Alzheimer's Disease Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.22 Billion |

| Market Size (2031) | USD 7.88 Billion |

| Growth Rate (2026 - 2031) | 8.58% CAGR |

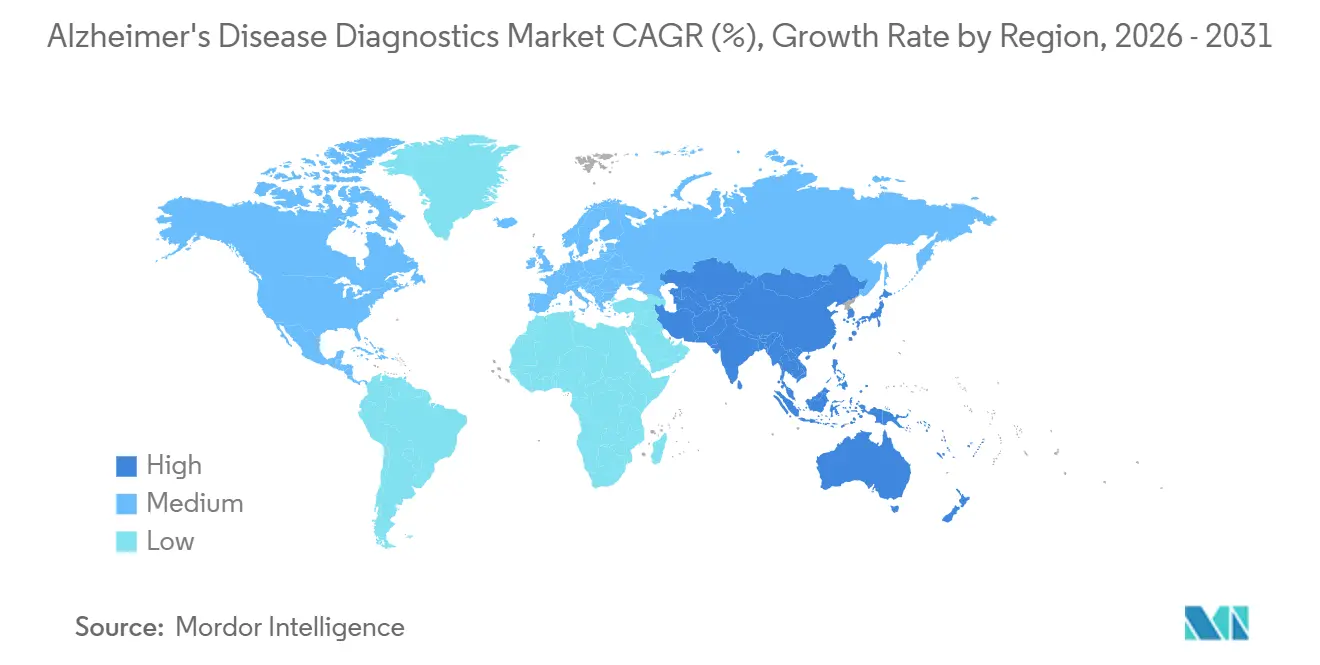

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

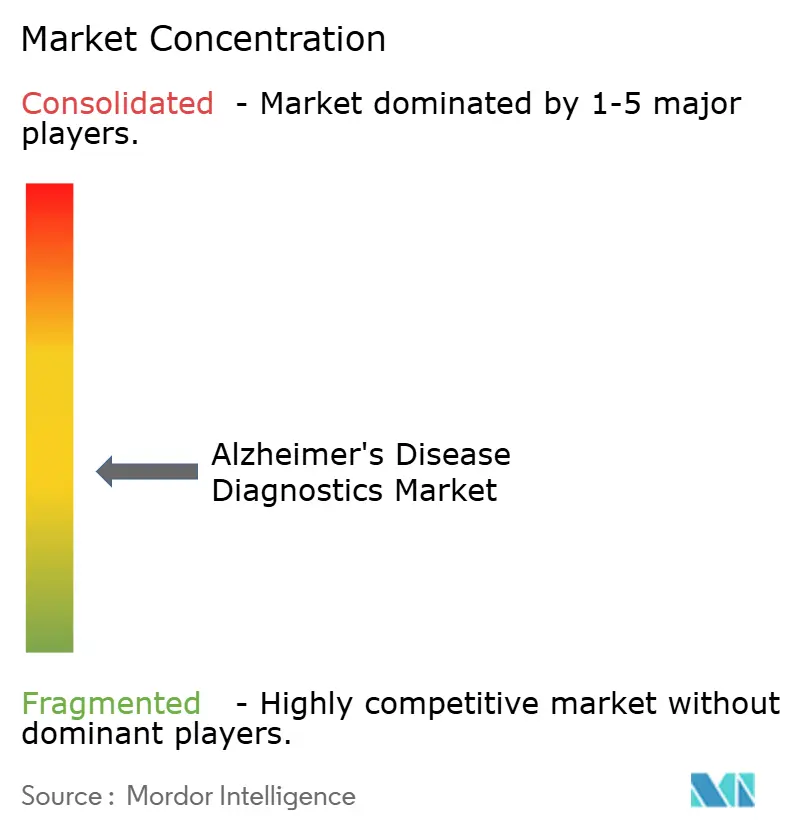

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alzheimer's Disease Diagnostics Market Analysis by Mordor Intelligence

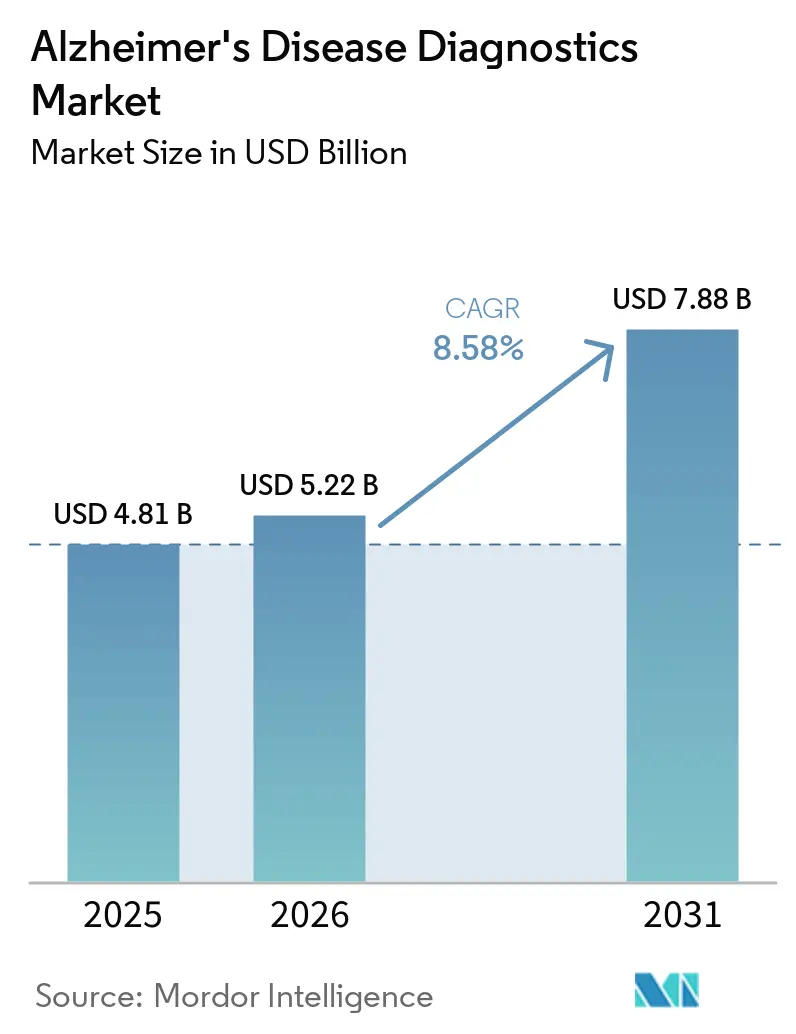

The Alzheimer's Disease Diagnostics Market size is expected to increase from USD 4.81 billion in 2025 to USD 5.22 billion in 2026 and reach USD 7.88 billion by 2031, growing at a CAGR of 8.58% over 2026-2031.

The market is moving into a faster growth phase because blood-based assays have started to lower the cost and operational friction tied to amyloid confirmation, which had long limited access to specialist pathways. The Alzheimer's disease diagnostics market is also benefiting from a closer tie between diagnostics demand and anti-amyloid therapy use, since treatment access increasingly depends on biomarker confirmation and, in some cases, broader risk profiling that can include ApoE4 status. The Alzheimer's disease diagnostics market is further supported by AI-enabled cognitive and imaging triage tools that help primary care and memory clinics identify likely cases earlier and send a better filtered population into confirmatory testing workflows. Even so, the Alzheimer's disease diagnostics market still faces a short-term gap between what is clinically feasible and what is commercially accessible, because reimbursement policy and assay standardization have not advanced as quickly as clinical adoption and regulatory clearances. This combination is pushing competition toward regulatory speed, laboratory reach, and workflow integration, while leaving meaningful room for companies that can connect screening, confirmation, and therapy-monitoring use cases inside the same care pathway.

Key Report Takeaways

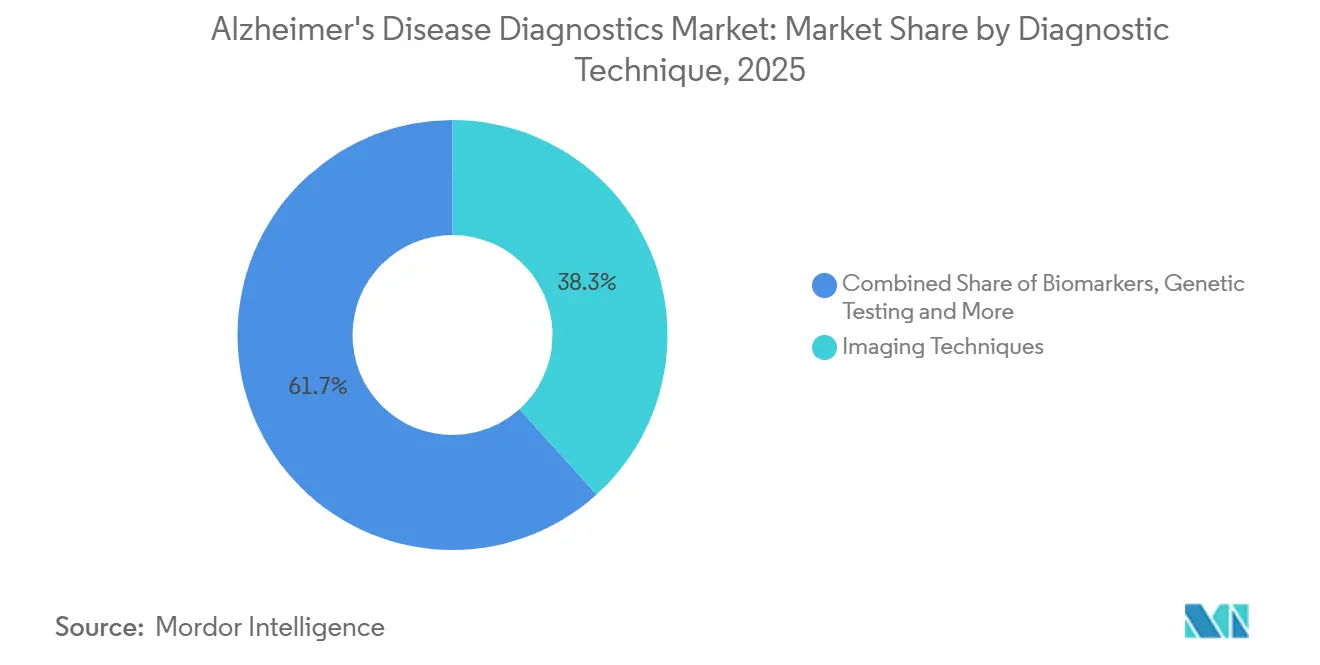

- By diagnostic technique, Imaging Techniques held 38.31% of revenue in 2025, while Biomarkers is projected to grow at 12.38% CAGR through 2031.

- By type, Diagnosis accounted for 55.24% of revenue in 2025, while Screening is forecast to expand at 11.52% CAGR through 2031.

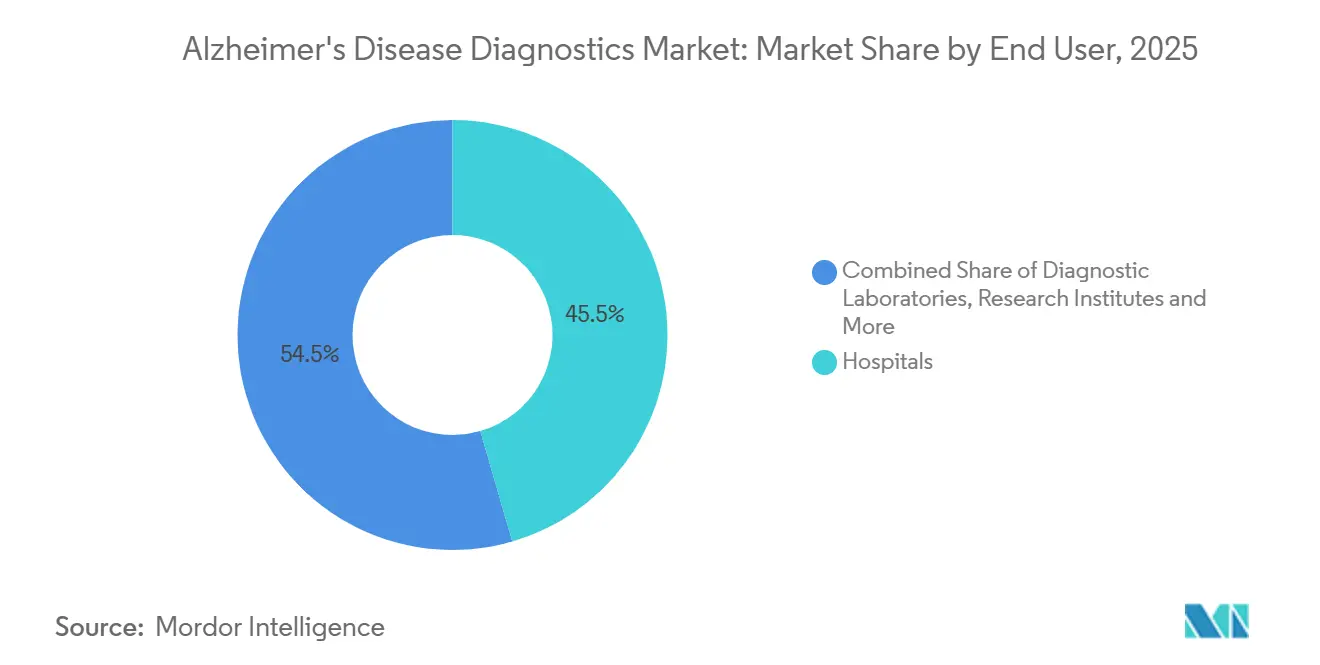

- By end user, Hospitals represented 45.52% of demand in 2025, while Diagnostic Laboratories is projected to record the fastest growth at 10.25% CAGR through 2031.

- By geography, North America held 43.22% of revenue in 2025, while Asia-Pacific is expected to advance at 12.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alzheimer's Disease Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Blood-Based Biomarkers | +2.3% | Global, early concentration in North America and Europe | Short term (≤ 2 years) |

| AI-Guided Imaging Triage In Memory Clinics | +1.1% | North America and Europe, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Expansion Of Pre-Symptomatic Testing Pathways | +0.9% | Global, led by North America, Japan, and Australia | Medium term (2-4 years) |

| Wider Use Of Cognitive Screening In Primary Care | +0.8% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Clinical Trial Companion Diagnostics Demand | +0.6% | Global, concentrated in the United States, Europe, and Japan | Short term (≤ 2 years) and Medium term (2-4 years) |

| Registry-Driven Case Finding And Referral Optimization | +0.3% | Core Europe, with early gains in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Blood-Based Biomarkers

The Alzheimer's disease diagnostics market is being reshaped by blood-based biomarkers after the FDA cleared Fujirebio's Lumipulse G pTau217/β-Amyloid 1-42 Plasma Ratio in May 2025 as the first blood-based in vitro diagnostic in the United States designed to identify amyloid pathology associated with Alzheimer's disease. The supporting multicenter study covered 499 cognitively impaired patients and showed a 91.7% positive predictive value and a 97.3% negative predictive value against PET and CSF reference standards, which gave clinicians a benchmark that was much closer to established confirmation methods than earlier screening tools had reached. By October 2025, Roche's Elecsys pTau181 became the only FDA-cleared blood test explicitly intended for primary care, and Labcorp then committed to a nationwide rollout in the United States by early 2026, which moved ordering power beyond the specialist neurologist base and into general practice workflows.

Quest Diagnostics reinforced the same shift by making the Fujirebio test available through its network of nearly 2,000 patient service centers, which gave the reference-lab route an immediate scale advantage in the Alzheimer's disease diagnostics market[1]Quest Diagnostics, “Quest Diagnostics to Offer FDA-Cleared Fujirebio Blood Test for Alzheimer's Disease,” Quest Diagnostics, questdiagnostics.com. The Alzheimer's Association then published its first clinical practice guideline for blood-based biomarker tests in 2025, including threshold expectations for triage and for PET or CSF substitution, which began to act as a practical filter for procurement and clinical adoption decisions. That framework supports faster consolidation around the assays that can meet both performance and workflow expectations, which is why the Alzheimer's disease diagnostics market is likely to reward a smaller group of clinically validated commercial platforms over the near term.

AI-Guided Imaging Triage in Memory Clinics

The Alzheimer's disease diagnostics market is also being supported by AI-guided imaging triage, because memory clinics are under pressure to handle larger referral volumes without relying on PET as the first step for every patient. A 2026 systematic review in the Journal of Medical Internet Research evaluated 66 studies and reported average diagnostic accuracy of 92.5%, with a standard deviation of 3.8%, and MCI-conversion AUCs of 0.922 across multimodal fusion architectures, which clearly outperformed single-modality baselines in the reviewed evidence base. TRACE4AD added a practical clinical example in a multicenter validation study that covered 797 subjects across 66 sites in Italy, the United States, and Canada, where AI-assisted neuropsychological and MRI staging predicted 24-month conversion to Alzheimer's dementia with clinically meaningful accuracy using structural imaging that is already widely available. This does not remove the role of PET from the Alzheimer's disease diagnostics market, because patients with intermediate blood-test results still need escalation and confirmatory imaging remains important for a smaller but higher-yield subset of cases.

Siemens Healthineers extended this direction in April 2026 by joining the Bio-Hermes-002 observational study and contributing Atellica IM biomarker assays to work across more diverse racial and ethnic populations, which addresses a major concern around whether AI and biomarker models trained in narrow cohorts can generalize well in real-world use. As these tools improve clinic throughput and case selection, the Alzheimer's disease diagnostics market is moving toward a model where AI improves the yield of each confirmatory test rather than simply replacing established modalities.

Expansion of Pre-Symptomatic Testing Pathways

The Alzheimer's disease diagnostics market is widening beyond symptomatic workups as pre-symptomatic testing pathways become more defined in clinical practice and research. In 2025, the International Working Group published a risk stratification framework in Nature Aging that described how asymptomatic individuals who are positive for amyloid and tau biomarkers can be triaged for prevention-focused management, which effectively created a new category of patients who now have a clearer reason to enter diagnostic pathways before functional decline is visible. That shift matters for the Alzheimer's disease diagnostics market because it broadens demand away from late-stage confirmation and toward earlier identification, longitudinal tracking, and risk-based counseling within specialist and research settings.

Roche expanded the same pathway in March 2026 when it received CE Mark for the Elecsys ApoE4 immunoassay, the first in vitro diagnostic immunoassay blood test designed to identify ApoE4 carriers, a variant it noted is present in 40% to 60% of people diagnosed with Alzheimer's disease. This adds a new genetic layer to patient workups and strengthens the role of multi-analyte panels inside the Alzheimer's disease diagnostics market, especially where treatment access and risk discussion are becoming more personalized. As more early-stage patients are identified, providers and laboratories are likely to rely on workflows that combine pathology detection, genetic risk information, and referral protocols rather than treating each of those steps as separate stand-alone events.

Wider Use of Cognitive Screening in Primary Care

The Alzheimer's disease diagnostics market is gaining another growth layer from primary care, where digital cognitive screening is starting to reduce one of the oldest barriers to earlier diagnosis, which is low physician confidence in identifying dementia without specialist support. The Alzheimer's Association's DETeCD-ADRD guideline in 2025 reported that 39% of primary care physicians were never or only sometimes comfortable making a dementia diagnosis, which makes simple digital tools more relevant because they lower the threshold for structured first-line assessment. Evidence from the Annals of Family Medicine showed that digital cognitive assessments can be deployed in primary care, with 4 of 7 pilot clinics reaching completion rates above 20% and most clinics still using the tool after 12 months, which gave this workflow a stronger operating case than many earlier screening pilots.

The Davos Alzheimer's Collaborative expanded the same model in February 2026 when University of Utah Health joined its U.S. Early Detection Expansion Program across five primary care clinics, linking digital assessment with referral pathways and blood biomarker testing. A Nature Medicine study in 2025 further validated a two-step model of self-administered digital cognitive assessment followed by blood-based amyloid testing, and it showed better detection performance than standard physician clinical assessment alone. As a result, the Alzheimer's disease diagnostics market is gaining a practical demand-creation layer in primary care that feeds more patients into laboratory and imaging workflows without requiring the first diagnostic step to take place inside a specialist center.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Reimbursement Friction For Advanced Testing | -1.5% | North America, with secondary effects in Europe and Asia-Pacific | Short term (≤ 2 years) and Medium term (2-4 years) |

| Limited Standardization Across Biomarker Assays | -0.9% | Global | Medium term (2-4 years) |

| Specialist Workforce Bottlenecks For Interpretation | -0.7% | Global, most acute in Asia-Pacific and South America | Long term (≥ 4 years) |

| Public-Health Stigma And Diagnosis Avoidance | -0.4% | Global, most pronounced in Asia-Pacific and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Reimbursement Friction for Advanced Testing

The Alzheimer's disease diagnostics market still faces a clear commercial barrier in reimbursement, even after clinical validation and regulatory approvals improved materially in 2025 and 2026. After the FDA cleared Fujirebio's blood test in May 2025, CMS initially proposed a reimbursement rate of USD 17 per test while an advisory-panel recommendation pointed to USD 130, which created a large gap between clinical value and economic viability for broad commercial laboratory deployment. A partial improvement took effect in January 2026 with the introduction of CPT codes 82233, 82234, and 84393 for individual analyte billing, which opened the possibility for multi-analyte panels to reach materially higher reimbursement levels than a single bundled rate would allow.

Even with that change, the Alzheimer's disease diagnostics market remains exposed to policy uncertainty because the ASAP Act was still pending in Congress as of mid-2026 and no fully settled Medicare pathway had been established for all FDA-approved blood-based screening tools[2]AdvaMed, “Earlier Answers, Better Care, How Expanded Access to Alzheimer's Testing Can Change Lives,” AdvaMed, advamed.org. This matters beyond diagnostics alone, because therapy use depends on timely confirmation and a slow reimbursement environment can delay the whole care pathway rather than only the laboratory test itself. The underlying policy mechanics, including the Clinical Laboratory Fee Schedule and the Advanced Diagnostic Laboratory Test designation process, continue to shape whether a test is priced on its own merits or benchmarked to broader laboratory coding structures that do not reflect its clinical role.

Limited Standardization Across Biomarker Assays

The Alzheimer's disease diagnostics market also faces a technical restraint in assay standardization, which directly affects comparability across laboratories, platforms, and clinical settings. An EFLM harmonization survey published in 2025 collected responses from 316 laboratories in more than 35 countries and reported marked variation across sample handling, assay choice, biomarker panels, and decision cutoffs, leading the committee to call for coordinated international harmonization. The Alzheimer's Association Global Biomarker Standardization Consortium Round Robin study quantified the same issue by applying 33 assay variants built on 8 analytical platforms to the same 40 patient samples, and it found that while plasma p-tau217 showed the best cross-platform agreement, plasma and CSF p-tau markers were not substantially correlated. That weakens a key assumption in the Alzheimer's disease diagnostics market, because many clinical decisions still depend on the idea that different assay formats can be interpreted in a broadly interchangeable way across care settings.

Pre-analytical variables add another layer of instability, since collection tube type, processing delay, and freeze-thaw cycles can shift biomarker measurements by up to 20% even before analytical differences are considered. Although the EU's IVDR framework and ISO-led standard-setting activity are pushing the field toward tighter quality expectations, the Alzheimer's disease diagnostics market still lacks a fully aligned system of mandatory cutoff harmonization across major regions, which means adoption can expand faster than consistency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diagnostic Technique: Imaging Leadership Holds While Biomarkers Scale Faster

Imaging Techniques accounted for 38.31% of the Alzheimer's disease diagnostics market share in 2025, which kept this category in the leading position because PET and MRI still anchor the specialist workup for amyloid burden, structural atrophy, and patient confirmation. The Alzheimer's disease diagnostics market still depends on installed imaging capacity in many high-value settings, since hospitals and memory clinics rely on long-established PET and MRI workflows that are already integrated into neurology referral pathways and treatment decisions. Biomarkers are the fastest-growing diagnostic technique with a 12.38% CAGR from 2026 to 2031, reflecting the shift of blood-based assays from research settings into routine in vitro diagnostic use across specialty care and primary care channels. This creates a dual-track structure in the Alzheimer's disease diagnostics industry, where imaging remains central for confirmation and follow-up while biomarker testing expands the number of patients who can enter diagnostic evaluation earlier and at lower operational cost. Genetic Testing remains a smaller category in current clinical use, yet its relevance is rising because ApoE4 status is becoming more important when clinicians assess treatment eligibility and risk discussions around anti-amyloid therapy.

GE HealthCare showed why imaging is unlikely to be displaced in a simple one-for-one manner when it received FDA approval in June 2025 for an expanded Vizamyl label that supports quantitative amyloid PET analysis and patient response monitoring for anti-amyloid therapy. That move extends PET into treatment monitoring, which gives Imaging Techniques a continuing role even as blood tests broaden first-line access inside the Alzheimer's disease diagnostics market. Cognitive Assessment Tests are also gaining steady traction, especially through AI-enabled digital platforms that support remote or front-end screening before patients move into biomarker or imaging confirmation. The interaction among techniques is therefore additive in many real-world settings, because blood-based testing, digital screening, imaging confirmation, and genetic risk assessment are increasingly being used as linked steps rather than isolated choices. Regulatory filters under the FDA 510(k) framework and the EU IVDR continue to determine how quickly newer assays can move from clinical promise into broad commercial use, which means market leadership depends not only on technology performance but also on execution across validation, clearance, and rollout.

By Type: Screening Moves Closer to Routine Care

Diagnosis held 55.24% of the by-type revenue in 2025, reflecting a history in which the most reliable demand came from symptomatic patients who had already advanced far enough to justify specialist referral, imaging, CSF workup, and formal clinical evaluation. Screening is the fastest-growing sub-segment at 11.52% CAGR from 2026 to 2031, showing that the Alzheimer's disease diagnostics market is starting to build real volume before severe functional decline becomes the trigger for testing. This shift is tied directly to blood-based assays, because they give primary care physicians and non-specialist channels a minimally invasive way to identify amyloid pathology with less friction than imaging-first pathways. Labcorp's nationwide rollout announcement in October 2025 for the FDA-cleared Elecsys pTau181 in primary care settings made that transition more concrete by linking the test to patients aged 55 and older with cognitive complaints and by placing access inside a large national service model. The Triage category is also improving because digital cognitive tools help physicians filter referrals before they move patients into blood-based or imaging confirmation, which reduces ordering friction and supports more structured use of confirmatory resources.

The Alzheimer's disease diagnostics market size for Screening is projected to expand at 11.52% CAGR through 2031, which shows how quickly the care model is shifting from late confirmation toward earlier identification of probable pathology. That growth is reinforced by the Alzheimer's Association's primary care guideline and by implementation work that shows digital assessment can stay in place beyond pilot use, which gives screening a more durable operating base inside routine care[3]Annals of Family Medicine, “Feasibility and Acceptability of Implementing a Digital Cognitive Assessment for Alzheimer Disease and Related Dementias in Primary Care,” Annals of Family Medicine, annfammed.org. The Alzheimer's disease diagnostics industry is therefore moving toward a wider front door, where patients can be screened, triaged, and referred through lower-friction pathways before they reach neurologists or imaging centers. That does not reduce the importance of Diagnosis as a category, because symptomatic confirmation, treatment qualification, and follow-up remain central to clinical decision making and revenue generation. Instead, the balance between Diagnosis, Screening, and Triage is changing because the Alzheimer's disease diagnostics market is adding new patient entry points rather than replacing the old ones. As these pathways mature, companies with strong links between digital tools, laboratories, and specialist handoff are better positioned to capture a larger share of testing volume across the full patient journey.

By End User: Reference Laboratories Gain Ground While Hospitals Remain Central

Hospitals accounted for 45.52% of end-user demand in 2025, which kept them in the leading position because they still concentrate neuroimaging, CSF analysis, specialist interpretation, and formal clinical workup in a single setting. The Alzheimer's disease diagnostics market continues to rely on hospitals as the main center for complex case resolution, especially when symptoms are advanced, imaging is needed, or treatment eligibility must be assessed across several diagnostic layers. Diagnostic Laboratories are growing at 10.25% CAGR from 2026 to 2031, which makes them the fastest-growing end-user category as blood-based assay processing migrates toward scaled reference-lab networks. Quest Diagnostics showed the strength of this shift in July 2025 when it rolled out access to the FDA-cleared Fujirebio Lumipulse test through nearly 2,000 U.S. patient service centers, widening geographic reach well beyond hospital-embedded testing capacity. This model gives the Alzheimer's disease diagnostics market a stronger primary care link, because physicians can order tests through broad laboratory networks without sending every patient directly into specialist centers as the first step.

The Alzheimer's disease diagnostics market size for Diagnostic Laboratories is projected to advance at 10.25% CAGR through 2031, and that pace reflects the advantage of high-throughput processing, national logistics, and physician outreach at scale. Academic and Research Institutes still play an important role because they absorb early demand for novel multi-analyte and research-use platforms, and their validation work often helps define where later in vitro diagnostic demand is likely to consolidate. The January 2026 reimbursement restructuring, including analyte-specific CPT codes, strengthened the operating case for scaled reference laboratories because it improved the payment structure for multi-analyte testing rather than leaving advanced panels inside a narrow bundled framework. This shifts competitive leverage in the Alzheimer's disease diagnostics industry toward laboratories that can handle large volumes profitably while maintaining validated workflows across different ordering channels. Hospitals are still likely to retain the heaviest concentration of complex interpretation and imaging-linked work, but the Alzheimer's disease diagnostics market is steadily redistributing front-end test access toward diagnostic lab networks. That redistribution is important because it changes who controls physician relationships, who captures repeat testing volume, and who becomes the practical gatekeeper for broad primary care adoption.

Geography Analysis

North America held 43.22% of the Alzheimer's disease diagnostics market share in 2025, giving it the largest regional position on the back of FDA regulatory momentum, a dense specialist neurology network, and the highest installed amyloid PET capacity among major regions. The United States has led the Alzheimer's disease diagnostics market regionally because two distinct blood-based in vitro diagnostic tests were cleared during 2025, which expanded commercial confidence and widened the range of clinical settings where testing could begin. Effective January 2026, new analyte-specific CPT codes also improved the route toward more viable Medicare reimbursement for blood-based testing, which matters because laboratory economics are central to scaling national access. Europe remains the second-largest regional block, and the May 2026 CE Mark approvals for Roche's Elecsys pTau217 and Fujirebio's Lumipulse G pTau217 Plasma assay opened the blood-biomarker channel across EU markets with a much broader commercial footprint than isolated country launches would have delivered. Germany adds another structural advantage through DEMREG, a national registry with 22 centers actively recruiting as of mid-2025, because it creates the real-world data base needed for local cutoff validation and ongoing performance assessment under the IVDR framework.

Asia-Pacific is the fastest-growing geography in the Alzheimer's disease diagnostics market, with a 12.15% CAGR projected from 2026 to 2031, and that pace reflects a large aging population, uneven specialist access, and a strong need for lower-friction diagnostic pathways. Japan is a key anchor in this regional shift because a 2025 study from Keio University and the University of Tokyo showed that plasma Aβ42/40 reached an AUC of 0.937 and detected amyloid accumulation earlier than PET visual reading thresholds in Japanese cohorts. That evidence gives the Alzheimer's disease diagnostics market a stronger local validation base for blood biomarkers in Japan, where domestic commercial positioning is also being supported by Fujirebio's parent group through regulatory steps and regional expansion efforts. China adds scale through policy and treatment dynamics, since lecanemab approval in January 2024 created an immediate need for companion diagnostic capacity in a system where specialist neurology access is still uneven across the country. Across Asia-Pacific, the Alzheimer's disease diagnostics market is therefore growing not only because patient numbers are rising, but also because blood-based and referral-linked tools fit better with the region's need to extend access beyond a narrow set of tertiary centers.

Middle East and Africa and South America remain early-stage territories in the Alzheimer's disease diagnostics market, where penetration is constrained by limited specialist workforces, weaker imaging infrastructure, and lower access outside major urban centers. GCC countries are leading diagnostic investment within the Middle East and Africa through government-backed healthcare expansion programs, which gives that sub-region a stronger foundation than most surrounding markets for future adoption. Brazil leads South America in diagnostic laboratory infrastructure and specialist neurology capacity, while Argentina remains a secondary hub with a smaller but still relevant concentration of expertise. Latent demand remains large across both regions because underdiagnosis is still widespread in lower-resource settings, which means the Alzheimer's disease diagnostics market has room to expand once workforce capacity, laboratory networks, and referral systems improve enough to support regular clinical use.

Competitive Landscape

The Alzheimer's disease diagnostics market has a moderately concentrated top tier, where Roche, Fujirebio, Siemens Healthineers, GE HealthCare, and Quanterix span the main commercial technology routes in blood biomarkers, amyloid PET imaging, and AI-enabled analysis. The current structure of the Alzheimer's disease diagnostics market is being reshaped less by exclusive control of a single marker and more by who can combine regulatory speed, assay automation, laboratory distribution, and clinical workflow fit into a scalable offering. A major example came in December 2025, when ALZpath and Siemens Healthineers signed a licensing agreement around ALZpath's proprietary pTau217 antibody, adding Siemens to a growing set of companies that already includes Roche, Beckman Coulter, Quanterix, and Alamar Biosciences in the use of the same core biomarker approach. That move reduced the room for differentiation based only on antibody access, which means execution around platform design, clearance timing, and commercial reach now carries more weight in the Alzheimer's disease diagnostics market. Companies that secured early reference-lab partnerships or rapid regulatory clearances are now better placed to capture physician ordering flow even when technical performance is moving closer across platforms.

Quanterix added another important competitive move in January 2026 with its FDA 510(k) submission for LucentAD Complete, a five-analyte algorithmic blood test designed to improve diagnostic clarity beyond what single-marker approaches can provide. That submission reflects a clear thesis within the Alzheimer's disease diagnostics market, which is that future differentiation may come from multi-analyte scoring and workflow intelligence rather than from one marker alone. Roche and Fujirebio strengthened their European position in May 2026 through CE Mark approvals for pTau217-based assays, giving both companies broader access to hospital and laboratory customers across EU member states at the same time. GE HealthCare defended imaging relevance in June 2025 by expanding the Vizamyl label into quantitative analysis and treatment response monitoring, which protects PET from being framed only as a legacy tool in a blood-based future. As a result, the Alzheimer's disease diagnostics market is increasingly competitive at the level of full pathway control, where laboratory access, physician adoption, therapy linkage, and post-diagnostic follow-up matter as much as core assay sensitivity.

White-space opportunities in the Alzheimer's disease diagnostics market remain strongest in therapy-monitoring diagnostics, point-of-care blood testing for lower-resource primary care settings, and AI-assisted imaging interpretation that can help radiologists manage expanding scan volumes. Companies without a steady CE or FDA clearance rhythm, or without direct access to major laboratory distribution channels, risk losing practical patient access even if their assay science is credible. At the same time, the mid-tier is diversifying rapidly because licensing agreements and route-to-market partnerships allow more entrants to participate without building every technology layer in-house. This keeps the Alzheimer's disease diagnostics market from looking tightly locked down by a single dominant firm, even though a relatively small group of established players still shapes the direction of commercial adoption, regulatory pacing, and clinician awareness.

Alzheimer's Disease Diagnostics Industry Leaders

F. Hoffmann-La Roche Ltd

GE HealthCare Technologies Inc.

Siemens Healthineers AG

Quanterix Corporation

H.U. Group Holdings, Inc. (Fujirebio Holdings, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Roche received CE Mark for Elecsys pTau217, developed in collaboration with Eli Lilly, measuring pTau217 protein to rule amyloid pathology in or out across primary and secondary care with a single-assay design and identical cutoffs across both settings. Clearance was based on real-world data from patients at the earliest clinical stages of disease.

- May 2026: Fujirebio received CE Mark for its Lumipulse G pTau217 Plasma assay under the EU's IVDR, enabling fully automated Alzheimer's blood testing on the LUMIPULSE G platform across European clinical laboratories.

Global Alzheimer's Disease Diagnostics Market Report Scope

As per the scope of the report, Alzheimer's disease diagnostics refers to the process and methods used to identify and confirm the presence of Alzheimer's disease in an individual.

The Alzheimer's disease diagnostics market is segmented by diagnostic technique, type, end user, and geography. By diagnostic technique, the market includes biomarkers, imaging techniques, genetic testing, and cognitive assessment tests. By type, it is categorized into diagnosis, screening, and triage. By end user, the segmentation covers hospitals, diagnostic laboratories, academic and research institutes, and other end users. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Biomarkers |

| Imaging Techniques |

| Genetic Testing |

| Cognitive Assessment Tests |

| Diagnosis |

| Screening |

| Triage |

| Hospitals |

| Diagnostic Laboratories |

| Academic and Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Diagnostic Technique | Biomarkers | |

| Imaging Techniques | ||

| Genetic Testing | ||

| Cognitive Assessment Tests | ||

| By Type | Diagnosis | |

| Screening | ||

| Triage | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Academic and Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of Alzheimer's disease diagnostics market?

The sector is valued at USD 5.22 billion in 2026 and is forecast to reach USD 7.88 billion by 2031 at an 8.58% CAGR.

Which diagnostic technique leads revenue today?

Imaging Techniques led with 38.31% of revenue in 2025 because PET and MRI remain central to specialist confirmation and monitoring workflows.

Which part of testing is growing fastest through 2031?

Screening is the fastest-growing type at 11.52% CAGR through 2031, supported by blood-based assays and digital first-line assessment in primary care.

Why are blood-based biomarkers changing clinical adoption?

They reduce the operational burden of amyloid confirmation, widen access beyond specialists, and fit more easily into national laboratory and primary care workflows.

Which end-user group is expanding the fastest?

Diagnostic Laboratories is the fastest-growing end-user group at 10.25% CAGR through 2031, as high-throughput reference labs take a larger role in front-end test access.

Which region offers the strongest near-term growth outlook?

Asia-Pacific has the fastest regional growth at 12.15% CAGR through 2031, supported by aging populations, local biomarker validation work, and a rising need for scalable testing pathways.

Page last updated on: