Neurodegenerative Disease Diagnostics Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

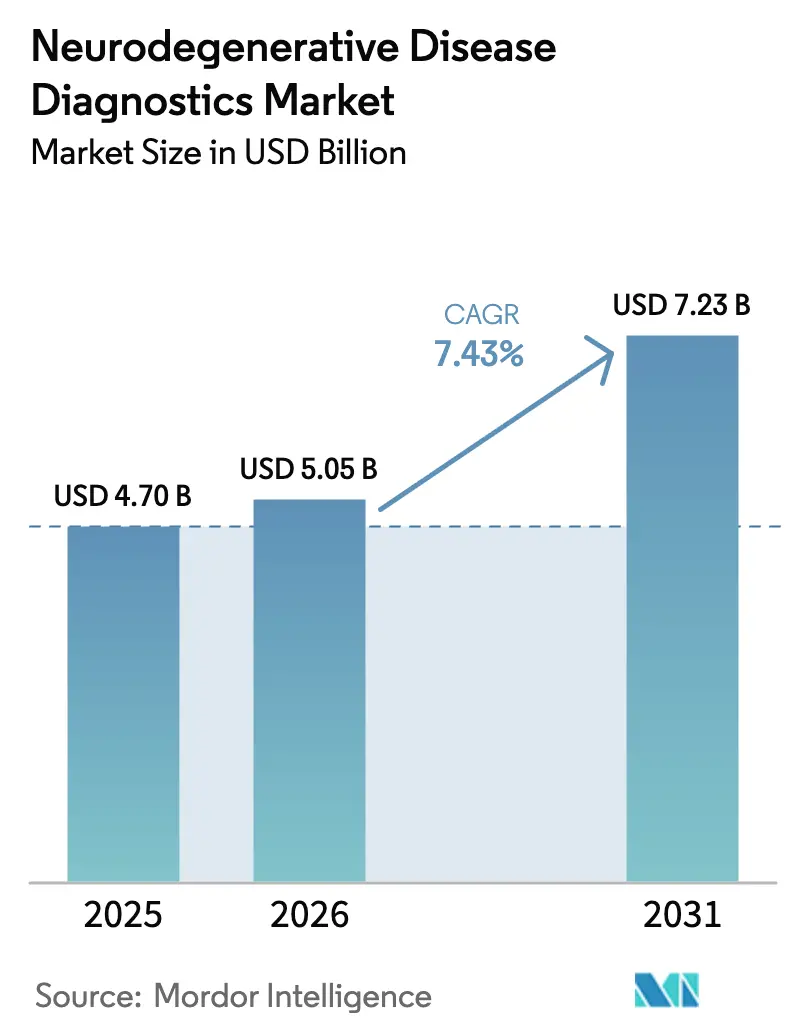

| Market Size (2026) | USD 5.05 Billion |

| Market Size (2031) | USD 7.23 Billion |

| Growth Rate (2026 - 2031) | 7.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurodegenerative Disease Diagnostics Market Analysis by Mordor Intelligence

Neurodegenerative Disease Diagnostics Market size market size in 2026 is estimated at USD 5.05 billion, growing from 2025 value of USD 4.70 billion with 2031 projections showing USD 7.23 billion, growing at 7.43% CAGR over 2026-2031.

A rapid pivot from cerebrospinal fluid sampling toward blood-based biomarkers is reshaping the competitive field. Leading companies are extending established imaging portfolios with molecular-level assays, while start-ups are commercializing plasma tests that allow earlier, primary-care intervention. Regulatory fast-track pathways and payer pilots that recognize the long-term cost savings of timely diagnosis further underpin demand. Heightened venture funding and big-tech cloud partnerships channel artificial-intelligence tools into image analysis and multimodal data fusion, creating new service revenue streams.

Key Report Takeaways

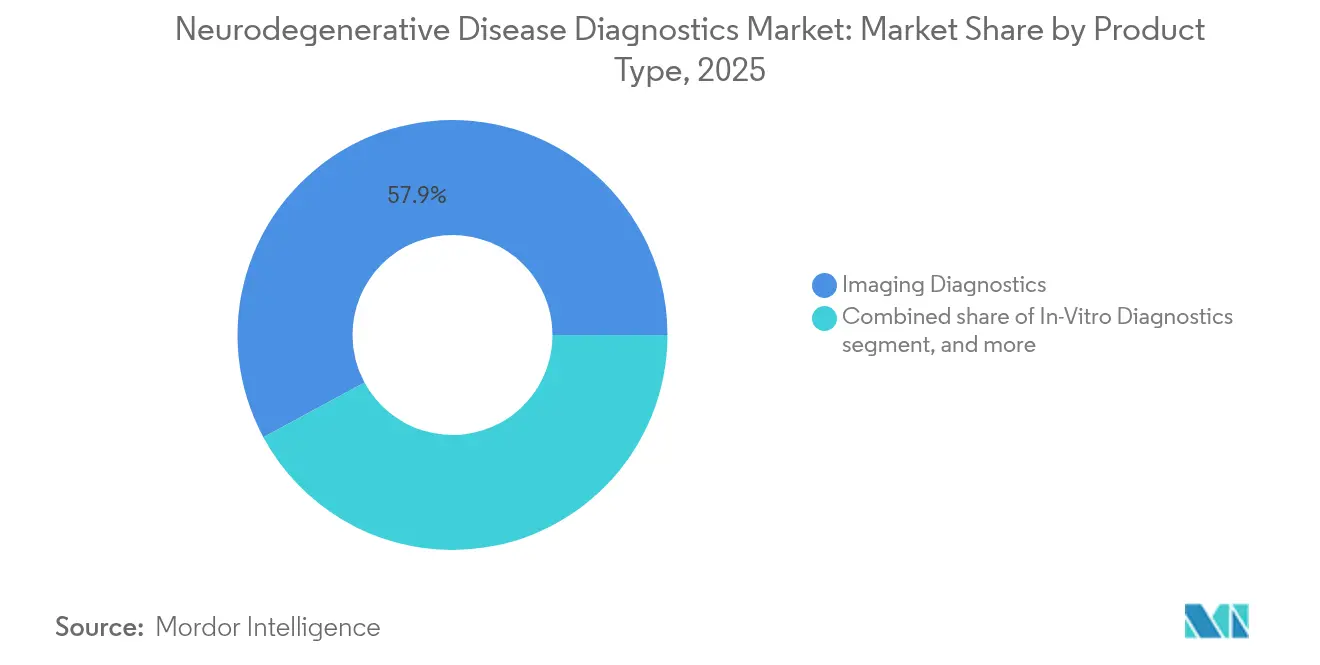

- By product type, imaging diagnostics led with 57.88% revenue share in 2025, while in-vitro diagnostics is forecast to expand at a 9.41% CAGR from 2026 to 2031.

- By biomarker type, protein assays (Aβ, Tau, α-synuclein) commanded 55.64% of 2025 sales, whereas genetic panels (SNCA, APP, MAPT, HTT, PSEN) are poised to grow at a 9.86% CAGR through the forecast period.

- By application, Alzheimer’s disease accounted for 49.10% of sector turnover in 2025, and Parkinson’s disease is advancing at a 10.50% CAGR to 2031.

- By end user, hospitals captured 46.02% of global revenue in 2025, while diagnostic laboratories are projected to register a 10.31% CAGR over 2026-2031.

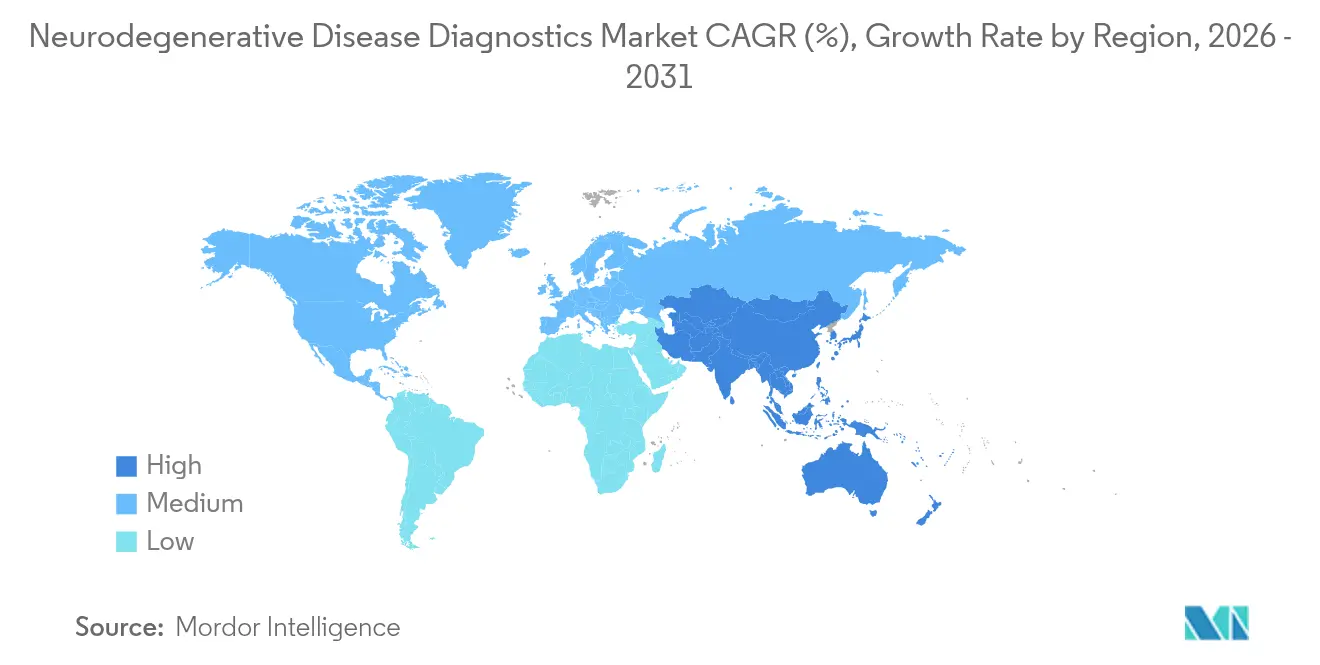

- By geography, North America held 41.78% of the market in 2025, whereas Asia-Pacific is expected to record the fastest regional growth at an 8.46% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurodegenerative Disease Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of neurodegenerative disorders | +2.1% | Global, led by North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Technological advancements in diagnostic imaging | +1.8% | North America & EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Expansion of fluid biomarker test availability | +2.3% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Supportive regulatory frameworks for early detection | +1.2% | North America, EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rising investments in precision neurology | +1.5% | Global, led by North America and China | Medium term (2-4 years) |

| Emergence of home-based cognitive screening tools | +0.8% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Neurodegenerative Disorders

The world is aging quickly; the World Health Organization estimates that 1 in 6 people will be at least 60 years old by 2030[1]World Health Organization, “Decade of Healthy Ageing Baseline Report,” who.int. China already faces 17 million early-stage Alzheimer’s patients, and local firms are promoting online self-assessment tools that channel suspects toward confirmatory plasma testing. With an estimated 75% of dementia cases still undiagnosed, primary-care physicians are turning to blood assays that can be performed in routine panels, reducing the need for in-hospital cerebrospinal taps.

Technological Advancements in Diagnostic Imaging

Artificial-intelligence platforms are lifting the sensitivity of MRI and PET scans. GE HealthCare and NVIDIA jointly train algorithms that locate subtle structural changes in seconds, easing radiologist backlogs. Hyperfine’s portable MRI allows bedside brain imaging in remote facilities, opening access to three billion individuals previously beyond reach. Novel PET tracers such as [18F]OXD-2314 visualize tau aggregates in non-Alzheimer’s tauopathies, broadening clinical indications.

Expansion of Fluid Biomarker Test Availability

C2N Diagnostics’ PrecivityAD2 plasma panel posts 89% accuracy against gold-standard amyloid PET, prompting Samsung to back a global lab rollout. Veravas’ VeraBIND Tau yields 96% sensitivity and 90% specificity, surpassing typical primary-care evaluations. Multi-analyte formats on Quanterix’s ultra-sensitive Simoa platform now combine p-Tau 217 with GFAP and NfL to refine prognostication.

Supportive Regulatory Frameworks for Early Detection

The US FDA has awarded Breakthrough Device status to several plasma tests, including Roche’s Elecsys p-Tau 217 and Beckman Coulter’s Access p-Tau217/β-Amyloid ratio, accelerating market entry. Darmiyan’s BrainSee software gained clearance to predict Alzheimer’s progression from standard MRI, demonstrating openness to digital diagnostics. China’s NMPA has authorized more than 40 neuroimaging radiopharmaceuticals, endorsing advanced diagnostics in the world’s largest aging population.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced diagnostic procedures | −1.4% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Limited reimbursement for novel assays | −1.1% | North America, Europe, expanding globally | Medium term (2-4 years) |

| Supply constraints of radiopharmaceuticals | −0.9% | North America & Europe, episodic global effects | Short term (≤ 2 years) |

| Data privacy and ethical concerns in AI diagnostics | −0.7% | Global, stricter in EU & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Diagnostic Procedures

Conventional amyloid PET can exceed USD 5,000 per scan and requires specialized cyclotron-adjacent facilities, limiting availability in low-resource settings[2]U.S. Food & Drug Administration, “Amyloid PET Scan Safety Communication,” fda.gov. Darmiyan prices its BrainSee AI at USD 1,500 per report, discounted to USD 300 if Medicare reimbursement is granted. Such disparities favor lower-cost plasma solutions but still restrain uptake where out-of-pocket payment dominates.

Limited Reimbursement for Novel Assays

Medicare covers only select molecular diagnostics that meet analytic-validity criteria and documented clinical utility. Providers must navigate lengthy prior-authorization steps and demonstrate that results will alter patient management. Private insurers follow suit, requesting real-world evidence of reduced downstream care costs before full coverage[3]Centers for Medicare & Medicaid Services, “Coverage Determination Process,” cms.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shift from Imaging Toward Molecular Testing

Imaging diagnostics have long anchored care pathways, yet the neurodegenerative disease diagnostics market is tilting toward molecular technologies as primary-care physicians request non-invasive screening. Fujirebio’s Lumipulse series now delivers amyloid results within three hours, a workflow compatible with high-throughput clinical labs. In-Vitro Diagnostics is forecast to outpace legacy modalities at a 9.41% CAGR on the back of regulatory clearances and falling per-test costs.

Radiopharmaceutical producers still secure dependable revenue from established PET tracers, but sporadic Mo-99 shortages during 2024 underscored supply risks. Digital solutions further depress imaging volume growth by triaging patients through blood tests before costly scans. AI software that converts raw MRI output into quantified brain atrophy indices adds value to existing systems yet aligns them with biomarker-centric workflows. The net result is a gradual rebalancing in favor of labs that can process plasma panels at scale.

By Biomarker Type: Genetic Panels Gather Momentum

Protein biomarkers such as Aβ42/40 and p-Tau 181 retained 55.64% share of the neurodegenerative disease diagnostics market size in 2025. Their popularity stems from validated immunoassay platforms and direct linkage to disease pathology.

Genetic markers are advancing fastest at a 9.86% CAGR, driven by cost-effective next-generation sequencing and point-of-care SNP assays. Beckman Coulter’s APOE ε4 cartridge provides results in under 90 minutes, guiding lifestyle counseling and trial eligibility. NfL continues to gain clinical traction as a pan-neurodegeneration marker useful in multiple sclerosis and traumatic brain injury. Meanwhile, GFAP and cell-free DNA profiles are emerging as adjuncts that improve sensitivity when combined with canonical proteins.

By Application: Parkinson’s Diagnostics Accelerate

Alzheimer’s retains 49.10% of the neurodegenerative disease diagnostics market share in 2025 owing to high prevalence and disease-modifying antibodies that necessitate biomarker confirmation.

Parkinson’s assays record the strongest 10.50% CAGR, propelled by CND Life Sciences’ Syn-One skin biopsy that detects alpha-synuclein aggregates months before motor onset. Multi-analyte CSF panels are refining multiple-sclerosis monitoring, while Huntington’s carriers benefit from predictive genotyping that informs family planning. Amyotrophic lateral sclerosis research leverages combined protein-gene signatures to shorten diagnostic delay.

By End User: Laboratories Spearhead Precision Medicine

Hospitals commanded 46.02% revenue in 2025 due to their imaging suites and neurological consult services.

Diagnostic laboratories are scaling test menus fast, achieving a 10.31% CAGR. Quest Diagnostics introduced a nationwide Alzheimer’s blood screen, and C2N Diagnostics’ pact with Unilabs extends coverage to over 75 countries. Imaging centers defend share by adopting AI overlays that boost interpretation throughput, while home-based platforms such as Linus Health feed pre-screened cases into lab pipelines.

Geography Analysis

North America accounted for 41.78% of 2025 revenue, supported by FDA Breakthrough Device programs and Centers for Medicare & Medicaid Services pilots that reimburse select plasma assays. The region also hosts the highest density of PET scanners and board-certified neurologists, sustaining volume for advanced imaging even as blood tests proliferate.

Asia-Pacific posts the strongest 8.46% CAGR to 2031. China’s launch of anti-amyloid antibody LEQEMBI has aligned therapeutic demand with diagnostic expansion; provincial health authorities are co-financing PET centers and subsidizing plasma tests for early-stage patients. Japanese consortia are piloting community clinics equipped with portable MRI units, while India invests in cloud-based cognitive-assessment kiosks marketed through primary care networks.

Europe grows steadily as national payers evaluate health-economic data submitted under the EU In Vitro Diagnostic Regulation. Scandinavian countries have already included plasma p-Tau in dementia pathways, and Germany’s Innovation Fund is trialing multi-marker panels linked to electronic health records. South America, the Middle East and Africa remain smaller today but represent sizeable white-space for mobile imaging and low-cost plasma kits as urban populations age.

Competitive Landscape

The field exhibits moderate concentration. Imaging incumbents—GE HealthCare, Siemens Healthineers and Philips—retain strong brand equity and service contracts but face mounting competition from molecular specialists.

Strategic alliances dominate. GE HealthCare collaborates with NVIDIA on accelerated image reconstruction, Amazon Web Services on generative-AI report drafting and Sutter Health on integrated diagnostic networks spanning more than 300 care sites.

Biomarker innovators raise sizeable rounds: CND Life Sciences closed USD 13.5 million in May 2025 to widen Syn-One distribution, while Quanterix licensed multiplex IP to pharma sponsors. Consolidation is also active; Lantheus paid USD 350 million for Life Molecular Imaging, securing the Neuraceq F-18 tracer that complements its cardiology nuclear portfolio. Sanofi’s USD 470 million acquisition of Vigil Neuroscience adds a TREM2 agonist program with companion-diagnostic potential.

Neurodegenerative Disease Diagnostics Industry Leaders

F. Hoffmann-La Roche Ltd

GE HealthCare

Creative Biogene

Danaher Corporation (Beckman Coulter, Inc.)

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Fujirebio received FDA clearance for the Lumipulse G p-Tau 217/β-Amyloid 1-42 plasma test, achieving 92% positive predictive value and 97% negative predictive value in trials.

- May 2025: CND Life Sciences raised USD 13.5 million to scale Syn-One skin-based alpha-synuclein testing.

- May 2025: Sanofi agreed to acquire Vigil Neuroscience for USD 470 million, adding VG-3927 to its pipeline.

- April 2025: Veravas launched VeraBIND Tau blood test with 96% sensitivity and 90% specificity.

- March 2025: Samsung invested USD 10 million in C2N Diagnostics for global expansion of Precivity blood tests.

- March 2025: Linus Health introduced Anywhere for Health Systems, recording 95% accuracy in early dementia detection.

Global Neurodegenerative Disease Diagnostics Market Report Scope

As per the scope of the report, neurodegenerative disease is a broad term used to denote a range of conditions that primarily affect the neurons in the brain. Neurodegenerative diseases are incurable, and neuron degradation leads to neurons' gradual death. The neurodegenerative disease diagnosis involves a combination of clinical evaluation and advanced imaging techniques.

The neurodegenerative disease diagnostics market is segmented into product type, application, end user, and geography. By product type, the market is segmented into diagnostic imaging and in-vitro diagnostics. By application, the market is segmented into Parkinson's disease, Alzheimer's disease, multiple sclerosis, Huntington's disease, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report also offers the market size and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Imaging Diagnostics | MRI |

| PET | |

| CT / SPECT | |

| In-Vitro Diagnostics | CSF Biomarker Assays |

| Blood-based Biomarker Tests | |

| Molecular Imaging Agents | |

| Digital & AI-Assisted Diagnostics |

| Protein (A?, Tau, ?-synuclein) |

| Neurofilament Light Chain (NfL) |

| Genetic (SNCA, APP, MAPT, HTT, PSEN) |

| Other Emerging Biomarker Types |

| Alzheimer's Disease |

| Parkinson's Disease |

| Multiple Sclerosis |

| Huntington's Disease |

| Amyotrophic Lateral Sclerosis (ALS) |

| Other Applications |

| Hospitals |

| Diagnostic Laboratories |

| Imaging Centers |

| Academic & Research Institutes |

| Home / Point-of-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Imaging Diagnostics | MRI |

| PET | ||

| CT / SPECT | ||

| In-Vitro Diagnostics | CSF Biomarker Assays | |

| Blood-based Biomarker Tests | ||

| Molecular Imaging Agents | ||

| Digital & AI-Assisted Diagnostics | ||

| By Biomarker Type | Protein (A?, Tau, ?-synuclein) | |

| Neurofilament Light Chain (NfL) | ||

| Genetic (SNCA, APP, MAPT, HTT, PSEN) | ||

| Other Emerging Biomarker Types | ||

| By Application (Disease) | Alzheimer's Disease | |

| Parkinson's Disease | ||

| Multiple Sclerosis | ||

| Huntington's Disease | ||

| Amyotrophic Lateral Sclerosis (ALS) | ||

| Other Applications | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| Imaging Centers | ||

| Academic & Research Institutes | ||

| Home / Point-of-Care Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the neurodegenerative disease diagnostics market in 2026?

It is valued at USD 5.05 billion in 2026, with a 7.43% CAGR projected to lift revenue to USD 7.23 billion by 2031.

Which biomarker category is expanding fastest?

Genetic markers are advancing at a 9.86% CAGR, outpacing proteins due to rapid point-of-care assay adoption and falling sequencing costs.

What drives Asia-Pacific growth?

Regulatory modernization, launch of disease-modifying therapies such as LEQEMBI and rapid expansion of diagnostic infrastructure combine to support an 8.46% CAGR.

Why are diagnostic laboratories growing faster than hospitals?

Laboratories benefit from high-throughput plasma assays that suit centralized automation and can be ordered directly by primary-care physicians.

Which companies lead imaging, and who leads biomarkers?

GE HealthCare, Siemens and Philips dominate imaging, while Fujirebio, C2N Diagnostics and Quanterix spearhead plasma-based biomarker innovation.

What is the key restraint on market expansion?

High costs of advanced imaging and uncertain reimbursement pathways for new assays slow adoption, particularly in emerging economies.

Page last updated on: