Online Reputation Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

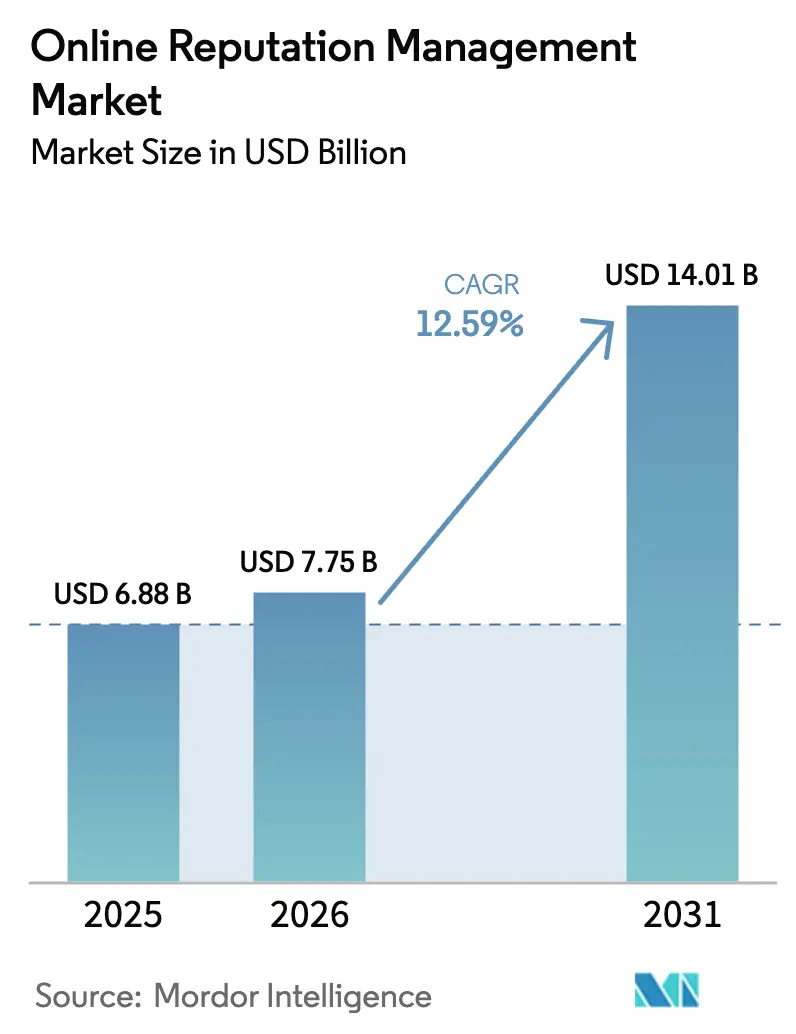

| Market Size (2026) | USD 7.75 Billion |

| Market Size (2031) | USD 14.01 Billion |

| Growth Rate (2026 - 2031) | 12.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Reputation Management Market Analysis by Mordor Intelligence

The online reputation management market size was valued at USD 6.88 billion in 2025 and estimated to grow from USD 7.75 billion in 2026 to reach USD 14.01 billion by 2031, at a CAGR of 12.59% during the forecast period (2026-2031). Growth is propelled by the tightening link between digital trust signals and buying behavior: 89% of United Kingdom shoppers consult ratings before purchasing decision. Artificial intelligence (AI) is now embedded across reputation workflows, from social-listening to automated response, while the October 2024 Federal Trade Commission (FTC) rule that fines fake reviews up to USD 51,744 per instance compels brands to adopt compliance-first platforms. Cloud deployment dominates because it scales AI inference across languages and channels, and small and medium enterprises (SMEs) are narrowing the capability gap through subscription software that removes heavy implementation costs. Sectoral momentum is strongest in healthcare, retail, and e-commerce, which all face intense public scrutiny and immediate revenue consequences when sentiment shifts.

Key Report Takeaways

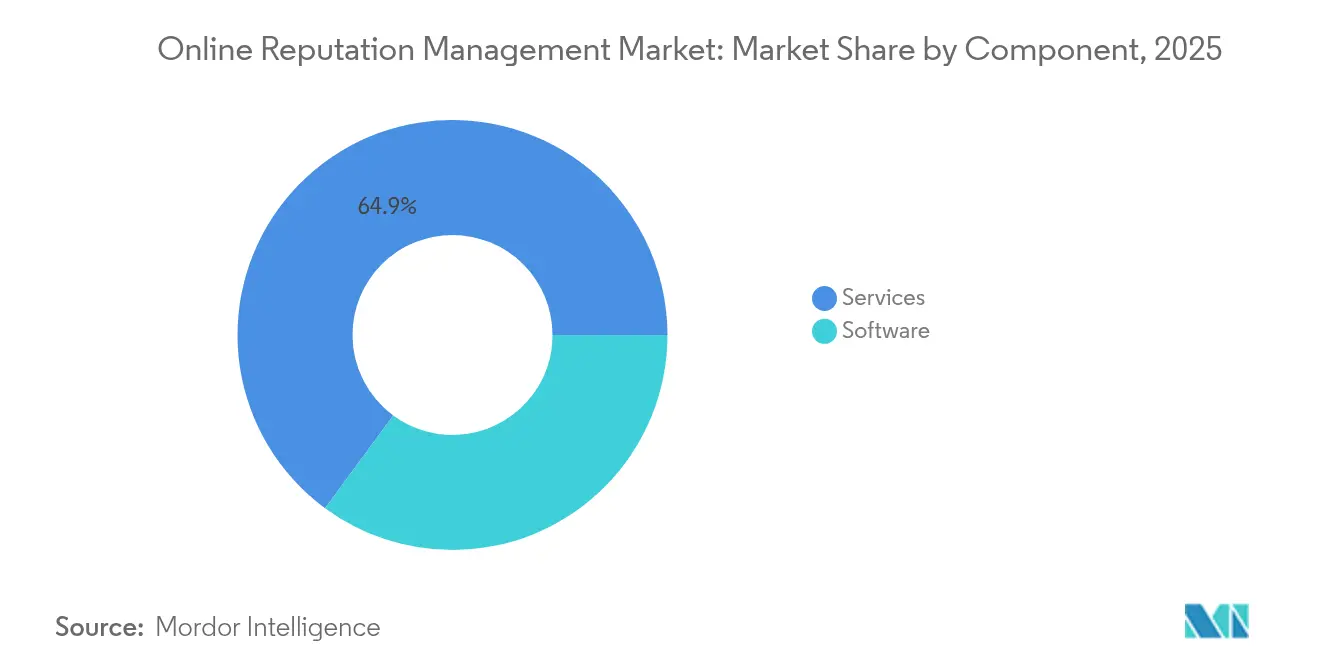

- By component, services held 64.90% of the online reputation management market share in 2025, while software is on track for a 17.09% CAGR to 2031.

- By enterprise size, large enterprises commanded 56.10% share in 2025; SME adoption is expanding at 16.68% CAGR.

- By deployment, cloud models controlled a 72.45% share in 2025 and are growing at an 18.14% CAGR.

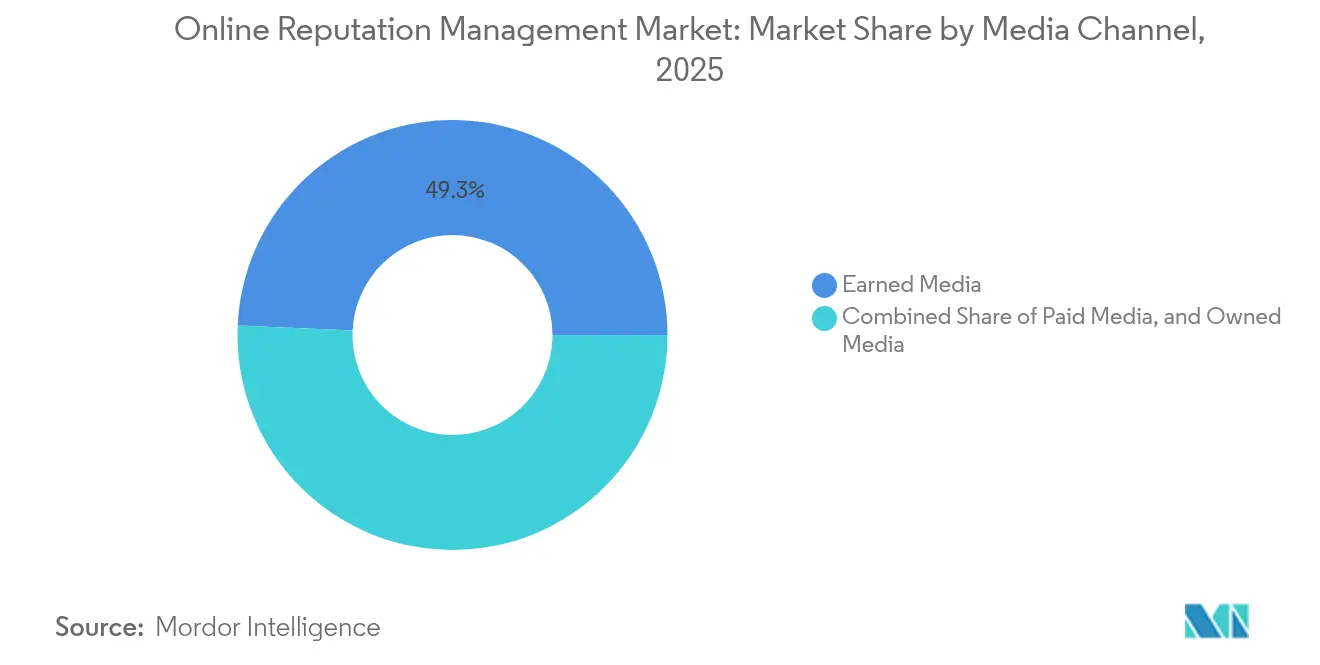

- By media channel, earned media captured 49.30% revenue in 2025; it also leads growth at 16.31% CAGR.

- By application, retail and e-commerce represented 24.20% of online reputation management market size in 2025, while healthcare is accelerating at 18.82% CAGR.

- By geography, North America accounted for 38.20% revenue in 2025; Asia-Pacific is advancing at 18.13% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Reputation Management Market Trends and Insights

Driver Impact Analyis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of e-commerce and digital-first brands | +2.1% | Global, with concentration in North America & Asia-Pacific | Medium term (2-4 years) |

| Social-media influence on purchase decisions | +1.8% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Online reviews as critical trust signals | +2.3% | Global | Short term (≤ 2 years) |

| Escalating reputational-crisis incidents | +1.5% | Global, heightened in North America & Europe | Medium term (2-4 years) |

| AI-driven sentiment analytics enable scale | +2.7% | North America, Asia-Pacific core, spill-over to Europe | Long term (≥ 4 years) |

| ESG-perception scores affect capital access | +1.2% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of E-commerce and Digital-First Brands

Pure-play online brands, operating without brick-and-mortar buffers, rely entirely on reputation dashboards to convert traffic into revenue. Their vulnerability to viral backlash increases adoption of 24-hour monitoring, multilingual alerting, and automated remediation. The FTC’s 2024 anti-fake-review rule makes authenticity non-negotiable, pushing platforms to certify review provenance and archive audit trails for potential enforcement actions[1]Federal Trade Commission, “FTC Finalizes Rule Banning Fake Reviews,” ftc.gov. Major marketplaces are simultaneously weighing reputation scores inside ranking algorithms, so a one-point dip can immediately suppress visibility. Consequently, spending on the online reputation management market is migrating from discretionary marketing budgets to mission-critical cost centers. The effect is most pronounced in Asia-Pacific, where social-commerce adoption outpaces traditional e-commerce, adding new channels that must be tracked in real time.

AI-Driven Sentiment Analytics Enable Scale

Natural-language processing models are now parsing sarcasm, emojis, and regional slang, lifting sentiment accuracy and predictive power. Early movers report 30% jumps in customer-satisfaction ratings and 50% declines in negative-press volume after embedding AI workflows. Cloud delivery provides elastic compute for continuous model retraining, a requirement when language trends evolve weekly. Integrations with customer-relationship-management (CRM) suites route high-risk cases directly to service staff, shortening resolution cycles. Vendors compete on transparency by surfacing model confidence scores and bias-mitigation protocols, a response to corporate compliance officers seeking defendable outputs. This capability gap is widening the competitive distance between AI-native platforms and manual service bureaus, accelerating the shift in the online reputation management market toward software.

Online Reviews as Critical Trust Signals

The modern consumer journey begins with peer endorsements: 77% of buyers scan reviews when selecting local businesses, and 79% expect a social-media response within 24 hours. Review economies have thus matured from feedback channels into public-credibility exchanges. The FTC now outlaws undisclosed incentives and fake testimonials, mandating clear sponsor declarations. Healthcare providers face an extra layer of complexity; HIPAA restrictions prevent them from revealing patient details when replying, yet patients increasingly choose doctors based on online ratings. Platforms serving this vertical encrypt identifiers and maintain segregated data stores to ensure compliance. The online reputation management market benefits as demand for healthcare-grade solutions outpaces generic tools.

ESG-Perception Scores Affect Capital Access

Environmental, social, and governance (ESG) narratives now influence lender risk models and institutional-investor screeners. The United States Securities and Exchange Commission (SEC) climate-risk disclosure mandates that took effect in March 2024 require public companies to publish carbon exposure scenarios. Banks have begun charging premium interest spreads to firms with low ESG sentiment, creating a direct financial incentive to monitor and improve reputational standing. AuditBoard notes that 90% of S&P 500 constituents now release sustainability reports, reflecting a shift from public-relations exercise to capital-markets imperative [2]AuditBoard, “2024 ESG Reporting Benchmark,” auditboard.com. Reputation platforms are embedding ESG dashboards that track commentary across investor calls, activist forums, and mainstream media. This converges with the online reputation management market’s expansion into finance teams that historically were outside the communications stack.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Free-speech and takedown legal limits | -1.4% | Global, particularly North America & Europe | Medium term (2-4 years) |

| High service costs for SMBs | -2.1% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Data-privacy regulations curb data use | -1.8% | EU, North America, expanding globally | Long term (≥ 4 years) |

| Opaque platform algorithms | -1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Service Costs for SMBs

Full-service reputation retainers often exceed USD 10,000 each year, yet the average small business devotes only USD 1,200 annually to all digital software spend. This mismatch creates a capability divide where large enterprises can afford AI-rich analytics while smaller firms monitor manually. Multi-tenant cloud architectures are reducing marginal costs, but pricing still reflects heavy data-processing overhead and specialized compliance staff. Vendors are responding with tiered offerings that prioritize alert triage and templated responses, delivering “good-enough” coverage while keeping fees below USD 100 per month. As cost elasticity remains a restraint, freemium models that upsell advanced reporting features may unlock latent demand and increase penetration of the online reputation management market among micro-enterprises.

Data-Privacy Regulations Curb Data Use

The European Union’s GDPR and the California Consumer Privacy Act require explicit consent for data collection, limit data retention periods, and introduce cross-border transfer hurdles. Nineteen United States states now enforce standalone privacy statutes, and more are poised to follow. Providers must maintain region-specific data stores, elevate encryption standards, and build consent-management modules, lifting operational costs. Data-localization rules can fragment global analytics, eroding the cross-market insights on which multinational brands rely. Privacy-preserving techniques such as differential privacy and on-device inference are emerging, but they remain technically complex and costly. Compliance drag is therefore subtracting up to 1.8 percentage points from the forecast CAGR of the online reputation management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Acceleration Drives Platform Innovation

Software captured the attention of budget holders by growing at 17.09% CAGR into 2031, signaling that automated analytics, not manpower, will dominate future workflows. The online reputation management market size for software platforms is forecast to climb sharply as enterprises embed APIs directly into CRM and marketing-automation stacks. Review-management suites apply machine learning to detect anomalous patterns that may signal paid review farms, a critical compliance safeguard under the FTC rule. Concurrently, sentiment dashboards are integrating generative AI to recommend response phrasing aligned with brand tone. Services remain essential for high-risk crisis management and regulatory guidance; their 64.90% online reputation management market share reflects deep domain expertise that software alone cannot fully replicate. However, margin pressure is intensifying as clients renegotiate hourly retainers in favor of hybrid, software-plus-consulting models.

In the services camp, demand persists for complex takedown negotiations, legal liaison, and multilingual public relations playbooks. Healthcare, financial services, and public-sector clients rely on consultancy teams to interpret regional regulations and craft compliant messaging. Yet the superior scalability of cloud tooling is shrinking engagement scopes. Platforms like Sprout Social now bundle listening, publishing, and case-management in a single interface, allowing in-house teams to handle volume previously outsourced. Over the forecast period, ecosystems that harmonize SaaS modules with expert advisory are expected to secure higher retention and expand the addressable slice of the online reputation management market.

By Enterprise Size: SME Adoption Narrows the Digital Trust Gap

Large enterprises accounted for 56.10% revenue in 2025, reflecting their need to guard brand equity across portfolios and geographies. These corporations integrate sentiment scores into business-intelligence dashboards and tie executive bonuses to net-promoter-score trajectories, elevating platform stickiness. Still, SME subscriptions are rising at 16.68% CAGR as vendors strip complexity from interfaces and offer pre-built workflows. Microsoft reports that 71% of small businesses linking software investments to revenue see tangible top-line gains . Such case studies validate the ROI narrative and widen funnel inflows.

Self-serve onboarding, drag-and-drop dashboards, and AI-drafted replies lower the skill barrier for time-constrained entrepreneurs. A cohort of micro-SaaS firms is packaging narrow use cases—like Google-Business-Profile optimization—at sub-USD 50 monthly price points, drawing previously unserved merchants into the online reputation management market. However, churn remains a risk when early-stage companies reprioritize cash flow, underscoring the importance of feature bundles that directly translate into revenue gains, such as review-to-webshop integration that posts positive ratings onto product pages in real time.

By Deployment Type: Cloud Dominance Reflects AI Compute Demands

Cloud solutions owned 72.45% of 2025 revenue and are expanding at 18.14% CAGR, a pattern inseparable from AI’s voracious appetite for compute. Real-time sentiment tracking requires elastic resources when viral spikes generate millions of mentions within hours. Hyperscale vendors deliver regionally redundant data centers that also solve latency concerns for multinational brands. The online reputation management market size associated with cloud deployments is on course to more than double by 2031 as even regulated industries adopt hybrid blueprints that isolate sensitive data locally but delegate model training to the cloud. On-premise suites endure in sectors like defense or banking where data sovereignty and internal-threat modeling override cost savings. Yet these clients increasingly request edge connectors into public-cloud AI services, becoming hybrid rather than strictly on-prem.

Cost transparency is another lure: subscription pricing converts capital expenditure into predictable operating expenses and avoids hardware refresh cycles. Cloud providers additionally shoulder regulatory audits, an advantage for companies without dedicated compliance teams. Security objections have softened as providers roll out zero-trust frameworks and end-to-end encryption with customer-managed keys. Consequently, competitive bids in the online reputation management market now rarely feature on-prem-only options unless mandated by statutory frameworks.

By Media Channel: Earned Media’s Authenticity Premium Sustains Leadership

Earned media retained 49.30% revenue in 2025 and is pacing at 16.31% CAGR, underscoring public appetite for third-party validation over branded assertions. Major news outlets and specialized review communities deliver credibility, and search engines increasingly privilege editorial links and independent testimonials. The FTC’s crackdown on undisclosed sponsorships has elevated the value of verifiable authenticity, steering advertising dollars toward public relations initiatives that secure unbiased coverage. Paid media and owned channels remain critical layers for narrative control yet lack the trust halo conferred by independent voices.

Tools that map journalist networks, pitch story angles, and forecast virality are becoming core modules inside reputation suites. AI summarizers generate briefing packs that help spokespeople align messaging to coverage gaps, deepening earned-media ROI. As algorithms surface highly shared articles in social feeds, earned placements now deliver compounding impressions far beyond initial publication. This reinforces its center-of-gravity role inside the online reputation management market, prompting firms to integrate social-listening data with press-database intelligence for unified stakeholder insights.

By Application: Healthcare Verticals Outpace Retail and E-commerce Expansion

Retail and e-commerce represented 24.20% of online reputation management market size in 2025, staying the largest slice because star ratings translate directly into cart-conversion rates. Many marketplaces auto-pause product listings whose average score dips below threshold, turning reputation into a revenue gate. Nevertheless, healthcare’s 18.82% CAGR through 2031 makes it the fastest-climbing vertical. Patient-experience transparency platforms like Birdeye capture appointment feedback and syndicate scores across provider directories, influencing choice architecture at critical health moments.

HIPAA constraints demand encryption, role-based access, and content-filtering that redacts personal health details before posting responses. Vendors capable of embedding these safeguards gain a pricing premium and customer loyalty. Government agencies and educational institutions also accelerate adoption, monitoring citizen or student sentiment to fine-tune service delivery. Custom lexicons and topic models capture nuances such as policy approval or campus-safety perceptions, indicating that specialized taxonomy support will be an emerging battleground inside the online reputation management market.

Geography Analysis

North America retained 38.20% revenue in 2025, a position secured by early e-commerce maturity, deep social-media penetration, and the FTC’s unambiguous fake-review enforcement that galvanizes investment in compliant tooling . United States brands were first to roll out cross-channel dashboards and now shape feature roadmaps for global vendors. Canada’s technology rebound, epitomized by Shopify’s ecosystem, funnels demand for ratings aggregation and sentiment alerts into small-merchant segments. Mexico’s rapid digital-payments adoption elongates the runway for regional expansion, though lower average selling prices necessitate lean delivery models.

Asia-Pacific is advancing at 18.13% CAGR, the fastest worldwide. China’s super-app model blurs social commerce, payments, and reviews, multiplying touchpoints that require unified oversight. India’s surge of new-to-internet consumers introduces linguistic diversity that stresses sentiment models trained on Western vocabularies. Japan and South Korea, with meticulous consumer expectations, push vendors toward sub-second alerting and nuanced politeness filters. Southeast Asian SMEs, buoyed by smartphone penetration, are leapfrogging desktop tools and adopting mobile-first SaaS, broadening the bottom-of-pyramid layer of the online reputation management market.

Europe exhibits steady momentum despite stringent data-protection mandates that lift compliance costs. GDPR shaped global best practices for privacy-by-design, compelling vendors to ship granular consent logs and data-minimization features. Germany, France, and the United Kingdom champion enterprise rollouts that integrate reputation metrics inside digital-customer-experience roadmaps. Southern Europe’s tourism-heavy economies recognize that review volatility affects seasonal bookings, nudging hospitality operators toward continuous listening platforms. Geopolitical complexities in Eastern Europe demand localized hosting and Cyrillic-trained models, challenges that full-stack providers are racing to solve.

Competitive Landscape

The online reputation management market is moderately fragmented yet trending toward consolidation as AI and compliance requirements lift technical entry barriers. Trustpilot’s corpus of 300 million consumer reviews offers a scale moat and network effects that smaller peers cannot replicate. Sprout Social’s end-to-end social suite, which grew revenue in double digits during 2024, demonstrates that integrated publishing plus reputation surveillance unlocks cross-sell synergies. Birdeye competes on vertical depth, winning healthcare contracts by embedding HIPAA workflows inside feedback loops.

Strategic alliances are emerging: cloud hyperscalers provide scalable AI backbones, while legal-tech firms layer policy engines that document compliance against FTC and GDPR requirements. Acquisition momentum is picking up—Software Combined Group’s May 2025 purchase of Removify illustrates aggregator plays that roll niche tools into broader portfolios. Product roadmaps revolve around explainable AI dashboards, ESG trackers, and region-specific data-residency guarantees. Vendors that can mesh these differentiators are poised to capture incremental online reputation management market share as procurement teams consolidate point solutions into unified platforms.

Competitive intensity is heightened by the cost of AI talent and GPU compute, which favors well-capitalized incumbents. New entrants differentiate through micro-specialization—offering, for instance, influencer-fraud detection tailored to Southeast Asian social-commerce platforms. Yet customer stickiness remains high once APIs and ticketing workflows are embedded, tempering churn risk. Over 2025-2030, experts anticipate selective mergers forming a top-tier cluster that collectively commands a majority of global revenue while niche boutiques thrive in local or vertical pockets of the online reputation management market.

Online Reputation Management Industry Leaders

WebiMax, Inc.

NetReputation, LLC

Reputation.com, Inc.

Birdeye, Inc.

Podium Corporation, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Software Combined Group announced the acquisition of Removify, marking its 10th software deal since 2020 and expanding its presence in reputation services.

- January 2025: Sprinklr launched local data-hosting in Germany and Saudi Arabia alongside AI-first feedback-management tools aimed at enterprise compliance requirements.

- September 2024: Trustpilot disclosed surpassing 300 million reviews and 64 million monthly active users, confirming that 89% of UK consumers consult ratings during purchase decisions.

- August 2024: The FTC formalized an enforcement framework targeting fake testimonials, undisclosed incentives, and bot-driven manipulation, introducing civil penalties up to USD 51,744 per violation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the online reputation management (ORM) market as all fee-based software platforms and managed services that help organizations or individuals monitor, analyze, and improve digital perceptions across review sites, search results, social networks, blogs, and news feeds.

Revenue from generic social-media dashboards, influencer marketing retainers, and paid ad spend sits outside this scope.

Segmentation Overview

- By Component

- Software

- Review-management platforms

- Social-listening tools

- SEO and content-suppression tools

- Services

- Managed reputation services

- Crisis-management consulting

- Brand monitoring and reporting

- Software

- By Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By Deployment Type

- Cloud-based

- On-premise

- By Media Channel

- Paid Media

- Earned Media

- Owned Media

- By Application / Industry Vertical

- Healthcare

- Automotive

- Hospitality

- Financial Services

- Media and Entertainment

- Retail and E-commerce

- Education

- Government and Public Sector

- Real Estate and Construction

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed software product managers, digital marketing directors, hospitality operators, and reputation consultants across North America, Europe, and Asia-Pacific. These conversations tested penetration assumptions, typical price bands, and adoption triggers, letting us refine model variables and reconcile secondary inconsistencies before final sizing.

Desk Research

We reviewed tier-1 public sources such as the U.S. Federal Trade Commission consumer complaint index, Eurostat ICT usage surveys, OECD Digital Economy indicators, and the World Bank Digital Adoption Index to benchmark review volumes, internet penetration, and brand risk exposure. Trade bodies like the Interactive Advertising Bureau and national retail associations provided data on review-driven purchase behavior, while company filings gathered through D&B Hoovers and news archives accessed via Dow Jones Factiva clarified vendor revenue splits. The sources above illustrate the wider pool of secondary material consulted; many additional references informed validation and context.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction of global ORM spend by blending business population counts with observed penetration rates and average annual contract values. Supplier roll-ups from sampled invoices and channel checks provide bottom-up markers that adjust totals. Key inputs include: (1) average number of reviews per business per month, (2) share of enterprises outsourcing crisis response, (3) cloud subscription price erosion, (4) regional digital adoption scores, and (5) regulatory milestones such as GDPR fine trends. Multivariate regression, cross-checked with three-year ARIMA projections, underpins the 2025-2030 outlook. Gaps in granular invoice data are bridged through respondent-validated ratios and historical growth corridors.

Data Validation & Update Cycle

Outputs pass a three-layer review: analyst, senior domain lead, and research quality team. Variances above preset thresholds trigger re-contact with sources. Reports refresh annually, with interim updates released when material events (for example, major platform policy shifts) occur.

Why Our Online Reputation Management Baseline Commands Reliability

Published figures often diverge because firms track different revenue streams, pick unlike baseline years, or roll forward forecasts using untested multipliers.

Key gap drivers here include: some studies cover only enterprise contracts, others bundle adjacent SEO or advertising spend, and refresh cadences vary. Mordor revisits variables each year, whereas several publishers recycle older assumptions. Currency conversion practices and scenario weighting further widen spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.88 B (2025) | Mordor Intelligence | - |

| USD 5.00 B (2025) | Regional Consultancy A | Tracks only enterprise contracts; omits self-service SaaS subscriptions |

| USD 1.34 B (2025) | Trade Journal B | Counts service agencies in 15 countries; excludes software revenue and freelancers |

| USD 9.45 B (2024) | Global Consultancy C | Bundles review platform ad sales and SEO contracts, inflating totals |

These comparisons show that Mordor's disciplined scope selection, yearly variable refresh, and dual-track modeling deliver a balanced, transparent baseline that decision-makers can trace to clear data points and repeatable steps.

Key Questions Answered in the Report

What is the current value of the online reputation management market?

The market is valued at USD 7.75 billion in 2026 and is projected to reach USD 14.01 billion by 2031.

Which component segment is growing the fastest?

Software is advancing at a 17.09% CAGR, outpacing services as companies prefer AI-enabled, scalable platforms.

Why is healthcare the fastest-growing application?

Strict privacy laws and patient reliance on reviews are driving healthcare to adopt HIPAA-compliant reputation tools, resulting in a 18.82% CAGR.

How does the FTC rule affect reputation strategies?

The October 2024 rule imposes fines on fake reviews, prompting brands to adopt platforms that verify authenticity and maintain audit trails.

Why are SMEs accelerating adoption despite budget limits?

Cloud subscriptions with simplified interfaces reduce upfront costs, allowing SMEs to access enterprise-grade monitoring and response workflows.

Page last updated on: