Hospital Acquired Disease Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.28 Billion |

| Market Size (2030) | USD 7.59 Billion |

| Growth Rate (2025 - 2030) | 7.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Acquired Disease Testing Market Analysis by Mordor Intelligence

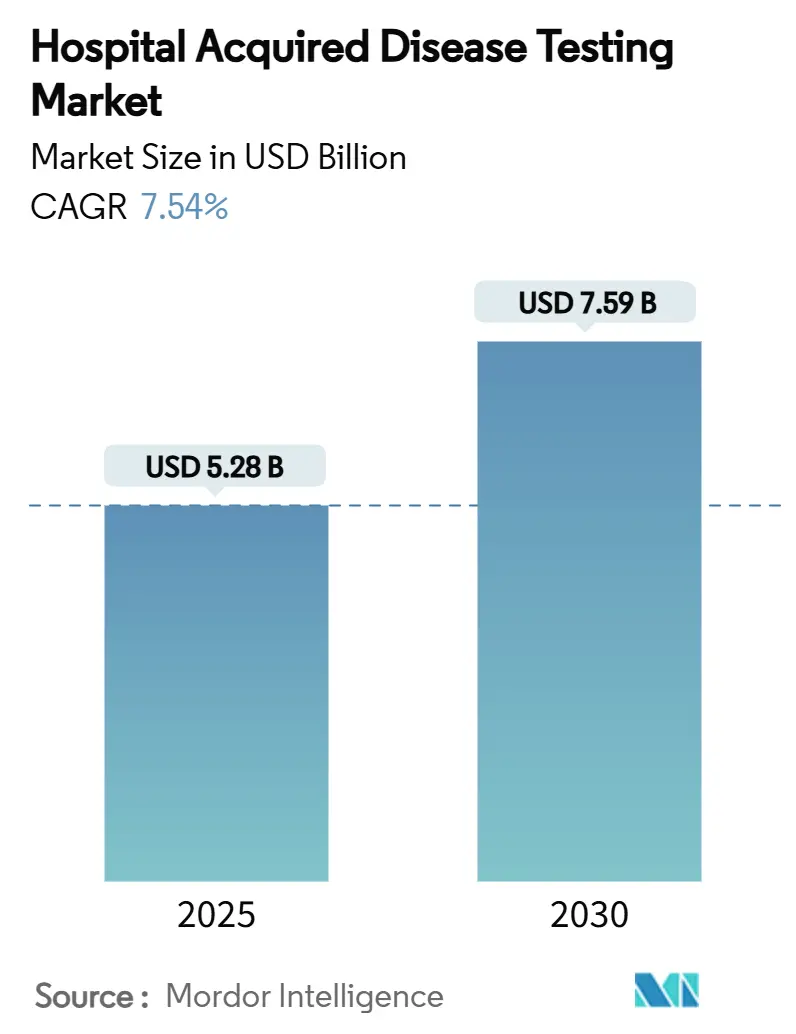

The hospital acquired disease testing market size stands at USD 5.28 billion in 2025 and is projected to reach USD 7.59 billion by 2030, expanding at a 7.54% CAGR through the period. Rising regulatory scrutiny, widespread adoption of molecular diagnostics, and demands for rapid pathogen identification now shape investment priorities across acute-care settings.[1]U.S. Food and Drug Administration, “FDA Takes Action Aimed at Helping to Ensure the Safety and Effectiveness of Laboratory Developed Tests,” FDA.gov Hospitals are replacing legacy culture techniques with syndromic multiplex PCR, while point-of-care (POC) innovations converge with artificial-intelligence (AI) analytics to curb antimicrobial resistance at the bedside.[2]Centers for Medicare & Medicaid Services, “Calendar Year 2025 Medicare Physician Fee Schedule Final Rule,” CMS.gov Vendors are intensifying M&A to secure niche technologies, and reimbursement changes—such as Medicare’s 2025 HCPCS codes—reward facilities that embed comprehensive infection-control testing within clinical workflows.

Key Report Takeaways

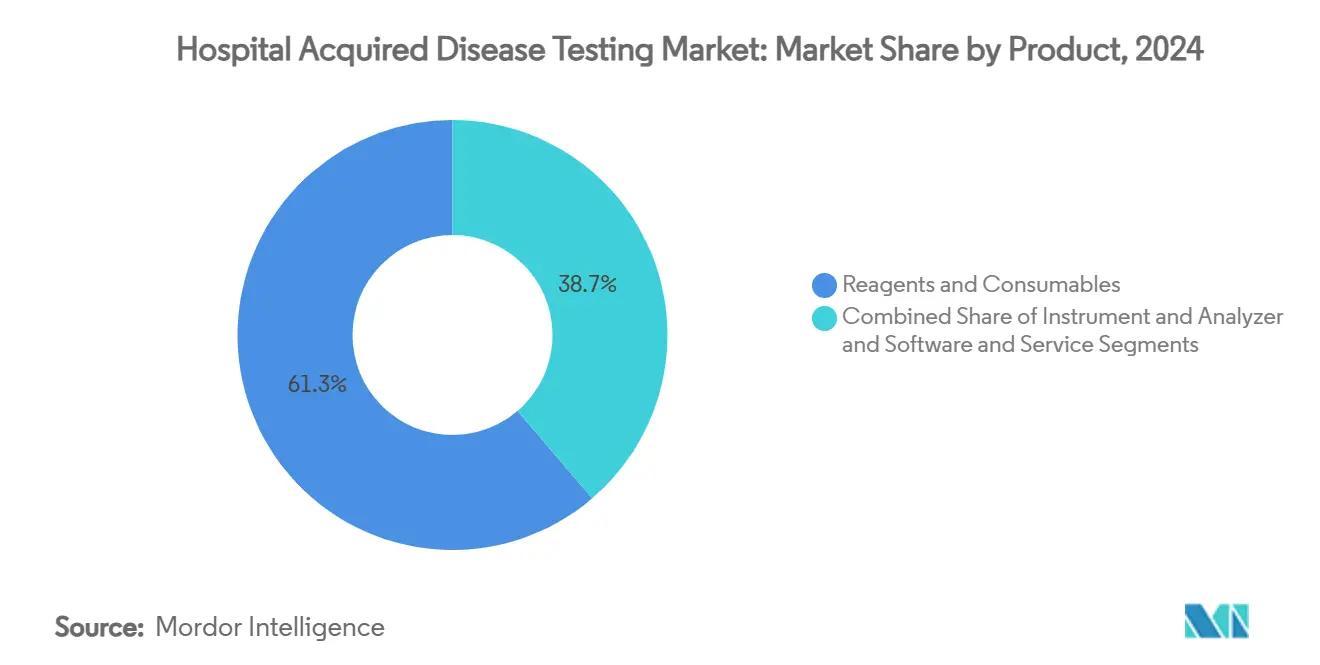

- By product, reagents and consumables led with 61.27% of the hospital acquired disease testing market share in 2024. Instruments and analyzers are forecast to advance at an 11.46% CAGR through 2030.

- By test technology, PCR and molecular diagnostics accounted for 53.42% share of the hospital acquired disease testing market size in 2024. Syndromic multiplex panels are projected to expand at a 10.83% CAGR between 2025-2030.

- By pathogen, MRSA captured 33.46% share of the hospital acquired disease testing market size in 2024, while carbapenem-resistant Enterobacteriaceae testing is poised for 11.36% CAGR through 2030.

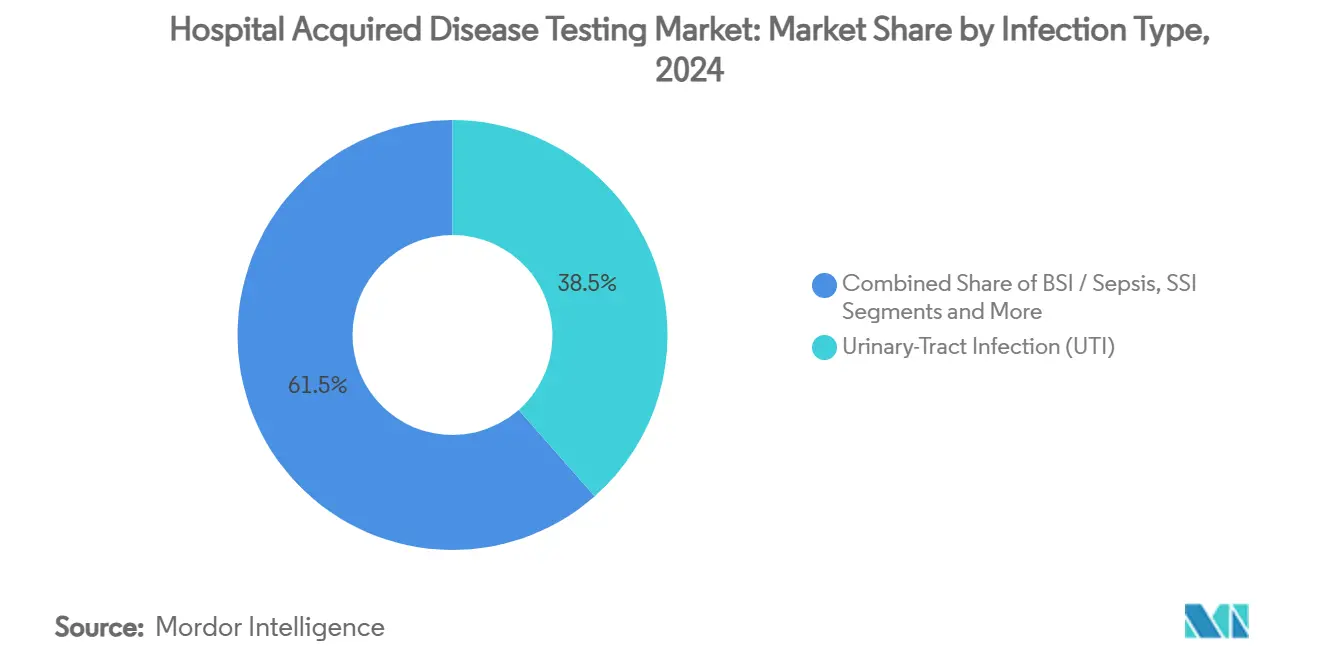

- By infection type, urinary-tract infection diagnostics held 38.50% of the hospital acquired disease testing market share in 2024; hospital-acquired pneumonia testing is growing at 10.49% CAGR to 2030.

- By end user, Hospitals and ICUs maintained 69.26% end-user dominance in 2024, whereas ambulatory surgical centers will grow at 10.56% CAGR.

- By geography, North America retained 38.75% regional share in 2024; Asia-Pacific is accelerating at a 9.14% CAGR.

Global Hospital Acquired Disease Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of HAIs globally | +1.8% | APAC, MEA, global | Medium term (2-4 years) |

| Accelerating adoption of rapid molecular diagnostics (PCR) | +2.1% | North America, EU, APAC | Short term (≤ 2 years) |

| Stricter infection-control regulations & penalties | +1.5% | North America, EU, global | Long term (≥ 4 years) |

| Expansion of point-of-care HAI testing in ICUs | +1.3% | Developed markets worldwide | Medium term (2-4 years) |

| AI-powered predictive analytics for outbreak prevention | +0.9% | North America, EU, APAC pilots | Long term (≥ 4 years) |

| Sustainability mandates driving single-use cartridges | +0.7% | EU, global rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of HAIs Globally

Antimicrobial-resistant pathogens caused 2.8 million infections and 35,000 U.S. deaths in 2024, extending hospital stays by 11.2 days and increasing mortality by 44.9%. Carbapenem-resistant Acinetobacter baumannii outbreaks in ICUs during 2024-2025 exposed persistent gaps in containment protocols.[3]Yi Kong, “Outbreak of Carbapenem-Resistant A. baumannii in an ICU,” Antimicrob Resist Infect Control, biomedcentral.com Such complexity pushes facilities to deploy rapid molecular assays that uncover resistance gene profiles within an hour, supporting timely isolation measures and optimized therapy.

Accelerating Adoption of Rapid Molecular Diagnostics (PCR)

Platforms like BioFire FilmArray identify up to 15 pathogens in 15 minutes, slashing traditional culture timelines of 24-72 hours. Each hour of delayed therapy elevates sepsis mortality by 7.6%, positioning rapid PCR as a frontline tool. QIAGEN’s QIAstat-Dx mini panel clearance in 2025 extends syndromic testing into outpatient clinics, while machine-learning algorithms reach 92% accuracy in predicting sepsis mortality five days post-ICU admission.

Stricter Infection-Control Regulations & Penalties

The FDA’s 2024 laboratory-developed test rule subjects high-risk in-house assays to premarket review, driving labs toward validated commercial kits. In parallel, Medicare’s Hospital-Acquired Condition Reduction Program reduces payments to facilities with excessive infection rates, creating a financial imperative for robust screening. EU hospitals must now document sustainable waste practices under the In-Vitro Diagnostic Regulation, encouraging closed-cartridge formats that limit biohazard exposure.

Expansion of Point-of-Care HAI Testing in ICUs

Bedside nucleic-acid tests complete workflows in 30 minutes with ≥95% sensitivity and 100% specificity, eliminating courier lag. The Finecare Procalcitonin rapid test correlates strongly with central-lab assays for sepsis markers, enabling immediate escalation or de-escalation of antibiotics. Active nasal surveillance cultures in ICUs predicted ventilator-associated pneumonia with 100% strain concordance, demonstrating preemptive value. Cloud-connected systems such as iPonatic feed real-time dashboards for infection-control teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced molecular panels in low-resource hospitals | -1.4% | LMICs, rural hospitals | Medium term (2-4 years) |

| Limited reimbursement for HAI screening in several regions | -1.1% | APAC, MEA, parts of EU | Long term (≥ 4 years) |

| Biofilm-related false-negative results lowering clinician trust | -0.8% | Global | Short term (≤ 2 years) |

| Regulatory uncertainty over AI/ML diagnostic algorithms | -0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Molecular Panels in Low-Resource Hospitals

Sample-to-result PCR instruments exceed USD 100,000, with per-test costs still near USD 9.50 despite microfluidic advances. Digital-twin pathology setups require USD 100,000-200,000 upfront, burdening LMIC budgets. Consequently, many facilities ration testing to only the most critical cases.

Limited Reimbursement for HAI Screening in Several Regions

Medicare MolDX covers syndromic panels from July 2024, yet private-payer uptake differs by state, delaying ROI for hospital labs. Vietnam lacks national POC testing policies, forcing providers to self-fund cardiac and coagulation assays despite clear clinical need. Gaps push administrators to favor selective rather than universal screening.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Secure Recurring Revenue Streams

Reagents and consumables held 61.27% of the hospital acquired disease testing market share in 2024, underscoring their role as revenue anchors in laboratories. Disposable cartridges, extraction kits, and assay-specific reagents are consumed with every test, so hospitals allocate steady budgets to guarantee uninterrupted supply. Closed-cartridge formats also satisfy sustainability rules that mandate reduced biohazard handling across European facilities.

Instruments and analyzers are projected to post an 11.46% CAGR to 2030, reflecting hospital investments in automation that trims manual pipetting and accelerates batch throughput. Vendors bundle middleware, barcode tracking, and auto-validation software to shrink technician workload and cut error rates. Software and service add-ons now deliver antimicrobial-stewardship dashboards, boosting platform stickiness and broadening revenue pools for manufacturers.

By Test Technology: Molecular Platforms Dominate Diagnostic Algorithms

PCR and other molecular assays accounted for 53.42% of hospital acquired disease testing market revenue in 2024, confirming their standing as the gold standard for rapid pathogen identification. Amplicon-based methods detect resistance genes within an hour, enabling clinicians to optimize therapy before cultures mature.

Syndromic multiplex panels are forecast to expand at a 10.83% CAGR, lifted by one-swab workflows that identify dozens of organisms and their resistance markers in parallel. Next-generation sequencing and MALDI-TOF extend coverage into outbreak forensics and ultra-rapid bacterial identification, respectively. Culture platforms remain relevant for phenotypic susceptibility confirmation, yet laboratories increasingly route initial detection through molecular pathways to shave days off time-to-result.

By Pathogen Tested: MRSA Retains the Largest Wallet Share

MRSA screening contributed 33.46% of 2024 revenue, driven by universal-admission policies in many North American and European hospitals. These policies, coupled with reimbursement incentives, keep demand consistent even as overall infection rates trend down slowly.

Carbapenem-resistant Enterobacteriaceae tests will register the fastest 11.36% CAGR because “nightmare bacteria” outbreaks raise acute-care alarm levels. Laboratories adopt cartridges that differentiate KPC, NDM, and OXA-48 genes in under an hour, permitting immediate isolation and contact tracing. Additional assay volumes come from Clostridioides difficile, vancomycin-resistant Enterococci, and multidrug-resistant Pseudomonas aeruginosa, all of which remain on stewardship watchlists.

By Infection Type: UTI Diagnostics Command the Highest Volume

Urinary-tract infection assays generated 38.50% of 2024 sales, making this category the single-largest contributor to hospital acquired disease testing market size. Catheter use and extended inpatient stays keep ordering frequency high across medical-surgical wards and long-term-care units.

Hospital-acquired and ventilator-associated pneumonia panels will rise 10.49% CAGR through 2030 as ICUs seek faster guidance for ventilated patients. Clinicians rely on multiplex respiratory cartridges that uncover polymicrobial infections, supporting early de-escalation once a precise pathogen set emerges. Bloodstream, surgical-site, and gastrointestinal infection testing sustain moderate growth because stewardship protocols mandate precise species-level confirmation before targeted therapy.

By End User: Acute-Care Providers Remain the Core Buyers

Hospitals and ICUs captured 69.26% of global revenue in 2024, reaffirming their central role in purchasing sophisticated diagnostic platforms and high-volume reagent packs. Elevated infection-risk profiles and 24/7 service needs push administrators to maintain broad assay menus.

Ambulatory surgical centers will achieve a 10.56% CAGR as outpatient procedures climb and payers demand same-day discharge safety. Independent reference labs continue to absorb overflow testing, while long-term-care facilities purchase rapid panels to control clusters that jeopardize vulnerable residents’ recovery trajectories.

Geography Analysis

North America contributed 38.75% global revenue in 2024 due to early molecular-diagnostic adoption, robust reimbursement, and aggressive antimicrobial-stewardship mandates. The FDA’s test-regulation final rule standardizes LDT oversight, further driving commercial kit uptake. Canada’s hospital modernization funds and Mexico’s private-sector expansions sustain regional momentum.

Asia-Pacific will notch a 9.14% CAGR through 2030. China’s hospital automation drive, India’s private tertiary chains, and Japan’s aging-population pressures expand molecular purchases. WHO assessments report that 61.99% of Northwest-China hospitals reached “advanced” infection-prevention status by 2025, yet multimodal strategy gaps point to continued diagnostic investment.

Europe steadies on IVDR compliance and eco-design directives that favor cartridge systems. Middle East & Africa and South America trail but represent upside as governments fund universal-health-coverage initiatives and pandemic lessons elevate infection-control budgets.

Competitive Landscape

The hospital acquired disease testing industry is moderately fragmented, with bioMérieux, Danaher (Cepheid), and Becton Dickinson among the leading players alongside Siemens Healthineers, Roche, and Thermo Fisher. bioMérieux's EUR 138 million SpinChip buyout adds 10-minute whole-blood assays, broadening its POC menu. Danaher's GeneXpert installed base surpasses 45,000 units worldwide, supported by USD 9.6 billion diagnostics revenue in 2024. BD considers divesting part of its life-sciences portfolio to refocus on high-growth segments.

Start-ups compete on culture-free phenotypic AST delivering ID + AST results in under 90 minutes, carving white-space in rapid antimicrobial stewardship. AI-native vendors bundle predictive dashboards with subscription models, selling "infection-control-as-a-service."

Hospital Acquired Disease Testing Industry Leaders

Abbott Laboratories

bioMérieux SA

F. Hoffmann-La Roche Ltd

Danaher

BD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: bioMérieux closed its EUR 138 million acquisition of SpinChip Diagnostics, gaining 10-minute myocardial-infarction immunoassays.

- June 2024: bioMérieux won FDA 510(k) clearance and CLIA waiver for the BIOFIRE SPOTFIRE Respiratory/Sore Throat Panel covering 15 respiratory pathogens in 15 minutes.

Global Hospital Acquired Disease Testing Market Report Scope

| Reagents & Consumables |

| Instruments & Analyzers |

| Software & Services |

| Culture-based Tests |

| Immunoassay |

| Polymerase Chain Reaction (PCR) |

| Syndromic Multiplex Panels |

| MALDI-TOF Mass Spectrometry |

| Next-Generation Sequencing |

| MRSA |

| Clostridioides difficile |

| Vancomycin-Resistant Enterococci (VRE) |

| Carbapenem-Resistant Enterobacteriaceae (CRE) |

| Pseudomonas aeruginosa |

| Acinetobacter baumannii |

| Urinary Tract Infection (UTI) |

| Blood-stream Infection (BSI) / Sepsis |

| Surgical Site Infection (SSI) |

| Hospital-Acquired Pneumonia / VAP |

| Gastro-intestinal (C. difficile) |

| Hospitals & Intensive Care Units |

| Independent/Reference Laboratories |

| Ambulatory Surgical Centers |

| Long-Term Care Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Reagents & Consumables | |

| Instruments & Analyzers | ||

| Software & Services | ||

| By Test Technology | Culture-based Tests | |

| Immunoassay | ||

| Polymerase Chain Reaction (PCR) | ||

| Syndromic Multiplex Panels | ||

| MALDI-TOF Mass Spectrometry | ||

| Next-Generation Sequencing | ||

| By Pathogen Tested | MRSA | |

| Clostridioides difficile | ||

| Vancomycin-Resistant Enterococci (VRE) | ||

| Carbapenem-Resistant Enterobacteriaceae (CRE) | ||

| Pseudomonas aeruginosa | ||

| Acinetobacter baumannii | ||

| By Infection Type | Urinary Tract Infection (UTI) | |

| Blood-stream Infection (BSI) / Sepsis | ||

| Surgical Site Infection (SSI) | ||

| Hospital-Acquired Pneumonia / VAP | ||

| Gastro-intestinal (C. difficile) | ||

| By End User | Hospitals & Intensive Care Units | |

| Independent/Reference Laboratories | ||

| Ambulatory Surgical Centers | ||

| Long-Term Care Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the hospital acquired disease testing market in 2025?

It is valued at USD 5.28 billion with a 7.54% forecast CAGR to 2030.

Which product segment generates the most recurring revenue?

Reagents and consumables contribute 61.27% of 2024 revenue due to per-test usage.

Which diagnostic technology is growing fastest?

Syndromic multiplex PCR panels are projected to rise at 10.83% CAGR through 2030.

What drives Asia-Pacific’s rapid growth?

Investments in hospital automation, rising infection-control awareness, and supportive governmental policies drive a 9.14% CAGR.

Which pathogen segment is expanding quickest?

Carbapenem-resistant Enterobacteriaceae testing will grow at 11.36% CAGR because of rising resistance alerts.

Why are point-of-care solutions gaining traction in ICUs?

Bedside assays deliver results in under 30 minutes, enabling immediate antibiotic stewardship and outbreak containment.

Page last updated on: