5G Base Station Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

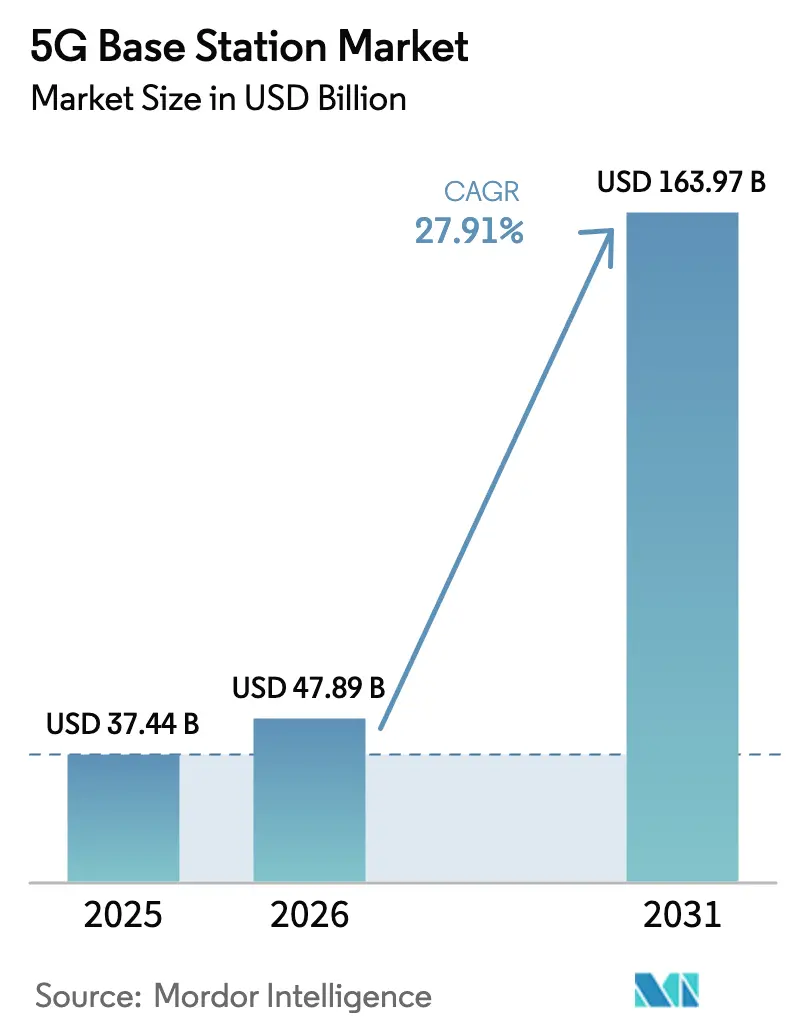

| Market Size (2026) | USD 47.89 Billion |

| Market Size (2031) | USD 163.97 Billion |

| Growth Rate (2026 - 2031) | 27.91% CAGR |

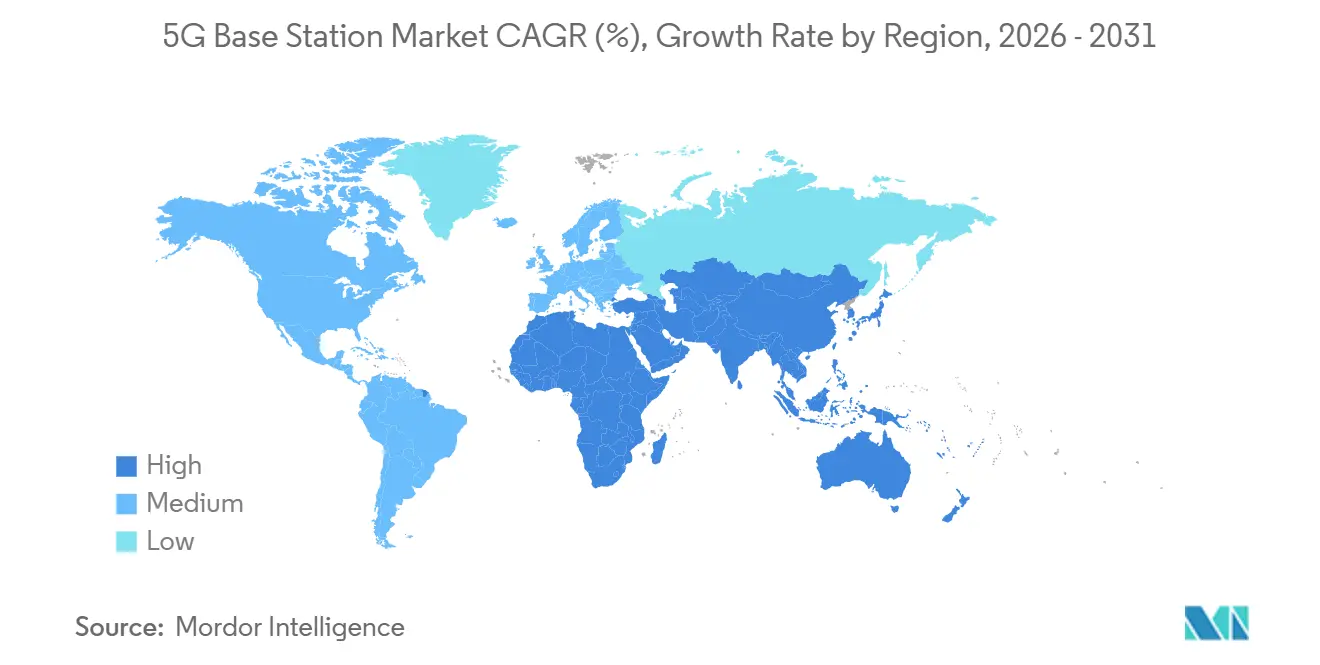

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

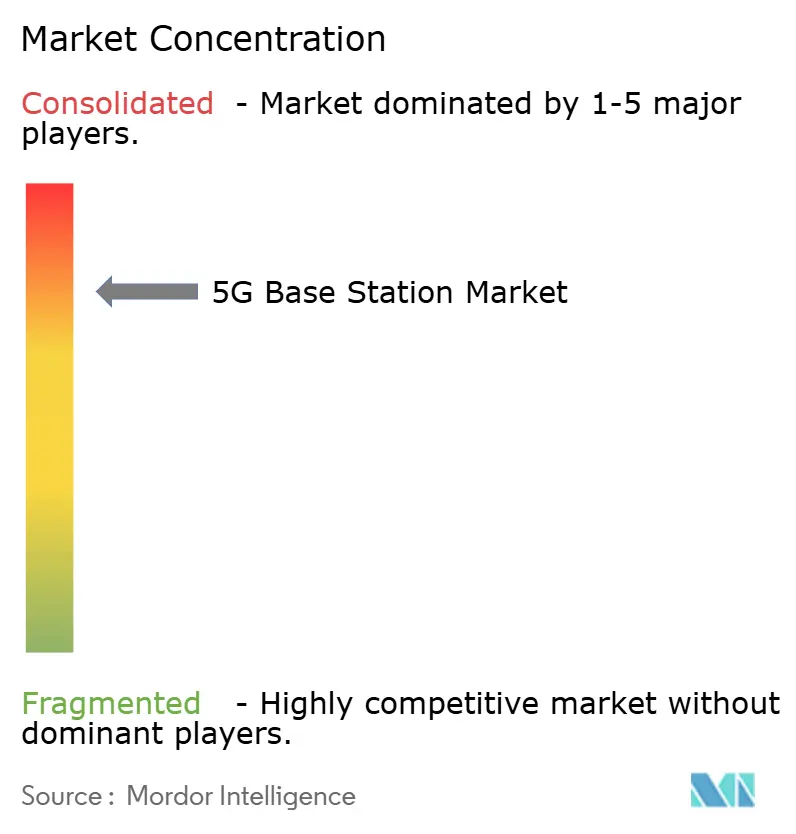

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G Base Station Market Analysis by Mordor Intelligence

The 5G base station market size is expected to grow from USD 37.44 billion in 2025 to USD 47.89 billion in 2026 and is forecast to reach USD 163.97 billion by 2031 at 27.91% CAGR over 2026-2031. Operators are prioritizing standalone architecture because it lowers per-gigabyte transmission costs and supports service differentiation. Small-cell densification, Open-RAN brownfield upgrades, and energy-efficient GaN power amplifiers are compressing deployment costs and shortening rollout timelines. Demand is also shifting toward high-power massive-MIMO radio units to meet escalating urban capacity requirements. Asia-Pacific, led by China and India, remains the volume anchor, while the Middle East records the fastest growth as sovereign wealth funds bankroll nationwide coverage. Competitive intensity is moderate: five vendors supply roughly three-quarters of global shipments, yet O-RAN interoperability is eroding entry barriers for specialist challengers.

Key Report Takeaways

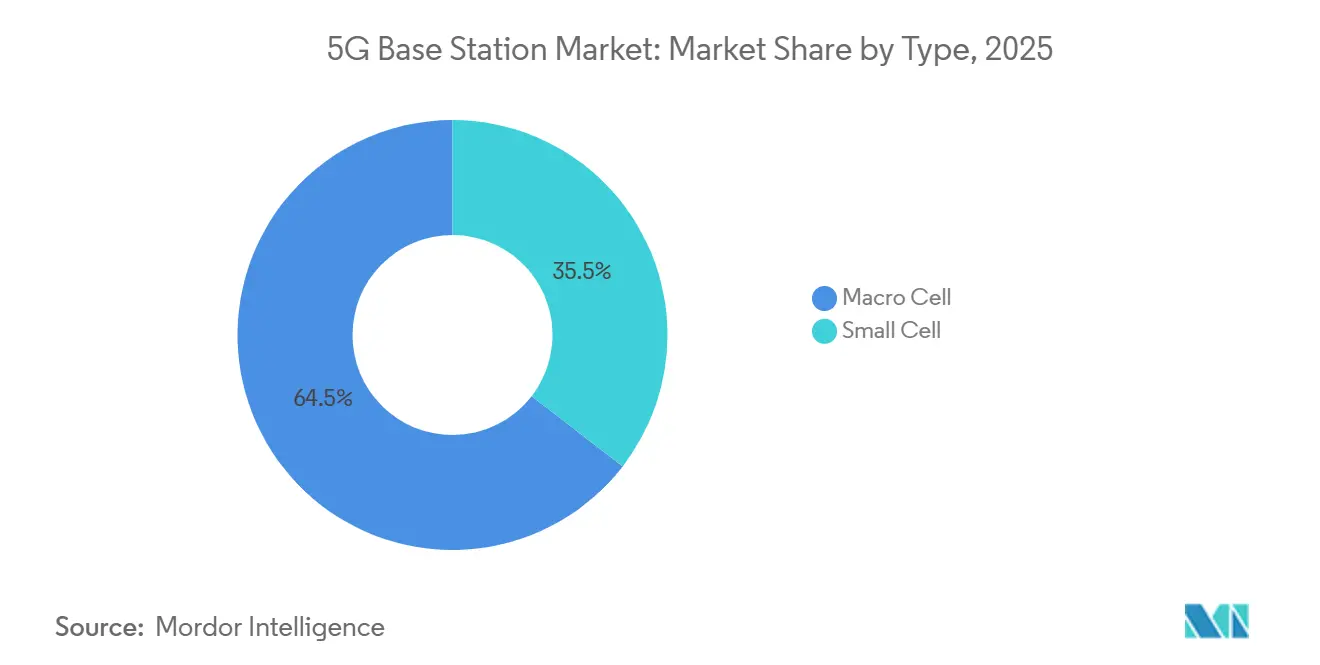

- By type, macro cell infrastructure led with 64.53% of 2025 revenue, while small cell deployments are projected to expand at a 28.34% CAGR through 2031.

- By architecture, non-standalone nodes accounted for 68.92% of 2025 installations; standalone configurations posted the fastest growth at a 28.37% CAGR.

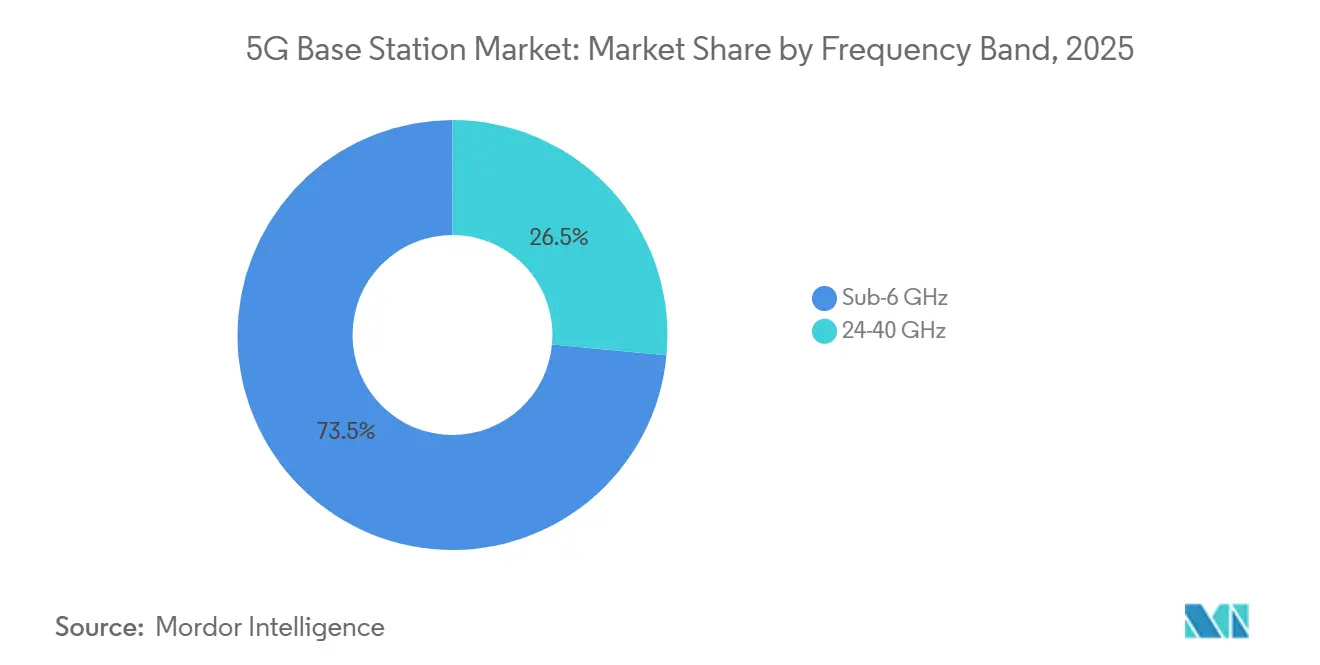

- By frequency band, sub-6 GHz accounted for 73.49% of 2025 deployments, whereas mmWave systems are forecast to rise at a 28.41% CAGR.

- By power rating, 10-40 W platforms captured 47.63% of 2025 shipments, while units above 40 W are increasing at a 28.61% CAGR.

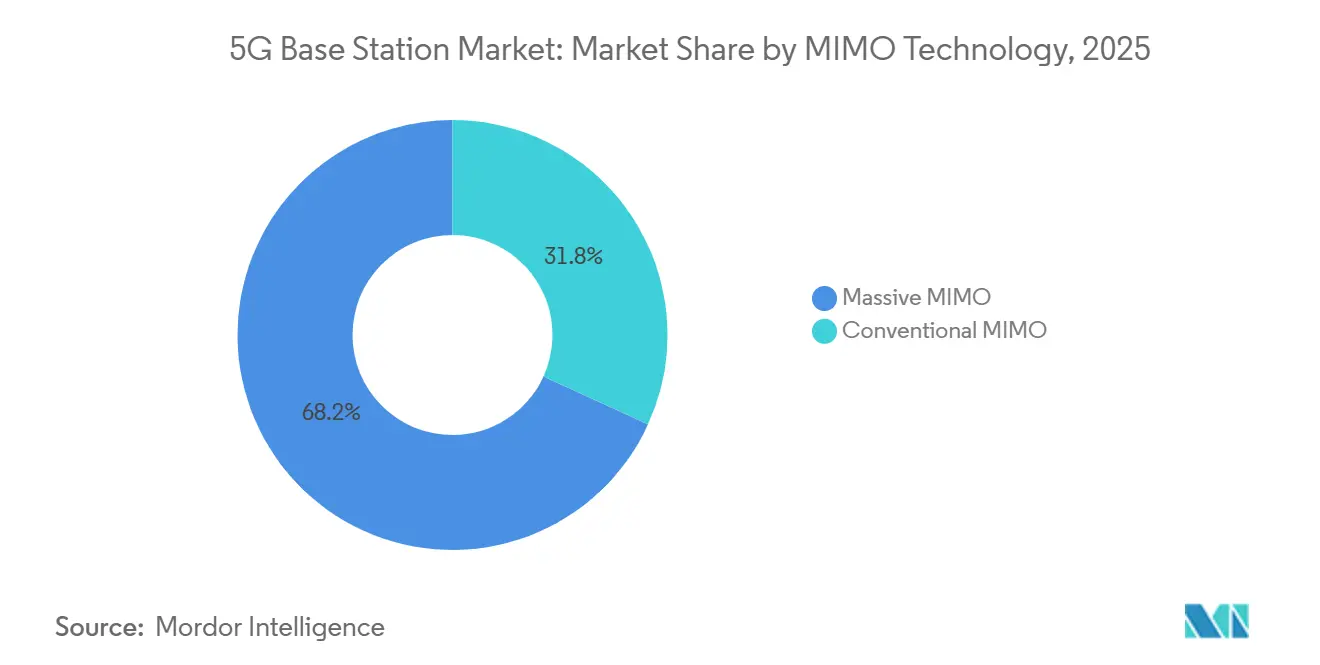

- By MIMO technology, massive MIMO accounted for 68.19% of 2025 deployments and is also the fastest-growing category, with a 28.44% CAGR.

- By end user, commercial mobile operators accounted for 72.34% of 2025 demand, while industrial private networks posted the fastest growth at a 29.11% CAGR.

- By geography, Asia-Pacific dominated with 56.74% of 2025 installations, whereas the Middle East is advancing at the highest 29.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 5G Base Station Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Mobile Data Traffic and Smartphone Penetration | +6.2% | Global, peak in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Superior Latency and Bandwidth Advantages of 5G | +5.8% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Government Spectrum Auctions and Infrastructure Stimulus | +5.1% | North America, Europe, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Open-RAN Driven Brown-Field Upgrade Cycle | +4.3% | North America and Europe with spillover to Asia-Pacific | Long term (≥ 4 years) |

| mmWave Small-Cell Roll-Outs for Private Industrial 5G | +3.9% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Energy-Efficient GaN PAs Cutting Total Site OPEX | +2.7% | Global, regulatory push in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Mobile Data Traffic and Smartphone Penetration

Global mobile data traffic surged to 120 exabytes per month in 2025 and is projected to more than double by 2031, forcing operators to add capacity quickly.[1]Ericsson, “Ericsson Mobility Report June 2025,” ericsson.com Smartphone ownership surpassed 78% of the population in 2025, but 5G-capable device adoption varies widely, creating staggered upgrade cycles across regions. In high-penetration markets, carriers monetize traffic through tiered enterprise SLAs, while in emerging economies, investment channels are directed toward macro cell coverage. The divergence concentrates capital in Asia-Pacific wide-area builds and North American small-cell densification. Rapid data growth, therefore, remains the primary engine of the 5G base station market.

Superior Latency and Bandwidth Advantages of 5G

Standalone 5G consistently delivers sub-10 ms latency, unlocking real-time industrial controls and autonomous vehicle coordination.[2]Nokia, “Industrial Automation Case Studies 2025,” nokia.com Urban macro cells now supply peak throughputs above 1 Gbps, yet the value skews toward premium enterprise and fixed-wireless users willing to pay for deterministic performance. Remote surgical trials achieved tactile feedback in 8 ms over standalone links, versus 45 ms over LTE, underscoring the qualitative leap in user experience. These performance gains justify aggressive densification and accelerate the expansion of the 5G base station market.

Government Spectrum Auctions and Infrastructure Stimulus

Between 2024 and 2025, regulators released more than 1,200 MHz of mid-band spectrum, generating USD 87 billion in proceeds now funneled into 5G rollouts.[3]Federal Communications Commission, “3.45 GHz Service Auction Fact Sheet,” fcc.gov India earmarked 30% of its auction revenues for rural broadband subsidies, de-risking carrier capex. Saudi Arabia formed a USD 6.4 billion fund in 2025 to drive 95% population coverage by 2028. These programs compress payback periods, lifting deployment velocity and bolstering the 5G base station market.

Open-RAN Driven Brownfield Upgrade Cycle

O-RAN specifications reduce multi-vendor integration costs by up to 35%, enabling operators to reuse towers, backhaul, and power assets. Vodafone’s 2,800-site upgrade trimmed per-site spend from USD 180,000 to USD 120,000 while improving energy efficiency by 18%. Dish Network demonstrated nationwide greenfield feasibility with Open RAN by mid-2025. The resulting cost arbitrage accelerates brownfield upgrades and intensifies competition, supporting long-run growth of the 5G base station market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and Long ROI Horizon | -4.8% | Global, acute in emerging markets with lower ARPU | Medium term (2-4 years) |

| Spectrum Fragmentation and Regulatory Delays | -3.2% | Global, particularly Europe and Asia-Pacific | Short term (≤ 2 years) |

| RF-Front-End Component Supply Bottlenecks | -2.6% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Sustainability Compliance Inflating Site Costs | -1.9% | Europe, emerging in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Long ROI Horizon

Standalone sites cost 60%-80% more than LTE equivalents, pushing payback to seven years for tier-1 operators. Verizon cited an average spend of USD 425,000 per C-band site in 2025, versus USD 240,000 for legacy LTE. Emerging-market ARPU below USD 2.50 hinders investment and widens the digital divide. Operators therefore triage capital toward dense urban clusters, slowing full-scale national rollouts and tempering the 5G base-station market’s growth curve.

Spectrum Fragmentation and Regulatory Delays

European states issued 19 different licensing frameworks across the 3.4-3.8 GHz band, forcing vendors into costly region-specific radio units. Installation permits averaged 9-14 months in major EU markets in 2025, compared with 4 months in the United States, delaying revenue realization. India’s postponement of the 6 GHz auction to late 2026 constrains mid-band capacity. These regulatory frictions extend deployment timelines, dampening near-term shipments in the 5G base station market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Small Cells Gain as Enterprises Bypass Carriers

Macro cell platforms retained 64.53% of the 2025 5G base station market share, confirming their central role in public carriers' wide-area coverage. At the same time, the small-cell slice of the 5G base station market is forecast to advance at a 28.34% CAGR through 2031 as private networks and urban densification accelerate. This divergence shows that the 5G base station market is tilting toward form factors capable of delivering deterministic latency in factories, stadiums, and transit hubs. Operators keep macro cells in rural and suburban grids because a single sub-6 GHz site can propagate three to five kilometers, minimizing tower leases and backhaul costs.

Enterprises, on the other hand, are installing pole- or ceiling-mounted radios priced well below tower gear, cutting real estate outlays by more than 90%. Integrated backhaul and edge compute shorten activation time from weeks to hours, making small cells the favored choice for Industry 4.0 projects within the 5G base station industry. Carriers also deploy curbside small cells in dense downtowns to relieve macro-sector congestion during peak traffic. As component prices fall, small cells will capture an expanding share of revenue, even as macro installations remain the volume cornerstone of the overall 5G base station market.

By Architecture: Standalone Migration Accelerates as Core Networks Mature

Non-standalone nodes accounted for 68.92% of 2025 installations, leveraging existing LTE cores to fast-track rollouts, yet standalone gear is projected to grow at a 28.37% CAGR. The cost advantage is decisive: fully cloud-native cores trim per-gigabyte delivery costs by 40%, enlarging the addressable 5G base station market size as traffic surges. Standalone sites also enable network-slicing service tiers, a feature that is already generating premium enterprise revenue streams for early adopters.

Migration speed hinges on virtualization readiness and handset support. In markets where 4G coverage is mature, operators are reallocating capex from radio overlays to core upgrades, accelerating the shift toward standalone 5G base stations. Rural operators still rely on non-standalone overlays to stretch limited budgets, but device makers are now shipping predominantly standalone-capable smartphones, collapsing the technology gap. By 2031, standalone sites will account for a majority of new deployments, reinforcing their strategic weight within the broader 5G base station industry.

By Frequency Band: Sub-6 GHz Dominates, mmWave Finds Industrial Niches

The Sub-6 GHz bands accounted for 73.49% of 2025 installations, reflecting their optimal blend of coverage radius and capacity. This dominance secures the largest share of the 5G base station market, while mmWave nodes are scaling at a 28.41% CAGR, driven by private factory networks and fixed-wireless alternatives to fiber. Operators in spectrum-scarce regions gravitate toward 3.3-3.8 GHz channels because each site can blanket multiple square kilometers, thereby maximizing 5G base-station market share linked to macro cells.

Industrial sites and dense venues flip the equation. A single mmWave small cell can deliver multi-gigabit throughput over distances of 100-200 meters, supporting autonomous robots, ultra-HD video analytics, and immersive reality. Falling radio prices and antenna-in-package integration further widen mmWave’s appeal, carving out a high-margin niche inside the 5G base station market. Even so, sub-6 GHz will remain the volume leader through 2031, ensuring balanced growth across the two frequency tiers.

By Power Rating: High-Power Units Surge with Massive-MIMO Arrays

Radio platforms rated 10-40 W captured 47.63% of 2025 shipments, anchoring mid-capacity suburban and urban sectors in the 5G base station market. Units above 40 W, however, are advancing at a 28.61% CAGR because massive-MIMO arrays need higher output to support 64-antenna beamforming and dense user clusters. The price premium on high-power radios lifts revenue faster than volume, enlarging the high-end slice of the 5G base station market.

Energy rules are simultaneously pushing vendors toward gallium-nitride power amplifiers that deliver more watts per square centimeter without breaching site limits. Operators in megacities now favor 80 W radios that double spectral efficiency while shrinking cabinet footprints by one-third. Below-10 W units persist in enterprise indoor grids and rural fixed-wireless access, where reach is secondary to low total cost. As networks densify, spend will increasingly flow to above-40 W gear, but the 10-40 W class will continue to serve as the backbone of the 5G base station industry.

By MIMO Technology: Massive MIMO Becomes the Urban Standard

Massive-MIMO systems accounted for 68.19% of 2025 deployments and are projected to grow at a 28.44% CAGR, underscoring their growing share in the 5G base station market. Field measurements show five-fold capacity gains in cells serving more than 100 concurrent users, making the economics compelling for urban operators. Early mover China Mobile alone activated 1.8 million massive-MIMO sites, underscoring the scale potential.

Component prices are falling as antenna-in-package techniques mature, lowering per-element costs by more than one-third year over year. This cost curve accelerates adoption beyond flagship cities and into high-traffic suburbs, broadening the massive-MIMO footprint in the 5G base station market. Conventional MIMO remains viable for rural corridors where user density is low and wide-area coverage is paramount. Yet the performance advantage means that massive MIMO is set to become the default for new capacity-driven builds across the wider 5G base-station industry.

By End User: Industrial Private Networks Outpace Carrier Deployments

Commercial mobile operators generated 72.34% of 2025 demand, reflecting their legacy footprint, but industrial private networks are climbing at a 29.11% CAGR, the fastest of any segment. Autonomous vehicles, machine-vision lines, and time-sensitive logistics demand sub-10 ms latency and data sovereignty, spurring factories, ports, and mines to finance their own infrastructure. This surge is opening a lucrative adjacency within the 5G base station market as equipment makers deliver ruggedized, explosion-proof radios and turnkey edge platforms.

Fixed-wireless access remains a secondary growth lever, especially in rural North America, where 5G can leapfrog cable and DSL. Government, defense, and smart-city agencies are also shifting spend toward standalone cores to guarantee mission-critical uptime. As enterprise use cases proliferate, industrial buyers will capture a larger share of the 5G base station market, even though public carriers continue to account for the bulk of installed sites. The result is a more diversified revenue mix that reinforces long-term expansion of the global 5G base station market.

Geography Analysis

In 2025, Asia-Pacific dominated with 56.74% of nodes, largely due to China's expansive 3.5 million-site network and India's ambitious USD 8.2 billion BharatNet Phase III backhaul initiative. This significant growth was driven by the region's focus on expanding connectivity and improving infrastructure to meet the rising demand for high-speed internet. By the close of 2025, 52% of mobile users in China were engaged, marking a pivotal shift in spending focus from mere coverage to enhanced capacity. This transition highlights the region's maturity in network development, as operators prioritize quality and efficiency. Meanwhile, Japan and South Korea took the lead, innovating with standalone cores and network slicing, and carving out premium service tiers. These advancements positioned the two countries as pioneers in next-generation network technologies, setting benchmarks for other markets to follow.

With a robust 29.94% CAGR, the Middle East emerges as the fastest-growing region, fueled by a hefty USD 15 billion in commitments from sovereign funds. This growth reflects the region's strategic investments in digital transformation and infrastructure development. Eyeing a 2028 deadline, Saudi Arabia, backed by a USD 6.4 billion fund, aims for an ambitious 95% population coverage. This initiative underscores the country's commitment to bridging the digital divide and enhancing connectivity for its population. In a move to fast-track its smart-city ambitions, the UAE, in 2025, set aside 300 MHz of new spectrum, propelling standalone rollouts. This allocation is expected to accelerate the adoption of advanced technologies, supporting the region's vision for sustainable and technologically advanced urban centers.

North America leads the charge, propelled by C-band deployments and initiatives for rural fixed-wireless programs. The FCC’s 100 MHz mid-band auction raised USD 21.8 billion that carriers must light up before build-out deadlines. Europe prioritizes Open-RAN retrofits and energy efficiency to meet the EU Energy Efficiency Directive, recording 18% energy savings in Vodafone’s 5,800-site trial. South America and Africa remain early-stage, though Brazil and South Africa pilot private 5G in mining and agriculture.

Competitive Landscape

In 2025, five key players - Huawei, Ericsson, Nokia, ZTE, and Samsung - dominated the global 5G base station market, collectively accounting for around 75% of shipments. While Huawei and ZTE held sway in the Asia-Pacific region, adhering to domestic content regulations, Ericsson and Nokia established their leadership in Europe and North America. Notably, Samsung carved out a 12% share in North America's Open-RAN segment, undercutting competitors by pricing its offerings 20% lower.

Competition is intensifying with strategic maneuvers. Ericsson's acquisition of Vonage aims to integrate network APIs with its radio offerings, while Nokia's collaboration with Microsoft Azure focuses on edge-compute co-location. The landscape is further highlighted by a 38% surge in patent filings for massive-MIMO algorithms in 2025, with Qualcomm, Ericsson, and Huawei collectively securing 62% of the Release-17 grants.

With 47 products achieving Open-RAN certification in 2025, switching costs have diminished, paving the way for newcomers like Mavenir and JMA Wireless to carve out niches in private networks. Sustainability is emerging as a key differentiator: Ericsson's 2025 radio models boast a 30% reduction in energy consumption compared to their 2023 counterparts, aiding operators in aligning with EU carbon objectives. Consequently, the competitive landscape is evolving, with a pronounced shift from mere capex pricing to a broader consideration of the total lifetime cost of ownership.

5G Base Station Industry Leaders

Huawei Technologies Co. Ltd

ZTE Corporation

Nokia Corporation

Telefonaktiebolaget LM Ericsson

Qorvo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ericsson won a USD 1.2 billion contract to supply 150,000 5G base stations for Bharti Airtel’s BharatNet Phase III expansion.

- January 2026: SK Telecom launched commercial network slicing with 5 ms latency and 99.999% uptime for industrial clients.

- December 2025: Nokia finished installing 2,800 Open-RAN sites for Vodafone in the UK and Germany, cutting energy use 18%.

- November 2025: Huawei shipped 1.2 million GaN-based radios and budgeted USD 800 million for 6G R&D.

Global 5G Base Station Market Report Scope

The 5G Base Station Market Report is Segmented by Type (Small Cell, and Macro Cell), Architecture (Stand-Alone, and Non-Stand-Alone), Frequency Band (Sub-6 GHz, and 24-40 GHz), Power Rating (Below 10 W, 10-40 W, Above 40 W), MIMO Technology (Conventional MIMO, and Massive MIMO), End User (Commercial Mobile Operators, Residential/Consumer FWA, Industrial Private Networks, Government and Defense, Smart Cities and Public Safety, Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Small Cell |

| Macro Cell |

| Stand-Alone |

| Non-Stand-Alone |

| Sub-6 GHz |

| 24-40 GHz |

| Below 10 W |

| 10-40 W |

| Above 40 W |

| Conventional MIMO |

| Massive MIMO |

| Commercial Mobile Operators |

| Residential/Consumer FWA |

| Industrial Private Networks |

| Government and Defense |

| Smart Cities and Public Safety |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Small Cell | ||

| Macro Cell | |||

| By Architecture | Stand-Alone | ||

| Non-Stand-Alone | |||

| By Frequency Band | Sub-6 GHz | ||

| 24-40 GHz | |||

| By Power Rating | Below 10 W | ||

| 10-40 W | |||

| Above 40 W | |||

| By MIMO Technology | Conventional MIMO | ||

| Massive MIMO | |||

| By End User | Commercial Mobile Operators | ||

| Residential/Consumer FWA | |||

| Industrial Private Networks | |||

| Government and Defense | |||

| Smart Cities and Public Safety | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the global 5G base station market in value terms today?

The 5G base station market size stands at USD 47.89 billion in 2026 and is set to reach USD 163.97 billion by 2031.

Which deployment architecture is growing fastest?

Standalone 5G base stations post the highest growth, advancing at a 28.37% CAGR as operators complete cloud-native core upgrades.

Why are small cells gaining traction over macro cells?

Enterprises favor small cells for private 5G because installation costs are lower and deterministic latency is easier to guarantee, driving a 28.34% CAGR for this segment.

Which region delivers the strongest growth outlook?

The Middle East leads with a 29.94% CAGR through 2031, supported by multi-billion-dollar sovereign infrastructure programs.

What is driving industrial adoption of private 5G networks?

Demands for sub-10 ms latency, data sovereignty, and automation resilience are pushing manufacturers, ports, and mines to invest directly in private 5G rather than rely on public carriers.

Page last updated on: