Base Station Antenna Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.81 Billion |

| Market Size (2031) | USD 9.47 Billion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Base Station Antenna Market Analysis by Mordor Intelligence

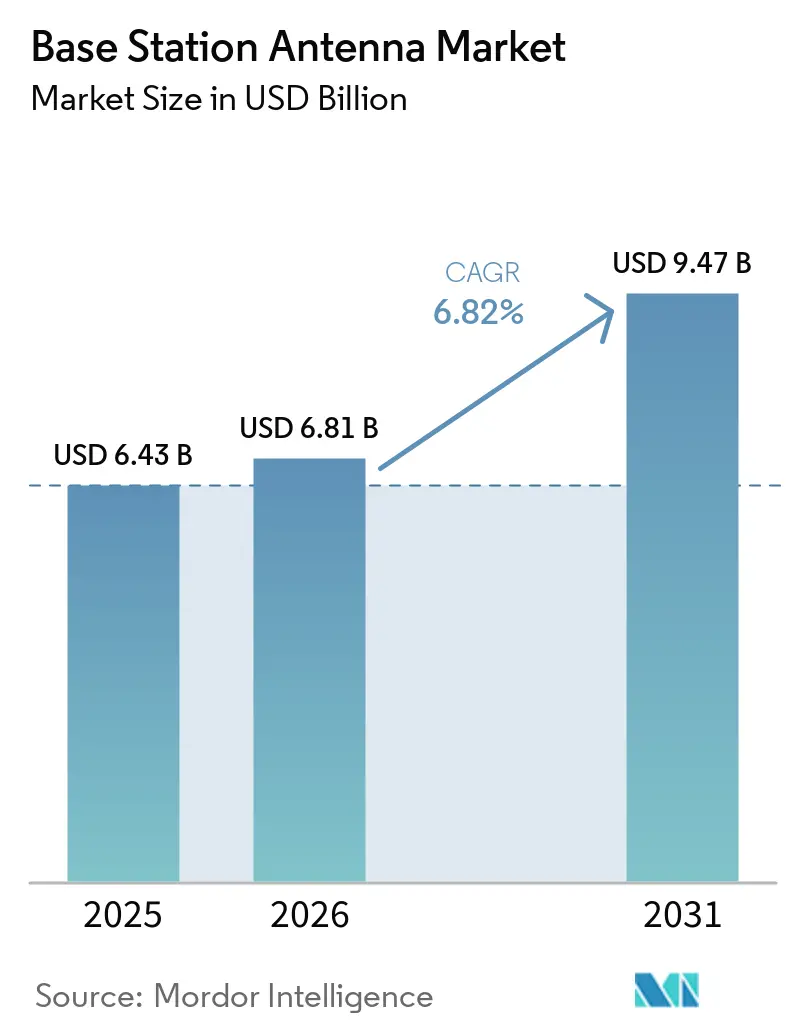

The base station antenna market size is expected to grow from USD 6.43 billion in 2025 to USD 6.81 billion in 2026 and is forecast to reach USD 9.47 billion by 2031 at 6.82% CAGR over 2026-2031. Operators are shifting toward high-port multiband arrays, massive MIMO radio units, and passive systems supporting tri-band configurations from the same tower footprint. The base station antenna market benefits from 5G and 5G-Advanced rollouts, driving broader bandwidth support and efficient spectrum use. Asia-Pacific leads in volume growth, while North America and Europe focus on value growth through wide-band massive MIMO and multibeam configurations. The market also prioritizes lowering tower load, improving gain efficiency, and managing passive intermodulation as networks densify. Competition remains fragmented, with manufacturers competing on product efficiency, integration, and reducing site complexity.

Key Report Takeaways

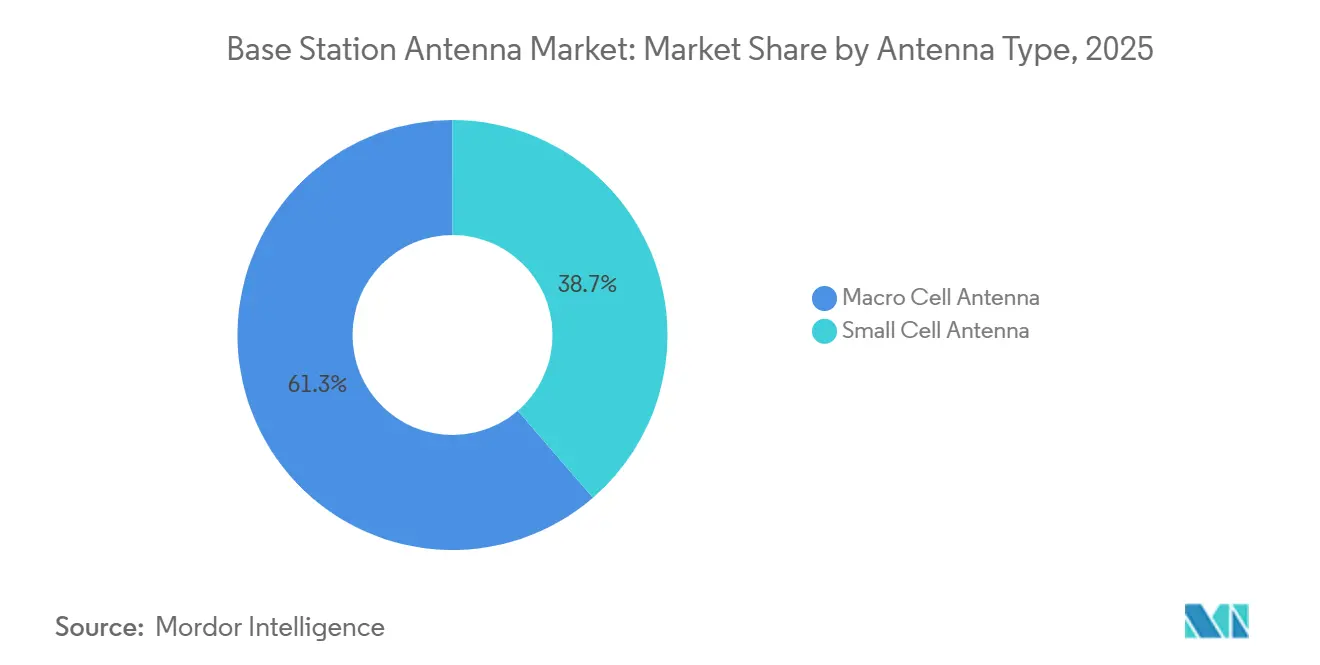

- By antenna type, macro cell antennas held 61.33% share in 2025, while small cell antennas are projected to expand at a 7.21% CAGR through 2031.

- By technology, 4G/LTE accounted for 45.89% of the base station antenna market size in 2025, while 5G is forecast to grow at a 7.42% CAGR through 2031.

- By frequency band, Sub-6 GHz accounted for 43.28% in 2025, while mmWave is set to grow at a 7.36% CAGR through 2031.

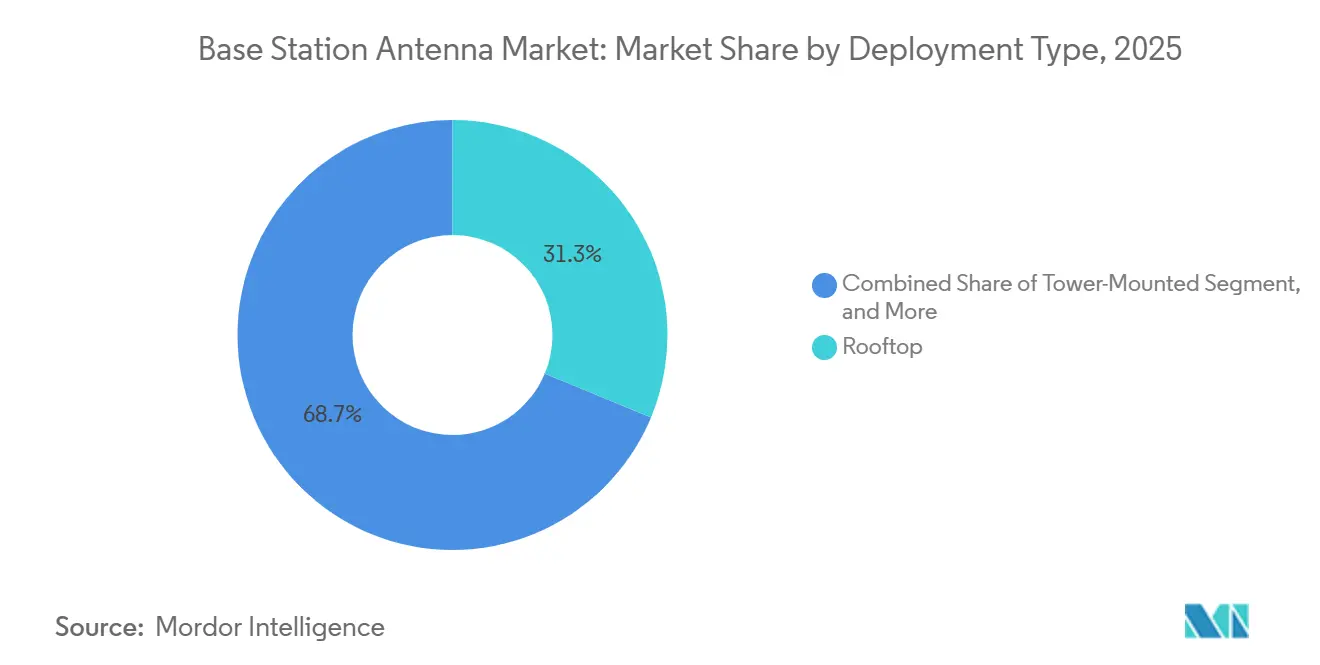

- By deployment type, rooftop installations retained 31.27% share in 2025, while tower-mounted deployments are expected to grow at a 7.68% CAGR through 2031.

- By polarization, dual-polarized antennas led with 57.81% share in 2025, while circular-polarized antennas are forecast to rise at a 7.33% CAGR through 2031.

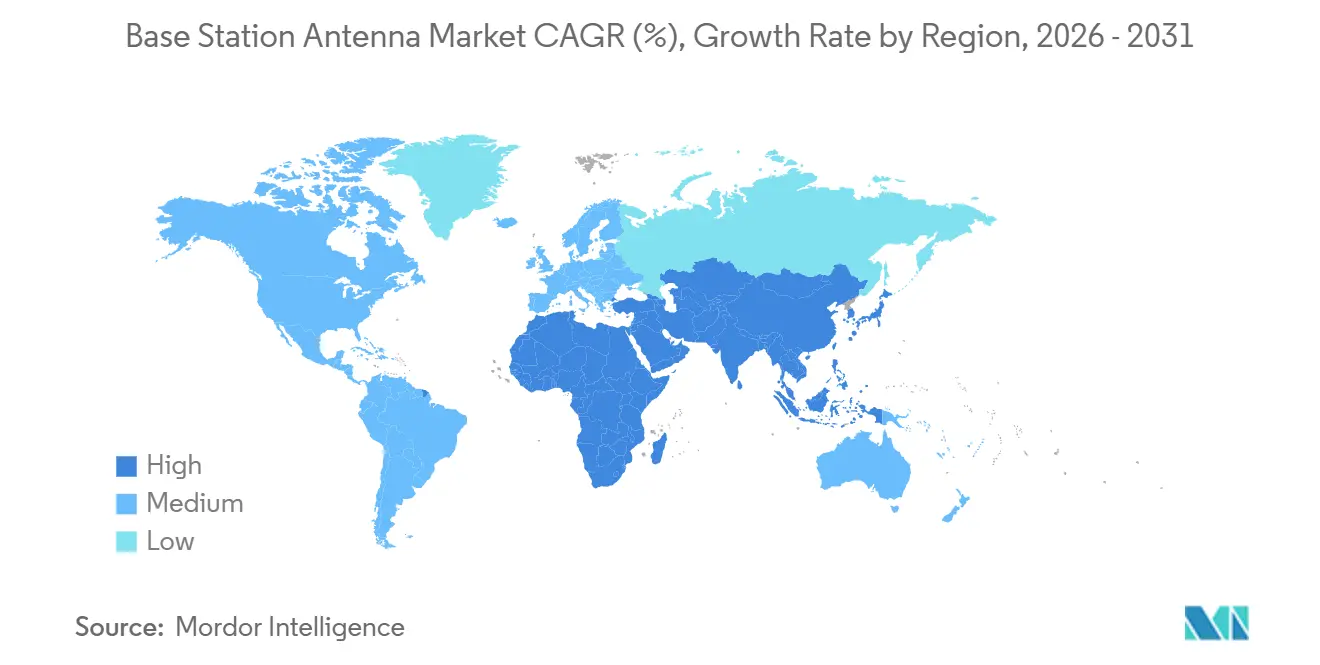

- By geography, Asia-Pacific captured 37.32% of the base station antenna market share in 2025 and is also the fastest-growing regional segment with a 7.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Base Station Antenna Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating 5G and 5G-Advanced Rollouts | +1.8% | Global, led by China, India, South Korea, the United States, and GCC markets | Short term (≤ 2 years) |

| Rising Mobile Data Traffic and Urban Densification | +1.2% | Global, strongest in North America, Western Europe, and North East Asia | Medium term (2-4 years) |

| Shift Toward Massive MIMO and Higher-Port Multiband Antennas | +0.9% | Asia-Pacific core, with spillover into Europe and North America | Medium term (2-4 years) |

| Expansion of Private 5G and Fixed Wireless Access | +0.7% | North America and the European Union primary, with rising activity in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Mid-Band Refarming and Tri-Band Retrofit Cycles | +0.4% | Asia-Pacific, Africa, and South America where 2G and 3G shutdown programs are active | Short term (≤ 2 years) |

| Open RAN and Neutral-Host Interoperability Demand | +0.3% | North America and the European Union leading, with early-stage adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating 5G and 5G-Advanced Macro Network Rollouts

The base station antenna market is drawing steady support from the widening base of commercial 5G networks and the early move toward 5G-Advanced. By April 2026, 392 operators had launched 5G networks globally, and 35 operators were investing in 5G-Advanced, which keeps antenna demand tied to both new coverage and upgrade programs.[1]GSA, “State of the Market April 2026,” GSA, gsacom.com This matters because the move from non-standalone to standalone, and then to 5G-Advanced, creates another round of antenna replacements rather than a one-time radio swap. Ericsson and T-Mobile reported live-network gains from AI-native RAN scheduling in 2026, including a 10% increase in spectral efficiency and up to a 15% improvement in downlink throughput, reinforcing the value of more advanced antenna and radio combinations at the site level. These rollout paths favor wider-bandwidth and higher-gain arrays, because enhanced uplink, carrier aggregation, and multi-band operation are difficult to support with legacy 4G-era mounts. The result is that the base station antenna market continues to expand, even in countries where macro coverage is already broad, as network evolution drives new hardware cycles.

Rising Mobile Data Traffic and Urban Network Densification

The base station antenna market is also being lifted by sustained growth in mobile data traffic and the heavier traffic concentration now seen in dense urban zones. Ericsson forecast that global mobile network data traffic will reach 310 exabytes per month by 2031, while 5G traffic share will rise from 34% at the end of 2024 to 83% by 2031. The United States alone recorded 132 trillion megabytes of mobile data usage in 2024, up 35% from the prior year, which shows that capacity pressure is still increasing even in mature markets. This creates a split investment pattern, such as dense urban sites require more advanced beamforming and sector antennas for capacity, while suburban and peri-urban sites still need higher-gain arrays for broader coverage. Small Cell Forum has identified 2026 as a critical year for scalable small-cell deployment, which means antenna suppliers are now tied not only to macro upgrades but also to the operational frameworks needed for denser site rollouts. The base station antenna market, therefore, benefits from a structural traffic pattern rather than a short-term capex spike, which supports a longer upgrade runway.

Shift Toward Massive MIMO and Higher-Port Multiband Antennas

The base station antenna market is moving toward more integrated products as operators replace stacked single-band hardware with high-port, multiband, and massive MIMO platforms. Ericsson commercially deployed the AIR 3284 triple-band FDD Massive MIMO radio on Telstra’s network in 2025, combining 1800 MHz, 2100 MHz, and 2600 MHz in a single unit and delivering up to 2 times downlink capacity and 3 times uplink capacity in field deployments. Huawei also launched its FDD tri-band Massive MIMO solution globally in 2025, and its first commercial deployment with MTN Nigeria delivered a 90% increase in LTE traffic handling and a 252% increase in user-perceived rates. NEC added to this direction in 2026 with a new Sub-6 GHz massive MIMO radio unit that improved uplink throughput by 48% and downlink throughput by 54% over current models. This consolidation trend lowers the number of separate antenna units at a site, but it raises the strategic value of each installed system because performance, footprint, and power efficiency now matter more than simple unit count. That shift is pushing the base station antenna market toward higher-value configurations, especially in urban macro layers where site space and structural tolerance are tight.

Expansion of Private 5GaAnd Fixed Wireless Access Networks

Private 5G and fixed wireless access are expanding the demand base for base station antennas beyond the traditional public macro network. Manufacturing had 374 active mobile private network deployments globally by April 2026, which shows that enterprises are becoming a recurring source of dedicated antenna demand. Ericsson forecast that FWA connections will grow from 185 million at the end of 2025 to 350 million by the end of 2031, with 90% of those links running on 5G. NTT DATA stated in 2026 that Cargill had deployed private 5G across 50 global sites and planned to add more than 100 sites annually, highlighting the recurring infrastructure demand driven by enterprise networks. On the FWA side, Ericsson, NBN Co, and Qualcomm demonstrated 5G mmWave download speeds above 1 Gbps at 14 kilometers in live field trials, which expands the practical range for mmWave antenna deployments in rural broadband use cases. Together, these use cases give the base station antenna market a broader mix of buyers and deployment models than it had in prior mobile upgrade cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Site CapEx and Lengthy Permitting Cycles | -1.4% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Spectrum Allocation Delays and Regulatory Fragmentation | -0.9% | The United States, Europe, India, and Africa | Medium term (2-4 years) |

| Tower Loading and Wind-Load Limits on Large Array Upgrades | -0.6% | Global, with strongest effect in mature macro markets such as North America, Europe, and Japan | Medium term (2-4 years) |

| Tariffs, Localization Rules, and RF Component Sourcing Volatility | -0.5% | North America first, with spillover into Asia-Pacific supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Site CapEx and Lengthy Permitting Cycles

The base station antenna market still faces a practical brake from site economics and the slow pace of local approvals. Alpha Wireless noted in 2025 that a traditional macro tower permit in the United States averaged 12 months, while full 5G densification approvals could stretch across several years when multiple municipalities were involved.[2]Alpha Wireless, “Navigating the 7 Major Hurdles of 5G Planning Approvals,” Alpha Wireless, alphawireless.com The FCC also identified local fees that it viewed as potentially non-compliant, including single-application charges of USD 25,776 in Thurston County, Washington, and USD 17,500 in Grant County, New Mexico. Those charges matter because they can push the cost of a new antenna placement well above the hardware cost itself. The FCC’s Build America rulemaking, issued in September 2025, seeks to lower these barriers, but the process will take time and not immediately change deployment economics. Until approval cycles shorten and fee structures become more predictable, operators will remain selective about densification, which keeps near-term antenna volumes below what traffic growth alone would justify.

Spectrum Allocation Delays and Regulatory Fragmentation

The base station antenna market is also constrained when operators do not know which bands will be assigned, when new licenses will be released, or how pricing will affect rollout budgets. GSMA reported in 2025 that a 10-percentage-point increase in the spectrum cost-to-revenue ratio reduces 5G coverage by 6 percentage points, thereby directly weakening the capex pool supporting antenna procurement. Spectrum policy is also unsettled across upper mid-band and 6 GHz discussions, which affects how vendors shape future antenna portfolios for both capacity and coverage layers. This uncertainty is especially important in markets that are still balancing mobile licensing against unlicensed use, because band plans drive antenna design choices long before deployment begins. In lower-income regions, delayed or fragmented auction schedules can also force operators to stretch older spectrum assets rather than move quickly to higher-value antenna upgrades. That makes the restraint more than a regulatory issue, because it slows product mix improvement across the base station antenna market, even when mobile traffic keeps rising.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Antenna Type: Macro Cell Architecture Anchors Revenue, Small Cells Accelerate

Macro cell antennas held a 61.33% share in 2025, making them the commercial foundation of the base station antenna market. Their position reflects the continuing need for wide-area coverage in 5G mid-band programs and the replacement of older dual-band arrays with higher-port multiband products. In dense urban sites, active antenna systems and massive MIMO units have increasingly displaced conventional passive sector hardware as operators prioritize capacity and spectral efficiency. Ericsson’s 2025 radio and antenna launch cycle showed that programmable, open-ready macro portfolios are becoming central to new site builds and refresh activity.

At the same time, traditional sector and multibeam products still hold their place in suburban and rural networks where traffic loads do not justify the added cost and complexity of high-end beam steering. Comba Telecom used MWC 2026 to position energy-efficient macro antennas more directly in line with operator procurement needs, highlighting its Helifeed 3.0 architecture and an energy-efficiency improvement of more than 20% across the full band. Small cell antennas are the fastest-growing segment, with a 7.21% CAGR through 2031, reflecting the rising role of indoor systems, street-level densification, and targeted capacity builds. The Small Cell Forum has described 2026 as a decisive deployment year, and Alpha Wireless has already responded with street-furniture-ready designs, such as the AW4032 Fusion platform, which supports dual-band coverage and 360° omnidirectional performance in visually sensitive locations.

By Technology: 4G/LTE Retains Commercial Weight, 5G Drives The Upgrade Agenda

The 5G segment is the fastest-growing technology layer in the base station antenna market, with a 7.42% CAGR through 2031. That growth continues to reflect ongoing global launch activity, the shift toward standalone cores, and the early spread of 5G-Advanced. By April 2026, 392 operators had launched 5G networks worldwide, and 35 were investing in 5G-Advanced, which keeps the upgrade path active across both mature and emerging markets. Within 5G, Sub-6 GHz continues to generate the most antenna volume because it aligns with the coverage geometry of mainstream rollouts, while higher-band systems are used more selectively in dense zones and for fixed wireless access. KDDI and Kyocera demonstrated in 2025 that compact repeater mesh designs could materially improve mmWave street coverage in Tokyo, supporting the long-term case for targeted high-band deployment rather than blanket rollout.

4G/LTE retained 45.89% of the base station antenna market size in 2025, which shows that LTE still carries real commercial weight even as 5G absorbs most of the future growth focus. This is especially true in Africa, South Asia, and South America, where operators continue LTE densification while also refarming sub-3 GHz assets for 5G migration. Huawei’s FDD tri-band Massive MIMO platform is a clear example of this bridge strategy, because it improves current LTE capacity while preserving a practical path toward later 5G evolution on the same site footprint. The result is that the traditional technology replacement cycle is becoming shorter and less distinct, because one antenna platform now has to support both current 4G traffic and future 5G expansion.

By Frequency Band: Sub-6 GHz Volume Anchors Mid-Band, mmWave Earns Its Deployment Case

Sub-6 GHz held 43.28% share in 2025 and remained the volume anchor of the base station antenna market. This position reflects the global importance of C-band and other mid-band layers that balance capacity and coverage more effectively than either low-band or mmWave in most national rollouts. GSA reported in 2025 that C-band was the most widely deployed 5G spectrum globally, and it also tracked heavy investment in legacy and evolving mid-band assets such as 1800 MHz. GSMA’s spectrum policy work also showed that regulatory attention is spreading upward into the 4.4-5.0 GHz and upper 6 GHz ranges, suggesting that upper mid-band antennas will become a more important product tier before the forecast period closes.

Low-band demand remains steady where operators still need wide-area coverage across rural, mountainous, or low-density regions. The high-band segment above 24 GHz is forecast to grow at a 7.36% CAGR through 2031, and that growth is increasingly tied to clear commercial use cases rather than speculative spectrum value. Nokia and EOLO deployed Europe’s first 5G standalone mmWave network in Italy in late 2024, showing that mmWave can support both urban capacity and rural fixed wireless access within the same commercial program. A 2025 IEEE study in Milan also found that mmWave performance in urban settings can exceed conventional propagation expectations through reflection paths and viable outdoor-to-indoor links, supporting better long-term economics for the segment. As those performance cases accumulate, the base station antenna market will continue to add high-band products where density, venue, and enterprise traffic justify the higher deployment cost.

By Deployment Type: Rooftop Maintains Share, Tower-Mounted Leads Growth

Rooftop installations retained a 31.27% share in 2025, indicating that the base-station antenna market still relies heavily on elevated urban positions, where tower land is scarce or expensive. Rooftops remain practical in dense, developed areas because they provide macro coverage without forcing operators to undertake full new-tower development. Tower-mounted systems, however, are the fastest-growing deployment type, with a 7.68% CAGR through 2031, driven by greenfield 5G expansion across South Asia, the Middle East, and Africa, as well as parts of South America. The FCC stated that more than 15,000 new towers were activated in the United States in 2024, underscoring that macro infrastructure growth still matters as operators face coverage obligations and rising traffic.

Pole-mounted deployments are gaining relevance because they better align with the small-cell densification model than traditional macro structures in busy city corridors. Alpha Wireless has shown how antenna design is adapting to this need through products that fit existing street furniture while supporting dual-band operation and broad azimuth coverage. Wall-mounted and ground-based systems continue to serve enterprise campuses, event venues, and temporary outdoor capacity builds, and those use cases are expanding with private 5G and neutral-host programs. The result is a more modular deployment mix in the base station antenna market, where vendors gain an advantage when a core design can be adapted across rooftop, pole, and tower contexts without major performance trade-offs.

By Polarization: Dual-Polarized Dominance, Circular-Polarized Gains On Convergence

Dual-polarized antennas held a 57.81% share in 2025, maintaining their dominance in the base station antenna market. Their lead reflects their direct fit with mainstream MIMO architectures from 2×2 to 8×8, as well as their established role in 5G NR deployment. This segment also benefits from greater portfolio depth and stronger manufacturing scale across both Chinese and Western suppliers, making it the default option for macro and rooftop builds. Single-polarized designs still retain a place in rural coverage and fixed-link applications where cross-polarization isolation is less important than cost and mechanical simplicity.

Circular-polarized antennas are forecast to grow at a 7.33% CAGR through 2031 as cellular networks move closer to non-terrestrial and satellite-linked architectures. GSA reported in April 2026 that 97 operators were investing in satellite-to-cellphone connectivity, which supports a gradual increase in demand for circular-polarized systems at gateway and convergence nodes. That shift will not displace dual-polarized products in the near term, but it does widen the product mix for vendors that can serve both terrestrial and NTN programs. Future regulatory clarity around coexistence and spectrum use will matter here, because circular-polarized deployments will grow faster once operators have a clearer path for integrating NTN services into existing cellular footprints

Geography Analysis

Asia-Pacific accounted for 37.32% of the base station antenna market size in 2025 and is projected to expand at a 7.74% CAGR through 2031. The region benefits from a layered growth pattern, with China undergoing a large-scale 5G refresh cycle, India in an active densification phase, and advanced markets like Japan and South Korea advancing network architecture. This supports both high-volume macro demand and higher-value upgrades tied to massive MIMO and wider-band antennas. Japan exemplifies this dual-track pattern, with Ericsson’s 4.5 GHz massive MIMO radios entering NTT DOCOMO’s production network and SoftBank advancing outdoor 7 GHz field verification. Asia-Pacific remains the main volume center of the base station antenna market while driving product evolution across macro, indoor, and multiband configurations.

North America holds a strong position in the base station antenna market by value, despite lower unit volumes compared to Asia-Pacific. Ericsson projects rising mobile data traffic per active smartphone in North America through 2030, with its FWA outlook showing increased fixed wireless subscriptions among major operators, supporting higher-value antenna deployments. Private 5G adds another demand layer, with large enterprise and industrial programs creating antenna opportunities outside the public carrier capex cycle. If FCC efforts to reduce wireless deployment barriers improve permitting timelines, North America will maintain above-average revenue per site despite slower tower growth compared to Asia-Pacific.[3]Federal Communications Commission, “Build America: Eliminating Barriers to Wireless Deployments,” Federal Communications Commission, fcc.gov

Europe maintains steady 5G antenna investment, while the Middle East, Africa, and South America show distinct growth patterns. Europe’s position is supported by standalone rollout activity and growing FWA interest, with Nokia’s Italy deployment with EOLO highlighting mmWave’s role in urban and rural broadband. The Middle East benefits from supportive spectrum economics, with the GSMA noting Saudi Arabia’s broad spectrum assignment and lower operator spectrum costs, which accelerate base-station and antenna procurement. In Africa and South America, growth is driven by the need for spectrum-efficient, multiband, and coverage-aware designs as operators expand 4G density and gradually adopt 5G.

Competitive Landscape

The base station antenna market is fragmented, with Chinese suppliers, Western specialists, and South Korean participants competing across price, design precision, and site-level performance. Chinese vendors leverage scale advantages stemming from their proximity to the world’s largest 5G deployment base, enabling cost compression and faster iteration. Western and non-Chinese suppliers focus on PIM control, efficiency gains, mechanical design, and reducing wind loads or site complexity in challenging installations. This competitive landscape allows both high-volume manufacturers and niche engineering players to succeed in different network layers. The market revolves around strengths in manufacturing scale, site engineering, and portfolio breadth rather than a single dominant vendor.

Strategic moves in 2025 and 2026 highlight evolving competition. Comba Telecom emphasized energy-efficient antenna architectures at MWC 2026 with its Helifeed 3.0 design, positioning efficiency as a core procurement requirement.[4]Comba Telecom, “The 2026 Antenna Evolution, Efficiency as the New Capacity,” Comba Telecom, comba-telecom.com RFS invested millions in factory infrastructure in 2025, showcasing the importance of manufacturing readiness and compliance in mission-critical and in-building connectivity. CellMax launched VERA technology in 2025, offering a 5+dB signal improvement without added interference, using measurable field performance as a differentiator. Ericsson’s triple-band FDD Massive MIMO deployment with Telstra demonstrated how large radio vendors defend premium positions through integration depth and multiband consolidation.

Opportunities are emerging in areas where traditional macro designs fall short. These include AI-ready, integrated antenna systems for AI-native RAN upgrades and software-driven network optimization, lighter massive MIMO hardware for structurally constrained towers, and convergence between terrestrial and non-terrestrial connectivity. Vendors capable of building portfolios across mainstream cellular and specialized configurations will benefit. This dynamic keeps the market open to innovation-led share shifts, even as scale remains critical.

Base Station Antenna Industry Leaders

Comba Telecom Systems Holdings Limited

Tongyu Communication Inc.

Radio Frequency Systems GmbH

Mobi Antenna Technologies (Shenzhen) Co., Ltd

Guangdong Shenglu Telecommunication Tech. Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Comba Telecom showcased its Green Intelligent Integrated Antenna Solution, Helifeed 3.0 green antenna, and ComFlex MAX DAS series with ORAN Gateway at MWC 2026 in Barcelona, positioning energy efficiency and Open RAN compatibility as dual competitive axes for its antenna portfolio.

- March 2026: SoftBank, in collaboration with AGC Inc., successfully conducted outdoor verification of a Functional Beamforming Lens Antenna at 29.7 GHz in Tokyo, achieving an estimated power consumption of 6W, compared with 50W for a comparable massive MIMO array, a potential design direction for energy-efficient 6G base-station antennas.

- January 2026: NEC developed a new 5G Sub-6 GHz Massive MIMO radio unit that delivers 48% uplink and 54% downlink throughput improvements over current models, with 42% power reduction in normal operation, and availability in Japan planned for H1 FY2026.

- December 2025: Ericsson’s 4.5 GHz Massive MIMO AIR 3255 radios, 25% more energy efficient and 20% lighter than prior-generation equivalents, became operational in NTT DOCOMO’s production 5G network in Japan, the first commercial deployment of this radio in a high-demand, high-congestion urban environment.

Global Base Station Antenna Market Report Scope

The Base Station Antenna Market comprises revenues generated from the sale and deployment of antenna systems used in wireless communication base stations to transmit and receive radio frequency (RF) signals across cellular networks. These antennas form a critical part of the radio access network (RAN) infrastructure and support mobile communication technologies, including 3G, 4G/LTE, and 5G. The market includes both passive and active antenna systems deployed across macro cell and small cell network architectures for public and private wireless communication networks.

The Base Station Antenna Market is Segmented by Antenna Type (Macro Cell Antenna, and Small Cell Antenna), Technology (3G, 4G/LTE, and 5G), Frequency Band (Low Band, Sub-1 GHz, Mid Band, 1 GHz-6 GHz, High Band, and Above 24 GHz), Deployment Type (Tower-Mounted, Rooftop, Pole-Mounted, Wall-Mounted, and Ground-Based), Polarization (Single Polarized, Dual Polarized, and Circular polarized), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Macro Cell Antenna | Sector Antenna |

| Active Antenna System | |

| Massive MIMO Antenna | |

| Multibeam Antenna | |

| Small Cell Antenna | Outdoor Small Cell Antenna |

| Indoor Small Cell Antenna |

| 3G | |

| 4G/LTE | |

| 5G | 5G Sub-6 GHz |

| 5G mmWave |

| Low Band, Sub-1 GHz | |

| Mid Band, 1 GHz-6 GHz | 1 GHz-2.6 GHz |

| 3.3 GHz-4.2 GHz | |

| 4.4 GHz-6.0 GHz | |

| High Band and Above 24 GHz |

| Tower-Mounted |

| Rooftop |

| Pole-Mounted |

| Wall-Mounted |

| Ground-Based |

| Single Polarized | Vertical Polarization |

| Horizontal Polarization | |

| Dual-Polarized | |

| Circular-Polarized |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Antenna Type | Macro Cell Antenna | Sector Antenna |

| Active Antenna System | ||

| Massive MIMO Antenna | ||

| Multibeam Antenna | ||

| Small Cell Antenna | Outdoor Small Cell Antenna | |

| Indoor Small Cell Antenna | ||

| By Technology | 3G | |

| 4G/LTE | ||

| 5G | 5G Sub-6 GHz | |

| 5G mmWave | ||

| By Frequency Band | Low Band, Sub-1 GHz | |

| Mid Band, 1 GHz-6 GHz | 1 GHz-2.6 GHz | |

| 3.3 GHz-4.2 GHz | ||

| 4.4 GHz-6.0 GHz | ||

| High Band and Above 24 GHz | ||

| By Deployment Type | Tower-Mounted | |

| Rooftop | ||

| Pole-Mounted | ||

| Wall-Mounted | ||

| Ground-Based | ||

| By Polarization | Single Polarized | Vertical Polarization |

| Horizontal Polarization | ||

| Dual-Polarized | ||

| Circular-Polarized | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the base station antenna market?

The base station antenna market is valued at USD 6.81 billion in 2026 and is forecast to reach USD 9.47 billion by 2031 at a 6.82% CAGR.

What is driving demand for base station antennas through 2031?

The main drivers are 5G and 5G-Advanced rollouts, higher mobile data traffic, urban densification, private 5G adoption, and wider use of massive MIMO and multiband antenna systems.

Which antenna type holds the largest share today?

Macro cell antennas led in 2025 with a 61.33% share because operators still need broad-area coverage and continued macro upgrades for 5G mid-band deployment.

Which technology layer is growing the fastest?

5G is the fastest-growing technology segment, with a projected 7.42% CAGR through 2031, while 4G/LTE still held the largest share at 45.89% in 2025.

Why does Sub-6 GHz remain so important for operators?

Sub-6 GHz held 43.28% share in 2025 because it provides a practical balance of capacity and coverage, making it the core band for most commercial 5G rollouts.

Which region is expected to grow the fastest over the forecast period?

Asia-Pacific is expected to grow the fastest, at a 7.74% CAGR through 2031, supported by China's scale, India's densification push, and continued network upgrades across advanced Asian markets.

Page last updated on: