Chip Antenna Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

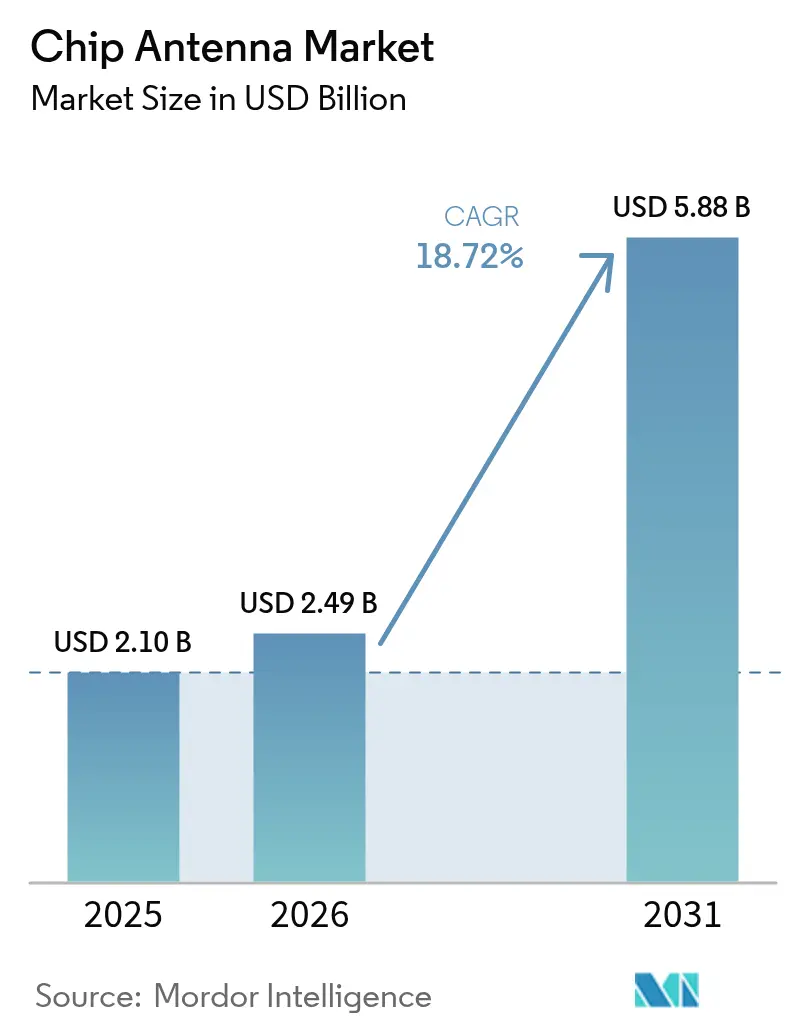

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 5.88 Billion |

| Growth Rate (2026 - 2031) | 18.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chip Antenna Market Analysis by Mordor Intelligence

The Chip Antenna Market size was valued at USD 2.10 billion in 2025 and estimated to grow from USD 2.49 billion in 2026 to reach USD 5.88 billion by 2031, at a CAGR of 18.72% during the forecast period (2026-2031).

Rapid miniaturization of consumer electronics, 5G roll-outs, and a growing fleet of IoT devices are the primary forces widening demand for compact, high-performance antennas that fit where classical PCB or FPC formats cannot. Design wins in Bluetooth Low Energy wearables, LTCC adoption in in-cabin radar, and Wi-Fi 6E reference mandates in smart appliances are accelerating volume shipments, while private 5G industrial networks supply an additional layer of long-term growth. Concurrently, patent disputes around fractal geometry and the technical hurdle of multi-radio coexistence in ultra-compact devices are pressing suppliers to pursue inventive materials and form factors that raise efficiency and shrink footprints.

Key Report Takeaways

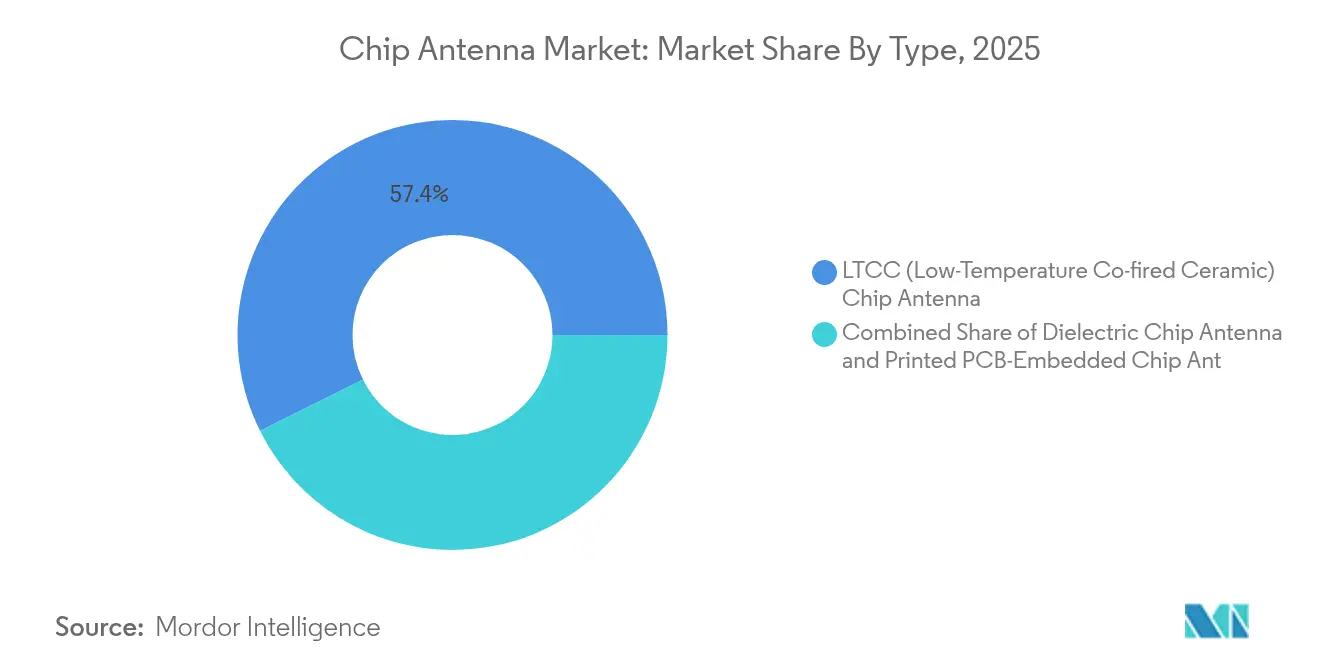

- By type, LTCC captured 57.35% of the chip antenna market share in 2025; dielectric ceramic is projected to grow at a 19.86% CAGR to 2031.

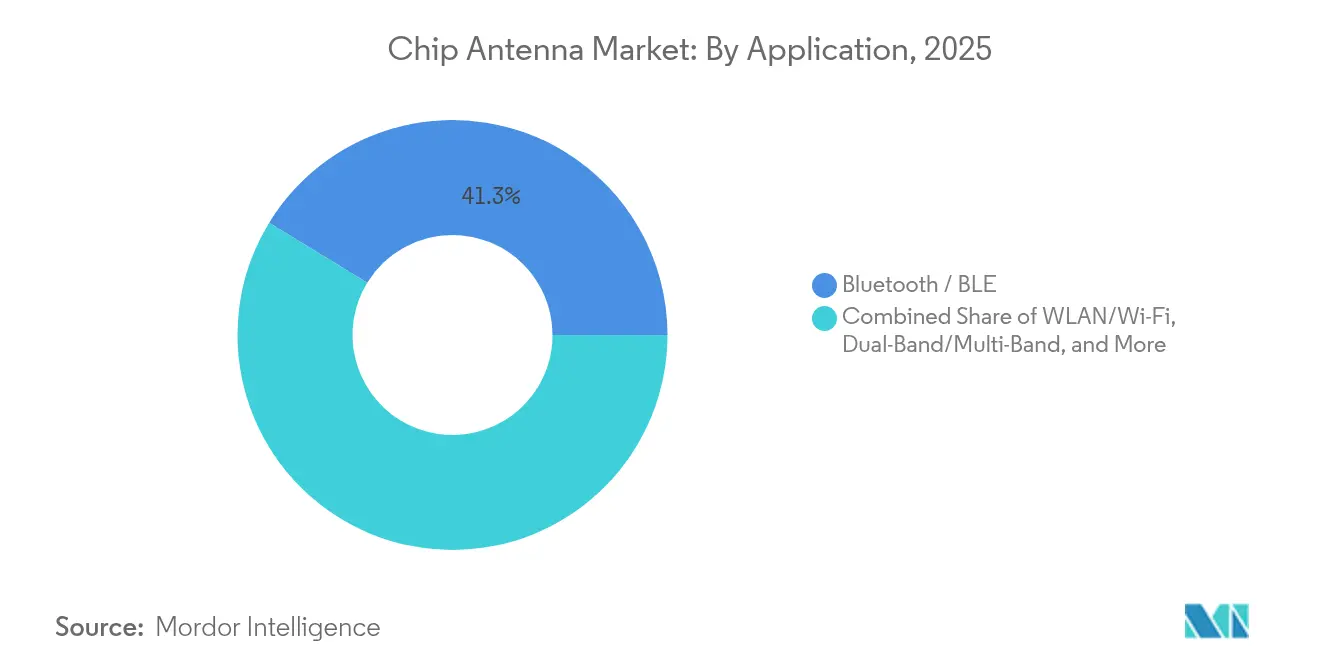

- By application, Bluetooth/BLE held 41.25% of the chip antenna market size in 2025, while GPS/GNSS is projected to expand at a 20.92% CAGR to 2031.

- By end-user, IT & telecommunications infrastructure accounted for 32.45% of revenue in 2025; automotive is advancing at a 19.73% CAGR through 2031.

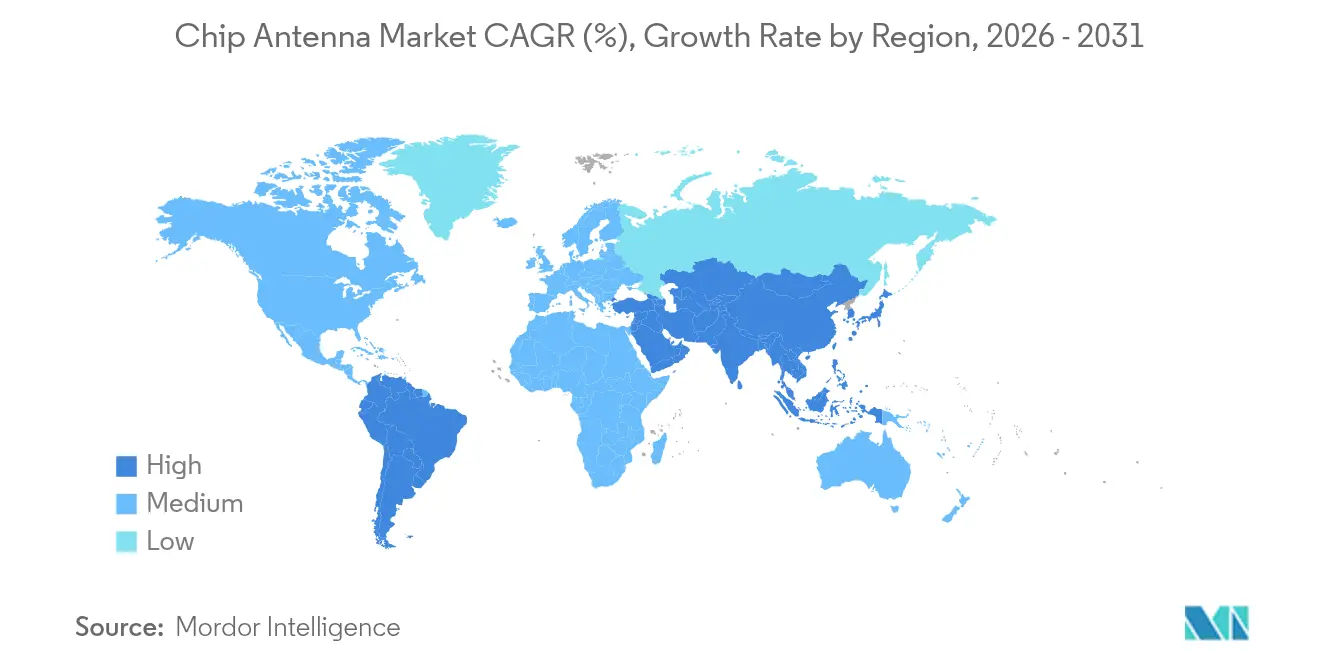

- By region, Asia Pacific led with 45.60% revenue share in 2025; North America is forecast to expand at a 19.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chip Antenna Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bluetooth-LE design wins for wearables | +4.80% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| LTCC antennas in in-cabin ADAS radar | +3.80% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Wi-Fi 6E reference designs in smart appliances | +3.40% | Global | Short term (≤ 2 years) |

| Private-5G industrial networks | +2.90% | North America, Europe, Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bluetooth-LE design wins for wearables in OEM clusters

Bluetooth Low Energy has become the de facto protocol for smart watches, fitness sensors, and emerging medical wearables. Tier-one OEMs have started standardizing antenna layouts across multiple product families, enabling economy-of-scale procurement and faster platform refresh cycles. Nordic Semiconductor’s nRF54L series underscores the trend with a higher-efficiency radio and reference layout optimized for chip antennas. Annual Bluetooth LE device shipments exceeded 1.8 billion in 2024, a figure that keeps antenna suppliers on an upward capacity trajectory. The design convergence is spreading into industrial and medical categories where reliability, biocompatibility, and firmware-over-air updates add further performance requirements. Consequently, vendors are investing in tunable impedance networks and high-dielectric ceramics to balance size with efficiency.

LTCC antennas adopted in-cabin ADAS radar modules

Automakers increasingly embed radar units behind headliners and dashboards to monitor occupants. These locations demand antennas that withstand heat cycles and deliver stable gain at 76-81 GHz. LTCC substrates meet both needs through low loss tangent and dimensional stability. Johanson Technology’s directional RHCP antenna combines AEC-Q200 qualification with a slim profile that resists detuning from plastic trim[1]Johanson Technology, “2440AT62B0085002U Automotive Antenna,” johansontechnology.com. Parallel R&D alliances, such as Indie Semiconductor with GlobalFoundries, target 77 GHz and 120 GHz radar SoCs that call for equally precise antenna arrays. These moves elevate chip antennas from discretionary items to safety-critical components governed by automotive PPAP and ISO 26262 workflows.

Wi-Fi 6E reference designs mandate chip antennas in smart appliances

Opening the 6 GHz band doubled the unlicensed spectrum ceiling, allowing appliance OEMs to embed true tri-band radios. Reference platforms from chipset vendors now circulate with explicit chip-antenna footprints to maintain isolation across 2.4, 5, and 6 GHz paths. Murata’s Type 2FY module, built around Infineon’s CYW55513, arrives pre-certified for U.S. and EU markets and demonstrates a sub-2 dB return loss uplift on 6 GHz when paired with a 7 mm LTCC antenna[2]Murata Manufacturing, “Type 2FY Wi-Fi 6E/BLE Module Release,” murata.com. Integration places fresh emphasis on spatial-filter structures and matching networks that only specialized antenna vendors currently supply at scale.

Private 5G industrial networks driving sub-6 GHz sensor demand

Factory and warehouse operators are rolling out private NR networks to connect robots, machine vision cameras, and sensor nodes. Investments are pacing at a 42% CAGR toward USD 3.5 billion by 2027, with early adopters citing latency cuts of 40 ms versus Wi-Fi in closed-loop controls. Sub-6 GHz chip antennas see heightened volumes because floor-mounted and ceiling-mounted sensors require compact, omnidirectional elements that tolerate metal enclosures. Advanced features such as ultra-reliable low-latency communication (URLLC) elevate return-loss targets and in-situ calibration support, pushing vendors to integrate temperature-stable ceramics and phased stamping techniques.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Efficiency gap vs. PCB/FPC in mmWave AR | -2.30% | North America, Asia Pacific | Medium term (2-4 years) |

| U.S. fractal-geometry IP litigation | -1.50% | Global (emphasis North America) | Short term (≤ 2 years) |

| Multi-radio coexistence detuning in wearables | -1.30% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Efficiency gap vs. custom PCB/FPC antennas in mmWave AR glasses

Augmented-reality eyewear streams multi-gigabit data over 24 GHz and higher bands. Custom copper traces etched into curved FPCs still outperform discrete chip antennas by up to 2 dB in total radiated power, a gap that directly impacts battery life and graphics latency. Research into transparent slot-loop antennas etched on metal-mesh films shows promise, but mass adoption remains limited due to higher bill-of-materials costs and fragile substrates. Consequently, premium AR/VR brands continue to specify tailored feed structures, sidelining off-the-shelf chip antennas in this niche.

U.S. fractal-geometry IP litigation disrupting supply-chain diversification

Litigation around multilevel fractal antennas, notably patents US9362617B2 and US11349200B2 held by Fractus SA, forces OEMs to weigh licensing fees against redesign timelines. The uncertainty discourages smaller suppliers from entering multi-band antenna niches, consolidating bargaining power among incumbents, and slowing alternative form-factor exploration. Project rollouts aimed at mid-band 5G or dual-band GNSS can face multi-quarter delays when infringement claims surface, translating to real revenue drag for the chip antenna market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: LTCC maintains lead through thermal stability

LTCC antennas held 57.35% of the chip antenna market share in 2025 due to their ability to operate at millimeter-wave frequencies with minimal performance drift under wide temperature swings. This dominance is reinforced by rising adoption in automotive radar modules that must endure up to +105 °C profiles on cabin roofs. Printed dielectric antennas trail in volume but post the fastest growth, riding a 19.86% CAGR as materials science innovations squeeze higher Q-factors into thinner substrates.

Demand is further bolstered by smartphone OEMs that value LTCC’s co-fired multilayer capability, allowing integration of filtering and matching networks inside the same ceramic block. Conversely, PCB-embedded antennas remain an attractive choice for cost-sensitive IoT gateways where performance tolerances are broad and unit counts run into millions. Continuous miniaturization funnels R&D dollars into ultra-short monopole geometries, aiding penetration in medical capsules that require 2.4 GHz telemetry yet measure under 10 mm.

By Application: Bluetooth leads while GPS accelerates

Bluetooth/BLE recorded 41.25% of 2025 revenue, kept aloft by wearables, smart locks, and hearing aids that need ultra-low power yet stable 2.4 GHz links. OEM standardization on BLE shapes a predictable design ecosystem in which catalog chip antennas shorten development cycles and cut certification costs. The GPS/GNSS segment is the fastest riser, moving at a 20.92% CAGR as connected cars, drones, and precision-agriculture handsets demand centimeter-level accuracy.

Next-generation GNSS receivers incorporating L1, L2, and L5 bands raise gain requirements, prompting antenna makers to tailor stacked ceramic resonators. Wi-Fi, especially Wi-Fi 6E, follows close behind as tri-band routers and smart appliances proliferate. Multi-protocol devices that juggle Bluetooth, Wi-Fi, and LPWAN push suppliers toward broadband or dual-feed architectures that keep impedance under control across an octave of frequencies.

By End-User: Telecom infrastructure dominates while automotive accelerates

IT & telecommunications operators captured 32.45% of the 2025 demand thanks to the densification of 5G small cells and back-haul radios. Indoor DAS and outdoor micro-sites now frequently employ chip antennas as reference elements for auto-calibration routines. Automotive electronics register the steepest climb, at a projected 19.73% CAGR to 2031, mirroring the shift toward advanced driver-assistance features that mandate radar, LTE, and Wi-Fi inside every trim level.

Consumer electronics retains a broad base, yet unit growth decelerates compared with connected-vehicle volumes. Healthcare devices emerge as a strategic frontier where regulatory compliance and biocompatibility elevate margins. Industrial IoT augments long-term visibility because predictive-maintenance sensors rely on low-profile antennas to fit inside metallic housings on factory floors.

Geography Analysis

Asia Pacific controls 45.60% of the chip antenna market revenue and is expanding at a forecast 19.48% CAGR through 2031. China deploys more than 2.3 million 5G base stations, sustaining a high-volume procurement pipeline for small-form antennas used in CPE routers and UE modules. Japan’s precision-manufacturing heritage positions local suppliers at the premium end of LTCC, cementing supply lines to tier-one automotive clients. South Korean conglomerates leverage in-house capabilities to embed custom multi-band antennas into smartphones and home appliances, reinforcing domestic vertical integration.

North America ranks second as telecom carriers refarm mid-band spectrum and EV makers push data-rich platforms that require robust sub-6 GHz links. The CHIPS and Science Act stimulates domestic substrate and packaging capacity, indirectly supporting antenna production in Arizona and Texas. Demand from defense and aerospace primes further incremental gains because SATCOM terminals and low-earth-orbit user equipment rely on phased arrays with ceramic feed networks.

Europe trails closely, anchored by Germany’s automotive sector and the EU’s strict EMC regulations that favor higher-quality dielectric solutions. The European Chips Act seeks to replicate parts of Asia’s supply chain, providing funding that could catalyze regional antenna fabrication over the next five years. Regulatory harmonization across L-band GNSS and 6-GHz Wi-Fi also influences antenna tuning priorities for products intended for continental markets.

Competitive Landscape

The global playing field blends specialized firms focused on high-frequency ceramics with diversified component conglomerates that spread risk across connectors, filters, and antennas. The chip antenna market is moderately fragmented; the top five suppliers controlled about 34% of revenue in 2024. Application-specific designs now dominate RFPs, rewarding vendors able to co-optimize radiation, filtering, and EMC performance within a single package.

Johanson Technology illustrates this specialization by rolling out a directional 2.4 GHz chip antenna sporting right-hand circular polarization for over-the-air robustness inside vehicles. Murata integrates chip antennas with certified radio modules, allowing appliance OEMs to meet certification windows without bespoke RF expertise. Molex invests in virtual-antenna technology to offer broadband coverage from 698 MHz to 10.5 GHz, targeting IoT endpoints that require protocol agility.

Intellectual property battles act as a soft barrier to entry. Fractus SA holds key fractal-geometry patents, spurring license negotiations that can influence cost structures for new entrants[3]Fractus SA, “Multilevel Antenna Patent Portfolio,” fractus.com. Meanwhile, suppliers experiment with additive manufacturing and glass-ceramic fusion to sharpen beam steering for sub-THz links aimed at next-generation AR headsets and fixed-wireless access. Buyers increasingly rate vendors by traceability, AEC-Q200 compliance, and dual-sourcing ability in light of geopolitical supply-chain scrutiny.

Chip Antenna Industry Leaders

Vishay Intertechnology, Inc.

Yageo Corporation

Johanson Technology,Inc.

Mitsubishi Materials Corporation

Antenova Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Johanson Technology debuted a directional RHCP 2.4 GHz chip antenna for automotive IoT, qualified to AEC-Q200 standards.

- April 2025: Murata launched the Type 2FY Wi-Fi 6E/BLE module featuring Infineon’s CYW55513, pin-compatible with earlier modules for easy upgrades.

- March 2025: Sivers Semiconductors unveiled new SATCOM and 5G antenna arrays at MWC 2025, broadening its chip-level phased-array portfolio.

- February 2025: Spectrum Control launched the SCRS-00-1001 RF+ SiP, down-converting 18-40 GHz to 2-18 GHz to shrink mmWave radio footprints.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the chip antenna market as the revenue generated from newly manufactured, surface-mount ceramic or dielectric antennas that are soldered directly onto printed circuit boards to enable short-range wireless links such as Bluetooth, Wi-Fi, GNSS, LPWAN, and emerging 5G sub-6 GHz/mmWave modules. According to Mordor Intelligence, devices integrating antenna-in-package solutions or printed PCB traces are not included, nor are external patch, FPC, or metal-stamp antennas.

Scope Exclusions: After careful scope review, we exclude revenues from custom millimeter-wave phased-array modules supplied as part of full radio boards.

Segmentation Overview

- By Type

- LTCC (Low-Temperature Co-fired Ceramic) Chip Antenna

- Dielectric Chip Antenna

- Printed PCB-Embedded Chip Antenna

- By Application

- WLAN/Wi-Fi

- Bluetooth/BLE

- Dual-Band/Multi-Band

- GPS/GNSS

- LPWAN (NB-IoT, LoRa, Sigfox)

- By End-User Industry

- Automotive

- Consumer Electronics

- Healthcare and Medical Devices

- IT and Telecommunications Infrastructure

- Industrial and Retail IoT

- Smart Grid and Smart Home

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East

- GCC

- Israel

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed RF-module OEMs, PCB contract manufacturers, and antenna-design consultants across Asia-Pacific, North America, and Europe to validate die attach yields, average selling prices, and multiband design win rates, filling data gaps left by desk work.

Desk Research

We mapped the market landscape using freely available tier-1 sources such as ITU wireless equipment reports, FCC equipment authorization datasets, UN Comtrade ceramic component export codes, IEEE Xplore papers on LTCC substrates, and statistics from trade bodies like the Bluetooth SIG. Annual reports, 10-Ks, and investor decks from leading component makers added shipment ranges, while press releases on 5G small-cell rollouts completed our demand signals. Supplementary intelligence was pulled from D&B Hoovers for company financial splits and Dow Jones Factiva for merger pipelines. The sources cited above illustrate the breadth of material consulted; many additional open databases and technical journals were referenced to cross-check figures and terminology.

Market-Sizing & Forecasting

A top-down demand pool was first reconstructed from global IoT device shipments, smartphone production, 5G small cell deployments, automotive telematics units, and Bluetooth/BLE module output. Results were then corroborated with selective bottom-up checkpoints such as sampled ASP × volume from leading suppliers to refine totals. Key variables like LTCC substrate output, dielectric raw-material costs, average multiband penetration, and regional 5G handset mix drive the base year. Forecasts to 2030 rely on multivariate regression blended with scenario analysis, with coefficients guided by primary-research consensus on IoT growth and ASP compression. Where supplier roll-ups were incomplete, weighted averages from proxy geographies bridged the gap.

Data Validation & Update Cycle

Model outputs undergo deviation checks against independent shipment trackers and customs flows before senior analyst sign-off. Our team refreshes the dataset annually, triggering interim revisions whenever policy shifts, major capacity additions, or material price shocks arise.

Why Mordor's Chip Antenna Baseline Commands Reliability

Published estimates frequently diverge because firms choose different antenna types, price stacks, and refresh cadences. We highlight below how such choices alter headline values.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.10 B (2025) | Mordor Intelligence | |

| USD 2.54 B (2024) | Regional Consultancy A | Relies on shipment proxies only, lacks price normalization by band count |

| USD 3.49 B (2025) | Industry Association B | Bundles multilayer PCB and coaxial antennas into the same pool |

| USD 1.83 B (2024) | Global Consultancy C | Focuses on consumer electronics, omits infrastructure and automotive demand |

Differences stem mainly from scope breadth, ASP assumptions, and update timetables. By aligning variables to clearly bounded chip-only revenues and refreshing every year, Mordor Intelligence delivers a balanced, traceable baseline that decision-makers can repeat and audit with confidence.

Key Questions Answered in the Report

What is the current value of the chip antenna market?

The chip antenna market size is USD 2.49 billion in 2026 and is forecast to reach USD 5.88 billion by 2031.

Which region leads the chip antenna market?

Asia Pacific holds the top position with 45.60% revenue share in 2025 and a projected 19.48% CAGR through 2031.

Why are LTCC antennas so dominant?

LTCC offers thermal stability and low loss at millimeter-wave frequencies, giving it 57.35% chip antenna market share in 2025, especially in automotive and high-frequency telecom equipment.

Which application segment is growing the fastest?

Which application segment is growing the fastest? GPS/GNSS applications are expanding at a 20.92% CAGR to 2031 as precise location services proliferate across automotive, drone, and precision-farming devices.

How does intellectual-property litigation affect suppliers?

Ongoing fractal-geometry patent disputes can delay product launches and elevate licensing costs, reducing supplier diversity and nudging prices upward for multi-band antenna designs.

What technological trend is reshaping smart appliances?

Wi-Fi 6E reference designs now mandate tri-band chip antennas, creating fresh demand for broadband ceramic parts that maintain low return loss across 2.4, 5, and 6 GHz bands.

Page last updated on: