Point-To-Point Antenna Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

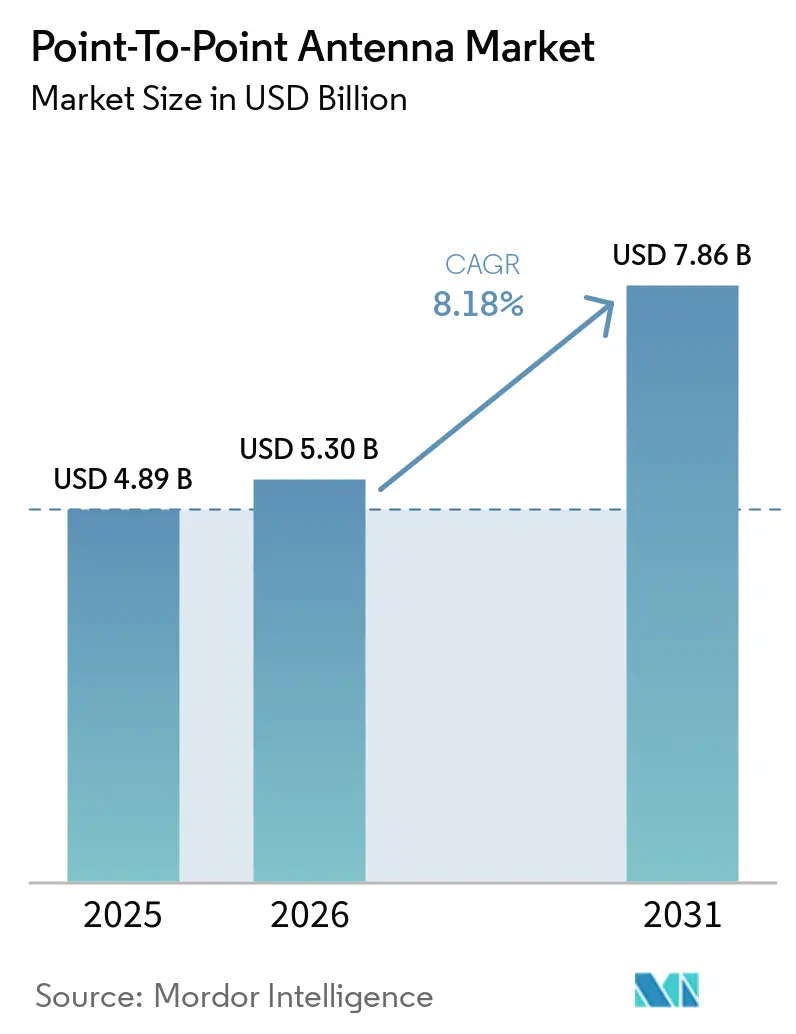

| Market Size (2026) | USD 5.30 Billion |

| Market Size (2031) | USD 7.86 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

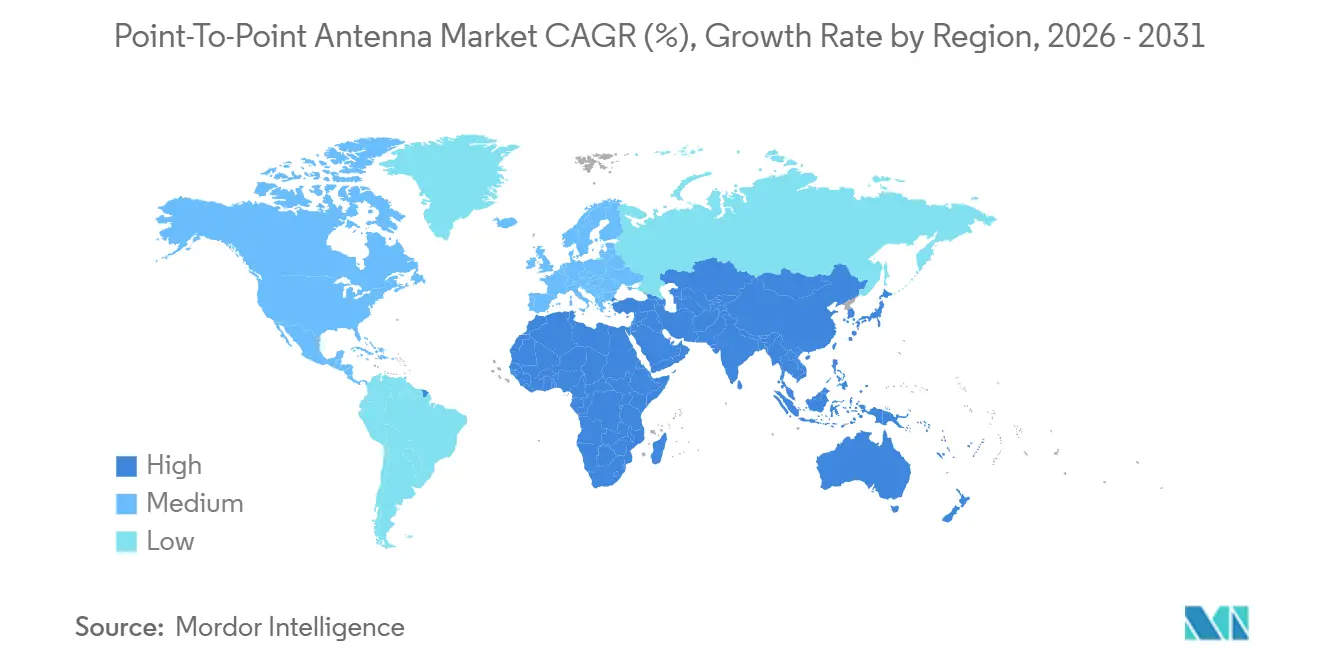

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Point-To-Point Antenna Market Analysis by Mordor Intelligence

The point-to-point antenna market size was USD 4.89 billion in 2025, and is expected to increase from USD 5.30 billion in 2026 to USD 7.86 billion by 2031, growing at a CAGR of 8.18% over 2026-2031. Rising 5G backhaul capacity needs, rural broadband subsidies, and industrial private-network rollouts are reshaping vendor strategies and procurement priorities. Operators shifting to E-band and V-band equipment are driving multigigabit link adoption, while dual-polarized designs help double spectral efficiency without new spectrum fees. Compact flat-panel antennas are reducing wind-load costs, accelerating rooftop deployments in dense cities. At the same time, low-Earth-orbit satellite competition and tightening ETSI class-4 regulations are pressuring margins, prompting manufacturers to invest in adaptive modulation and low-sidelobe feeds.

Key Report Takeaways

- By antenna type, parabolic dishes led the point-to-point antenna market with 58.38% share in 2025; flat panels are poised to expand at an 8.78% CAGR through 2031.

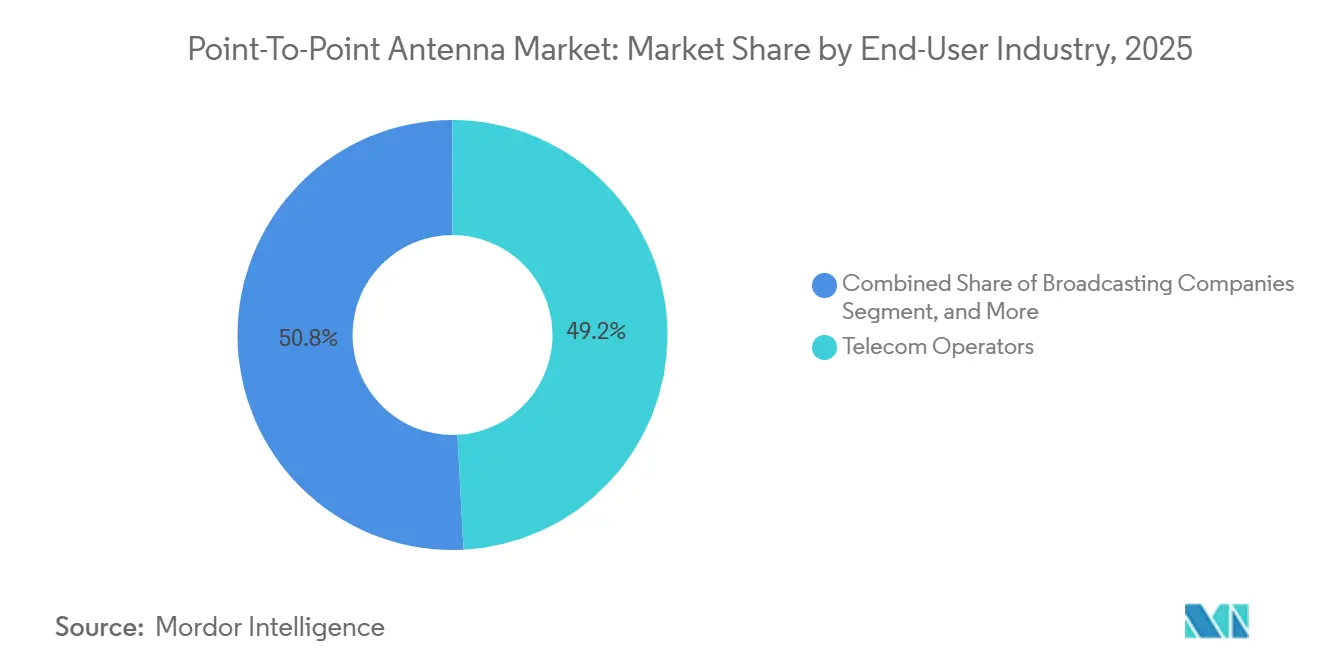

- By end-user industry, telecom operators accounted for 49.19% of the market in 2025, while enterprises and industrial facilities are advancing at an 8.83% CAGR, outpacing telecom operators’ 5G densification spending.

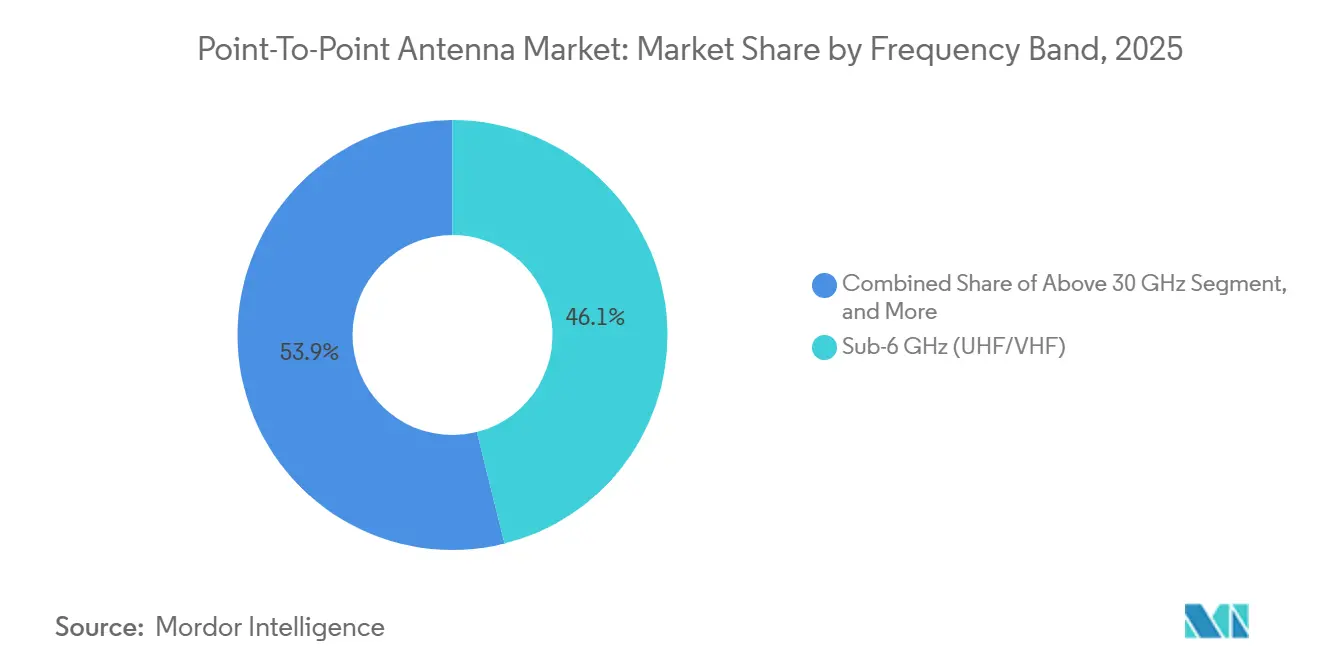

- By frequency band, the sub-6 GHz (UHF/VHF) segment accounted for 46.11% market share in 2025, and millimeter-wave equipment above 30 GHz achieved a 9.06% CAGR in the point-to-point antenna market between 2026 and 2031.

- By polarization, dual-polarized configurations held 51.28% share in 2025 and are projected to register a 9.11% CAGR through 2031.

- By geography, Asia-Pacific commanded 38.33% of the point-to-point antenna market share in 2025, while the Middle East is forecast to be the fastest-growing region, with a 8.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Point-To-Point Antenna Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Demand for 5G Backhaul Capacity | +2.1% | Global, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Rural Broadband Funding Programs | +1.3% | North America, Europe | Long term (≥ 4 years) |

| Rapid Fiber-to-Tower Buildout Gaps | +1.5% | Global, Asia-Pacific, Africa | Short term (≤ 2 years) |

| Millimeter-Wave License Liberalization | +1.2% | Asia-Pacific | Medium term (2-4 years) |

| Proliferation of Private LTE/5G Campuses | +0.9% | Global, Europe, North America | Medium term (2-4 years) |

| Defense Shift to Low-Probability-Intercept Links | +0.7% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Demand For 5G Backhaul Capacity

5G radio networks need backhaul throughput that is 10-20 times higher than 4G, which is pushing operators to millimeter-wave and E-band systems delivering multi-gigabit speeds.[1]International Telecommunication Union, “5G Backhaul Capacity Trends,” itu.int MTN Nigeria’s deployment of 25 Gbps links in 2025 illustrates how legacy sub-10 GHz microwave paths are being retired in favor of new high-capacity routes.[2]MTN Nigeria, “25 Gbps Microwave Deployment,” mtn.ng Vendors such as Cambium Networks supply 10 Gbps E-band radios equipped with adaptive modulation and cross-polarization, enabling carriers to maximize spectrum use without fresh licenses.

Rural Broadband Funding Programs

Subsidies under the United States Rural Digital Opportunity Fund and the European Connecting Europe Facility 2 are underwriting fixed-wireless builds that depend on point-to-point backhaul, with 40% of U.S. winning bids specifying microwave aggregation.[3]Federal Communications Commission, “Rural Digital Opportunity Fund Results,” fcc.gov Because regulatory latency limits favor microwave over satellite, wireless ISPs can secure 10-year revenue guarantees before investing in equipment.[4]National Telecommunications and Information Administration, “BEAD Program,” ntia.gov Similar grants in Canada and Spain are spurring local operators to blend fiber and point-to-point links for last-mile coverage.

Rapid Fiber-to-Tower Buildout Creating Last-Mile Gaps

Permitting delays and labor shortages leave thousands of live 5G sites awaiting fiber, so carriers deploy microwave links for interim connectivity, often for 12-24 months. RAD’s 2025 industrial campus projects showed 1 Gbps symmetrical service over 10 km distances, which helped plant operators avoid month-long fiber trenching delays. The approach is most visible in Africa and Southeast Asia, where fiber reaches less than 20% of cell towers.

Millimeter-Wave License Liberalization in Emerging Asia

India’s 2025 consultation on administrative E-band and V-band allocation eliminates auction fees that can top USD 1 million per MHz, accelerating deployments for Bharti Airtel and Vodafone Idea. Japan’s pending 40 GHz auction targets dense urban backhaul, while South Korea’s existing E-band framework has already reduced average spectrum cost by 35% relative to 6-30 GHz bands. This liberalization cuts the total cost of ownership, favoring flat-panel vendors with pre-certified millimeter-wave gear.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum Re-Farming for 5G Mobile | -1.4% | Global, North America, Europe | Short term (≤ 2 years) |

| High Wind-Load Compliance Costs | -0.6% | Global, cyclone-prone regions | Medium term (2-4 years) |

| Tightening ETSI Class-4 Radiation Rules | -0.5% | Europe, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Rising Satellite Backhaul Competition | -0.8% | Africa, South America, rural Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spectrum Re-Farming for 5G Mobile Eroding Microwave Bands

In recent years, regulators in North America and Europe have reallocated C-band spectrum blocks to support the deployment of 5G networks. This decision has compelled microwave licensees to transition to higher-frequency bands, which are characterized by shorter ranges and require additional towers to maintain network coverage. The relocation process has incurred high costs totaling USD 9.7 billion, placing considerable financial strain on operators' budgets. Furthermore, this shift has created short-term gaps in network availability, particularly in areas where E-band frequencies have not yet received national clearance for use.

High Wind-Load Compliance Costs for Parabolic Dishes

Parabolic dishes, commonly used in communication systems, often exceed 0.5 m² in frontal area, which violates wind-load limits in regions prone to extreme weather conditions such as hurricanes and typhoons. To address this issue, structural reinforcement is often required to ensure the stability of these installations, with costs ranging from USD 5,000 to USD 15,000 per tower. These additional expenses have prompted carriers to adopt alternative solutions, such as 60% smaller flat-panel units. These compact units not only comply with wind-load regulations but also streamline compliance with building codes. This transition has resulted in reduced leasing fees and expedited rooftop approvals, particularly in areas like the United States Gulf Coast, which frequently experiences hurricanes, and Japan’s Pacific seaboard, known for its susceptibility to typhoons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Frequency Band: Millimeter-Wave Dominance Emerges

The Sub-6 GHz (UHF/VHF) band retained 46.11% of 2025 revenue, yet millimeter-wave systems above 30 GHz are projected to post a 9.06% CAGR, underscoring how 5G densification is tilting demand toward ultra-wide channels. Within this high-band slice, E-band and V-band links deliver up to 25 Gbps, giving urban carriers headroom for multi-sector massive-MIMO sites. As nations harmonize E-band plans under ITU-R F.2086, vendors can ship single-SKU radios to multiple markets, compressing inventory costs. Although traditional 6-30 GHz microwave remains indispensable for rural spans over 50 km, the arrival of low-cost flat panels erodes its exclusivity in suburban corridors.

Steady regulatory liberalization is making millimeter-wave the default choice in India, Japan, and South Korea, where spectrum below 6 GHz is exhausted. The point-to-point antenna market size for millimeter-wave gear is forecast to surpass USD 3 billion by 2031, accounting for almost 40% of the overall value. Conversely, sub-6 GHz units keep their foothold in broadcast and public-safety systems that need diffraction and non-line-of-sight performance rather than peak capacity. Such diversity supports multi-band portfolios from CommScope and SIAE Microelettronica, which hedge exposure as license frameworks evolve.

By Antenna Type: Flat Panels Challenge Parabolic Incumbency

Parabolic dishes accounted for 58.38% of revenue in 2025, driven by their >45 dBi gain across 6-30 GHz. Yet flat-panel and slotted waveguide shipments are rising at an 8.78% CAGR thanks to wind-load advantages and quick installs. Cambium’s PTP 850CX delivers comparable reach in a housing 60% smaller than legacy reflectors, cutting tower rent and permitting cycles. Siklu’s 70/80 GHz phased arrays add electronic beam steering, removing mechanical alignment tasks and enabling rooftop crews to finish a link in under 30 minutes.

The point-to-point antenna market share for flat panels is likely to approach 45% in urban millimeter-wave backhaul by 2031, aided by municipal codes capping rooftop equipment size. Parabolic models will still dominate long-haul 6-GHz paths spanning deserts, mountains, and offshore rigs, markets where link budgets edge out form-factor concerns. Meanwhile, horn and Yagi variants retain specialized uses in quick-deploy disaster recovery and sub-GHz public-safety nets.

By Application: Private Networks Narrow the Telecom Backhaul Lead

Telecom backhaul accounted for 42.29% of 2025 deployments, so it still anchors the point-to-point antenna market, yet enterprise connectivity is advancing at an 8.95% CAGR and is on track to erode carriers' dominance during the forecast window. Fixed-wireless internet service providers also leverage microwave aggregation to serve rural subscribers where fiber remains unviable, while TV broadcast studios continue to depend on sub-6 GHz links for studio-to-transmitter paths that prize reliability over raw throughput. Private LTE and 5G campuses now demand symmetrical 1 Gbps links for real-time video analytics and machine automation, favoring millimeter-wave radios paired with dual-polarized flat panels that can be installed quickly on factory rooftops. Military and public-safety agencies add a steady trickle of high-margin orders for encrypted, low-probability-intercept radios that resist jamming in contested environments.

The addressable pool for enterprise links is expanding fastest in manufacturing hubs across North America, Germany, and Japan, where firms adopt Industry 4.0 workflows that cannot wait for multi-year fiber trenching projects. As a result, the point-to-point antenna market for enterprise connectivity is projected to leapfrog wireless ISP revenue by 2029. Meanwhile, carriers pursue hybrid fiber-microwave rollouts that plug temporary gaps in 5G densification, sustaining telecom backhaul volumes even as their share slips below 40% near the end of the period. Broadcast demand remains largely flat, but refresh cycles toward high-definition and IP workflows keep legacy 6-7 GHz paths alive. Collectively, these trends diversify demand across at least five major application buckets, spreading risk for vendors while raising the importance of software-defined radios that can be retuned as customers pivot among use cases.

By End-User Industry: Enterprises and Defense Outpace Carrier Spend

Telecom operators held 49.19% of end-user demand in 2025, reflecting massive 5G backhaul investment, but enterprises and industrial facilities are expanding at an 8.83% CAGR, and their share is expected to top 30% by 2031. Manufacturers, logistics providers, and energy companies gravitate toward turnkey microwave kits bundled with cloud orchestration, easing deployment for IT teams that lack RF specialists. Wireless ISPs remain a resilient niche because rural broadband subsidies in the United States and Europe offset capital risk, allowing small providers to finance high-capacity E-band links on 10-year subsidy contracts. Broadcast networks continue to renew long-haul 7 GHz paths for studio distribution, though the segment’s absolute growth is modest.

Defense and government agencies inject premium revenue into the point-to-point antenna market, purchasing ruggedized radios with FIPS-validated encryption and frequency hopping that cost two to three times commercial equivalents. Consequently, the point-to-point antenna market share associated with military procurement is small in volume yet outsized in profit contribution. Enterprises, by contrast, favor subscription-based management suites that compress operating expenses, a dynamic that benefits vendors such as Cambium Networks and Ubiquiti. As carriers off-load non-strategic towers to neutral-host companies, tower owners will also emerge as a discrete buying center for backhaul radios, further redistributing demand away from legacy operator accounts.

By Polarization: Dual-Polarized Designs Become the New Baseline

Dual-polarized antennas captured 51.28% of 2025 revenue and are growing at a 9.11% CAGR because they double spectral efficiency within the same channel license, a decisive advantage in congested urban corridors. Operators can now run independent horizontal and vertical streams at adaptive modulation rates up to 4096-QAM, hitting multigigabit throughput without new spectrum fees. Single-polarized equipment persists in cost-sensitive public-safety networks and legacy rural backbones where traffic growth is modest, but its relevance fades as 5G densification accelerates.

Regulatory frameworks such as ETSI EN 302 217 mandate cross-polarization discrimination of 30 dB or better, prompting antenna vendors to redesign feed horns and radomes for higher fidelity. As these stricter patterns become mandatory in new deployments, dual-polarized gear shifts from a premium option to a default specification, especially on towers that cannot accommodate multiple dishes. This evolution boosts the point-to-point antenna market size for integrated dual-polar solutions while gradually shrinking demand for add-on XPIC modules. Looking ahead, quad-polar systems under early field test could appear late in the decade, but widespread adoption will hinge on whether operators can secure matching four-carrier licenses at an acceptable cost. For now, dual polarization remains the sweet spot, balancing link capacity, hardware complexity, and regulatory compliance.

Geography Analysis

Asia-Pacific accounted for 38.33% of 2025 revenue, driven by significant developments in countries like India and Japan. India continued to rely on microwave technology for 54% of its towers, while Japan set an ambitious target of deploying 50,000 millimeter-wave sites by 2027 to enhance its network infrastructure. In December 2025, India introduced a backhaul framework that opened six microwave bands, along with E-band and V-band, specifically for fixed-wireless applications. This move eliminated auction premiums, which had previously hindered the expansion of rural connectivity. Meanwhile, in China, integrated RAN procurements obscure exact volumes; however, anecdotal evidence indicates that state carriers predominantly prefer domestic vendors for 70 GHz links used in metro ring networks.

The Middle East, led by the UAE and Saudi Arabia, is the fastest-growing sub-region, with a 8.92% CAGR. du and Ericsson validated 1 Gbps millimeter-wave reach over 2 km in Dubai’s April 2026 trial, proving suitability for smart-city IoT backhaul. Qatar’s Lusail project leverages 25 Gbps E-band hops to pipe real-time analytics, showcasing the smart city's dependence on gigabit microwave. North America benefits from USD 62.85 billion in combined federal subsidy pools that prioritize hybrid fiber-wireless designs in low-density counties. However, C-band re-farming has squeezed long-haul microwave out of urban corridors, hastening a pivot to 70-90 GHz rooftop hops while satellite challengers such as Starlink court remote oil fields.

Europe invests in rural gigabit coverage through CEF-2, with priority given to regions where fiber trenching costs exceed EUR 50,000 (USD 56,500) per kilometer. Operators migrating off the cleared 3.7-4.2 GHz channels incur additional costs to retune to higher bands, prompting carriers in Germany and France to negotiate multiyear E-band tower leases at discounted rates. South America is bridging fiber buildouts with interim microwave. Eletronet’s BRL 157 million (USD 31 million) 2026 expansion leaves a 500-meter gap between many towers, which is filled by low-cost 18 GHz dishes. Brazil’s varied climate also lifts demand for rain-fade-resistant dual-carrier solutions.

Competitive Landscape

The market is moderately consolidated, with CommScope, SIAE Microelettronica, and Intracom Telecom collectively holding a significant share of shipments and relying on long-standing carrier accounts. Cambium Networks and Ubiquiti penetrate the wireless ISP and enterprise markets through cloud-control platforms that reduce operating expenses. Siklu, BridgeWave, and Aviat specialize in millimeter-wave technology and fielding phased arrays that significantly reduce installation time.

Strategic moves focus on vertical integration and compliance agility. SIAE’s 2025 Ka-band partnership with Qorvo embeds adaptive beamforming ICs to maintain link quality at 10 dB or less of rain attenuation. Cambium’s 2026 Evo cloud suite unifies PTP and PTMP management, appealing to MSPs that lack RF engineers. LEO satellite operators remain disruptive entrants; Starlink touts sub-50 ms latency, threatening remote microwave backhaul, though regulatory coordination and rooftop rights slow terrestrial cannibalization.

Vendor responses include class-4 ETSI-certified antennas with 30 dB cross-polarization discrimination, ensuring compliance with the 2024 radiation regulations while maintaining optimal performance. These antennas are designed to meet stringent industry standards without compromising efficiency or reliability. Additionally, defense procurement has emerged as a significant growth area. HEICO’s acquisition of Southwest Antennas in April 2026 has strategically expanded its aerospace portfolio by incorporating ruggedized sub-8.5 GHz products. This move aims to address the growing demand for low-intercept probability contracts, which are critical for secure, covert communication systems in defense applications.

Point-To-Point Antenna Industry Leaders

Cambium Networks Corporation

Ubiquiti Inc.

Siklu Communication Ltd.

SIAE Microelettronica S.p.A.

Intracom Telecom S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cambium Networks launched the Evo cloud platform to automate configuration and monitoring across PTP 850 and cnWave lines, cutting OPEX for ISPs and enterprises.

- April 2026: HEICO bought 90% of Southwest Antennas, broadening its defense-grade RF catalog.

- April 2026: du and Ericsson completed the UAE’s first commercial millimeter-wave extended-range trial, achieving 1 Gbps at 2 km to support smart-city services.

- April 2026: Ondas acquired World View Enterprises for USD 140 million, adding stratospheric balloon relays that complement terrestrial microwave.

Global Point-To-Point Antenna Market Report Scope

The Point-to-Point Antenna Market is the global industry focused on the design, manufacturing, deployment, and sale of antennas for dedicated wireless communication links between two fixed locations. These antennas enable high-capacity, line-of-sight data transmission for applications such as telecom backhaul, broadband connectivity, broadcasting, defense communications, and enterprise networking. The market encompasses antennas operating across multiple frequency bands, including Sub-6 GHz, 6-30 GHz, and above 30 GHz, supporting varying range, bandwidth, and performance requirements.

The Point-to-Point Antenna Market Report is Segmented by Frequency Band (Sub-6 GHz, 6-30 GHz, and Above 30 GHz), Antenna Type (Parabolic Dish, Flat Panel and Slotted Waveguide, Yagi, Horn, and Other Antenna Type), Application (Telecom Backhaul, Wireless Broadband ISP, TV Broadcast Distribution, Military and Public Safety Networks, and Enterprise Connectivity), End-User Industry (Telecom Operators, Internet Service Providers, Broadcasting Companies, Defense and Government Agencies, and Enterprises and Industrial Facilities), Polarization (Single-Polarized, Dual-Polarized, and Cross-Polarized), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Sub-6 GHz (UHF/VHF) |

| 6-30 GHz (Microwave) |

| Above 30 GHz (Millimeter-Wave) |

| Parabolic Dish |

| Flat Panel and Slotted Waveguide |

| Yagi |

| Horn |

| Other Antenna Type |

| Telecom Backhaul |

| Wireless Broadband ISP |

| TV Broadcast Distribution |

| Military and Public Safety Networks |

| Enterprise Connectivity |

| Telecom Operators |

| Internet Service Providers |

| Broadcasting Companies |

| Defense and Government Agencies |

| Enterprises and Industrial Facilities |

| Single-Polarized |

| Dual-Polarized |

| Cross-Polarized |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Frequency Band | Sub-6 GHz (UHF/VHF) | |

| 6-30 GHz (Microwave) | ||

| Above 30 GHz (Millimeter-Wave) | ||

| By Antenna Type | Parabolic Dish | |

| Flat Panel and Slotted Waveguide | ||

| Yagi | ||

| Horn | ||

| Other Antenna Type | ||

| By Application | Telecom Backhaul | |

| Wireless Broadband ISP | ||

| TV Broadcast Distribution | ||

| Military and Public Safety Networks | ||

| Enterprise Connectivity | ||

| By End-User Industry | Telecom Operators | |

| Internet Service Providers | ||

| Broadcasting Companies | ||

| Defense and Government Agencies | ||

| Enterprises and Industrial Facilities | ||

| By Polarization | Single-Polarized | |

| Dual-Polarized | ||

| Cross-Polarized | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large will the point-to-point antenna market be by 2031?

Mordor Intelligence projects the point-to-point antenna market size to reach USD 7.86 billion by 2031 at an 8.18% CAGR.

Which antenna type is growing fastest?

Flat-panel antennas are forecast to post an 8.78% CAGR through 2031, narrowing the gap with parabolic dishes.

What drives millimeter-wave adoption in Asia-Pacific?

Liberalized E-band and V-band licensing in India and Japan, along with 5G densification targets, are accelerating millimeter-wave backhaul rollouts.

How are rural broadband subsidies affecting demand?

US and EU funding programs de-risk fixed-wireless projects, leading to higher orders for point-to-point backhaul links among regional ISPs.

Which vendors dominate the market today?

CommScope, SIAE Microelettronica, and Intracom Telecom hold a combined 37% share, but Cambium Networks and Ubiquiti are rapidly expanding in enterprise and ISP channels.

What is the role of dual-polarization?

Dual-polarized antennas double spectral efficiency within existing licenses, helping operators meet multigigabit backhaul targets without new spectrum purchases.

Page last updated on: