Market Overview

| Study Period | 2021 - 2031 |

|---|---|

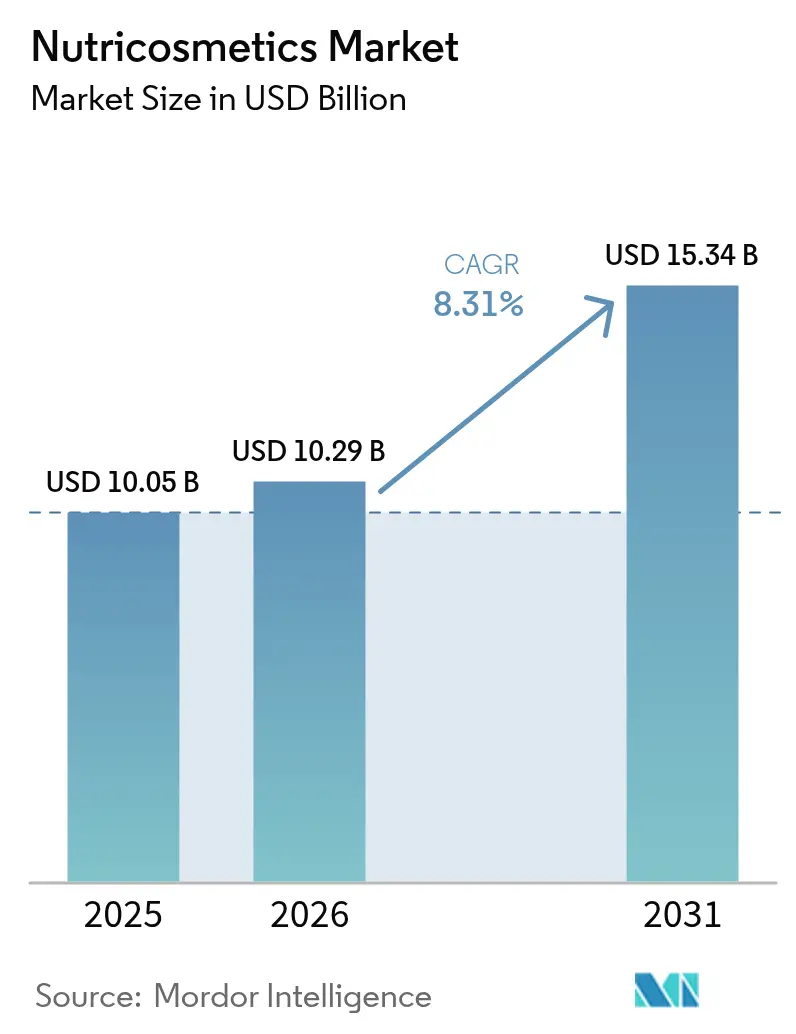

| Market Size (2026) | USD 10.29 Billion |

| Market Size (2031) | USD 15.34 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

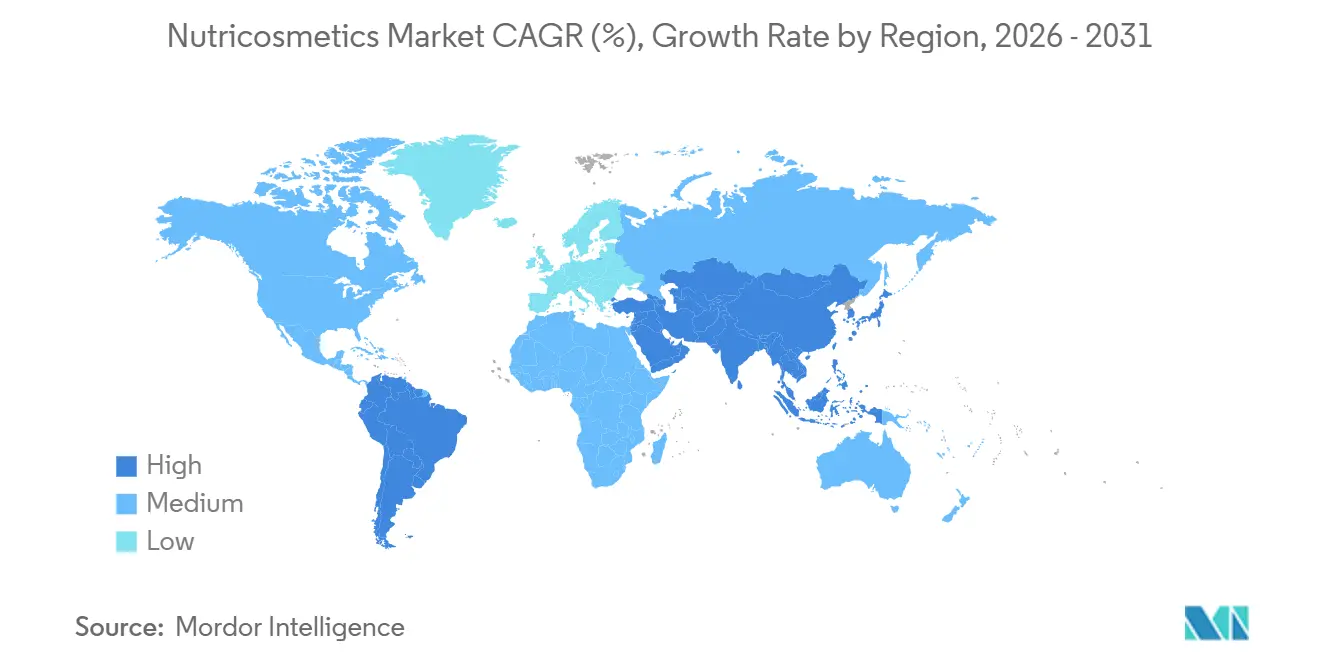

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nutricosmetics Market Analysis by Mordor Intelligence

The nutricosmetics market size was valued at USD 10.05 billion in 2025, reached USD 10.29 billion in 2026, and is projected to grow to USD 15.34 billion by 2031, registering a compound annual growth rate (CAGR) of 8.31% during the forecast period of 2026-2031. The increasing demand for beauty-from-within products, rising preventive health expenditures, and strong clinical validation have shifted ingestible beauty supplements from discretionary purchases to essential wellness products. Millennials and Gen-Z represent the majority of adopters, showing a 60% higher willingness to pay for science-backed products compared to older demographics, supporting premium pricing strategies. Social media advocacy complements clinical data, accelerating product lifecycles and driving demand spikes that are less common in traditional topical cosmetics. Asia-Pacific currently dominates the nutricosmetics market, accounting for nearly half of global revenue due to the region's long-standing acceptance of functional foods. However, North America is experiencing the fastest growth, driven by regulatory clarity and the rise of subscription-based e-commerce, which has increased average selling prices. On the supply side, research-intensive pharmaceutical companies and agile direct-to-consumer (D2C) brands are reshaping competition through advancements such as AI-assisted formulation, vegan collagen innovations, and microbiome-focused personalization tools.

Key Report Takeaways

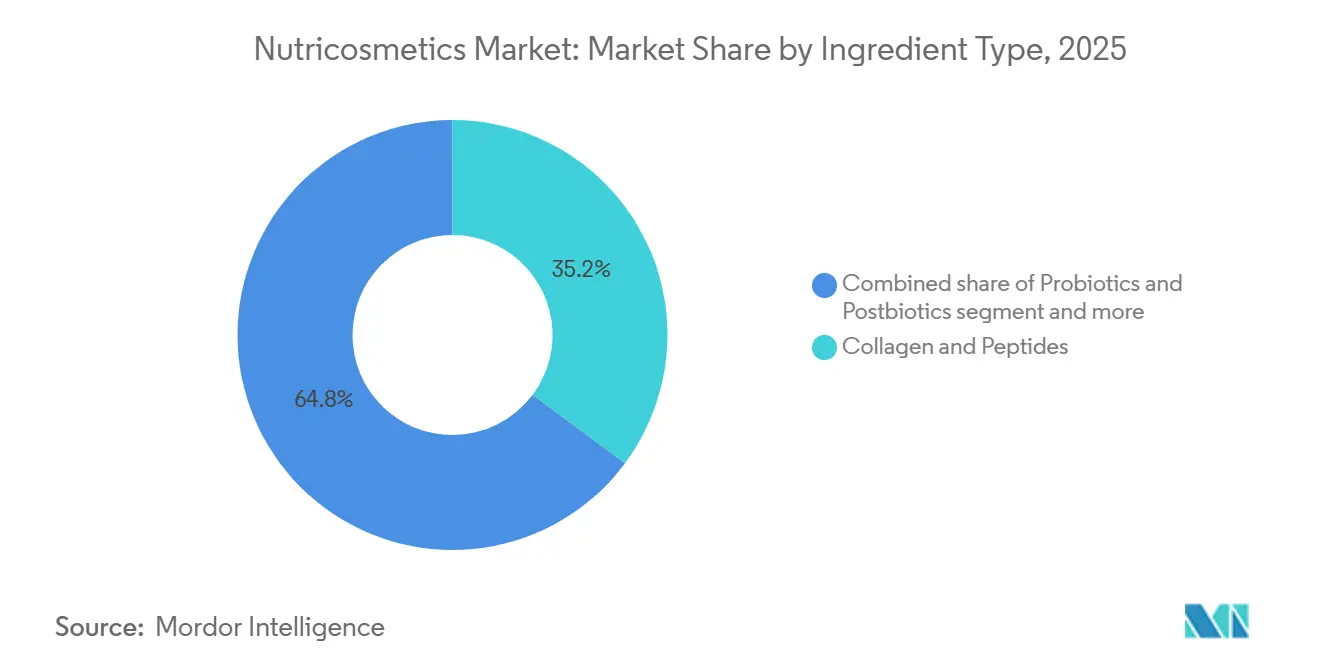

- By ingredient type, collagen and peptides commanded 35.17% of the nutricosmetics market size in 2025, whereas probiotics and postbiotics are forecast to advance at a 9.46% CAGR through 2031.

- By form, powders and liquids accounted for 42.99% of the nutricosmetics market size in 2025; gummies and soft-chews are set to climb at a 9.98% CAGR during the same period.

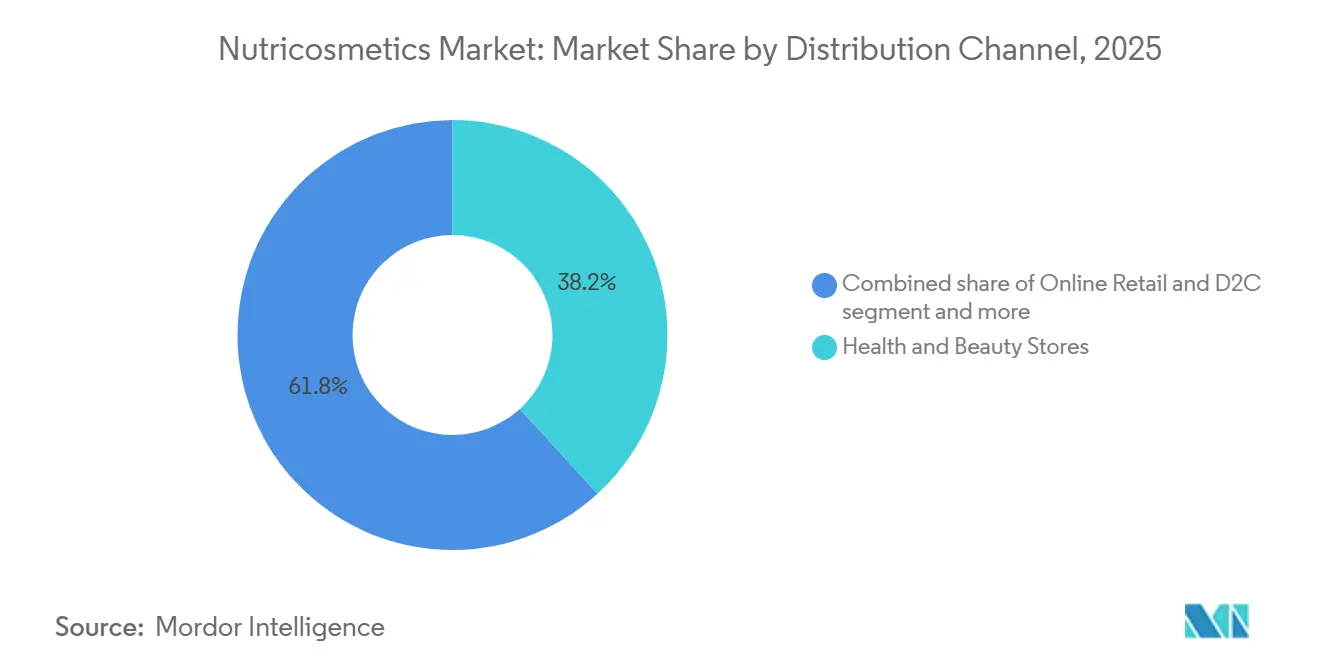

- By distribution channel, health and beauty stores held 38.23% revenue share in 2025, yet online retail and D2C are poised to expand at a 10.27% CAGR to 2031.

- By geography, North America led with 48.47% nutricosmetics market share in 2025, while Asia-Pacific is projected to post the highest regional CAGR at 9.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nutricosmetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of dietary supplements among millennials and Gen-Z | +1.8% | Global, with concentration in North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Growth of holistic wellness and beauty-from-within factors | +1.5% | Global, strongest in Japan, South Korea, and Western Europe | Long term (≥ 4 years) |

| Aging population boosting anti-aging spend | +1.3% | North America, Europe, and Japan | Long term (≥ 4 years) |

| Influence of social media platforms and beauty bloggers | +1.2% | Global, with peak impact in North America, Europe, and Southeast Asia | Short term (≤ 2 years) |

| Collagen-centric product innovation cycles (peptides, marine, vegan) | +1.0% | Global, with research and development hubs in Japan, Europe, and North America | Medium term (2-4 years) |

| E-commerce personalization engines boosting D2C supplement sales | +1.1% | Global, accelerated in China, India, and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising adoption of dietary supplements among millennials and Gen-Z

The growth of the nutricosmetics market is significantly driven by the rising adoption of dietary supplements among younger consumers, particularly Millennials and Gen-Z. These health-conscious groups prioritize wellness and are inclined toward preventive and beauty-from-within solutions, incorporating supplements into their daily routines to enhance skin, hair, and overall vitality. Their familiarity with digital shopping platforms, subscription models, and personalized nutrition enables greater engagement with nutricosmetics products, allowing brands to offer tailored solutions effectively. According to the CRN Consumer Survey on Dietary Supplements, dietary supplements have achieved mainstream acceptance in the U.S., with 74% of adults using them and 55% identified as “regular users” during 2023–2024 [1]Source: CRN, "Three-quarters of Americans Take Dietary Supplements; Most Users Agree They are Essential to Maintaining Health, CRN Consumer Survey Finds ", crnusa.org. Millennials and Gen-Z form a significant part of this trend, showing strong interest in innovative formulations, functional ingredients, and convenient formats such as gummies, powders, and ready-to-drink shots. Additionally, their preference for clean-label, natural, and ethically sourced products drives market growth, encouraging brands to develop offerings like collagen, probiotics, vitamins, and postbiotic solutions that align with their health, beauty, and lifestyle priorities.

Growth of holistic wellness and beauty-from within factors

The growing emphasis on holistic wellness is transforming consumer perceptions of beauty, shifting the focus from external aesthetics to internal health as the foundation of appearance. Consumers increasingly associate skin quality, hair strength, and aging outcomes with overall well-being, which includes factors such as nutrition, stress management, gut health, and lifestyle balance. This perspective is driving demand for beauty-from-within solutions, positioning nutricosmetics as an integral part of daily self-care and wellness routines rather than optional beauty products. This shift in behavior is evident in changing self-care habits. Currently, 64% of Americans engage in self-care to some extent, an increase from 57% five years ago, highlighting the growing normalization of wellness-focused consumption. Among these individuals, 28% report practicing self-care "very often," reflecting a deeper and more consistent commitment to health-oriented behaviors [2]Source: Civic Science, "More Americans Prioritizing Self-Care Amid Declining Well-Being", civicscience.com. As self-care becomes more deliberate and frequent, consumers are increasingly open to incorporating daily ingestible products, such as collagen, probiotics, antioxidants, and botanical supplements, which offer long-term beauty and health benefits.

Aging population boosting anti-aging spend

The growing global aging population is a significant driver for the nutricosmetics market, as older consumers increasingly seek anti-aging solutions that work internally. With rising life expectancy, aging is now approached proactively, with consumers adopting beauty and wellness supplements to maintain skin firmness, hair density, and overall vitality. Nutricosmetics, positioned at the intersection of nutrition and beauty, are being embraced as a preventive measure rather than a corrective treatment. Demographic trends highlight the scale of this opportunity. According to the World Health Organization, by 2030, one in six people worldwide will be aged 60 years or older, with this population segment increasing from 1 billion in 2020 to 1.4 billion. By 2050, the number of individuals aged 60 and above is expected to double to 2.1 billion. This demographic shift initially emerged in high-income countries, where aging populations are already significant. For example, as of 2025, 30% of Japan’s population (2025) is projected to be over 60 years old, creating established, high-spending consumer bases for anti-aging products [3]Source: World Health Organization, "Ageing and health", who.int. Older consumers are increasingly prioritizing healthy aging, appearance, and long-term wellness, driving demand for clinically supported nutricosmetics such as collagen, peptides, antioxidants, and cellular-support nutrients.

Influence of social media platforms and beauty bloggers

Social media platforms serve as discovery tools and trust facilitators, where user-generated content and influencer endorsements significantly influence purchase decisions compared to traditional advertising. By mid-2025, TikTok's #BeautySupplements hashtag garnered over 1.2 billion views, with viral trends such as "skin cycling" routines, combining topical actives with oral supplements, boosting cross-category sales. Brands leveraging nano-influencers, creators with fewer than 10,000 followers but highly engaged niche audiences, achieved cost-per-acquisition rates 40% lower than those of paid search campaigns. The Federal Trade Commission's updated endorsement guidelines in 2024, mandating clear disclosure of material connections between influencers and brands, initially raised compliance concerns but ultimately strengthened consumer trust in verified partnerships. The influence of this channel is expected to peak in the short term as platforms enhance algorithm transparency and consumers become more resistant to ad fatigue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and fragmented regulatory frameworks (FDA/EFSA/NMPA) | -0.9% | Global, with acute friction in cross-border e-commerce between United States, European Union (EU), and China | Long term (≥ 4 years) |

| Marine-collagen supply-chain vulnerability | -0.6% | Global, with concentration risk in North Atlantic and Pacific fishing zones | Medium term (2-4 years) |

| Lack of product awareness in developing regions | -0.5% | Sub-Saharan Africa, rural South Asia, and Latin America (excluding Brazil and Mexico) | Long term (≥ 4 years) |

| Consumer-pill-fatigue limiting dosage compliance | -0.4% | Global, with higher incidence in markets with polypharmacy prevalence (e.g., United States, Germany) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent and fragmented regulatory frameworks (FDA/EFSA/NMPA)

Differences in regulatory standards among the FDA, EFSA, and NMPA create compliance challenges, increasing time-to-market and legal expenses for brands aiming for multi-region launches. The FDA categorizes beauty supplements as dietary supplements under the Dietary Supplement Health and Education Act (DSHEA), allowing structure-function claims without pre-market approval but prohibiting disease-related claims. In contrast, EFSA mandates substantiation dossiers for any health claims and enforces a restrictive list of approved claims. Efforts to harmonize these regulations remain stalled due to conflicting national priorities between consumer protection and market access. As a result, brands must navigate a fragmented regulatory landscape, which tends to benefit larger companies with dedicated regulatory affairs teams.

Marine-collagen supply-chain vulnerability

Marine collagen sourcing primarily occurs in wild-caught fisheries located in Norway, Iceland, and Japan, making the supply chain vulnerable to climate-induced stock fluctuations and geopolitical fishing conflicts. Rising ocean temperatures have caused cod and haddock populations to migrate northward, leading to reduced yields in traditional fishing areas and a 22% increase in raw material prices between 2023 and 2025. Compliance with traceability requirements under the EU's Illegal, Unreported, and Unregulated (IUU) Fishing Regulation and the U.S. Seafood Import Monitoring Program has created documentation challenges for smaller suppliers, resulting in procurement consolidation among vertically integrated processors. While aquaculture-derived collagen presents a potential alternative, concerns over antibiotic residues and lower peptide bioavailability hinder its widespread adoption. Brands are also investigating enzymatic extraction methods using fish processing by-products, such as discarded skin and bones, to enhance yield efficiency. However, scaling these methods requires significant capital investment in enzymatic reactors and cold-chain logistics, which many mid-tier suppliers are unable to afford.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Collagen Leadership Meets Probiotic Momentum

In 2025, collagen and peptides represented 35.17% of the nutricosmetics market, supported by robust clinical evidence and widespread consumer awareness. Hydrolyzed marine collagen is notable for its high bioavailability, delivering effective results at lower doses. Additionally, precision-fermented vegan collagen, produced without animal-derived sources, appeals to ethically conscious consumers and reduces allergen risks, thereby expanding the potential customer base.

Probiotics and postbiotics are expected to grow at a 9.46% CAGR, driven by increasing research on the gut-skin connection. Supplements containing specific strains that reduce inflammation and enhance skin barrier function are gaining recommendations from dermatologists. Some brands are also combining collagen with probiotics to achieve synergistic effects. Furthermore, vitamins, carotenoids, omega-3 fatty acids, and botanical extracts continue to support incremental market growth. Reformulations emphasizing improved bioavailability and clean-label transparency are contributing to a more diverse and functional ingredient portfolio within the nutricosmetics market.

By Form: Powder Flexibility Versus Gummy Engagement

In 2025, powders and liquids accounted for 42.99% of the nutricosmetics market, driven by their flexible dosing options and rapid absorption. These formats are particularly favored for their versatility, allowing consumers to easily incorporate supplements into their daily routines, such as adding powders to smoothies or using liquid ampoules for quick, on-the-go consumption. Advances in solubility technology have enabled higher concentrations of active ingredients in smaller servings, making it more convenient for users to meet recommended intake levels while maintaining product efficacy.

Gummies and soft-chews are expected to experience the highest growth among form factors, with a projected CAGR of 9.98% through 2031. These formats have gained popularity due to significant improvements in flavor masking and sugar-free formulations, which have addressed earlier challenges related to potency and taste. This has made them particularly appealing to first-time supplement users and those seeking a more enjoyable, candy-like experience. While tablets and capsules remain widely used due to their cost-effectiveness and established presence in the market, they face limitations related to ease of swallowing, which can deter some consumers. Continued innovation in product formats, including the development of more palatable and convenient options, is expanding consumer choices and driving sustained growth in the nutricosmetics market.

By Distribution Channel: Expertise Anchors Stores, Personalization Powers Online

In 2025, health and beauty stores contributed 38.23% of the nutricosmetics market revenue, leveraging expert staff and in-store diagnostic tools to assist consumers in selecting appropriate supplements. These stores provide a personalized shopping experience, where trained professionals guide customers based on their specific needs and preferences. The strategic placement of these stores near topical beauty products promotes larger basket sizes and facilitates education-driven upselling. Many flagship stores utilize end-cap displays for products like collagen shots and probiotic sachets, effectively capturing impulse purchases and driving additional revenue. This approach not only enhances customer engagement but also strengthens brand loyalty by offering a comprehensive beauty and wellness solution.

Online retail and direct-to-consumer (D2C) platforms are projected to grow at a compound annual growth rate (CAGR) of 10.27%, driven by data-driven personalization engines. These platforms utilize advanced algorithms to analyze customer data and provide tailored product recommendations, creating a seamless and customized shopping experience. Wearable devices provide insights that enable automated subscription adjustments, improving customer retention by ensuring timely replenishment of products. Large marketplaces, such as Amazon, extend market reach, with Nestlé’s Vital Proteins achieving over USD 200 million in annual e-commerce sales. While traditional supermarkets continue to cater to entry-level products, they face difficulties in showcasing premium, science-backed offerings. This has led brands to adopt omnichannel strategies to balance accessibility with differentiation, combining the convenience of online shopping with the tactile experience of physical stores to meet diverse consumer preferences.

Geography Analysis

North America held a 48.47% share of the nutricosmetics market in 2025. This growth is supported by FDA oversight, which enhances consumer trust, increased venture-capital investments in personalized nutrition, and the ability of consumers to absorb premium pricing. Retailer GNC’s shift toward metabolic health aisles reflects the mainstream adoption of targeted nutricosmetics, indicating a broader consumer interest in functional beauty products. Additionally, a surge in patent filings related to microbiome modulators underscores the region's robust innovation pipeline, with companies focusing on advanced formulations to address specific health and beauty concerns. The growing popularity of e-commerce platforms and subscription-based models is also contributing to the accessibility and adoption of nutricosmetics in the region.

Asia-Pacific is expected to achieve the highest regional CAGR of 9.45% through 2031, driven by a long-standing familiarity with functional foods and supportive regulatory frameworks in countries like Japan and South Korea. In Japan, consumers prioritize healthy aging and frequently incorporate collagen powders into their daily routines, reflecting a deep-rooted culture of preventive health. South Korea's beauty-focused culture fosters rapid innovation with fermented botanicals, supported by a strong domestic market for beauty and wellness products. Meanwhile, China's growing acceptance of confectionery as a health-food carrier highlights potential for format diversification, with increasing investments in research and development to cater to evolving consumer preferences. The region's established infrastructure for functional foods and supplements further supports its fastest projection in the nutricosmetics market.

Europe is experiencing steady growth, driven by stringent EFSA standards that ensure product safety and promote environmental sustainability. Sustainability initiatives are encouraging brands to redesign packaging, as demonstrated by Vital Proteins’ 90% reduction in plastic usage through the adoption of paper canisters. Furthermore, the region's focus on clean-label products and natural ingredients aligns with consumer demand for transparency and eco-friendly solutions, further supporting market growth. The increasing prevalence of wellness trends and the rising awareness of the benefits of nutricosmetics among European consumers are expected to sustain the region's market momentum. Additionally, collaborations between manufacturers and retailers to promote innovative products are further driving growth in this region.

Regulatory Landscape

Nutricosmetics are primarily governed under food-supplement and dietary-supplement rules, with claim substantiation as the main compliance constraint. In the United States, products fall under the FDA dietary supplement framework (DSHEA/FDCA), where structure-function claims are permitted but disease claims are prohibited. In March 2026, FDA's Office of Dietary Supplement Programs held a public meeting (Docket FDA-2026-N-2047) to discuss the scope of dietary supplement ingredients, including modern classes such as proteins, enzymes, and microbials, which is relevant for microbiome and fermentation-led nutricosmetic actives.

In the European Union, EFSA-driven health-claim authorization under Regulation (EC) No 1924/2006 continues to shape go-to-market strategy and labeling. The European Court of Justice judgment in Case C-386/23 (Novel Nutriology) in 2025 reinforced that botanical health claims remain unauthorized unless on the EU permitted list. The European Commission issued Regulations (EU) 2025/2222 and 2025/2223 to formalize refusals of specific claims that did not meet substantiation requirements. Member-state implementation also evolves through national updates, such as Ireland's S.I. No. 226/2026 amending food supplements rules to align with EU annex changes, which adds another layer of complexity for cross-border launches and e-commerce listings.

Value Chain Analysis

The nutricosmetics value chain runs from bioactive sourcing (marine and bovine collagen, fermentation-derived proteins, carotenoids, botanicals, probiotics and postbiotics) to ingredient processing and standardization, formulation and delivery-format engineering (powders, liquids, gummies/soft-chews), and contract manufacturing under supplement-grade quality systems. Brand-led commercialization then targets health and beauty stores as well as online and D2C subscription models. Quality management and documentation (identity testing, contaminants, stability, and claim support) cut across the chain and shape supplier selection, particularly for premium science-led products.

A structural shift is increasing reliance on partnerships and exclusivity to secure differentiated actives and reduce supply risk. L'Oréal Groupe's 2024 agreement with Debut to develop bio-identical ingredients that replace conventionally sourced materials is one example. Crystal Tomato's November 2024 exclusive with Lucas Meyer Cosmetics (Clariant) for enhanced colorless carotenoids, backed by clinical testing at the Skin Research Institute of Singapore, is another. These moves point to a value-chain tilt toward biotech-enabled inputs, localized clinical validation, and ingredient-branding as competitive levers alongside traditional supplement manufacturing and retail distribution.

Competitive Landscape

The nutricosmetics market demonstrates a moderate level of consolidation. Established multinational conglomerates with diversified wellness and beauty portfolios compete alongside agile direct-to-consumer (D2C) disruptors and strong regional players, creating a dynamic competitive landscape. Larger companies leverage their brand recognition and extensive distribution networks, while smaller innovators focus on niche segments with specialized formulations and personalized offerings, aligning with evolving consumer preferences for efficacy and convenience.

Opportunities for growth exist in areas such as vegan collagen alternatives, which utilize genetically engineered yeast strains or plant-based precursor blends to cater to ethical and allergen-conscious consumers. However, commercialization in this segment faces challenges due to the need for novel food approvals, which can delay product launches. Another emerging area is postbiotic formulations, which involve heat-killed probiotic strains and their metabolites. These formulations offer greater stability compared to live cultures, but evolving regulatory guidelines on labeling and health claims create uncertainty for new market entrants.

Regulatory compliance plays a critical role in differentiating market players. Frameworks such as ISO 22000 for food safety management and NSF/ANSI 173 for dietary supplement quality act as competitive barriers. These certifications increase entry challenges for undercapitalized companies while signaling quality assurance and reliability to institutional buyers, distributors, and international partners. Companies that prioritize rigorous quality standards and transparent manufacturing practices are better positioned to build trust, expand distribution networks, and achieve sustainable growth in the competitive nutricosmetics market.

Nutricosmetics Industry Leaders

-

Nestlé Health Science

-

Shiseido Company Ltd.

-

Amway Corporation

-

Herbalife Nutrition Ltd.

-

Suntory Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Mechanism-led platforms and novel actives are creating whitespace beyond traditional collagen-centric positioning, especially in segments linking cellular aging and skin outcomes. In January 2026, Tru Niagen extended into beauty-from-within with Tru Niagen Beauty, a NAD-precursor supplement positioned for skin, hair, and nail health. This aligns with a broader shift toward cellular-health narratives and premium science-backed claims within the supplement framework.

Format innovation and ingredient supply integration are also reshaping competition. At Vitafoods Europe 2026, Tosla and Geltor introduced a vegan signaling-collagen liquid shot using Geltor's PrimaColl, while Pharmactive presented Kyoh for hair-follicle support. These product moves reinforce pipelines tied to specific benefit areas such as hair growth support and skin barrier effects, with liquid delivery as a recurring format choice. On the supply side, Solabia Group completed its acquisition of Mibelle Biochemistry in July 2026, adding scale and biotech-oriented active-ingredient capabilities that can support faster formulation cycles and broader ingredient portfolios for nutricosmetics brands operating across regions with different claim and ingredient rules.

Recent Industry Developments

- May 2026: Nature's Bounty launched Age-Defying Skin Renewal, a dietary supplement formulated with ceramides positioned to reinforce the skin barrier. The release puts more emphasis on skin-lipid and barrier-repair ingredients in ingestible beauty, widening the active-ingredient set beyond collagen-centric offerings.

- March 2026: Vital Proteins (Nestle Health Science) launched Collagen Sparkling Water, a functional beverage featuring VERISOL collagen peptides and vitamin C for skin, hair, and nail support. The launch advances nutricosmetics into ready-to-drink formats and pushes beauty-from-within into occasions traditionally owned by beverages.

- November 2025: Elasten, a German collagen supplement brand, launched in the United States with a drinking-ampoule format built around a proprietary collagen complex plus vitamins and minerals. Entering the US market with a science-positioned liquid delivery format increases competitive pressure in premium ingestible skincare, particularly in channels that favor trial and repeat purchases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the nutricosmetics market covers ingestible products marketed for beauty-from-within benefits, where nutrients are taken orally to support skin, hair, and nail appearance and condition.

Scope exclusions: We do not count topical cosmetics, salon services, or clinical aesthetic procedures, even if they are positioned alongside oral beauty routines.

Segmentation Overview

-

By Ingredient Type

- Collagen and Peptides

- Vitamins and Minerals

- Carotenoids and Antioxidants

- Omega-3 and EFAs

- Probiotics and Postbiotics

- Botanical Extracts

-

By Form

- Tablets and Capsules

- Powders and Liquids

- Gummies and Soft-Chews

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Health and Beauty Stores

- Online Retail and D2C

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America, Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the backbone of the model by clarifying what is sold, where it is sold, and how consumption trends are shifting across major regions. We referenced public sources such as FDA dietary supplement resources, European Commission food supplement and claims guidance, national health surveys and statistical offices, and trade data portals that indicate cross-border movement of key beauty ingredients.

To tighten assumptions, we also reviewed company annual reports, investor presentations, reputable press, and association websites tracking dietary supplement and beauty wellness trends. For market mapping and cross checks, we used paid subscriptions for company financials and intelligence, plus a patent database to understand active ingredient pipelines and claim directions. These desk sources are not exhaustive, and additional public and paid references were used to compile data, validate it, and address open questions during analysis.

Primary Interviews and Surveys

Primary interviews and surveys were used to confirm real world pricing, channel mix, and what buyers actually consider a nutricosmetic versus a regular supplement. We spoke with stakeholders across brands, ingredient suppliers, distributors, and retail channel participants across APAC, EMEA, and the Americas so the same assumptions were not reused across very different consumer and regulatory settings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 42% |

| Mid tier: 45% | Functional/Unit leaders: 36% | EMEA: 34% |

| Smaller Players: 22% | Managers: 50% | Americas: 24% |

Market-Sizing & Forecasting

Sizing started with a top-down build where demand pools were reconstructed using dietary supplement consumption signals, beauty and wellness spending context, and the penetration of oral beauty products by region, before totals were split into skin, hair, and nail use cases. Once that shape was stable, we corroborated it with selective bottom-up approximations such as sampled price points by form factor (tablets and capsules, powders and liquids, gummies and soft chews), channel checks across online versus store-based retail, and supplier side sense-checks on ingredient intensity.

A few inputs that materially steer the model include form-factor shifts toward gummies and soft chews, average selling price progression by pack size, online share change by region, claim-led demand (collagen, peptides, vitamins and minerals, and similar), and regulatory and labeling constraints that affect how products are marketed. Where bottom-up coverage was thin for smaller markets, gaps were handled through proxy ratios from comparable countries and then adjusted using interview feedback.

For forecasting, scenario analysis was applied around price inflation versus premiumization, changes in e-commerce adoption, and the pace of new product launches, which were then translated into annual growth paths. The final forecast was kept practical by using variables that can be refreshed each year from public indicators and repeatable field checks.

Data Validation & Update Cycle

Outputs were validated through triangulation between independent signals, including demand-side indicators, channel observations, and supply-side commentary, and then checked for year-to-year jumps that did not align with known market events. When a variance was found, assumptions were revisited, and follow-up calls were triggered to confirm whether the issue came from scope, pricing, or geography mix.

Before sign-off, the model goes through multi-step analyst reviews where calculation logic, unit consistency, and currency timing are rechecked. Reports are refreshed annually, with interim updates when major regulatory changes, pricing shocks, or category disruptions occur, and a final pre-delivery pass is completed so clients receive the most current view.

Mordor Intelligence's Nutricosmetics Market Sizing Compared With Other Published Estimates

Published market sizes for nutricosmetics often differ because firms do not always count the same product set, and they may also anchor to different years, currencies, and price assumptions. Variations also show up when one estimate leans more on broad nutrition categories, while another ties the demand pool to clearly marketed beauty claims and validated channel mixes.

In this study, the key gap drivers were mainly around what is treated as a nutricosmetic, how functional foods and beverages are handled versus supplement-only views, and how fast average prices are assumed to move as gummies and premium collagen formats grow. Differences in refresh cadence matter too, since a year change in pricing and online mix can shift value totals even if volumes look steady.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.05 B (2025) | |

| Industry Publisher A | USD 7.78 B (2025) | This estimate is lower mainly because the included scope leans toward a narrower oral supplement view and applies a different regional weighting, which reduces the value contribution from high-priced formats. |

| Industry Publisher B | USD 7.50 B (2025) | This number can move depending on whether functional foods and functional beverages are fully counted, and on how pack-price progression is treated as premium collagen and gummies expand. |

The table shows that most of the spread comes from scope choices and price mechanics rather than from a disagreement that the category is growing. By keeping functional forms and channels explicit, and by tying prices to observed form-factor mixes, the estimate stays traceable to repeatable checks, which is why the higher 2025 value is reached by Mordor Intelligence.

Key Questions Answered in the Report

How large will global sales of beauty supplements reach by 2031?

Revenue is projected to hit USD 15.34 billion by 2031, supported by an 8.31% CAGR from 2026 to 2031.

Which ingredient category is growing the fastest?

Probiotics and Postbiotics are expanding at a 9.46% CAGR thanks to growing evidence linking gut health and skin clarity.

Why are gummies and soft chews gaining popularity over tablets?

Gummies and soft-chews improve taste and reduce pill fatigue, lifting adherence especially among younger users, and are forecast to post a 9.98% CAGR.

Which region offers the highest growth headroom?

Asia-Pacific shows the fastest regional CAGR at 9.45% as aging consumers and Gen-Z simultaneously fuel demand.

Page last updated on: