Fintech Blockchain Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

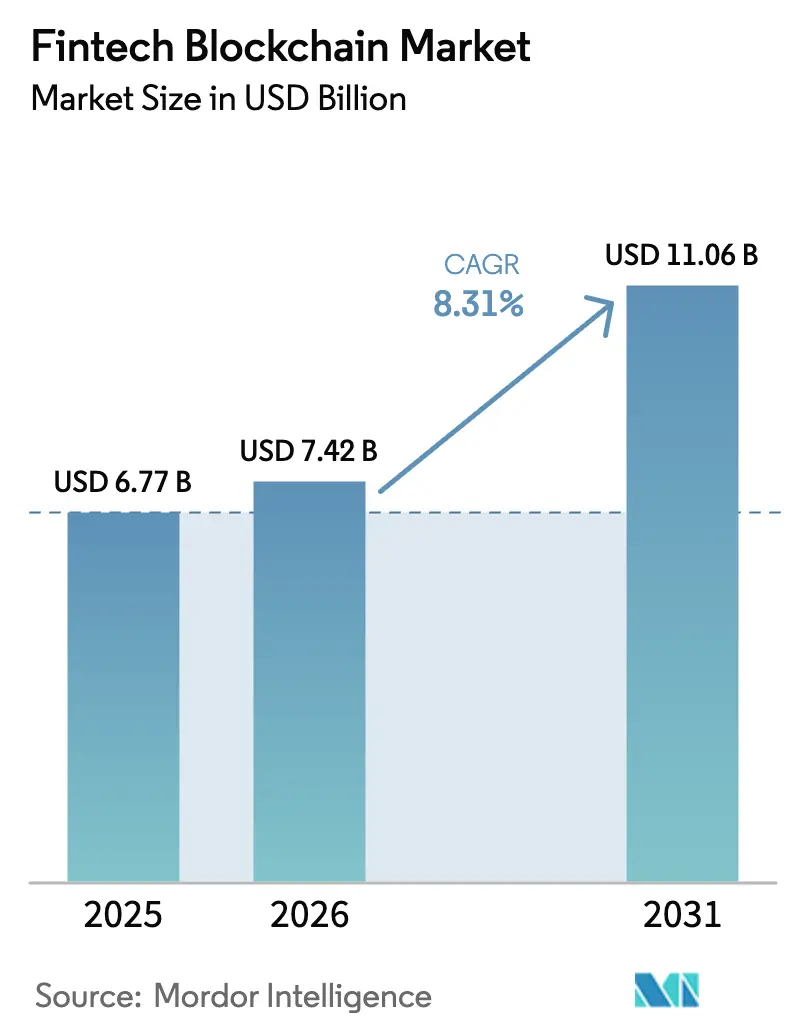

| Market Size (2026) | USD 7.42 Billion |

| Market Size (2031) | USD 11.06 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

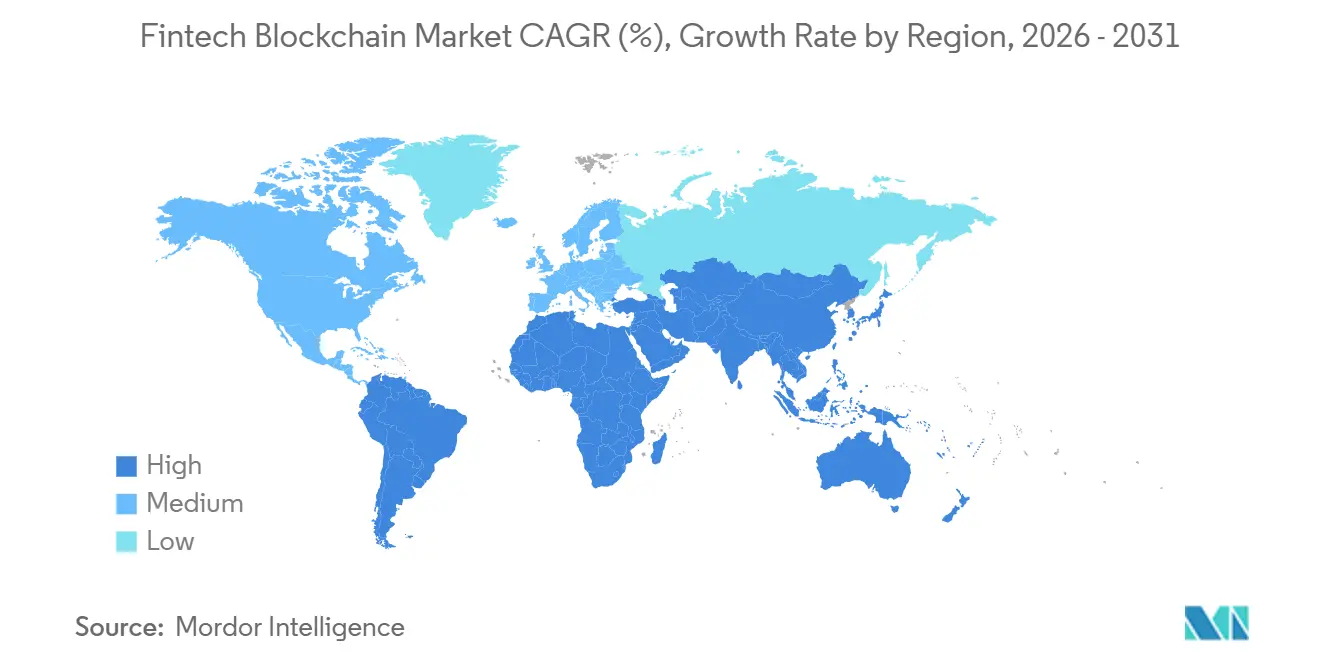

| Fastest Growing Market | Middle East |

| Largest Market | North America |

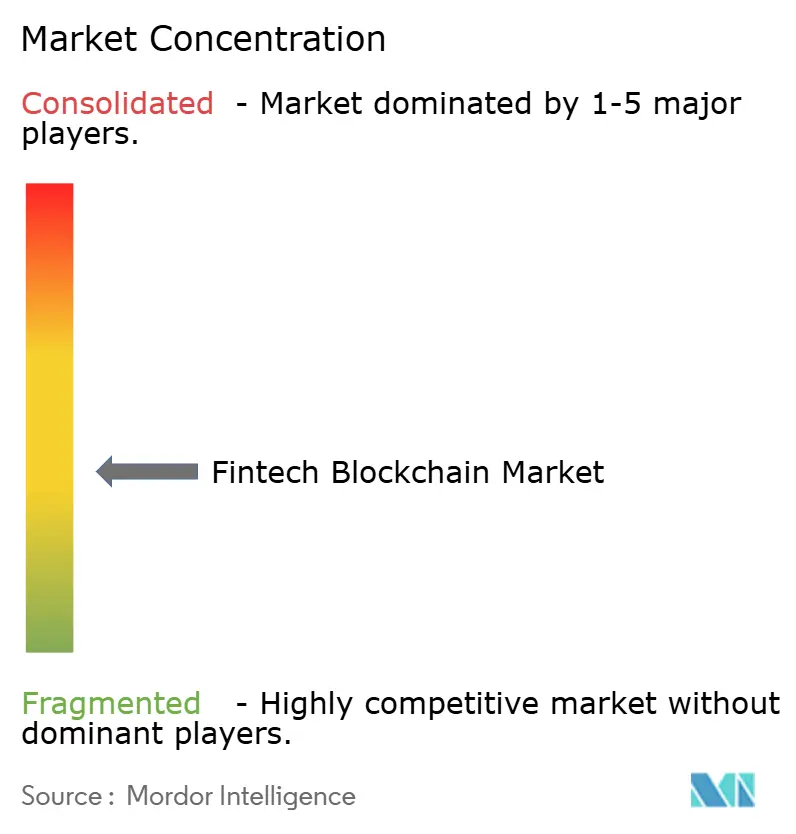

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fintech Blockchain Market Analysis by Mordor Intelligence

The fintech blockchain market size is expected to increase from USD 6.77 billion in 2025 to USD 7.42 billion in 2026 and reach USD 11.06 billion by 2031, growing at a CAGR of 8.31% over 2026-2031. Rapid movement from limited pilots to production-grade platforms for real-time settlement, tokenized collateral, and embedded compliance engines is reshaping operating models across banking, payments, and insurance. Incumbent networks such as SWIFT have shifted strategy by adding distributed-ledger modules, while Basel capital rules now steer banks toward permissioned tokenization of traditional assets rather than speculative crypto holdings. Enterprise buyers continue to favor middleware that bridges legacy cores to multiple ledgers, but the rise of low-cost Layer-2 rollups is steadily diverting spending to protocol infrastructure. Regionally, the United States dominates revenue on the back of the GENIUS Act and spot Bitcoin ETF approvals, whereas the Middle East provides the highest growth tailwind as central-bank digital-currency pilots move into live settlement rails.

Key Report Takeaways

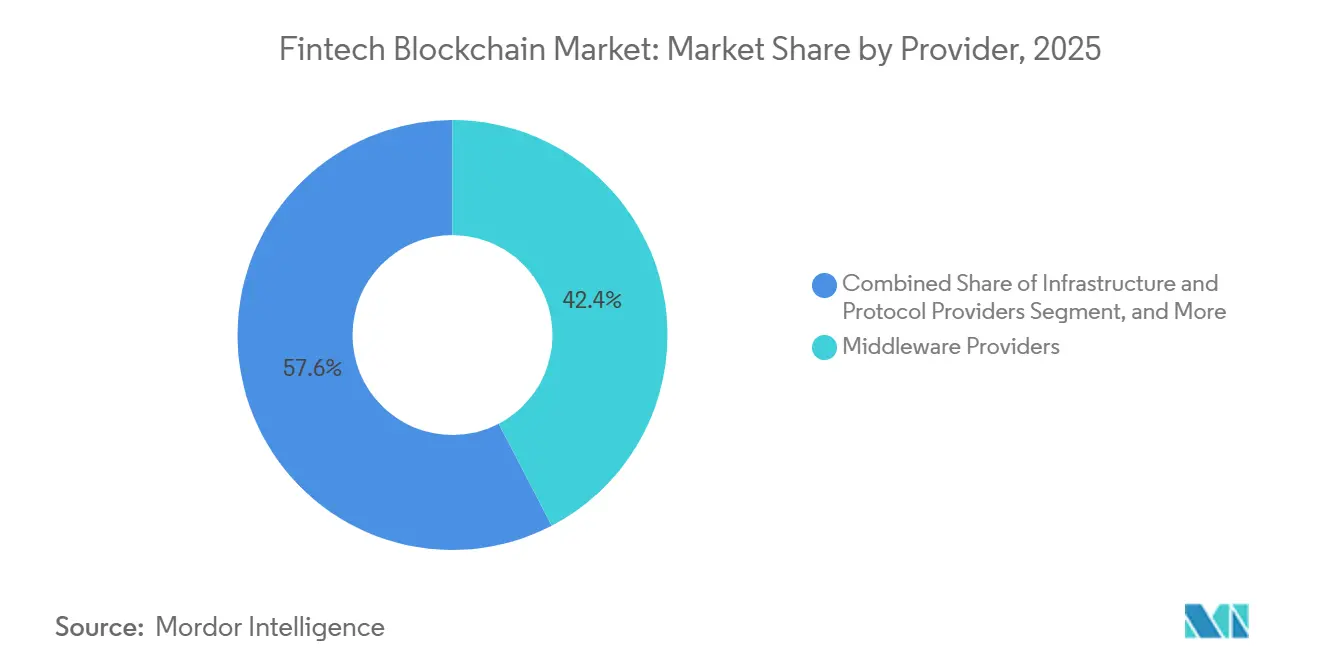

- By provider, middleware led with 42.36% revenue share in 2025, while infrastructure and protocol providers are expanding at an 8.89% CAGR through 2031.

- By application, payments, clearing, and settlement captured 39.56% in 2025, whereas identity management is advancing at a 9.51% CAGR.

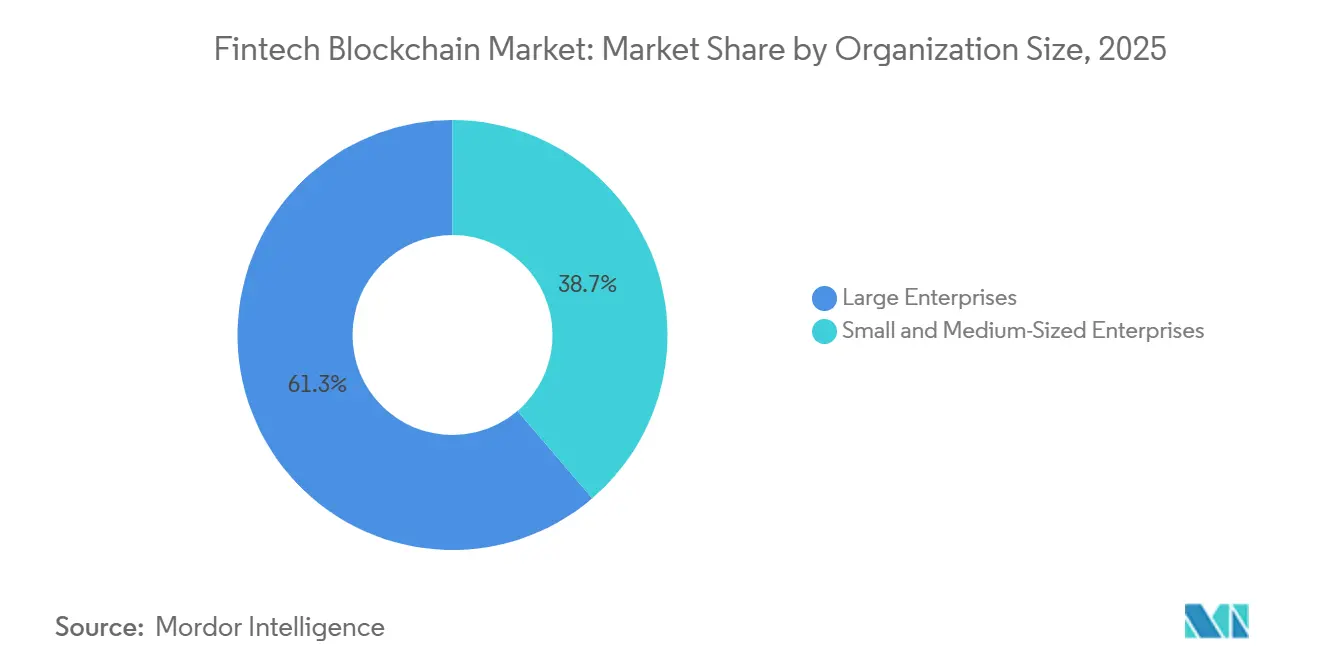

- By organization size, large enterprises accounted for 61.27% of 2025 spending, yet small and medium-sized enterprises are growing at an 8.76% CAGR.

- By end-user vertical, banking held a 55.78% revenue share in 2025, while insurance recorded the fastest growth at an 8.93% CAGR.

- By geography, North America commanded 42.39% of global revenue in 2025, but the Middle East is projected to register the strongest 9.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fintech Blockchain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Blockchain for Cross-Border Payments | +1.8% | Global with early concentration in Asia-Pacific corridors and Middle East wholesale channels | Medium term (2-4 years) |

| Growing Tokenization of Real-World Assets | +1.5% | North America and Europe lead issuance, Asia-Pacific secondary trading emerging | Long term (≥ 4 years) |

| Rising Demand for Compliance Automation (RegTech) | +1.3% | Global, particularly Europe under MiCA and United States GENIUS Act jurisdictions | Short term (≤ 2 years) |

| Expansion of Stablecoins in Corporate Treasury | +1.0% | North America corporates, Latin America remittances, Asia-Pacific e-commerce settlement | Medium term (2-4 years) |

| Surge in Embedded Finance and BaaS Integrations | +1.2% | North America and Europe fintech ecosystems, Asia-Pacific super-apps | Short term (≤ 2 years) |

| Higher Venture Funding for Decentralized Finance Platforms | +0.9% | North America and Europe venture hubs, spillover to Singapore and Hong Kong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Blockchain for Cross-Border Payments

SWIFT’s September 2025 rollout of a distributed-ledger module signaled a pivot by the 40 million messages per day network toward instant, on-chain visibility, narrowing the technology gap with Ripple and Stellar corridors.[1]SWIFT, “SWIFT Explores Blockchain Interoperability for Cross-Border Payments,” swift.com The Bank for International Settlements confirmed that Project mBridge settled USD 22 billion in wholesale trades during 2025, compressing settlement time from two days to seconds and halving fees. Consumer remittance lanes are following suit, evidenced by MoneyGram’s integration of Stellar rails that cut transaction costs below 1%. Asia-Pacific, which accounts for 42% of global remittance volume, offers the largest sandbox thanks to supportive rules under Singapore’s Payment Services Act. As regulatory certainty grows, cross-border corridors are expected to tip decisively toward blockchain rails well before 2031.

Growing Tokenization of Real-World Assets

The World Economic Forum projects that tokenized real-world assets could represent USD 16 trillion by 2030, yet liquidity remains fragmented across permissioned venues.[2]World Economic Forum, “Tokenization of Real-World Assets Could Represent USD 16 Trillion Market by 2030,” weforum.org The European Investment Bank scaled digital-bond issuance from EUR 100 million in 2021 to EUR 600 million (USD 648 million) by 2025, proving operational savings over book-entry systems. Siemens’s EUR 60 million (USD 65 million) digital bond on Polygon reduced issuance costs by 40% and bypassed intermediaries. Tokenized commodities such as Paxos Gold now exceed USD 1 billion outstanding, furnishing on-chain collateral for decentralized lending pools. Basel Group 1 treatment for tokenized traditional assets eliminates punitive capital weights, opening bank balance sheets to tokenized collateral.

Rising Demand for Compliance Automation (RegTech)

Chainlink’s Adaptive Compliance Engine enables smart contracts to query sanctions lists in real-time, automating checks that were previously handled through multi-day manual reviews.[3]Chainlink, “Adaptive Compliance Engine,” chain.link Europe’s MiCA framework, effective January 2025, mandates transaction monitoring for crypto-asset service providers, creating a surge in demand for blockchain-native analytics middleware. The United States GENIUS Act offers safe-harbor status for compliant tokenized securities, pushing issuers to embed disclosure logic directly into smart contracts. Banks are adopting decentralized identifiers based on W3C Verifiable Credentials to slash onboarding time and reduce breach risk. FATF guidance clarifies that DeFi protocols with identifiable operators still fall under AML rules, driving adoption of permissioned identity layers.

Expansion of Stablecoins in Corporate Treasury

Stripe’s USD 1.1 billion acquisition of Bridge underscored the strategic value of stablecoin infrastructure for merchant settlement. Visa’s Tokenized Asset Platform allows banks to issue fiat-backed tokens on Ethereum Layer-2 networks, reducing interchange by 30 basis points and settling card flows instantly. Shopify merchants using Solana Pay process more than 2 million transactions monthly with fees under USD 0.01. Corporate treasurers in Latin America now hold stablecoins to hedge currency volatility, while Asia-Pacific e-commerce firms settle cross-border orders in tokenized USD to dodge costly correspondent chains. As audit and attestation frameworks mature, stablecoin floats are expected to migrate from retail wallets to enterprise treasuries at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Gaps Among Permissioned Ledgers | -1.2% | Global, with acute friction in Europe where multiple consortia run in silos | Medium term (2-4 years) |

| Scarcity of Tokenized-Asset Secondary Liquidity | -0.9% | North America and Europe primary issuance, Asia-Pacific trading underdeveloped | Long term (≥ 4 years) |

| Cross-Chain Bridge Cyber-Risk Exposure | -0.7% | Global, with heightened scrutiny in North America and Europe | Short term (≤ 2 years) |

| Capital-Charge Impact of Basel Crypto Rules on Banks | -1.1% | Global banking systems, European and North American banks most constrained | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps Among Permissioned Ledgers

Enterprises often participate in multiple consortia, Hyperledger Fabric, R3 Corda, and Canton, yet divergent consensus and data models force parallel infrastructure, inflating costs and back-office reconciliation. Chainlink’s CCIP promises cross-chain messaging but remains confined to public networks because most permissioned ledgers restrict external oracle access. The European Blockchain Services Infrastructure illustrates the challenge: 27 member states adopted varied identity schemas, blocking seamless data exchange. Banks, therefore, face a choice between surrendering flexibility to a dominant consortium or running isolated networks that sacrifice network effects. Until a universal interoperability layer meets privacy, audit, and throughput needs, multi-ledger fragmentation will temper large-scale rollouts.

Capital-Charge Impact of Basel Crypto Rules on Banks

Basel’s December 2024 framework assigns a 1,250% risk weight to unbacked crypto, functionally excluding it from bank balance sheets. European banks already operating near Capital Requirements Regulation buffers now incur an 8-12% capital add-on even for Group 1 tokenized assets, stalling growth of digital-bond trading desks. United States banks must secure supervisory approval under SR 22-6 before engaging in crypto activities, raising compliance overhead that regional lenders struggle to absorb. In Japan, Financial Services Agency rules require crypto operations to be ring-fenced in separately capitalized subsidiaries, fragmenting economies of scale. The result is a two-tier market dominated by well-capitalized global banks, with smaller institutions relegated to custodial or agency roles, concentrating systemic exposure in a handful of providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Provider: Middleware Orchestrates Multi-Ledger Workflows

Middleware providers held 42.36% of the fintech blockchain market share in 2025, underscoring enterprise demand for abstraction layers that bridge legacy core systems to multiple distributed ledgers without rip-and-replace disruption. Platforms such as IBM Blockchain process over 20,000 transactions per second for trade-finance consortia, enabling confidential data segregation and granular permissioning. Application and solution vendors controlled roughly 35% of spending as banks opted for turnkey payment, custody, and compliance modules that accelerate time-to-market. The fintech blockchain market size allocation for infrastructure and protocol providers is rising at an 8.89% CAGR because firms now spin up self-hosted nodes on Ethereum Layer-2 rollups, Polygon proof-of-stake chains, and Avalanche subnets that achieve sub-second finality and negligible fees. Canton Network’s privacy-preserving synchronization is attracting capital markets operators seeking a single source of truth without over-sharing order books. Oracle’s integration of Blockchain Platform into its Fusion Cloud suite illustrates how software giants bundle ledger services with ERP and supply-chain modules to lock in enterprise workflows.

Demand patterns are set to evolve as large banks insource protocol expertise for cost and latency control, while mid-tier institutions favor managed middleware that outsources node maintenance and governance upgrades. Open-source ecosystems are also shifting the competitive balance because Hyperledger Fabric, Corda, and Ethereum each offer pluggable consensus, enabling third-party service firms to monetize support rather than proprietary code. As firms deploy multi-ledger architectures, neutral orchestrators that normalize APIs and event streams across networks stand to capture outsized wallet share. Consequently, middleware is expected to retain leadership in absolute revenue, even though protocol spending posts the faster growth rate through 2031.

By Application: Identity Management Gains Traction Beyond Payments

Payments, clearing, and settlement remained the anchor, commanding 39.56% of 2025 spending as incumbents integrated blockchain tracking and on-demand liquidity services. Identity management, however, posted the highest 9.51% CAGR as banks adopted W3C Verifiable Credentials to centralize know-your-customer outcomes while decentralizing raw data storage. The fintech blockchain market size attached to exchanges and remittance platforms represented about 22%, driven by Coinbase institutional brokerage and Stellar MoneyGram corridors. Smart contracts supporting letter-of-credit workflows and parametric insurance captured roughly 18%, with Chainlink oracles feeding data into more than 10,000 live contracts. Compliance management rounded out 12% as MiCA rules forced real-time blockchain analytics in Europe.

Looking ahead, identity layers are poised to leapfrog payments once decentralized identifiers integrate seamlessly into mobile wallets and government e-ID programs. Bank onboarding that once took days now completes in minutes, freeing staff capacity and improving conversion. As cross-border trade digitizes bills of lading and certificates of origin, identity and compliance modules will intertwine, enabling straight-through processing from contract initiation to customs clearance. Tokenized loyalty and decentralized credit scoring pilots in Asia-Pacific super-apps further broaden application scope, ensuring the fintech blockchain market continues to diversify beyond its payment roots.

By Organization Size: SMEs Leverage BaaS for Instant Settlement

Large enterprises generated 61.27% of 2025 revenue, reflecting the regulatory complexity and capital intensity of running permissioned networks. JPMorgan Onyx and HSBC FX Everywhere illustrate how megabanks internalize ledger infrastructure to shave intraday funding costs. Yet, small and medium-sized enterprises are expanding at an 8.76% CAGR, propelled by Banking-as-a-Service platforms that abstract away node management. Synctera and Treasury Prime integrated stablecoin rails in 2025, allowing more than 500 fintech clients to settle invoices and foreign exchange within seconds at sub-1% spreads. In Latin America, stablecoin settlement helps SMEs hedge macro volatility, as seen when Nubank piloted USDC flows for cross-border payments.

As regulatory sandboxes in Singapore, the United Arab Emirates, and the United Kingdom lower entry barriers, SMEs can test custody and lending modules without full licenses, accelerating adoption. The fintech blockchain market share of SMEs is therefore expected to rise steadily, even as large enterprises maintain topline dominance. Key to scaling is the commoditization of compliance through API-based identity services, which allows smaller firms to satisfy travel-rule obligations and jurisdictional reporting without building bespoke controls.

By End-User Verticals: Insurance Automates Claims via Oracle

Banking captured 55.78% revenue in 2025, anchored by cross-border payments, tokenized-bond issuance, and repo funding on blockchain rails. Non-banking financial services, including asset managers and broker-dealers, accounted for about 28%, led by BlackRock’s tokenized money-market fund, which processed USD 500 million in subscriptions. Insurance logged the fastest 8.93% CAGR, fueled by parametric products that use oracles to settle claims automatically. Lemonade reduced travel-insurance claims processing from weeks to hours through on-chain triggers, cutting administrative costs by 40%. Reinsurers such as Swiss Re and Munich Re are testing smart contracts that programmatically allocate losses across treaty layers, a process previously hampered by manual reconciliation.

Demand momentum in insurance is poised to continue as climate-linked disasters surge, prompting underwriters to seek automated payout mechanisms tied to weather data. Decentralized insurance protocols like Nexus Mutual processed USD 100 million in cover during 2025, demonstrating willingness among crypto-native users to hedge on-chain risk. Overall, diversification beyond banking reduces revenue cyclicality and broadens the fintech blockchain industry’s value proposition across financial services silos.

Geography Analysis

North America’s fintech blockchain market size remains the benchmark as regulators clarify tokenized-asset treatment and institutional investors scale ETF flows. United States banks use GENIUS Act protections to tokenize corporate bonds, while Canada expands custody licenses to non-bank entities, and Mexico’s fintech-law amendments permit sandbox pilots that already process 8% of the high-value corridor to the United States. With major cloud providers headquartered in the region, enterprises enjoy abundant infrastructure choice, reinforcing the current revenue lead.

Europe benefits from early digital-bond frameworks and MiCA’s uniform passporting, which reduces legal fragmentation and encourages continental deployment. Germany’s electronic securities law has already enabled direct issuance of EUR-denominated bonds on-chain. France captured Circle’s European headquarters relocation, highlighting policy competitiveness. Meanwhile, the United Kingdom, now outside the European Union, uses a digital-securities sandbox to maintain relevance, plus Switzerland’s independent DLT law continues to attract custody startups.

Asia-Pacific exhibits heterogeneous progress. China’s retail digital currency dwarfs other CBDC pilots by volume, yet strict capital controls limit cross-border use. Japan’s Digital Yen, India’s blockchain-enhanced UPI, and South Korea’s tokenized-bond sandbox position the region for rapid deployment once interoperability questions are resolved. Australia’s delay of the CHESS replacement underscores implementation complexity but also confirms long-term commitment to large-scale adoption. Across the region, super-apps integrating blockchain loyalty points and micro-insurance are likely to widen retail participation.

Competitive Landscape

Competition remains moderate, with the top five vendors, IBM, Microsoft, Ripple, Coinbase, and Circle, collectively holding about 38% share. Tech incumbents capitalize on entrenched enterprise relationships: Microsoft embeds ledger access in Azure Active Directory, while Amazon Web Services provides one-click managed nodes, shortening proof-of-concept cycles for corporate buyers. IBM targets regulated consortia, pairing Hyperledger Fabric with consulting to lock in multi-year support contracts.

Crypto-native firms differentiate via regulatory alignment and custodial depth. Coinbase Prime processed USD 500 billion in 2025 volume, offering segregated cold storage and insurance that satisfy institutional due diligence standards. Circle’s USDC expansion to 15 networks widens its moat in stablecoin liquidity and cross-chain reach. Ripple’s focus on on-demand liquidity corridors, coupled with partnerships like Mastercard’s Southeast Asia pilot, reinforces payment use-case dominance.

White-space opportunities revolve around secondary trading for tokenized assets and cross-chain interoperability middleware. Zero-knowledge proof vendors such as Polygon zkEVM are positioned to deliver privacy-preserving settlement that meets audit requirements, while Aave Arc illustrates the future of permissioned DeFi liquidity pools for regulated institutions. Strategic alliances dominate competitive moves: Visa’s Tokenized Asset Platform with HSBC and Citi exemplifies payment networks servicing banks as neutral infrastructure rather than as direct rivals. Consulting majors like Accenture and Tata Consultancy Services capture systems-integration revenue, confirming that services remain pivotal for mainstream adoption.

Fintech Blockchain Industry Leaders

Accenture PLC

AlphaPoint Corporation

Amazon Web Services Inc.

Bitfury Group Limited

BTL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Circle expanded USDC to six additional networks, bringing total integrations to 15.

- November 2025: JPMorgan Chase’s Onyx platform surpassed USD 1 trillion in intraday repo and FX volume for the year.

- October 2025: European Investment Bank issued EUR 150 million (USD 162 million) in digital bonds on Ethereum mainnet with 60-second settlement.

- September 2025: SWIFT launched a blockchain ledger for real-time cross-border payment tracking with 30 correspondent banks.

Global Fintech Blockchain Market Report Scope

The Fintech Blockchain Market Report is Segmented by Provider (Middleware Providers, Application and Solution Providers, Infrastructure and Protocol Providers), Application (Payments, Clearing, and Settlement, Exchanges and Remittance, Smart Contract, Identity Management, Compliance Management/KYC, Other Applications), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Verticals (Banking, Non-Banking Financial Services, Insurance), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Middleware Providers |

| Application and Solution Providers |

| Infrastructure and Protocol Providers |

| Payments, Clearing, and Settlement |

| Exchanges and Remittance |

| Smart Contract |

| Identity Management |

| Compliance Management / KYC |

| Other Applications |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Banking |

| Non-Banking Financial Services |

| Insurance |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Provider | Middleware Providers | ||

| Application and Solution Providers | |||

| Infrastructure and Protocol Providers | |||

| By Application | Payments, Clearing, and Settlement | ||

| Exchanges and Remittance | |||

| Smart Contract | |||

| Identity Management | |||

| Compliance Management / KYC | |||

| Other Applications | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises | |||

| By End-User Verticals | Banking | ||

| Non-Banking Financial Services | |||

| Insurance | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How fast is the fintech blockchain market expected to grow through 2031?

The market is projected to expand at an 8.31% CAGR, rising from USD 7.42 billion in 2026 to USD 11.06 billion by 2031.

Which provider category currently leads spending?

Middleware providers hold the largest share at 42.36% because they connect legacy cores to multiple blockchains without major infrastructure replacement.

What application area is growing the quickest?

Identity management is advancing at a 9.51% CAGR as banks deploy decentralized identifiers to streamline know-your-customer workflows.

Which region shows the highest growth momentum?

The Middle East registers the fastest regional CAGR at 9.39% due to CBDC pilots and progressive virtual-asset licensing in the United Arab Emirates and Saudi Arabia.

Why are capital rules important for blockchain adoption in banking?

Basel’s bifurcated framework levies a 1,250% risk weight on unbacked crypto, steering banks toward permissioned tokenization and limiting speculative holdings on balance sheet.

How concentrated is the competitive landscape?

The top five vendors account for about 38% of revenue, reflecting moderate concentration with ample space for specialized entrants in custody, compliance, and interoperability.

Page last updated on: