Point Of Care Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 58.76 Billion |

| Market Size (2031) | USD 92.92 Billion |

| Growth Rate (2026 - 2031) | 9.90% CAGR |

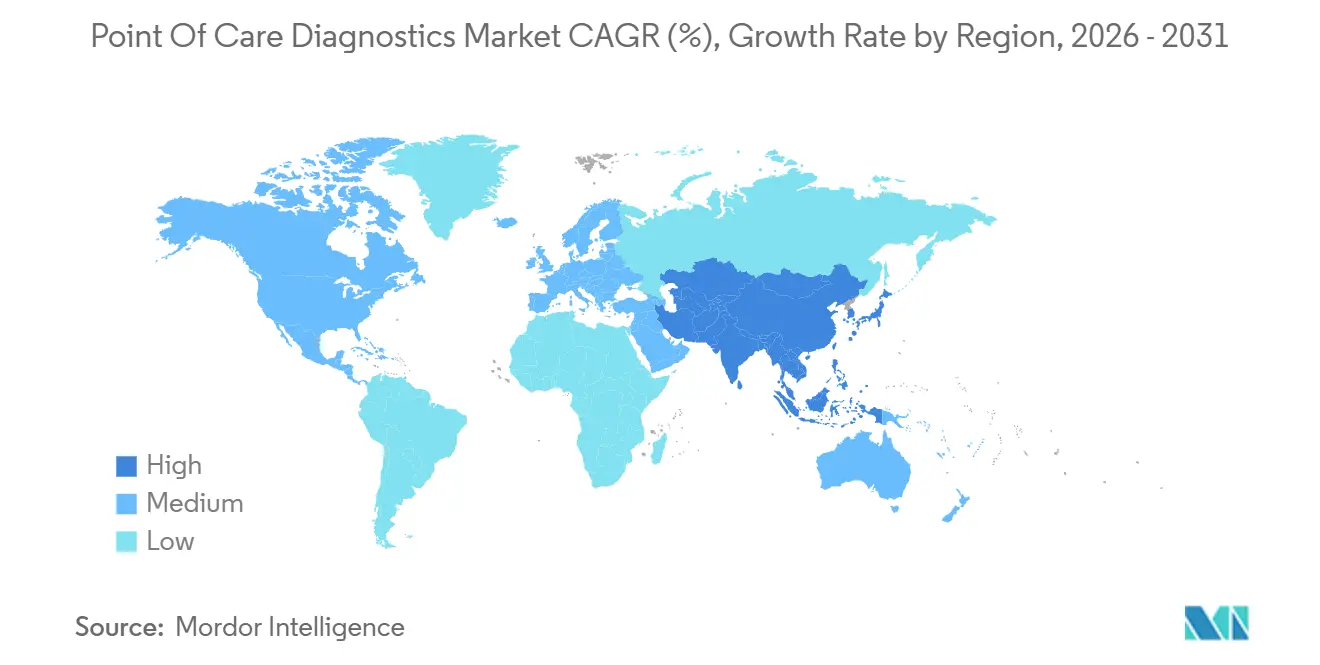

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

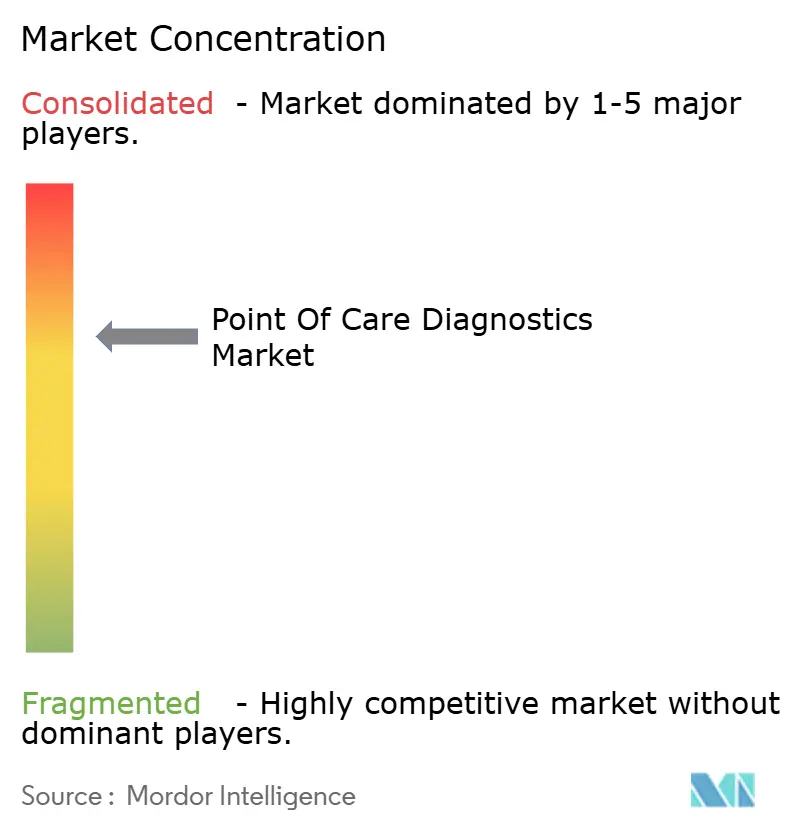

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Point Of Care Diagnostics Market Analysis by Mordor Intelligence

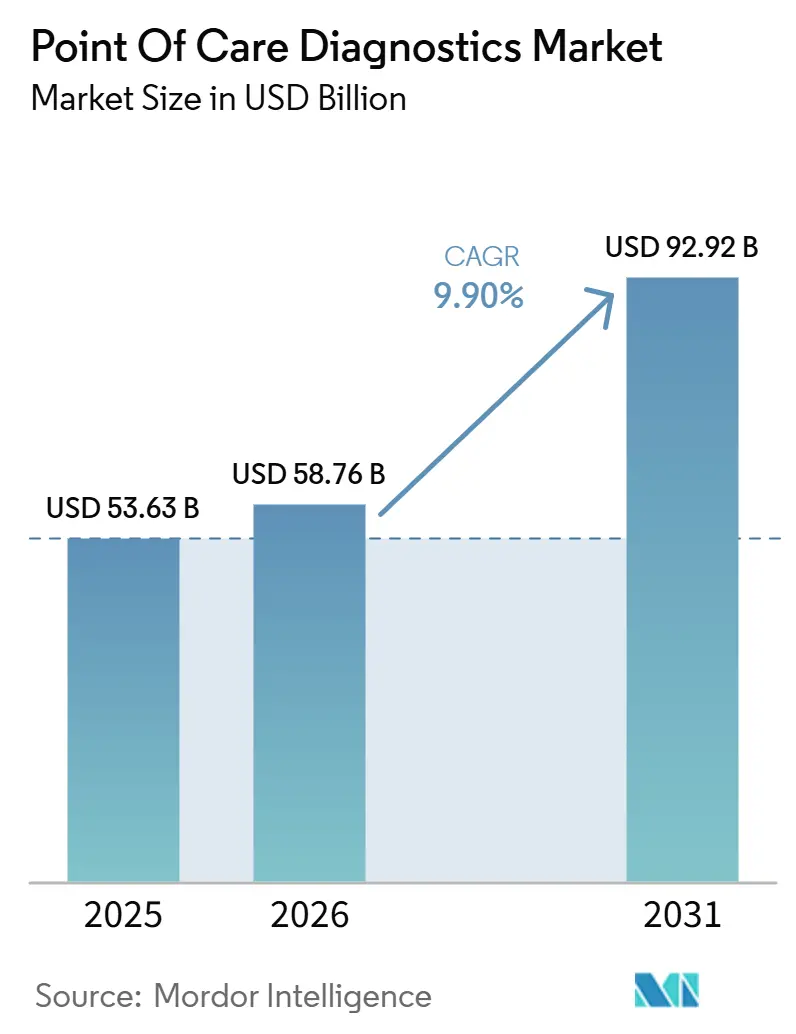

The Point Of Care Diagnostics Market size is projected to expand from USD 53.63 billion in 2025 and USD 58.76 billion in 2026 to USD 92.92 billion by 2031, registering a CAGR of 9.90% between 2026 to 2031.

This growth reflects a decisive shift in diagnostic capacity from centralized laboratories to settings that bring clinicians and patients into the same physical or virtual space, compressing decision cycles from days to minutes. Regulatory bodies have accelerated CLIA-waived clearances for rapid molecular respiratory panels, enabling physician offices and retail clinics to run assays that once required high-complexity labs. Demand has also been buoyed by rising chronic disease prevalence, pandemic-driven public health mandates, and the integration of Bluetooth-enabled continuous glucose monitors that feed real-time data to electronic health records. At the same time, competitive intensity is climbing as incumbents defend cartridge ecosystems while new entrants exploit AI-enhanced smartphone readers to bypass proprietary hardware. Reimbursement reforms that pay for remote monitoring are tilting diagnostic volumes toward home-care settings, creating fresh opportunities for device makers able to satisfy both clinical and consumer expectations.

Key Report Takeaways

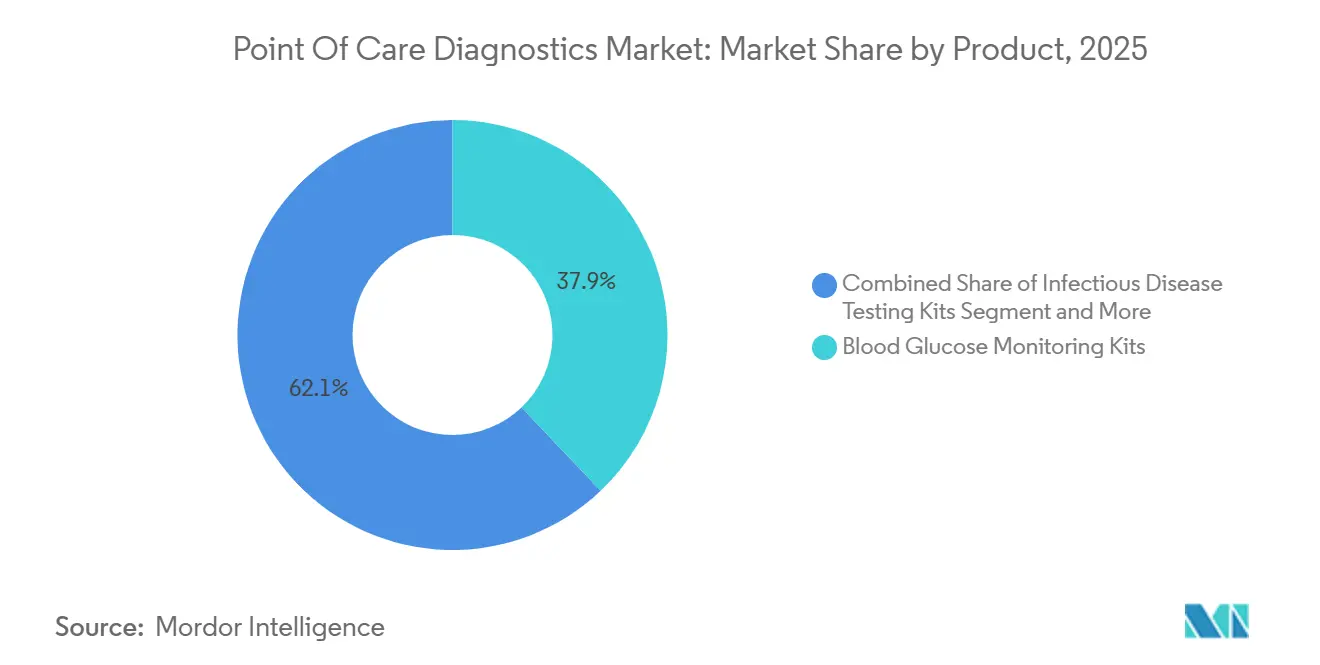

- By product category, glucose monitoring kits captured 37.94% of the point-of-care diagnostics market share in 2025, while infectious disease kits are forecast to expand at a 10.27% CAGR through 2031.

- By platform, lateral flow assays led with 34.12% revenue share in 2025; molecular diagnostics platforms are advancing at a 10.51% CAGR to 2031.

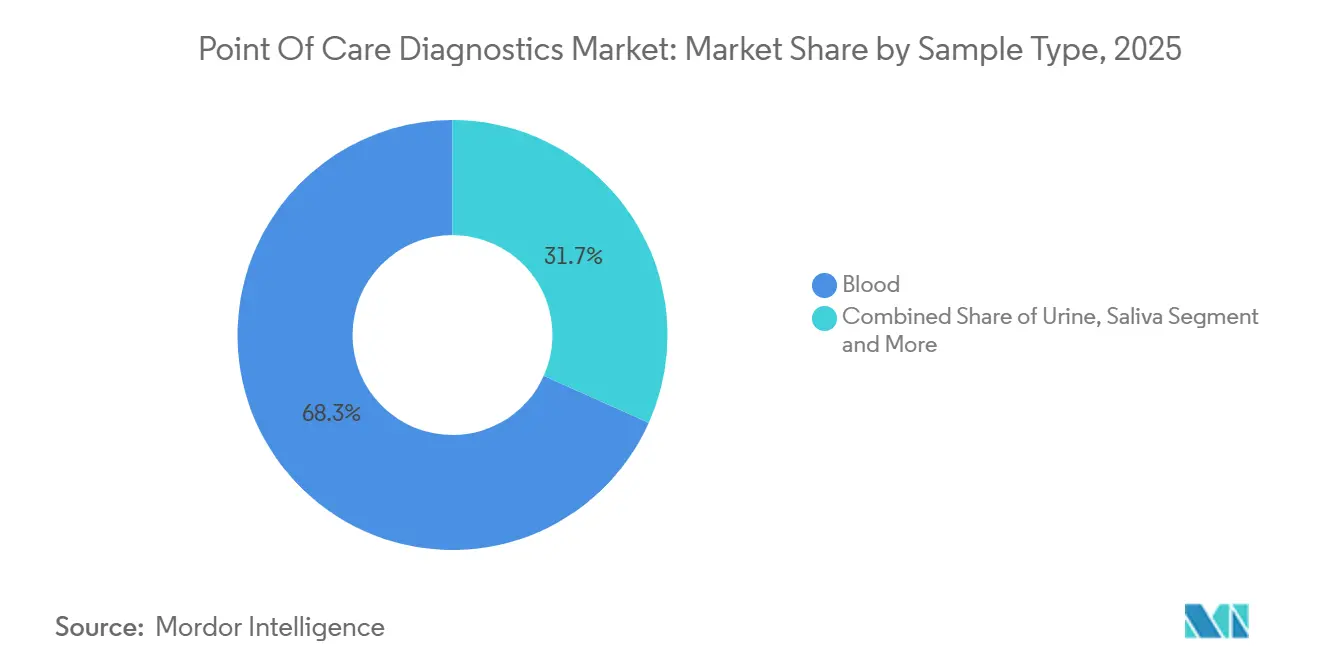

- By sample type, blood accounted for 68.26% of overall test volume in 2025, whereas nasal and throat swabs are projected to rise at a 10.42% CAGR through 2031.

- By mode of purchase, over-the-counter channels held a 61.44% share of the point-of-care diagnostics market size in 2025; prescription-based tests are the fastest-growing channel at a 10.01% CAGR to 2031.

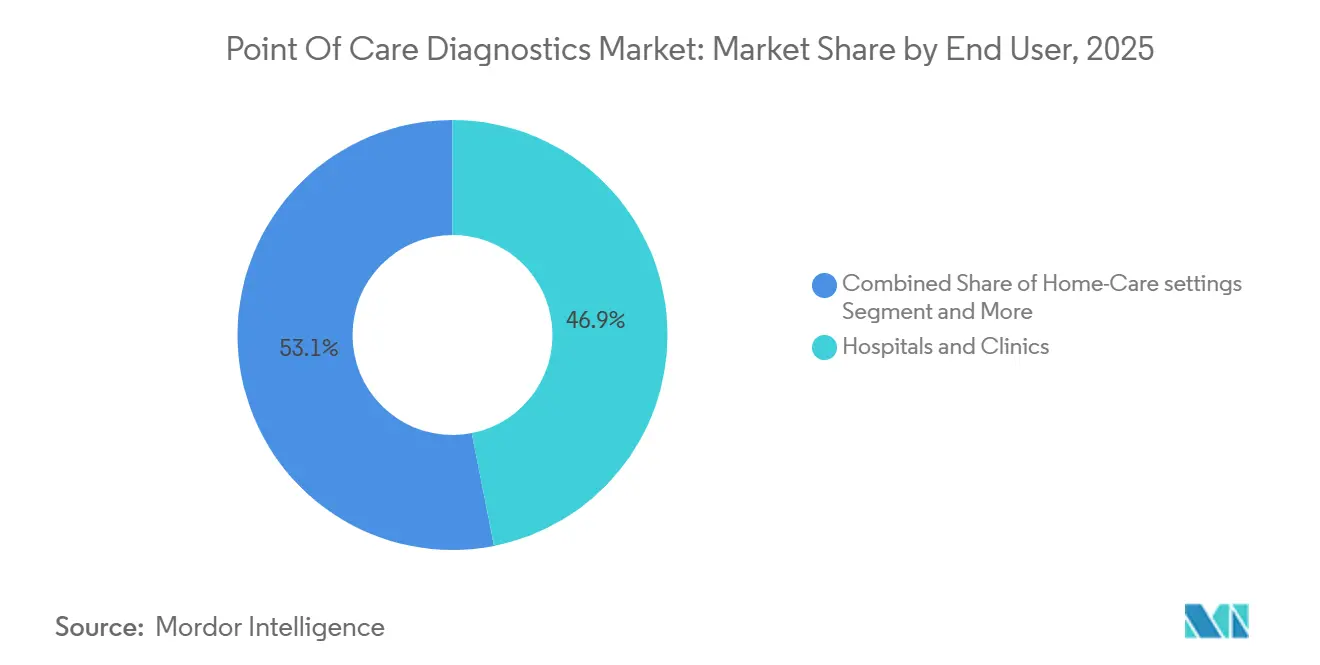

- By end user, hospitals and clinics retained 46.92% of 2025 demand, yet home-care settings are set to grow at an 11.28% CAGR through 2031.

- By geography, North America commanded 45.67% of 2025 revenue; Asia-Pacific is forecast to post the highest regional CAGR at 10.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Point Of Care Diagnostics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic & Infectious Diseases | +2.5% | Global, with acute burden in APAC and Sub-Saharan Africa | Long term (≥ 4 years) |

| Technological Advances & Home-Based POC Uptake | +2.0% | North America & EU lead; APAC adoption accelerating | Medium term (2-4 years) |

| Surge in CLIA-Waived Molecular Respiratory Tests | +1.5% | North America dominates; EU and APAC following | Short term (≤ 2 years) |

| Increasing Regulatory Approvals for Novel Assays | +1.2% | Global, with FDA and EMA as pace-setters | Medium term (2-4 years) |

| AI-Enabled Smartphone Lateral-Flow Analytics | +0.8% | North America and EU early adopters; APAC scale potential | Medium term (2-4 years) |

| Microfluidic Paper-Chips in Philanthropic Screenings | +0.5% | Sub-Saharan Africa and South Asia priority regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic and Infectious Diseases

Globally, 537 million adults lived with diabetes in 2024, and the International Diabetes Federation projects 643 million by 2030, underscoring sustained demand for glucose monitoring kits.[1]International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” idf.org Parallel outbreaks, such as dengue in Southeast Asia and mpox in Central Africa, have prompted governments to stockpile rapid diagnostic tests. WHO prequalified 12 new malaria rapid tests in 2025, allowing procurement agencies to source assays that meet stringent sensitivity thresholds for low-parasitemia detection. Abbott supplied 15 million malaria tests to India’s National Health Mission the same year, covering districts where laboratory microscopy remains unavailable in 40% of primary health centers. Cepheid’s GeneXpert MTB/RIF Ultra assay shortened tuberculosis time-to-treatment in South African clinics from 14 days to under 2 hours, demonstrating the clinical advantage of rapid molecular testing. This dual burden of chronic management and outbreak response creates a structural tailwind that lifts the point-of-care diagnostics market across income settings.

Technological Advances and Home-Based POC Uptake

Medicare introduced CPT 99454 in the 2025 Physician Fee Schedule, reimbursing USD 64 per patient per month for devices transmitting physiological data at least 16 days a month. Roche’s CoaguChek systems now qualify for virtual INR consultations under this code, while Abbott’s Bluetooth-enabled FreeStyle Libre 3 Plus streams glucose readings every minute for remote insulin titration. Dexcom’s over-the-counter Stelo sensor, approved in June 2024, opened continuous glucose monitoring to 30 million U.S. Type 2 diabetics previously outside insurance coverage. Smartphone penetration above 70% in many emerging markets further lowers barriers for cloud-linked diagnostic devices. As sensor miniaturization converges with reimbursement reform, the hospital-centric testing model is giving way to decentralized, patient-directed workflows that expand the point-of-care diagnostics market.

Surge in CLIA-Waived Molecular Respiratory Tests

FDA granted CLIA-waived status to eight molecular respiratory panels between 2024 and 2025, including Cepheid’s Xpert Xpress Flu/RSV and Roche’s cobas Liat Influenza A/B & RSV, permitting deployment in physician offices without high-complexity lab certification.[2]U.S. Food and Drug Administration, “Medical Device Databases,” fda.gov Molecular POC assays reach sensitivities above 95% while delivering results in 15-20 minutes, compared with 50-70% for antigen-based lateral flow tests. CMS reimburses CLIA-waived molecular assays at USD 45-75 per panel, creating an economic incentive for practices to upgrade. Cartridge demand responded sharply, with Cepheid shipping 2.3 million Xpert Xpress units in Q3 2024, a 35% year-on-year surge. The waived designation effectively shifts highly sensitive PCR testing from reference labs to frontline clinicians, reinforcing the growth trajectory of the point-of-care diagnostics market.

Increasing Regulatory Approvals for Novel Assays

FDA cleared 47 new POC devices in 2024, 22% more than the prior year, under an expedited 510(k) pathway for products demonstrating substantial equivalence to predicate systems. Notable examples include Sonic Incytes’ Velacur ONE urinalysis analyzer and NOWDiagnostics’ finger-stick ADEXUSDx Syphilis Test. China’s NMPA authorized Roche’s cobas Liat platform in 2024, unlocking access to 36,000 township health centers that serve 600 million rural residents. The European Medicines Agency granted CE-IVD marks to 12 new POC cardiac biomarker assays during 2024-2025, enabling one-hour myocardial infarction rule-outs in emergency departments. Faster approvals compress time-to-market, allowing manufacturers to ride outbreak-driven demand spikes and broaden the global footprint of the point-of-care diagnostics market.

Restraints Impact Analysis of Point Of Care Diagnostics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulations & Reimbursement Gaps | -1.5% | Global, acute in North America and EU | Medium term (2-4 years) |

| Product Recalls & Accuracy Concerns | -1.0% | North America leads; global spillover | Short term (≤ 2 years) |

| QC Non-Compliance Penalties in US POLs | -0.5% | United States exclusively | Short term (≤ 2 years) |

| Cold-Chain Gaps for Molecular Cartridges in Africa | -0.3% | Sub-Saharan Africa and remote APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations and Reimbursement Gaps

FDA guidance issued in 2024 raised analytical validation thresholds for POC molecular tests to at least 95% positive and 98% negative percent agreement across three diverse clinical sites. CMS then cut payment for several CLIA-waived codes by 8-12% in the 2025 fee schedule, squeezing the economics for smaller practices.[3]Centers for Medicare & Medicaid Services, “2025 Physician Fee Schedule Final Rule,” cms.gov Private insurers, such as Anthem, introduced prior-authorization rules that limit respiratory pathogen panels to high-risk patients. In Europe, the In Vitro Diagnostic Regulation deadline of May 2025 forced roughly 30% of legacy POC devices off the market because manufacturers could not secure notified-body audits. These policy shifts raise compliance costs and curb near-term adoption, tempering growth in the point-of-care diagnostics market.

Product Recalls and Accuracy Concerns

The FDA issued Class I recalls for 3.7 million TRUEresult and TRUEtrack glucose meters in May 2024 after software errors produced falsely elevated readings in hypoglycemic patients. Abbott followed with a voluntary recall of 3.6 million FreeStyle Libre 2 readers in October 2024 due to battery overheating risks. Such events erode clinician confidence, prompting hospital procurement committees to demand third-party accuracy audits before adopting new platforms. A 2024 College of American Pathologists survey found 18% of POC glucose meters in physician offices reported out-of-range results, compared with 4% for central laboratory analyzers. Ongoing safety alerts create scrutiny that can delay purchasing decisions, softening short-term demand within the point-of-care diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Point Of Care Diagnostics Market Segment Analysis

By Product:

Glucose Monitoring Anchors Revenue, Infectious Disease AcceleratesGlucose monitoring kits maintained 37.94% of the point-of-care diagnostics market share in 2025, supported by the ubiquity of capillary blood glucose meters and the rapid uptake of CGM sensors. Infectious disease kits, however, are forecast to grow at a 10.27% CAGR through 2031 as global health agencies prequalify new rapid assays for malaria, tuberculosis, and sexually transmitted infections. Cardiometabolic panels built around high-sensitivity troponin and BNP markers are standard in 85% of U.S. emergency departments for rapid myocardial infarction rule-outs. Coagulation kits, led by Roche’s CoaguChek, benefit from Medicare reimbursement for patient self-testing of INR. Pregnancy and fertility kits retain high volume in retail channels, while digital ovulation monitors are carving premium subsegments. Blood gas and electrolyte cartridges remain mission-critical in critical care units, and AI-enabled hematology analyzers such as Sight Diagnostics’ OLO are lowering the entry threshold for urgent care clinics.

The product mix is likely to rebalance as closed-loop insulin delivery systems pair CGMs with automated pumps, yet novel infectious disease panels promise faster relative growth. Manufacturers that integrate wireless connectivity and cloud analytics into commodity product lines stand to extend lifetime revenue per user, fortifying their positions within the point of care diagnostics market.

By Platform:

Molecular Diagnostics Outpace Lateral FlowLateral flow assays captured 34.12% of revenue share in 2025, driven by entrenched pregnancy and antigen test volumes. Molecular diagnostics platforms, however, are scaling at a 10.51% CAGR, supported by PCR cartridges that deliver sample-to-answer results in under 30 minutes without high-complexity lab certification. Dipsticks and test strips remain the highest-volume consumables but face commoditization as smartphone cameras replace dedicated optical readers.

Microfluidic cartridges, such as Abbott’s i-STAT, house multiple chemistries, electrolytes, blood gases, and cardiac markers in a palm-sized single-use chip that returns results in under 10 minutes. Immunoassay analyzers serve mid-throughput hospital labs, bridging the gap between bedside testing and central automation. As PCR becomes simpler and cheaper, molecular systems are expected to erode lateral flow's share in physician offices, home care, and retail clinics, further expanding the market for high-sensitivity diagnostics at the point of care.

By Sample Type:

Blood Dominates, Respiratory Swabs SurgeBlood draws accounted for 68.26% of overall test volume in 2025, led by glucose, cardiac biomarker, and coagulation assays. Respiratory swabs are projected to rise at a 10.42% CAGR through 2031 as national surveillance programs institutionalize same-visit PCR testing for influenza, RSV, and SARS-CoV-2. Urine remains routine in pregnancy and urinalysis testing, while saliva is gaining acceptance in HIV self-testing and nascent oral glucose monitoring. Sweat and tear specimens stay niche but underscore continued innovation in non-invasive sampling. The pivot toward nasal and throat swabs reflects a public-health imperative to triage respiratory infections quickly, reinforcing the versatility of the point-of-care diagnostics market.

Respiratory-focused sampling also shortens antiviral prescribing windows, while capillary blood retains unmatched breadth across analytes. Vendors that support both specimen types diversify revenue streams, positioning them for sustained participation in the broader point-of-care diagnostics industry.

By Mode of Purchase:

OTC Channels Lead, Prescription Segment AcceleratesOver-the-counter test kits accounted for 61.44% of 2025 revenue, driven by pregnancy tests, glucose meters, and emerging consumer-friendly molecular assays. Prescription-based diagnostics are forecast to grow at a 10.01% CAGR through 2031 as payers cover complex panels that require clinical oversight, such as CLIA-waived PCR respiratory assays and cardiac biomarker tests. FDA guidance issued in 2024 set analytical benchmarks for OTC molecular tests, spurring device makers to improve sensitivity and specificity. Dexcom’s Stelo sensor illustrates boundary blurring by selling CGM technology directly to consumers yet integrating data with physician dashboards. Reimbursement for self-testing of coagulation parameters under CPT 99454 further narrows the gap between retail convenience and clinician-supervised care. The coexistence of OTC and prescription channels broadens consumer access and sustains the multi-tiered growth path of the point-of-care diagnostics market.

By End User:

Home-Care Settings Disrupt Hospital-Centric ModelHospitals and clinics commanded 46.92% share of 2025 demand, driven by emergency departments that rely on rapid cardiac and coagulation panels to triage acute cases. Home-care settings, however, are pacing the field with an 11.28% CAGR through 2031, driven by Medicare reimbursement for remote physiologic monitoring and advancements in cellular-connected CGM and INR devices. Roche’s CoaguChek and Abbott’s Libre 3 Plus enable patients to self-test and push data to physicians who can adjust therapy without in-person visits. Ambulances, retail clinics, and workplace wellness programs are also deploying compact analyzers to expedite diagnosis and reduce downstream healthcare costs. As chronic disease prevalence mounts, the ability to monitor patients continually rather than episodically will remain a pivotal growth vector for the point-of-care diagnostics market size.

Geography Analysis

North America Point Of Care Diagnostics Market

North America retained 45.67% revenue share in 2025, supported by a dense network of CLIA-certified physician office laboratories and generous Medicare coverage for both molecular and remote monitoring devices. The FDA cleared 47 POC devices in 2024 under its accelerated 510(k) process, fostering rapid commercialization cycles. Cepheid maintains an installed base of 12,000 GeneXpert units across urgent care centers and emergency departments, driving cartridge growth of 35% year over year in Q3 2024. However, reimbursement cuts for certain waived tests and private-payer prior authorization hurdles may temper future expansion.

APAC Point Of Care Diagnostics Market

Asia-Pacific is the fastest-growing region, projected to log a 10.74% CAGR through 2031 as China and India roll out rural health initiatives. China’s NMPA cleared Roche’s cobas Liat system in 2024, unlocking access to a network of 36,000 township clinics serving 600 million residents. India’s National Health Mission distributed 15 million Abbott malaria rapid tests in 2025 to areas where microscopy is unavailable in 40% of primary centers. Japan, South Korea, and Australia are also expanding coverage for CGM and AI-enabled diagnostics, expanding the point-of-care diagnostics market in developed Asia.

Europe, Africa and Oceania Point Of Care Diagnostics Market

Europe is navigating the stringent IVDR regime that removed roughly 30% of legacy POC devices from the market by May 2025. Germany expanded reimbursement for patient-managed INR testing, while the UK’s National Health Service deployed Roche cobas Liat units in 200 general practices to curb inappropriate antibiotic prescribing. Southern European nations procured rapid respiratory assays ahead of the 2025 flu season, acknowledging laboratory staffing gaps in rural areas. Cold-chain limitations continue to constrain molecular cartridge deployment in parts of Africa and remote Pacific islands, yet donor-funded programs are bridging those gaps. Overall, regional policies and infrastructure investments shape a mosaic of opportunities that together reinforce the growth trajectory of the point of care diagnostics market.

Competitive Landscape

The point of care diagnostics industry shows moderate concentration: the top five vendors, Abbott, Roche, Siemens Healthineers, Danaher, and QuidelOrtho, collectively hold a majority of global share. Roche strengthened its position by acquiring LumiraDx in 2024, adding multi-parameter diagnostics platforms popular in UK primary care. Danaher’s Cepheid unit leverages its broad GeneXpert footprint to lock in high-margin cartridge sales, shipping 2.3 million Xpert Xpress units in Q3 2024 alone. Abbott integrates its FreeStyle Libre CGM with LibreView cloud software, retaining users through data services.

Competition is intensifying as AI-enabled readers convert commodity test strips into connected diagnostics. Sight Diagnostics’ OLO hematology analyzer employs computer vision to deliver complete blood counts in 10 minutes and now operates in 150 U.S. urgent care centers. Paper-based microfluidic devices priced under USD 2 per test, funded by the Bill & Melinda Gates Foundation, threaten to undercut lateral flow assays in mass-screening programs. Meanwhile, patent expirations in glucose test strips invite value-brand competition, pressuring incumbent margins.

Regulatory compliance remains a moat: FDA’s 2024 guidance requires extensive multi-site validation, favoring firms with established clinical trial infrastructure. Strategic partnerships are also shaping the landscape; Dexcom integrates its CGM sensors with Tandem and Insulet insulin pumps, forming closed-loop ecosystems that reinforce device stickiness. As high-sensitivity molecular and AI-driven platforms capture hospital and urgent care channels, low-cost paper-chip assays address mass-screening needs in resource-constrained regions, confirming the diverse yet interconnected future of the point of care diagnostics market.

Point Of Care Diagnostics Industry Leaders

F. Hoffmann-La Roche Ltd

Abbott Laboratories

Siemens Healthineers AG

Danaher Corporation

QuidelOrtho

- *Disclaimer: Major Players sorted in no particular order

Point Of Care Diagnostics Market Companies Covered in this Report

- Abbott Laboratories

- Accubiotech Co. Ltd.

- Beckton Dickinson

- bioMérieux

- Bio-Rad Laboratories

- Chembio Diagnostics Inc.

- Danaher Corporation (Cepheid & Beckman Coulter)

- EKF Diagnostics

- Roche

- HemoCue AB

- Johnson & Johnson

- LumiraDx

- Nova Biomedical

- Orasure Technologies

- PTS Diagnostics

- QuidelOrtho

- Radiometer Medical ApS

- Sekisui Diagnostics

- Siemens Healthineers

- Trinity Biotech plc

- Werfen (Instrumentation Laboratory)

Recent Industry Developments in Point Of Care Diagnostics Market

- December 2025: Roche received FDA clearance and a CLIA waiver for its first point-of-care PCR test for whooping cough, providing results in 15 minutes.

- November 2025: Sciverse Solutions and Bhat Biotech collaborated in November 2025 to co-develop AI-enabled molecular diagnostic platforms for portable point-of-care testing in India.

- June 2025: Philips launched the Flash 5100 POC cart-based point-of-care ultrasound system with AI-powered automation software

Point Of Care Diagnostics Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the point-of-care (POC) diagnostics market as all disposable tests, instruments, and connected readers that deliver clinical results at or near the patient, including physician offices, ambulances, pharmacies, and home settings, spanning glucose monitoring, infectious disease, cardiometabolic, pregnancy, hematology, urinalysis, coagulation, and emerging molecular formats.

Scope exclusion: veterinary POC products, standalone data management software, and central lab rapid analyzers are outside this review.

Segments Covered in This Report

- By Product

- Glucose Monitoring Kits

- Infectious Disease Testing Kits

- Cardiometabolic Testing Kits

- Coagulation Monitoring Kits

- Pregnancy & Fertility Testing Kits

- Blood Gas / Electrolyte & Metabolite Kits

- Hematology Testing Kits

- Tumor / Cancer Marker Testing Kits

- Urinalysis Testing Kits

- Cholesterol Test Strips

- By Platform

- Lateral Flow Assays

- Dipsticks & Test Strips

- Microfluidics-Based Platforms

- Immunoassays (CLIA & FIA)

- Molecular Diagnostics (PCR, INAAT)

- By Sample Type

- Blood

- Urine

- Saliva

- Nasal / Throat Swab

- Other Specimens (Sweat, Tear, CSF)

- By Mode of Purchase

- Over-the-Counter (OTC)

- Prescription-Based

- By End User

- Hospitals & Clinics

- Home-Care Settings

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interview laboratory managers, emergency physicians, retail clinic buyers, and POC device distributors across North America, Europe, Asia-Pacific, and selected Middle East hubs. These discussions validate adoption curves, typical device utilization, reagent pull-through, and forward ASP expectations that secondary sources seldom quantify with precision.

Desk Research

We begin with structured desk work that pulls 10-K filings, device registrations, and trade statistics from agencies such as the US FDA, the European Medicines Agency, and UN Comtrade, which anchor shipment counts and average selling prices. Supplementary context is drawn from peer-reviewed journals (e.g., Clinical Chemistry), global health portals of the WHO, and market-wide policy notes released by the OECD. Company investor decks, earnings transcripts, and procurement databases like D&B Hoovers and Dow Jones Factiva enrich competitive share and price erosion insights. This list is illustrative, not exhaustive; many additional sources guide indicator selection and sense checks throughout the build.

Market-Sizing & Forecasting

A top-down demand pool is first reconstructed from diabetes prevalence, respiratory infection incidence, emergency department visit volumes, and pharmacy footprint expansion, which are then translated into test opportunities through setting-specific penetration rates. Supplier roll-ups (sampled kit volumes multiplied by blended ASPs) provide a bottom-up cross-check, with gaps bridged by channel checks and invoice triangulation. Key model variables include chronic disease incidence, rapid test reimbursement codes, OTC kit sales growth, molecular platform installed base, and currency movements. Multivariate regression, complemented by scenario analysis for pandemic-driven surges, projects each driver before results cascade into the five-region outlook.

Data Validation & Update Cycle

Outputs pass variance filters against historic shipments, periodic analyst peer reviews, and anomaly alerts triggered when quarterly sales swings exceed our +/-7% threshold. Reports refresh yearly, and material regulatory or recall events prompt interim revisions, ensuring clients receive the newest view before publication.

How Mordor Intelligence's Point Of Care Diagnostics Market Size Compares to Other Published Estimates

Published figures often diverge because firms pick dissimilar product baskets, pricing assumptions, and refresh cadences.

Key gap drivers include narrower test menus, single-region price anchoring, and conservative uptake multipliers used by some publishers, whereas Mordor's model covers multi-setting usage, reconciles kit and cartridge ASP drift every year, and applies currency-consistent conversions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 53.63 B (2025) | Mordor Intelligence | - |

| USD 31.57 B (2024) | Global Consultancy A | Excludes OTC self-testing kits and applies static ASP assumptions |

| USD 15.05 B (2024) | Market Research Firm B | Limits scope to five core products and uses 2019 exchange rates |

Taken together, the comparison shows how Mordor's annually refreshed, scope-complete model yields a balanced baseline that decision makers can trace back to transparent variables and repeatable steps, reducing uncertainty when allocating resources or screening new POC opportunities.

Key Questions Answered in the Report

How large will be point of care diagnostics market in 2026?

The point of care diagnostics market size is estimated to be USD 58.76 billion in 2026, with a projected CAGR of 9.9% through 2031.

Which product category currently generates the most revenue?

Glucose monitoring kits lead with 37.94% of 2025 revenue, supported by widespread use of capillary meters and continuous glucose monitors.

What is driving the rapid growth of molecular diagnostics at the point of care?

CLIA-waived status for PCR respiratory panels, higher clinical sensitivity, and streamlined sample-to-answer workflows are pushing molecular platforms ahead.

Which region will grow the fastest by 2031?

Asia-Pacific is expected to post the highest CAGR at 10.74%, propelled by approvals in China and large-scale public-health procurements in India.

What level of market concentration exists among leading vendors?

The top five companies control a majority of global revenue, reflecting moderate concentration with room for niche and disruptive entrants.

Page last updated on: