Allulose Crystal Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.29 Billion |

| Market Size (2031) | USD 0.43 Billion |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

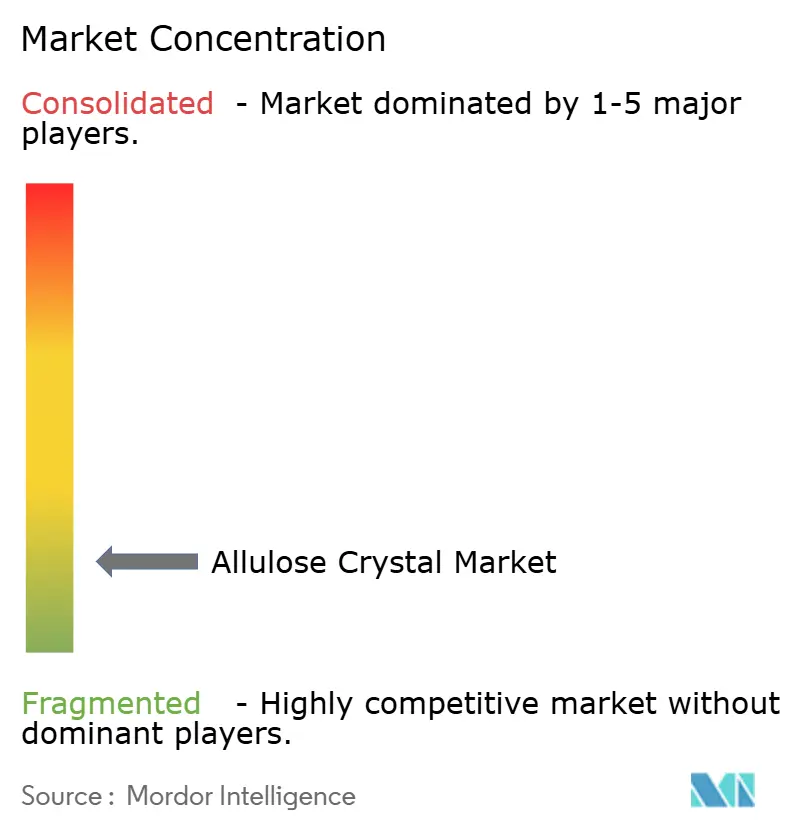

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Allulose Crystal Market Analysis by Mordor Intelligence

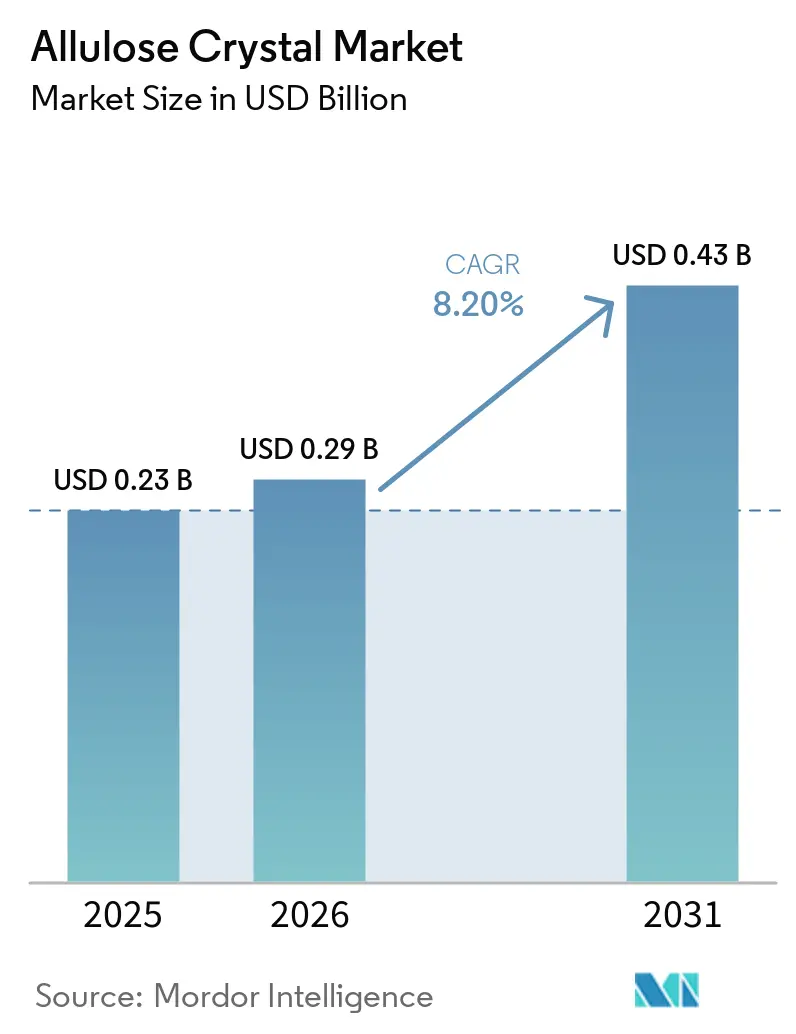

The allulose crystal market was valued at USD 0.23 billion in 2025 and reached USD 0.29 billion in 2026, reaching USD 0.43 billion by 2031, with a CAGR of 8.20% during 2026–2031. This growth reflects a significant shift in global sweetener demand driven by three key factors: the US FDA's decision to exempt allulose from "Added Sugars" declarations on Nutrition Facts labels, a growing body of clinical evidence supporting allulose's near-zero glycaemic impact, and advancements in industrial-scale enzyme immobilization technologies that are reducing the cost premium compared to conventional sweeteners. With a calorific value of approximately 0.2–0.4 kcal/g compared to sucrose's 4.0 kcal/g, allulose is emerging as a functionally superior rare sugar sweetener, offering both economic and consumer labeling advantages that earlier sugar alternatives could not achieve simultaneously.

Key Report Takeaways

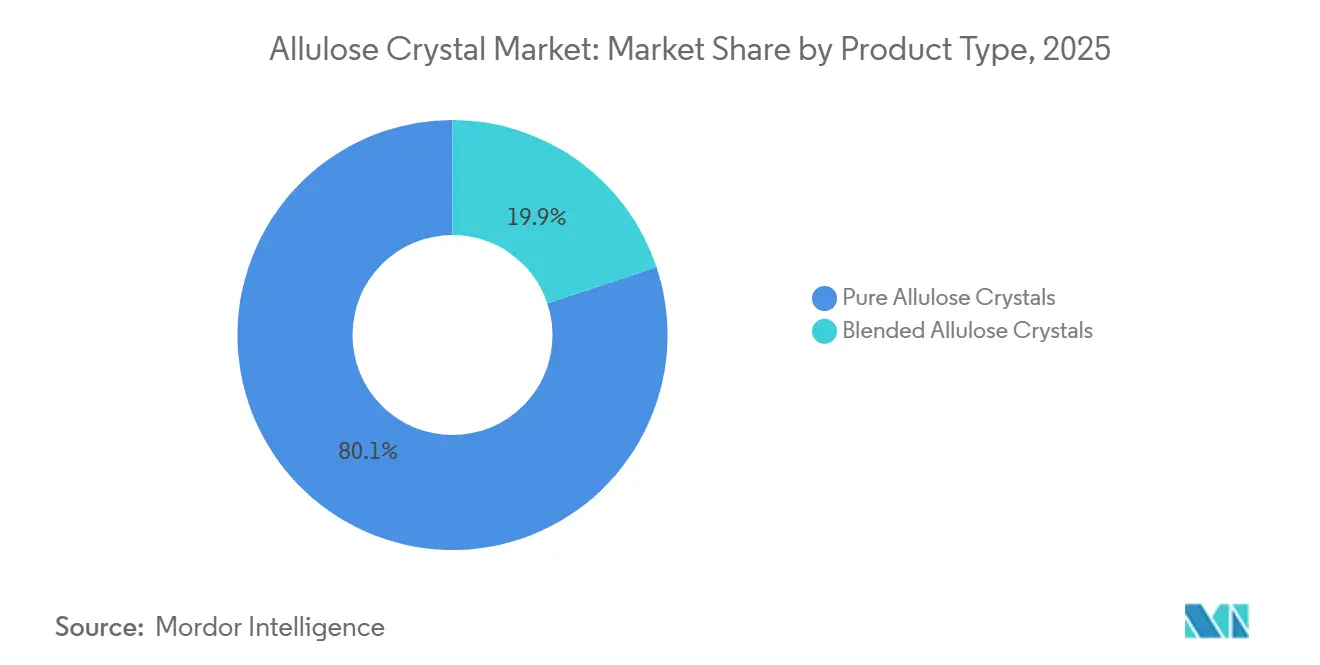

- By product type, pure allulose crystals captured 80.12%% of the 2025 market, while blended allulose crystals are advancing at a 9.29%% CAGR through 2031.

- By source, corn-based allulose retained a 72.12% share of the allulose crystal market size in 2025, while the sugar beet-based allulose segment is forecast to grow at an 8.56% CAGR through 2031.

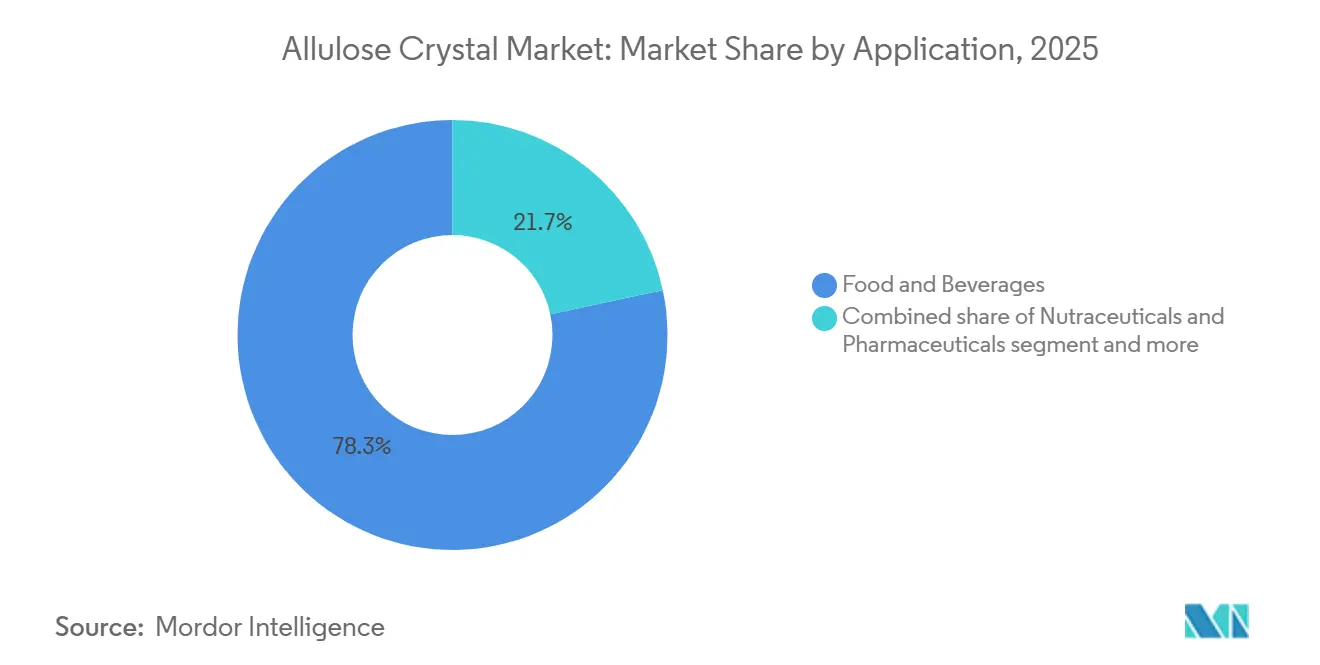

- By application, food and beverages accounted for 78.34% of demand in 2025, whereas nutraceuticals and pharmaceuticals are expanding fastest at an 8.87% CAGR between 2026-2031.

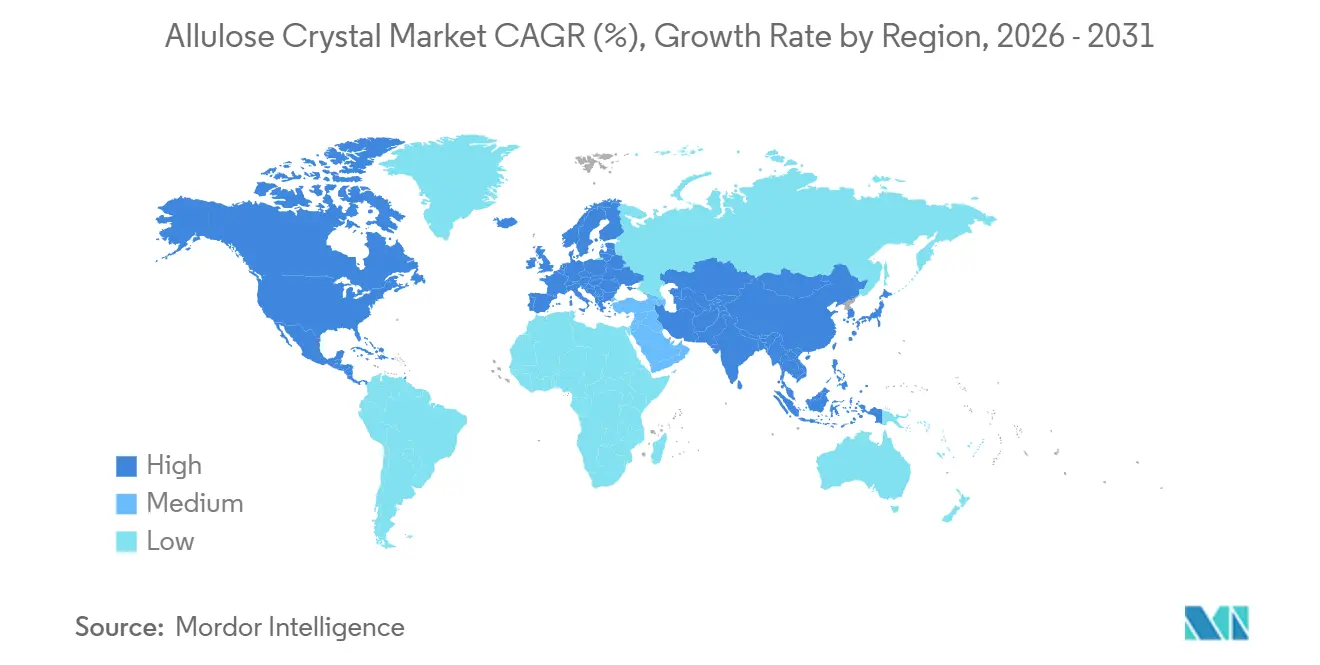

- By geography, North America accounted for 36.02% of 2025 revenue, but Asia-Pacific is the fastest-growing region, with a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Allulose Crystal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sugar-like reduced-calorie sweetening | +2.8% | Global | Short term (≤ 2 years) |

| Clean-label replacement of polyols in premium formulations | +1.3% | North America and the European Union | Medium term (2–4 years) |

| Growing demand for functional and better-for-you foods | +1.5% | Global | Medium term (2–4 years) |

| Increasing regulatory acceptance of allulose in key markets | +1.2% | Asia-Pacific core, spill-over to the Middle East and Africa | Short to medium term |

| Rising product innovation in reduced-sugar foods and beverages | +0.9% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Advancements in rare sugar production technologies | +0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for sugar-like reduced-calorie sweetening

The increasing demand for reduced-calorie sweetening solutions with sugar-like properties is a significant driver of the allulose crystal market. Food and beverage manufacturers are actively seeking alternatives that lower sugar content without compromising taste, texture, or functionality. Allulose stands out among alternative sweeteners for its sweetness profile and sensory experience, which closely resemble those of conventional sugar while offering significantly fewer calories. This makes it particularly appealing for use in beverages, bakery products, and confectionery. The rising prevalence of diabetes is further boosting the demand for low-calorie sweetening ingredients. According to the International Diabetes Federation (IDF) Diabetes Atlas 2025, 11.1% of the global adult population aged 20–79 years, equivalent to approximately 1 in 9 adults, had diabetes, with over 40% remaining undiagnosed. By 2050, the number of adults with diabetes is projected to reach approximately 853 million, marking a 46% increase[1]Source: International Diabetes Federation, "Diabetes Facts & figures", idf.org. As consumers become increasingly aware of the importance of blood sugar management and reducing overall sugar intake, the demand for sugar alternatives like allulose is expected to grow significantly, driving market expansion across food, beverage, and nutritional applications.

Clean-label replacement of polyols in premium formulations

The increasing demand for clean-label ingredients is driving the substitution of polyols and artificial sweeteners with allulose in premium food and beverage formulations. Manufacturers are focusing on sweetening solutions that deliver a sugar-like taste and functionality while meeting consumer preferences for simpler, more recognizable ingredient lists. This trend is particularly prominent among younger demographics, such as Gen Z and Millennials, who are willing to pay 20–30% more for products labeled as organic, natural, high-protein, or free from artificial ingredients[2]Source: Ingredion, "Less mystery, more meaning: Clean labels win consumer preference", ingredion.com. As consumers pay closer attention to product labels and prioritize naturally derived ingredients, food manufacturers are reformulating premium products with allulose to improve label appeal without compromising taste or product quality. The rising demand for clean-label sweetening solutions is anticipated to drive the adoption of allulose crystals across various premium food and beverage applications.

Growing demand for functional and better-for-you foods

The increasing demand for functional, health-focused foods is a key driver of the allulose crystal market. Consumers are prioritizing food and beverage products with enhanced nutritional profiles, reduced sugar content, and added health benefits, all while maintaining taste quality. The growth of the functional food industry further contributes to this market expansion. In Europe, the United Kingdom represents 23% of functional and fortified food and beverage sales, followed by Germany (16%), France (12%), Spain (10%), and Italy (9%) [3]Source: Glanbia Nutritionals, "Opportunities in Fortifying Functional Food and Beverage in Europe", glanbianutrition.com . As wellness, balanced nutrition, and healthier dietary choices gain importance among consumers, food manufacturers are incorporating ingredients like allulose to create products that meet these demands. This focus on health-oriented formulations is anticipated to sustain the demand for allulose crystals in the global food and beverage market.

Increasing regulatory acceptance of allulose in key markets

The increasing regulatory acceptance of allulose in major food and beverage markets is driving the growth of the allulose crystal market. Regulatory approvals provide manufacturers with the confidence to incorporate allulose into a broader range of products, supporting commercialization and fostering product innovation. As food safety authorities continue to recognize allulose as a viable low-calorie sweetening ingredient, its application is expanding across beverages, bakery products, confectionery, dairy products, and nutritional foods. Regulatory clarity further strengthens consumer trust and promotes investment in production capacity, product development, and supply chain expansion. Favorable labeling provisions and wider acceptance of allulose in key markets enable food companies to market reduced-sugar products more effectively while maintaining taste and functionality. As more countries assess and approve allulose for food applications, its global adoption is anticipated to grow, creating opportunities for market expansion across various end-use industries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of crystallization and purification | -1.8% | Global | Long term (≥ 4 years) |

| Competition from established alternative sweeteners | -0.9% | North America and European Union | Short term (≤ 2 years) |

| Limited production capacity and supply concentration | -0.7% | Global | Medium term (2–4 years) |

| Formulation challenges in some applications | -0.4% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High cost of crystallization and purification

The high cost of crystallization and purification poses a significant challenge to the allulose crystal market. Producing food-grade allulose crystals requires specialized processing technologies, advanced purification systems, and strict quality control measures to ensure the desired levels of purity, consistency, and functionality. These intricate manufacturing processes result in higher production costs than those of conventional sweeteners, making allulose a relatively expensive option for food and beverage manufacturers. This cost issue is particularly critical in price-sensitive applications, where manufacturers must balance affordability with sugar-reduction goals. Elevated ingredient costs can hinder the adoption of allulose in mass-market products, prompting some manufacturers to opt for lower-cost sweeteners or sweetener blends. Consequently, the premium pricing of allulose crystals can restrict market penetration, particularly in emerging markets and competitive food and beverage segments where cost efficiency is a key factor in purchasing decisions.

Competition from established alternative sweeteners

The allulose crystal market faces significant competition from established alternative sweeteners, including stevia, erythritol, monk fruit, sucralose, and xylitol. These sweeteners have achieved broader market penetration and consumer recognition, supported by well-developed supply chains, extensive application histories, and widespread use across various food and beverage categories. Their established presence poses challenges for allulose in gaining market share, particularly among manufacturers who have optimized product formulations around existing sweetening systems. The competitive environment is further intensified by ongoing advancements in alternative sweetener technologies, including blends designed to enhance taste, functionality, and cost efficiency. Although allulose provides several formulation benefits, manufacturers may be reluctant to transition from familiar sweeteners due to reformulation costs, ingredient sourcing challenges, and established consumer preferences. Consequently, competition from well-entrenched sweetener alternatives may slow the adoption of allulose in certain food and beverage applications, thereby limiting its overall market growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pure Crystals Anchor Volume While Blends Drive Formulation Premiumization

Pure allulose crystals accounted for 80.12% of market revenue in 2025, driven by their functional versatility across a wide range of food manufacturing applications. The crystal form provides consistent Maillard browning in baked goods, lowers the freezing point of frozen desserts to maintain a soft-scoop texture, and enables caramelization reactions that sugar alcohols cannot. Research published in ResearchGate (2025) also highlighted that these attributes help extend bakery shelf life by slowing starch retrogradation.

Blended allulose crystals are projected to be the fastest-growing product type, with a CAGR of 9.29% over 2026–2031. This growth is attributed to their cost-effective formulations, which address the economic challenges of pure allulose. By blending allulose with stevia leaf extract or monk fruit concentrate at optimized ratios, manufacturers leverage sweetness synergy effects. This approach reduces the total allulose content required per kilogram of finished product while maintaining a clean, full-sugar sweetness profile. Companies such as Cargill, Tate & Lyle, and Ingredion are actively commercializing this strategy through branded blend systems.

By Source: Corn Feedstock Defines Baseline Supply as Sugar Beet Builds Strategic Position

In 2025, corn-based allulose accounted for 72.12% of market revenue, supported by the geographic and economic advantages of corn starch as a feedstock in regions such as North America, South Korea, and China. The well-established corn wet-milling supply chains in the United States and the grain processing industry in South Korea provide a cost-stable and high-volume substrate for enzymatic production. This enables producers like Tate & Lyle (Loudon, Tennessee), Samyang Corporation (Ulsan, Korea), and Shandong Bailong Chuangyuan (China) to achieve production efficiencies that beet- or cane-sourced alternatives currently cannot match at scale.

Sugar beet-based allulose is projected to grow at a CAGR of 8.56% during 2026–2031, driven primarily by European supply chain strategies rather than cost competition with corn-based alternatives. Savanna Ingredients GmbH, a spinoff of Pfeifer & Langen based in Elsdorf, Germany, produces crystalline allulose from non-GMO sugar beet fructose. The company holds a self-affirmed US GRAS designation, making it the only European-origin crystalline allulose producer with active commercial supply channels in both North America and Europe.

By Application: Food and Beverage Volume Is Structural, Nutraceuticals Offer the Next Growth Frontier

The food and beverages segment accounted for 78.34% of market revenue in 2025. This dominance is attributed to allulose's unique functional performance in thermally processed formats and its regulatory labeling advantage under FDA rules. Within this segment, the Bakery and Confectionery sub-category holds the largest share. Allulose's ability to facilitate a genuine Maillard reaction, unlike the surface browning seen with many polyols, makes it essential for clean-label reformulations of cookies, muffins, and protein bars.

The nutraceuticals and pharmaceuticals segment is the fastest-growing application, with a CAGR of 8.87% projected for 2026–2031. This growth is driven by an expanding clinical evidence base, which is encouraging product development in dietary supplements, medical nutrition, and oral pharmaceutical delivery systems. A 2025 clinical review published in Glycoforum by researchers from Kagawa University, home to Japan's Rare Sugar Research Center, highlighted D-allulose's superior postprandial glucose suppression in type 2 diabetes patients. This study was the first to use continuous glucose monitoring to assess the effectiveness of dietary therapy.

Geography Analysis

In 2025, North America accounted for the largest geographic market share, holding 36.02% of revenue. This dominance is supported by a robust regulatory framework unparalleled in other regions. The US FDA's GRAS (Generally Recognized as Safe) framework has issued at least six no-objection letters for D-allulose applications. However, Canada had not included allulose in its List of Permitted Sweeteners as of March 2025, creating a regulatory disparity that hinders cross-border product harmonization for North American food manufacturers. This regulatory gap has implications for manufacturers aiming to streamline product offerings across the region.

The Asia-Pacific region is the fastest-growing geographic segment, with a 9.18% CAGR projected for 2026–2031. This growth is driven by simultaneous transformations in supply and demand across multiple markets. China's NHC (National Health Commission) Announcement No. 4 of 2025, issued on July 2, 2025, officially approved D-allulose as a new food ingredient. Following this approval, domestic producers such as Baolingbao Biotechnology and Shandong Bailong Chuangyuan have increased capacity investments, with Baolingbao targeting an annual production capacity of 30,000 tonnes. This approval has catalyzed regional production and market expansion efforts.

Europe remains the most commercially under-penetrated major market. The EFSA (European Food Safety Authority) NDA Panel issued a negative opinion on D-allulose as a novel food in June 2025, resulting in a regulatory holding pattern of uncertain duration. This regulatory stance has limited the market's growth potential in the region. Meanwhile, the Middle East and Africa offer long-term growth potential, driven by high rates of type 2 diabetes and obesity in Gulf Cooperation Council countries. Functional and reduced-sugar foods are gaining consumer interest in these regions. However, underdeveloped cold-chain infrastructure and limited regulatory frameworks for novel sweetener ingredients pose challenges to near-term commercialization.

Competitive Landscape

The allulose crystal market is highly fragmented, reflecting an industry where production is technically accessible to multiple players. However, achieving commercial viability requires sustained capital investment in enzyme platforms, purification infrastructure, and application development support. Fewer than five producers control the majority of commercial-scale crystalline allulose capacity globally, yet none holds a dominant market share sufficient to set prices unilaterally. This competitive structure benefits ingredient buyers through pricing competition but limits producers' ability to invest in demand-creation and co-development programs.

Strategic approaches in the market can be broadly categorized into two groups. The first group includes integrated ingredient companies such as Ingredion, Tate & Lyle, Cargill, and Roquette, which position allulose as part of a broader sugar-reduction solution portfolio. The second group comprises specialist rare-sugar producers like Matsutani Chemical, Samyang Corporation, Bonumose, and Savanna Ingredients, whose competitive advantage lies in proprietary enzyme technology and process efficiency. These two strategies highlight the diverse approaches adopted by market players to address varying consumer and industry needs.

White-space opportunities are evident in two specific areas. First, the combination of allulose with functional fibers and proteins in co-processed crystalline blends remains technically underdeveloped. This is despite clinical research suggesting metabolic synergy between allulose and prebiotic dietary fiber. Samyang Corporation is actively pursuing this blend architecture through its co-located allulose and prebiotics production facilities in Ulsan, South Korea. Such developments indicate potential for innovation and growth in the market, particularly in addressing unmet technical and consumer demands.

Allulose Crystal Industry Leaders

-

Ingredion Incorporated

-

Tate and Lyle PLC

-

Matsutani Chemical Industry Co. Ltd.

-

CJ CheilJedang Corporation

-

Bonumose, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Truvia has expanded its sweetener portfolio with the introduction of Allulose Plus Stevia Sweetener and Monk Fruit Sweetener, a tri-blend product designed to provide a sugar-like taste with zero calories per serving. This sweetener combines allulose, stevia, and monk fruit extract to minimize bitterness and aftertaste while maintaining functionality for baking, beverages, and everyday recipes. Formulated as a convenient 1:1 sugar replacement, the product utilizes allulose's properties to deliver sugar-like taste, browning, and caramelization.

- September 2024: Samyang Corporation has completed the construction of a new Specialty Plant in Ulsan, South Korea, establishing the largest allulose production facility in the country. With an investment of approximately KRW 140 billion (USD 104–105 million), the facility includes production lines for allulose and prebiotics, offering a total annual specialty ingredients capacity of 25,000 tons. The allulose plant alone has an annual production capacity of 13,000 tons, over four times Samyang's previous capacity, and can produce both liquid and crystalline allulose for domestic and export markets.

- July 2024: Roquette and Bonumose have entered into a global cooperation agreement to advance the development and commercialization of tagatose, a low-calorie sweetener of natural origin with a sugar-like taste and clinically supported health benefits. The partnership combines Bonumose's proprietary enzymatic technology for producing high-purity rare sugars with Roquette's expertise in large-scale starch and sweetener manufacturing. This collaboration aims to enhance scalability, production efficiency, and global availability of tagatose to address the increasing demand for sugar-reduction solutions.

Global Allulose Crystal Market Report Scope

| Pure Allulose Crystals |

| Blended Allulose Crystals |

| Corn-Based Allulose |

| Sugar Beet-Based Allulose |

| Sugarcane-Based Allulose |

| Other Plant-Based Sources |

| Food and Beverages | Bakery and Confectionery |

| Beverages | |

| Dairy and Frozen Desserts | |

| Others | |

| Nutraceuticals and Pharmaceuticals | |

| Other Applications |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Pure Allulose Crystals | |

| Blended Allulose Crystals | ||

| By Source | Corn-Based Allulose | |

| Sugar Beet-Based Allulose | ||

| Sugarcane-Based Allulose | ||

| Other Plant-Based Sources | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Beverages | ||

| Dairy and Frozen Desserts | ||

| Others | ||

| Nutraceuticals and Pharmaceuticals | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook of the allulose crystal market?

The allulose crystal market was valued at USD 0.23 billion in 2025 and reached USD 0.29 billion in 2026. The market is projected to grow to USD 0.43 billion by 2031, registering a CAGR of 8.20% during the 2026–2031 forecast period.

Which product type holds the largest share of the allulose crystal market?

Pure allulose crystals accounted for the largest share of the market in 2025, representing 80.12% of total revenue.

Which application segment dominates the allulose crystal market, and which is growing the fastest?

Food and beverages is the largest application segment, accounting for 78.34% of the global market in 2025.

Which region leads the allulose crystal market, and which region is expected to witness the highest growth?

North America held the largest share of the allulose crystal market in 2025, accounting for 36.02% of total revenue.

Page last updated on: