audit logs, expanding use cases into autonomous logistics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited interoperability across blockchain networks | –8.3% | Global, complex enterprise environments | Medium term (2-4 years) |

| Regulatory uncertainty on cross-border data/crypto rules | –6.7% | Global, jurisdiction-specific | Long term (≥ 4 years) |

| Scalability and energy-use concerns in public chains | –4.9% | Global, public-chain adopters | Short term (≤ 2 years) |

| Shortage of Web3 talent for enterprise projects | –3.8% | Emerging markets in particular | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Interoperability Across Blockchain Networks

Supply-chain partners often operate disparate ledgers that fail to communicate natively, forcing costly middleware builds. Hyperledger Cacti and other cross-chain frameworks are advancing, yet the absence of universally accepted validation rules and dispute mechanisms prolongs deployment timelines. Enterprises with diverse vendor ecosystems remain wary of vendor lock-in, making interoperability a strategic prerequisite before large-scale rollouts.

Regulatory Uncertainty on Cross-Border Data/Crypto Rules

The European Union’s MiCA regulation offers a compliance foundation, but interpretations differ across member states, complicating projects that span production, logistics, and finance flows within a single blockchain. Data-sovereignty statutes such as GDPR challenge immutable architectures, while the legal enforceability of smart contracts remains unsettled in several jurisdictions. Consequently, multinational corporations pause expansions until clarity emerges, dampening near-term growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Anchor Ecosystem Evolution

Platform offerings accounted for 56.62% of the blockchain supply chain market size in 2025, underscoring enterprise appetite for scalable backbones that serve multiple use cases. Vendor roadmaps emphasize modular APIs, AI-powered analytics, and integration accelerators that embed blockchain into existing MES, WMS, and ERP systems. Services, projected to rise at a 48.10% CAGR, include architecture design, data migration, change management, and managed operations packages. As pilot programs graduate to production, enterprises redirect budgets from experimentation to long-term operational support.

Implementation proof points such as IBM Food Trust highlight how unified platforms condense deployment cycles and foster network effects among suppliers and regulators. The blockchain supply chain market size tied to professional services is further amplified by partner ecosystems that bundle cybersecurity, tokenomics, and continuous-compliance modules, creating recurring revenue streams for system integrators.

By Blockchain Type: Hybrid Configurations Gain Momentum

Public architectures held 42.10% revenue share in 2025, owing to open validation and easy onboarding for diverse partners. Yet sensitivity around pricing models, supplier lists, and contract terms drives many corporates toward hybrid frameworks combining on-chain transparency with permissioned data enclaves. The hybrid sub-segment is projected to register a 49.20% CAGR, reflecting the balance between network reach and data privacy.

VeChain’s weighted delegated proof-of-stake update, rolled out via its StarGate program, epitomizes this shift. The design gives enterprise nodes governance influence while preserving public verification guarantees. As national data-residency laws tighten, hybrid deployments allow regional segmentation without sacrificing global synchronization, promoting adoption in industries with sensitive formulation or defense supply chains.

By Deployment Model: Cloud Delivery Lowers Barriers

Cloud-hosted networks seized 60.72% of the blockchain supply chain market share in 2025, and their 49.40% projected CAGR signals sustained preference for managed infrastructure. AWS, Microsoft, and Google allocate dedicated nodes, compliance blueprints, and pay-as-you-go token management that shorten proof-of-concept stages from months to weeks. This flexibility lets companies pilot regionally and scale globally without capex or specialist DevOps teams.

On-premise setups still resonate with firms bound by strict air-gap mandates or latency-sensitive factory-floor controls. However, cloud-native connector kits now link on-prem ledger slices to public chains, making hybrid cloud the default trajectory for multinational manufacturers looking to harmonize data across continents.

By Organization Size: SMEs Accelerate Network Effects

Large enterprises represented 50.75% of 2025 spend, leveraging mature IT estates to integrate blockchain into workflow orchestration. Yet SMEs are forecast to outpace at 50.10% CAGR as subscription-based platforms eliminate steep entry costs. Low-code dashboards and pre-configured smart-contract libraries empower smaller suppliers to meet master-contractor data mandates without in-house blockchain engineers.

Service providers such as Tata Consultancy Services are building SME-centric accelerators that merge generative AI with blockchain data ingestion, elevating usability while embedding predictive analytics capabilities.

By Application: Smart Contracts Redefine Efficiency

Product traceability delivered 37.55% of 2025 revenue, laying the groundwork for higher-order applications. Smart contracts, set to expand at a 50.60% CAGR, auto-enforce service level agreements, trigger escrow releases, and administer parametric insurance payouts on cargo delays. This reduces counterparty friction and frees finance teams to focus on exception management. Payment and settlement solutions leveraging stablecoins are gaining traction in cross-border B2B trade, while counterfeit-prevention modules help luxury and pharma brands address gray-market leakage.

Geography Analysis

North America secured 39.15% of 2025 revenue, energized by early-mover enterprises, robust venture funding, and comparatively clear legal frameworks. Walmart, Home Depot, and major automotive OEMs anchor multi-tier networks that funnel adoption down their supply chains. US regulators have issued guidance clarifying digital record admissibility, easing auditor concerns. Canada emphasizes natural-resource traceability, whereas Mexico leverages blockchain for near-shoring logistics transparency.

Asia-Pacific is on track for a 50.30% CAGR, driven by China’s state-backed Belt and Road blockchain trade corridors, Japan’s Society 5.0 digitization blueprint, and India’s PLI-backed manufacturing expansion. Government-sponsored sandboxes fast-track pilots in cross-border duties, e-invoice authentication, and carbon-credit clearinghouses. Australia’s mining exporters adopt ledger-anchored emissions reporting to satisfy global buyers’ ESG scrutiny.

Europe’s momentum comes from stringent sustainability legislation. Digital Product Passport mandates require granular lifecycle data, steering manufacturers toward blockchain-enabled traceability. Germany’s Industry 4.0 clusters integrate blockchains with IoT and 5G factory networks, while the United Kingdom focuses on supply-chain finance tokenization aligned to its fintech strengths. Emerging hubs in the Middle East, South America, and Africa adopt ledger solutions to streamline customs processing and boost trade-port competitiveness.

Regulatory Landscape

Supply chain blockchain deployments increasingly align to formal digital-trust and provenance regimes rather than ad hoc pilots. In the European Union, Commission Implementing Regulation (EU) 2025/2531 established technical standards for qualified electronic ledgers under the eIDAS 2.0 framework, creating a clearer pathway for DLT-based trust services that support legally recognized records and audit trails across multi-party supply chains.

Standards and public programs are also tightening operational guidance for trade and traceability workflows. ISO published ISO 5909:2026 for electronic bills of lading based on DLT, while the European Commission advanced Digital Product Passport interoperability through Commission Implementing Decision (EU) 2026/1736 (harmonized standards supporting DPP data exchange). In the United States, the House passed H.R. 1664 (Deploying American Blockchains Act of 2025), directing a Department of Commerce program focused on blockchain deployment for competitiveness and supply chain resiliency, reinforcing government-backed adoption channels alongside technical references such as NIST IR 8536 (Second Public Draft, 2025).

Value Chain Analysis

The value chain begins with enterprise blockchain platforms and blockchain-as-a-service stacks (cloud infrastructure, node services, identity and key management). Systems integrators and engineering firms follow, designing network governance, data models, and integrations to ERP/TMS/WMS and IoT telemetry. Data origination comes from manufacturers, tiered suppliers, logistics providers, and customs and trade documentation actors, who feed event data (production lots, shipments, handoffs, inspections) into smart contracts and shared ledgers. Downstream, auditors, regulators, and financial institutions consume verifiable records for compliance reporting, dispute resolution, and trade finance or invoice settlement.

Recent activity points to where value capture is shifting. Logistics operators and customs documentation workflows are becoming prime insertion points, as shown by Teleport partnering with The Hashgraph Group (April 2026) to develop a digital customs documentation system using Hedera Consensus Service. At the same time, OEM distribution networks are using private blockchain layers for interoperable visibility, reflected in XPENG selecting Vinturas (March 2026) for a private blockchain network across its European finished-vehicle distribution. Bottlenecks remain around interoperability with legacy enterprise systems, data ownership and governance across partners, and cross-network standards, which sustains demand for middleware, shared identifiers, and integration accelerators delivered by major platform vendors and integrators.

Competitive Landscape

Vendor diversity keeps concentration low as incumbents and niche specialists coexist. IBM, Microsoft, Oracle, and SAP embed blockchain into established ERP suites, capturing clients that value single-vendor accountability. Their offerings emphasize scalability, enterprise-grade security, and integration with analytics and AI modules.

Specialists such as VeChain, OriginTrail, and Ambrosus focus on sector-specific pain points, including sustainability incentives, pharmaceutical serialization, and cold-chain integrity. Hardware and cloud providers like Huawei and AWS extend value by coupling edge-sensor data ingestion with tamper-proof ledger storage.

IBM and SAP pledged deeper integration of generative AI and blockchain workflows, aiming to unify contract analytics with traceability data. Meanwhile, security innovation advances via hardware key-custody modules leveraging TEEs and HSMs. As interoperability frameworks mature, alliances between public-chain foundations and enterprise software leaders are set to reshape the vendor map.

Blockchain Supply Chain Industry Leaders

IBM Corporation

Oracle Corporation

Microsoft Corporation

SAP SE

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-led traceability programs and standardized digital-trust frameworks are creating near-term whitespace for blockchain as a verifiable record and anchoring layer, particularly where multi-party data must be shared without a single controlling intermediary. The EU Digital Product Passport Registry going live (July 2026) creates a concrete integration surface for product identifiers and metadata across sectors, and blockchain-based anchoring becomes a design option for provenance integrity when enterprises need tamper-evident auditability across suppliers, logistics partners, and assurance providers. This fits with enterprise deployments already running at production scale in traceability and compliance workflows, including Walmart-style recall traceability patterns and DNV-style consumer-facing provenance disclosures.

A second opportunity area is digitized trade documentation and settlement, where blockchain can connect shipping events to finance triggers. ISO 5909:2026 for DLT-based electronic bills of lading reduces process ambiguity for cross-border usage, and initiatives such as Teleport and The Hashgraph Group building digital customs documentation (April 2026) show commercial momentum in logistics paperwork modernization. Payments and reconciliation also remain an active application lane through on-chain settlement constructs used in transportation and logistics, supported by cloud deployment (already the dominant delivery model in 2025) and by enterprise requirements for interoperability layers that connect IoT telemetry and back-office systems into a continuous compliance record.

Recent Industry Developments

- May 2026: SAP introduced Autonomous Supply Chain Management capabilities at SAP Sapphire, highlighting Joule Assistants and Industry AI scenarios across planning, manufacturing, and logistics. The initiative strengthens the control-tower and orchestration layer that many blockchain traceability projects integrate with, shifting buyer attention toward end-to-end workflow automation and data harmonization.

- February 2026: Oracle released new AI agents for Oracle Fusion Cloud Supply Chain and Manufacturing, enabled through Oracle AI Agent Studio for Fusion Applications. For blockchain supply chain use cases, this expands the scope for automated exception handling and document processing around provenance, compliance, and supplier collaboration data that can be anchored to ledgers.

- June 2025: Oracle launched Oracle Trade and Supply Chain Finance Cloud to help banks speed access to capital and digitize financing workflows. The rollout supports tokenization and smart-contract-adjacent settlement patterns in supply chain finance, increasing the relevance of verifiable shipment and invoice events generated by multi-party blockchain networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks revenue earned from blockchain platforms and related services that are implemented to run supply chain processes, including traceability, compliance records, and smart contract based workflows. The figures are reported in USD across major regions.

Scope exclusions: We exclude internal IT labor that is not billed externally, pure crypto trading activity, and generic database upgrades that do not use blockchain for supply chain use cases.

Segmentation Overview

- By Component

- Platform

- Services

- By Blockchain Type

- Public

- Private

- Consortium

- Hybrid

- By Deployment Model

- Cloud

- On-premise

- By Organization Size

- Large Enterprises

- SMEs

- By Application

- Payment and Settlement

- Product Traceability

- Counterfeit Detection

- Smart Contracts

- Risk and Compliance Management

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of the Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and build a practical set of adoption and spend signals that can be repeated year after year. We referenced public sources such as the World Bank, OECD digital economy publications, UN Comtrade trade statistics, NIST guidance publications, and WIPO patent data. These inputs were used to understand digitization readiness, cross-border shipment intensity, and the direction of enterprise blockchain innovation.

To link those indicators to real buying behavior, we also reviewed company filings, product documentation, press releases, and industry association pages describing traceability programs and compliance needs. In parallel, we used paid subscription sources for company financials and news screening, along with a patent database for keyword based trend checks, so key assumptions could be anchored to observable activity. This list is not exhaustive, and we also consulted other public and paid sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were completed with supply chain technology decision makers, system implementers, and solution specialists across key regions to validate adoption timing and typical deal structures. The respondent input helped confirm which use cases get funded first, such as product traceability and risk and compliance reporting, and then to align pricing ranges and rollout pace with what buyers are actually purchasing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 18% | APAC: 40% |

| Mid tier: 49% | Functional/Unit leaders: 37% | EMEA: 36% |

| Smaller Players: 18% | Managers: 45% | Americas: 24% |

Market-Sizing & Forecasting

Our sizing starts with a top-down demand pool build tied to enterprise supply chain digitization needs and then maps those needs to blockchain specific adoption. We convert the resulting adoption view into revenue using realistic pricing and rollout assumptions. In practice, we map where blockchain is chosen as the system of record for traceability, counterfeit detection, smart contracts, and risk and compliance, and then estimate the annual spend captured by platforms and services.

To keep the totals grounded, we cross check against selective bottom-up approximations, including sampled contract values from public announcements, channel feedback on typical implementation scope, and a simple volume times ASP check for active deployments. Key model inputs include the pace of cloud based deployments versus on-premises, the share of consortium and private networks used for enterprise programs, average implementation duration, the service to platform revenue mix over the first two years of a rollout, and region level adoption timing differences that were validated through interviews.

For forecasting, we used scenario analysis with multivariate regression style checks. Drivers such as trade intensity proxies, compliance pressure, and enterprise digital investment cycles guide the slope, and then expert feedback is used to keep growth rates within credible rollout capacity. Where bottom-up signals were missing for smaller geographies or niche use cases, we filled gaps by applying peer region adoption patterns and then re-testing totals with interview based sanity checks before finalizing the curve.

Data Validation & Update Cycle

Validation is done through multiple passes, since early enterprise technology markets can show sharp swings when a single assumption changes. We compare outputs against independent signals such as public pilot to production conversions, patenting direction, and the pace of compliance led traceability programs. When we see unusual jumps, we trace them back to specific inputs for correction.

Before sign-off, the model is reviewed by another analyst to confirm that definitions, unit economics, and regional splits follow the same logic across both the full history and forecast. Reports are refreshed annually, and interim updates are triggered when material events occur, such as a major regulation shift, a step change in enterprise adoption, or a clear pricing reset. Right before delivery, we run a final pass so clients receive the latest updated view rather than an earlier snapshot.

Mordor Intelligence's Blockchain Supply Chain Market Estimate Compared With Other Published Estimates

Published market sizes for blockchain in supply chain often differ, even when the topic label looks the same, because the underlying spend being counted is not always consistent. The main drivers are what gets treated as supply chain scope, how platform versus services revenue is handled, and how quickly adoption is assumed to move from pilots to scaled deployments.

Publicly visible program activity and contract announcements, when paired with interview confirmed pricing ranges and rollout durations, are used as checks to connect Mordor Intelligence to a 2025 market size of USD 1.20 B, rather than a wider number that may include broader enterprise blockchain or adjacent logistics software spend. The remaining spread across published figures is commonly explained by whether payments and settlement use cases are counted inside supply chain, how cloud subscriptions are annualized, and whether aggressive scenario curves are reported as the main case.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.20 B (2025) | |

| Trade Journal A | USD 3.27 B (2025) | Uses a broader definition that can blend supply chain blockchain with wider enterprise blockchain adoption, and it often reports fast scaling assumptions without separating platform revenue from services timing. |

| Regional Consultancy B | USD 4.02 B (2025) | Likely includes adjacent spend such as general logistics software digitization and multi-industry blockchain programs, and it can apply higher average contract values without consistent checks against rollout durations. |

Across the table, the main takeaway is that scope and revenue treatment drive most of the gap, not a disagreement that adoption is rising. By keeping the counted revenue tied to identified supply chain use cases and to repeatable pricing and rollout inputs, the final number stays transparent and easier to re-create when clients update their own assumptions.

Key Questions Answered in the Report

How fast is the blockchain supply chain market expected to grow to 2031?

It is forecast to expand from USD 1.2 billion in 2025 to USD 12.41 billion by 2031 at a 47.65% CAGR.

Which region will add the most new revenue through 2031?

Asia-Pacific, projected to advance at a 50.30% CAGR on the back of government-backed digital-trade programs and manufacturing modernization.

What segment leads current spending?

Platform solutions command 56.62% of 2025 revenue as enterprises prefer scalable backbones that support multiple use cases.

Why are smart contracts drawing heightened interest?

They automate SLA enforcement and payment triggers, helping reduce invoice-processing cycle times by up to 90% in production environments.

What is the biggest hurdle to wider enterprise adoption?

Interoperability gaps between disparate blockchains, which add integration cost and prolong deployment timelines.

How are SMEs participating despite limited IT budgets?

Subscription-based cloud platforms offer low-code dashboards and pre-built smart-contract libraries, allowing SMEs to meet upstream data-sharing mandates without hiring blockchain specialists.

Page last updated on: