Neurodiagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

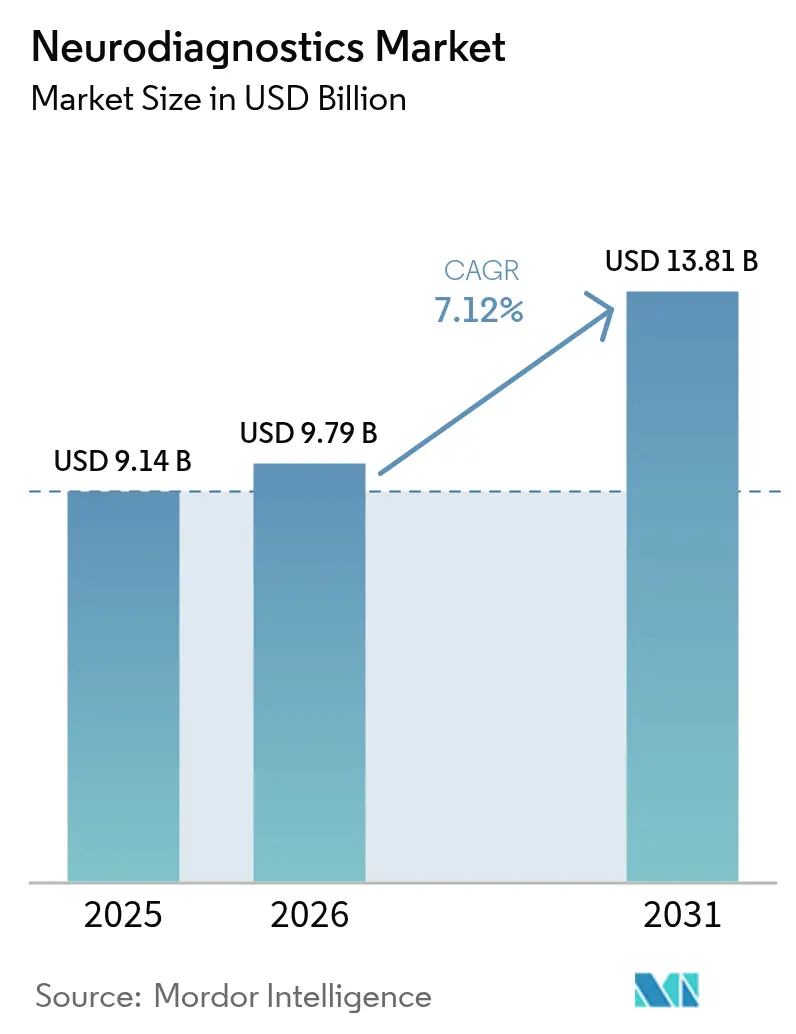

| Market Size (2026) | USD 9.79 Billion |

| Market Size (2031) | USD 13.81 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurodiagnostics Market Analysis by Mordor Intelligence

Neurodiagnostics market size in 2026 is estimated at USD 9.79 billion, growing from 2025 value of USD 9.14 billion with 2031 projections showing USD 13.81 billion, growing at 7.12% CAGR over 2026-2031. This steady expansion mirrors the global shift from reactive neurological care to proactive, precision-driven assessments that rely on artificial intelligence, blood-based biomarkers and minimally invasive point-of-care technologies. An aging population, the clinical urgency to diagnose neurodegenerative disorders earlier, and government-backed “neurotech moonshot” programs continue to stimulate capital investment, accelerate regulatory pathways and push traditional diagnostic workflows toward cloud-enabled, data-centric models. At the same time, the Neurodiagnostics market experiences intense competition as imaging multinationals add AI analytics, while AI-native start-ups and biomarker specialists pioneer disruptive solutions that bypass fixed infrastructure. As these structural forces converge, decision-makers in healthcare systems, med-tech manufacturing and life-science research recalibrate strategies around scalability, sustainability and workforce-efficiency, positioning the Neurodiagnostics market for resilient long-term growth.

Key Report Takeaways

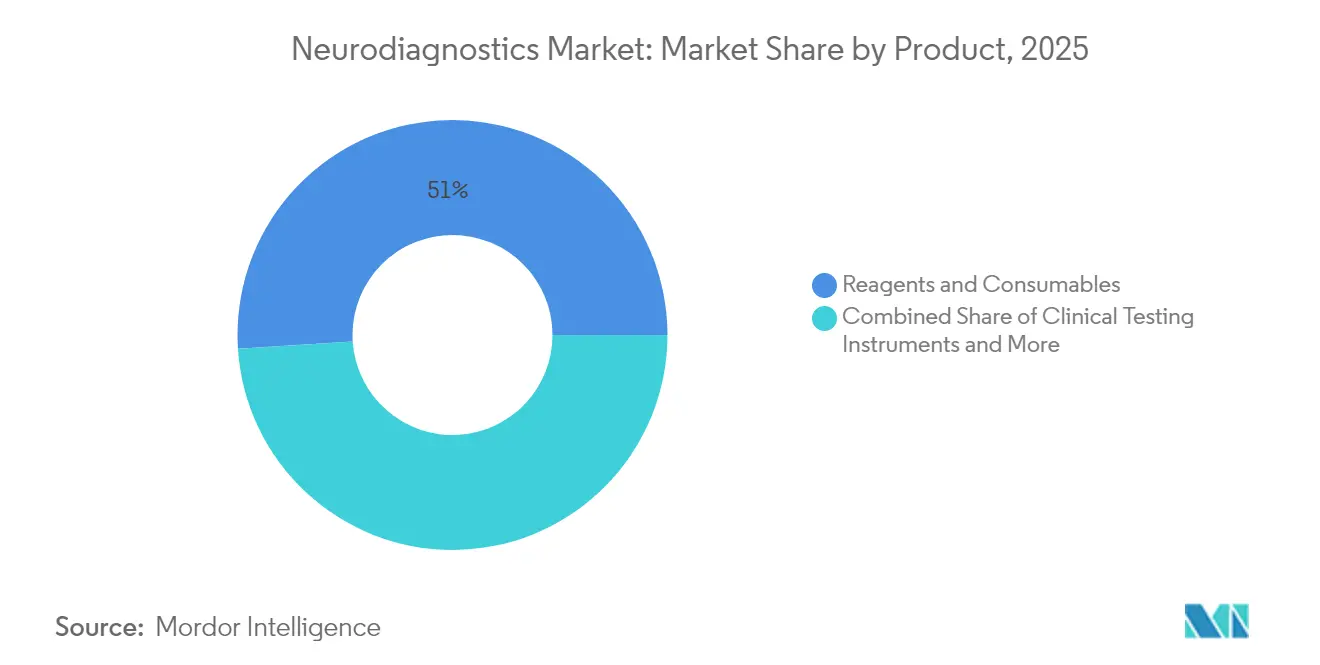

- By product, reagents & consumables captured 51.02% of the Neurodiagnostics market share in 2025; gene therapy is projected to expand at a 9.28% CAGR through 2031.

- By technology, neuroimaging platforms led with 68.10% revenue in 2025, whereas neuroinformatics & AI analytics platforms are advancing at an 11.45% CAGR to 2031.

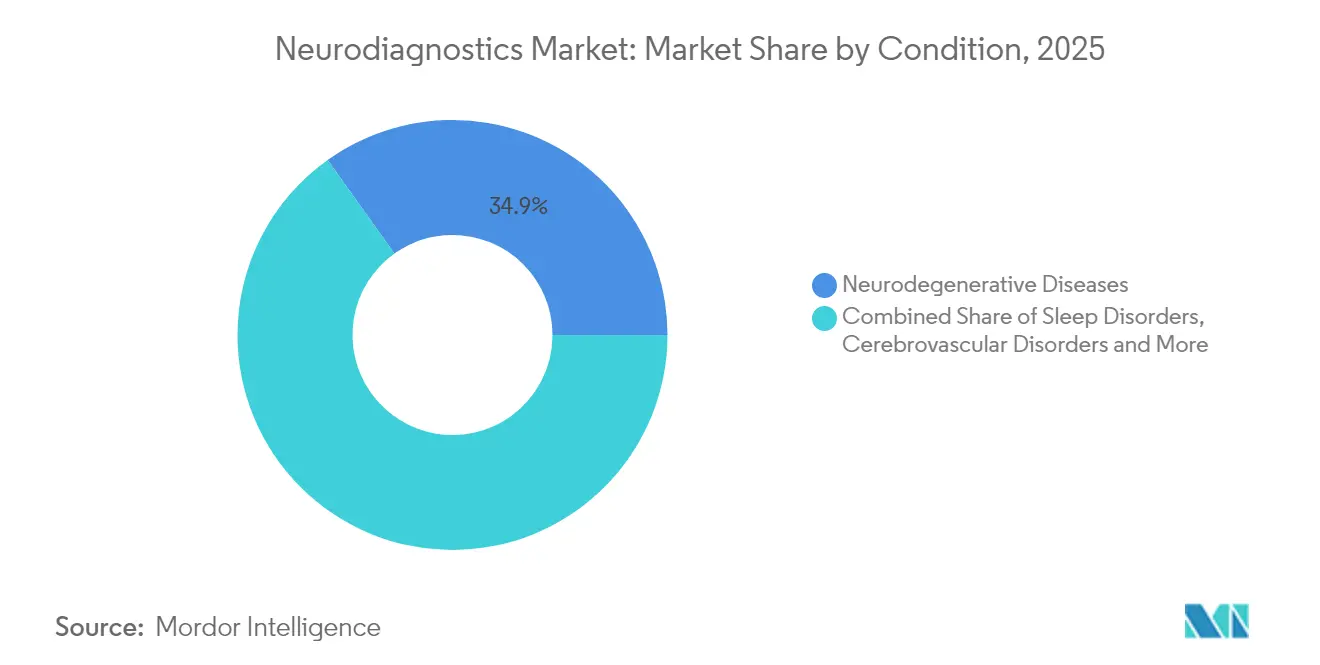

- By condition, neurodegenerative diseases accounted for 34.86% of the 2025 revenue base, while sleep-disorder diagnostics are forecast to grow at a 10.45% CAGR through 2031.

- By end user, hospitals & surgical centers held 59.55% of 2025 revenues; ambulatory care & emergency settings are set to rise at a 10.26% CAGR to 2031.

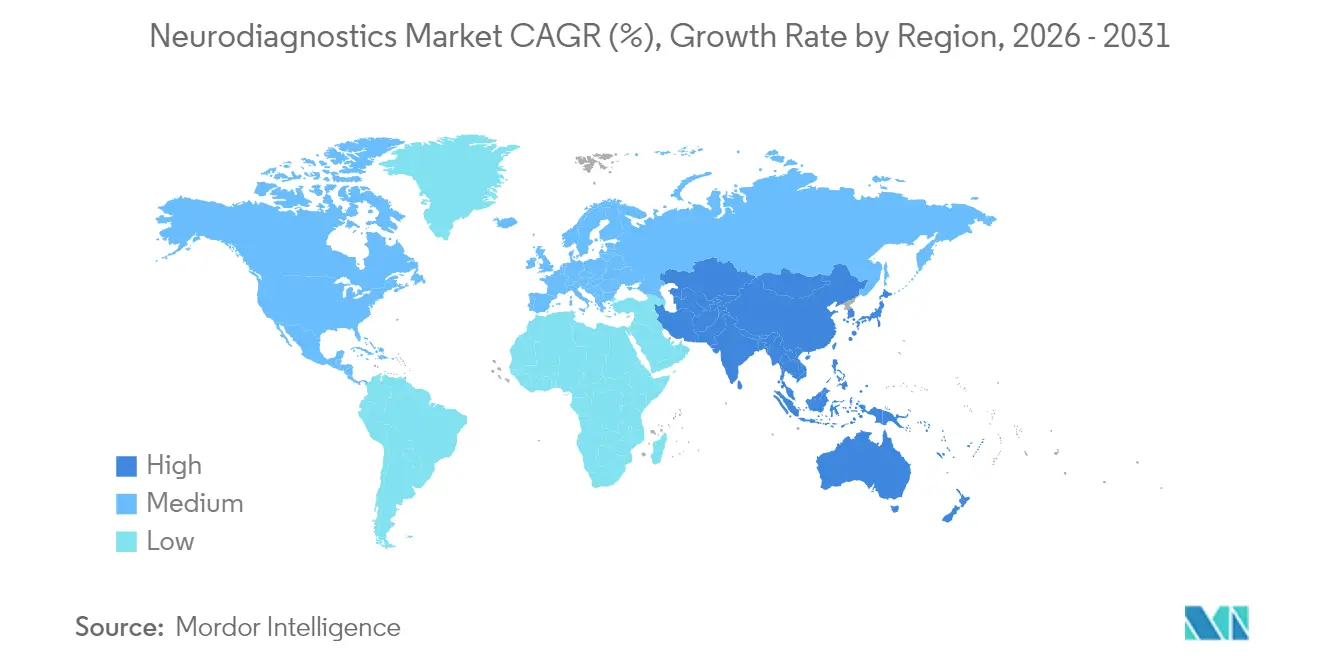

- By geography, North America commanded 36.00% of 2025 revenue, yet Asia-Pacific is projected to record the highest regional CAGR at 9.28% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurodiagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of neurological disorders | +1.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Growing adoption of novel diagnostic imaging technologies | +1.5% | North America, EU, rapidly in APAC | Medium term (2-4 years) |

| Rising geriatric population and longevity | +1.2% | Global, acute in Japan and Germany | Long term (≥ 4 years) |

| Emergence of blood-based NFL and other neurological biomarkers | +1.0% | North America, EU, expanding to APAC | Medium term (2-4 years) |

| Rapid expansion of point-of-care EEG wearables in emerging markets | +0.8% | APAC core, spill-over to MEA & Latin America | Short term (≤ 2 years) |

| Government neurotech moonshot funding & public-private consortia | +0.6% | North America, EU, UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Novel Diagnostic Imaging Technologies

Artificial-intelligence-enabled scanners now shorten MRI sessions to under an hour while automating protocol selection, slice positioning and reconstruction, raising throughput without compromising image quality[1]Philips, “Philips Accelerates Precise Imaging with Unique AI Technologies in MRI to Improve Patient Outcomes,” philips.com. Dual-engine reconstruction algorithms deliver noise-reduced, high-resolution neuro images that support quantitative tissue volume mapping and early lesion detection. Vendors are prioritizing helium-free magnets that require as little as 7 liters of coolant, cutting lifetime operating costs and easing procurement barriers in cash-strapped health systems. Competitive pressure intensifies as Canon Medical and United Imaging roll out comparable AI-ready platforms, forcing incumbents to accelerate upgrade cycles. For providers, these enhancements translate into higher scanner utilization, faster clinical decisions and improved patient satisfaction, all of which reinforce purchasing intent and embed AI workflows at the core of the Neurodiagnostics market.

Emergence of Blood-Based NFL and Other Neurological Biomarkers

Plasma assays targeting phosphorylated tau217, neurofilament-light chain and MTBR-tau243 are redefining neurological work-ups by offering non-invasive alternatives to lumbar puncture and PET imaging, with diagnostic accuracy above 85% in multi-center trials. Large diagnostic firms are partnering to co-develop high-throughput assays for automated immuno-analyzers, unlocking economies of scale and reducing per-test costs. The U.S. FDA’s breakthrough-device pathway accelerates review cycles, yet payer hesitation persists; reimbursement rates for plasma-based Alzheimer’s panels still lag behind legacy modalities. Despite pricing doubts, neurologists increasingly integrate biomarker panels into memory-clinic protocols, leading to earlier referrals, stratified trial enrollment and personalized therapeutics. As validation expands to Parkinson’s, ALS and traumatic brain injuries, biomarker developers gain a multi-disease revenue stream that underpins the long-run expansion of the Neurodiagnostics market.

Rising Geriatric Population and Longevity

By 2030, people aged 65 years and above will exceed 1 billion globally, intensifying demand for cognitive-health monitoring and neurodegenerative screening. Nations with advanced longevity—Japan, Germany, Italy—are funding preventive neurology programs aimed at delaying disease onset and reducing social-care costs. Public hospitals respond by expanding memory clinics and integrating remote EEG and brain-vital-sign platforms into community health centers. On the supply side, device makers are miniaturizing headsets and optimizing user interfaces to accommodate elderly populations with limited mobility and dexterity. Investment flows into purpose-built neurology centers, such as the USD 1.1 billion Cleveland Clinic Neurological Institute, create anchor customers for premium scanners and analytics subscriptions. Collectively, these shifts embed age-centric design and service models into every layer of the Neurodiagnostics market value chain.

Rapid Expansion of Point-of-Care EEG Wearables in Emerging Markets

Portable EEG headsets fitted with dry, soft-tip electrodes are removing long-standing logistical barriers tied to gel application and specialist set-up time, enabling seizure triage in emergency departments and rural clinics. Implantable continuous EEG systems extend monitoring windows from hours to months, capturing low-frequency seizure events and refining drug-response algorithms. In-ear and behind-the-ear devices now generate high-fidelity data suitable for sleep-stage scoring, supporting the fast-growing home-sleep-testing market. Academic consortia in India and Brazil apply graph attention networks to ultra-low-cost headsets, pushing the marginal exam cost below USD 10 and broadening access across public-health programs. Regional distributors leverage tele-neurology networks to route data to urban specialists, shrinking diagnostic backlogs and accelerating therapy initiation in underserved settings. The quick uptake in Asia-Pacific and South America underscores the decentralization trend reshaping the Neurodiagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance costs of advanced neurodiagnostic systems | -1.2% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Shortage of trained neurotechnologists & neuroradiologists | -0.9% | North America, EU, expanding globally | Medium term (2-4 years) |

| Reimbursement uncertainty for novel biomarker and AI-based tests | -0.7% | North America, EU | Short term (≤ 2 years) |

| Data privacy & cybersecurity concerns with cloud-connected brain data | -0.4% | Global, regulations vary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Advanced Neurodiagnostic Systems

Total ownership expenses for a helium-cooled 3-Tesla MRI can surpass USD 3 million when factoring installation, shielding and annual service contracts, an outlay that strains mid-size providers in Latin America and Southeast Asia. Although helium-free magnets cut running costs by 20-30%, the upfront premium still inhibits adoption. Multisite hospital systems therefore centralize high-end scanners, compelling peripheral clinics to refer patients and elongating care pathways. Laboratory automation promises long-term savings, yet “dark labs” require robotic track lines, AI middleware and redundant cybersecurity layers, with deployment estimates ranging between USD 10 million and USD 15 million for a 500-test-per-hour facility. Without subsidized financing or risk-sharing contracts, many regional providers postpone modernization, slowing the penetration curve of premium modalities within the Neurodiagnostics market.

Shortage of Trained Neurotechnologists & Neuroradiologists

The United States projects a 19% shortfall in neurologists by 2025, while vacancy rates for EEG technologists already exceed 12% at tertiary hospitals[2]Neurology Clinical Practice, “Functional Seizure Clinics,” neurology.org. European associations cite similar gaps, particularly in smaller states where pay differentials drive outbound migration. Provider networks respond by launching cross-training programs for ICU nurses and respiratory therapists, yet certification timelines can stretch 18 months, prolonging staffing bottlenecks. AI decision-support and auto-triage tools ease workload, but regulatory frameworks mandate human sign-off, limiting immediate productivity gains. Remote reading hubs offer interim relief, routing scans and EEG traces to central specialists; however, reimbursement for tele-interpretation remains patchy. Workforce constraints therefore inflate turnaround times and reduce effective scanner utilization, tempering growth prospects for the Neurodiagnostics market in otherwise high-demand regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Drive Revenue While Gene Therapy Accelerates

Reagents & consumables produced recurrent cash flows equal to 51.02% of 2025 revenue as clinicians increasingly order serial blood-based panels for neurofilament-light chain, phosphorylated tau and GFAP monitoring. Instrument vendors strategically bundle proprietary cartridges with middleware analytics, cementing laboratory stickiness and smoothing quarterly revenue visibility in the Neurodiagnostics market. Clinical testing instruments—chiefly portable EEG systems, handheld transcranial Doppler units and point-of-care biomarker analyzers—form the second-largest contributor, propelled by hospital attempts to shorten emergency-department dwell times. Diagnostic imaging systems remain mission-critical, yet ASP pressure intensifies as capital budgets shift toward software subscriptions, cloud storage and cybersecurity upgrades.

Gene-therapy-linked diagnostics, though representing a small base, are scaling at a 9.28% CAGR through 2031 on the back of brain-computer-interface trials and CRISPR-mediated interventions for inherited ataxias. Neurodiagnostics market size for gene-therapy-companion tests is forecast to surpass USD 1.07 billion by 2031, supported by the need to genotype patients, monitor vector biodistribution and verify on-target protein restoration. Vendors such as Beckman Coulter offer RUO panels covering p-Tau217 and GFAP, creating de-facto standards for biomarker endpoints in clinical trials. As regulatory agencies finalize guidelines on surrogate markers and long-term safety monitoring, the consumables franchise will deepen, reinforcing the product-portfolio diversity vital for sustainable Neurodiagnostics market growth.

By Technology: AI Analytics Disrupts Neuroimaging Dominance

Neuroimaging technologies preserved a commanding 68.10% revenue share in 2025, underpinned by a global installed base exceeding 45,000 MRI and CT scanners dedicated to neurological applications. Generative reconstruction algorithms now deliver sub-millimeter isotropic resolution, enhancing lesion detectability and surgical-planning precision. Vendor-neutral analytic suites integrate DICOM-level segmentation with cognitive-decline prediction, further extending scanner reach into preventive neurology.

Neuroinformatics & AI analytics platforms, although starting from a smaller revenue base, are expanding at 11.45% CAGR and are projected to account for a double-digit share of the Neurodiagnostics market size by 2031. Cloud-deployed seizure-prediction engines achieve area-under-curve scores of 0.97, facilitating risk-stratified care pathways. Multilingual natural-language-processing modules mine electronic health-records for subtle cognitive changes, prompting earlier imaging referrals. As GE Healthcare layers AWS native-services into its Edison platform, competition pivots from hardware specifications to algorithmic performance, cybersecurity credentials and clinical-trial validation data sets, fundamentally re-ranking supplier differentiation in the Neurodiagnostics market.

By Condition: Sleep Disorders Emerge as Growth Driver

Neurodegenerative-disease diagnostics delivered 34.86% of 2025 revenue owing to higher Alzheimer’s prevalence and broadened access to plasma-based biomarker panels. MRI volumetry and amyloid-PET remain cornerstones, but laboratories increasingly combine imaging with plasma p-Tau217, cutting diagnostic latency and enabling therapy initiation during prodromal stages. Cerebrovascular-stroke work-ups benefit from AI-enhanced CT angiography that flags occlusions within three minutes, slashing door-to-needle times and improving patient outcomes.

Sleep-disorder diagnostics, historically limited to specialist labs, are scaling at a 10.45% CAGR as single-lead ECG deep-learning algorithms classify sleep stages with 88–90% accuracy in home environments. Newly cleared headset wearables transmit raw EEG to cloud platforms for REM-behavior disorder detection, addressing a patient population exceeding 80 million globally. Given reimbursement parity with in-lab polysomnography in several U.S. states, payer acceptance propels adoption in primary-care and cardiology practices, broadening the Neurodiagnostics market footprint in behavioral health and chronic-disease management.

By End User: Ambulatory Care Transforms Service Delivery

Hospitals & surgical centers retained 59.55% revenue dominance in 2025 as comprehensive care models demand co-located imaging, laboratory and neurosurgical capabilities. Center-of-excellence strategies consolidate high-complexity cases, supporting multi-modality equipment investments and specialized staff recruitment. Diagnostic labs exploit high-volume biomarker testing to win send-out business from community clinics, while academic institutes secure grant funding to trial novel AI algorithms and investigational tracers.

Ambulatory care & emergency settings, however, record a 10.26% CAGR as point-of-care EEG, handheld MRI and blood-based biomarker kits migrate advanced capabilities to urgent-care chains and mobile stroke units. Functional seizure clinics embedded within epilepsy centers reduce inpatient referrals by 18%, demonstrating cost-containment potential. Tele-consult hubs allow community nurses to acquire EEG and push data to metropolitan neurophysiologists, expanding service coverage in workforce-scarce regions. As reimbursement frameworks evolve to favor outpatient diagnostics, provider capital shifts toward scalable, software-defined solutions that reinforce the decentralized growth trajectory of the Neurodiagnostics market.

Geography Analysis

North America remained the revenue leader with 36.00% share in 2025, propelled by NIH BRAIN Initiative grants totaling USD 321 million in 2025 that cushion academic-industry collaboration pipelines. U.S. payers continue to reimburse MRI and bio-assay bundles under value-based-care pilots, encouraging integrated diagnostic algorithms within accountable-care organizations. Canada, through Pan-Canadian AI strategy funds, supports provincial tele-neurology portals, while Mexico’s private hospitals import portable EEG headsets to close specialist gaps.

Europe sustains high adoption due to robust universal healthcare financing and stringent but predictable CE-mark pathways. Germany refits radiology departments with helium-free scanners to align with sustainability targets, and its aging demographic keeps demand for neurodegenerative screening elevated. The U.K.’s Advanced Research and Invention Agency awarded USD 69 million to precision neurotechnology projects, sparking venture activity in Oxford and Cambridge clusters. Mediterranean markets improve access to plasmapheresis-based biomarker assays through EU solidarity funds, yet workforce shortages slow implementation, tempering Neurodiagnostics market penetration in rural areas.

Asia-Pacific, registering the fastest pace at 9.28% CAGR, benefits from China’s 28% medtech expansion and a strategic pivot toward high-end imaging and AI platforms led by United Imaging and Mindray. Japan’s healthcare-2035 roadmap embeds neuro-preventive screening into annual wellness checks, driving bulk procurement of EEG wearables for municipal clinics. India’s National Digital Health Mission subsidizes cloud PACS and tele-EEG gateways, unlocking tier-II city demand. South Korea aligns reimbursement with AI-augmented imaging policy, whereas Australia’s Medicare funds home-sleep studies, accelerating sleep-disorder diagnostics adoption. Collectively, these policy levers make the region the principal incremental volume contributor to the global Neurodiagnostics market.

Competitive Landscape

The competitive arena shows moderate consolidation as Siemens Healthineers, GE Healthcare and Philips collectively anchor imaging hardware, service contracts and installed-base upgrades. Siemens targets 6-8% annual growth via its “New Ambition” strategy that expands precision-therapy and digital-diagnostics portfolios, thereby stretching platform synergies across oncology and neurology. GE leverages cloud partnerships with AWS to inject generative AI into routine workflows, enhancing decision-support and optimizing scanning protocols in real time. Philips positions its SmartSpeed Precise dual-AI engine as a differentiator, bundling workflow oracles and helium-free sustainability narratives to capture green-procurement budgets.

Start-ups specializing in biomarker assays and AI-only software steal mind-share by promising hospital-system ROI without heavy capital layouts. Lantheus’ USD 350 million acquisition of Life Molecular Imaging underscores incumbent appetite for tracer portfolios that complement existing imaging franchises. Partnership intensity escalates; Philips’ joint work with NVIDIA to co-develop foundation models demonstrates how tech giants with premium GPU stacks have become indispensable allies for rapid algorithm training.

Meanwhile, full-automation “dark labs” and direct-to-consumer neuro-wellness platforms challenge incumbent service lanes. Large reference labs pilot robotic halls that can process 50,000 biomarker tests daily, reducing manpower by 40% and reshaping cost curves. Natus, Nihon Kohden and other electrophysiology majors defend share by extending subscription bundles that combine hardware, cloud analytics and managed staffing, signaling a shift from transactional equipment sales to lifetime-value revenue streams within the Neurodiagnostics market.

Neurodiagnostics Industry Leaders

Siemens Healthineers

Thermo Fisher Scientific, Inc

GE Healthcare

Koninklijke Philips N.V.

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Natus Medical unveiled BrainWatch, a point-of-care EEG platform engineered for critical-care environments.

- April 2025: Epiminder received FDA authorization for Minder, the first U.S.-approved implantable continuous EEG device aimed at drug-resistant epilepsy patients.

Global Neurodiagnostics Market Report Scope

As per the scope of the report, Neurodiagnostics are tests and imaging procedures that are performed to diagnose problems with the brain, nervous system, and sleep habits of humans. Neurodiagnostic testing includes two types of imaging tests or scans (Example: X-ray, CT scan, MRI scan, PET scan) and electrical impulse detection (Example: EEG, EMG). Neurodiagnostic testing may be conducted as part of a neurological exam that involves the monitoring and analysis of the nervous system, which will enable the efficient initiation of treatment procedures. The market is segmented By Product Type (Clinical Testing Instruments, Diagnostic and Imaging Systems, Reagents, and Consumables), End-user (Hospitals, Diagnostic Laboratories, Imaging Centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Reagents & Consumables |

| Clinical Testing Instruments |

| Diagnostic & Imaging Systems |

| Neuroimaging Technologies |

| In-Vitro Diagnostics |

| Neuroinformatics & AI Analytics Platforms |

| Neurodegenerative Diseases |

| Cerebrovascular Disorders |

| Epilepsy & Seizure Disorders |

| Sleep Disorders |

| Headache & Migraine |

| Others (TBI, CNS Infections, Tumors) |

| Hospitals & Surgical Centers |

| Diagnostic Laboratories & Imaging Centers |

| Ambulatory Care & Emergency Settings |

| Research & Academic Institutes |

| Specialized Neurology Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Reagents & Consumables | |

| Clinical Testing Instruments | ||

| Diagnostic & Imaging Systems | ||

| By Technology | Neuroimaging Technologies | |

| In-Vitro Diagnostics | ||

| Neuroinformatics & AI Analytics Platforms | ||

| By Condition | Neurodegenerative Diseases | |

| Cerebrovascular Disorders | ||

| Epilepsy & Seizure Disorders | ||

| Sleep Disorders | ||

| Headache & Migraine | ||

| Others (TBI, CNS Infections, Tumors) | ||

| By End User | Hospitals & Surgical Centers | |

| Diagnostic Laboratories & Imaging Centers | ||

| Ambulatory Care & Emergency Settings | ||

| Research & Academic Institutes | ||

| Specialized Neurology Centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the neurodiagnostics market?

The neurodiagnostics market size is USD 9.79 billion in 2026.

What compound annual growth rate (CAGR) is forecast for the market through 2031?

The market is projected to expand at a 7.12% CAGR between 2026 and 2031.

Which product category holds the largest revenue share today?

Reagents & consumables lead the product landscape with 51.02% of 2025 revenue.

Which region is expected to grow the fastest over the forecast period?

Asia-Pacific is set to record the highest regional growth at a 9.28% CAGR through 2031.

What technological trend is disrupting traditional neuroimaging dominance?

Neuroinformatics and AI analytics platforms are rising rapidly, advancing at an 11.45% CAGR.

Page last updated on: