Degenerative Disc Disease Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

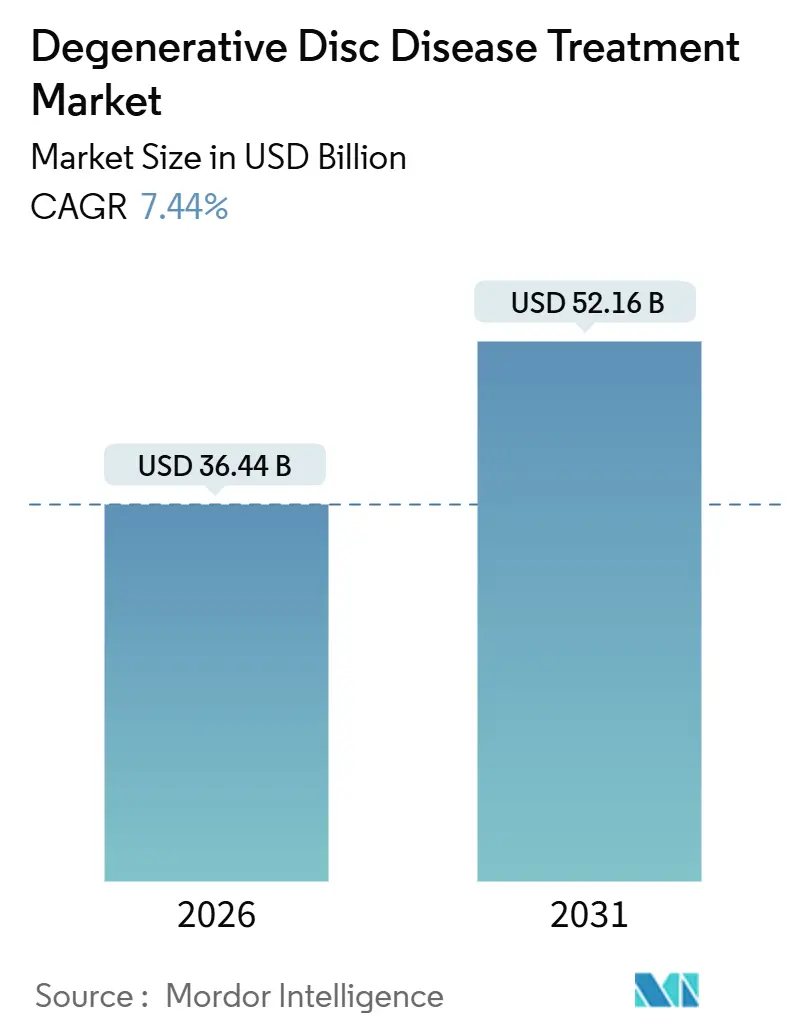

| Market Size (2026) | USD 36.44 Billion |

| Market Size (2031) | USD 52.16 Billion |

| Growth Rate (2026 - 2031) | 7.44% CAGR |

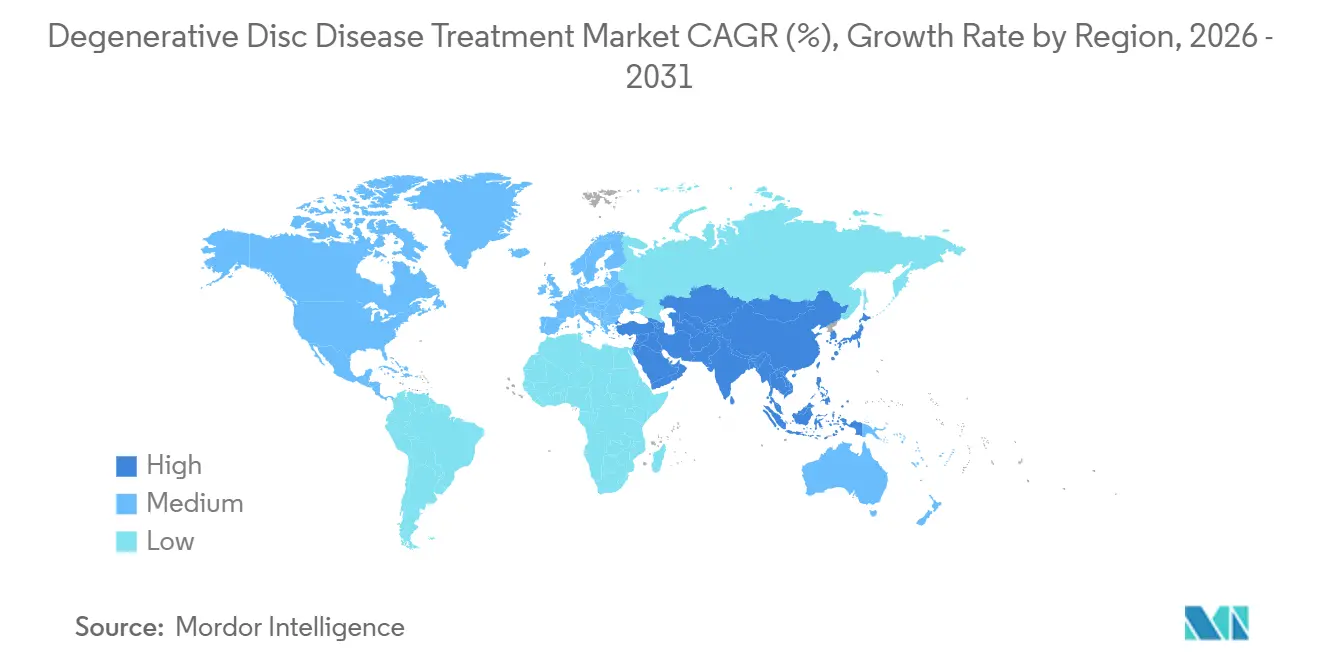

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Degenerative Disc Disease Treatment Market Analysis by Mordor Intelligence

The Degenerative Disc Disease Treatment Market size is estimated at USD 36.44 billion in 2026, and is expected to reach USD 52.16 billion by 2031, at a CAGR of 7.44% during the forecast period (2026-2031).

Demand is rising as aging populations and sedentary workstyles swell the global incidence of low back pain, while payers press providers to favor shorter-stay, value-based interventions. Surgical procedures still dominate revenue, yet non-surgical options—especially digital rehabilitation programs and cell-based biologics—are growing faster as recent reimbursement reforms reward motion preservation and opioid-sparing care.[1]Centers for Medicare & Medicaid Services, “2025 Outpatient Prospective Payment System Final Rule,” CMS, cms.gov Device makers are leaning on AI-guided navigation and robotic platforms to protect margins, whereas regenerative-medicine entrants court mid-career patients who wish to stay active without permanent hardware. Geographic growth is led by Asia-Pacific, where accelerated device approvals and expanded public insurance coverage are unlocking previously unmet demand.[2]Ministry of Health, Labour and Welfare, “2024 White Paper on Health and Welfare,” MHLW, mhlw.go.jp Headline risks include price caps from centralized procurement, counterfeit implant influx in low-income regions, and lingering evidence gaps for certain motion-preservation systems.

Key Report Takeaways

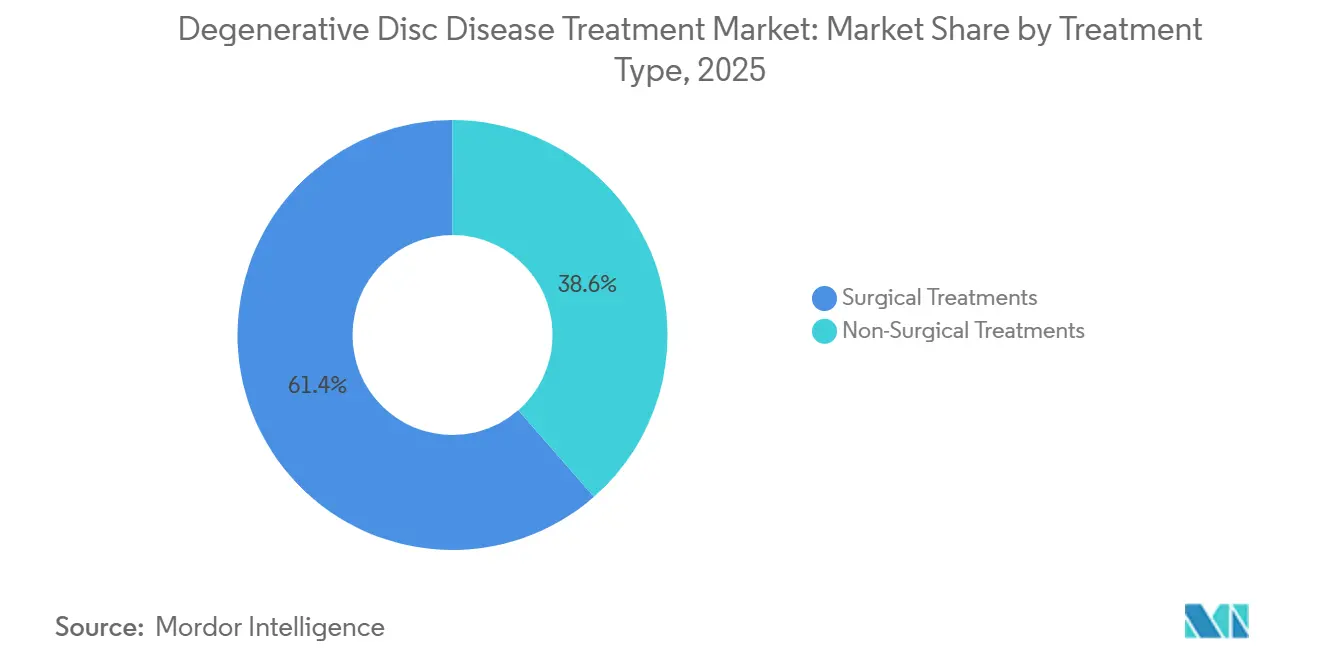

- By treatment type, surgical procedures retained 61.44% revenue share in 2025, while non-surgical modalities are forecast to expand at a 9.54% CAGR through 2031, the fastest among all treatment categories.

- By product type, devices and implants held 43.67% of 2025 sales but biologics are projected to grow at an 11.84% CAGR, outpacing every other product segment to 2031.

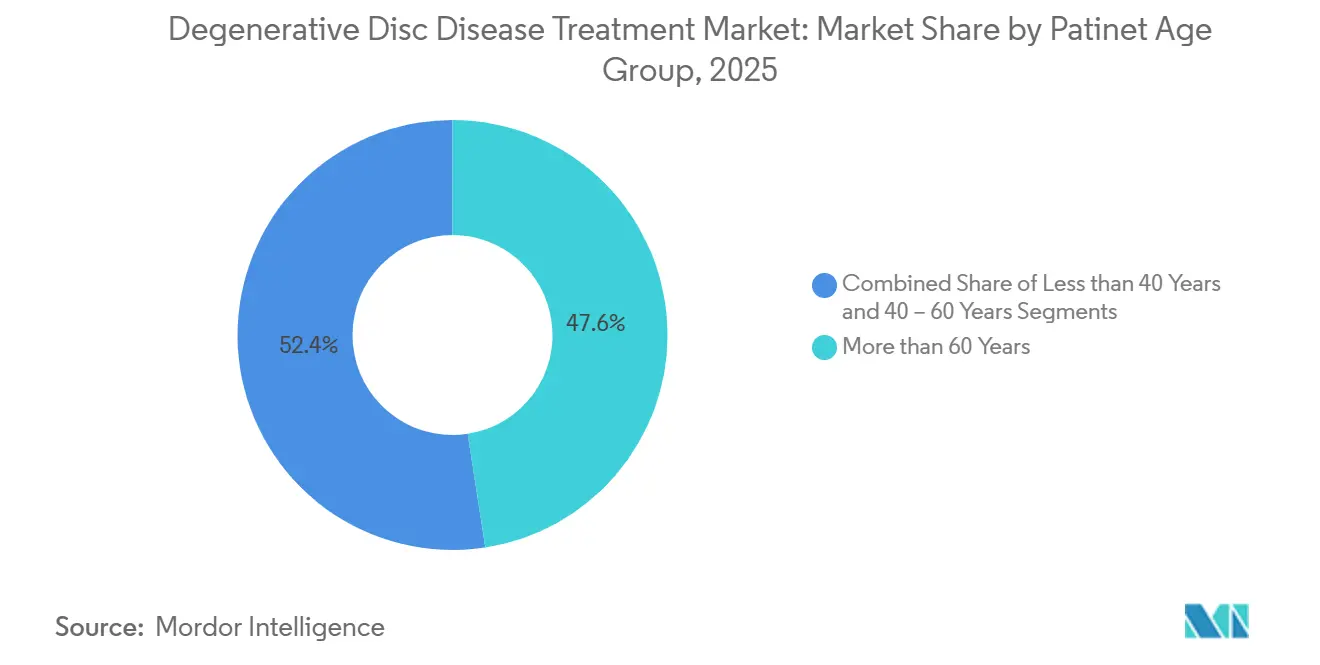

- By patient age, individuals older than 60 accounted for 47.57% of 2025 demand, whereas the 40–60 cohort is set to record a 9.32% CAGR, the highest growth rate among age groups.

- By end user, hospitals generated 54.25% of 2025 revenue, yet ambulatory surgical centers are expected to expand at a 10.67% CAGR, capturing the largest incremental volume shift.

- By geography, North America controlled 36.16% of 2025 receipts; however, Asia-Pacific is projected to lead regional growth at a 9.44% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Degenerative Disc Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Global Population & Rising Prevalence of Lumbar Disorders | +1.8% | Global, strongest in Japan, Germany, Italy | Long term (≥ 4 years) |

| Shift Toward Minimally-Invasive Spine Procedures | +1.5% | North America, EU core, urban APAC | Medium term (2–4 years) |

| Favorable Reimbursement Reforms in Major Markets | +1.2% | United States, Germany, United Kingdom, Australia | Short term (≤ 2 years) |

| Commercialization of Regenerative Biologics | +1.0% | North America, EU, early adoption in South Korea, Japan | Long term (≥ 4 years) |

| Emerging AI-Guided Spinal Navigation Systems | +0.9% | North America, Western Europe, select APAC hospitals | Medium term (2–4 years) |

| Home-Based Digital Rehab Platforms Reducing Surgical Demand | +0.7% | United States, United Kingdom, Nordics, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Global Population & Rising Prevalence of Lumbar Disorders

The World Health Organization confirms that low back pain remains the top non-fatal disease burden and forecasts cases to soar from 619 million in 2020 to 843 million by 2050. Japan expects citizens aged 65 and older to reach 30% of the population by 2030, already driving a 22% jump in lumbar-spine procedures between 2020 and 2025. India’s national insurance scheme reports disc degeneration in 18% of orthopedic claims, underscoring unmet needs across middle-income nations. Payers are prioritizing interventions that shorten recovery and limit revision surgery, which benefits motion-preservation implants and emerging biologics. As longevity expands in every region, the degenerative disc disease treatment market should see a durable base of age-linked demand.

Shift Toward Minimally-Invasive Spine Procedures

Endoscopic and percutaneous techniques are reducing length of stay, infection rates, and readmissions. A 2024 meta-analysis in Spine showed unilateral biportal endoscopic discectomy cut hospital stays by 40% versus open surgery.[3]Jae Hwan Lee, “Unilateral Biportal Endoscopic Discectomy Versus Open Microdiscectomy: A Meta-analysis,” Spine, journals.lww.com The U.S. FDA cleared 14 minimally invasive implant systems in 2025, while U.S. ambulatory surgical center revenue for percutaneous laminotomy multiplied 20-fold between 2018 and 2023. Insurers prefer these approaches under bundled payments, accelerating uptake across urban centers worldwide.

Favorable Reimbursement Reforms in Major Markets

Policy is shifting from volume to value. The 2025 U.S. Outpatient Prospective Payment System raised ambulatory surgical center rates 2.9% and introduced codes for non-opioid analgesia. Germany now requires proof of 12 weeks of conservative care before reimbursing fusion, doubling physiotherapy utilization since 2023. Australia links payment to 12-month functional scores through the ePPOC registry. These reforms reward technologies that deliver durable outcomes and penalize high-revision hardware, nudging clinicians toward biologics and motion-preservation devices.

Commercialization of Regenerative Biologics

DiscGenics’ injectable disc-cell therapy finished Phase 2 enrollment in 2024, posting a 2.1-point Oswestry Disability Index gain at six months versus saline control. Mesoblast’s allogeneic cell product showed positive 24-month durability and eyes a 2027 biologics license application. Europe now allows conditional approval based on 12-month data for unmet needs, potentially speeding introductions. If pricing remains under USD 25,000 per dose, health-economic models suggest biologics could capture up to 20% of surgical volume by deferring hardware implantation in younger patients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Cost & Pricing Pressure | -1.1% | United States, Germany, Japan | Medium term (2–4 years) |

| Regulatory Hurdles for Novel Biologics | -0.8% | North America, EU, slower APAC uptake | Long term (≥ 4 years) |

| Limited Long-Term Evidence for Motion-Preservation Implants | -0.5% | North America, Western Europe | Medium term (2–4 years) |

| Surge in Counterfeit Spinal Implants | -0.3% | South Asia, Sub-Saharan Africa, parts of South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment Cost & Pricing Pressure

The 2026 U.S. Physician Fee Schedule proposes a 2.8% conversion-factor cut, slicing roughly USD 400 from lumbar-fusion reimbursement. Germany’s joint committee declared total disc arthroplasty devices priced above EUR 8,000 (USD 8,720) not cost-effective, compressing regional pricing. Japan trimmed cervical artificial-disc payment 12% in April 2025, citing sparse 10-year outcomes. Such moves squeeze manufacturer margins and hasten consolidation.

Regulatory Hurdles for Novel Biologics

The FDA’s 2024 guidance demands 24-month durability and MRI-based disc-height data, extending trials by up to two years and adding USD 15 million to costs. Europe requires 15-year post-market surveillance for advanced therapies, prompting Kuros Biosciences to pause its European study in 2025. Resource-rich firms can comply, but smaller innovators risk stall-out.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Non-Surgical Gains Ground Despite Surgical Dominance

Surgical procedures generated 61.44% of 2025 revenue, yet they are set to grow at only 7.2%—below the overall degenerative disc disease treatment market CAGR. Non-surgical modalities are projected to rise 9.54%, buoyed by payer incentives for conservative care. Fusion remains the primary surgical workhorse, but a 2024 Spine Journal study tracking 1,200 patients found total disc arthroplasty delivered equivalent pain relief with 22% less adjacent-segment degeneration. Endoscopic surgery, still under 10% of surgical volume, is flourishing in ambulatory settings where shorter case times enlarge throughput. Microdiscectomy faces reimbursement pressure as bundle contracts penalize readmissions. On the conservative side, CDC opioid-dose caps have spurred interest in non-opioid agents such as tanezumab, which awaits FDA approval.

Physical therapy is now a gatekeeper, with Germany requiring 12 weeks of documented conservative care before fusion authorization, doubling utilization since 2023. Stem-cell injections are drawing venture funding; DiscGenics secured USD 10 million in 2024 to advance its Phase 2 program. The degenerative disc disease treatment market size for non-surgical care is therefore poised to expand fastest as sequencing strategies delay or avert operative intervention.

By Product Type: Biologics Outpace Devices on Innovation Premium

Devices and implants supplied 43.67% of 2025 revenue, but their 6.8% CAGR points to commoditization, while biologics are projected to climb 11.84%, the highest product-level growth. Artificial discs earned expanded indications in 2025, opening multi-level use cases. Yet fixation hardware pricing keeps sliding; MedPAC reports lumbar-fusion implant acquisition costs fell 14% from 2020 to 2024. Bone-graft substitutes already replace autograft in 60% of cases, and Medtronic’s Infuse Bone Graft alone cleared USD 700 million in 2025 sales.

Cell-based products face stringent oversight but promise premium returns. The degenerative disc disease treatment market share for biologics could climb rapidly once first-generation therapies secure durable-outcome data. Pharmaceuticals remain a quarter of revenue, yet the impending arrival of high-priced non-opioid analgesics will likely bifurcate the category into low-cost generics and specialty brands. Navigation software and digital therapeutics round out the “Others” bucket and are expanding at double-digit rates after CMS allowed separate billing for AI surgical planning in 2025.

By Patient Age Group: Mid-Career Cohort Drives Growth

Individuals above 60 accounted for 47.57% of 2025 demand, but the 40–60 segment will grow fastest at 9.32% through 2031 as employers focus on rapid return-to-work outcomes. A 2024 JAMA Network Open study showed workers aged 45–55 returned to full duty six weeks sooner with disc arthroplasty versus fusion, translating into USD 12,000 productivity savings per case. Under-40 patients lag in absolute numbers yet post an 8.1% growth rate due to early degeneration linked to sedentary lifestyles.

Germany now mandates second opinions from motion-preservation specialists for fusion candidates under 50, shifting younger patients toward artificial discs. For seniors, the 2025 U.S. national coverage decision tightened fusion criteria, directing many toward non-surgical care. The degenerative disc disease treatment market size for mid-career adults is set to expand most rapidly, attracting premium biologics and motion-preservation solutions

By End User: ASCs Capture Outpatient Migration

Hospitals produced 54.25% of 2025 revenue, yet ambulatory surgical centers are forecast to clock a 10.67% CAGR as payers steer cases to lower-cost sites. MedPAC tracked a 20-fold jump in ASC percutaneous laminotomy receipts from 2018 to 2023. Integrated orthopedic clinics are gaining share by bundling imaging, therapy, and surgery, posting 15% lower episode costs than hospital-based care in a 2024 AAOS case study.

ASCs increasingly mirror hospital capability; 42% had installed robotic guidance by 2025, up from 18% in 2023. CMS added 11 spine procedures to the ASC list in 2025, including two-level lumbar fusion, likely shifting 25,000 cases per year by 2027. Hospitals are forming ASC joint ventures to retain procedural revenue, while orthopedic clinics leverage superior patient-experience scores to win payer contracts.

Geography Analysis

North America captured 36.16% of 2025 sales, but rising price pressure holds its forecast CAGR to 6.8%. The 2025 U.S. outpatient rule favors minimally invasive procedures and digital rehab via separate non-opioid codes. Canada’s bundled-payment pilots in Ontario and British Columbia achieved 18% cost savings versus fee-for-service in 2024, mainly from implant and length-of-stay reductions. Mexican private hospitals reported 22% growth in international spine patients during 2024, while public facilities face austerity constraints. The region’s strategic question is whether value-based payment will depress device margins faster than innovation can forge new premium categories.

Asia-Pacific is projected to grow 9.44%, the fastest regional pace. China slashed spinal-implant prices 60% through centralized procurement in 2024, yet broadened insurance access to 200 million additional beneficiaries. India’s scheme now covers 550 million citizens, with disc degeneration ranking third among orthopedic claims. Japan accelerated minimally invasive device approvals by allowing conditional clearance on 12-month evidence. South Korea granted the first conditional license for a cell-based disc therapy in 2025. Australia ties reimbursement to 12-month outcomes via ePPOC, rewarding motion-preservation devices with lower revision rates. Rapid volume growth raises quality-control risks, highlighted by WHO’s 2024 alert on counterfeit implants in South Asia.

Europe is set to grow. Joint clinical assessments under the 2021/2282 regulation compel richer real-world evidence; Germany’s cost-effectiveness review already squeezed prices on artificial discs. The NHS digital pathway mandate cut surgical referrals 14% in its first year. France now requires MRI-based Modic changes before approving fusion reimbursement. Italy’s registry revealed outcome variation across regions, prompting center-of-excellence efforts. Middle East & Africa grow as GCC nations add planned-care spine pathways; Saudi Arabia’s 2024 strategy includes accountable-care bundles. South America expands, led by Brazil, whose regulator cleared six new fixation devices in 2024.

Competitive Landscape

The degenerative disc disease treatment market is moderately concentrated. Incumbents defend margins by integrating AI navigation; Medtronic’s AiBLE with Mazor X Stealth trimmed operating time 18 minutes in 2024, enhancing bundled-payment economics. Globus Medical’s ExcelsiusGPS surpassed 100,000 cases in 2025, and participating hospitals cut implant costs 12% by reducing revisions. White-space opportunities lie in motion-preservation systems and digital therapeutics: Hinge Health recorded 62% surgery avoidance at 12 months, winning mandates from three major U.S. insurers.

Regenerative entrants push a different value proposition. DiscGenics’ cell therapy and Mesoblast’s allogeneic product both logged positive mid-stage data, aiming to defer or eliminate hardware in younger patients. The Centers for Disease Control and Prevention estimates U.S. musculoskeletal spending at USD 635 billion in 2024, giving payers reason to back durable, less invasive options. Patent filings for spinal navigation algorithms rose 34% from 2022 to 2024, underscoring investment in software differentiation. Firms able to verify long-term outcomes through registries command premium pricing; those relying on commodity hardware face price erosion as group-purchasing organizations consolidate demand.

Degenerative Disc Disease Treatment Industry Leaders

Medtronic

Globus Medical

Johnson & Johnson Services LLC

Stryker

HIGHRIDGE Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Dr. Todd H. Lanman presented 24-month Synergy Disc IDE data showing significant pain and functional gains over ACDF at DOCS Health’s 7th Spine Arthroplasty Summit.

- October 2025: Centinel Spine received two-level FDA approval for prodisc C Vivo and prodisc C SK cervical TDR devices, expanding indications to C3–C7 reconstruction.

- July 2025: Highridge Medical licensed U.S. rights for activL lumbar disc and began domestic production ahead of a late-2025 launch.

- January 2025: Proprio Vision secured FDA clearance for its Paradigm AI-guided navigation system with 99% screw-placement accuracy across 342 cases.

Global Degenerative Disc Disease Treatment Market Report Scope

Degenerative Disc Disease (DDD) is treated through non-surgical methods like physical therapy, medications, and lifestyle changes, with surgery reserved for severe cases. The goal is to reduce inflammation, strengthen muscles, and improve mobility to alleviate symptoms.

The Degenerative Disc Disease Treatment Market Report is segmented by Treatment Type, Product Type, Patient Age Group, End User, and Geography. By Treatment Type, the market is segmented into Non-Surgical and Surgical. By Product Type, the market is segmented into Devices & Implants, Biologics, Pharmaceuticals, and Others. By Patient Age Group, the market is segmented into Less than 40 Years, 40–60 Years, and More than 60 Years. By End User, the market is segmented into Hospitals, Specialty Orthopedic Clinics, ASCs, and Rehab Centers. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America.The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Non-Surgical Treatments | Pharmacological Therapy |

| Physical Therapy | |

| Stem-Cell Therapy | |

| Surgical Treatments | Spinal Fusion |

| Total Disc Arthroplasty | |

| Microdiscectomy | |

| Endoscopic Spine Surgery |

| Devices & Implants | Artificial Discs |

| Spinal Fixation Devices | |

| Biologics | Bone Graft Substitutes |

| Cell-based Regenerative Products | |

| Pharmaceuticals | NSAIDs |

| Opioids | |

| Corticosteroids | |

| Others |

| Less than 40 Years |

| 40 – 60 Years |

| More than 60 Years |

| Hospitals |

| Specialty Orthopedic Clinics |

| Ambulatory Surgical Centers (ASCs) |

| Rehab & Physiotherapy Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Non-Surgical Treatments | Pharmacological Therapy |

| Physical Therapy | ||

| Stem-Cell Therapy | ||

| Surgical Treatments | Spinal Fusion | |

| Total Disc Arthroplasty | ||

| Microdiscectomy | ||

| Endoscopic Spine Surgery | ||

| By Product Type | Devices & Implants | Artificial Discs |

| Spinal Fixation Devices | ||

| Biologics | Bone Graft Substitutes | |

| Cell-based Regenerative Products | ||

| Pharmaceuticals | NSAIDs | |

| Opioids | ||

| Corticosteroids | ||

| Others | ||

| By Patient Age Group | Less than 40 Years | |

| 40 – 60 Years | ||

| More than 60 Years | ||

| By End User | Hospitals | |

| Specialty Orthopedic Clinics | ||

| Ambulatory Surgical Centers (ASCs) | ||

| Rehab & Physiotherapy Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the degenerative disc disease treatment market in 2026?

The degenerative disc disease treatment market size is USD 36.44 billion in 2026.

What is the projected CAGR through 2031?

The market is forecast to advance at a 7.44% CAGR to 2031.

Which treatment category is growing fastest?

Non-surgical modalities are expected to post the highest growth, at a 9.54% CAGR.

Which region is set to lead future growth?

Asia-Pacific is projected to expand at a 9.44% CAGR, the fastest among all regions.

How are ambulatory surgical centers impacting the market?

ASCs are forecast to grow at 10.67% CAGR as payers migrate cases to lower-cost outpatient settings.

What technological trend is reshaping surgical procedures?

AI-guided navigation and robotic platforms are improving accuracy, cutting operating time, and reducing revision rates.

Page last updated on: