United States Brain Health Supplements Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

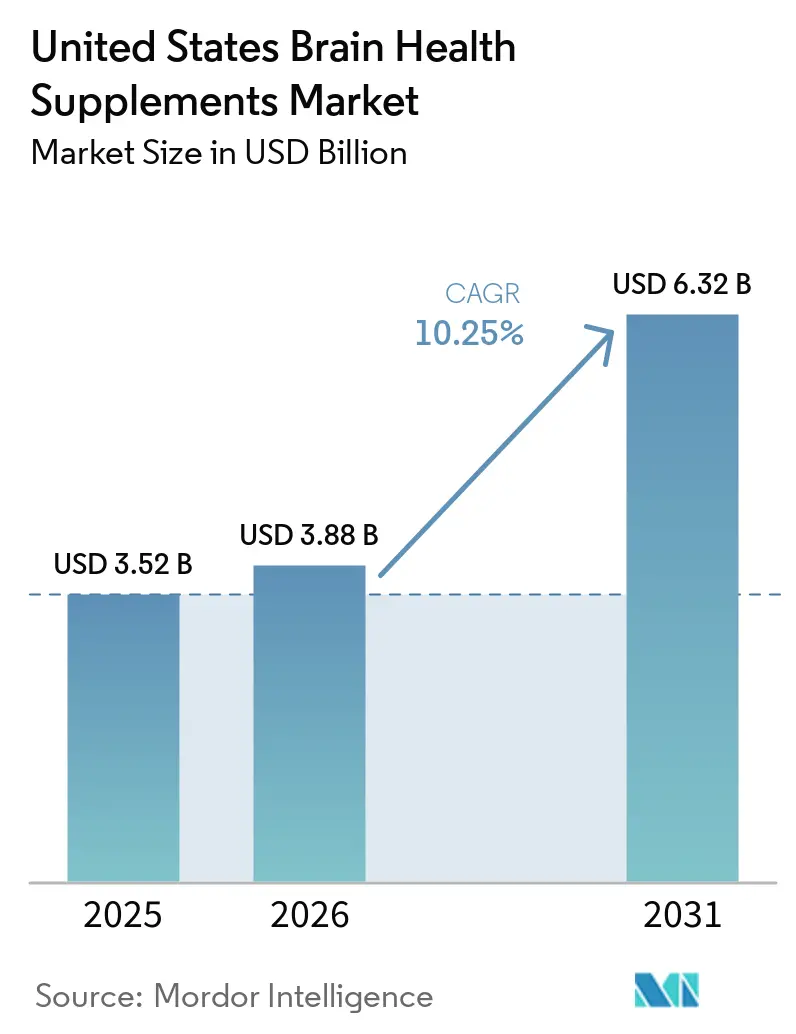

| Base Year Market Size (2025) | USD 3.52 Billion |

| Market Size (2026) | USD 3.88 Billion |

| Market Size (2031) | USD 6.32 Billion |

| Growth Rate (2026 - 2031) | 10.25% CAGR |

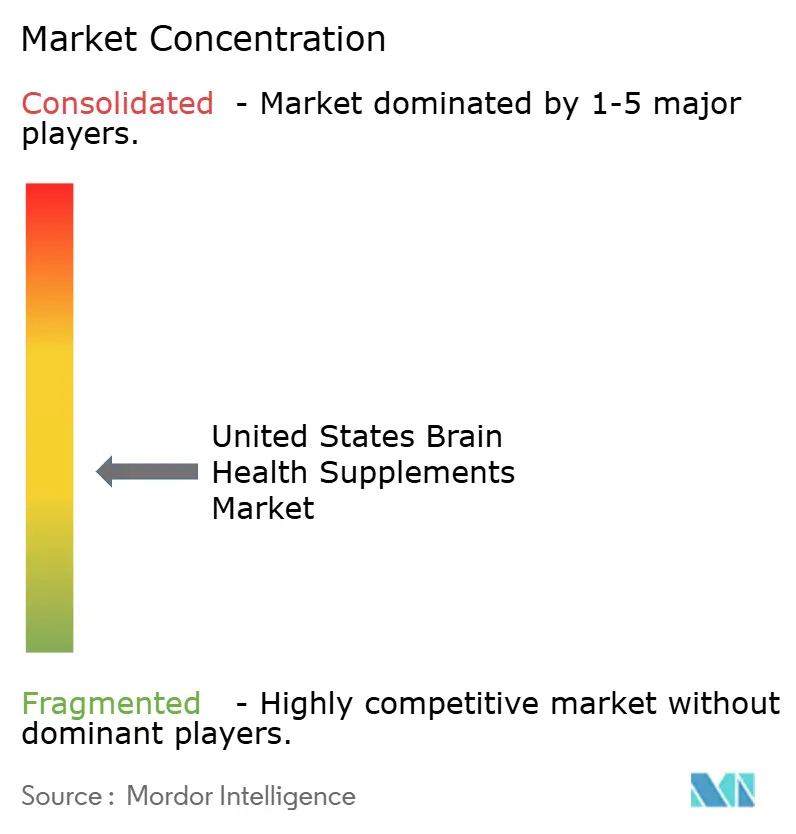

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Brain Health Supplements Market Analysis by Mordor Intelligence

The United States Brain Health Supplements Market size is projected to be USD 3.52 billion in 2025, USD 3.88 billion in 2026, and reach USD 6.32 billion by 2031, growing at a CAGR of 10.25% from 2026 to 2031.

The market is being supported by 3 durable demand shifts, rising mental health self-care among consumers, wider use of nootropic ingredients across age groups, and a move among older adults toward preventive nutrition before cognitive decline becomes more visible. The United States also remains a favorable setting for product commercialization because the DSHEA framework gives supplement brands more room to test formulations and launch new products than many markets in Europe and Asia Pacific, which keeps the innovation pipeline active. Launch activity reflects that flexibility, with 258 new products carrying mental clarity claims in 2024 and 203 launches carrying focus support claims in the same year. Consumer behavior is also moving in the same direction, with 37% of U.S. adults reporting supplement use for cognitive function in 2025 and 55% of consumers making supplement purchases through social media or live-stream platforms, which continues to expand the digital runway for the United States brain health supplements market. Competitive strategy is becoming more disciplined because the FTC’s 2024 action against Quincy Bioscience raised the cost of unsupported memory claims, while brands that fund finished-product validation now have a clearer way to stand out in the United States brain health supplements market.

Key Report Takeaways

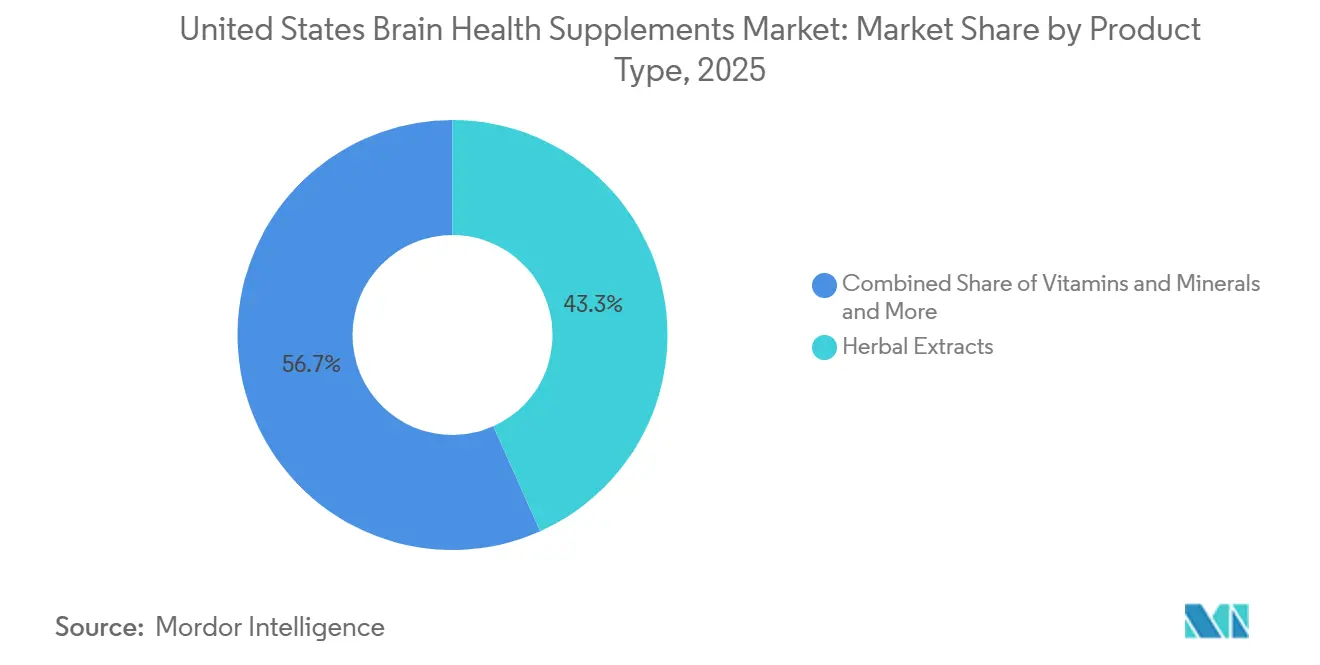

- By product type, herbal extracts held 43.31% of the United States brain health supplements market share in 2025, while vitamins and minerals are projected to grow at a 12.38% CAGR through 2031.

- By dosage form, capsules accounted for 36.24% of the United States brain health supplements market size in 2025, while softgels are forecast to expand at a 13.52% CAGR through 2031.

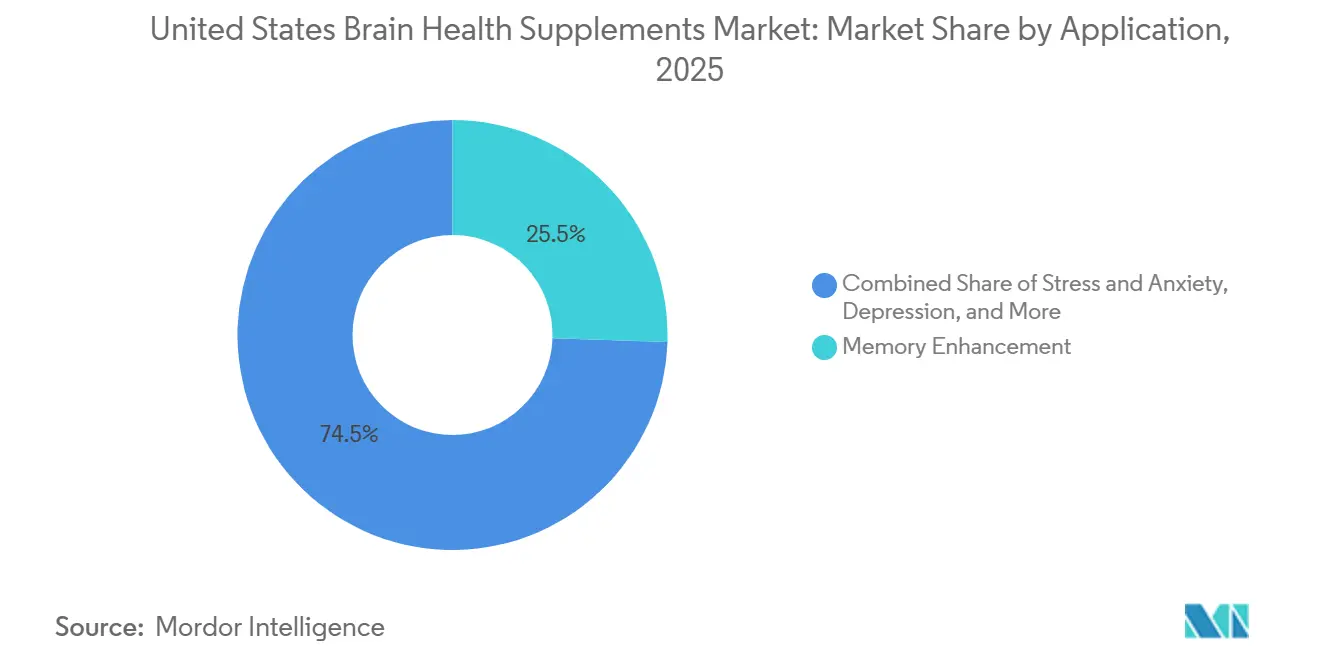

- By application, memory enhancement captured 25.52% of the United States brain health supplements market size in 2025, while stress and anxiety are expected to advance at a 12.25% CAGR through 2031.

- By distribution channel, pharmacies and drug stores led with 48.24% of the United States brain health supplements market share in 2025, while online sales are projected to rise at a 12.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Brain Health Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Mental Health And Cognitive Self-Care Awareness | +1.8% | National, with higher early adoption in Northeast and West Coast metros | Medium term (2-4 years) |

| Clean-Label Botanical And Nootropic Preference | +1.4% | National, concentrated in premium wellness corridors in California, New York, Washington, and Colorado | Medium term (2-4 years) |

| Rising Stress, Anxiety, And Sleep-Led Cognitive Complaints | +1.6% | Urban-dense metros including New York, San Francisco, Chicago, and Los Angeles | Short term (≤ 2 years) |

| Aging Baby Boomer Demand For Preventive Memory Maintenance | +2.0% | National, with highest concentration in Florida, Arizona, Texas, and Southeast retirement corridors | Long term (≥ 4 years) |

| DTC Nootropic Education, Personalized Quizzes, And Subscription Models | +1.0% | National, strongest in digitally engaged urban and suburban Millennial and Gen Z populations | Short term (≤ 2 years) |

| Polypharmacy Avoidance And Demand For Gentle Brain-Support Formats | +0.7% | National, with higher relevance in aging-population-heavy states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Mental Health and Cognitive Self-Care Awareness Among US Consumers

Mental health moved further into the wellness mainstream in 2025, and that shift continues to lift the United States brain health supplements market because consumers increasingly treat cognitive support as part of daily self-care rather than occasional intervention. Among women consumers, 65% actively sought products for mental well-being in 2025, and 94% of consumers said mental health was crucial to overall wellness, which broadens demand well beyond older memory-focused buyers[1]NielsenIQ, “Mental Health & Wellness in 2025,” NielsenIQ, nielseniq.com. Product activity followed that behavioral change, with 190 launches carrying brain health claims and 177 launches carrying cognitive sharpness positioning in 2024. This pattern matters because it widens the age profile of the category and pulls younger adults into the United States brain health supplements market for performance, clarity, and resilience rather than decline management alone. It also means brands can no longer rely on senior-focused messaging only, since the category now sits closer to everyday wellness routines than to occasional cognitive concern.

Clean-Label Botanical and Nootropic Preference in the US Premium Wellness Sector

Preference for clean-label products is strengthening product selection in the United States brain health supplements market, especially in premium channels where consumers are checking ingredient quality, origin, and testing standards more closely. Brands such as Mind Lab Pro, Thorne, and Pure Encapsulations have benefited from this shift by leaning on transparent formulas, standardized extracts, and third-party testing rather than broad lifestyle positioning alone. The effect is not only demand growth, because clean-label expectations also create a higher operating bar for smaller brands that want premium pricing without comparable proof. As a result, the brain health supplements industry is seeing more investment move toward validation, certification, and formulation discipline in order to defend premium shelf position.

Rising Stress, Anxiety, and Sleep-Led Cognitive Complaints in High-Pressure US Urban Centers

The fastest-growing application in the United States brain health supplements market is stress and anxiety, which is projected to rise at a 12.25% CAGR through 2031 as more consumers connect cognitive performance problems with stress load and poor sleep. In 2025, 58% of U.S. corporate workers said they used dietary supplements specifically to manage work-related stress, which shows how directly workplace pressure is feeding demand for cognitive support products. Ingredient trends also show this shift, with GABA sales up 561% through December 2024 and shilajit posting 40% Q1 sales growth at The Vitamin Shoppe in 2025, alongside continued strength in magnesium. This is pushing the category toward formulas that sit between focus support and sleep recovery, which narrows the old boundary between daytime cognition and nighttime restoration. The United States brain health supplements market therefore gains from a broader set of use cases, because stress, brain fog, mood strain, and sleep disruption are now being addressed through overlapping products rather than isolated ones.

Aging US Baby Boomer Demographic Seeking Preventive Memory Maintenance

Aging demographics remain a long-cycle support for the United States brain health supplements market because older adults are moving into preventive memory routines before major symptoms appear. The category is also drawing in adults earlier than past generations did, with the 45 to 55 age cohort becoming more active in preventive cognitive care. Nestlé Health Science’s BrainXpert clinical program shows why this matters, since the company began the COGNIKET-MCI trial across nearly 30 sites to study ketogenic ingredients as alternative brain energy sources in people with mild cognitive impairment, with completion expected in 2026 and 2027. That clinical direction brings medical nutrition and consumer supplementation closer together, which can lift price points and raise consumer expectations for evidence. It also gives the United States brain health supplements market a more stable demand base because older adults often value trust, physician comfort, and product credibility more than short-term promotional pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Efficacy Skepticism And Dose Standardization Gaps | -1.1% | National, amplified in markets with higher health literacy in the Northeast and West Coast | Medium term (2-4 years) |

| Strict FDA And FTC Regulatory Scrutiny On Cognitive Claims | -0.9% | National, with enforcement concentrated on brands with national retail distribution | Short term (≤ 2 years) |

| Delayed Or Subjective Benefits Limiting Repeat Purchase Rates | -0.8% | National, most acute in first-time buyer segments across DTC and pharmacy channels | Medium term (2-4 years) |

| Self-Medication Caution And Supplement-Drug Interaction Risk | -0.5% | National, concentrated in older demographic segments in Florida, Arizona, Texas, and the Southeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Efficacy Skepticism and Dose Standardization Gaps Across Key Active Ingredients

Efficacy skepticism remains one of the clearest restraints on the United States brain health supplements market because consumers and regulators are questioning whether marketed formulas reflect doses and outcomes seen in human research. Harvard Health noted that the evidence gap remains meaningful across much of the category, and the COSMOS multivitamin study was highlighted as one of the few controlled trials showing reliable episodic memory benefits, with an effect comparable to slowing cognitive aging by 2 years in adults aged 60 and older[2]Harvard Health Publishing, “Don't Buy Into Brain Health Supplements,” Harvard Medical School, health.harvard.edu. Sales performance also shows where skepticism is surfacing, with phosphatidylserine down 23.5% and ginkgo biloba down 12.1% in U.S. cognitive supplement sales through December 2024. Those declines suggest that legacy ingredient familiarity is not enough when consumers cannot connect product claims with strong finished-product evidence. Brands that are clearer on dose, testing, and expected outcomes are therefore better placed to gain trust in the United States brain health supplements market than those relying on broad reputation alone.

Strict FDA and FTC Regulatory Scrutiny on Cognitive Structure-Function Claims

Regulatory pressure is a real operating constraint in the United States brain health supplements market because unsupported memory, clarity, and focus claims are now drawing visible enforcement attention. In 2024, the National Advertising Division found that BrainPack Daily Adult Gummy Vitamins overstated cognitive performance benefits in claims around memory, clarity, and focus, and it recommended that those claims be discontinued. The FTC then won its December 2024 case against Quincy Bioscience, requiring the maker of Prevagen to stop making memory improvement claims that were not backed by rigorous evidence. This changes competition because smaller brands face higher compliance costs when they lack legal and regulatory resources, while large brands must also be more careful about how they translate ingredient science into consumer-facing language. The result is a United States brain health supplements market where product differentiation can no longer lean heavily on aggressive cognition claims unless brands are prepared to support them with stronger validation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Herbal Extracts Anchor Market, Vitamins and Minerals Build Momentum

Herbal extracts led the United States brain health supplements market with 43.31% of the United States brain health supplements market share in 2025, making them the core product group in the category. That leadership reflects continued consumer interest in plant-derived cognitive support and in familiar herbal names such as bacopa monnieri, ginkgo biloba, ashwagandha, and lion’s mane mushroom. The segment still contains visible internal rotation, since ginkgo biloba sales declined 12.1% through December 2024 while mushroom-based cognitive ingredients posted meaningful gains, showing that buyers are not treating botanical products as interchangeable. This keeps herbal extracts important to the United States brain health supplements market, but it also raises the need for better proof, clearer positioning, and stronger differentiation within the botanical set.

Vitamins and minerals is projected to be the fastest-growing product type, with United States brain health supplements market size for this segment expected to expand at a 12.38% CAGR between 2026 and 2031. Momentum here is being driven by renewed demand for B-vitamin complexes, magnesium threonate, and longevity-linked ingredients such as NAD+ precursors. In tracked U.S. sales through December 2024, vitamin B12 rose 720% and vitamin B3 rose 609%, while NAD+ search volume at The Vitamin Shoppe increased 500% in 2025, which shows how strongly the category is benefiting from longevity and energy messaging. Harvard’s coverage of the COSMOS multivitamin findings also gives this group a more credible evidence point than many other ingredient classes have enjoyed in the past. Natural molecules such as omega-3 fatty acids, phosphatidylserine, and citicoline still occupy a premium layer within the broader product set, especially among practitioner-oriented brands that sell credibility as much as formulation complexity.

By Dosage Form: Capsules Lead, Softgels Emerge as the Premium Bioavailability Play

Softgels is the fastest-growing dosage form in the United States brain health supplements market, and the segment is forecast to rise at a 13.52% CAGR through 2031. Demand is improving because softgels fit well with lipid-based cognitive ingredients, support a more premium user experience, and appeal to consumers who are paying closer attention to how a product is delivered, not only what appears on the label. The format also fits older consumers well because it is generally perceived as easier to swallow than harder solid forms. This gives softgels a strong role in the United States brain health supplements market as brands try to connect efficacy messaging with convenient daily use.

Capsules remained the leading dosage form and accounted for 36.24% of the United States brain health supplements market size in 2025. Their lead came from manufacturing efficiency, consumer familiarity, and their ability to carry multi-ingredient nootropic stacks without major format constraints. At the same time, format diversification is becoming more visible, with searches for creatine gummies rising 1,300% at The Vitamin Shoppe in 2025 and liquid vitamin sales there climbing 50%, which shows that buyers are increasingly willing to move beyond the capsule default. Tablets and powders still serve practical roles through pharmacy, mass retail, and flexible dosing use cases, while liquids and shots are gaining ground in premium direct-to-consumer settings. BEVIMI’s May 2026 launch of Uno Protect, a patent-pending liquid formulation with 10 clinically studied actives, shows how newer delivery formats are being used to reposition the United States brain health supplements market beyond traditional oral routines.

By Application: Memory Enhancement Holds Share Lead, Stress and Anxiety Accelerates Fastest

Memory enhancement held the largest application position in the United States brain health supplements market with a 25.52% share in 2025. The segment is supported by 2 groups at once, older adults looking for preventive maintenance and working-age consumers trying to manage digital fatigue, overload, and stress-linked memory lapses. Search activity confirms that memory remains a strong entry point into the category, with Prevagen ranking as the most searched memory and focus supplement brand in the United States and drawing 272,900 average monthly searches from December 2023 to November 2024[3]NutraIngredients, “The Evolution of Cognitive Health Supplements Market,” NutraIngredients, nutraingredients.com. Attention and focus products also continue to overlap with productivity-led purchasing among younger adults, which keeps memory enhancement central to the United States brain health supplements market even as the user base broadens.

Stress and anxiety is the fastest-growing application and is expected to record a 12.25% CAGR through 2031. This reflects a market shift where stress-related cognitive complaints are increasingly being treated as supplement-addressable rather than purely clinical concerns. The adjacent mood and sleep-recovery categories are adding to that shift because more products now combine ingredients such as GABA, magnesium, ashwagandha, and L-theanine to address multiple symptoms in one formulation. NielsenIQ’s 2025 finding that 94% of consumers viewed mental health as crucial to overall wellness helps explain why these applications are moving faster, since they draw from a large consumer base with broad everyday relevance. This makes the United States brain health supplements market less dependent on a single cognitive use case and more responsive to the wider mental wellness conversation.

By Distribution Channel: Pharmacy Leads on Trust, Online Leads on Growth

Online sales is the fastest-growing distribution channel in the United States brain health supplements market and is projected to grow at a 12.82% CAGR through 2031. The channel is benefiting from direct-to-consumer education, quiz-based product selection, recurring subscription models, and the rising role of social commerce in supplement discovery. In 2025, 55% of U.S. consumers purchased supplements through social media or live-stream platforms, and 40% said they were willing to accept AI-generated product recommendations, which supports stronger digital conversion for brands with advanced customer acquisition systems. These behaviors give online players more room to personalize, retain, and cross-sell, which is why the United States brain health supplements market continues to see channel power shift toward digital models.

Pharmacies and drug stores retained the largest channel position, accounting for 48.24% of the United States brain health supplements market share in 2025. Trust remains the main advantage in this channel because shoppers often associate the pharmacy setting with advice, safety, and compatibility with existing medication use. That matters especially for older adults, who are more likely to seek pharmacist comfort before starting cognitive products. Supermarkets and hypermarkets are also widening their role, particularly as the category extends into gummies, functional foods, and snack-adjacent formats. MOSH High Protein’s expansion into more than 2,000 Target stores in May 2026 shows how the United States brain health supplements market is reaching broader retail traffic and moving closer to mainstream food and wellness shopping habits.

Geography Analysis

The brain health supplements market in the United States is national in reach, but demand is not developing at the same pace across all regions. Premium wellness corridors such as California, New York, Washington, and Colorado tend to adopt nootropics, adaptogens, and clean-label formulations earlier than the rest of the country, which aligns with stronger premium wellness activity and greater interest in ingredient quality. West Coast metros continue to matter because they combine high-income consumers, dense digital wellness communities, and quicker acceptance of newer cognitive formats. Urban centers such as New York, San Francisco, Chicago, and Los Angeles also fit the fastest-growing use cases in the United States brain health supplements market, since stress, anxiety, sleep disruption, and attention fatigue are closely tied to the product demand patterns.

Florida, Arizona, Texas, and the broader Southeast remain important to the United States brain health supplements market because these areas carry a heavier concentration of older adults who are more likely to seek preventive memory support. That supports stronger demand for clinically framed products, pharmacy-led purchasing, and messaging tied to long-term cognitive maintenance rather than short-term performance. The Northeast continues to stand out for premium direct-to-consumer and practitioner-style purchasing, where consumers appear more willing to pay for research-backed formulations and higher testing standards. The Midwest is a meaningful expansion zone because wider pharmacy access and mainstream retail exposure can help the category move beyond early-adopter coastal centers. Geography in the United States brain health supplements market therefore affects product mix and channel mix more than it changes the national direction of demand.

Digital engagement is now reducing some of the regional gaps that used to separate early-adopter markets from later-moving ones. Online discovery, quiz-based selling, and social commerce are making it easier for brands to scale beyond coastal wellness hubs and reach suburban and secondary markets more efficiently. At the same time, national enforcement activity means claims discipline has to travel with brands wherever they sell, especially when products gain mass retail distribution across the country. The result is a United States brain health supplements market where regional variation shapes the speed of adoption, the preferred claims, and the strongest channel, but not the overall national growth path.

Competitive Landscape

The United States brain health supplements market remains moderately concentrated, with more than 20 active participants and a mix of consumer health incumbents, pharmacy-heavy brands, and specialized nootropic players competing across price points and channels. Large names in the category include Reckitt Benckiser, Nestlé Health Science, Nature Made, Nature’s Bounty, Quincy Bioscience, Mind Lab Pro, Neurohacker Collective, and HVMN, which gives the market both scale-driven and specialist-led competition. The top 5 players accounted for a significant share of revenue in 2025, leaving a meaningful share in the hands of mid-market and direct-to-consumer brands. That structure keeps the United States brain health supplements market open enough for new entrants to gain traction, but not so fragmented that scale, trust, and retail access stop mattering.

Competition is now dividing into 3 clear models in the United States brain health supplements market. Pharmaceutical-heritage companies compete on credibility, shelf access, and broad retail trust, while direct-to-consumer nootropic specialists compete on ingredient complexity, transparency, and subscription retention. Mid-tier brands sit between those positions and often use third-party testing, practitioner alignment, or standardized extracts to justify higher pricing without the same distribution power. Clinical validation is also becoming more important because regulatory pressure has made unsupported cognitive claims harder to sustain, and because consumers are showing more skepticism toward broad promise-based branding. Pricing remains uneven across the United States brain health supplements market, with premium nootropic stacks and medically framed products coexisting beside lower-priced multivitamin and mass-market offerings, which keeps willingness to pay highly segmented.

Strategic activity is picking up as larger companies try to secure stronger positions in the United States brain health supplements market. Unilever’s acquisition of Onnit in 2024 showed that major consumer goods infrastructure is moving into a category that had previously been led more heavily by wellness-focused specialists. Herbalife’s March 2026 agreement to acquire Bioniq’s personalized supplement assets points to biomarker-driven personalization as a competitive direction with more commercial value ahead. BEVIMI’s May 2026 launch of a patent-pending liquid formula adds a different signal, since it shows that delivery technology and formulation intellectual property are becoming more relevant in the United States brain health supplements market than they were in earlier, branding-led phases. White-space opportunities remain strongest around clinically credible direct-to-consumer brands and around hybrid formats that push cognitive support beyond the standard capsule routine.

United States Brain Health Supplements Industry Leaders

Quincy Bioscience

Reckitt Benckiser Group PLC

NOW Foods

Nature Made (Pharmavite)

Jarrow Formulas, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: MOSH, the brain health nutrition brand co-founded by Maria Shriver and Patrick Schwarzenegger, raised USD 13 million in a Series A round led by Main Street Advisors and expanded its high-protein brain health product line into more than 2,000 Target stores nationwide, the brand's largest retail expansion to date and a signal that mass-market grocery is actively embracing the brain health supplement category.

- May 2026: BEVIMI launched Uno Protect, a patent-pending liquid brain health formulation combining 10 clinically studied actives in a shelf-stable single serving, utilizing a proprietary liquid stabilization technology licensed across the company's product portfolio. The founding team includes former operating leadership from Thorne HealthTech and the former Chief Scientific Officer of Tempus, positioning the product at the intersection of clinical-grade formulation and DTC distribution.

United States Brain Health Supplements Market Report Scope

As per the scope of the report, brain health supplements are products formulated to support and enhance cognitive functions such as memory, focus, mental clarity, and overall brain vitality. They typically contain ingredients like vitamins, minerals, herbs, amino acids, and other compounds believed to promote neuronal health, improve blood flow to the brain, reduce inflammation, and support neurotransmitter activity. These supplements are used to help maintain cognitive performance, potentially delay age-related decline, and support mental well-being.

The United States brain health supplements market is segmented by product type, dosage form, application, and distribution channel. By product type, the market includes natural molecules, herbal extracts, and vitamins and minerals. By dosage form, it is categorized into capsules, tablets, softgels, gummies, powders, liquids and shots, and other forms. By application, the market covers memory enhancement, attention and focus, stress and anxiety, sleep and recovery, depression and mood, and other uses. By distribution channel, it is divided into pharmacies and drug stores, online, supermarkets and hypermarkets, and other channels. For each segment, the market size and forecast are provided in terms of value (USD).

| Natural Molecules |

| Herbal Extracts |

| Vitamins and Minerals |

| Capsules |

| Tablets |

| Softgels |

| Gummies |

| Powders |

| Liquids and Shots |

| Other Dosage Forms |

| Memory Enhancement |

| Attention and Focus |

| Stress and Anxiety |

| Sleep and Recovery |

| Depression and Mood |

| Other Applications |

| Pharmacies and Drug Stores |

| Online |

| Supermarkets and Hypermarkets |

| Other Distribution Channels |

| By Product Type | Natural Molecules |

| Herbal Extracts | |

| Vitamins and Minerals | |

| By Dosage Form | Capsules |

| Tablets | |

| Softgels | |

| Gummies | |

| Powders | |

| Liquids and Shots | |

| Other Dosage Forms | |

| By Application | Memory Enhancement |

| Attention and Focus | |

| Stress and Anxiety | |

| Sleep and Recovery | |

| Depression and Mood | |

| Other Applications | |

| By Distribution Channel | Pharmacies and Drug Stores |

| Online | |

| Supermarkets and Hypermarkets | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the 2026 value of the United States brain health supplements space?

The United States United States brain health supplements market reaches USD 3.88 billion in 2026 and is projected to reach USD 6.32 billion by 2031 at a 10.25% CAGR.

Which product type leads U.S. demand for cognitive supplements?

Herbal extracts led with 43.31% share in 2025, supported by continued demand for plant-based ingredients such as bacopa, ashwagandha, ginkgo, and lion's mane.

Which application is growing fastest in U.S. brain health supplements?

Stress and anxiety is the fastest-growing application, with a projected 12.25% CAGR through 2031 as buyers connect cognitive strain with work stress and poor sleep.

Why are online sales rising so quickly for U.S. cognitive support products?

Online sales is forecast to grow at 12.82% CAGR through 2031 because social commerce, AI-based recommendations, quizzes, and subscriptions are making discovery and repeat purchase easier.

What is the largest channel for brain health supplements in the United States?

Pharmacies and drug stores remained the largest distribution channel in 2025 with 48.24% share, helped by trust, clinical adjacency, and stronger relevance for older consumers.

Page last updated on: