Brain Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

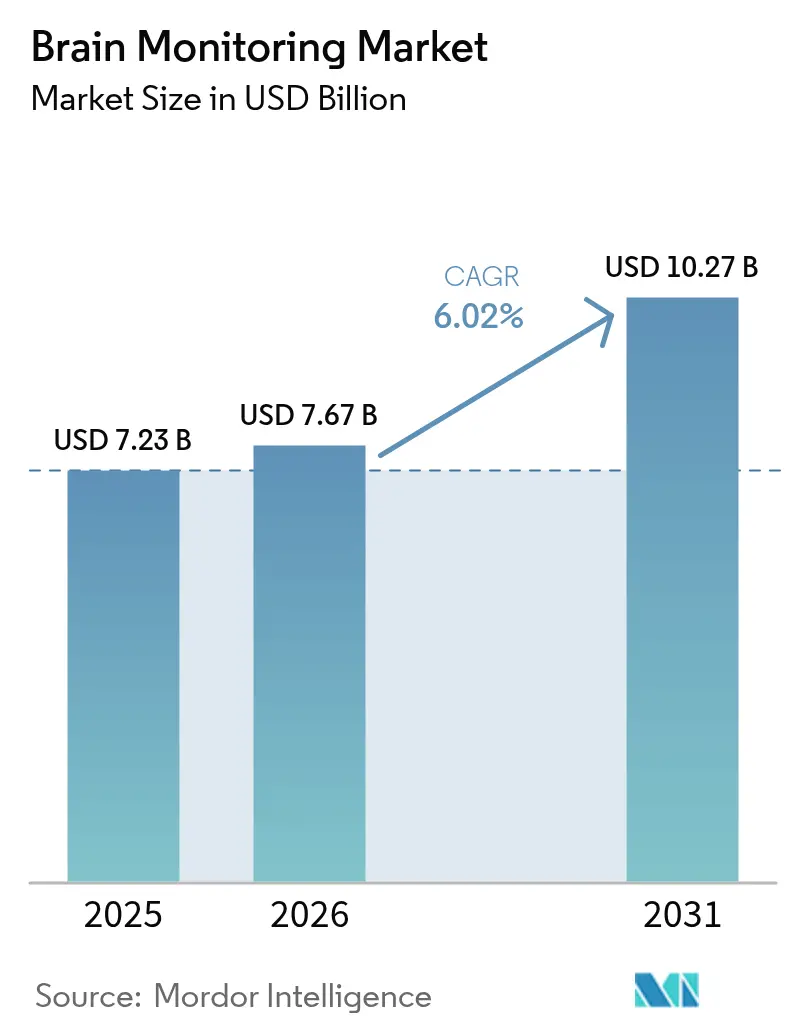

| Market Size (2026) | USD 7.67 Billion |

| Market Size (2031) | USD 10.27 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

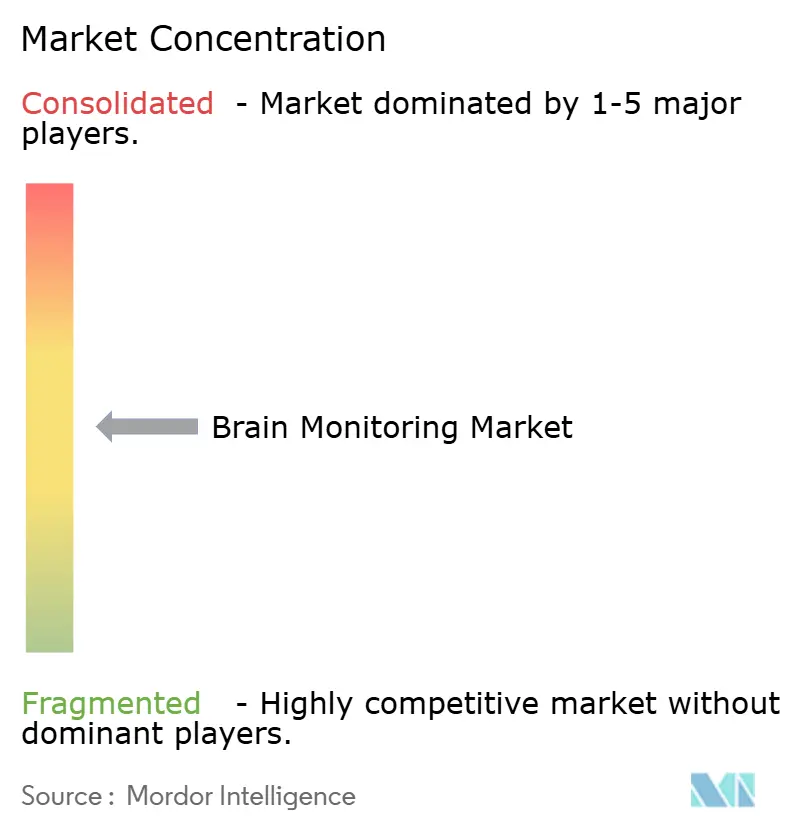

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brain Monitoring Market Analysis by Mordor Intelligence

The brain monitoring market size is expected to grow from USD 7.23 billion in 2025 to USD 7.67 billion in 2026 and is forecast to reach USD 10.27 billion by 2031 at 6.02% CAGR over 2026-2031. Demand is expanding as neurological disorders climb to the top of the global disease burden, so providers are investing in faster, more portable diagnostic tools. Advancements in artificial intelligence (AI) are improving multimodal data interpretation, while minimally invasive and wearable sensors are moving routine monitoring into emergency rooms, rehabilitation centers, and homes. Fixed systems still dominate hospital spending, yet growth is strongest in compact and cloud-connected devices that support tele-neurology and decentralized trials. Vendors are refocusing from standalone hardware toward integrated software-as-a-medical-device (SaMD) platforms that automate data analysis, ease staffing gaps, and create recurring revenue from analytics subscriptions.

Key Report Takeaways

- By product type, electroencephalograph systems held 30.18% of the brain monitoring market share in 2025, while accessories are projected to climb at an 7.78% CAGR to 2031.

- By procedure, non-invasive techniques commanded 73.12% of the brain monitoring market size in 2025; invasive modalities record the fastest CAGR at 6.72% through 2031.

- By modality, fixed systems retained 60.65% revenue share in 2025, whereas portable and wearable devices will expand at a 7.05% CAGR to 2031.

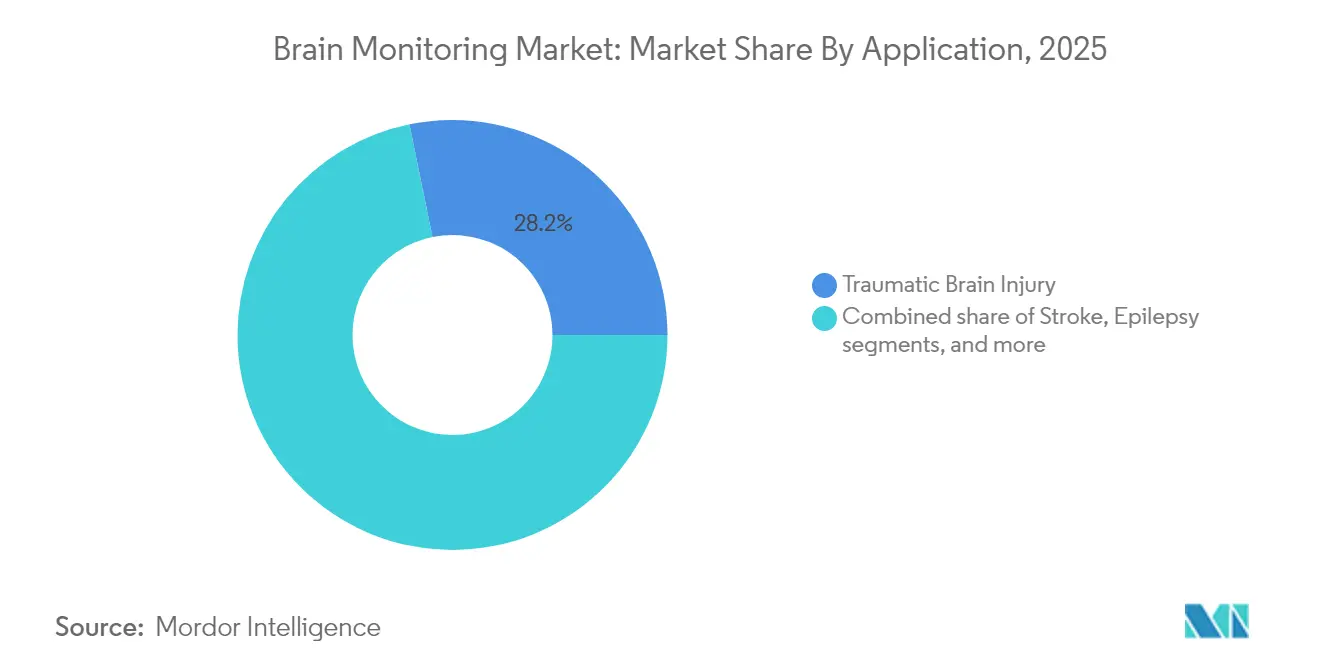

- By application, traumatic brain injury accounted for 28.21% of the brain monitoring market size in 2025; Alzheimer’s monitoring solutions are advancing at a 6.90% CAGR to 2031.

- By end-user, hospitals occupied 66.12% of spending in 2025, while home-care and tele-neurology platforms are forecast to grow at 7.50% annually through 2031.

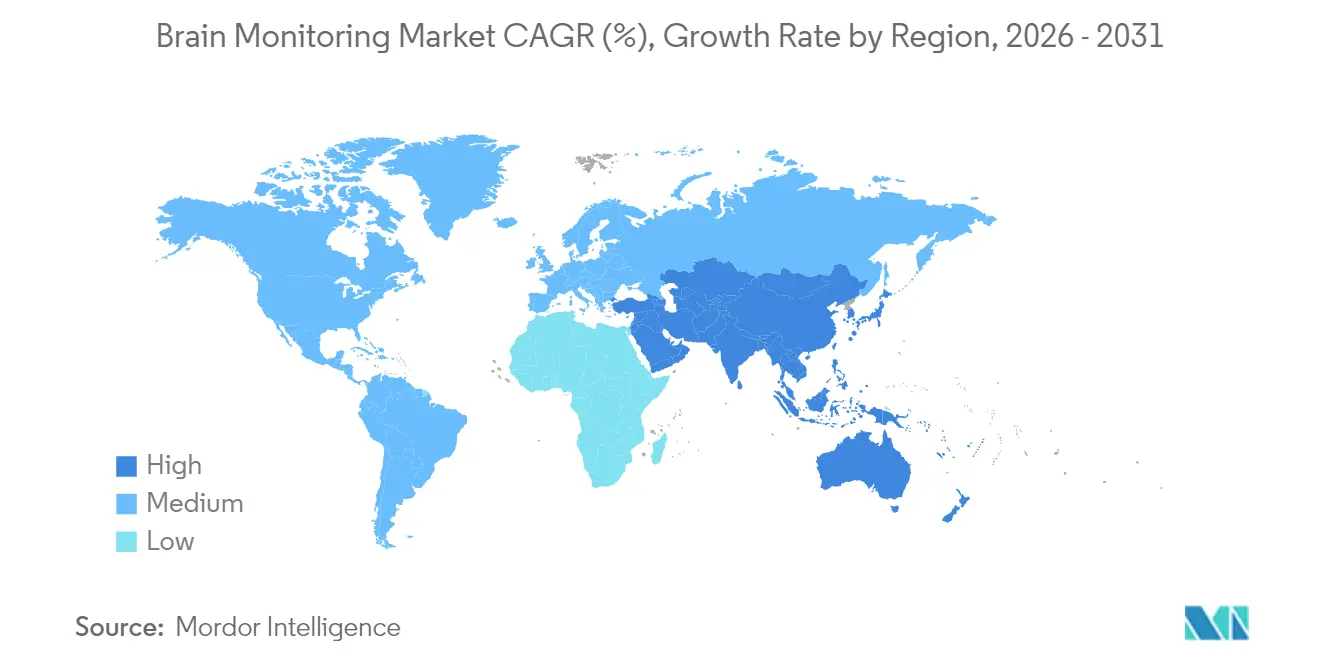

- By geography, North America led with 37.28% share in 2025; Asia Pacific records the highest regional CAGR of 8.26% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Brain Monitoring Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating prevalence of neurological disorders | +2.5% | Global; especially low- and middle-income countries | Long term (≥ 4 years) |

| AI-enabled multimodal analytics | +2.0% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Wearable and minimally invasive brain sensors | +1.5% | Global; early uptake in high-income regions | Medium term (2-4 years) |

| Investment surge in neuro-critical-care infrastructure | +1.1% | North America, Europe, China, Japan, GCC | Short term (≤ 2 years) |

| Brain-focused drug trials seeking objective biomarkers | +0.9% | North America, Europe, Japan | Medium term (2-4 years) |

| Accelerated approvals for SaMD modules | +0.7% | North America, Europe, developed Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence of Neurological Disorders

Cases of stroke, dementia, epilepsy, and neuropathies now affect more than 3 billion individuals—43% of the global population—over 18% jump since 1990.[1]World Health Organization, “Over 1 in 3 people affected by neurological conditions, the leading cause of illness and disability worldwide,” who.int These conditions generate 443 million years of healthy life lost each year, intensifying pressure on health systems. Growing longevity worsens exposure to age-linked illnesses such as Alzheimer’s, while metabolic diseases like diabetes triple the incidence of neuropathy. The widening gap between patient demand and neurologist supply pushes hospitals to adopt automated monitoring that triages high-risk cases and feeds data into centralized interpretation hubs. Over the next decade, universal screening programs and community clinics are expected to rely on lower-cost neural sensors to catch early deterioration, sustaining long-run expansion of the brain monitoring market.

AI-Enabled Multimodal Analytics for Enhanced Diagnostic Accuracy

Machine-learning algorithms now integrate EEG, imaging, hemodynamics, and clinical scores to predict mortality or poor outcomes in traumatic brain injury with up to 95.6% accuracy.[2]Seun Orenuga et al., “Traumatic Brain Injury and Artificial Intelligence: Shaping the Future,” MDPI, mdpi.com FDA-cleared platforms such as Ceribell Clarity deliver bedside electrographic status-epilepticus detection within minutes, freeing critical-care teams from manual review. Hospitals in North America and Europe are embedding these SaMD modules into existing monitors, creating service contracts that bundle cloud analytics with consumables. As reimbursement codes recognize algorithm-assisted interpretation, adoption in urban Asia-Pacific centers is accelerating. Over the medium term, richer data pipelines will shorten decision times in stroke and intensive-care units, lifting utilization across the brain monitoring market.

Proliferation of Wearable and Minimally Invasive Brain Sensors

Flexible dry-electrode headbands, ear-EEG inserts, and sub-millimeter neuro-wrapping sensors now capture brain activity in ambulatory settings without gels or wires.[3]Deblina Sarkar, “Wearable Devices for Cells,” MIT News, news.mit.edu Sports federations pilot helmet liners that quantify impact kinematics, while sleep clinics issue earbud-style devices that track overnight micro-arousals. Hospitals value these wearables for step-down care after neurosurgery, and pharmaceutical firms deploy them in decentralized trials to capture real-world endpoints. As validation studies prove parity with lab-grade systems, insurers show interest in home-based monitoring pathways that cut readmissions. The result is steady penetration of consumer-grade and prosumer devices that feed data back to clinical dashboards, enlarging addressable volumes for the brain monitoring market.

Investment Surge in Neuro-Critical-Care Infrastructure

Government and private payers are upgrading stroke centers, neuro-ICUs, and military trauma units. The U.S. Defense Health Program earmarked dedicated funds for brain-injury research in its FY 2025 budget NIH’s Blueprint MedTech issued USD 17 million in 2024 to speed device translation.[4]National Institutes of Health, “Blueprint MedTech continues to fuel the innovation of devices,” nibib.nih.gov Large private hospital chains in China and the Gulf are following suit, purchasing rapid EEG carts and multimodal bedside systems. Because capital budgets are already released, the uplift to equipment sales and service contracts will materialize within two years.

Restraints Impact Analysis of Brain Monitoring Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High purchase and upkeep costs for advanced modalities | -1.2% | Global; strongest drag in low- and middle-income economies | Medium term (2-4 years) |

| Global shortage of trained neuro-technologists | -0.9% | Worldwide; severe in developing regions | Long term (≥ 4 years) |

| Interoperability and cybersecurity risks | -0.6% | Global; heightened in strict data-protection jurisdictions | Medium term (2-4 years) |

| Uncertain reimbursement for ambulatory solutions | -0.4% | North America, Europe, developed Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Purchase and Upkeep Costs for Advanced Modalities

Magnetoencephalography and fMRI systems can exceed USD 3 million, with annual service contracts adding 10–15% of list price. Even mainstream EEG rigs require consumables and calibration that strain hospital operating budgets. Replacement cycles accelerate as vendors launch AI-ready models, prompting finance committees to defer purchases in price-sensitive markets. Open-source wearable fNIRS prototypes from academic labs promise relief, yet certification remains years away, so cost remains a mid-term drag on the brain monitoring market.

Global Shortage of Trained Neuro-Technologists

ICUs in many regions lack staff able to place electrodes, interpret traces, or maintain devices. During the COVID-19 pandemic, tele-neurology visits in the United States shot from 3.9% to 94.6%, underscoring workforce gaps. Although AI triage eases some pressure, complex cases still need expert review. The multiyear training pipeline means talent shortages will restrain equipment utilization, especially in emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Brain Monitoring Market Segment Analysis

By Product Type:

EEG Systems Lead While Accessories AccelerateEEG systems generated the most significant slice of the brain monitoring market in 2025 by capturing 30.18% revenue. Hospitals rely on them for seizure diagnostics, sedation depth checks, and cerebral ischemia surveillance. Portable rapid-EEG carts now transform emergency workflows by delivering seizure detection within 10 minutes at the bedside, boosting device turnover. Accessories—caps, dry electrodes, cables—grow fastest at an 7.78% CAGR because every new unit drives recurring consumable demand. Flexible polymer electrodes improve comfort and cut setup time, widening EEG use in pediatrics and tele-monitoring. As more hospitals standardize on disposable caps to limit infection risk, the accessories sub-segment will outpace the overall brain monitoring market.

By Procedure:

Non-invasive Dominates While Invasive Gains PrecisionNon-invasive modalities such as scalp EEG, fNIRS, and transcranial Doppler controlled 73.12% of 2025 revenue thanks to lower risk and simpler staffing. Their appeal broadens as algorithm-enhanced systems approximate invasive accuracy. Yet critical-care units still depend on intracranial pressure (ICP) probes and depth electrodes for refractory cases. These invasive tools expand at a 6.72% CAGR as new nanomembrane sensors enter trials, delivered through blood vessels and eliminating skull penetration. Over time, hybrid solutions may blur categories further, sustaining growth in both cohorts of the brain monitoring market.

By Modality:

Fixed Systems Maintain Leadership as Wearables Gain MomentumFixed/standalone systems anchored in neuro-ICUs still hold a 60.65% share, valued for multiparameter fusion and deep analytics. Stereotactic surgery suites also rely on large-format displays and high-frame-rate cameras for guidance. Nonetheless, portable & wearable devices register a 7.05% CAGR, buoyed by cloud connectivity and battery advances. Ear-canal EEG, adhesive forehead patches, and visor-mounted near-infrared sensors now cover stroke recovery, sleep medicine, and consumer wellness. As payers reimburse remote monitoring bundles, hospitals deploy loaner kits that stream encrypted data to command centers, expanding the reach of the brain monitoring market.

By Application:

Traumatic Brain Injury Leads While Alzheimer’s Monitoring AcceleratesTraumatic brain injury segment accounted for 28.21% of 2025 revenue because military, sports, and emergency-medicine stakeholders insist on continuous monitoring. Ultra-sensitive blood assays for neurofilament light (NfL) complement EEG, enabling early discharge decisions. In contrast, Alzheimer’s disease and other dementias trail in share but grow fastest at 6.90% CAGR. AI models parsing longitudinal EEG and imaging detect preclinical decline, and wearable sensors capture daily activity patterns that signal cognitive shifts. As aging populations swell, policy makers push earlier intervention, cementing this segment’s influence on the brain monitoring market.

By End-User:

Hospitals Maintain Dominance as Home-Care Platforms ExpandHospitals accounted for 66.12% of the 2025 market size, driven by bundled capital purchases, service contracts, and staff training programs. Neuro-ICUs integrate EEG into ventilator dashboards, and academic centers run high-density research arrays. Yet home-care and tele-neurology platforms show 7.50% CAGR, leveraging reimbursement for remote physiologic monitoring. Stroke survivors now leave the hospital with wearable headbands that alert clinicians to seizure-like activity. Telestroke networks link rural emergency departments to on-call specialists at urban hubs, widening access and supporting growth across the brain monitoring market.

Geography Analysis

North America and Europe Brain Monitoring Market

North America held 37.28% of global sales in 2025, supported by robust insurance coverage, NIH grants, and a dense network of level-one trauma centers. The brain monitoring market size in the region is expanding at a steady 5.95% CAGR as hospitals refresh fleets to AI-enabled models and outpatient providers embrace remote EEG kits. Europe follows with mature yet methodical procurement; growth runs at 5.72% as budget oversight slows but does not halt adoption. Noteworthy is a handheld ocular laser that detects TBI biomarkers during the golden hour after injury, a potential standard of care in ambulances.

APAC Brain Monitoring Market

Asia-Pacific posts the quickest gains at an 8.26% CAGR. China funds stroke centers in tier-2 cities; Japan pilots insurance codes for home EEG; India’s private hospitals import rapid-EEG carts for emergency departments. Given that 80% of neurological deaths occur in low- and middle-income countries, regional demand for affordable, low-maintenance devices remains high. Local manufacturers have begun supplying cost-effective alternatives, reinforcing supply-chain resilience in the brain monitoring market.

MEA and South America Brain Monitoring Market

The Middle East & Africa and South America expand from smaller bases as Gulf states build neuro-critical centers and Brazilian hospitals join telestroke networks. However, currency volatility and procurement hurdles temper acceleration. Multilateral lenders and public-private partnerships are expected to underwrite pilot programs that demonstrate clinical and economic value, creating footholds for future market growth.

Competitive Landscape

The competitive field mixes diversified med-tech groups—Medtronic, GE Healthcare, Philips—with focused innovators such as Ceribell and Advanced Brain Monitoring. Incumbents leverage global service organizations and multi-modality portfolios, while specialists differentiate through AI algorithms that reduce reading time or flag status epilepticus. Partnerships with providers have become decisive: Arkansas Children’s adopted Zeto’s FDA-cleared dry-electrode headset to speed pediatric EEG acquisition.

Acquisitions continue as firms seek technology adjacencies. Aditxt purchased Brain Scientific’s NeuroCap and NeuroEEG assets to accelerate telehealth expansion. Meanwhile, Medtronic’s BIS LoC OEM module opens licensing revenue by embedding depth-of-anesthesia indices into third-party monitors.

Competitive focus is shifting from hardware margins to analytics subscriptions and clinical-workflow integration. Vendors that provide cloud dashboards, cybersecurity patches, and algorithm updates lock hospitals into multi-year agreements, raising switching costs. As SaMD approvals accelerate, software capabilities will dictate future share capture within the brain monitoring market.

Brain Monitoring Industry Leaders

GE Healthcare

Koninklijke Philips N.V.

Medtronic PLC

Natus Medical Incorporated

Nihon Kohden Corporation

- *Disclaimer: Major Players sorted in no particular order

Brain Monitoring Market Companies Covered in this Report

- Abbott Laboratories

- Advanced Brain Monitoring

- Boston Scientific

- BrainScope Company Inc.

- Cadwell

- Cerenion

- Compumedics

- Elekta

- EMOTIV Inc.

- GE Healthcare

- Koninklijke Philips

- Masimo

- Medtronic

- Mespere LifeSciences

- Natus Medical

- Neurable Inc.

- NeuraSignal, Inc.

- NeuroSky Inc.

- Nihon Kohden

- Siemens Healthineers

- Zeto, Inc.

Market Opportunities and Future Outlook

The fastest whitespace is forming as brain monitoring moves from episodic, in-hospital testing to connected, lower-setup workflows in outpatient clinics and home-care pathways. A clear proof point is the run of FDA 510(k) clearances in 2026 focused on faster acquisition and updates to form factors. Zeto, Inc. received 510(k) clearance (K260455) for the New Wave outpatient and home EEG system (April 2026), while Ceribell received 510(k) clearances for its Instant EEG Headset (K254033, February 2026) and Brain Monitor Headband (K260363, April 2026). Together, these clearances support expansion of billable monitoring beyond the neuro-ICU into EDs, ambulatory neurology practices, and step-down care, while sustaining accessory demand (caps, electrodes, cables) as installed bases grow.

A second opportunity area is emerging where quantitative neuroimaging, AI analytics, and platform distribution converge. GE HealthCare's announced intent (September 2025) to acquire icometrix highlights how neuro workflow software and brain MRI assessment capabilities are being pulled into broader imaging and monitoring portfolios, consistent with the market trend toward vendors shifting from standalone hardware toward integrated software-as-a-medical-device platforms. Partnerships and licensing arrangements that embed algorithms into existing fleets can reduce switching friction for providers and support cloud-connected analytics subscription models. At the same time, hospital procurement priorities around interoperability and cybersecurity increase the value of vendors that can package devices, software updates, and enterprise integration into multi-year agreements.

Recent Industry Developments in Brain Monitoring Market

- June 2026: GE HealthCare signed a software license and distribution agreement with NordicNeuroLab covering neuroimaging software. The deal strengthens GE HealthCare's ability to bundle neuro-focused software with imaging workflows, supporting broader deployment of quantitative brain assessment capabilities across its installed base.

- March 2026: Medtronic and GE HealthCare expanded their multi-year global strategic alliance to integrate Medtronic technologies including BIS Advance brain monitoring, Nellcor pulse oximetry, capnography, and regional oximetry into GE HealthCare monitoring platforms. The expanded integration agenda increases the reach of BIS-based brain monitoring through large-scale patient-monitoring platforms and can simplify purchasing for hospitals standardizing on unified vendor ecosystems.

- September 2025: GE HealthCare announced its intent to acquire icometrix, an AI-powered brain imaging analysis specialist focused on neurological disorders. The planned acquisition adds quantitative brain MRI assessment tools to GE HealthCare's neurology portfolio, aligning with the market shift toward software-led differentiation and workflow automation for brain monitoring and imaging pathways.

Brain Monitoring Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the brain monitoring market is defined as revenues earned from medical devices and related accessories used to record, image, or track brain activity and physiology in clinical and research settings, where results support diagnosis, monitoring, or treatment decisions.

Scope exclusions: We exclude consumer neuro-wellness headsets, software-only cognitive tests, and neuromodulation or stimulation equipment.

Segments Covered in This Report

- By Product Type

- Magnetoencephalograph (MEG) Systems

- Electroencephalograph (EEG) Systems

- Transcranial Doppler (TCD) Ultrasound

- Cerebral Oximeters

- Magnetic Resonance Imaging (MRI) Devices

- Intracranial Pressure (ICP) Monitors

- Computerized Tomography (CT) Devices

- Positron Emission Tomography (PET) Devices

- Accessories

- Electrodes

- Sensors

- Cables

- Gels & Pastes

- Other Accessories

- Other Brain Monitoring Devices

- By Procedure

- Invasive Monitoring

- Non-invasive Monitoring

- By Modality

- Fixed / Standalone Systems

- Portable & Wearable Systems

- By Application

- Traumatic Brain Injury

- Stroke

- Epilepsy

- Parkinson's Disease

- Alzheimer's & Other Dementias

- Sleep Disorders

- Other Neurological Conditions

- By End-User

- Hospitals

- Diagnostic & Imaging Centers

- Ambulatory Surgical & Specialty Clinics

- Home-care Settings & Tele-neurology Platforms

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model, then to stress test assumptions that cannot be observed directly in one single dataset. We typically start with public health statistics and procedure volumes, then align those with device utilization patterns that affect how often brain monitoring is actually used in routine care.

Sources reviewed include, as examples, the World Health Organization for neurological burden signals, the US CDC for condition prevalence and care setting trends, OECD health data for imaging and hospital activity proxies, and the US FDA public databases for device clearances and indications. We also reference peer reviewed clinical journals for modality adoption (for example, EEG use in epilepsy pathways), trade association publications where available, and company filings and investor presentations for revenue mix and geographic exposure. In parallel, we use paid subscriptions for company financials and intelligence, news and financials, and patent databases to cross check timelines and product positioning. These sources are illustrative only, and many other references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work was used to confirm purchasing behavior, how procurement is bundled, and how utilization differs by care setting and geography. Interviews and surveys covered device manufacturers and channel partners, along with clinicians, imaging and neurodiagnostic lab staff, and hospital procurement stakeholders across APAC, EMEA, and the Americas, so gaps from desk research could be closed and then rechecked against real world pricing and adoption logic.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 18% | APAC: 42% |

| Mid tier: 52% | Functional/Unit leaders: 23% | EMEA: 31% |

| Smaller Players: 21% | Managers: 59% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the demand pool is reconstructed using neurological caseload signals and care setting capacity, then mapped to modality level utilization and replacement cycles. Once that structure is in place, we corroborate through selective bottom-up approximations, such as sampled average selling prices multiplied by estimated unit placements, and we apply supplier and channel checks to reduce overcounting from bundling.

Key inputs used in the model include installed base and replacement timing for monitoring equipment, procedure and test volumes for neurodiagnostics, hospital and imaging center capacity utilization, modality mix shifts between EEG and imaging led monitoring, and price progression by system type (including service and accessory attach rates). Where local data is thin, gaps are handled through region proxies from comparable healthcare markets, and then corrected using interview feedback on utilization and pricing ranges.

Forecasting is done using scenario analysis supported by expert views on adoption drivers and constraints, then anchored to a small set of measurable variables that move predictably over time, such as neurodiagnostic throughput, imaging access, and capital spending cycles. A final pass is made to ensure currency conversion timing and inflation assumptions are applied consistently across regions.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and large variances are flagged early so assumptions can be revisited. Checks include year over year growth sanity tests, cross comparisons against related device categories, and reconciliation of price and volume logic so implied utilization stays realistic.

Before sign-off, the work goes through multi step analyst review where calculations are rechecked and any anomalies are traced back to the exact input that created them. If a key assumption changes, such as a reimbursement shift, a new regulatory clearance, or a sudden change in hospital capital spending, experts are re-contacted to confirm the direction and timing. Reports are refreshed annually, with interim updates for material events, and a final pre delivery sweep is done so clients receive the latest updated view.

Mordor Intelligence's Global Brain Monitoring Market Market Estimate Compared With Other Published Estimates

Published market values for brain monitoring often do not match because the market can be framed in different ways, and those choices flow into the underlying calculations. Differences usually come from what counts as brain monitoring, whether imaging modalities are included, how accessories and service revenue are treated, and how pricing is converted across regions and years.

In this market, the biggest gap drivers are scope and usage assumptions. Some estimates focus mainly on neurodiagnostic devices and leave out imaging based monitoring, while others include consumer oriented headsets or stimulation equipment, which expands the total. The spread in 2025 values also reflects whether pricing is modeled as a single global average or built up by region and care setting, and whether replacement cycles and utilization are validated with hospital and lab respondents, a scope and validation approach applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.23 B (2025) | |

| Global Consultancy A | USD 6.14 B (2025) | Narrower device-only framing is likely, with limited clarity on imaging inclusion and accessory or service attach rates, which can pull the total down even when end-user coverage is broad. |

| Industry Publisher B | USD 5.91 B (2025) | Scope appears centered on brain monitoring systems products with less transparency on modality coverage and regional ASP build-up, which can understate markets where imaging and higher-spec systems drive value. |

Taken together, the table indicates that scope choices and the way price and utilization are constructed explain most of the difference. By tying the model to observable demand signals and then checking pricing and usage with frontline respondents, the estimate stays traceable to clear steps and practical inputs, which also makes future updates easier to replicate.

Key Questions Answered in the Report

How are artificial-intelligence algorithms reshaping clinical use of brain monitoring devices?

AI engines now deliver near-instant interpretation of EEG and multimodal signals, enabling emergency teams to recognize seizures or elevated intracranial pressure without waiting for a specialist consult. This improves triage accuracy and shortens treatment decision time in intensive-care and stroke units.

What factor is driving the surge of wearable brain monitoring solutions in sports medicine?

Athletic programs are adopting helmet inserts and headbands that record impact forces during play, then relay real-time risk scores to trainers. This continuous feedback loop supports evidence-based return-to-play decisions and lowers long-term liability for teams and leagues.

Why are hospitals prioritizing integrated software-as-a-medical-device (SaMD) modules over standalone hardware upgrades?

SaMD platforms add new diagnostic features through cloud updates, allowing facilities to unlock advanced analytics and automated reporting on existing monitors without major capital spending or downtime.

How is the shortage of trained neuro-technologists influencing purchasing decisions?

Administrators favor systems with automated electrode placement guidance, AI-assisted artifact removal, and remote reading capabilities because these features reduce dependence on scarce EEG technologists and make high-acuity monitoring feasible in community hospitals.

What role do objective biomarkers play in neurological drug development?

Pharmaceutical sponsors embed high-frequency EEG and blood-based neuro-filament assays into clinical trials to obtain quantifiable evidence of drug effect, accelerating regulatory review and improving confidence in efficacy claims.

How are data-security concerns shaping adoption of connected brain monitoring devices?

Procurement teams now demand end-to-end encryption, cybersecurity certifications, and seamless electronic-health-record integration before approving networked monitors, prompting vendors to invest heavily in secure firmware and compliance testing.

Page last updated on: