Blockchain In Media, Advertising, And Entertainment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

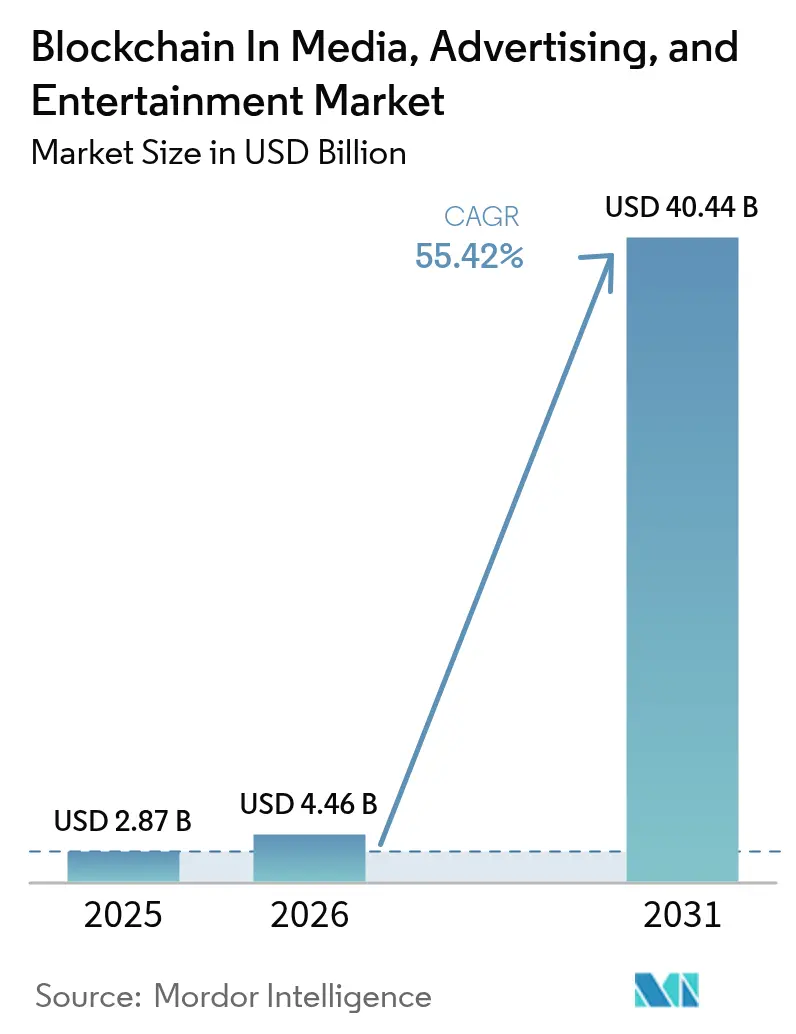

| Market Size (2026) | USD 4.46 Billion |

| Market Size (2031) | USD 40.44 Billion |

| Growth Rate (2026 - 2031) | 55.42% CAGR |

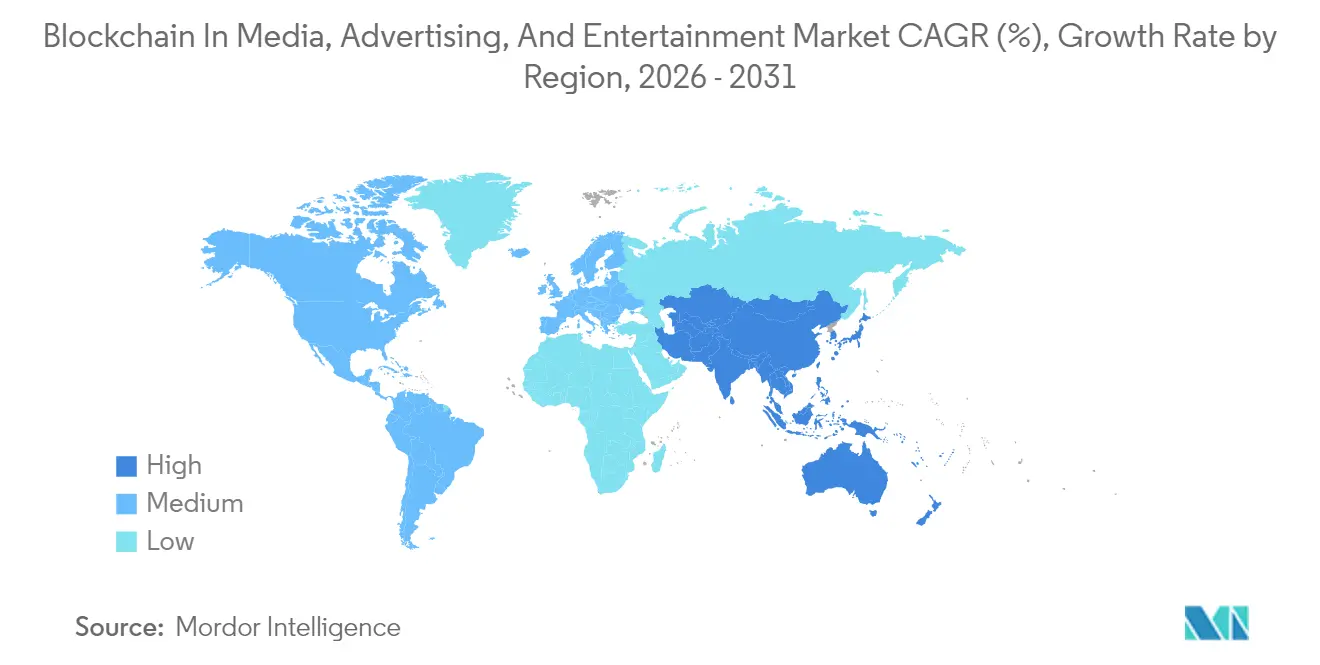

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain In Media, Advertising, And Entertainment Market Analysis by Mordor Intelligence

The blockchain in media, advertising, and entertainment market size in 2026 is estimated at USD 4.46 billion, growing from 2025 value of USD 2.87 billion with 2031 projections showing USD 40.44 billion, growing at 55.42% CAGR over 2026-2031. Surging creator demand for direct monetization, advertisers’ insistence on verifiable ad metrics, and rights holders' push for automated royalties collectively propel the blockchain in the media, advertising, and entertainment markets, while permissioned networks balance transparency with content-access controls. Public chains captured early share thanks to NFT liquidity, yet consortium and hybrid architectures are scaling fast as studios protect prerelease assets. Large enterprises currently dominate spending, but falling integration costs enable smaller studios to deploy blockchain in weeks, thereby broadening the user base. Regionally, North America supplies a high share of revenue, yet the Asia-Pacific now shows the steepest growth trajectory as public policy initiatives converge with a digitally savvy fan base. All told, the blockchain in media, advertising, and entertainment markets continues to reward innovators who link programmable money, tokenized IP, and audience engagement into a single frictionless loop.

Key Report Takeaways

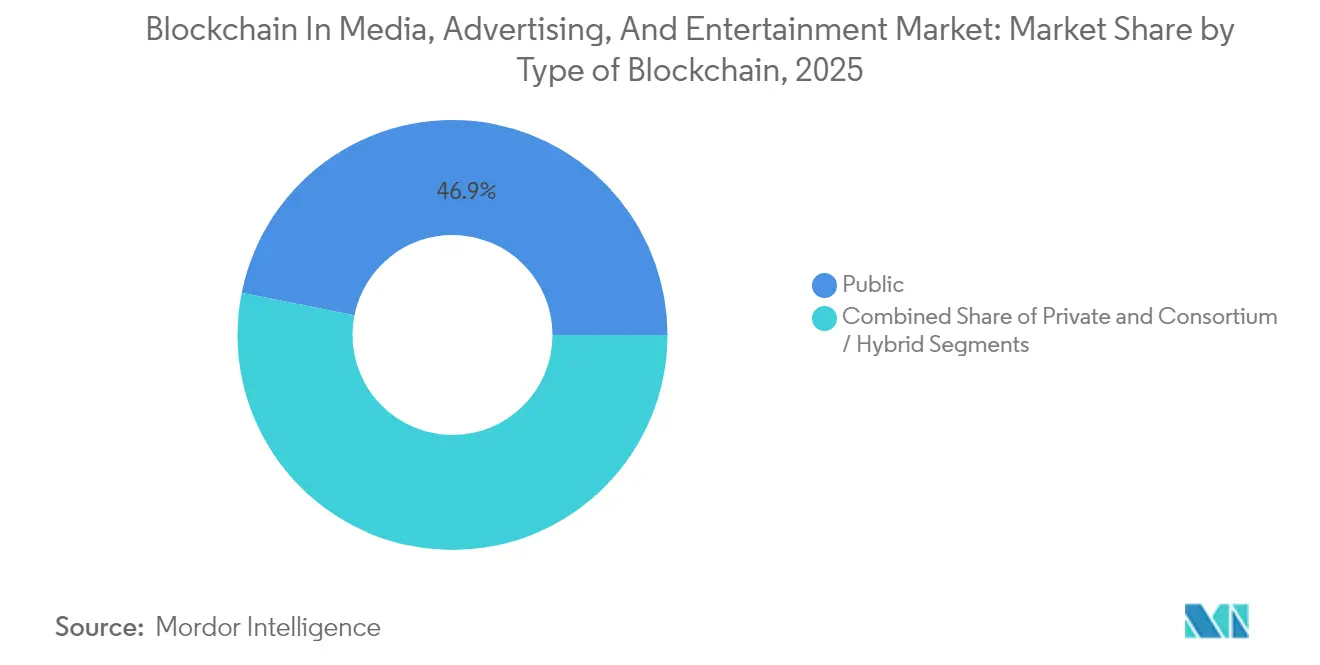

- By type of blockchain, public chains held 46.85% of the blockchain in media, advertising, and entertainment market in 2025, while consortium and hybrid models are forecast to expand at a 60.02% CAGR through 2031.

- By enterprise size, large enterprises commanded 63.10% of the blockchain in media, advertising, and entertainment market size in 2025, whereas small and medium enterprises are expected to advance at a 59.85% CAGR to 2031.

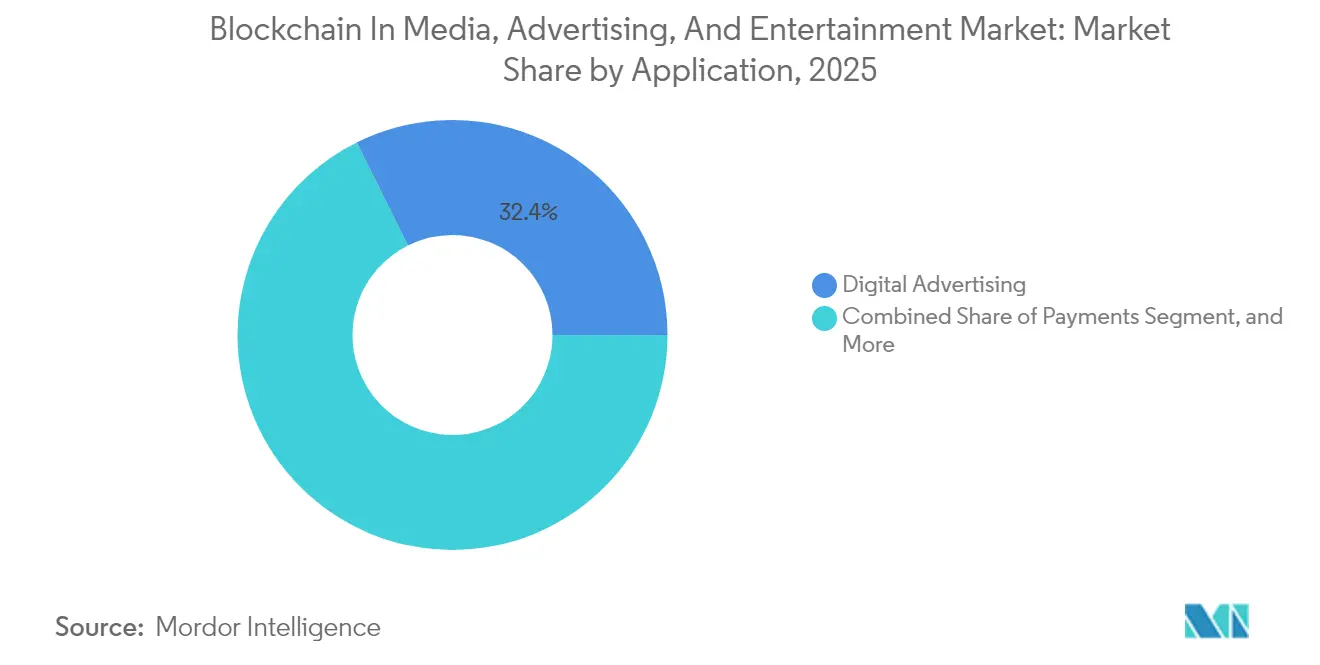

- By application, digital advertising led with 32.35% revenue share of the blockchain in media, advertising, and entertainment market in 2025; licensing and rights-management smart contracts are projected to accelerate at a 61.35% CAGR through 2031.

- By media segment, gaming accounted for 30.55% of the spending on blockchain in the media, advertising, and entertainment market in 2025, but sports tokenization is poised for a 60.95% CAGR toward 2031.

- By geography, North America contributed 38.40% of the revenue in the blockchain in media, advertising, and entertainment market in 2025, while the Asia-Pacific is set to lead the field with a 60.35% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blockchain In Media, Advertising, And Entertainment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commoditization of Content and Piracy | +8.5% | Global, acute in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Disintermediation between Creators and Audience | +9.2% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Demand for Secure and Faster Transactions | +7.8% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Need to Curb Programmatic Advertising Fraud | +8.1% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Decentralized Autonomous Production Studios | +6.4% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Tokenization of Royalty Streams | +10.3% | Global, early traction in music and film | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tokenization of Royalty Streams

Tokenizing royalties embeds payout logic into smart contracts that execute instantly when content is streamed or screened, compressing settlement cycles from close to two years to near real-time.[1]Royal, “Tokenized Music Royalties Platform,” royal.io Independent musicians receive 85-95% of streaming income, a sharp reversal of legacy splits, while fans obtain fractional ownership in song catalogs, deepening loyalty and liquidity. Venture funding reached USD 55 million in 2024 for startups that fractionalize back-catalog assets, signalling strong investor confidence in the blockchain in the media, advertising, and entertainment market. Film studios are piloting similar models, using on-chain box-office oracles to trigger residuals and eliminate accounting disputes. As these contracts eliminate reconciliation friction, they help expand blockchain adoption in the media, advertising, and entertainment markets, with increased penetration across music and visual media.

Disintermediation between Creators and Audience

Blockchain video networks enable creators to stream content directly to viewers without surrendering 30-50% of their platform fees, thereby securing higher margins and reducing cash-collection cycles.[2]Theta Labs, “Decentralized Video Delivery Network,” thetatoken.org Theta’s edge-node incentives drop delivery costs by roughly 60%, while NFT pre-sales now bankroll independent films before cameras roll. Cross-border micro-payments in stablecoins circumvent currency controls, turning globally scattered fan communities into instant financiers. Pilot data from 2024 indicate that over 40 projects have been funded through NFT sales, demonstrating tangible momentum behind the blockchain in the media, advertising, and entertainment sectors. In regions with patchy banking rails, creators collect funds in minutes rather than weeks, underscoring blockchain’s ability to undercut entrenched intermediaries.

Need to Curb Programmatic Advertising Fraud

Ad fraud siphoned USD 84 billion from marketers during 2024, a loss that galvanized adoption of blockchain verification layers. Brave, AdEx, and similar networks log every impression on-chain and pay publishers only after fraud-detection oracles confirm human engagement. Early brand pilots report reductions in fraud of 30-40% and improved return on ad spend, bolstering the appeal of blockchain in media, advertising, and entertainment markets to advertisers. Immutable audit trails simplify reconciliations and shift budgets toward premium inventory. Video formats, once vulnerable to domain spoofing, now gain cryptographic proof of placement, restoring trust in programmatic campaigns.

Demand for Secure and Faster Transactions

Cross-border licensing once relied on SWIFT wires, which consumed up to 5-7 business days and 3-5% of the deal value. In 2024, distributors began settling film rights with USDC in ten minutes, sidestepping forex spreads and chargeback risk. Stablecoin rails also enable sub-USD micro-transactions, reviving pay-per-view and in-game purchase models that were previously unviable. Live-event broadcasters lock in rights hours before kickoff and settle instantly, a capability essential for real-time sports coverage. As transaction risk decreases, more stakeholders become involved with the blockchain in the media, advertising, and entertainment markets, thereby reinforcing network effects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Standardization and Interoperability | -5.7% | Global, acute in fragmented enterprise deployments | Medium term (2-4 years) |

| Expensive and Time-Consuming Deployment | -4.2% | Global, disproportionate impact on SMEs | Short term (≤ 2 years) |

| Regulatory Uncertainty for Tokenized Revenue | -6.1% | North America and Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Carbon Footprint Concerns | -3.8% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardization and Interoperability

Digital assets minted on Ethereum seldom interoperate natively with rights contracts on Polygon, forcing right-holders to juggle parallel inventories.[3]InterWork Alliance, “Token Taxonomy Framework,” interwork.org Only a fifth of media projects have implemented emerging token-taxonomy frameworks, limiting asset portability and liquidity. Bridge protocols like CCIP and LayerZero facilitate transfers while incurring gas costs and introducing additional attack surfaces, as they lack shared metadata schemas for sync and mechanical licenses, and automated royalty aggregation stalls. Consequently, enterprises may delay investment, tempering their adoption of blockchain in media, advertising, and entertainment markets until standards converge.

Regulatory Uncertainty for Tokenized Revenue

Divergent rules blur the distinction between NFTs and fan tokens, making it unclear whether they qualify as securities. The U.S. Securities and Exchange Commission issued multiple Wells notices in 2024, chilling some launches. Meanwhile, Europe’s MiCA framework demands costly registration yet offers clarity. Studios tackling global audiences must geo-block certain regions, adding compliance overhead that smaller creators cannot absorb. Inconsistent tax treatment further complicates ROI calculations, encouraging pilot-only projects in more favorable jurisdictions like Singapore. Resolution of these gray areas remains pivotal for scaling the blockchain in the media, advertising, and entertainment industries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Blockchain: Hybrid Models Gain Enterprise Trust

Consortium and hybrid networks are projected to grow at a rapid 60.02% CAGR, far outstripping public-chain momentum, despite public blockchains holding 46.85% of the blockchain in media, advertising, and entertainment market in 2025. Permissioned governance offers selective data disclosure, a must for studios guarding prerelease content. Hybrid models hash contract fingerprints onto Ethereum, preserving public auditability while keeping deal terms private, thereby mitigating the risk of leaks. Private Hyperledger instances reached 5,000 TPS during a Hollywood pilot, reaffirming the performance edge for post-production workflows. Yet, public chains retain value for creators chasing global NFT liquidity, underscoring a dual-stack future across the blockchain in the media, advertising, and entertainment market.

Hybrid adoption also benefits from on-chain privacy tools, such as zero-knowledge proofs, which mask sensitive fields while allowing public confirmation of royalty splits. Studio consortia can now validate that payments occurred without exposing exact amounts to rivals. As open-source frameworks mature, integration friction falls, encouraging more mid-tier broadcasters to migrate. Over the forecast horizon, hybrid architectures are expected to anchor 40% of new deployments, solidifying their status as the default enterprise pattern for the blockchain in the media, advertising, and entertainment market.

By Enterprise Size: SMEs Accelerate Adoption

Although large enterprises controlled 63.10% of transactional value in 2025, SMEs are closing fast with a 59.85% CAGR through 2031. Ready-made contract templates from Thirdweb and Alchemy shrink development cycles from months to weeks. Managed node services on AWS and Azure, further lower cost, letting studios spin up environments for under USD 50,000, compared with six-figure custom builds earlier. An artist survey revealed that blockchain usage is expected to triple to 38% by 2024, highlighting grassroots momentum across the blockchain in media, advertising, and entertainment market.

SME traction is especially acute in South America and Southeast Asia, where creators lack entrenched distribution partners yet boast large online audiences. Token-gated streaming concerts in Brazil attracted 5,000 artists within six months, demonstrating that small players can punch above their weight when equipped with Web3 infrastructure. As no-code tooling proliferates, SMEs could surpass large enterprises in new project count by 2028, tilting the competitive balance within the blockchain in the media, advertising, and entertainment market.

By Application: Smart Contracts Redefine Rights Management

Digital advertising still leads revenue at 32.35%, but licensing and royalty smart contracts are racing ahead at 61.35% CAGR. A blockbuster film encoded its waterfall into Solidity in 2024, triggering payouts within 48 hours of box-office reports, replacing quarterly checks and auditors. Transparent ledgers eliminate reconciliation disputes and reduce legal overhead. Stablecoin rails support instant cross-border settlements, making smart contracts the killer app inside the blockchain in media, advertising, and entertainment market.

Payments and gaming hover in the mid-teens share zone, while live streaming grows from a smaller base as decentralized video networks deliver 90-95% revenue retention for creators. Ancillary uses such as supply-chain tracking for merchandise and anti-counterfeit labeling remain niche but are on the rise. The pivot from speculative NFT drops toward workflow automation signals a maturation phase across the blockchain in media, advertising, and entertainment industries.

By Media Segment: Sports Tokenization Accelerates

Sports franchises now tokenize tickets, memorabilia, and governance rights, driving a blistering 60.95% CAGR, outpacing gaming’s still-hefty 30.55% share. European football clubs alone issued 50 fan tokens in 2024, raising USD 300 million and letting supporters vote on jersey designs. NFT-based tickets hard-code resale caps, clawing back USD 1.5 billion that once slipped to scalpers. Such traction positions sports as the innovation lab of the blockchain in media, advertising, and the entertainment market.

Music and film trails in the mid-teens share but ride the tailwinds from catalog tokenization and NFT crowdfunding alike. Advertising content leverages brand-minted collectibles that reward engagement, lifting recall by 25-30% compared with static banners. Though news-and-publishing use cases remain early, deepfake concerns are nudging publishers toward immutable content logs, hinting at future upside for the blockchain in media, advertising, and entertainment market.

Geography Analysis

North America contributed 38.40% of the revenue in 2025, with California studios accounting for over 60% of the regional spend amid robust venture backing. Canada’s tax incentives anchor blockchain gaming in Toronto and Vancouver, whereas Mexico’s adoption lags but gains impetus from remittance-driven stablecoin flows. The region’s early lead shifts focus toward scaling concerns, cross-chain orchestration, and regulatory compliance platforms; yet, its growth rate now trails emerging hotspots, reflecting market maturity within the blockchain industry in media, advertising, and entertainment.

Asia-Pacific is forecast to soar at 60.35% CAGR, the fastest worldwide. China’s state-run Blockchain-based Service Network enables compliant NFT-like “digital collectibles,” circumventing crypto trading bans. Japan’s Web3 roadmap supplies tax carve-outs that spur Sony and Bandai Namco to launch blockchain games. India’s Bollywood NFTs target a vast diaspora, and South Korea’s K-pop tokens sell out instantly, generating templates for fan-sourced financing. Australia and Southeast Asia contribute modest shares today but capitalize on improved payment rails by integrating blockchain technology into regional content-export strategies that stitch together the media, advertising, and entertainment market.

Europe, South America, the Middle East, and Africa fill the remainder. MiCA provides legal certainty that accelerates the development of German and U.K. rights registries. France’s luxury houses merge couture with film NFTs, enhancing experiential marketing. Brazil and Argentina utilize stablecoins to mitigate the drag of inflation, although infrastructure deficits slow their adoption. Dubai and Riyadh leverage free-zone perks to magnetize Web3 studios, while Nigeria pilots blockchain music streams targeting diaspora downloads. Collectively, these diverse initiatives underscore the global reach of blockchain in the media, advertising, and entertainment sectors.

Competitive Landscape

The marketplace remains fragmented, with no vendor exceeding a 10% share, resulting in a concentration score of 3. Cloud giants AWS, Microsoft, and Oracle package blockchain-as-a-service, locking in studios that value support contracts over maximum decentralization.[4]Microsoft, “Azure Blockchain for Media,” azure.microsoft.com Blockchain natives like Theta Labs and Livepeer chase creators with token incentives and revenue splits of 90 percent or more, vying to rearchitect video delivery models. Consulting integrators Accenture, Ernst and Young, Infosys monetize bespoke consortium builds and maintenance, bridging enterprise needs to protocol layers.

Differentiation arcs around decentralization versus governance. Public-chain advocates stress composability and global liquidity; enterprise leaders prize validator allowlists and private data channels. Zero-knowledge proof deployments attempt to reconcile both camps, enabling privacy on public rails, though production rollouts were scarce in 2024. ISO’s brand-new interoperability standard may accelerate vendor consolidation as protocols converge; yet, proprietary ecosystems defend incumbency for now, preserving fragmentation within the blockchain in the media, advertising, and entertainment market.

Looking forward, white-space opportunities exist for orchestration middleware that stitches public NFT markets to private studio ledgers. Chainlink CCIP and LayerZero already target this niche, and early adopters cite smoother asset mobility and shorter integration cycles as key benefits. Cross-chain services could become the kingmakers, granting them outsize influence over the blockchain in the media, advertising, and entertainment industry’s eventual platform hierarchy.

Blockchain In Media, Advertising, And Entertainment Industry Leaders

IBM Corporation

Microsoft Corporation

Ernst and Young Global Limited

The Bitfury Group Limited

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft Azure expanded its managed rights-management service to include ISO-compliant interoperability modules, cutting deployment times by 25%.

- November 2024: VeChain pilots video authenticity checks with a leading Chinese streamer, hashing 10,000 hours of footage.

- October 2024: Theta Labs partnered with Sony to embed decentralized video delivery into PlayStation streaming, shrinking bandwidth costs by 40%.

- October 2024: Infosys launched a media-centric blockchain consulting line in North America and Europe.

Global Blockchain In Media, Advertising, And Entertainment Market Report Scope

The report on the Blockchain in Media, Advertising, and Entertainment Market segments the industry by various criteria. These include the type of blockchain (public, private, and consortium/hybrid), enterprise size (small and medium-sized enterprises versus large enterprises), and application (covering areas such as licensing and rights management, digital advertising, smart contracts, payments, online gaming, live streaming, and more). Additionally, the media segments analyzed encompass music, film, TV, advertising content, gaming, sports, news, publishing, and other categories. Geographically, the report spans North America (including the United States, Canada, and Mexico), South America (with a focus on Brazil, Argentina, and the rest of the continent), Europe (covering Germany, the United Kingdom, France, Italy, Spain, Russia, and others), Asia-Pacific (highlighting China, Japan, India, South Korea, Australia, and the rest of the region), and the Middle East and Africa (with specific attention to Saudi Arabia, the United Arab Emirates, Turkey, South Africa, Nigeria, and Egypt). All market forecasts are expressed in terms of value (USD).

| Public |

| Private |

| Consortium / Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Licensing and Rights Management |

| Digital Advertising |

| Smart Contracts |

| Payments |

| Online Gaming |

| Live Streaming |

| Other Applications |

| Music |

| Film and TV |

| Advertising Content |

| Gaming |

| Sports |

| News and Publishing |

| Other Media Segments |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type of Blockchain | Public | ||

| Private | |||

| Consortium / Hybrid | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Appliaction | Licensing and Rights Management | ||

| Digital Advertising | |||

| Smart Contracts | |||

| Payments | |||

| Online Gaming | |||

| Live Streaming | |||

| Other Applications | |||

| By Media Segment | Music | ||

| Film and TV | |||

| Advertising Content | |||

| Gaming | |||

| Sports | |||

| News and Publishing | |||

| Other Media Segments | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the blockchain in media, advertising, and entertainment market in 2026?

It stands at USD 4.46 billion and is projected to grow sharply to USD 40.44 billion through 2031.

What is the forecast CAGR for blockchain in media and entertainment through 2031?

The market is expected to register a robust 55.42% CAGR from 2026 to 2031.

Which segment is expanding fastest within blockchain media applications?

Smart contracts for licensing and royalty management are advancing at a 61.35% CAGR.

Which region will witness the strongest growth?

Asia Pacific is set to record a 60.35% CAGR, outpacing all other regions.

Why are sports organizations embracing blockchain?

Tokenized tickets and fan tokens unlock new revenue and engagement, leading the sports vertical to a 60.95% CAGR.

What is the main barrier to wider blockchain adoption in media?

Regulatory ambiguity around tokenized revenue remains the most significant constraint.

Page last updated on: