Antenna Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.22 Billion |

| Market Size (2031) | USD 39.18 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

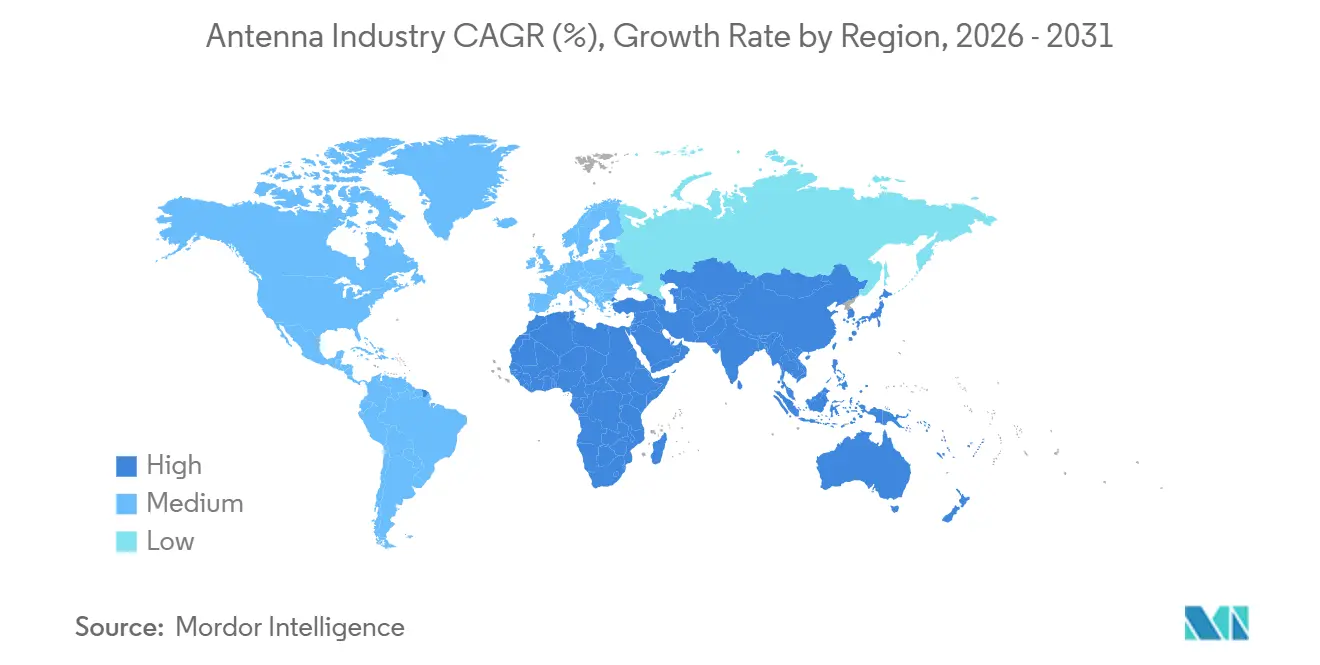

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

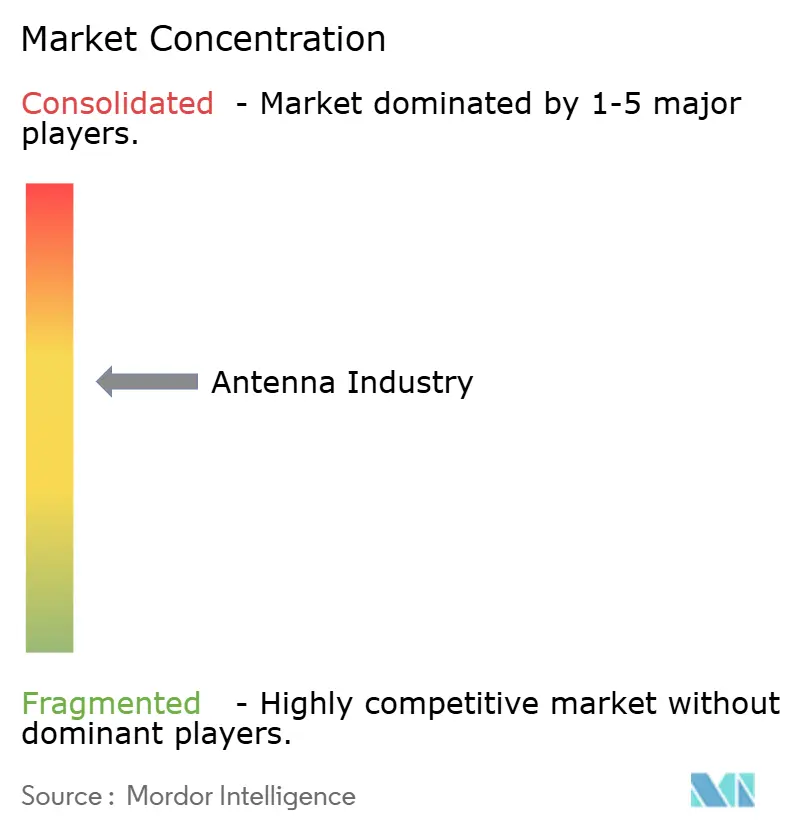

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antenna Market Analysis by Mordor Intelligence

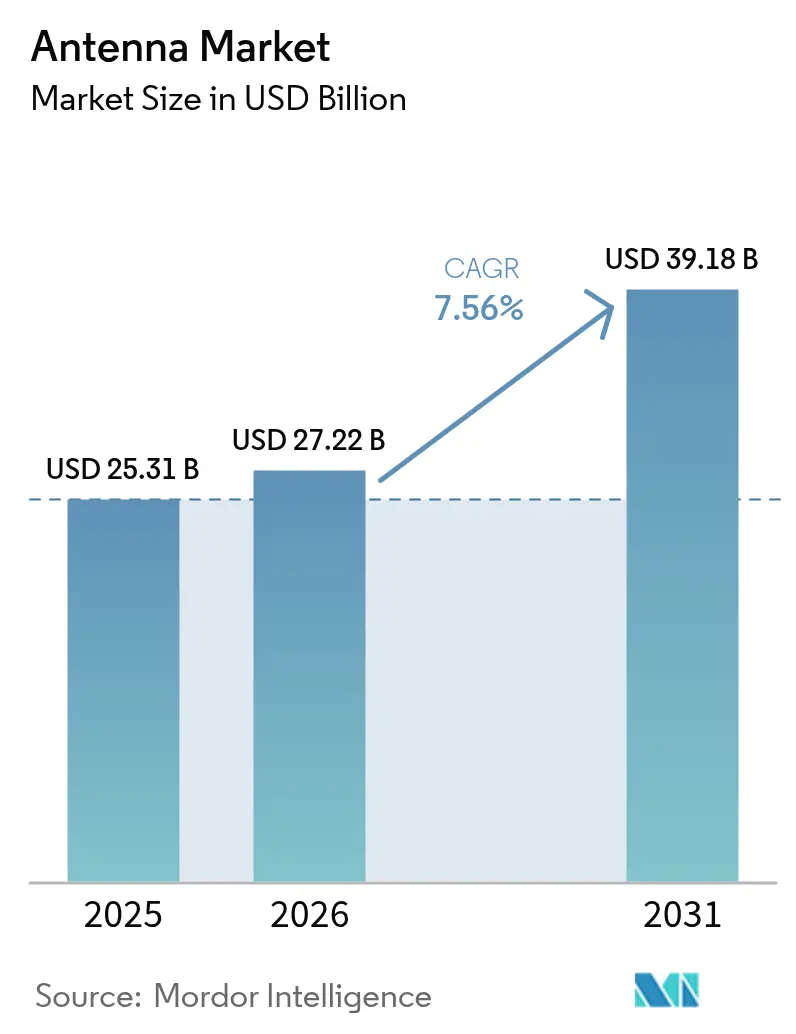

The antenna market size is expected to grow from USD 25.31 billion in 2025 to USD 27.22 billion in 2026 and is forecast to reach USD 39.18 billion by 2031 at 7.56% CAGR over 2026-2031. Demand is migrating from single-band passive radiators toward tightly integrated multi-band assemblies that accommodate 5 G millimeter-wave, non-terrestrial satellite, and vehicle-to-everything links within the same footprint. Device makers are wrestling with higher bill-of-materials costs for phased-array and massive multiple-input multiple-output structures even as consumer margins tighten, so vendors capable of shipping antenna-in-package modules at scale are widening their pricing advantage. Asia Pacific dominates new base-station deployments, while North American and European operators upgrade to 5 G standalone cores, boosting orders for active panels, small cells, and infrastructure-grade remote radio heads. Automotive connectivity rules in the United States and European Union are adding multi-port roof modules to every new car, further enlarging the addressable antenna market across the mobility, telematics, and advanced driver-assistance ecosystems.

Key Report Takeaways

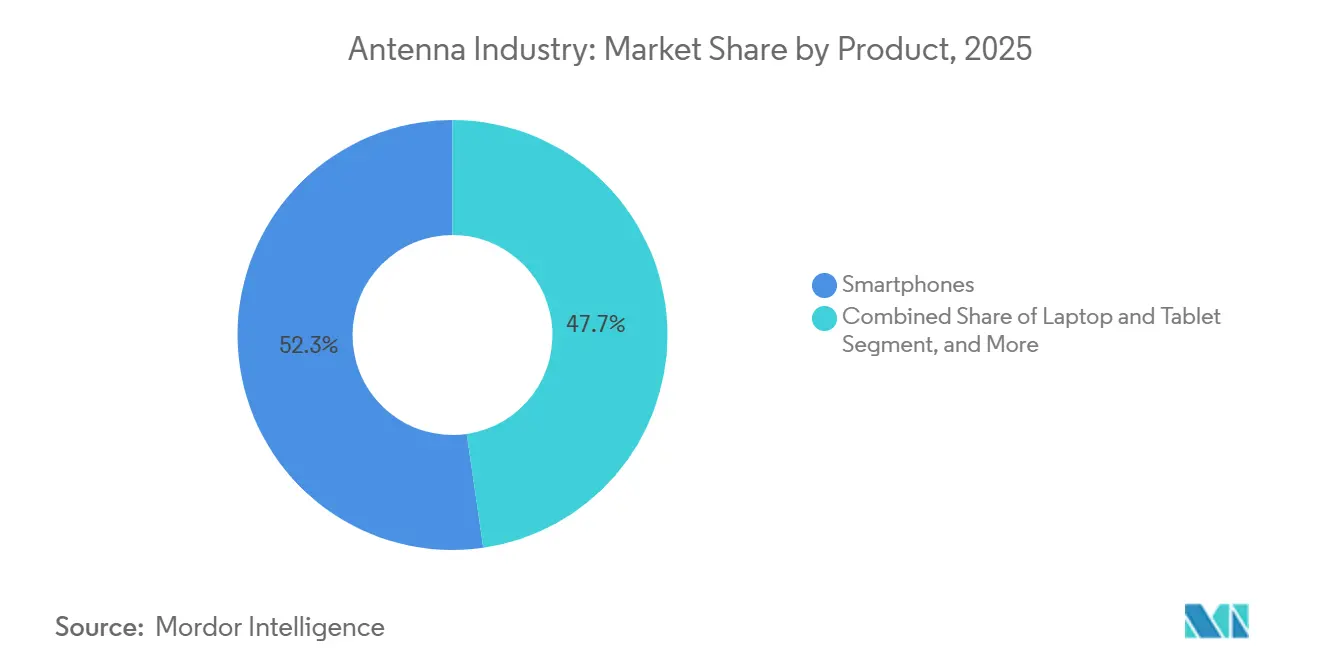

- By product category, smartphones led with 52.28% of antenna market share in 2025, while wearables and hearables are projected to record a 7.70% CAGR through 2031.

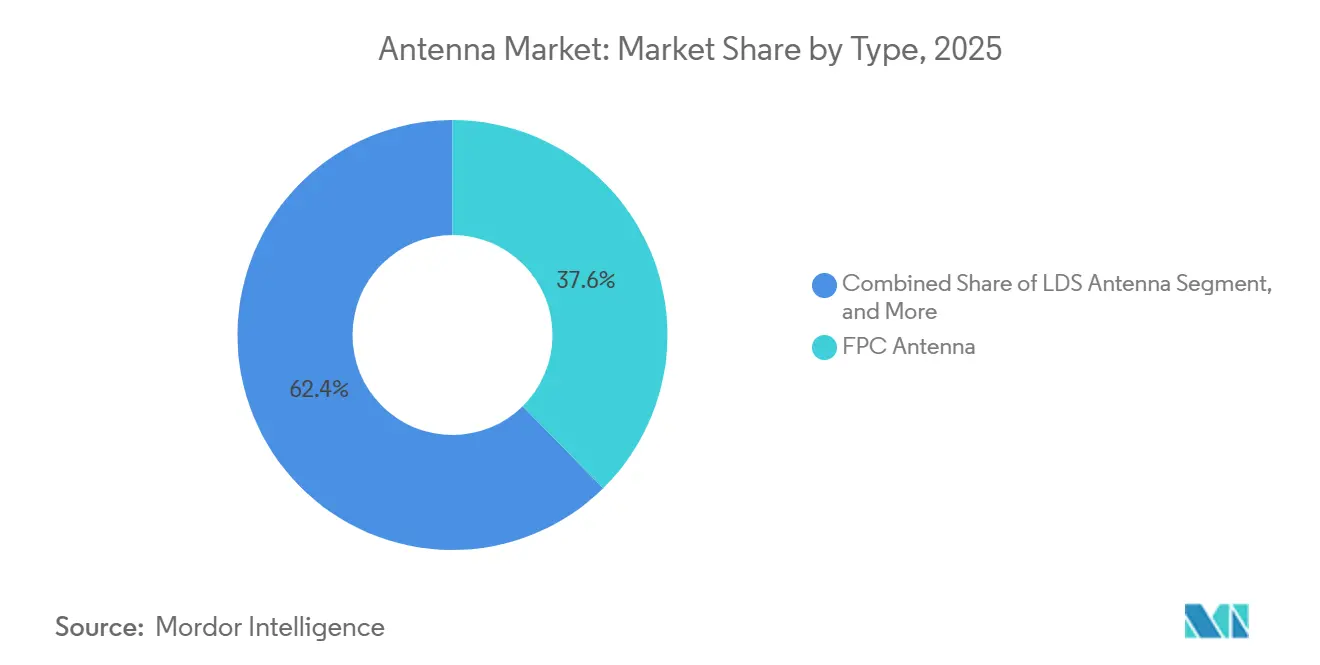

- By type, flexible printed-circuit antennas captured 37.63% of shipments in 2025; liquid-crystal polymer variants are forecast to advance at 7.59% CAGR over the same period.

- By technology, antenna-in-package modules held 35.82% share of the antenna market size in 2025, whereas antenna-on-chip integration is projected to expand at 7.66% CAGR between 2026-2031.

- By frequency, the 1-6 GHz slice accounted for 42.48% of revenue in 2025, but bands above 30 GHz are poised to grow at 7.61% CAGR.

- By application, main cellular links generated 45.91% of demand in 2025, yet GNSS antennas are on track for a 7.73% CAGR, propelled by driver-assistance targets.

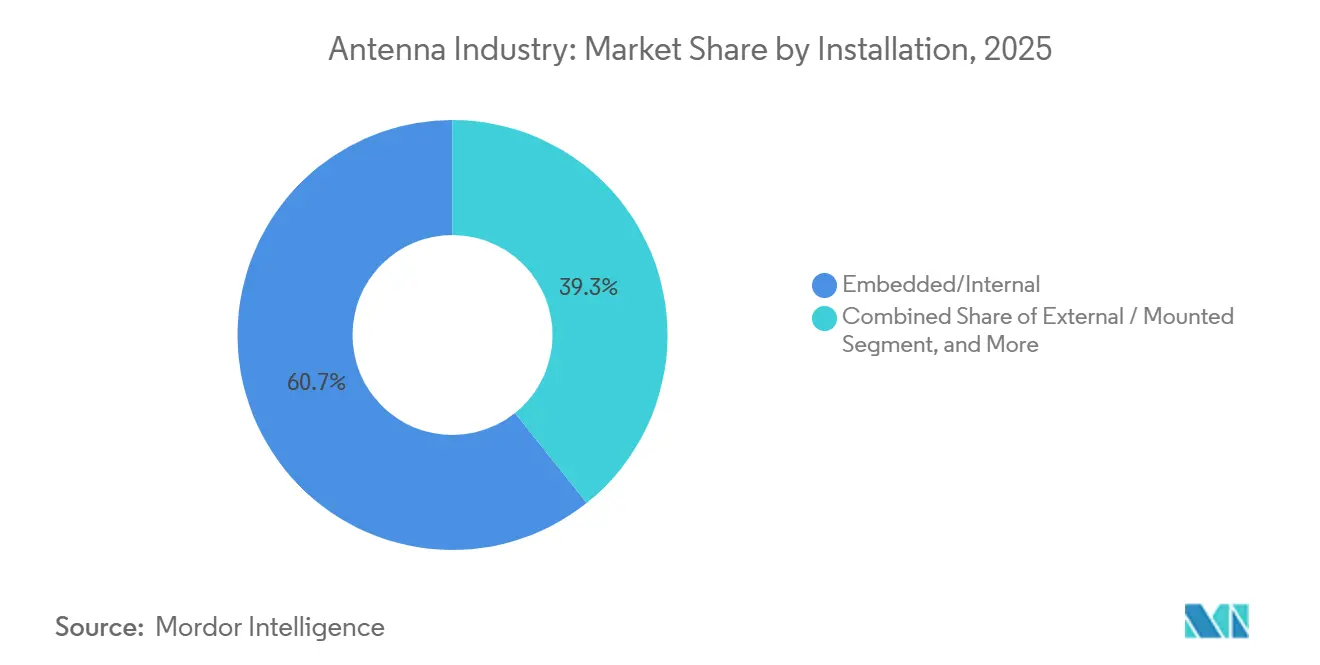

- By installation, embedded and internal configurations represented 60.73% of 2025 volumes and are projected to advance at 7.79% CAGR, outpacing external mounts.

- By end-user industry, automotive and mobility is set for the fastest climb, rising at 7.84% CAGR as vehicle-to-everything adoption accelerates.

- By geography, Asia-Pacific represented 47.71% in 2025 and Middle East and Africa is forecast to register the fastest 7.63% CAGR through 2031.the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antenna Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 5G and mmWave Rollouts Requiring High-Density Active Antennas | +1.8% | Global, with concentration in North America, Europe, and Asia Pacific urban centers | Medium term (2-4 years) |

| Proliferation of IoT Endpoints Driving Multi-Band, Ultra-Compact Designs | +1.4% | Global, particularly Asia Pacific manufacturing hubs and North America smart-city deployments | Long term (≥ 4 years) |

| Automotive V2X Mandates in US and EU Boosting Multi-Port Vehicular Antennas | +1.2% | North America and Europe, with spillover to Asia Pacific automotive export markets | Short term (≤ 2 years) |

| Defense Demand for Rugged Phased-Array and Conformal Antennas | +0.9% | North America and Europe defense procurement, with selective Middle East adoption | Long term (≥ 4 years) |

| Satellite Flat-Panel Growth for Mobility and Non-Terrestrial Networks | +0.8% | Global, with early traction in North America maritime and aviation sectors | Medium term (2-4 years) |

| Flexible and Wearable Antennas for Healthcare and Consumer AR Devices | +0.7% | North America and Europe healthcare markets, Asia Pacific consumer electronics manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in 5 G and mmWave Rollouts Requiring High-Density Active Antennas

Mobile operators are moving from passive distributed systems to self-contained active panels that embed radios, beamforming logic, and power amplification, slashing feeder-cable losses and unlocking dynamic spectrum sharing. A 64-element phased-array inside a ten-centimeter aperture now delivers sub-degree beam steering at 26-28 GHz, enabling compact urban micro-cells that recoup spectrum investments faster. China reported 2.4 million live 5 G macro sites by the close of 2024 and targets 3.5 million during 2025, keeping active-antenna order books full even as handset penetration plateaus.[1]Reuters Staff, “China 5 G Base Station Targets,” Reuters, reuters.com Thermal loads of 150-200 W per panel demand liquid or advanced heat-pipe cooling, nudging unit prices upward, yet operators accept the premium because spectral efficiency rises sharply once beamforming is deployed. Compliance checks for electromagnetic exposure above 24 GHz add planning delays, particularly across European jurisdictions that apply stricter field-strength limits than North American rules.

Proliferation of IoT Endpoints Driving Multi-Band, Ultra-Compact Designs

Asset trackers, smart meters, and environmental sensors increasingly pack four or more radios, forcing antenna footprints smaller than 50 cm³ to cover sub-1 GHz, 2.4 GHz, 5 GHz, and sometimes 6 GHz. Research has demonstrated MEMS-switched architectures that hop between bands while keeping isolation better than 25 dB, boosting battery life by up to 40% compared with fixed-band units.[2]IEEE Staff, “Reconfigurable Antennas for IoT Nodes,” IEEE Transactions on Antennas and Propagation, ieee.org Substrates that embed passive filters and matching networks inside the ceramic stack free 30% of board real estate and trim material costs around 15%. Singapore and Barcelona codified multi-band antennas into municipal procurement specs, creating templates that other smart-city projects replicate. Ultra-compact radiators inevitably suffer narrower bandwidth and lower efficiency, so design handbooks now devote entire chapters to impedance tuning in millimeter-scale layouts.[3]Johanson Technology Engineers, “Chip Antenna Design Handbook,” Johanson Technology, johansontechnology.com

Automotive V2X Mandates in US and EU Boosting Multi-Port Vehicular Antennas

Finalized U.S. rules allocate the 5.9 GHz slice for cellular vehicle-to-everything, requiring carmakers to pair 5 G NR modems with roof-mounted radiators that also accommodate satellite and Wi-Fi links. The European eCall statute demands GNSS accuracy better than 5 m, pushing multi-frequency L1 + L5 antennas into every new passenger model. SAE guidance limits gain variation across azimuth to less than 3 dB, effectively banning windshield-embedded solutions and driving demand for shark-fin modules. Latency targets below 20 ms force bandwidth wider than 10 MHz, eliminating narrowband monopoles and favoring wideband planar inverted-F or patch arrays. As a result, antenna content per vehicle is projected to almost double across the decade.

Defense Demand for Rugged Phased-Array and Conformal Antennas

Armed forces are replacing mechanical dishes with electronically scanned arrays that shift beams in microseconds, a prerequisite for tracking hypersonic threats and maintaining satellite links during high-G turns. U.S. Navy awards support conformal arrays that hug curved airframes, cutting radar cross-section while preserving ±60-degree scan coverage. NASA prototypes on polyimide survive −150 °C to +120 °C swings, clearing harsh-environment hurdles for small-sat constellations. Qualification cycles under MIL-STD-810 and MIL-STD-461 span 18+ months, shielding incumbents but rewarding newcomers able to compress testing through additive manufacturing. Price premiums remain steep—often 10-50× commercial equivalents—yet volumes climb as unmanned platforms proliferate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising RF Front-End Power-Efficiency Constraints at mmWave | -0.9% | Global, with acute impact in North America and Europe smartphone markets | Short term (≤ 2 years) |

| Supply-Chain Concentration in East Asia Creating Geopolitical Risk | -0.7% | Global, particularly affecting North America and Europe original equipment manufacturers | Medium term (2-4 years) |

| Environmental Regulations on Fluorinated Antenna Substrates | -0.5% | Europe and North America, with potential spillover to Asia Pacific export-oriented manufacturers | Long term (≥ 4 years) |

| Competition from Integrated Chip-Antenna Modules Reducing Discrete Demand | -0.6% | Global, with strongest effect in consumer electronics and wearables segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising RF Front-End Power-Efficiency Constraints at mmWave

Continuous millimeter-wave streaming drains a handset battery in roughly four hours because each spatial stream consumes 2-3 W at 28 GHz. Hybrid RF-mmWave architectures that down-shift to sub-6 GHz save 35% energy but require dual antenna chains and 20% more board area. Gallium-nitride amplifiers raise efficiency for infrastructure yet remain too costly for handsets, and glass or silicon interposers that slash insertion loss command a 3-4× materials premium. This economics gap limits consumer adoption of mmWave antennas outside fixed-wireless and hotspot devices.

Supply-Chain Concentration in East Asia Creating Geopolitical Risk

Roughly 70% of flexible printed-circuit antennas and 85% of liquid-crystal polymer substrates ship from China, Japan, South Korea, and Taiwan. Trade controls placed several Chinese suppliers on the U.S. Entity List, delaying automotive launches by up to nine months and forcing Western brands to carry bigger safety stocks. Reshoring faces steep labor and skills hurdles, and European semiconductor funding still sidesteps antenna assembly, leaving regional gaps unaddressed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Liquid-Crystal Polymer Substrates Gain Share in Premium Tiers

Liquid-crystal polymer substrates held 37.63% of antenna market share in 2025 and are set for the fastest 7.59% CAGR because flagship phones now demand dielectric constants below 3.0 for efficient 30-plus GHz radiation. Flexible printed-circuit designs remain entrenched in mid-range devices thanks to lower tooling outlay, but their thermal stability falters beyond 85 °C, pushing OEMs toward hybrid stacks that laminate thin liquid-crystal polymer films onto polyimide cores. Stamped metal antennas keep traction in cars and industrial controls where crashworthiness outweighs cost, while laser direct-structured modules shave 30% assembly steps in wearables by eliminating separate boards. Institute of Electrical and Electronics Engineers measurements show liquid-crystal polymer inserts yield 0.3 dB less path loss at 28 GHz, translating into 7% higher effective radiated power and justifying a 20-25% materials premium. Tooling vendors are re-calibrating die-sets for metal-polymer combinations that survive minus 40 °C to plus 125 °C automotive cycles, broadening their market beyond smartphones.

Across 2026-2031, flexible printed-circuit specialists are diversifying into matte-black solder-mask finishes that mitigate display glare in foldables, while liquid-crystal polymer pioneers court base-station suppliers seeking low-loss 38-40 GHz backhaul links. Stamped antennas pick up momentum as vehicles adopt multi-gigabit Ethernet loops requiring shielded housings, and laser direct structuring scales into consumer augmented-reality eyewear where every gram counts. Emergent meta-polymer and molded-interconnect devices stay niche, but defense primes test them for conformal radomes. Overall, liquid-crystal polymer has become the performance benchmark, and its uptake re-weights raw-material procurement across the entire antenna market.

By Technology: Antenna-on-Chip Integration Accelerates in Wearables

Antenna-in-package captured 35.82% share of the antenna market size in 2025 by moving radiators onto ceramic or glass carriers attached to the transceiver die. The next leap is antenna-on-chip, projected to surge 7.66% CAGR as foundries leverage redistribution layers and through-silicon vias to print emitters directly on silicon. Wearables, hearing aids, and implantables embrace this path because it removes coax traces, cuts insertion loss, and trims thickness below 0.8 mm, unlocking sleeker industrial designs. Active antenna systems that co-package amplifiers and phase shifters dominate base-station upgrades, while printed-flexible formats continue as the cost floor for mass-market accessories.

Between 2026 and 2031, printed-flexible suppliers differentiate through rapid iteration cycles, whereas antenna-in-package houses standardize modules for Wi-Fi 7 and 60 GHz unlicensed backhaul. Phased-array panels migrate from defense into automotive radar, and antenna-on-chip prototypes hit 4 dB realized gain in 2 mm² footprints, enough for medical patches transmitting telemetry through flesh. Glass interposers support sub-half-wavelength element spacing above 30 GHz, enabling 120° beam steering without grating lobes and lighting a clear route for premium phones and tablets.

By Frequency Range: Millimeter-Wave Segment Gains Momentum

Sub-6 GHz still brings 42.48% of 2025 revenue because it backs LTE, Wi-Fi 6E, and early 5 G NR, but frequencies above 30 GHz will grow at 7.61% CAGR as urban densification unlocks new spectrum. The math is punishing: path loss rises with the square of frequency, so 28 GHz links shed 28 dB more than 2.4 GHz over the same span. Phased arrays with 256 elements claw back 24 dB beamforming gain, sustaining 200-300 m cell radii on city streets. Regulators plan to triple usable spectrum for 6 G, forcing antenna designers to stretch fractional bandwidth past 30% across Ku-, Ka-, and even D-band windows.

Millimeter-wave uptake is strongest in fixed-wireless hubs, train stations, stadiums, and airport hot zones. Sub-1 GHz retains relevance for IoT meters that value range over data rate, while 6-30 GHz slots fuel satellite terminals and dedicated backhaul. Compliance with international coordination rules for frequencies above 24 GHz remains the pacing item; clearance procedures can stall citywide rollouts by 12-18 months, prompting equipment makers to pre-certify modular arrays that swap feeds as licenses clear.

By Product: Wearables Drive the Miniaturization Frontier

Smartphones led the antenna market with 52.28% share in 2025 and continue to add ports for 4×4 MIMO, ultra-wideband, and millimeter-wave. Wearables and hearables, however, will post the fastest 7.70% CAGR; their footprints shrink below 10 cm³ yet must radiate Bluetooth Low Energy, GNSS, and sometimes cellular links reliably through human tissue. Silver-nanowire traces on polyimide maintain resonance despite 5 mm bends, resolving early detuning issues in smartwatches. Laptops and tablets adopt extra antennas for 6 GHz Wi-Fi, but metal chassis enforce placement in display bezels, crimping efficiency. Routers and access points escape size limits, so external dipoles that add 5-8 dB gain extend coverage 40-60%, a key selling point to home-office buyers.

Looking ahead, augmented-reality headsets will require co-located 60 GHz and 6 GHz antennas for high-bandwidth video plus control channels, accelerating research into multi-layer printed structures. Smartphones migrate from four to six or eight antennas, lifting bill-of-materials by USD 2-3 each but promising double-digit throughput lifts. Wearable suppliers co-design battery, radio, and enclosure early in the cycle to minimise electromagnetic coupling, giving antenna engineers a permanent seat at the product architecture table.

By Application: GNSS Antennas Surge with ADAS Adoption

Cellular links accounted for 45.91% of 2025 demand, yet GNSS antennas will outpace the field at 7.73% CAGR as affordable dual-frequency receivers push positional accuracy toward sub-meter. Automotive lane-centering algorithms rely on simultaneous L1 and L5 reception that mitigates ionospheric errors, delivering precise localization without roadside beacons. Bluetooth Low Energy radiators become chip-scale, enabling disposable medical patches, while Wi-Fi antennas stretch from 2.4 GHz to 7.125 GHz, a 45% bandwidth jump that demands log-periodic or tapered-slot layouts. NFC coils stay key for payments, but their resonance at 13.56 MHz hinges on high Q rather than far-field gain, so designers focus on loop inductance and shielding.

From 2026 onward, GNSS modules standardize multi-constellation reception, and cellular front ends adapt dynamic spectrum sharing, letting one antenna swing from 4 G to 5 G without RF relays. Wi-Fi 7 drafts introduce 320 MHz channels demanding even wider fractal geometries, while Bluetooth smart beacons carry direction-finding antennas that offer sub-meter indoor location, blurring use-case lines between short-range and satellite navigation.

By Installation: Embedded Designs Dominate IoT Nodes

Embedded and internal radiators formed 60.73% of 2025 shipments and will climb at 7.79% CAGR because aesthetic, vandal-proof housings matter in consumer and industrial IoT. Internal smartphone antennas typically post −3 dB to −5 dB realized gain because of ground-plane coupling, yet PCB layout tricks recover bandwidth for 5 G NR bands. External vehicle antennas gain 7-10 dB advantage, doubling effective range, but must clear specific absorption rate thresholds for occupants in convertibles and motorcycles. Infrastructure panels migrate from passive 8-port to active 64-port arrays, adding 40-60 kg to tower loads, forcing operators to budget reinforcing brackets.

As smart-city lamppost sensors multiply, rugged epoxy-potted PCB antennas brave −40 °C winters and tropical downpours, blending RF, power, and edge compute under one seal. Mounted configurations remain vital in marine, aviation, and rail where radomes protect high-gain patches from airflow and salt fog, yet falling prices for conformal embedded panels will nibble at legacy whip and dome volumes by decade-end.

By End-User Industry: Automotive Leads the Growth Trajectory

Consumer electronics consumed 48.64% of antenna market revenue in 2025 but is maturing, while automotive and mobility is projected to rise 7.84% CAGR as every new vehicle integrates cellular, Wi-Fi, GNSS, and vehicle-to-everything in rooftop modules. Average antenna count per car is on course to jump from eight devices in 2024 to fourteen by 2030, fed by ultra-wideband keys, 77 GHz radar, and 60 GHz cabin monitoring. SAE isolation rules force 20 dB separation between cellular and vehicle-to-everything channels, driving OEMs to redesign roofs for spatial diversity.

Defense volumes remain smaller but each phased-array commands a 10-50× price premium over commercial units, and military buyers are certifying additive-manufactured conformal apertures that shave months off prototyping. Remote patient monitors, drug-delivery pumps, and implantables grow the healthcare slice, but strict IEC 60601 emissions caps limit peak power, steering designers toward higher-efficiency radiators. In smart factories, private 5 G deployments demand IP65-rated antennas rated for −40 °C to +85 °C, opening a parallel industrial IoT channel for suppliers fluent in harsh-environment qualification.

Geography Analysis

Asia Pacific retained 47.71% of antenna market share in 2025 thanks to China’s 2.4 million live 5 G sites and a 3.5 million target by end-2025, a build-out that funnels continuous orders for remote radio heads and active antenna units. Japan’s operators completed nationwide 5 G coverage in 2025 and pivoted to small-cell densification in Tokyo, Osaka, and Nagoya, rolling out palm-sized antenna-in-package modules that tuck into street furniture. South Korea allocated KRW 625 billion (USD 470 million) for 6 G research consortia in 2025, mandating terahertz demo links by 2027 to seed next-decade opportunities. India’s USD 19 billion spectrum auction in 2024 unlocked 5 G service across 150 cities in 2025, spurring bulk orders for consumer and fixed-wireless antennas as operators chase urban middle-class subscribers. Concentrated manufacturing gives regional vendors a 15-20% cost edge, reinforcing Asia Pacific’s leadership even as Western buyers seek alternative sources.

Middle East and Africa is forecast to register the fastest 7.63% CAGR through 2031. Saudi Telecom’s SAR 12 billion (USD 3.2 billion) expansion aims for 95% 5 G population coverage by 2027, emphasizing active units that swap spectrum between 4 G and 5 G users. The United Arab Emirates mandates fiber or fixed-wireless in all new builds, pulling rooftop antennas into residential layouts. South Africa’s long-delayed 700 MHz and 3.5 GHz allocations in 2024 cleared the way for rural 5 G rollouts, while Israel’s aerospace exports keep advanced phased-array demand steady. Currency swings and import tariffs can inflate antenna prices 20-30% in Nigeria or Egypt, slowing handset penetration, but infrastructure wins offset retail headwinds.

North America and Europe together form the second-largest block. The United States Federal Communications Commission finalized 5.9 GHz vehicle-to-everything rules in 2024, adding USD 150-200 in antenna content per car by 2028. European eCall requirements push multi-band GNSS reception into every new passenger vehicle, and Germany’s factory-owned 3.7-3.8 GHz licenses spawn private 5 G networks that need IP65-rated indoor-outdoor arrays. The United Kingdom’s GBP 200 million (USD 250 million) 6 G research program funds reconfigurable intelligent surfaces and terahertz radiators at universities and startups. Strict electromagnetic-compatibility and specific absorption rate limits in Europe demand bespoke antenna variants, raising non-recurring engineering spend 10-15% but generating regional engineering jobs.

Competitive Landscape

The top five players captured roughly 38% of 2025 revenue, leaving the antenna market moderately fragmented and ripe for specialists. Vertically integrated giants leverage in-house substrate, metallization, and assembly lines to shave 15-20% costs versus fabless rivals, an advantage magnified when materials such as liquid-crystal polymer experience spot shortages. Semiconductor vendors are eroding discrete share by embedding antenna-on-chip radiators inside modem packages, collapsing the bill-of-materials and re-routing margin toward advanced wafer-level packaging. Glass interposers allow sub-half-wavelength spacing above 30 GHz, enabling wide-angle beam steering without grating lobes and creating new competitive moats for suppliers that control through-silicon-via processes.

White-space opportunities remain in automotive vehicle-to-everything modules, where the pivot from dedicated short-range to 5 G protocols resets design baselines, and in satellite flat-panel terminals displacing gimbaled dishes on ships and aircraft. Gallium-nitride power amplifiers, forecast to own more than half of infrastructure shipments, align with antenna suppliers able to co-design radiators that minimize thermal drift. Additively manufactured conformal arrays for unmanned aeronautics compress lead times from twelve to three weeks, giving agile shops a toehold against incumbents. Compliance engineering poses a barrier: a full over-the-air, specific absorption rate, and electromagnetic-compatibility lab costs USD 2-5 million, slowing startups unless they partner with accredited test houses.

Strategic moves underline shifting ground. Qualcomm’s software-driven tuning lets handset OEMs deploy lower-cost passive radiators without sacrificing throughput, while Murata’s 5 mm-square 28 GHz antenna-in-package hits 25 dB element isolation in mass volume. Amphenol bolstered its automotive reach by scooping a European shark-fin pioneer, and CommScope introduced a 64-port active panel that raises sector capacity 30% for 3.5 GHz 5 G macro cells. Texas Instruments embedded 24 GHz radar antennas on-chip, slicing USD 3-5 from every blind-spot monitor, and Luxshare opened a 50 000 m² Vietnamese plant that hedges geopolitical risk for smartphone contracts. These moves illustrate how technology integration, geographic diversification, and vertical specialization are the decisive battlegrounds.

Antenna Industry Leaders

Molex, LLC

Amphenol Corporation

Airgain, Inc.

Galtronics USA, Inc

Sunway Communication

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Qualcomm launched the Snapdragon X80 5 G modem-RF system with software impedance tuning that boosts median downlink throughput 18%.

- January 2025: Murata began mass production of a 28 GHz antenna-in-package module measuring 5 mm × 5 mm × 0.8 mm, shipping more than 2 million units monthly to a Korean handset maker.

- December 2024: Amphenol acquired a European vehicle-to-everything antenna specialist, adding 120 engineers and shark-fin patents to its automotive lineup.

- November 2024: CommScope introduced a 64-port massive MIMO panel for 3.5 GHz 5 G, delivering 30% higher sector capacity than its 32-port predecessor.

Global Antenna Market Report Scope

An antenna is the intermediator between the radio waves propagating through space and current-carrying conductors. It works as the transducer that converts the radiofrequency field into alternating current. The two basic types of antenna are receiving antenna and transmitting antenna. Antennas can be designed to transmit and receive radio waves in all horizontal directions equally (omnidirectional antennas) or preferentially in a particular direction (directional, high-gain, or 'beam' antennas).

The Antenna Market Report is Segmented by Type (Stamping, FPC, LDS, LCP, MPI/Meta-Polymer), Technology (AoC, AiP, Active/Smart, Printed/Flexible, Phased-Array/Massive-MIMO), Frequency Range (Sub-1 GHz, 1-6 GHz, 6-30 GHz, >30 GHz), Product (Smartphone, Laptop/Tablet, Wearables/Hearables, Networking Equipment, Other Connected Devices), Application (Main Cellular, Bluetooth/BLE, Wi-Fi/WLAN, GNSS/GPS, NFC/RFID/UHF), Installation (Embedded/Internal, External/Mounted, Infrastructure/Base-Station), End-User Industry (Consumer Electronics, Military/Defense, Automotive/Mobility, Healthcare/Medical Devices, Industrial IoT/Smart Cities), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Stamping Antenna |

| FPC Antenna |

| LDS Antenna |

| LCP Antenna |

| MPI / Meta-Polymer Antenna |

| Antenna-on-Chip (AoC) |

| Antenna-in-Package (AiP) |

| Active / Smart Antenna Systems |

| Printed and Flexible Antennas |

| Phased-Array and Massive-MIMO Antennas |

| Sub-1 GHz (LF, VHF, UHF) |

| 1 to 6 GHz (L, S, C Bands) |

| 6 to 30 GHz (X, Ku, K, Ka) |

| > 30 GHz (mmWave, EHF, 5G FR2) |

| Smartphone |

| Laptop and Tablet |

| Wearables and Hearables |

| Networking Equipment (Routers, APs) |

| Other Connected Devices |

| Main Cellular |

| Bluetooth / BLE |

| Wi-Fi / WLAN |

| GNSS / GPS |

| NFC / RFID / UHF |

| Embedded / Internal |

| External / Mounted |

| Infrastructure and Base-Station |

| Consumer Electronics |

| Military and Defense |

| Automotive and Mobility |

| Healthcare and Medical Devices |

| Industrial IoT and Smart Cities |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type | Stamping Antenna | ||

| FPC Antenna | |||

| LDS Antenna | |||

| LCP Antenna | |||

| MPI / Meta-Polymer Antenna | |||

| By Technology | Antenna-on-Chip (AoC) | ||

| Antenna-in-Package (AiP) | |||

| Active / Smart Antenna Systems | |||

| Printed and Flexible Antennas | |||

| Phased-Array and Massive-MIMO Antennas | |||

| By Frequency Range | Sub-1 GHz (LF, VHF, UHF) | ||

| 1 to 6 GHz (L, S, C Bands) | |||

| 6 to 30 GHz (X, Ku, K, Ka) | |||

| > 30 GHz (mmWave, EHF, 5G FR2) | |||

| By Product | Smartphone | ||

| Laptop and Tablet | |||

| Wearables and Hearables | |||

| Networking Equipment (Routers, APs) | |||

| Other Connected Devices | |||

| By Application | Main Cellular | ||

| Bluetooth / BLE | |||

| Wi-Fi / WLAN | |||

| GNSS / GPS | |||

| NFC / RFID / UHF | |||

| By Installation | Embedded / Internal | ||

| External / Mounted | |||

| Infrastructure and Base-Station | |||

| By End-User Industry | Consumer Electronics | ||

| Military and Defense | |||

| Automotive and Mobility | |||

| Healthcare and Medical Devices | |||

| Industrial IoT and Smart Cities | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving short-term demand inside the antenna market?

Active 5 G rollouts in dense cities and vehicle-to-everything mandates in the United States and European Union add immediate volumes across infrastructure and automotive segments.

Which product category will grow fastest through 2031?

Wearables and hearables are projected to expand at a 7.70% CAGR as medical telemetry and augmented-reality headsets require ultra-compact multi-band radiators.

How are geopolitical risks affecting antenna supply?

Roughly 70% of flexible printed-circuit output sits in East Asia, so export controls or tariffs can delay Western product launches by up to nine months and push OEMs to diversify sourcing.

Why are liquid-crystal polymer substrates gaining share?

Flagship smartphones need substrates with low loss above 30 GHz, and liquid-crystal polymer films cut insertion loss by 0.3 dB at 28 GHz compared with polyimide, boosting radiated power 7%.

Which frequency bands will see the highest growth?

Bands above 30 GHz will register the quickest climb at 7.61% CAGR as operators extend millimeter-wave 5 G and seed early 6 G trials.

How many antennas will future passenger vehicles contain?

Average antenna counts are forecast to rise from eight units in 2024 to around fourteen by 2030 as vehicles incorporate cellular, vehicle-to-everything, GNSS, radar, and ultra-wideband links.

Page last updated on: