Genetic Disease Diagnostic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

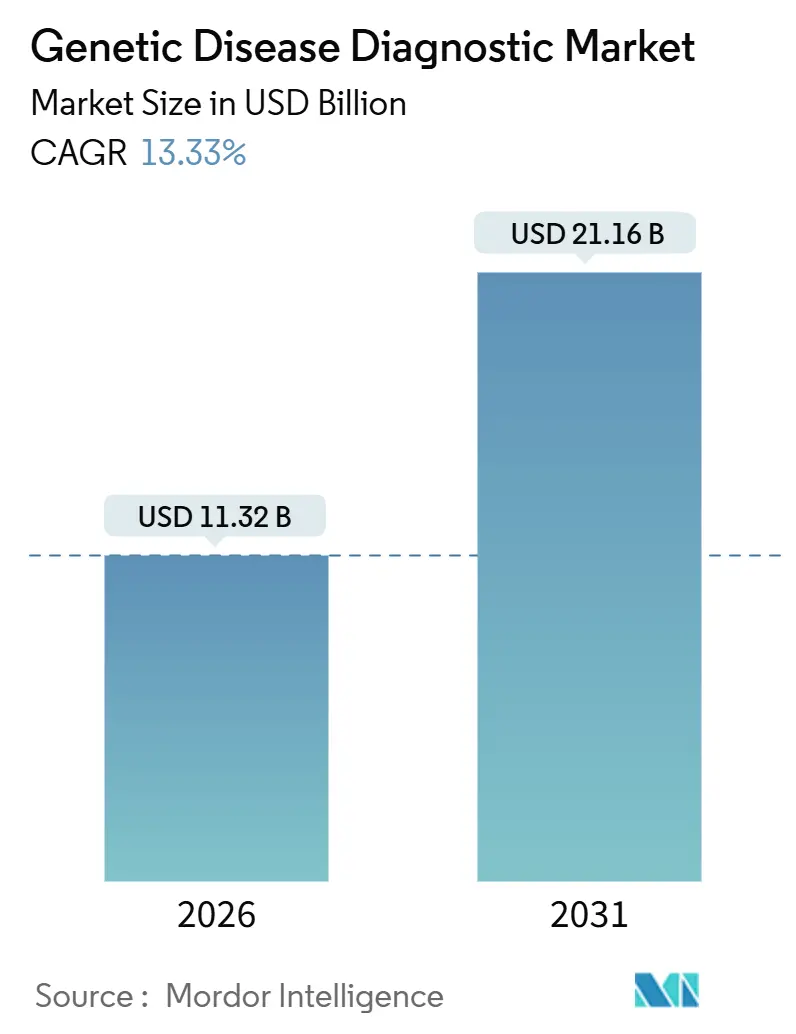

| Market Size (2026) | USD 11.32 Billion |

| Market Size (2031) | USD 21.16 Billion |

| Growth Rate (2026 - 2031) | 13.33% CAGR |

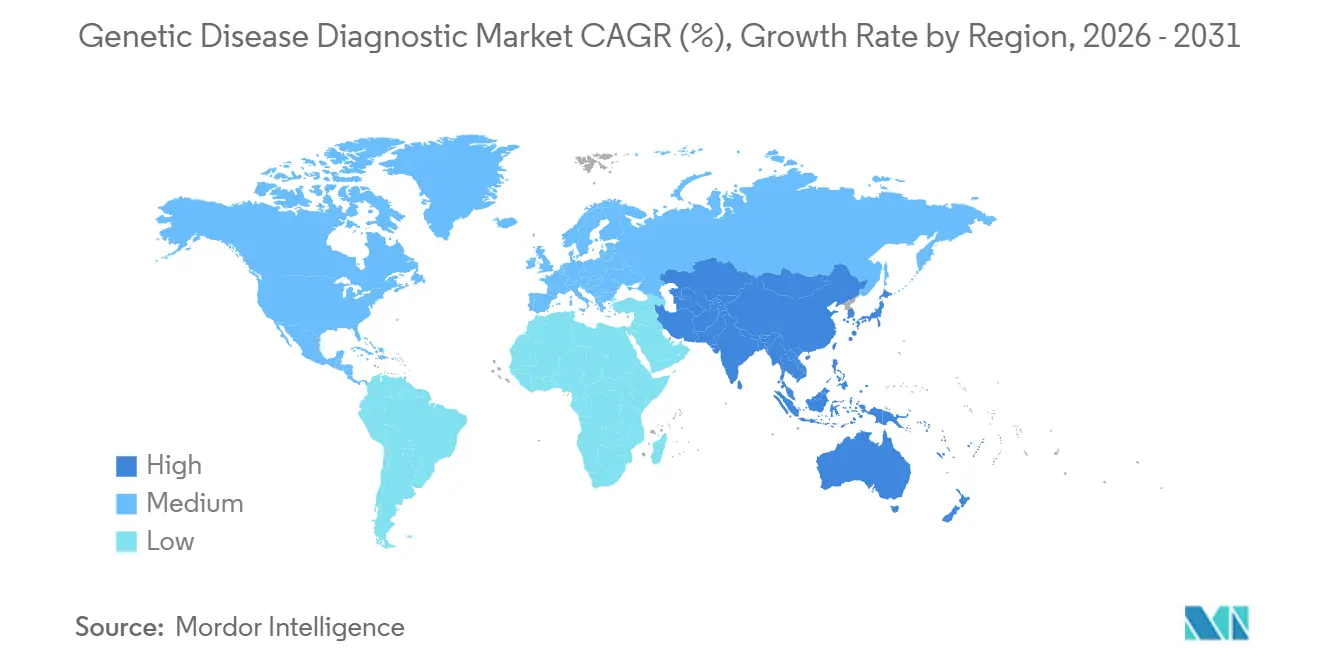

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Genetic Disease Diagnostic Market Analysis by Mordor Intelligence

The Genetic Disease Diagnostic Market size is estimated at USD 11.32 billion in 2026, and is expected to reach USD 21.16 billion by 2031, at a CAGR of 13.33% during the forecast period (2026-2031).

Falling per-genome costs, wider reimbursement for multi-gene panels, and streamlined workflows are accelerating adoption across oncology, newborn screening, and pharmacogenomics. The January 2026 expansion of next-generation sequencing (NGS) coverage in the United States removed prior-authorization hurdles, giving laboratories a direct volume catalyst. Consumables still anchor revenue, yet cloud bioinformatics and AI-driven interpretation capture most incremental margin, confirming that actionable insights, not raw reads, drive purchasing decisions. Platform vendors are racing to integrate long-read, optical, and digital PCR capabilities to address variant classes missed by short-read NGS while preserving regulatory compliance. Across regions, sovereign genome programs and newborn-screening mandates sustain a long-term pipeline of clinically relevant variants that expand test menus and lock users into the genetic disease diagnostic market.

Key Report Takeaways

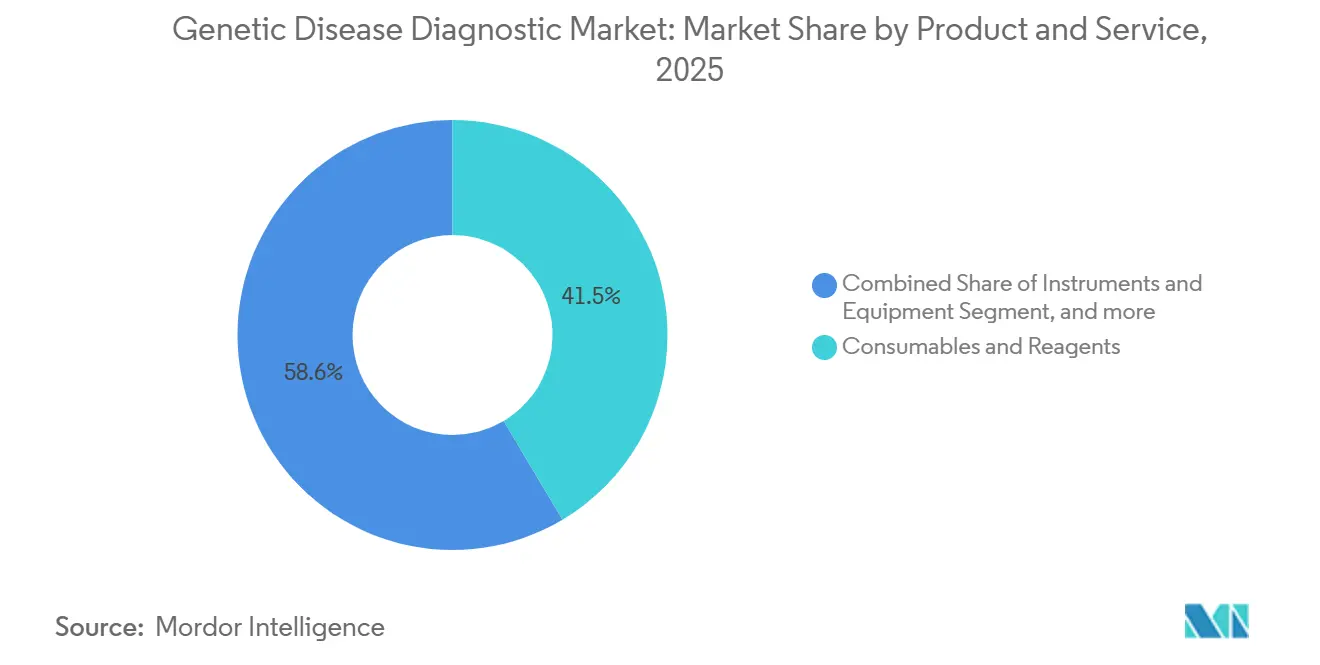

- By product & service, consumables accounted for 41.45% of revenue in 2025, whereas software & services are forecast to grow at a 15.65% CAGR through 2031.

- By test type, diagnostic testing dominated with a 52.34% share in 2025, while pharmacogenomic panels are projected to record a 16.78% CAGR to 2031.

- By technology, the polymerase chain reaction accounted for 34.56% of 2025 revenue; next-generation sequencing is poised for a 17.43% CAGR through 2031.

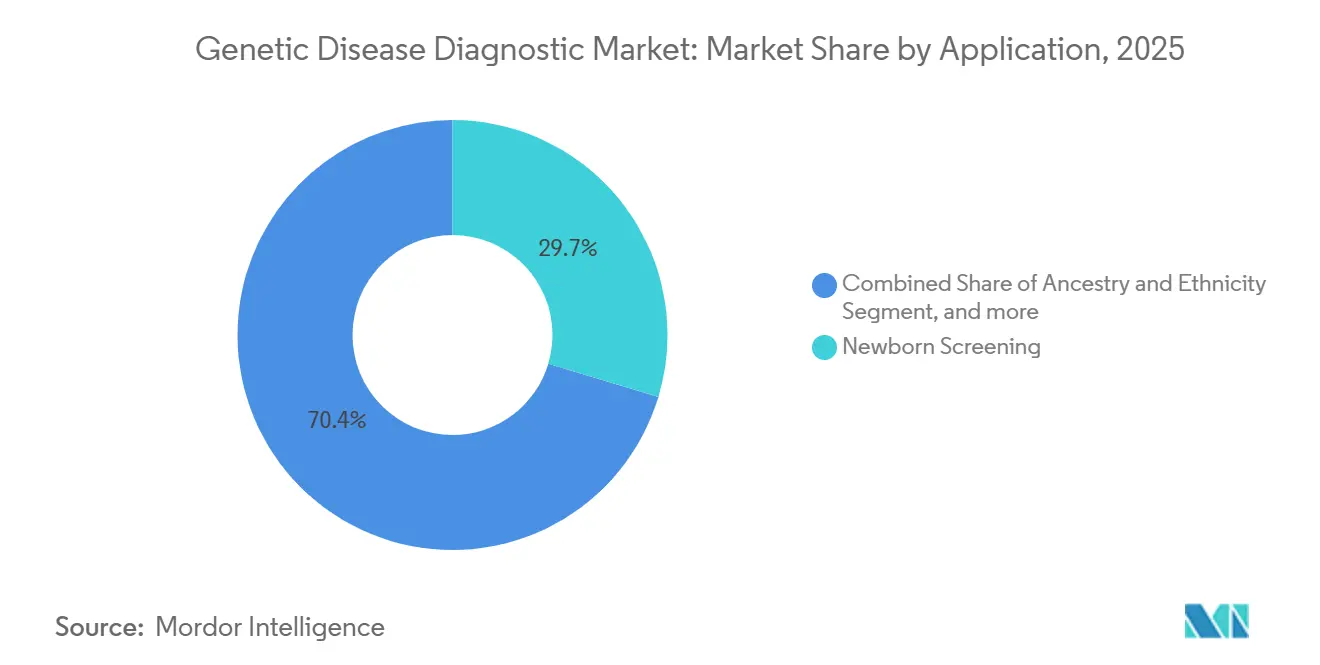

- By application, newborn screening led with 29.65% of 2025 demand, yet health and wellness risk assessment is expected to expand at a 17.54% CAGR to 2031.

- By end user, diagnostic laboratories accounted for 42.45% of revenue in 2025, whereas hospitals & clinics are slated to grow at a 16.54% CAGR through 2031.

- By geography, North America captured 43.12% of the market share in 2025; Asia-Pacific is projected to post a 14.54% CAGR across the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Genetic Disease Diagnostic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of genetic disorders | +2.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Technological advancements in sequencing | +3.5% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Expanding newborn-screening programs | +2.1% | North America, Europe, select Asia-Pacific | Long term (≥ 4 years) |

| Adoption of personalized medicine paradigms | +2.4% | North America, Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| EHR-based genomic data integration | +1.6% | North America, Europe, early pilots in Asia-Pacific | Long term (≥ 4 years) |

| Scale-up of population-genomics initiatives | +1.9% | Global, with national programs in UK, US, China, Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Genetic Disorders Worldwide

One in ten Americans lives with a rare condition, most with an underlying genetic etiology, prompting clinicians to favor broad sequencing panels over sequential single-gene tests[1]National Organization for Rare Disorders, “Rare Disease Facts and Statistics,” rarediseases.org. The December 2025 inclusion of Duchenne muscular dystrophy and metachromatic leukodystrophy in the U.S. newborn panel underscores the importance of early genomic detection in preventing irreversible organ damage. Oncology adds volume because tumor mutational burden and microsatellite instability testing are now baseline criteria for immunotherapy eligibility, and the FDA’s 2024 clearance of a 523-gene panel confirmed regulators' view that multi-gene assays are first-line diagnostics. Payers have responded by expanding coverage, yet 40% of orders still face 2-week authorization delays, pushing laboratories to deploy real-time benefit-verification software to trim friction. As prevalence data improve, health-system executives increasingly view universal sequencing as a cost-effective alternative to the diagnostic odyssey.

Technological Advancements in Genomic Sequencing Platforms

Between 2022 and 2025, NGS throughput doubled while whole-exome sequencing dropped below USD 600 per sample, enabling laboratories to price exomes on par with legacy panels. Illumina’s late-2025 partnership with MyOme to distribute NovaSeq X units in regional hubs demonstrates a pivot from mega-labs toward 48-hour neonatal turnaround. Optical genome mapping detects structural variants missed by short-read NGS, and Bionano Genomics installations expanded across U.S. academic centers in 2025. Long-read HiFi sequencing from Pacific Biosciences secured FDA breakthrough status for Fragile X syndrome, accelerating clinical validation[2]U.S. Food & Drug Administration, “510(k) Clearance for TruSight Oncology Comprehensive,” fda.gov. Collectively, these innovations erase the technical divide between research- and clinic-grade sequencing, keeping the genetic disease diagnostic market on a steep learning curve.

Increasing Government Support for Newborn Screening Programs

Federal grants funded the BEACONS consortium to pilot whole-genome sequencing alongside biochemical tests in five states, identifying actionable findings in 3.2% of newborns and reducing five-year hospitalization costs by USD 120,000 per affected infant. The United Kingdom’s 200,000-infant genome program and Japan’s April 2025 reimbursement for 50 sequenced conditions illustrate parallel momentum outside the United States. Longitudinal datasets generated by these programs refine variant classifications, shrinking the 30% rate of uncertain significance that burdens clinicians. ISO 15189 accreditation assures quality, yet debates over incidental findings and long-term data storage continue to shape protocol design. Cumulatively, policy tailwinds make newborn sequencing the most legislatively secure growth pillar in the genetic disease diagnostic market.

Growing Adoption of Personalized Medicine Paradigms

By 2025, pharmacogenomic testing will accompany 12% of U.S. hospital discharges, double the 2022 level, led by CYP2D6 and CYP2C19 genotyping that cut adverse drug events by 28% in a 50,000-patient cohort. Tumor profiling now guides targeted therapy selection for 65% of metastatic solid-tumor cases, and CMS’s January 2026 reimbursement expansion eliminated coverage gaps that had confined access to academic centers. Direct-to-consumer firms such as Color Health pivoted into primary care, integrating hereditary cancer panels into routine checkups. Regulatory scrutiny sharpened after the FDA warned 23andMe in 2024 over unvalidated risk reports, signaling that clinical claims must be evidence-backed regardless of distribution model. The convergence of payment, guideline, and technology drivers cements pharmacogenomics as the fastest-growing niche within the genetic disease diagnostic market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of genetic testing procedures | -1.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Data privacy and ethical concerns | -1.2% | Global, heightened in Europe and North America | Medium term (2-4 years) |

| Limited reimbursement for multi-gene panels | -1.5% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| Shortage of skilled genetic counselors | -0.9% | Global, critical gaps in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Genetic Testing Procedures

List prices for whole-exome sequencing still exceed USD 1,500 in many U.S. labs, and uninsured patients may pay over USD 3,000 out of pocket[3]American College of Medical Genetics, “Clinical Utility of Whole-Exome Sequencing,” acmg.net. Prior-authorization denials cause one-quarter of insured patients to abandon hereditary-cancer testing, wasting clinician time and eroding confidence. In low-income countries, the absence of reimbursement and limited lab capacity leaves broad sequencing unattainable, forcing reliance on low-resolution tests. Direct-to-consumer kits at USD 99–199 lack clinical accuracy, sowing confusion about test utility. Although CMS broadened oncology coverage, gaps persist for carrier screening, pharmacogenomics, and predictive panels, capping volume expansion in those subsegments of the genetic disease diagnostic market.

Data Privacy and Ethical Concerns

A 2023 breach at 23andMe exposed data of 6.9 million users, leading to a USD 30 million settlement and prompting California to draft the Genetic Information Privacy Act. Europe intensified GDPR enforcement, fining a laboratory EUR 5 million for inadequate minimization practices. U.S. HIPAA violations involving genomic data rose 40% between 2023 and 2025, and new federal guidance requires business-associate agreements to explicitly cover genomic datasets. Patient surveys show 60% would rather not learn incidental findings for untreatable disorders, complicating consent protocols. Privacy anxieties can deter enrollment in population-scale studies, thereby limiting the availability of variant databases essential to the genetic disease diagnostic market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Software Drives Margins While Consumables Anchor Volume

Consumables accounted for 41.45% of 2025 revenue, a steady stream that monetizes installed sequencers and secures recurring cash flow for platform vendors. The genetic disease diagnostic market size attributed to consumables is projected to rise in line with test volumes but at a slower pace than software-driven sales. Cloud bioinformatics and AI interpretation services are forecast to grow at a 15.65% CAGR to 2031, reflecting hospitals’ need to outsource variant curation and report generation. This shift moves gross margins from reagents toward subscription models, diversifying vendor revenue. Open-source pipelines funded by a USD 30 million NIH grant threaten proprietary margins, yet laboratories still pay for validated, regulatory-compliant workflows that minimize audit risk. Competition intensifies as Chinese reagent suppliers enter with prices 40% below incumbents, forcing Western vendors to bundle consumables with software to defend share.

Capital-equipment demand lags due to leasing models and long refresh cycles, though sub-USD 100,000 benchtop sequencers democratize access for community hospitals. Service providers pivot to software licensing after high debt loads revealed the danger of overbuilt labs; the Invitae bankruptcy accelerated this pivot. AI-enabled platforms cut manual variant review 60%, improving throughput and highlighting the genetic disease diagnostic market share vulnerability for labs tied to in-house curation teams. The next competitive frontier will be interoperability that lets users mix low-cost reagents with best-of-breed software, breaking vendor lock-in.

By Test Type: Diagnostics Lead, Pharmacogenomics Accelerates

Diagnostic panels held a commanding 52.34% share in 2025, reflecting entrenched oncology and rare-disease demand. The genetic disease diagnostic market size for diagnostic testing is projected to remain dominant as multi-gene oncology panels become the standard of care. Pharmacogenomics, however, is forecast to post the fastest CAGR of 16.78%, propelled by hospital formulary committees embracing preemptive genotyping to curb adverse events. Medicare’s reimbursement gap slows uptake, but employer wellness programs and self-insured systems pay out of pocket to avoid downstream treatment costs. Prenatal and carrier testing grow steadily in high-risk populations, yet face ethical debates over expansion to non-medical traits.

Newborn sequencing volumes will climb after the 2025 U.S. mandate adds two neuromuscular disorders, giving states until 2028 to comply. Predictive testing remains underpenetrated because many patients eschew knowledge about untreatable conditions, despite expanded BRCA guidelines. Collectively, the test-type mix is shifting from reactive disease diagnosis toward proactive therapy optimization, diversifying revenue streams across the genetic disease diagnostic market.

By Technology: NGS Takes the Growth Crown, PCR Holds Installed Base

Next-generation sequencing is projected to deliver a 17.43% CAGR, the brightest technology outlook, as costs drop and benchtop systems reduce capital barriers. Polymerase chain reaction retained a 34.56% revenue share in 2025, reflecting massive installed infrastructure and clinician familiarity. Still, payers increasingly reimburse broad panels over single-gene assays, tilting volume toward NGS. Microarrays keep niche applications in cytogenetics, but optical genome mapping captured a meaningful share by detecting significant structural variants that arrays miss. Long-read platforms, awarded FDA breakthrough status, now address repeat-expansion disorders, opening new clinical indications.

Digital PCR emerges as a minimal-residual-disease tool, measuring circulating tumor DNA at sub-0.01% sensitivity, yet remains adjunctive rather than primary. Pricing wars accelerate as Chinese firms undercut reagent costs, pushing Western vendors to differentiate through integrated software and compliance packages. Over the forecast period, NGS's market share in the genetic disease diagnostics market will expand as laboratories retire older platforms for multi-omics workflows.

By Application: Newborn Programs Scale, Wellness Testing Finds Payors

Newborn screening accounted for 29.65% of 2025 revenue and will grow as additional disorders are added to mandatory panels. The genetic disease diagnostic market size linked to wellness testing is projected to grow the fastest, supported by a 17.54% CAGR driven by employer adoption of polygenic-risk scoring. Still, reimbursement remains elusive, and insurers classify many wellness tests as investigational despite emerging evidence of preventive value. Carrier screening expands in consanguineous regions under government mandates, and early statistics from the UAE show a 30% reduction in dual-carrier marriages after national rollout.

Ancestry testing shrank after a major breach eroded public trust, prompting consumer-facing companies to rebrand toward clinical partnerships. Traits testing stays in regulatory gray zones, with the FDA cautioning firms that medical inference requires validation. Segmentation indicates a bifurcated path: regulated medical applications secure reimbursement while direct-pay wellness solutions explore value-based employer models.

By End User: Labs Lose Growth Leadership to Hospitals

Diagnostic laboratories retained 42.45% of the revenue share in 2025, but hospitals and clinics are projected to grow faster at a 16.54% CAGR as point-of-care sequencers enable same-admission diagnoses. Reference-lab consolidation, exemplified by a large 2024 acquisition, reduces the number of national players to a duopoly and heightens pricing scrutiny. Academic medical centers poured COVID-era capital into CLIA-certified genomics labs, raising in-house capacity to 25% of U.S. teaching hospitals.

Fee-schedule disparities still reimburse reference labs at higher rates, creating a financial drag on hospital vertical integration, yet clinical imperatives often trump margin. Research institutes lend variant-interpretation expertise to clinical partners, helping mitigate counselor shortages. Hybrid models emerge in which urgent neonatal cases remain in-house while high-volume carrier panels are sent to reference labs, optimizing speed and cost trade-offs across the genetic disease diagnostic market.

Geography Analysis

North America accounted for 43.12% of 2025 revenue, powered by dense reimbursement and guideline adoption. The January 2026 CMS ruling eliminating prior authorization for many panels is expected to lift U.S. volumes 25% over the forecast period. Canada expanded hereditary-cancer coverage, yet rural wait times persist, reflecting provincial disparities. Mexico remains a self-pay market except for private hospital partnerships, limiting penetration.

Europe confronts the new In Vitro Diagnostic Regulation, raising compliance costs and pushing smaller labs to purchase CE-marked kits. Germany now reimburses CYP2D6 and CYP2C19 testing, cutting adverse drug events 30%, while the UK newborn genome program identifies actionable findings in 2.8% of infants. Southern Europe lags in reimbursement, driving medical tourism north.

Asia-Pacific posts the highest 14.54% CAGR, buoyed by China’s million-genome program, Japan’s reimbursed newborn sequencing, and India’s GenomeIndia reference panel. Australia covers BRCA and Lynch testing nationally, and South Korea funds pharmacogenomics for anticoagulants, reducing stroke incidence 15%. Combined, population-scale sequencing and expanding reimbursement make the region the strategic frontier for the genetic disease diagnostic market.

The Middle East invests in consanguinity-mitigation programs: Saudi Arabia’s 100,000-genome database informs premarital counseling, and the UAE’s carrier-screening mandate is already shifting marriage patterns. Africa pilots pharmacogenomics for HIV therapies, and South Africa reports a 25% drop in treatment discontinuation. Latin America trails; Brazil’s public system reimburses no genomic tests, though academic centers fill research gaps. Overall, geography splits mature payor-driven markets from emerging state-funded initiatives, both feeding long-run demand.

Competitive Landscape

The top five companies held roughly 40% of global revenue in 2025, indicating moderate concentration. Sequencing-platform leaders defend share through proprietary chemistries that bind consumable spend, yet reagent price deflation from Chinese entrants squeezes margins. Reference laboratories process 80% of U.S. tests, leveraging scale, but high capital intensity was underscored when a leading player exited via bankruptcy, later absorbed by a dominant lab.

Software specialists capture 15% of bioinformatics spend by automating variant interpretation, reducing manual review by 60% and eroding the consulting business of clinical geneticists. AI patents for natural-language phenotype extraction rose 60% in two years, filed by incumbents and startups alike. Optical genome mapping, long-read sequencing, and digital PCR vendors exploit niche-variant classes, creating competitive flanks that incumbents must address or acquire.

White-space lies in pharmacogenomics, where reimbursement gaps create a self-pay employer market. Direct-to-consumer brands pivot into clinical channels, integrating results into primary care to regain trust after privacy concerns. Over the forecast period, winners will pair low-cost reagents with interoperable software, satisfy evolving regulatory demands, and secure data rights for AI training, reinforcing moats within the genetic disease diagnostic market.

Genetic Disease Diagnostic Industry Leaders

Illumina, Inc.

Myriad Genetics

23andMe

Invitae

Natera

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: NHS launches the world's first national genetic register. This program will monitor thousands of individuals at higher risk of developing cancer due to inherited genetic mutations. It aims to provide regular checks and tracking to improve early detection and prevention.

- February 2025: Medicover Genetics announced that its TarCET Kit, an NGS-based genetic testing product received CE marking under the EU IVDR regulation. This certification ensures the product complies with strict European safety and efficacy standards. The TarCET Kit offers panels for various genetic conditions, used alongside IVD Analysis Software for accurate diagnostics.

Global Genetic Disease Diagnostic Market Report Scope

As per the scope of the report, genetic disease diagnostic involves identifying genetic mutations or abnormalities that cause inherited or acquired diseases. It includes products like genetic testing kits, sequencing machines, and reagents, as well as services such as DNA analysis, counseling, and interpretation. These diagnostics aid in early detection, personalized treatment, and disease management.

The Genetic Disease Diagnostic Market is Segmented by Product & Service (Consumables & Reagents, Instruments & Equipment, and Software & Services), Test Type (Diagnostic, Prenatal & Newborn, Predictive & Presymptomatic, Carrier, and Pharmacogenomic), Technology (NGS, PCR, Microarray, Cytogenetics/FISH, and Other Technologies), Application (Ancestry & Ethnicity, Traits Screening, Genetic Disease Carrier Status, Newborn Screening, and Health & Wellness-Risk Assessment), End User (Hospitals & Clinics, Diagnostic Laboratories, and Research & Academic Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Consumables & Reagents |

| Instruments & Equipment |

| Software & Services |

| Diagnostic |

| Prenatal & Newborn |

| Predictive & Presymptomatic |

| Carrier |

| Pharmacogenomic |

| Next-Generation Sequencing (NGS) |

| Polymerase Chain Reaction (PCR) |

| Microarray |

| Cytogenetics/FISH |

| Other Technologies |

| Ancestry & Ethnicity |

| Traits Screening |

| Genetic Disease Carrier Status |

| Newborn Screening |

| Health & Wellness-Risk Assessment |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product & Service | Consumables & Reagents | |

| Instruments & Equipment | ||

| Software & Services | ||

| By Test Type | Diagnostic | |

| Prenatal & Newborn | ||

| Predictive & Presymptomatic | ||

| Carrier | ||

| Pharmacogenomic | ||

| By Technology | Next-Generation Sequencing (NGS) | |

| Polymerase Chain Reaction (PCR) | ||

| Microarray | ||

| Cytogenetics/FISH | ||

| Other Technologies | ||

| By Application | Ancestry & Ethnicity | |

| Traits Screening | ||

| Genetic Disease Carrier Status | ||

| Newborn Screening | ||

| Health & Wellness-Risk Assessment | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Research & Academic Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the projected CAGR for the genetic disease diagnostic market through 2031?

The market is forecast to expand at a 13.33% CAGR from 2026 to 2031.

Which region is expected to grow the fastest over the forecast period?

Asia-Pacific is projected to record a 14.54% CAGR, outpacing all other regions.

Which segment holds the largest 2025 share by technology?

Polymerase chain reaction held 34.56% of technology revenue in 2025.

Why are software and services growing faster than consumables?

Laboratories increasingly outsource AI-enabled variant interpretation, pushing software revenue at a 15.65% CAGR.

What policy change in 2026 most benefits U.S. test volumes?

CMS removed prior-authorization requirements for many NGS panels, expected to raise volumes by 25%.

How are newborn screening mandates influencing demand?

The 2025 addition of two neuromuscular disorders to the U.S. panel and similar global programs drive steady growth in newborn sequencing.

Page last updated on: